e-workshop - 6/9/2015 aging and financial inclusion (micropensions)

TRANSCRIPT

Aging and Financial Inclusion Helping Clients to Prepare for Old Age

Parul Khanna Associate Director-Projects

Live-tweet the session! @MicroCredSummit, @CFI_ACCION

use #Commit100M

Sonja Kelly Fellow

Use the Q&A box on the top-right to send questions

to the Panelists.

Eppu Mikkonen-Jeanneret Head of Policy

The Center for Financial Inclusion (CFI) commits to bringing greater attention to the issue of aging and financial services, by: • Conducting supply-side research in the fall of 2014 on the obstacles

to older adults accessing and using the financial services that could help to improve their lives.

CFI will also partner with HelpAge International to conduct demand-side research in the fall of 2014 to better understand the income streams and expenses of older adults in Colombia.

• Publishing a white paper on these two research efforts and conduct

two roundtable discussions -- one focused on the Latin America region and one focused globally -- that will galvanize support around this issue.

CFI Campaign Commitment in 2014

See more at www.microcreditsummit.org/make-a-commitment.html

Str

ate

gie

s to

Co

ve

r O

ld-A

ge

Ex

pe

nse

s, C

olo

mb

ia (

20

13

)

4

The Micro-Pension® Ecosystem and Model Micro Pension Foundation | http://www.micropensionfoundation.org

Micro-Pension® is a Registered Trade-mark and Brand-name of Invest India Micro Pension Services Private Limited

The microPension-VISA LAB is an India-based non-profit entity focussed on retirement literacy and on developing innovative technology-led solutions to improve access to contributory social security programs by low income unbanked informal sector workers in developing countries

5

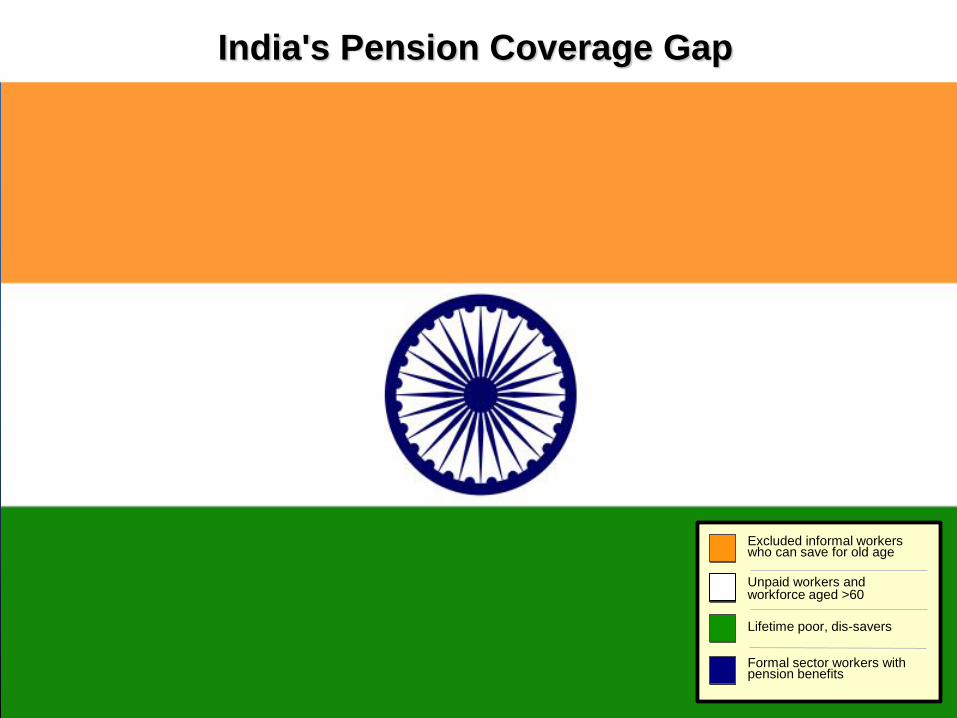

Lifetime poor, dis-savers

Unpaid workers and workforce aged >60

Excluded informal workers who can save for old age

Formal sector workers with pension benefits

India's Pension Coverage Gap

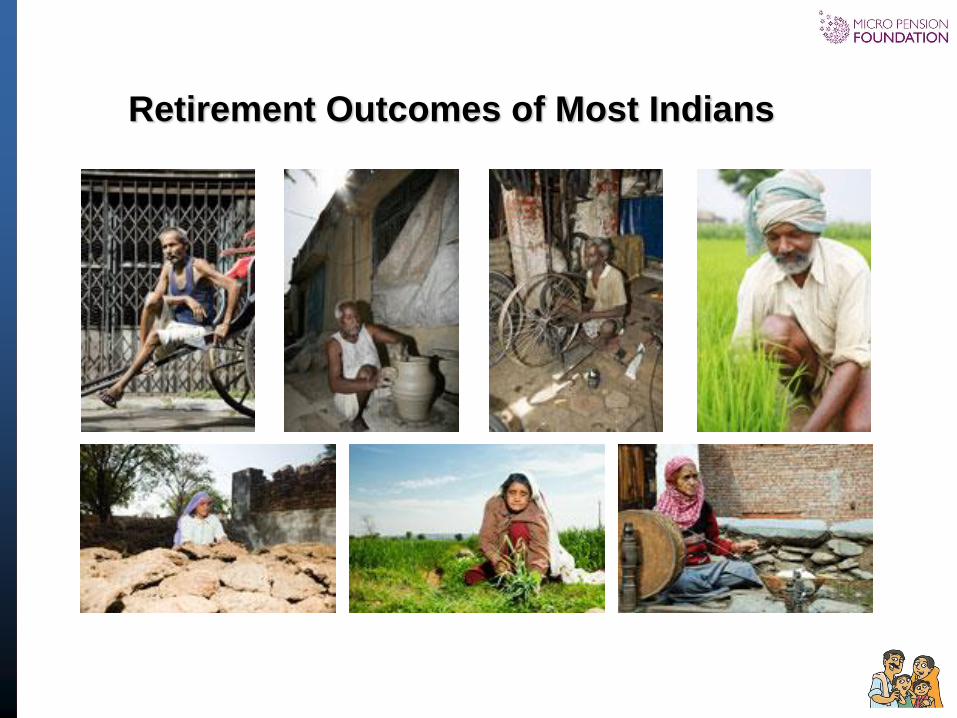

1. Children

2. God

3. Government

4. Kismet

Retirement Portfolio of Most Indians

Retirement Outcomes of Most Indians

● The Lab is a specialised R&D facility housed within the non-profit

Micro Pension Foundation.

● The Lab develops innovative technology-led solutions to improve

access to contributory social security programs by low income

unbanked informal sector workers in developing countries.

● It also provides technical assistance and expert advisory services

to governments, regulators and multilateral aid agencies in design

and turn-key implementation of inclusive pension and social

security programs.

MicroPension-VISA Inclusion Lab

9

Micro-Pension® Operating Model

10

1. A young person is educated and encouraged by a credible outreach partner (MFI, cooperative, NGO, SHG federation) to voluntari ly open an individual “micro-pension” account.

2. She starts saving a small part of her income into an integrated social security solution. Her contributions are managed by well regulated financial institutions in her own name and grow over time.

3. Even if she changes her location or job, she is able to continue transmitting her micro-savings directly and accurately into her social security product basket using a prepaid card or a bank account.

4. When she is old, her accumulations are paid back directly into her repaid card or bank account as a monthly pension for the rest of her life.

5. Along the way, she has easy and simple access to objective information and an effective complaints redressal mechanism.

Simple, Secure, Convenient, Affordable

11

Micro Pension® Impact Footprint

14.5%

16%

18.8%

>100,000 customers

Between 25,000 and 100,000 customers

<25,000 customers

Aggregate base of ~1.1 mn clients as on March 2014

12

Education & Enrolment

Clients are educated and enrolled by

trained/ certified field staff for an

integrated product solution.

Each client gets a unique and portable

"micro-pension" account number using

a central IT platform that stores static,

transactional and savings value data

over time.

Clients also receive government co-

contributions directly into their NPS-

Lite and AABY accounts.

Ongoing Contributions

Clients periodically deposit micro-

savings into their own bank a/c or

prepaid card.

Prepaid savings are kept in escrow

pending transfer to relevant financial

institution for investment.

Micro-savings are debited using a

standing instruction mandate (SI) on

each client's prepaid card or through

an SI or ECS on their bank a/c.

Reconciled micro-savings are

transferred by regulated payment

partners directly to product providers.

Services and Benefits

Social security contributions and

government co-contributions grow

over time.

Redemptions, insurance claims and

pension benefits are transferred

directly into each client's bank a/c or

prepaid card.

Clients receive periodic account

statements showing contributions

and accumulations over time.

For information, redemptions, claims

or compliants, clients simply call the

national Micro Pension® HelpLine.

Micro-Pension® Operating Model

13

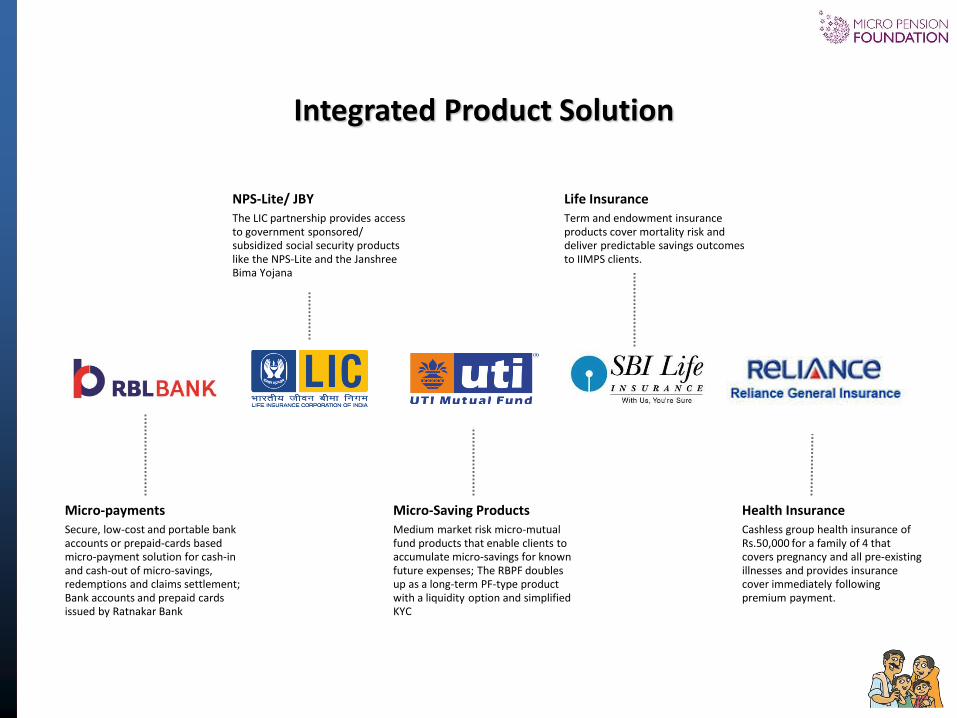

Micro-payments Secure, low-cost and portable bank accounts or prepaid-cards based micro-payment solution for cash-in and cash-out of micro-savings, redemptions and claims settlement; Bank accounts and prepaid cards issued by Ratnakar Bank

Life Insurance Term and endowment insurance products cover mortality risk and deliver predictable savings outcomes to IIMPS clients.

Micro-Saving Products Medium market risk micro-mutual fund products that enable clients to accumulate micro-savings for known future expenses; The RBPF doubles up as a long-term PF-type product with a liquidity option and simplified KYC

NPS-Lite/ JBY The LIC partnership provides access to government sponsored/ subsidized social security products like the NPS-Lite and the Janshree Bima Yojana

Health Insurance Cashless group health insurance of Rs.50,000 for a family of 4 that covers pregnancy and all pre-existing illnesses and provides insurance cover immediately following premium payment.

Integrated Product Solution

14

1. Education and Enrolment

15

1 MICRO-PENSION® FIELD PROCESS

16

2 MICRO-PENSION® FIELD PROCESS

17

3 MICRO-PENSION® FIELD PROCESS

18

4 MICRO-PENSION® FIELD PROCESS

19

5 MICRO-PENSION® FIELD PROCESS

20

6 MICRO-PENSION® FIELD PROCESS

21

7 MICRO-PENSION® FIELD PROCESS

22

8 MICRO-PENSION® FIELD PROCESS

23

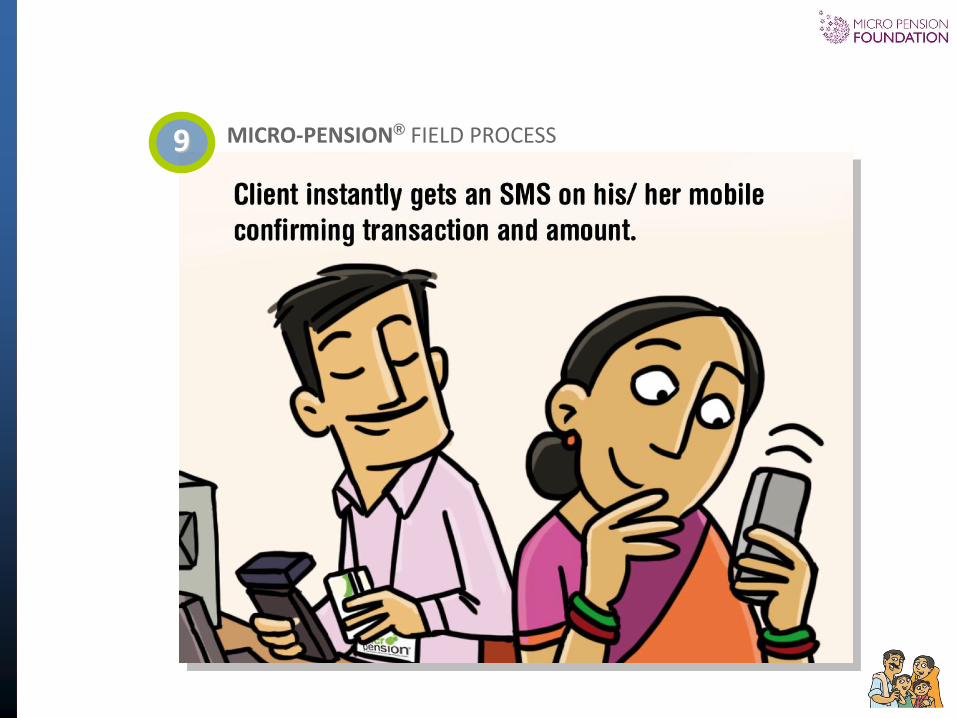

9 MICRO-PENSION® FIELD PROCESS

24

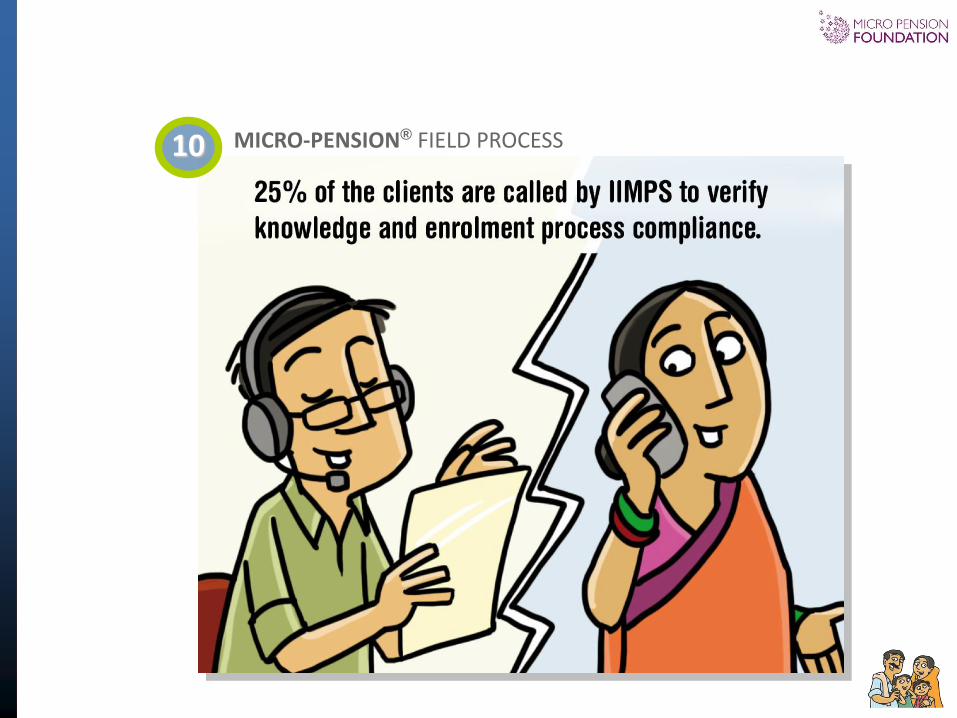

10 MICRO-PENSION® FIELD PROCESS

25

2. Secure Micro-Payments

26

Life insurance

Cash-in, real-time accounting and reconciliation in a simple,

single payment transaction at a BC outlet

Prepaid value periodically debited and transferred to each product provider's accounts as per client SI mandate

The microPension-VISA Prepaid Solution

Prepaid account balance is kept safely in escrow in the

client's name with a scheduled commercial bank

Health, accident insurance

Children's education/ marriage

Retirement savings

Low income, unbanked, excluded informal sector person with intermittent income and unpredictable cash-flow in a remote location

Integrated basket of well regulated Social Security and

Micro-saving Products

27

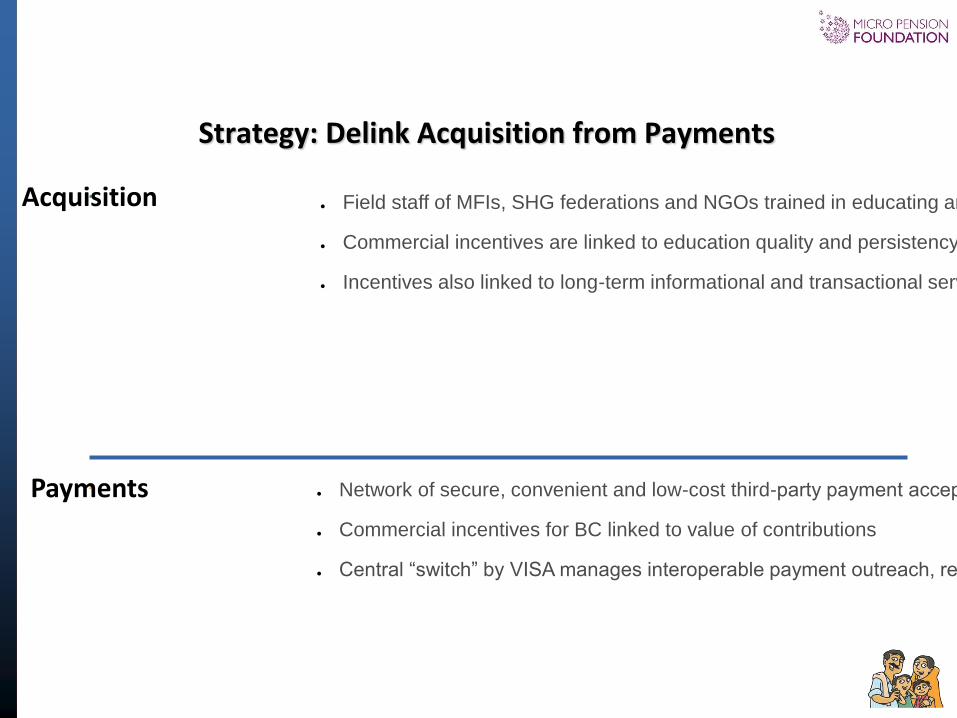

Acquisition

Payments

● Field staff of MFIs, SHG federations and NGOs trained in educating and enrolling beneficiaries use standard IEC tools and an electronic application documentation process.

● Commercial incentives are linked to education quality and persistency using periodic reminders

● Incentives also linked to long-term informational and transactional services (statements, claims processing)

● Network of secure, convenient and low-cost third-party payment acceptance points (BCs) that “load” cash onto prepaid cards

● Commercial incentives for BC linked to value of contributions

● Central “switch” by VISA manages interoperable payment outreach, real-time cash reconciliation and daily MIS

Strategy: Delink Acquisition from Payments

28

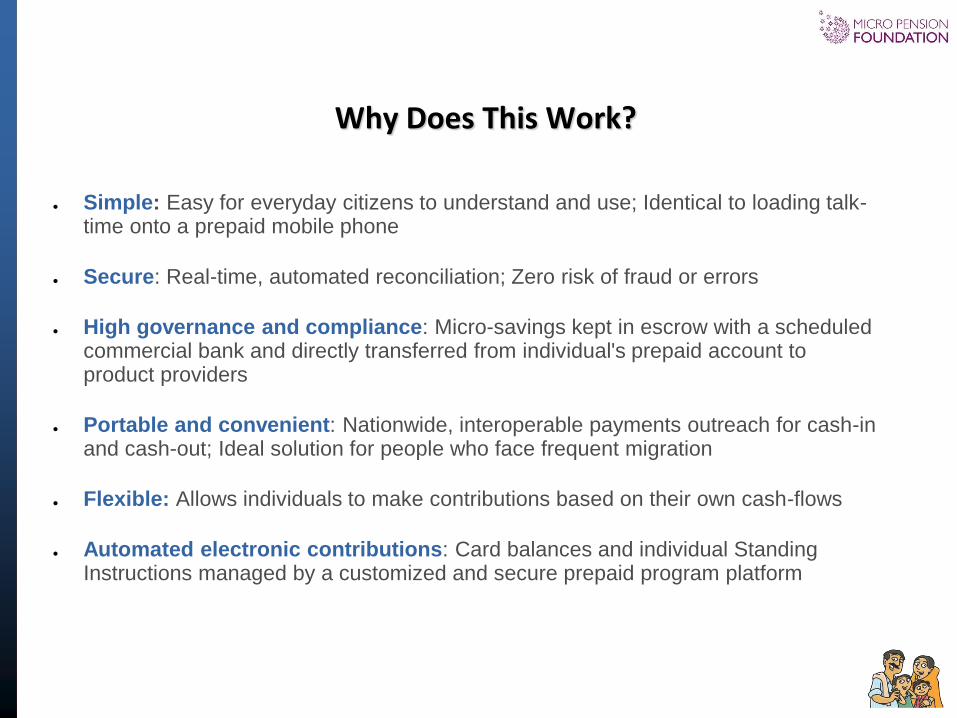

● Simple: Easy for everyday citizens to understand and use; Identical to loading talk-time onto a prepaid mobile phone

● Secure: Real-time, automated reconciliation; Zero risk of fraud or errors

● High governance and compliance: Micro-savings kept in escrow with a scheduled commercial bank and directly transferred from individual's prepaid account to product providers

● Portable and convenient: Nationwide, interoperable payments outreach for cash-in and cash-out; Ideal solution for people who face frequent migration

● Flexible: Allows individuals to make contributions based on their own cash-flows

● Automated electronic contributions: Card balances and individual Standing Instructions managed by a customized and secure prepaid program platform

Why Does This Work?

29

● Affordable: Transaction fees linked to transaction size; Does not penalize the poor

● Near zero capital cost for microPOS device and prepaid cards

● Immediately implementable: Does not await bank penetration to remote locations; Harnesses VISA's existing secure back-office capacity and global experience with electronic payments; Harnesses existing telecom outreach.

Why Does This Work? /2

30

3. Ongoing Servicing

31

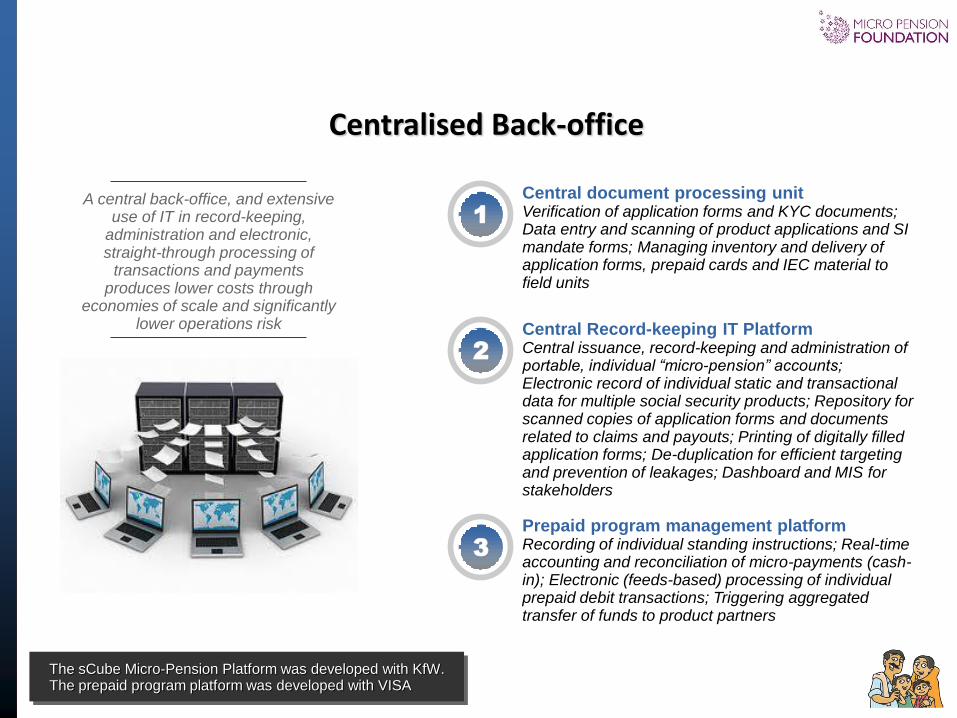

Centralised Back-office

Central document processing unit Verification of application forms and KYC documents; Data entry and scanning of product applications and SI mandate forms; Managing inventory and delivery of application forms, prepaid cards and IEC material to field units

Central Record-keeping IT Platform Central issuance, record-keeping and administration of portable, individual “micro-pension” accounts; Electronic record of individual static and transactional data for multiple social security products; Repository for scanned copies of application forms and documents related to claims and payouts; Printing of digitally filled application forms; De-duplication for efficient targeting and prevention of leakages; Dashboard and MIS for stakeholders

Prepaid program management platform Recording of individual standing instructions; Real-time accounting and reconciliation of micro-payments (cash-in); Electronic (feeds-based) processing of individual prepaid debit transactions; Triggering aggregated transfer of funds to product partners

1

2

3

A central back-office, and extensive use of IT in record-keeping,

administration and electronic, straight-through processing of

transactions and payments produces lower costs through

economies of scale and significantly lower operations risk

The sCube Micro-Pension Platform was developed with KfW. The prepaid program platform was developed with VISA

32

Excluded low income individual

1. Standard, Aadhaar-enabled “e-KYC” for citizens who would

otherwise struggle with identity documents

2. Multiple financial product access with a single authentication

3. Low cost: Physical KYC, data-entry and verification not

required

4. Shorter enrollment process

1. Multiple KYC documents not required for different product

providers for static data changes – client uses biometric

authentication service to update UID database with multiple

product providers

2. Secure authentication-based cash-out of insurance claims,

withdrawals from mutual fund or receipt of pension benefits,

etc. using a microATM

Convenient, low cost enrolment

Secure cash-out

“Aadhaar” is the brand name of the unique identity number issued to every Indian by the Unique Identification Authority of India (UIDAI). As on date, over 600 million Aadhaar numbers have already been issued by the UIDAI. Most of the Micro-Pension target population may already have an Aadhaar.

IIMPS is registered with UIDAI as a KYC User Agency (KUA) and Aadhaar Authentication Agency (AUA)

Integration with Aadhaar

33

National Multilingual HelpLine

Field compliance audit Call-backs to new clients to verify knowledge of concepts, product features, benefits, rights and process and also verify enrollment process compliance

Reminders Calls to new clients and to irregular savers to encourage continued savings discipline

HelpDesk Centralised port for collating, reporting and resolving complaints and queries and effectively addressing requests for claims settlement, changes in static data, withdrawals, statements, etc.

Surveys Periodic calls for behavioral finance studies among persistent, irregular and dormant clients to produce business-level MIS for IIMPS and partner stakeholders

Field-staff support Support to field-staff and certified counselors to more effectively address client queries; Also used in training needs assessment surveys

Client protection Verifying receipt of payouts including pension payments, insurance claims settlement and withdrawals of liquid savings

1 6

2

3

5

4

The national MicroPension HelpLine was launched in 2011 with support from NABARD. Over the last 24 months, the HelpLine has made ~300,000 outbound calls to both existing and new clients to confirm client knowledge and verify education process compliance

34

This is beginning to work...

35

THANK YOU http://www.micropensionfoundation.org http://www.giftapension.com

For more information, please write to [email protected]

Aging and Financial Inclusion Helping Clients to Prepare for Old Age

Don’t forget to tweet your takeaways of this E-workshop @MicroCredSummit using #Commit100M

To follow up with the panelists: Parul Khanna: [email protected]

Sonja Kelly: [email protected] Eppu Mikkonen-Jeanneret: [email protected]

Join CFI in announcing YOUR CAMPAIGN COMMITMENT: mcs2015.org/commitonline

Feel free to write to us at [email protected]