e04 depreciation

DESCRIPTION

ekonomi teknikTRANSCRIPT

Department of Chemical Engineering and Applied

ChemistryUniversity of Toronto

Course: CHE349 File: CHE349/Depreciation13

Copyright: Joseph C. Paradi1996-2004

Centre for Management of Technology and Entrepreneurship

Depreciation

2Course: CHE349

Centre for Management of Technology and Entrepreneurship

Introduction

An asset starts to lose value as soon as it is purchased. Perhaps the only exception to this is art, collectibles, etc.

The best example is a car. It loses about 20-30% of its value when the customer takes delivery.

The word "Depreciation" actually has many meanings: physical amortisation market value value to owner appraisal impaired usefulness taxation

While these seem very different, they are usually related to each other in the end.

3Course: CHE349

Centre for Management of Technology and Entrepreneurship

Reasons for Depreciation

We will concentrate on the loss in value which occurs for several reasons: Use related physical loss - As something is used, it wears out and must

be replaced or repaired, but its value declines along with the "wear and tear" it suffers.

Often, this aspect is measured with respect to units of production which in the car's case is measured in kilometres driven, hours of use on an aeroplane engine or light bulb or pump.

Time related physical loss - Even if not used, things will deteriorate with time as nature or other effects take their toll. Rusting in storage, chemical deterioration, paint drying in can, etc

Not surprisingly, his is usually measured in units of time, such as a 10 year old car, a 40 year old sewage treatment plant, etc.

Functionality related loss - Loss can occur without any physical changes.

Value can be lost over time as fashion changes, furniture, clothes, new laws - pollution.

4Course: CHE349

Centre for Management of Technology and Entrepreneurship

Depreciation - Definition

Depreciation involves a procedure where the cost of an asset less its estimated salvage value is distributed over the asset’s estimated useful life in a systematic, rational manner.

5Course: CHE349

Centre for Management of Technology and Entrepreneurship

Further thoughts

Depreciation is an accounting “fiction” from an Engineering Economy point of view: GAAP (Generally Accepted Accounting Principles) requires to

match expenses to incomes. this requires that we take an asset that has a life longer than

the fiscal year and “depreciate” it over its “useful life” the methods used to depreciate the asset’s value is usually up

to the company, but only for its own books\ the tax treatment is mandated by law - and is usually different

From the Engineering Economy point of view the purchase is treated as a cash flow at time 0 and then as a cost of capital over its life - as we saw before

Depreciation does NOT involve any cash flows, so it is of no interest to us in calculations we make.

6Course: CHE349

Centre for Management of Technology and Entrepreneurship

Value and other Definitions

Models of depreciation can be used to estimate the loss of value of an asset over time )it can also determine the value of the asset at any point in time).

Basis - usually based on First Costs, plus installation expenses. This may be altered if additions or capital improvements are made later

Recovery Period (ND) - life to compute depreciation Salvage Value (S) - value on disposition Book Value (BVt) - it is = First Cost - Depreciation Depreciation (Dt) - the deduction, or cost, assigned to

an accounting period Pools - treatment of the same type of equipment as a

pooled resource.

7Course: CHE349

Centre for Management of Technology and Entrepreneurship

More on Values

Market Value - The value of an asset when sold in an arms-length free market environment. But, this can only be accurate if we actually sell it. Therefore,

this is usually an estimate, even based on a formal appraisal by experts. The other way is to use a depreciation model that fits the situation.

Book Value - The value calculated for accounting purposes according to an agreed upon model. This can be imposed by legislation or rules, or by industry

practice or by a good estimate of the life and value of the asset

Scrap Value - Value of the material recovered. Salvage Value - Can be the actual value at the life

end, estimated value, or specific trade-in value.

8Course: CHE349

Centre for Management of Technology and Entrepreneurship

Why is book value of assets needed? To make managerial decisions, it is necessary to know

the value of assets owned by the company

For planning purposes, an estimate of the value of the owned assets is important

Government tax legislation requires calculation of profits (income and expenses). There are particular rules for calculating depreciation.

9Course: CHE349

Centre for Management of Technology and Entrepreneurship

Methods: Straight Line

This assumes that the rate of loss is constant over the asset's life - expressed in a stated amount or a certain percentage of the FC value.

Algebraically, the assumption is that the rate of loss in asset value is constant and based on the purchase value.

Estimate depreciation and book value are as follows:

where: Dsl(n) = the depreciation amount for period n using straight line depreciation method

P = purchase price or current market value S = salvage value after N periods N = useful life of the asset. BVsl = the book value at the end of period n using straight line

( )sl

P SD n

N

( )sl

P SBV n P n

N

10Course: CHE349

Centre for Management of Technology and Entrepreneurship

Straight Line Example 1

Small computers purchased by a company cost $7000 each. Past records indicate that they should have a useful life of 5 years, after which they will be disposed of, with no salvage value. Determine: The depreciation charge during year 1 The depreciation charge during year 2 The book value of the computers at the end of year 3

Dsl(1) = 7000 / 5 = $1400

Dsl(2) = 7000 / 5 = $1400

BV(3) = 7000 – 3 [7000 / 5] = $2800

11Course: CHE349

Centre for Management of Technology and Entrepreneurship

Straight Line Example 2

The Gigabit software company has purchased a RAID unit (fault tolerant disk array) for $250,000. It is expected to last for 6 years, with a salvage value of $10,000. Use the straight line depreciation method to calculate: i. The depreciation amount for year 1 ii. Depreciation amount for year 6. iii. The book value at the end of year 4. iv. The accumulated depreciation at the end of year 4.

Amount to amortise $250,000 – 10,000 = 240,000 Depreciation Year 1 40,000 Depreciation for year 6 40,000 Book value at year 4 90,000 Accumulated depreciation at year 4 160,000

12Course: CHE349

Centre for Management of Technology and Entrepreneurship

Method: Declining Balance

The loss of value of the asset is modelled as a constant proportion of the asset's current value.

This method uses a percentage applied to the remaining balance of the item in each accounting period.

Of course, the asset never completely depreciates.

( ) ( 1)

( ) (1 )

( ) (1 )

1

db db

ndb

ndb

n

D n BV n d

BV n P d

BV n S P d

Sd

P

Depreciation for period n

Book Value at the end of Period n

Calculating the rate of depreciation when there is a given Salvage value

13Course: CHE349

Centre for Management of Technology and Entrepreneurship

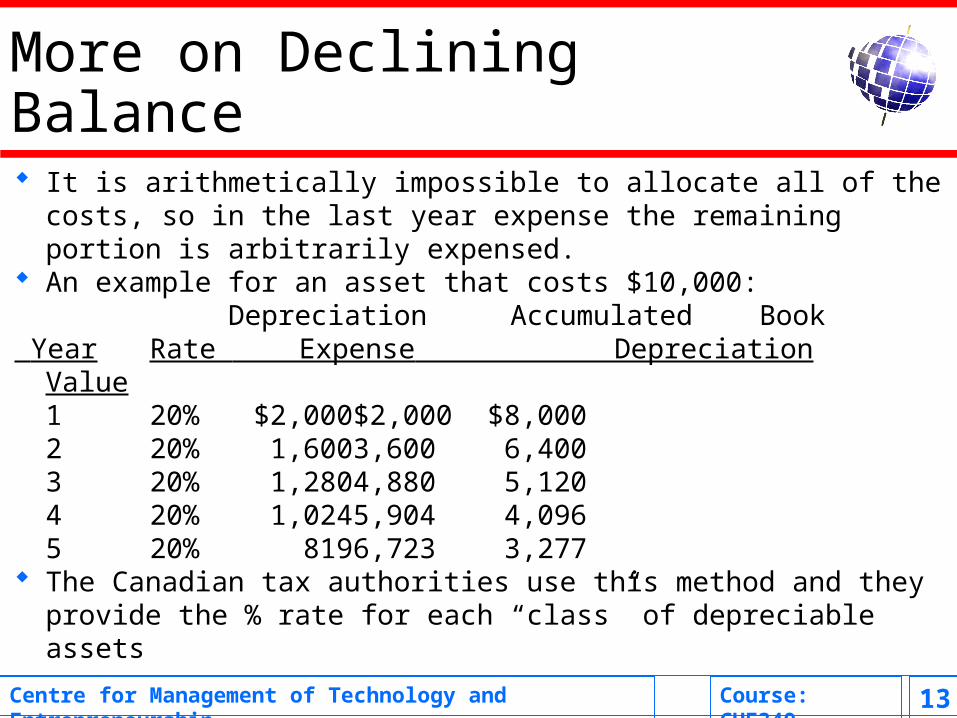

More on Declining Balance

It is arithmetically impossible to allocate all of the costs, so in the last year expense the remaining portion is arbitrarily expensed.

An example for an asset that costs $10,000: Depreciation Accumulated Book

Year Rate Expense Depreciation Value1 20% $2,000 $2,000 $8,0002 20% 1,600 3,600 6,4003 20% 1,280 4,880 5,1204 20% 1,024 5,904 4,0965 20% 819 6,723 3,277

The Canadian tax authorities use this method and they provide the % rate for each “class” of depreciable assets

14Course: CHE349

Centre for Management of Technology and Entrepreneurship

Declining Balance Example

Small computers purchased by a company cost $7000 each. Past records indicate that they should have a useful life of 5 years, after which they will be disposed of, with no salvage value. Use a depreciation rate of 40% for the declining-balance method and determine: The depreciation charge during year 1 The depreciation charge during year 2 The book value of the computers at the end of year 3

Ddb1 = BV(0) * (0.4) = 7000 (0.4) = $2800

Ddb2 = BV(1) * (1-0.4)*0.4 = (7000–2800) (0.4) = $1680

BVdb3 = 7000 (1-0.4)3 = $1512

15Course: CHE349

Centre for Management of Technology and Entrepreneurship

Declining Balance and Salvage Value Here, we are given a specific Salvage value that will be

met at the end of the useful life of the asset $10,000. Depreciation Accumulated Book

Year Rate Expense Depreciation Value1 36.9% $3,690 $3,690 $6,3102 36.9% 2,328 6,019 3,9813 36.9% 1,469 7,488 2,5124 36.9% 927 8,415 1,5855 36.9% 585 9,000 1,000

Recall that the equation here is:d = 1 - (S/P)1/N

16Course: CHE349

Centre for Management of Technology and Entrepreneurship

Declining Balance with Salvage - Simple Example A machine was purchased to automate the blow-

moulding segment of the plastic manufacturing process for $120,000. The company decided to use the declining balance depreciation method over a 5 year period to a salvage value of $40,000. What percentage was used in this case?

i = 1 - (S/P)1/N

i = 1 - (40/120)1/5

i = 19.7258% = 19.73%

17Course: CHE349

Centre for Management of Technology and Entrepreneurship

Declining Balance with S Example The Gigabit software company has purchased a RAID unit (fault

tolerant disk array) for $250,000. It is expected to last for 6 years, with a salvage value of $10,000. Use the declining balance depreciation method to calculate: i. The depreciation amount for year 1 ii. Depreciation amount for year 6. iii. The book value at the end of year 4. iv. The accumulated depreciation at the end of year 4.

Amount to amortise $250,000 – 10,000 = 240,000 Declining balance R = 1 - (S/FC)1/N

Thus R=1-((10,000/250,000)1/6) = 0.4152 = 41.52% Depreciation Year 1 250,000*0.4152 = 103,800 Depreciation for year 6 250K*(1-0.4152)5 * 0.4152 = 7,100 Book value at year 4 250K*(1-0.4152)4 = 29,240 Accum dep. at year 4250K – 29,240 = 220,760

18Course: CHE349

Centre for Management of Technology and Entrepreneurship

0

100

200

300

400

500

600

700

800

900

1000

0 1 2 3 4 5 6 7 8 9 10

Book Value against Time

Years

Dolla

rs

Straight Line to zero S

5%

10%

25%

50%

Straight Line to 30% Salvage Value

19Course: CHE349

Centre for Management of Technology and Entrepreneurship

Double Declining Balance

Double Declining Balance (DDB) is a version of the DB method and sometimes referred to as the 200% method

It is twice the straight line rate and can be used when the N is known:

dmax = 2/N So if N=10, the DDB rate is = 2/10 = 0.2 or 20% of the

book value is written off (removed each year) Another common DB method used is the 150% of

Straight Line method where dmax = 1.5/N Once you calculate the rate, it is just a Declining

Balance method

20Course: CHE349

Centre for Management of Technology and Entrepreneurship

Method: Sum-of-the-Digits

This is another form of accelerated depreciation. The formula is composed of a denominator which is the sum of the years digits (1+2+3+4+5=15). The numerator is the year of life of the machine in inverse order. Using the same example of a $10,000 asset:Year Rate Depreciation Accumulated Book

Expense Depreciation Value1 5/15 $3,335 $3,335 $6,6652 4/15 2,668 6,003 3,9973 3/15 2,001 8,004 1,9964 2/15 1,334 9,338 6625 1/15 662 10,000 - 0 -

21Course: CHE349

Centre for Management of Technology and Entrepreneurship

Method: Unit-of-Production

In this seldom used case, we use the machine’s production life as the basis:

(FC - S)/U = Per Unit Depreciation Rate Using the $10,000 asset example and the fact that the

machine is estimated to produce 50,000 units in its life:Year Unit Dep Depr'n Accumulated Book

Units made Expense Depreciation Value1 15,000 $0.20 $3,000 $3,000 $7,0002 12,500 .20 2,500 5,500 4,5003 10,000 .20 2,000 7,500 2,5004 7,500 .20 1,500 9,000 1,0005 5,000 .20 1,000 10,000 - 0 -

22Course: CHE349

Centre for Management of Technology and Entrepreneurship

A Combined Example

A fine chemicals manufacturing company purchased a water jet mixer machine 4 years ago for $380,000. It will have a salvage value of $30,000 two years from now. Calculate its book value today if we used:

Straight line depreciationFacts: P = $380,000 S = $30,000 N = 6 n = 4Book Value = 380,000 – 4*((380,000-30,000)/6) = 146,667

Declining balance depreciation at ?%First, calculate the rate of depreciation needed to get to S=$30,000i = (30,000/380,000)1/6 = 34.5%Book Value = 380,000 – Yr1 – Yr2 – Yr3 – Yr4

= 380,000 – 131,110 – 85,874 – 56,245 – 36,834= $69,937