earnings release 3rd quarter 2009 - relações com ... 28.8% compared with the 2q09. net revenues...

TRANSCRIPT

1

Earnings Release 3rd Quarter 2009

São Paulo, november 13th, 2009. Alpargatas (BOVESPA - Nível 1: ALPA3 and ALPA4), today released

its 3rd

quarter 2009 (3Q9) results and the accrued in the first nine months of the year. This report

contains Alpargatas’ performance and that of its controlled companies in 3Q9, or simply “quarter”.

The variations mentioned herein refer to the second quarter 2009 (2Q9) and third quarter 2008

(2Q8). To maintain the comparability, the 3Q8 financial statements include 100% of Alpargatas

Argentina’s results.

1. Introduction

Alpargatas’ third quarter performance is the result of the company’s ongoing efforts to achieve

excellence in managing the business. We improved on our second quarter sales volumes and

revenues through continuous innovation in our products, in association with strong brands. We have

maintained austerity in managing costs and expenditures, with measures that have driven

profitability. We have accelerated the cash conversion cycle by controlling our current accounts,

resulting in increased cash generation. We have reduced indebtedness, improving our overall

financial position. Together, these measures improved Alpargatas’ consolidated performance. From

the second to the third quarter of 2009, net revenues grew 16.4%; gross margin increased by 7.7

percent, reaching 45.7%, and EBITDA increased 153.0%, with a margin of 19.2%. We ended the first

nine months of the year as a more solidly based company, better positioned to take advantage of the

markets in which we operate as a result of the expansion of the global economy and the sporting

events scheduled for the next decade.

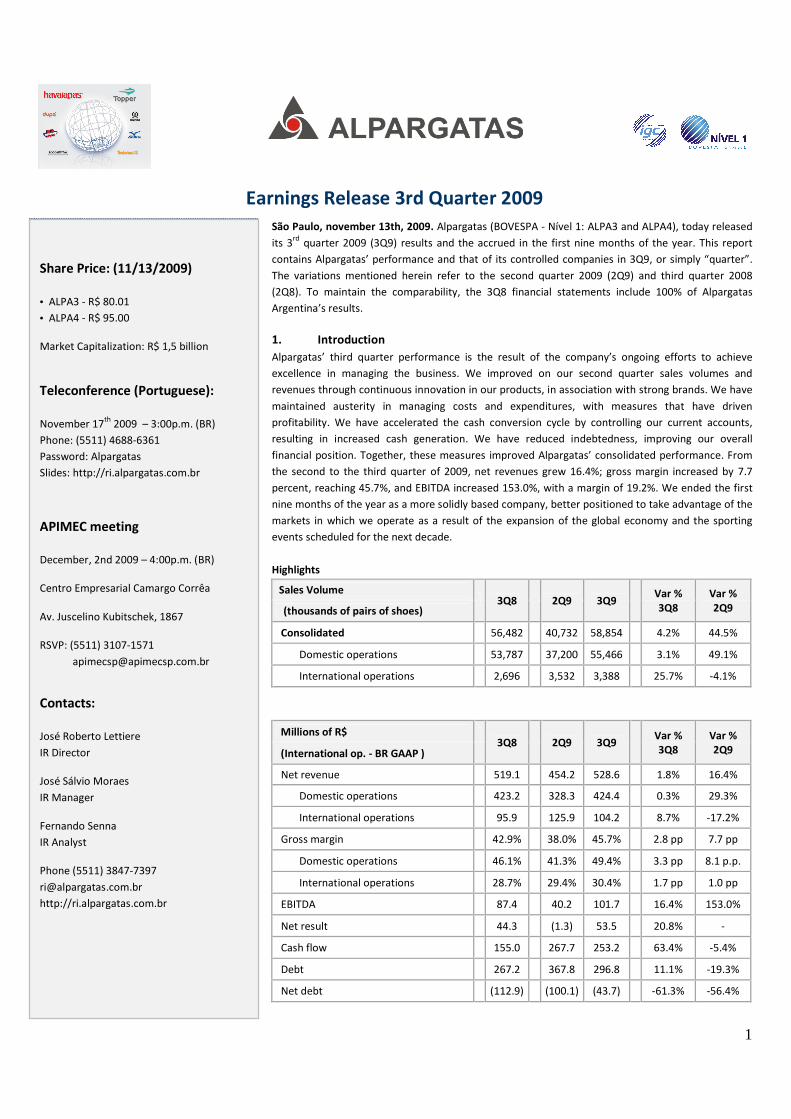

Highlights

Sales Volume 3Q8

2Q9 3Q9

Var %

3Q8

Var %

2Q9 (thousands of pairs of shoes)

Consolidated 56,482 40,732 58,854 4.2% 44.5%

Domestic operations 53,787 37,200 55,466 3.1% 49.1%

International operations 2,696 3,532 3,388 25.7% -4.1%

Millions of R$ 3Q8

2Q9 3Q9

Var %

3Q8

Var %

2Q9 (International op. - BR GAAP )

Net revenue 519.1 454.2 528.6 1.8% 16.4%

Domestic operations 423.2 328.3 424.4 0.3% 29.3%

International operations 95.9 125.9 104.2 8.7% -17.2%

Gross margin 42.9% 38.0% 45.7% 2.8 pp 7.7 pp

Domestic operations 46.1% 41.3% 49.4% 3.3 pp 8.1 p.p.

International operations 28.7% 29.4% 30.4% 1.7 pp 1.0 pp

EBITDA 87.4 40.2 101.7 16.4% 153.0%

Net result 44.3 (1.3) 53.5 20.8% -

Cash flow 155.0 267.7 253.2 63.4% -5.4%

Debt 267.2 367.8 296.8 11.1% -19.3%

Net debt (112.9) (100.1) (43.7) -61.3% -56.4%

Share Price: (11/13/2009)

• ALPA3 - R$ 80.01

• ALPA4 - R$ 95.00

Market Capitalization: R$ 1,5 billion

Teleconference (Portuguese):

November 17th

2009 – 3:00p.m. (BR)

Phone: (5511) 4688-6361

Password: Alpargatas

Slides: http://ri.alpargatas.com.br

APIMEC meeting

December, 2nd 2009 – 4:00p.m. (BR)

Centro Empresarial Camargo Corrêa

Av. Juscelino Kubitschek, 1867

RSVP: (5511) 3107-1571

Contacts:

José Roberto Lettiere

IR Director

José Sálvio Moraes

IR Manager

Fernando Senna

IR Analyst

Phone (5511) 3847-7397

http://ri.alpargatas.com.br

Earnings Release

1. DOMESTIC OPERATIONS Volume de vendas

Domestic operations

Sales volume

Sandals (millions of pairs)

Sports footwear (000’s of pairs)

Industrial textiles (000’s of m

Sandals

Sandals sales volume increased 53.1% compared with the second quarter 2009 (and 4.2% against 3Q08), driven by the success of

collection. The models reached the stores in July and high consumer acceptance led to a

Sports footwear

The 1.5% increase compared with the second quarter volume reflects the recovery in sales in the sports footwear segment. Ther

volume compared with the 3Q08 due to focus on marketing the premium

revenues in the sporting goods business.

Industrial textiles

The transportation and agribusiness sectors showed signs of recovery during the quarter. This, together with the strong perfo

architecture segment, was reflected in the industrial textiles business, which had its best results so far this year. The num

grew 28.8% compared with the 2Q09.

Net revenues

Domestic operations

Net revenues – R$ million

Net revenues from domestic operations totaled R$ 424.4 million, 29.3% up on 2Q09. This performance caps a critical first seme

consumption, reinforcing projections of continued revenue growth in the fourth quarter and

footwear and industrial textiles, allied with price increases, were the main drivers of revenue growth in the quarter

performance and continued expansion, with the opening of new

24%

Earnings Release 3rd Quarter 2009

3Q08 2Q09 3Q09

50,4 34,3 52,5

Sports footwear (000’s of pairs) 3.343 2.881 2.923

m2) 4.459 3.088 3.976

Sandals sales volume increased 53.1% compared with the second quarter 2009 (and 4.2% against 3Q08), driven by the success of

collection. The models reached the stores in July and high consumer acceptance led to a growth in market share.

The 1.5% increase compared with the second quarter volume reflects the recovery in sales in the sports footwear segment. Ther

volume compared with the 3Q08 due to focus on marketing the premium footwear brands Topper and Mizuno, whose higher added value boosted

The transportation and agribusiness sectors showed signs of recovery during the quarter. This, together with the strong perfo

architecture segment, was reflected in the industrial textiles business, which had its best results so far this year. The num

3Q08 2Q09 3Q09

423,2 328,3 424,4

Net revenues from domestic operations totaled R$ 424.4 million, 29.3% up on 2Q09. This performance caps a critical first seme

consumption, reinforcing projections of continued revenue growth in the fourth quarter and in 2010. The higher sales volumes in sandals, sports

footwear and industrial textiles, allied with price increases, were the main drivers of revenue growth in the quarter

performance and continued expansion, with the opening of new Havaianas franchises.

62%

24%

9%5%

DOMESTIC OPERATIONS

Net revenue per business

Sandals

Sporting goods

Retail

Industrial textiles

2

Variations

3Q08 2Q09

4,2% 53,1%

-12,6% 1,5%

-10,8% 28,8%

Sandals sales volume increased 53.1% compared with the second quarter 2009 (and 4.2% against 3Q08), driven by the success of the new Havaianas

growth in market share.

The 1.5% increase compared with the second quarter volume reflects the recovery in sales in the sports footwear segment. There was a reduction in

footwear brands Topper and Mizuno, whose higher added value boosted

The transportation and agribusiness sectors showed signs of recovery during the quarter. This, together with the strong performance in the

architecture segment, was reflected in the industrial textiles business, which had its best results so far this year. The number of m2 commercialized

Variations

3Q08 2Q09

0,3% 29,3%

Net revenues from domestic operations totaled R$ 424.4 million, 29.3% up on 2Q09. This performance caps a critical first semester for footwear

in 2010. The higher sales volumes in sandals, sports

footwear and industrial textiles, allied with price increases, were the main drivers of revenue growth in the quarter. This was reinforced by retail

Earnings Release

Profit and gross margin

Domestic operations

Gross profit – R$ million

Gross margin

Domestic operations showed a significant increase in gross profit during the quarter. In comparison with 2Q09, gross profit i

gross margin by 8.1 percentage points. This growth was due to the dilution of fixed co

manufacture of sandals and sports footwear, with a ten percentage point increase in manufacturing efficiency (standard hours

production). In the comparison with 3Q08, the variations in profit and gross margin were also positive (7.4% and 3.3% respectively), mainly as a result

of the 20% average reduction in the cost of the company’s principal raw materials, most notably rubber.

EBITDA

Domestic operations

EBITDA – R$ million

EBITDA Margin

Os fatores mais relevantes que explicam a variação do EBITDA das operações

� Ganho de R$ 76,2 milhões em razão dos aumentos do volume de vendas, do preço médio e da margem bruta

� Economia de R$ 11,5 milhões decorrente de

� Recuperação não recorrente de impostos (PIS/Cofins) de R$ 13,3 milhões, contabilizado no 2T9.

The most relevant factors explaining the EBITDA variation in domestic operations compared with 2Q09 are:

� A R$ 76.2 million gain due to increases in sales volume, average prices and gross margin.

� Savings of R$ 11.5 million from restructuring and reduction in operating expenses.

� A non-recurring R$ 13.3 million tax recovery (PIS/Cofins) in 2Q09.

The main events for the business in Brazil were:

Sandals

Launch of the 2009/2010 Havaianas collection, most notably:

Ebitda 2Q09 Volume / Price /Gross Margin

Earnings Release 3rd Quarter 2009

3Q08 2Q09 3Q09

195,3 135,7 209,7

46,1% 41,3% 49,4%

Domestic operations showed a significant increase in gross profit during the quarter. In comparison with 2Q09, gross profit i

gross margin by 8.1 percentage points. This growth was due to the dilution of fixed costs resulting from higher sales and greater productivity in the

manufacture of sandals and sports footwear, with a ten percentage point increase in manufacturing efficiency (standard hours

iations in profit and gross margin were also positive (7.4% and 3.3% respectively), mainly as a result

of the 20% average reduction in the cost of the company’s principal raw materials, most notably rubber.

3Q08 2Q09 3Q09

90,2 36,4 103,9

21,3% 11,1% 24,5%

Os fatores mais relevantes que explicam a variação do EBITDA das operações nacionais, em relação ao 2T9, são:

dos aumentos do volume de vendas, do preço médio e da margem bruta

Economia de R$ 11,5 milhões decorrente de ganhos com reestruturação e com a produtividade do SG&

Recuperação não recorrente de impostos (PIS/Cofins) de R$ 13,3 milhões, contabilizado no 2T9.

The most relevant factors explaining the EBITDA variation in domestic operations compared with 2Q09 are:

to increases in sales volume, average prices and gross margin.

Savings of R$ 11.5 million from restructuring and reduction in operating expenses.

recurring R$ 13.3 million tax recovery (PIS/Cofins) in 2Q09.

Launch of the 2009/2010 Havaianas collection, most notably:

/

Restructuring and Productivity

Gains

Non-recurring tax recovery

Others

3

Variations

3Q08 2Q09

7,4% 54,5%

3,3 pp 8,1 pp

Domestic operations showed a significant increase in gross profit during the quarter. In comparison with 2Q09, gross profit increased by 54.5% and

sts resulting from higher sales and greater productivity in the

manufacture of sandals and sports footwear, with a ten percentage point increase in manufacturing efficiency (standard hours x hours spent in

iations in profit and gross margin were also positive (7.4% and 3.3% respectively), mainly as a result

Variations

3Q08 2Q09

15,2% 185,4%

3,2 pp 13,4 pp

nacionais, em relação ao 2T9, são:

dos aumentos do volume de vendas, do preço médio e da margem bruta.

com a produtividade do SG&A (despesas operacionais).

Ebitda 3Q09

Earnings Release

� Havaianas Top Wash – produced with Havaianas Brasil residues, the sandal is a concrete demonstration of Alpargatas’ concern with the

sustainability of its business.

� Havaianas IPÊ – the innovations in the line generated a tenfold increase in sales compared with the last collection, bolstering the IPÊ

Institute, dedicated to the preservation of Brazil’s flora and fauna.

� Launch of the Dupé 2009/2010 collection with 30 models; reformula

the major TV channels in the Northeast of the country.

� Participation of Havaianas and Dupé in Francal, an important footwear fair held in São Paulo.

Sporting goods

Topper

� Outstanding sales of the “The One Professional” football boot. The model is used by a number of professionals playing in the Brazilian sp

soccer series.

� Launch of clothing line with new materials and designs for shirts, shorts and pants.

� New running and tennis footwear aligned with the strategy to position the Topper brand in a number of different sports categories and in

leading sporting goods distribution channels.

Mizuno

Realization of the second stage of the Mizuno 10 miles competition in São Paulo. The race

Rio de Janeiro, Belo Horizonte and Brasília.

� Participation in the fourth edition of the São Paulo Running Show, the most important street racing and triathlon event in th

Retail

� A 158% increase in the number of sales outlets in comparison with 3Q08.

� Launch of the Timberland Spring/Summer collection, the highlights being the Canvas and Leather lines, aimed at increasing sha

brand among the youth public.

2. INTERNATIONAL OPERATIONS

The international operations are made up of the Alpargatas USA, Alpargatas Europe and Alpargatas Argentina businesses. On Sep

the breakdown of net revenues from the international operations was

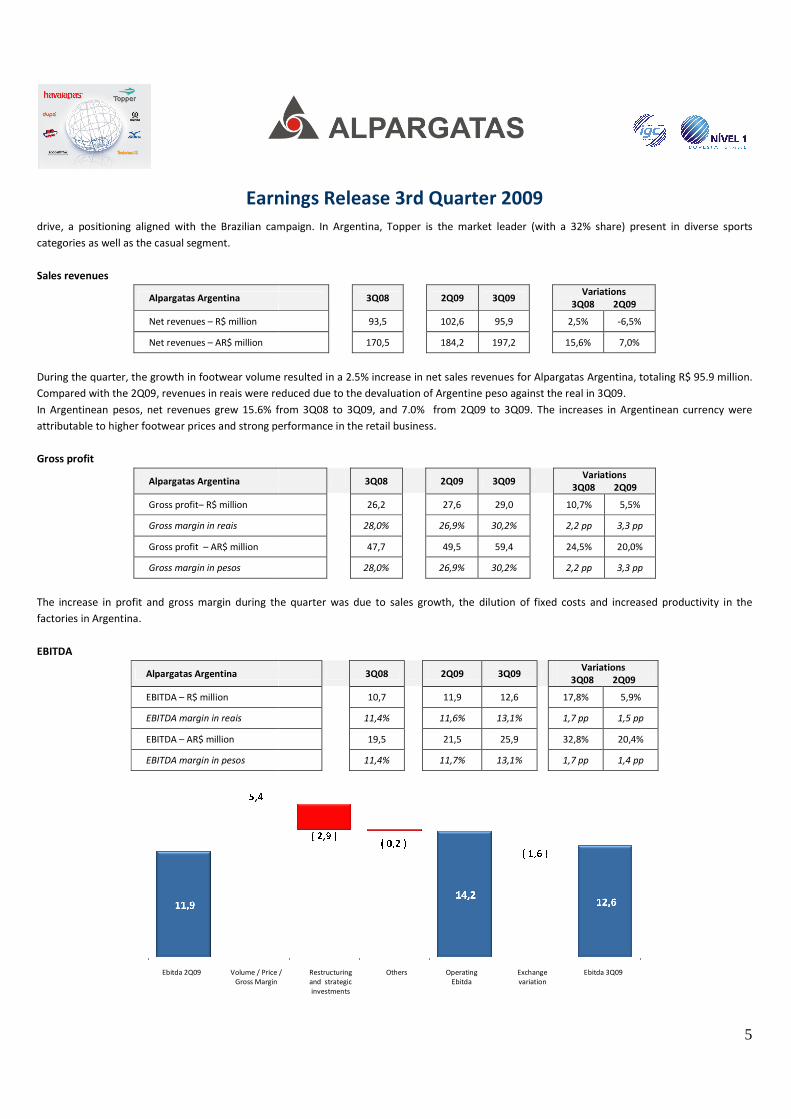

Alpargatas Argentina

Sales volume

Alpargatas Argentina

Sales volume

Footwear (000’s of pairs)

Textiles (000’s of m2)

Alpargatas Argentina’s footwear sales topped three million pairs in the quarter, 30% up on 2Q09, and 18.7% up on 3Q08. The st

the result of the new Topper launch in the country. The “El Corazón Manda” campaign was la

Earnings Release 3rd Quarter 2009

produced with Havaianas Brasil residues, the sandal is a concrete demonstration of Alpargatas’ concern with the

the innovations in the line generated a tenfold increase in sales compared with the last collection, bolstering the IPÊ

Institute, dedicated to the preservation of Brazil’s flora and fauna.

Launch of the Dupé 2009/2010 collection with 30 models; reformulation of the brand’s website and launch of an advertising campaign on

the major TV channels in the Northeast of the country.

Participation of Havaianas and Dupé in Francal, an important footwear fair held in São Paulo.

sales of the “The One Professional” football boot. The model is used by a number of professionals playing in the Brazilian sp

Launch of clothing line with new materials and designs for shirts, shorts and pants.

otwear aligned with the strategy to position the Topper brand in a number of different sports categories and in

leading sporting goods distribution channels.

Realization of the second stage of the Mizuno 10 miles competition in São Paulo. The race is part of the Mizuno calender, which includes races in

Participation in the fourth edition of the São Paulo Running Show, the most important street racing and triathlon event in th

ase in the number of sales outlets in comparison with 3Q08.

Launch of the Timberland Spring/Summer collection, the highlights being the Canvas and Leather lines, aimed at increasing sha

The international operations are made up of the Alpargatas USA, Alpargatas Europe and Alpargatas Argentina businesses. On Sep

the breakdown of net revenues from the international operations was:

3Q08 2Q09 3Q09

2.529 2.285 3.001

4.316 4.040 5.371

Alpargatas Argentina’s footwear sales topped three million pairs in the quarter, 30% up on 2Q09, and 18.7% up on 3Q08. The st

the result of the new Topper launch in the country. The “El Corazón Manda” campaign was launched in July, reinforcing the brand’s irreverence and

16%84%

INTERNATIONAL OPERATIONS

Breakdown of net revenues

Alpargatas USA &

Alpargatas Europe

Alpargatas Argentina

4

produced with Havaianas Brasil residues, the sandal is a concrete demonstration of Alpargatas’ concern with the

the innovations in the line generated a tenfold increase in sales compared with the last collection, bolstering the IPÊ

tion of the brand’s website and launch of an advertising campaign on

sales of the “The One Professional” football boot. The model is used by a number of professionals playing in the Brazilian special

otwear aligned with the strategy to position the Topper brand in a number of different sports categories and in

is part of the Mizuno calender, which includes races in

Participation in the fourth edition of the São Paulo Running Show, the most important street racing and triathlon event in the country.

Launch of the Timberland Spring/Summer collection, the highlights being the Canvas and Leather lines, aimed at increasing share for the

The international operations are made up of the Alpargatas USA, Alpargatas Europe and Alpargatas Argentina businesses. On September 30th 2009,

Variations

3Q08 2Q09

18,7% 30,0%

24,4% 32,9%

Alpargatas Argentina’s footwear sales topped three million pairs in the quarter, 30% up on 2Q09, and 18.7% up on 3Q08. The strong performance is

unched in July, reinforcing the brand’s irreverence and

Earnings Release

drive, a positioning aligned with the Brazilian campaign. In Argentina, Topper is the market leader (with a 32% share) presen

categories as well as the casual segment.

Sales revenues

Alpargatas Argentina

Net revenues – R$ million

Net revenues – AR$ million

During the quarter, the growth in footwear volume resulted in a 2.5% increase in net sales revenues for Alpargatas Argentina,

Compared with the 2Q09, revenues in reais were reduced due to the devaluation of

In Argentinean pesos, net revenues grew 15.6% from 3Q08 to 3Q09, and 7.0% from 2Q09 to 3Q09. The increases in Argentinean cu

attributable to higher footwear prices and strong performance in the retail

Gross profit

Alpargatas Argentina

Gross profit– R$ million

Gross margin in reais

Gross profit – AR$ million

Gross margin in pesos

The increase in profit and gross margin during the quarter was due to sales growth, the dilution of fixed costs and increased

factories in Argentina.

EBITDA

Alpargatas Argentina

EBITDA – R$ million

EBITDA margin in reais

EBITDA – AR$ million

EBITDA margin in pesos

Ebitda 2Q09 Volume / Price Gross Margin

Earnings Release 3rd Quarter 2009

drive, a positioning aligned with the Brazilian campaign. In Argentina, Topper is the market leader (with a 32% share) presen

3Q08 2Q09 3Q09

93,5 102,6 95,9

170,5 184,2 197,2

During the quarter, the growth in footwear volume resulted in a 2.5% increase in net sales revenues for Alpargatas Argentina,

Compared with the 2Q09, revenues in reais were reduced due to the devaluation of Argentine peso against the real in 3Q09.

In Argentinean pesos, net revenues grew 15.6% from 3Q08 to 3Q09, and 7.0% from 2Q09 to 3Q09. The increases in Argentinean cu

attributable to higher footwear prices and strong performance in the retail business.

3Q08 2Q09 3Q09

26,2 27,6 29,0

28,0% 26,9% 30,2%

47,7 49,5 59,4

28,0% 26,9% 30,2%

The increase in profit and gross margin during the quarter was due to sales growth, the dilution of fixed costs and increased

3Q08 2Q09 3Q09

10,7 11,9 12,6

11,4% 11,6% 13,1%

19,5 21,5 25,9

11,4% 11,7% 13,1%

/

Restructuring and strategic investments

Operating Ebitda

Exchange variation

Others

5

drive, a positioning aligned with the Brazilian campaign. In Argentina, Topper is the market leader (with a 32% share) present in diverse sports

Variations

3Q08 2Q09

2,5% -6,5%

15,6% 7,0%

During the quarter, the growth in footwear volume resulted in a 2.5% increase in net sales revenues for Alpargatas Argentina, totaling R$ 95.9 million.

Argentine peso against the real in 3Q09.

In Argentinean pesos, net revenues grew 15.6% from 3Q08 to 3Q09, and 7.0% from 2Q09 to 3Q09. The increases in Argentinean currency were

Variations

3Q08 2Q09

10,7% 5,5%

2,2 pp 3,3 pp

24,5% 20,0%

2,2 pp 3,3 pp

The increase in profit and gross margin during the quarter was due to sales growth, the dilution of fixed costs and increased productivity in the

Variations

3Q08 2Q09

17,8% 5,9%

1,7 pp 1,5 pp

32,8% 20,4%

1,7 pp 1,4 pp

Ebitda 3Q09

6

Earnings Release 3rd Quarter 2009

The main factors behind Alpargatas Argentina’s variation in EBITDA compared with 2Q09 are:

� A R$ 5.4 million gain from volume/price/gross margin resulting from sales growth, cost dilution and manufacturing productivity.

� Restructuring costs and strategic investments were R$ 2.9 million up on the 2Q09, mainly due to increased spending on advertising and

promoting the new Topper brand.

� A R$ 1.6 million exchange loss due to the appreciation of the real against the Argentinean peso.

Alpargatas USA and Alpargatas Europe

Sales volume

Alpargatas USA and Alpargatas Europe 3Q08

2Q09 3Q09

Variações

3Q08 2Q09 Sales volume

Sandals (000’s of pairs) 167 1.224 387 131,7% -68,4%

The volume of sandals commercialized in the USA and Europe reached 386,800 pairs, an increase of 131.7% compared with 3Q08. The volume increase

for the calendar year was 21.5%. This strong result is due to the success of the communication campaigns, increased consumer awareness of the brand

and the expansion of the number of sales outlets. The 68.4% reduction in volume compared with 2Q09 is due to seasonal factors. Sandal sales are

stronger in the spring and summer in the northern hemisphere and are concentrated in the second quarter of the year. To minimize the effect of

seasonal variations in sales, we are working on Havianas line extensions to develop products for year round consumption.

Sales revenues

Alpargatas USA and Alpargatas Europe 3Q08 2Q09 3Q09 Variations

3Q08 2Q09

Net revenues – R$ million 2,4 23,3 8,2 241,7% -64,8%

The strategy of substituting intermediate distribution channels with our own operations has contributed to an increase in the average price of sandals

and in revenues. Alpargatas Europe operates directly in the Spanish, English, French, Italian and Portuguese markets, through more than 3,700 sales

outlets. The same is true for Alpargatas USA, which sells directly to large American customers, with the number of sales outlets totaling around 3

thousand. Increases in volume and average price ensured higher sales revenues. Net revenues for the subsidiaries increased 241.7% compared with

the 3Q08, totaling R$ 8.2 million; the increase compared with the first three quarters of 2008 was 191.4%. The reduction in volume against 2Q09 was

the result of seasonal factors.

Gross profit

Alpargatas USA and Alpargatas Europe 3Q08 2Q09 3Q09 Variations

3Q08 2Q09

Gross profit – R$ million 1,3 9,5 2,7 107,7% -71,6%

Gross margin 54,2% 40,8% 32,9% - 21,2 pp -7,8 pp

Gross profit in the subsidiaries grew 107.7% in comparison with 3Q08 as a result of higher revenues. For the nine months of 2009, gross profit

increased R$ 16.7 million compared with same period last year. In the comparison with 2Q09, profits and gross margin were lower due to the effect of

seasonal factors.

EBITDA

Operations that are maturing or growing require strategic investments to expand and consolidate the Havaianas brand in the target market. These

expenditures are directed at communication and distribution, as well as administrative and commercial personnel. These strategic investments explain

why the subsidiaries’ EBITDA is still negative.

Earnings Release

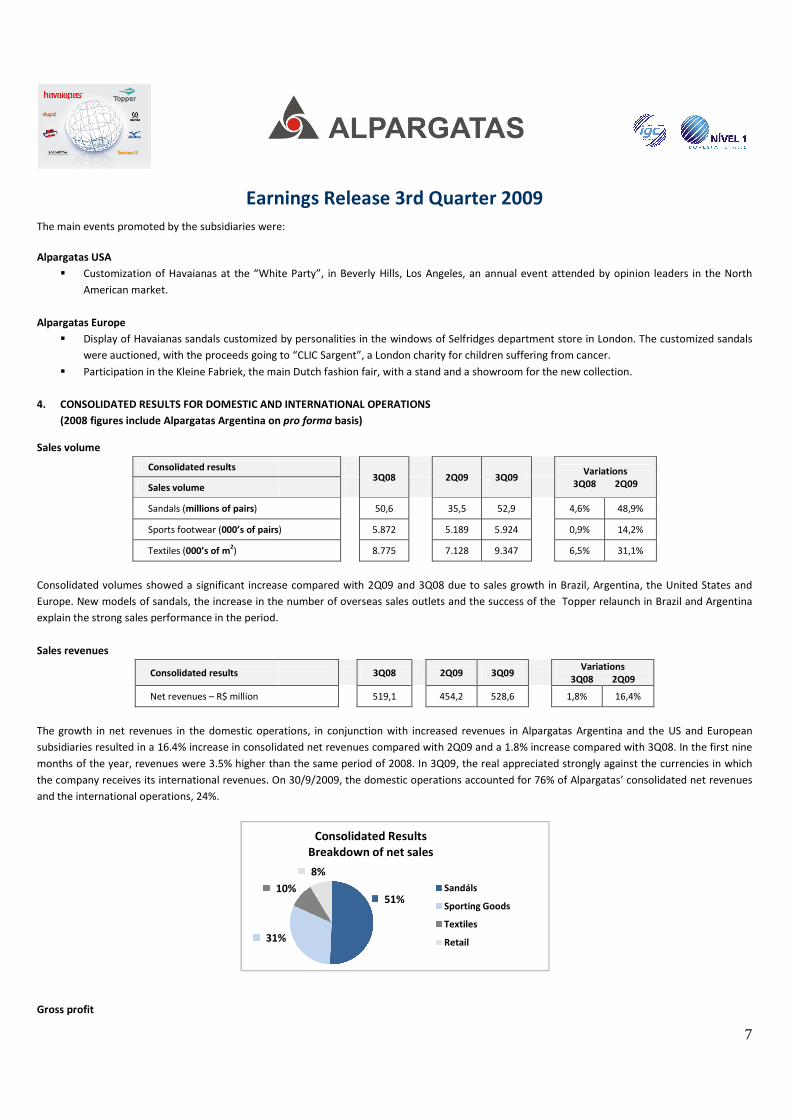

The main events promoted by the subsidiaries were

Alpargatas USA

� Customization of Havaianas at the “White Party”, in Beverly Hills, Los Angeles, an annual event attend

American market.

Alpargatas Europe

� Display of Havaianas sandals customized by personalities in the windows of Selfridges department store in London. The customi

were auctioned, with the proceeds going to “CLIC

� Participation in the Kleine Fabriek, the main Dutch fashion fair, with a stand and a showroom for the new collection.

4. CONSOLIDATED RESULTS FOR DOMESTIC AND INTERNATIONAL OPERATIONS

(2008 figures include Alpargatas Argentina on

Sales volume

Consolidated results

Sales volume

Sandals (millions of pairs)

Sports footwear (000’s of pairs)

Textiles (000’s of m2)

Consolidated volumes showed a significant increase compared with 2Q09 and 3Q08 due to sales growth in Brazil, Argentina, the

Europe. New models of sandals, the increase in the number of overseas sales outlets and th

explain the strong sales performance in the period.

Sales revenues

Consolidated results

Net revenues – R$ million

The growth in net revenues in the domestic operations, in conjunction with increased revenues in Alpargatas Argentina and the

subsidiaries resulted in a 16.4% increase in consolidated net revenues compared with 2Q09 a

months of the year, revenues were 3.5% higher than the same period of 2008. In 3Q09, the real appreciated strongly against th

the company receives its international revenues. On

and the international operations, 24%.

Gross profit

31%

10%

Earnings Release 3rd Quarter 2009

The main events promoted by the subsidiaries were:

Customization of Havaianas at the “White Party”, in Beverly Hills, Los Angeles, an annual event attend

Display of Havaianas sandals customized by personalities in the windows of Selfridges department store in London. The customi

were auctioned, with the proceeds going to “CLIC Sargent”, a London charity for children suffering from cancer.

Participation in the Kleine Fabriek, the main Dutch fashion fair, with a stand and a showroom for the new collection.

CONSOLIDATED RESULTS FOR DOMESTIC AND INTERNATIONAL OPERATIONS

(2008 figures include Alpargatas Argentina on pro forma basis)

3Q08

2Q09 3Q09

50,6 35,5 52,9

) 5.872 5.189 5.924

8.775 7.128 9.347

Consolidated volumes showed a significant increase compared with 2Q09 and 3Q08 due to sales growth in Brazil, Argentina, the

Europe. New models of sandals, the increase in the number of overseas sales outlets and the success of the Topper relaunch in Brazil and Argentina

3Q08 2Q09 3Q09

519,1 454,2 528,6

The growth in net revenues in the domestic operations, in conjunction with increased revenues in Alpargatas Argentina and the

subsidiaries resulted in a 16.4% increase in consolidated net revenues compared with 2Q09 and a 1.8% increase compared with 3Q08. In the first nine

months of the year, revenues were 3.5% higher than the same period of 2008. In 3Q09, the real appreciated strongly against th

the company receives its international revenues. On 30/9/2009, the domestic operations accounted for 76% of Alpargatas’ consolidated net revenues

51%

31%

10%

8%

Consolidated Results

Breakdown of net sales

Sandáls

Sporting Goods

Textiles

Retail

7

Customization of Havaianas at the “White Party”, in Beverly Hills, Los Angeles, an annual event attended by opinion leaders in the North

Display of Havaianas sandals customized by personalities in the windows of Selfridges department store in London. The customized sandals

Sargent”, a London charity for children suffering from cancer.

Participation in the Kleine Fabriek, the main Dutch fashion fair, with a stand and a showroom for the new collection.

Variations

3Q08 2Q09

4,6% 48,9%

0,9% 14,2%

6,5% 31,1%

Consolidated volumes showed a significant increase compared with 2Q09 and 3Q08 due to sales growth in Brazil, Argentina, the United States and

e success of the Topper relaunch in Brazil and Argentina

Variations

3Q08 2Q09

1,8% 16,4%

The growth in net revenues in the domestic operations, in conjunction with increased revenues in Alpargatas Argentina and the US and European

nd a 1.8% increase compared with 3Q08. In the first nine

months of the year, revenues were 3.5% higher than the same period of 2008. In 3Q09, the real appreciated strongly against the currencies in which

30/9/2009, the domestic operations accounted for 76% of Alpargatas’ consolidated net revenues

Earnings Release

Consolidated results

Gross profit – R$ million

Gross Margin

The increase in gross profit in the quarter is due principally to the increase in profit and gross margin from domestic opera

Argentina. The dilution of fixed costs and the increase in manufacturing productivity l

with the 2Q09 and a 8.3% increase compared with 3Q08. In consequence, the consolidated gross margin grew 7.7% and 2.8% compar

and 3Q08, respectively.

EBITDA

Consolidated results

EBITDA – R$ million

EBITDA Margin

The most relevant factors explaining the variation in consolidated EBITDA compared with 2Q09 are:

� A R$ 69.1 gain in volume/price/gross margin, mainly from domestic operations.

� Savings of R$ 14.0 million from restructuring and reduced operating expenditures.

� Non-recurring tax recovery (PIS/Cofins) of R$ 13.3 million in 2Q09.

Net profit

Consolidated results

Net profit– R$ million

Net margin

Ebitda 2Q09 Volume / Price

Earnings Release 3rd Quarter 2009

3Q08 2Q09 3Q09

222,8 172,7 241,4

42,9% 38,0% 45,7%

The increase in gross profit in the quarter is due principally to the increase in profit and gross margin from domestic opera

Argentina. The dilution of fixed costs and the increase in manufacturing productivity led to a 39.8% increase in consolidated gross profit compared

with the 2Q09 and a 8.3% increase compared with 3Q08. In consequence, the consolidated gross margin grew 7.7% and 2.8% compar

3Q08 2Q09 3Q09

87,4 40,2 101,7

16,8% 8,9% 19,2%

variation in consolidated EBITDA compared with 2Q09 are:

A R$ 69.1 gain in volume/price/gross margin, mainly from domestic operations.

Savings of R$ 14.0 million from restructuring and reduced operating expenditures.

of R$ 13.3 million in 2Q09.

3Q08 2Q09 3Q09

44,3 -1,3 53,5

8,5% - 10,1%

Restructuring and

Productivity Gains

Operating Ebitda

Exchange variation

Non-recurring tax recovery

Others

8

Variations

3Q08 2Q09

8,3% 39,8%

2,8 pp 7,7 pp

The increase in gross profit in the quarter is due principally to the increase in profit and gross margin from domestic operations and Alpargatas

ed to a 39.8% increase in consolidated gross profit compared

with the 2Q09 and a 8.3% increase compared with 3Q08. In consequence, the consolidated gross margin grew 7.7% and 2.8% compared with 2Q09

Variations

3Q08 2Q09

16,4% 153,0%

2,4 pp 10,4 pp

Variations

3Q08 2Q09

20,8% -

1,6 pp -

Exchange variation

Ebitda 3Q09

9

Earnings Release 3rd Quarter 2009

Alpargatas’ excellent performance in the quarter, with an increase in revenues and profitability, was reflected in the company’s net profit, which grew

by R$ 54.8 million from 2Q09 to 3Q09, corresponding to a 20.8% increase compared with 3Q08. The main reasons for this increase in consolidated net

profit compared with 2Q09 are:

� A R$ 61.5 million increase in EBITDA.

� A positive R$ 6.0 million variation in the company’s equity investment in the Tavex Corporation.

� A R$ 19.7 million increase in corporation tax (IRRF/CSLL) due to the profits generated in the quarter.

Cash flow

On September 30, 2009, Alpargatas had a cash balance of R$ 253.2 million, R$ 76.2 million more than on December 31, 2008. The acceleration of the

cash conversion cycle, the result of careful current account management, is the main explanation for the growth in cash generation. The largest inflow

in the period was from EBITDA, which reached R$ 198.3 million, due to solid operating performance, particularly during the third quarter of the year.

Working cash productivity generated a gain of R$ 1.1 million and investments in permanent assets totaled R$ 39.6 million. Debt amortization and

shareholder remuneration constituted the main cash disbursements, totaling R$ 75.4 million.

Ebitda Financial income

Net profit 2Q09

Return of investments in

subsidiaries Income taxes

IRRF/CSLL Others Net profit

3Q09

Cash balance on December 31st, 2008

EBITDA

Working capital

investment Fixed asset

investment Operational

sub-total Exchange variation

Financial result

Payment of income

tax (IR/CSLL)

Debt amortization

(net of loans)

Sub-total Shareholder remuneration

Cash balance on September

30th, 2009

10

Earnings Release 3rd Quarter 2009

Indebtedness

On September 30, 2009, consolidated financial indebtedness stood at R$ 296.8 million, of which R$ 251.9 million was accounted for by São Paulo

Alpargatas and R$ 44.9 million by Alpargatas Argentina, with the following profile:

� R$ 162.2 million (55% of the total) due in the short term, of which 48% was in foreign currency for financing the working capital of the US

and European subsidiaries, and 52% was in reais, in loans from the BNDES and the Banco do Nordeste.

� R$ 134.6 million (45% of the total) due in the long term, of which 33% was in foreign currency (Alpargatas Argentina) and 67% in reais.

Consolidated net debt was reduced to R$ 43.7 million in the third quarter of the year compared with R$ 100.1 million on June 30th, 2009. The

reduction in debt debt underscores Alpargatas’ financial robustness, which corresponds to 0.1 times the company’s 2008 EBITDA.

5. CAPITAL MARKETS

Alpargatas shares performed well in the first nine months of 2009. The preferential shares (ALPA4) appreciated by 63%, on a par with the 64%

variation in the Ibovespa index. The three advances corresponding to interest on own capital approved by the Administrative Council totaled R$ 24.4

million, R$ 14.6 million of which was paid in May, R$ 4.9 million in August and R$ 4.9 million in October. On November 13, the Council voted to

advance another R$ 4.9 million in interest on own capital, payable on December 18.

6. SUBSEQUENT EVENTS

Alpargatas filed a public offer with the Comisión Nacional de Valores in Buenos Aires to acquire all outstanding Alpargatas Argentina shares at the price

of AR$ 3.40 (three pesos and forty centavos) per share. This offer will facilitate the integration between the companies in Brazil and Argentina and will

permit further investments in manufacturing, logistics, brand communication and people development.

In an Extraordinary General Shareholders Meeting held on October 29th, Pedro Pullen Parente and Cláudio Borin Guedes were elected to the

Administrative Council. We extend our thanks to the outgoing council members Carlos Pires Oliveira Dias and José Alberto Diniz de Oliveira.

7. OUTLOOK

In the long term, the World Cup in 2014 and the Olympic Games in 2016 will be important events for the market and for our brands. The growth and

increasing maturity of our subsidiaries in the United States and Europe and the increased synergies resulting from the integration with Alpargatas

Argentina will also boost Alpargatas’ performance. We are very well positioned for growth in this promising market as a result of our production

capacity, our innovative products, our professional talents and the passion our brands inspire in consumers.

11

Earnings Release 3rd Quarter 2009

Attachment I – Balance Sheet 09/30 (thousands of R$)

ASSETS 2009 2008 (a)

LIABILITIES 2009 2008 (a)

Current Assets 981,486 929,225 Current Liabilities 433,443 404,670

Cash and banks 27,503 22,650 Suppliers 113,519 130,895

Financial applications 225,711 157,103 Financing 162,329 98,074

Clients (net after Provision for Doubtful Debtors) 401,706 383,259 Restructuring and debt agreements 13,298 27,714

Stocks 250,818 309,693 Salaries and payroll charges 71,156 79,099

Other accounts receivable 13,238 23,451 Contingencies provision 8,030 9,246

Anticipated expenses 8,416 6,068 Income Tax and Social Contribution Provision 9,490 7,607

Recoverable taxes 35,067 9,926 Taxes payable 16,525 10,838

Differed Income Tax and Social Contribution 19,027 17,075 Interest over our own capital and dividends payable 5,164 16,413

Other accounts payable 33,932 24,784

Long Term Assets 90,249 94,815 Long Term Liabilities 251,902 376,259

Goods destined to sale 6,374 6,775 Financing 134,509 174,849

Recoverable taxes 19,652 22,305 Restructuring and debt agreements 30,458 99,816

Differed Income Tax and Social Contribution 27,743 34,690 Taxes payable provision 36,965 36,121

Tax and labor compulsory deposit 12,785 10,492 Income Tax and Social Contribution Provision 18,254 31,652

Other accounts receivable 23,695 20,553 Contingencies provision 26,729 28,103

Other accounts payable 4,987 5,718

Permanent Assets 650,541 722,504 Minority Equity 36,715 44,776

Investments 85,441 124,955 Net Equity 1,000,216 920,837

Fixed assets 292,630 334,598 Realized capital stock 391,803 391,804

Intangible 265,389 254,034 Capital reserve 270,395 177,336

Differed 7,081 8,917 Treasury stocks (28,326) (28,609)

Profit reserves 405,107 390,819

Equity Assessment (38,763) (10,513)

Total Assets 1,722,276 1,746,543 Total Liabilities 1,722,276 1,746,543

Book value per share (R$) 57.42 52.43

(a) The 2008 numbers include Alpargatas Argentina (pro forma)

12

Earnings Release 3rd Quarter 2009

Attachment II – Results Statement (thousands of R$)

3Q9 3Q8 (a)

9M9 9M8 (a)

Gross sales revenue 623.034 617.318 1.698.310 1.655.512

Net sales revenue 528.607 519.085 1.438.749 1.390.134

Sold products costs (287.210) (295.456) (844.875) (811.003)

Gross profits 241.397 223.629 593.875 579.131

gross margin 45,7% 43,1% 41,3% 41,7%

Operational Revenues (Expenses) (161.241) (153.765) (462.658) (407.612)

Sales (122.678) (117.252) (371.458) (336.051)

General and Administrative (26.013) (26.690) (76.856) (76.356)

Administrators’ compensation (1.113) (1.051) (3.317) (2.964)

Differed amortization (5.676) (3.807) (14.611) (9.450)

Others (5.762) (4.965) 3.584 17.209

Operational Profit - EBIT 80.156 69.864 131.217 171.519

operational margin 15,2% 13,5% 9,1% 12,3%

Financial revenues 8.028 3.721 23.783 10.497

Financial expenses (12.503) (7.574) (42.082) (25.727)

Exchange Variation (636) 134 (5.620) (1.304)

Premium amortization 0 (2.544) 0 (7.632)

Equity accounting (2.406) (7.328) (15.270) (10.066)

Operational Income 72.639 56.273 92.028 137.287

Differed Income Tax and Social Contribution (18.013) (10.082) (17.365) (21.442)

Minority Equity (1.131) (1.858) (1.927) (8.307)

Net Income 53.495 44.333 72.736 107.538

EBITDA – millions of R$ 101,7 87,4 198,3 212,9

EBITDA margin 19,2% 16,8% 13,8% 15,3%

(a) The 2008 numbers include Alpargatas Argentina (pro forma)

13

Earnings Release 3rd Quarter 2009

Attachment III – EBITDA Calculation

National operations (millions of R$)

3Q9 3Q8 (a)

9M9 9M8 (a)

Operational Profit - EBIT 86,5 76,0 145,6 170,5

(+) Depreciation and amortization 12,1 10,5 34,5 29,9

(+/-) Items without a cash effect 5,3 3,7 8,5 3,2

(=) EBITDA 103,9 90,2 188,6 203,6

Alpargatas Argentina(millions of R$ - BRGAAP)

3Q9 3Q8 (a)

9M9 9M8 (a)

Operational Profit - EBIT 9,5 8,3 22,5 33,3

(+) Depreciation and amortization 2,6 3,1 8,9 8,5

(+/-) Items without a cash effect 0,5 (0,7) 1,8 (1,3)

(=) EBITDA 12,6 10,7 33,2 40,5

National and international operations results

consolidation (millions of R$)

3Q9 3Q8

(a) 9M9 9M8

(a)

Operational Profit - EBIT 80,9 69,9 131,9 171,5

(+) Depreciation and amortization 16,3 14,5 46,8 39,5

(+/-) Items without a cash effect 4,5 3,0 19,5 1,9

(=) EBITDA 101,7 87,4 198,3 212,9

(a) The 2008 numbers include Alpargatas Argentina (pro forma)

We calculated the EBITDA adding to the Operational Profit - EBIT depreciation and amortization and adding or subtracting, according to each case,

items without a cash effect. The EBITDA should not be considered an alternative to the net profit as an indicator of the operational performance or

an alternative to the cash flow as a liquidity indicator. The EBITDA does not have a standardized meaning and its calculation at Alpargatas may not

be comparable to that done by other companies.