east and south east operating area housing … · house building 13 house building ... (ssr) level,...

TRANSCRIPT

EAST AND SOUTH EAST OPERATING AREA HOUSING MARKET REPORT August 2014

HCA East & South East operating area housing market report, August 2014

Page 2

Contents

Introduction ................................................................................................................ 3

Summary .................................................................................................................... 3

The Housing Market .................................................................................................. 4

House prices 4

Affordability 6

Housing transactions 7

Private rental market 9

Mortgages 11

New homes ............................................................................................................... 12

Residential land values 12

House building 13

House building programmes managed by the HCA 15

Society ...................................................................................................................... 17

Homelessness 17

Additional information ............................................................................................ 18

East and South East HCA operating area 18

HCA case studies 18

HCA East & South East operating area housing market report, August 2014

Page 3

Introduction

This housing market report has been produced by the Homes and Communities Agency’s Strategic and Market Intelligence Team, to provide the reader with contextual information on house building and the housing market.

It is compiled predominantly from publically available data, and sources and links have been provided where appropriate. Any calculation and analysis is offered for clarity, but should not be taken as a statement of HCA policy.

The HCA’s East and South East (ESE) operating area (OA) consists of:

The following counties: Buckinghamshire, Cambridgeshire, East Sussex, Essex, Hertfordshire, Kent, Norfolk, Suffolk, Surrey and West Sussex, and,

The unitary authorities of Brighton and Hove, Medway Towns, Peterborough, Southend on Sea and Thurrock.

Greater London is not part of the ESE OA.

Housing market data are often only available at Standard Statistical Region (SSR) level, so the information contained within this report does not always exactly match the HCA’s OA boundaries. Our commentary will be clear about which geographical area is being referred to.

Where data are available at local authority level they are shown as maps, in the relevant sections. Our maps have been produced using ‘SIGnet’, the HCA’s bespoke online mapping tool, which we make available for the use of all public sector organisations, free of charge. Please contact us for details on how to obtain this service.

Summary

In April 2014, ONS simple average regional house prices were £217,686 in East

Anglia and £310,889 in the South East. These represent a 4.0% and a 7.6%

increase, respectively, compared to the previous year.

In the twelve months to March 2014, 101,443 homes were sold in the East

region and 153,859 in the South East. These are 28.4% and 28.1% more than in

the previous year.

Average median private rents in March 2014 were £625 per month in the East

SSR and £750 in the South East SSR. These figures are a 4.2% and 0.0%

increase, respectively, from the previous year.

The number of households facing mortgage possession action in court has

decreased over the last year by 14.3% in the East SSR and by 11.6% in the

South East.

House building starts totalled 25,820 in the year ending Q1 2014 in the East

South East OA, which is a 26.0% increase compared to the previous twelve

months.

House building programmes managed by the HCA for 1 April 2013 – 31 March

2014 show 9,439 housing starts (8,571 of which were affordable) and 7,096

(6,100) completions across the ESE OA. There were also 3,814 Help to Buy

completions in the OA.

Households accepted as homeless totalled 1,893 in Q1 2014 in the ESE OA.

This is a 5.6% increase compared to this quarter in the previous year.

HCA East & South East operating area housing market report, August 2014

Page 4

The Housing Market

House prices

Following the price dip of 2008-09, the average national house price has increased by 20.5% (Q1 2009 to Q1 2014), largely driven by housing markets in London and the South East. Over the same period the average East Anglia price increased by 13.2%, whilst in the South East prices increased by 17.9%.

Average prices in East Anglia are below the national average, with this gap having widened slightly. Prices in the South East, however, are consistently higher than the English average.

Figure 1 – House prices: simple average, all dwelling types

Table 1 – House prices: simple average, all dwellings

Average house price:

% change Q1 2013 Q1 2014

England 253,175 270,884 7.0%

East Anglia 209,327 217,686 4.0%

South East 288,943 310,889 7.6%

Source: Regulated Mortgage Survey, in ONS House Price Index Table 12, Apr 2014. http://www.ons.gov.uk/ons/taxonomy/index.html?nscl=House+Price+Indices

HCA East & South East operating area housing market report, August 2014

Page 5

House prices are typically highest in areas closer to London. The local authority area with the lowest median house valuation in the OA is Peterborough at £126,000, and the highest is Elmbridge at £465,000 (Landmark/Calnea).

Figure 2 – Average (median) house price valuation, by local authority

Source: Landmark/Calnea, median valuation, May 2014.

HCA East & South East operating area housing market report, August 2014

Page 6

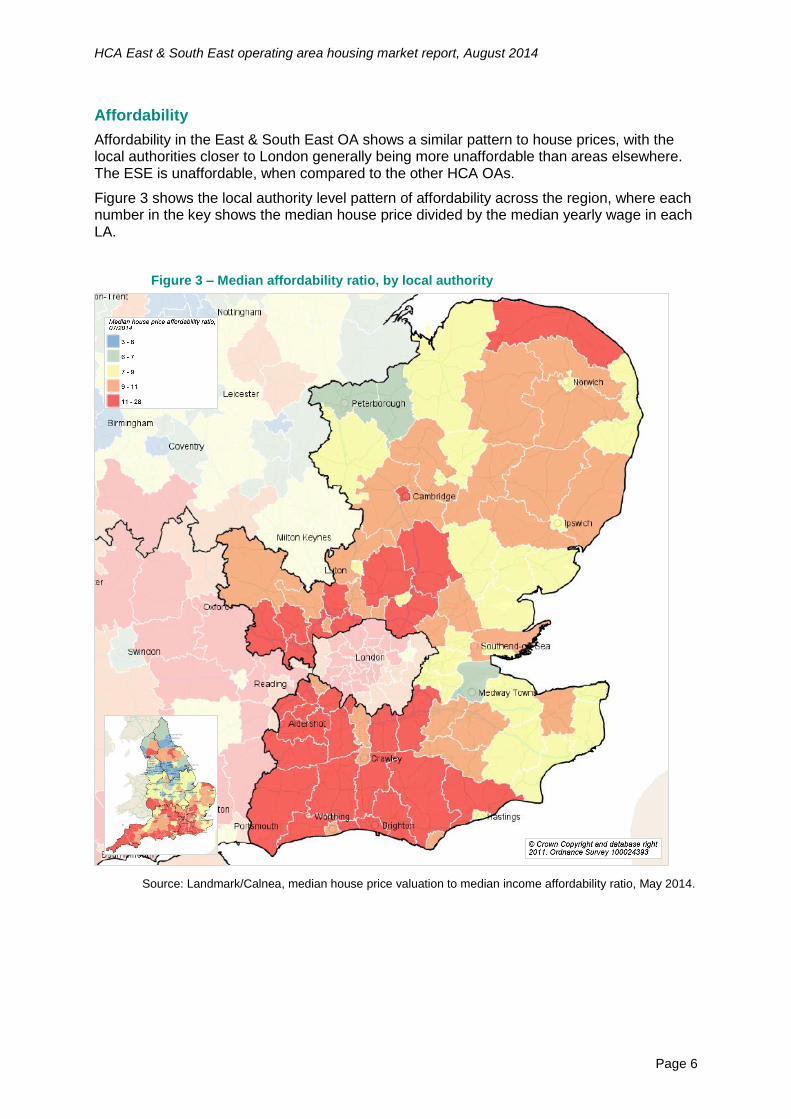

Affordability

Affordability in the East & South East OA shows a similar pattern to house prices, with the local authorities closer to London generally being more unaffordable than areas elsewhere. The ESE is unaffordable, when compared to the other HCA OAs.

Figure 3 shows the local authority level pattern of affordability across the region, where each number in the key shows the median house price divided by the median yearly wage in each LA.

Figure 3 – Median affordability ratio, by local authority

Source: Landmark/Calnea, median house price valuation to median income affordability ratio, May 2014.

HCA East & South East operating area housing market report, August 2014

Page 7

Housing transactions

House transactions in the South East and East SSRs have been consistently above the national average, with a sharp increase in the relative number of sales since early 2013.

Figure 5 – Housing transactions per 1,000 households

Note: The number of households is from the 2011 Census and, for convenience, is held to be consistent for subsequent years.

Table 2 – Housing transactions: number of sales in the preceding 12 months

March 2013 March 2014 % change

England 656,156 838,236 27.7%

South East 120,116 153,859 28.1%

East 78,991 101,443 28.4%

Source: Land Registry, published in DCLG live table 5841, June 2014.

https://www.gov.uk/government/statistical-data-sets/live-tables-on-housing-market-and-house-prices

1

Reproduced with kind permission of Land Registry. This material is Crown copyright and is reproduced with the permission of Land Registry under delegated authority from the Controller of HMSO.

HCA East & South East operating area housing market report, August 2014

Page 8

Figure 6 – Total sales in the last 12 months, as a percentage of all residential properties

Source: Landmark/Calnea, May 2014.

HCA East & South East operating area housing market report, August 2014

Page 9

Private rental market

Rents in the East SSR are similar to the England averages, whilst rents in the South East are consistently higher.

Figure 7 – Private rents, £ per month – distribution of rent levels

In England median rents roughly increased with inflation over the year. However in the East SSR median rents have risen more rapidly, while the South East SSR has remained static.

Table 3 – Average private rents, £ per month

Median rents Mean rents

March 13 March 14 March 13 March 14

England £585 £595 £724 £720

East £600 £625 £677 £690

South East £750 £750 £849 £864

Source: VOA Private Rental Market Statistics, March 2014. http://www.voa.gov.uk/Corporate/Publications/browseStatistics.html

HCA East & South East operating area housing market report, August 2014

Page 10

Rents show a similar geographical distribution to house prices, with local authority average prices increasing the closer they are to London, and the lowest prices mostly in coastal towns. The local authority area with the lowest average monthly rents in the ESE OA is Ipswich (median £475, mean £481) and the highest rents are in South Buckinghamshire (median £1,200, mean £1,530).

Figure 8 – Median private rents by local authority, £ per calendar month

Source: VOA Private Rental Market Statistics, March 2014.

http://www.voa.gov.uk/Corporate/Publications/browseStatistics.html

HCA East & South East operating area housing market report, August 2014

Page 11

Mortgages

The total number and value of mortgages sold for house purchase in the UK has been following an upward trajectory since late 2012, but are still below pre-2008 levels.

Figure 9 – Approvals for lending secured on dwellings, UK

Source: © Bank of England: Bankstats, Part A, table 5.4, seasonally adjusted, Q1 2014. http://www.bankofengland.co.uk/statistics/Pages/default.aspx

The number of households facing mortgage possession action in court has decreased by 12.5% in England over the last year. This national trend is mirrored in the OA with a 14.3% decrease in possession claims issued in county courts in the East SSR between Q1 2013 to Q1 2014, and 11.6% in the South East.

Figure 10 – Number of claims for mortgage possession2 issued in county courts, per

1,000 households, quarterly

Source: Ministry of Justice, Mortgage and Landlord Possession Statistics, May 2014. https://www.gov.uk/government/collections/mortgage-and-landlord-possession-statistics

2 These figures represent court actions for possession and not numbers of homes actually taken.

HCA East & South East operating area housing market report, August 2014

Page 12

New homes

Residential land values

The Savills residential development land value indices show relative changes in land values. Following a halving of value from 2007 to 2009, greenfield land values in Great Britain have returned to three quarters of their 2007 value. Indexed values in the Eastern region are calculated to have risen to nearly three quarters of their 2007 level, and more in the South East3.

Figure 11: Greenfield residential land value growth index, quarterly (June 2005 = 100)

Urban land values fell proportionally further post-2007, and the British average value is now just over half of its peak level. Prices in the Eastern area are just under half of their 2007 value, whilst the South East area has increased to nearly two thirds of its 2007 value.

Figure 12: Urban residential land value growth index, quarterly (June 2005 = 100)

Source: Savills Research, Development Land Statistical Supplement, June 2014.

3 ‘Northern’ comprises the North East, North West and Yorkshire and The Humber SSRs. ‘Eastern’ comprises the East Midlands

and East of England SSRs. The indices are based on valuations rather than transactions.

HCA East & South East operating area housing market report, August 2014

Page 13

House building

In the twelve months to March 2014, 16,170 new homes were started on site in the East of England SSR and 21,980 in the South East SSR. This is a 26.4% increase on the previous year in the East and 17.5% increase in the South East.

Across England, starts in the past twelve months were 31.4% higher than the previous year.

Figure 13 – House building activity, SSRs, quarterly

Table 4 – House building activity, starts and completions, twelve-month periods

East of England SSR South East SSR

Starts on site

in twelve months to Q1

Completions on site in

twelve months to Q1

Starts on site in twelve

months to Q1

Completions on site in

twelve months to Q1

2009 13,230 15,950 19,970 24,450

2010 14,480 15,280 19,500 20,020

2011 14,850 15,690 20,070 21,710

2012 12,790 14,060 18,700 19,630

2013 16,170 14,650 21,980 19,320

Source: DCLG house building, Live Tables 213 (England) and 253a (LAs), Q1 2014. https://www.gov.uk/government/statistical-data-sets/live-tables-on-house-building

HCA East & South East operating area housing market report, August 2014

Page 14

In the East and South East OA, the local authority with the greatest number of starts in the year ending Q1 2014 was Aylesbury, with 1130 starts (990 completions). The local authority with the fewest starts was Malden with 20 starts (60 completions).

Figure 14 – Number of starts on site, from Q2 2013-Q1 2014, by local authority

Source: CLG house building, Live Tables 213 (England) and 253a (LAs), August 2014.

HCA East & South East operating area housing market report, August 2014

Page 15

House building programmes managed by the HCA

The HCA official statistics show that 38,845 housing starts (34,461 housing completions) were delivered through programmes managed by the HCA in England in 2013-14. In the ESA OA they represented 37% of all house building starts (31% of all completions), which compares to a national average (excluding London) of 35% for all starts, (36% of all completions).

Nationally, 19,401 new homes were sold with the assistance of a Help to Buy equity loan in 2013-14 under the Help to Buy programme. Within the ESE 3,814 units were delivered, which represents 17% of all house building completions in the OA.

Table 5 – HCA housing starts on site and completions, 1 Apr 2013 – 31 March 20144

England ESE OA

Starts on site

Affordable Rent 25,486 6,237

Social Rent 2,638 489

Intermediate Rent 0 0

Affordable Home Ownership 4,738 1,845

Total Affordable 32,862 8,571

Market 5,983 868

Total 38,845 9,439

Completions

Affordable Rent 17,094 3,377

Social Rent 4,487 1,099

Intermediate Rent 117 55

Affordable Home Ownership 5,945 1,569

Total Affordable 27,643 6,100

Market 6,818 996

Total 34,461 7,096

Help to Buy completions

Total 19,401 3,814

Source: © Homes and Communities Agency, National Housing Statistics, June 2014. http://www.homesandcommunities.co.uk/housing-statistics

4 A ‘start’ and ‘completion’ may be defined differently to the DCLG housebuilding statistics above; units may be

counted at different points in time in the construction process.

HCA East & South East operating area housing market report, August 2014

Page 16

Figure 15 – HCA housing starts on site, 1 Apr 2013 – 31 March 2014

Source: © Homes and Communities Agency, National Housing Statistics, June 2014.

HCA East & South East operating area housing market report, August 2014

Page 17

Society

Homelessness

Following falls in the homelessness rate per capita between 2003 and 2009, homelessness in England has stabilised in the last four years.

Over the last ten years, homelessness rates in the South East and the East of England SSRs have both followed a similar pattern, with the South East at a lower level than the national average.

Figure 16 - Rate of homeless acceptances per 1,000 households, per quarter

Note: The number of households is from the 2011 Census and, for convenience, is held to be consistent for all years.

Table 6 – Homelessness acceptances

Q1 2014 Q1 2013

Number of

households

accepted as

homeless

No of house-

holds accepted,

per 1,000

households

Number of

households

accepted as

homeless

No of house-

holds accepted,

per 1,000

households

England 12,520 0.56 13,230 0.58

ESE OA 1,893 0.45 1,792 0.42

Source: Local Authority action under statutory homelessness provisions, DCLG Live Table 784a. https://www.gov.uk/government/statistical-data-sets/live-tables-on-homelessness

The ESE OA local authorities that accepted the greatest numbers of households as statutory homeless in the latest quarter were Brighton and Hove (160, 1.30 per 1,000 households) and Basildon (90, 1.22 per 1,000 households). At a household per capita level, Brighton accepted the most homeless households in the OA.

HCA East & South East operating area housing market report, August 2014

Page 18

Additional information

East and South East HCA operating area

Geograph

ical coverage

Data Source/link

Population ESE OA 10,204,174 2011 Census (ONS)

Household projections

ESE OA 2014: 4,399,000 2021: 4,741,000

https://www.gov.uk/government/statistical-data-sets/live-tables-on-

household-projections table 406

Tenure Breakdown

ESE OA Owned / Shared ownership 69% Social 14% Private rent or rent free 17%

2011 Census (ONS)

Number on LA waiting list

ESE OA April 2014: 256,935 https://www.gov.uk/government/statistical-data-sets/live-tables-on-rents-

lettings-and-tenancies table 600

Number of Housing Benefit Claimants

EAST SSR SE SSR

390,895 542,910

https://stat-

xplore.dwp.gov.uk/default.aspx July 2014

JSA claimant count, age 16-64 (Seasonally adjusted)

EAST SSR SE SSR

69,700 (1.9%) 82,800 (1.5%)

http://www.nomisweb.co.uk/ June 2014

% in public sector employment

EAST SSR SE SSR

15.3% 16.7%

http://www.ons.gov.uk/ons/rel/pse/public-sector-employment/q1-

2014/index.html table 6, Q1 2014

Gross Value Added (GVA) per head

EAST SSR SE SSR

19,658 22,221

2012:http://www.ons.gov.uk/ons/rel/

regional-accounts/regional-gross-value-added--income-approach-/december-2013/stb-regional-gva-2012.html

Number of local authorities

ESE OA 85 HCA

Number of LEPs ESE OA 8 HCA

Parliamentary party coverage

ESE OA

www.parliament.co.uk

Number of LSOAs in England’s 10% most deprived

ESE OA 161( 5% of the 10% most deprived LSOAs)

Indices of Multiple Deprivation 2010

HCA case studies

For local HCA case studies, click here: http://www.homesandcommunities.co.uk/casestudy-list

Homes and Communities Agency Strategic and Market Intelligence Team Fry Building 2 Marsham Street London SW1P 4DF [email protected]

Publication date: August 2014