eastern division united states securities and exchange commission · pdf file ·...

TRANSCRIPT

UNITED STATES DISTRICT COURTNORTHERN DISTRICT OF ILLINOIS

EASTERN DIVISION

UNITED STATES SECURITIES ANDEXCHANGE COMMISSION,

Plaintiff,

v.

ROBERT G. PEARSON and ILLINOISSTOCK TRANSFER COMPANY (d/b/a ISTSHAREHOLDER SERVICES),

Defendants.

Case No. 14 C 3785

Hon. Rebecca R. PallmeyerMagistrate Judge Young B. Kim

RECEIVER’S FIFTH QUARTERLY STATUS REPORTFOR THE PERIOD APRIL 1, 2015 THROUGH JUNE 30, 2015

Jill L. Nicholson, not individually but solely in her capacity as the court-appointed

receiver (the “Receiver”) for the estates of Illinois Stock Transfer Company d/b/a ist Shareholder

Services (the “Company”) and Robert G. Pearson (collectively, the “Receivership Estates”),

respectfully submits this Receiver’s Fifth Quarterly Status Report (the “Report”) covering the

period of April 1, 2015 through June 30, 2015 (the “Reporting Period”) pursuant to paragraph 54

of the Order Appointing Receiver entered on May 22, 2014 (the “Receiver Order”). For the

Court’s convenience, a Table of Contents is provided below.

TABLE OF CONTENTS

I. PROCEDURAL HISTORY................................................................................................ 2

II. SUMMARY OF ACTIONS TAKEN BY THE RECEIVER DURING THEREPORTING PERIOD....................................................................................................... 3

A. The Liquidation Plan............................................................................................... 3

B. Creditor Claims Proceedings .................................................................................. 4

1. The Claims Process..................................................................................... 4

Case: 1:14-cv-03785 Document #: 188 Filed: 07/28/15 Page 1 of 19 PageID #:1933

2

2. Status of Claims Determinations ................................................................ 6

III. ASSET RECOVERY........................................................................................................ 10

A. Accounts Receivable............................................................................................. 11

B. Insurance Policies ................................................................................................. 11

C. Turnover from Pearson ......................................................................................... 12

D. Liquidated and Unliquidated Claims .................................................................... 13

IV. FINANCIAL AFFAIRS.................................................................................................... 13

A. Overview............................................................................................................... 13

B. The Qualified Settlement Fund............................................................................. 14

C. Receiver’s BMO Bank Account ........................................................................... 15

D. Administrative Expenses ...................................................................................... 15

E. Estimated Liabilities ............................................................................................. 17

V. ADMINISTRATION OF THE RECEIVERSHIP ESTATES.......................................... 17

A. Estimated Distribution .......................................................................................... 17

B. Recommendations for the Continuation of the Receivership Estates ................... 18

I. PROCEDURAL HISTORY

On May 22, 2014, the United States Securities and Exchange Commission (the “SEC”)

commenced the above-captioned action (the “SEC Action”) against Pearson and the Company

(collectively, the “Receivership Defendants”) by filing a complaint (the “Complaint”) in the

United States District Court for the Northern District of Illinois (the “Court”). The SEC’s

Complaint alleges, inter alia, that Pearson and the Company commingled customer funds with

the Company’s funds and that Pearson and the Company misappropriated customer funds.

The SEC filed several ex parte motions with its Complaint on May 22, 2014, all of which

were granted by the Court. [Dkt Nos. 11-15]. In particular, subsequent to the filing of the

Case: 1:14-cv-03785 Document #: 188 Filed: 07/28/15 Page 2 of 19 PageID #:1934

3

Complaint, the Court entered a Temporary Restraining Order (the “TRO”), an Asset Freeze

Order (the “Asset Freeze Order”), and the Receiver Order on May 22, 2014. On July 9, 2014,

the Court entered a judgment (the “Judgment”) against Pearson with Pearson’s consent. The

Judgment (a) enjoins Pearson from violating federal securities laws; (b) requires Pearson to

disgorge ill-gotten gains and to pay pre-judgment interest in an amount to be determined by the

Court upon motion of the SEC; and (c) extends the Asset Freeze Order against Pearson until

further order of the Court. [Dkt. No. 56]. On July 9, 2014, the Court also entered an order

extending the TRO and the Asset Freeze against the Company until further order of the Court.

[Dkt. No. 56]. On December 19, 2014, the Court entered an order approving the Liquidation

Plan (defined herein) which, as more fully described below, governs the distributions of estate

assets to the various creditor constituencies. [Dkt. 130]. For a detailed description of the

functions provided by the Company in its capacity as a transfer agent, see the Receiver’s First

Quarterly Report. [Dkt. No. 65].

II. SUMMARY OF ACTIONS TAKEN BY THE RECEIVER DURING THEREPORTING PERIOD

A. The Liquidation Plan

The Receiver has been operating under the Amended Liquidation Plan (the “Liquidation

Plan”) which was approved by the District Court on December 19, 2014. During the period

covered by this Report, the Receiver has endeavored to marshal and to maximize assets for

distribution to those creditors with allowed claims (the “Allowed Claims”)1 against the

Receivership Estates. The Liquidation Plan has created two receivership estates for purposes of

distribution to claimants. The first estate (“Estate 1”) relates to assets and liabilities in

1 To the extent there may be differences between the description of the Liquidation Plan ordefinitions contained herein and the Liquidation Plan approved by the Court, the terms of the LiquidationPlan approved by the Court shall govern.

Case: 1:14-cv-03785 Document #: 188 Filed: 07/28/15 Page 3 of 19 PageID #:1935

4

connection with the Company while the second estate (“Estate 2,” and together with Estate 1, the

“Receivership Estates”) addresses assets and liabilities of Pearson personally. No funds related

to or generated by the Company (that is, Estate 1 funds) will be used to make distributions to

Pearson’s individual creditors (Estate 2 creditors). Under each of the estates are specific classes

of creditors (the “Classes”). The Liquidation Plan identifies the treatment for each Class of

claims. Note that claims in different Classes are treated differently. A detailed discussion

regarding the Classes of claims found for each estate can be found in both the Liquidation Plan

and the Receiver’s Third Quarterly Report filed on January 30, 2015 [Dkt No. 132].

B. Creditor Claims Proceedings

1. The Claims Process

Per the order entered on August 6, 2014 [Dkt. No. 66], the Court established September

30, 3014 at 5:00 p.m. CST as the deadline (the “Claims Bar Date”) by which claimants were

required to submit proofs of claim (“Proofs of Claim”) to KCC Class Action Services, LLC

(“KCC”), the Receiver’s claims agent. Subject to an order of the Court, any party who failed to

submit a Proof of Claim by the Claims Bar Date: (i) will not, with respect to any such claim, be

treated as holding an allowed claim against the Receivership Estates; (ii) will be forever barred,

estopped and enjoined from asserting any claim against the Receivership Estates; and (iii) will

not receive any distribution on account of such claim.

During the Reporting Period, the Receiver spent considerable time evaluating claims filed

against the Receivership Estates. As part of that process, each claim has been evaluated and will

either be deemed to be an Allowed Claim or Disallowed Claim as such terms are defined under

the Liquidation Plan. The Receiver is currently in the process of furnishing each claimant with

notice of the Receiver’s determination (the “Claim Determination”).

Case: 1:14-cv-03785 Document #: 188 Filed: 07/28/15 Page 4 of 19 PageID #:1936

5

Each claimant (including claimants holding allowed, disallowed, and/or partially

disallowed/allowed claims) will have 20 calendar days after the Claim Determination is mailed

to submit a written objection (the “Objection”) to the Receiver’s Claim Determination (the

“Objection Deadline”). Such Objection must actually be received by the Receiver on or before

the Objection Deadline at Illinois Stock Transfer Company & Robert G. Pearson Receivership,

P.O. Box 10352, Chicago, IL 60610. In the event the Objection is not received by the Objection

Deadline, the Receiver’s Claim Determination shall be deemed final. To date, the Receiver has

received ten (10) Objections.

If a claimant timely submits an Objection to the Receiver’s Claim Determination and the

Receiver determines that the claimant has satisfactorily cured all grounds for the Receiver’s

initial Claim Determination, the Receiver may issue a revised determination (the “Revised

Determination”) changing the status of the claim from disallowed to allowed. As in the case of

the original Claim Determination, each claimant will have 20 calendar days after the Revised

Determination is mailed to submit a written Objection to the Receiver’s Revised Determination.

This protocol was established to: (a) allow claimants to provide further information and

evidence to the Receiver they believe are essential to the adjudication of their claims; (b) provide

claimants with notice of the proper classes, if any, to which their claims have been assigned

under the Liquidation Plan; and (c) allow the parties to endeavor to reach a consensual resolution

without the need for the Court’s intervention in an effort to reduce the administrative burden

upon the Court.

As part of the claims process, the Receiver will continue to submit to the Court claims

determination motions (the “Claims Determination Motions”) on a rolling basis as claims are

reviewed by the Receiver. Each motion contains: (a) the name of the claimant; (b) the amount

Case: 1:14-cv-03785 Document #: 188 Filed: 07/28/15 Page 5 of 19 PageID #:1937

6

asserted by the claimant in its Proof of Claim; and (c) whether the Receiver has deemed the

claim as (i) allowed in its entirety, (ii) allowed in some respects and disallowed as to others, or

(iii) disallowed in its entirety. If the claim is not consensually resolved at the time of the filing of

the applicable Claims Determination Motion, the claimant may file a written objection with the

Court to the Claims Determination Motion (the “Claims Motion Objection”). Upon a claimant’s

filing of a Claims Motion Objection with the Court, the Court will determine the allowed amount

and proper classification of the claim (if any) by utilizing summary procedures to ensure the

expeditious administration of the claims process and the administration of the Receivership

Estates.

2. Status of Claims Determinations

The Receiver’s claims agent mailed a total of 1,599 claims packets to interested parties,

including issuers, shareholders, vendors, governmental authorities, employees, independent

contractors, and any other party that may have had a claim as revealed by the Company’s books

and records. The Receiver received 132 Proofs of Claim by the Claims Bar Date. The Court

also permitted one late-filed claim to be deemed timely filed, bringing the total number of claims

deemed timely filed to 132. Claims that were filed by the Claims Bar Date and were authorized

by the Court to be deemed timely filed aggregate $7,398,136.14. The following chart identifies

the total amount of timely filed claims by constituency.

Claim TypeNo. of Claims

ReceivedTotal Asserted

Amount of Claims

Employee or IndependentContractor

3$95,634.94

Governmental Authority 1 Unliquidated

Issuer 45 $3,734,389.90

Case: 1:14-cv-03785 Document #: 188 Filed: 07/28/15 Page 6 of 19 PageID #:1938

7

Shareholder 70 $2,727,091.72

Vendor/Trade 12 $472,269.58

Other 1 $368,750.00

TOTALS OF TIMELYCLAIMS

132 $7,398,136.14

It appears that certain claimants incorrectly categorized their claims. As such, the chart above

reflects the Receiver’s continued efforts to reclassify claims to their appropriate categories

identified on the Proof of Claim forms.

To date, the Receiver has issued Claim Determinations regarding 120 of the 132 claims.

Of these 120 Claim Determinations, 74 claims have been allowed by both the Receiver and the

District Court pursuant to the Receiver’s First, Second, and Third Claims Determination Motions

that were filed on March 30, 2015, April 23, 2015, and June 11, 2015. The total dollar amount

of claims allowed by both the Receiver and the Court pursuant to the Allowance Motions is

$3,369,773.32 The following chart sets forth the amount of Allowed Claims under each of the

Classes provided under the Liquidation Plan.

ESTATE 1 - IST

CLASS AMOUNT OF ALLOWED CLAIMS

Class I – Allowed Claims of Customers $3,297,307.23

Class II – Allowed Claims of Vendors $56,142.79

Class III – Allowed Claims of Employees $0.00

Class IV – Allowed Claims of GeneralCompany Claimants

$6,757.05

Case: 1:14-cv-03785 Document #: 188 Filed: 07/28/15 Page 7 of 19 PageID #:1939

8

ESTATE 2 - PEARSON

CLASS AMOUNT OF ALLOWED CLAIMS

Class I – Pearson General Claims $9,566.25

Claimants whose claims have been allowed by both the Receiver and the Court are deemed to

hold Allowed Claims and will be entitled to share in the pro rata distribution in their respective

Classes under the Liquidation Plan.

The Receiver has determined that an additional ten (10) claims are deemed allowed in

full, and seven (7) in part, and will be the subject of future Claims Determination Motions to be

filed with the District Court. These additional claims are not presently included in the totals

above, but will be added to the table once such claims have also been finally allowed by the

Court.

To date, the Receiver has issued 54 Claims Determinations2 disallowing claims in full or

in part.3 These claims were deemed disallowed for a variety of reasons, including, but not

limited to, failure to pay all outstanding amounts due and owing to the Company, failure to

provide necessary written documentation supporting a claim, duplicative claims, and/or

discrepancies between the claimant’s asserted claim and the books and records of the Company.

Of the 54 claims the Receiver initially deemed disallowed, the Receiver has received a total of

nine (9) Objections, as well as one (1) Objection to a notice allowing the claim in its entirety.

2 The Receiver has revised two of the previously disallowed claims to Allowed Claims. Thesetwo claims were disallowed due to the claimants’ failure to satisfy their Issuer AR obligations. Once theclaimants satisfied in full the Issuer AR, the claims were allowed.

3 Those claimants who received a Claims Determination notice indicating a partial disallowanceof a claim will also receive a notice indicating that the remaining portion of the claim is deemed allowedupon the expiration of the 20-day objection period (assuming no objection has been tendered to theReceiver).

Case: 1:14-cv-03785 Document #: 188 Filed: 07/28/15 Page 8 of 19 PageID #:1940

9

As required by the Receiver Order, the Receiver has previously submitted to chambers a

list of all known creditors with addresses and amounts of their claims as reflected by the

Company’s books and records in connection with the Receiver’s First Quarterly Report. In

connection with the current Report, the Receiver submits as Exhibit B a list of creditors who

have submitted claims with addressees and the amounts of their claims as reflected by KCC, the

court-appointed claims agent, as well as the status of the determination of such claims, i.e.,

whether such claims have been: (a) allowed in full by the Court and the Receiver and are final

allowed claims (“Final Allowed Claims”); (b) allowed in full by the Receiver and awaiting the

filing of a Claims Determination Motion (“Pending Allowed Claims”); (c) disallowed in full by

the Court and the Receiver (“Final Disallowed Claims”); (d) disallowed in full by the Receiver

and awaiting the filing of a Claims Determination Motion (“Pending Disallowed Claims”); (e)

allowed in part and disallowed in part by the Court and the Receiver (“Final Partially

Disallowed/Allowed Claims”); (f) allowed in part and disallowed in part by the Receiver and

awaiting the filing of a Claims Determination Motion (“Pending Partially Disallowed/Allowed

Claims”); (g) allowed or disallowed, in their entirety or in part, and for which the Receiver has

received a timely objection (the “Disputed Claims”); or (h) claimants to whom a Claims

Determination Letter has yet to be sent (“Remaining Claims”). This list includes those claimants

who have submitted claims after the Claims Bar Date. Those who have failed to submit Timely

Claims have been identified in Exhibit B.

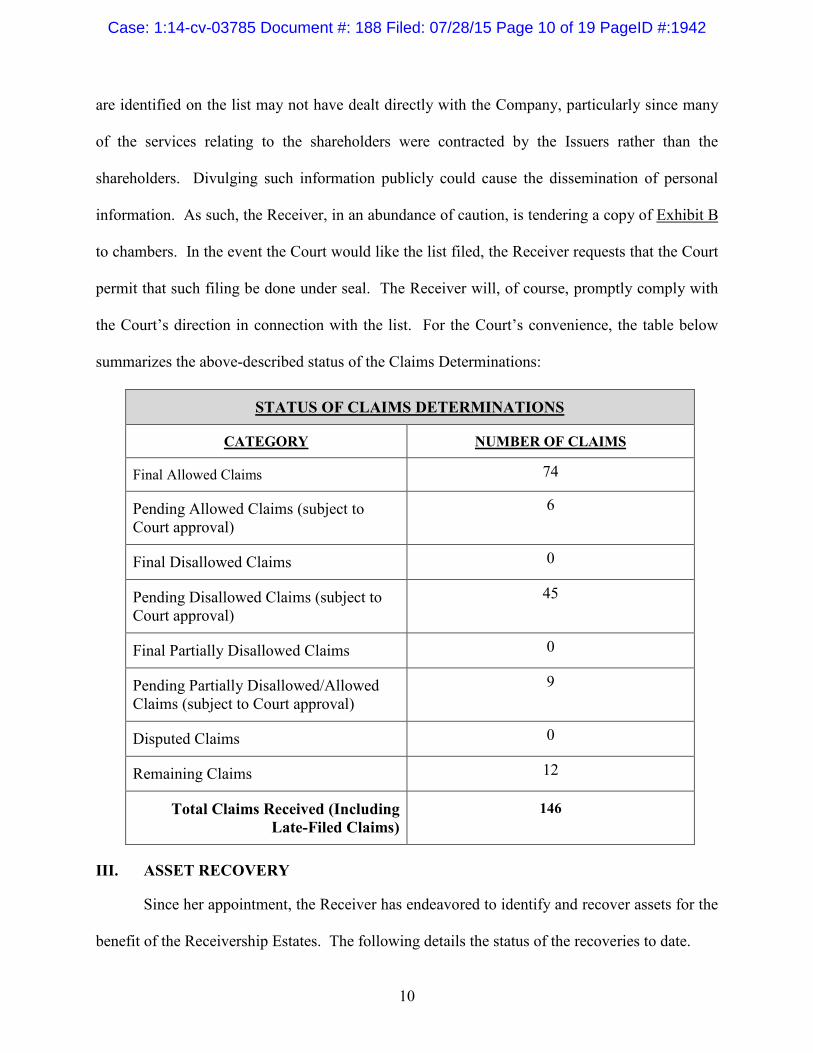

The Receiver has not publicly filed Exhibit B as it includes personal details such as

names, addresses, and claim amounts of shareholders. Unlike a typical receivership case, where

shareholders may have dealt directly with and/or contracted with a receivership defendant, a

transfer agent situation presents a unique and novel scenario. Certain of the shareholders who

Case: 1:14-cv-03785 Document #: 188 Filed: 07/28/15 Page 9 of 19 PageID #:1941

10

are identified on the list may not have dealt directly with the Company, particularly since many

of the services relating to the shareholders were contracted by the Issuers rather than the

shareholders. Divulging such information publicly could cause the dissemination of personal

information. As such, the Receiver, in an abundance of caution, is tendering a copy of Exhibit B

to chambers. In the event the Court would like the list filed, the Receiver requests that the Court

permit that such filing be done under seal. The Receiver will, of course, promptly comply with

the Court’s direction in connection with the list. For the Court’s convenience, the table below

summarizes the above-described status of the Claims Determinations:

STATUS OF CLAIMS DETERMINATIONS

CATEGORY NUMBER OF CLAIMS

Final Allowed Claims 74

Pending Allowed Claims (subject toCourt approval)

6

Final Disallowed Claims 0

Pending Disallowed Claims (subject toCourt approval)

45

Final Partially Disallowed Claims 0

Pending Partially Disallowed/AllowedClaims (subject to Court approval)

9

Disputed Claims 0

Remaining Claims 12

Total Claims Received (IncludingLate-Filed Claims)

146

III. ASSET RECOVERY

Since her appointment, the Receiver has endeavored to identify and recover assets for the

benefit of the Receivership Estates. The following details the status of the recoveries to date.

Case: 1:14-cv-03785 Document #: 188 Filed: 07/28/15 Page 10 of 19 PageID #:1942

11

For the Court’s convenience, an inventory of all assets recovered by the Receiver to date

and their related disposition is included in Exhibit C.

A. Accounts Receivable

Prior to the closure of the Company on July 8, 2014, the Receiver directed the Company

to generate invoices to all customers for all outstanding amounts due and owing to the Company

(the “Issuer AR”). A total of $194,009.21 in Issuer AR invoices were sent by the Receiver. To

date and as a result of the Receiver’s ongoing and continued efforts, the Receiver has collected

$162,050.79 of this amount, leaving $31,958.42 (or 16.47% of the total Issuer AR) to be

collected as of July 20, 2015. The Receiver has sent several demand letters to those issuers with

remaining Issuer AR and sent final demand letters on July 1, 2015 setting forth a final payment

deadline of July 15, 2015.

The vast majority of issuers have satisfied their obligations. In fact, three issuers account

for the majority of the outstanding Issuer AR. Collectively, these three issuers owe $22,389.81

(or 70%) of the remaining $31,958.42 Issuer AR. Of this amount, Cortland Bank presently owes

$12,394.51. These three issuers and the other remaining issuers with outstanding Issuer AR did

not file claims against the receivership estates. As a result, the Receiver was unable to utilize the

provisions of the Liquidation Plan which disallowed any claims against the estates by issuers

with outstanding Issuer AR. (Liquidation Plan, §§ 1.02, 2.09, 2.10). Given the recalcitrance of

these certain issuers, the Receiver is exploring mechanisms to enforce recovery, including the

commencement of litigation.

B. Insurance Policies

As of the commencement of the receivership, the Company had in place certain insurance

policies, including an errors and omissions (“E&O”) policy with coverage of $1 million. The

E&O carrier denied coverage on July 16, 2014. After a careful review of the policy terms and

Case: 1:14-cv-03785 Document #: 188 Filed: 07/28/15 Page 11 of 19 PageID #:1943

12

the E&O denial letter and in consultation with her special counsel, the Receiver will not be

pursuing coverage under the E&O policy.

In addition to the E&O policy, the Company also maintained coverage under two fidelity

bond policies, each with a coverage limit of $5 million. Coverage under the second policy is

triggered only when the $5 million policy limit is exhausted under the first policy. On August

28, 2014, the Receiver filed Proofs of Loss with both fidelity bond carriers. One of the fidelity

bond carriers has notified the Receiver that it has rescinded its fidelity bond policy. The

Receiver is currently exploring her options in connection with the policy and the fidelity carrier’s

alleged assertion of rescission.

C. Turnover from Pearson

On May 28, 2015, the Receiver filed the Receiver's Motion Regarding Turnover of

Assets of Robert G. Pearson, which was granted in part and denied in part on June 15, 2015. As

of July 20, 2015, the Receiver has collected the following from Robert Pearson. Note that the

funds identified below with an asterisk have posted after July 20, 2015 and will be included as

funds received on the Receiver’s Sixth Quarterly Status Report.

ASSET AMOUNT COLLECTED

50% Interest In Sale ofWheaton Building

$95,702.74

*100% Morgan Stanley IRA(awaiting receipt of check)

$206,803.00

Mass Mutual Life InsurancePolicies Liquidation Value (3policies)

$32,387.64

*50% Morgan Stanley JointAccount

$24,151.22

Sale of Personal Stocks &Related Dividends

$5,729.32

Bank Accounts – Fifth Third $2,935.57

Case: 1:14-cv-03785 Document #: 188 Filed: 07/28/15 Page 12 of 19 PageID #:1944

13

* From Fifth Third BankAccounts

$8,000.00

TOTAL $375,709.49

The Receiver is expecting an approximately additional $900.00 from Fifth Third Bank. Note

that the Receiver has reserved all rights to pursue additional funds from Pearson by seeking

further turnover orders from the Court.

D. Liquidated and Unliquidated Claims

The Receiver must first consult with the SEC regarding any litigation that may be

commenced pursuant to the terms of the Receiver Order. The Receiver has not currently

initiated any litigation against third parties. However, the Receiver has issued a demand letter

with respect to the Company’s auditor and will be carefully evaluating her next steps based on

information recently tendered by the Company’s auditor in response to the Receiver’s demand

letter. The Receiver has been in settlement negotiations with the auditor, but an acceptable

settlement has not been reached to date. The Receiver is also contemplating a possible action

against Carol Pearson.

Once the Receiver commences litigation against any third parties, the Receiver will

supplement any subsequent status reports with information relating to those actions, including

the need for forensic and/or investigatory resources, the approximate valuation of claims, and the

anticipated or proposed methods of enforcing such claims.

IV. FINANCIAL AFFAIRS

A. Overview

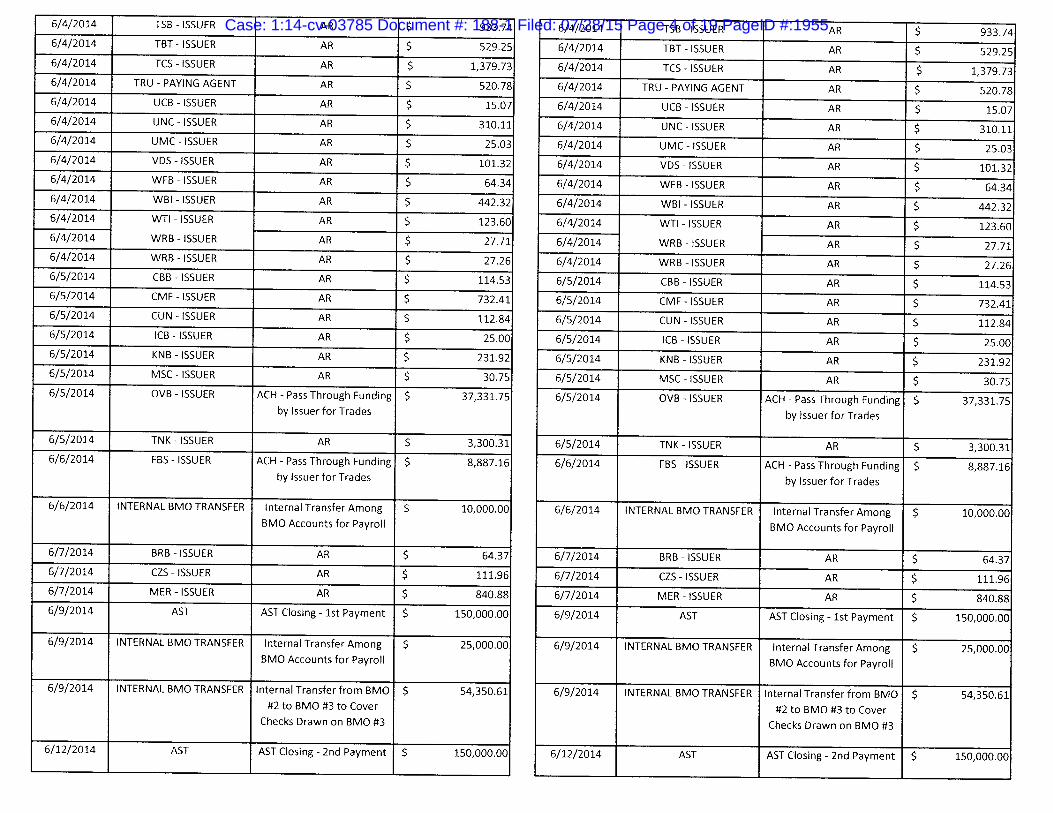

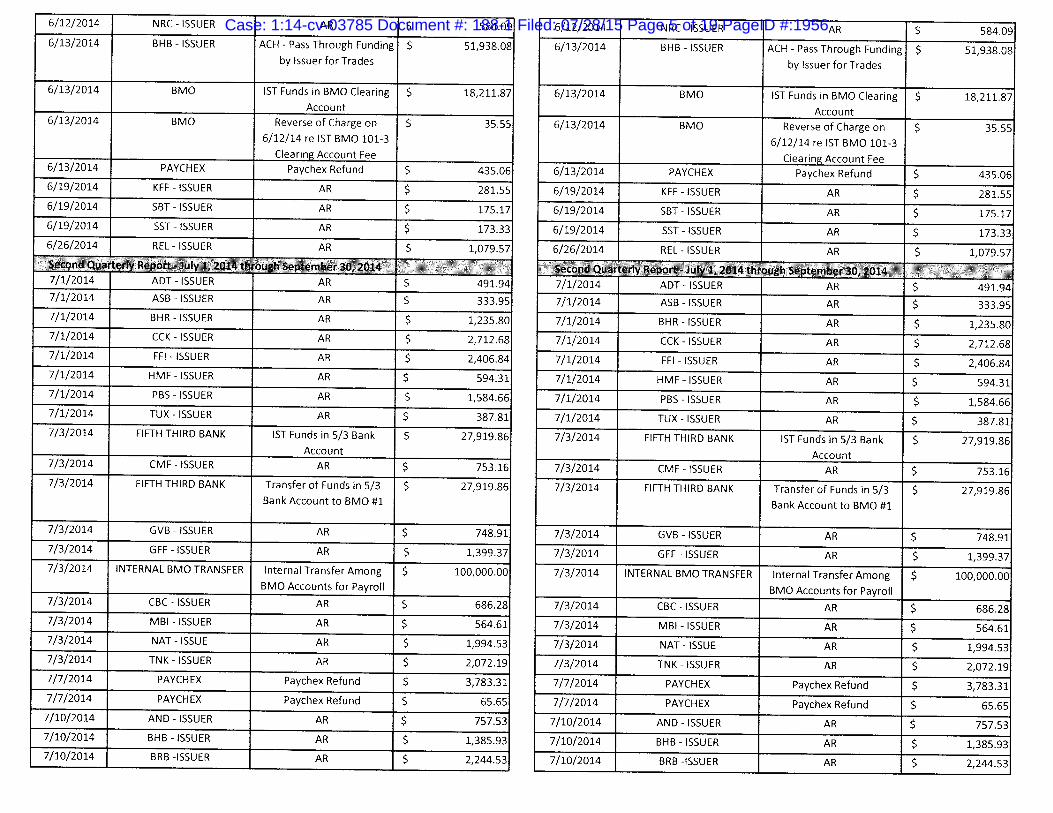

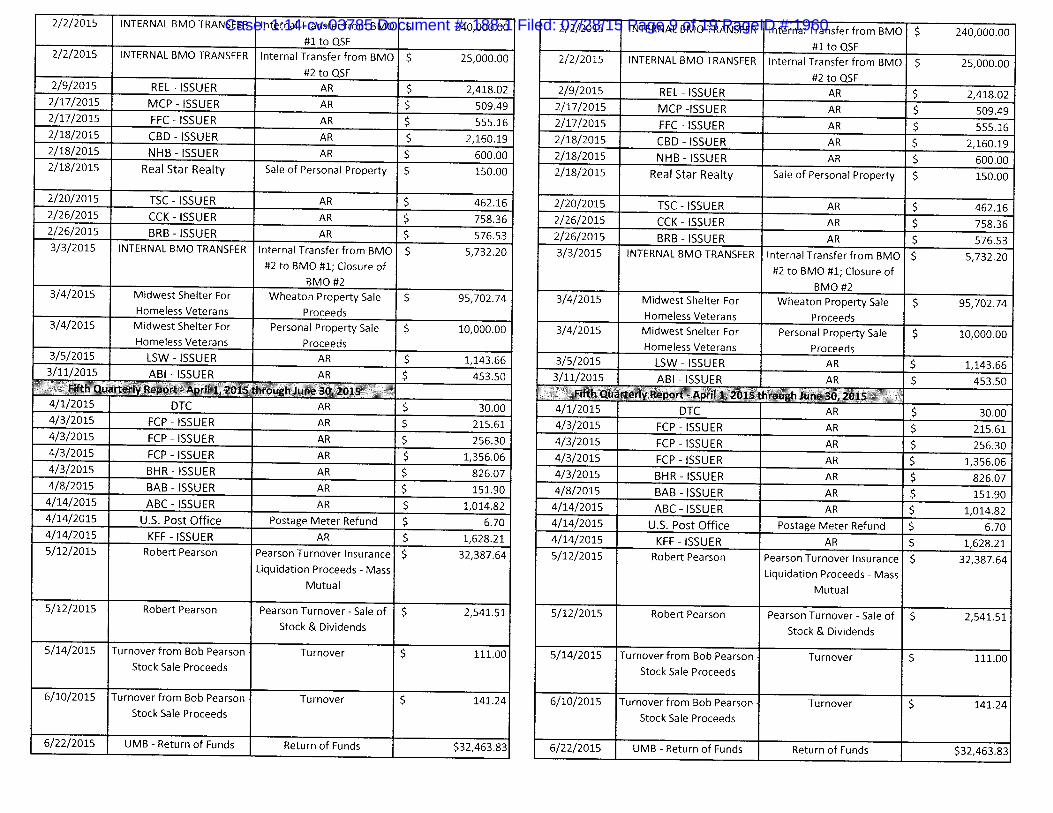

Attached hereto as Exhibit A, as noted by the Receiver Order, are schedules of income

Case: 1:14-cv-03785 Document #: 188 Filed: 07/28/15 Page 13 of 19 PageID #:1945

14

and expenses.4 As of July 20, 2015 the Receiver is holding $4,911,600.31. These funds are held

in: (a) a qualified settlement fund account and (b) one receiver’s account at BMO as detailed

below. Note that the $4,916,600.31 is after the deduction of administrative expenses that have

been paid in the amount of $1,323,050.46 as itemized below. For the Court’s convenience, a

schedule of all of the Company’s assets located to date is attached hereto as Exhibit C.

B. The Qualified Settlement Fund

The Receiver has worked with the Receiver’s claims agent KCC to establish a Qualified

Settlement Fund (“QSF”), which maintains a separate and independent tax identification number

from the Company. There are two sub-accounts held in connection with the QSF: (1) an account

related to the Company’s assets and (2) an account related to Pearson’s assets. As of July 20,

2015, the QSF’s Company account holds $4,874,576.55, which is comprised of funds removed

from the Company’s accounts, funds generated by the sale of assets to AST, funds transferred

from bank accounts opened by the Receiver at the inception of the receivership, funds generated

by the sale of the Wheaton Property, and collected Issuer AR. As of July 20, 2015, the QSF’s

Pearson sub-account holds $5,000.00. The Pearson sub-account will never hold more than

$5,000.00 as the Liquidation Plan provides that the total amount that may be paid to Pearson’s

individual creditors is capped at $5,000.00. (Liquidation Plan, §§ 1.02 and 2.04).

4 Note that the names of employees on the schedule of expenses have been redacted to avoiddissemination of employees’ salary and/or wage information. In addition, the amount of the ASTmilestone payments have been redacted. The Receiver will be glad to provide an unredacted copy ofthese schedules to chambers upon the Court’s request.

Also note that the income and expense ledgers of Exhibit A include transfers among variousReceiver accounts. By way of example, on July 25, 2014, the Receiver transferred $5 million from theReceiver’s BMO account to the receivership’s Qualified Settlement Fund Account as a result of theShutdown of the Company. Such transfers are not expenses of the estates, but are identified solely for thepurpose of demonstrating to the Court the movement of funds among the receivership accounts.

Case: 1:14-cv-03785 Document #: 188 Filed: 07/28/15 Page 14 of 19 PageID #:1946

15

C. Receiver’s BMO Bank Account

The Receiver has closed all bank and brokerage accounts with the exception of the BMO

bank account below. As of July 20, 2015, the following bank accounts had the following

amounts:

BANK ACCOUNT NO. AMOUNT IN ACCOUNT STATUS

BMO Harris(Receiver’s Account)

***538 $37,023.76 Account Open

The Receiver is currently utilizing the BMO bank account for the payment of certain small

invoices, including fees incurred related to monthly storage of records at Iron Mountain during

the pendency of the receivership.

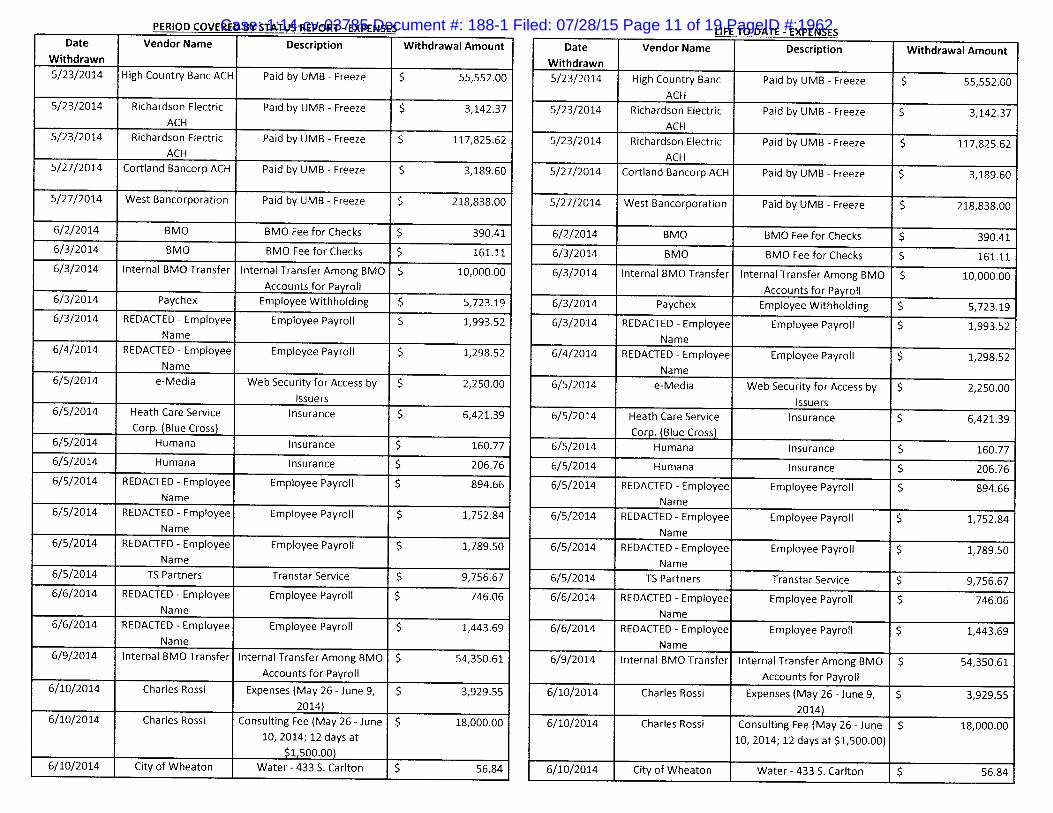

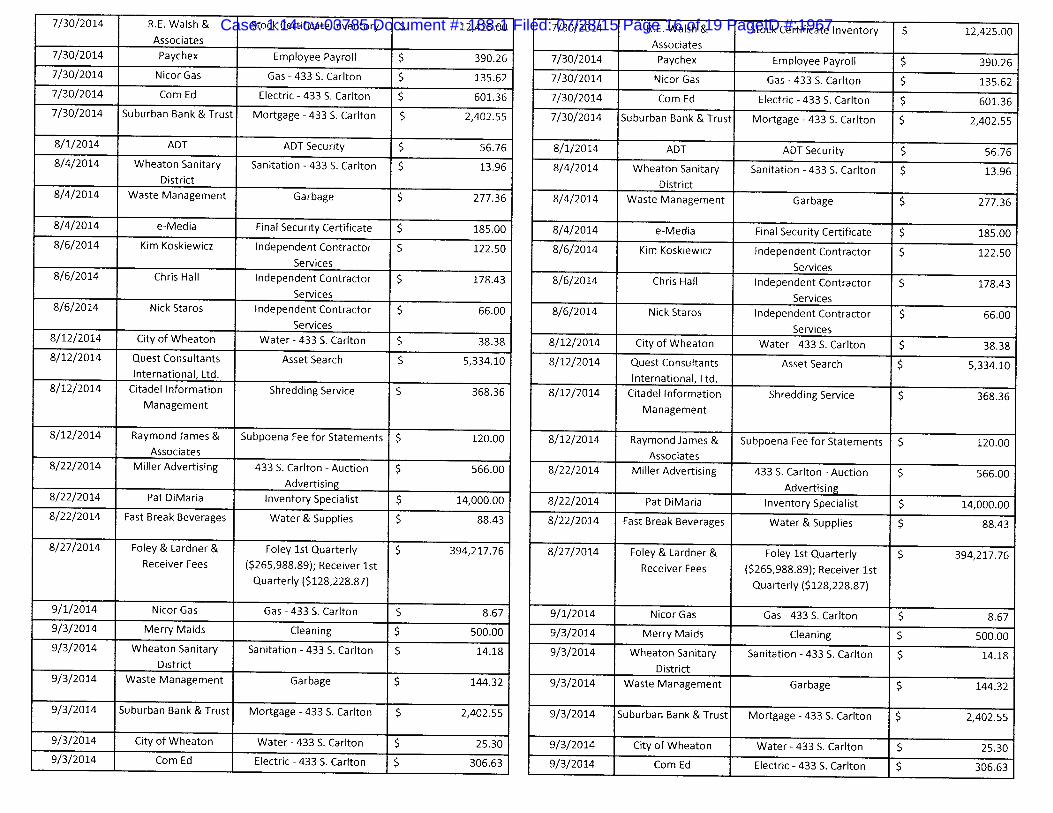

D. Administrative Expenses

The amount of administrative expenses paid through July 20, 2015 is $1,323,050.46. For

the Court’s convenience, the following chart summarizes the nature of the administrative

expenses:

Type of Expenditure Amount

Administration Fees (Wall Street JournalPublications Fees, Bank Fees, Stop Payment byIssuers, Asset Searches, Filing Fees, etc.)

$21,281.78

Building Expenses (Sanitation, Water, Gas,Electric, Taxes, Mortgage, etc.)

$21,920.41

Business Expenses (Postage, Phone, Internet,Document Destruction, IndependentContracting Services, etc.)

$12,771.99

Court-Appointed Professionals (Rossi;Teamwerks; DiMaria; R.E. Walsh &Associates; Foley & Lardner; Receiver; ShawFishman; Financial Advisors, LLC, etc.)

$1,025,018.72

Employee Related Expenses (Payroll,Withholding, Paychex Processing etc.)

$121,759.39

Insurance (Medical, E&O, Property, etc.) $33,791.50

Transtar Deconversion Fees $86,006.67

Case: 1:14-cv-03785 Document #: 188 Filed: 07/28/15 Page 15 of 19 PageID #:1947

16

Taxes (Tax Related Notices, etc.) $500.00

QSF (Claims Agent & QSF AdministrativeFees)

$20,627.17

TOTAL $1,343,677.63

The aforementioned amounts include all of the administrative expenses necessary to

administer the estates, including, inter alia, overhead related to the operation of the Company;

securing the Company’s offices, records, and electronic data; reconciliation of accounts and

assets held by the Company; evaluation and processing of transactions during the interim period

after the commencement of the receivership and prior to the Company’s Shutdown; employee

payroll taxes; health insurance; property insurance; casualty insurance; utilities; bank charges;

out of pocket expenses in connection with postage, copying, and travel for Issuer transactions

and shareholder meetings; deconversion fees associated with the transfer of records to successor

transfer agents through the Transtar system; professional fees related to the inventorying of the

Company’s extensive hard-copy records; the use of former FBI agents to inventory the contents

of the Company’s vault; the marketing, negotiation and successful sale of the Company’s

customer accounts; recovery of assets such as bank accounts, accounts receivable, and vehicles

for the benefit of the receivership; attendance at hearings before the Court; preparation of

quarterly reports as directed by the Receiver Order; the transition of Issuers to new platforms;

creation and implementation of the claims solicitation process and procedure; fielding hundreds

of Issuer, shareholder, and creditor inquiries; and establishment of the QSF, to name a few.

Note that the fees and costs incurred by the Receiver and her counsel during the fifth

quarterly fee application period have not been included in the aforementioned amount as such

amounts are subject to fee applications to be reviewed and approved by the Court.

Case: 1:14-cv-03785 Document #: 188 Filed: 07/28/15 Page 16 of 19 PageID #:1948

17

E. Estimated Liabilities

As noted below, the total timely filed claims asserted against the Company is

$7,398,136.14 plus an additional unliquidated claim asserted by the Illinois Department of

Employment Security. This amount does not take into consideration any claims that may be

disallowed by the Receiver as part of the claims reconciliation process. In addition, this number

does not include the ongoing costs of administration of the estates, which includes ongoing

storage fees related to the Company’s documents, fees and costs that will be incurred by the

Receiver and professionals and consultants retained by the Receiver, and other expenditures that

may be necessary in connection with the administration of the estates.

V. ADMINISTRATION OF THE RECEIVERSHIP ESTATES

A. Estimated Distribution

As of the date of the filing of this Report, the assets the Company held are less than the

total amount of Timely Claims. The same is true with respect to Timely Claims against Pearson.

Note, however, that while certain claims may be timely filed, such claims still may be disallowed

in connection with the claims resolution process. As such, it is necessarily true that the more

Timely Claims that are deemed Allowed Claims, the lower the percentage of recovery will be to

claimants with Allowed Claims. Conversely, if the Receiver obtains material recoveries for the

estates in the future, the percentage of recovery will increase. However, as it currently stands,

total liabilities exceed the funds in the Receiver’s possession. Absent additional recoveries from

various third parties, claimants can currently expect less than a 100% distribution.

On July 21, 2015, the Receiver directed KCC to make an initial interim distribution of

25% from the QSF to claimants in Class I of the Liquidation Plan with Allowed Claims (that is,

customers of IST including issuers and their respective shareholders). In order to process such

distributions, KCC requires receipt of W-9s from each of the claimants for purposes of accurate

Case: 1:14-cv-03785 Document #: 188 Filed: 07/28/15 Page 17 of 19 PageID #:1949

18

tax accounting. To date, the Receiver has not received W-9s from approximately 13 claimants

with Allowed Claims in Class I. The Receiver will continue to request these W-9s and upon

their receipt will advise KCC to release the 25% interim distribution to those claimants with

Allowed Claims in Class I.

The Receiver is also calculating the distributions to those with Allowed Claims in Classes

II and III of the Liquidation Plan. Class II Allowed Claims are subject to a maximum

distribution of $25,000 pursuant to the Vendor Carve Out of the Liquidation Plan, and Class III

Allowed Claims are subject to a maximum distribution of $5,000 under the Employee Carve Out

of the Liquidation Plan. Class II Allowed Claims will share pro rata in the $5,000. Similarly,

Class III Allowed Claims will share pro rata in the $25,000. Distributions to Classes II and III

will be made when each of the claims in those classes have been fully and finally adjudicated.

The Receiver estimates that process to conclude within the next two months with a distribution

to Class II and III expected in the fall of 2015.

B. Recommendations for the Continuation of the Receivership Estates

The Receiver notes that the continuation of the Receivership Estates is necessary and

warranted at this time in order to move forward with the administration of claims and the

recovery of assets under the Liquidation Plan. The Receiver will continue to assess and

investigate possible avenues of recovery for the benefit of the Receivership Estates. The

Receiver will also continue to apprize the Court of any developments through ongoing quarterly

status reports and is glad to furnish interim updates at status hearings that may be set by the

Court.

/s/ Jill L. NicholsonNot individually, but solely as Receiver forthe Estates of Illinois Stock TransferCompany and Robert G. PearsonFoley & Lardner LLP

Case: 1:14-cv-03785 Document #: 188 Filed: 07/28/15 Page 18 of 19 PageID #:1950

19

321 North Clark Street, Suite 2800Chicago, IL 60654Ph: (312) 832-4500Fax: (312) 832-4700

Case: 1:14-cv-03785 Document #: 188 Filed: 07/28/15 Page 19 of 19 PageID #:1951

EXHIBIT A

Case: 1:14-cv-03785 Document #: 188-1 Filed: 07/28/15 Page 1 of 19 PageID #:1952

Case: 1:14-cv-03785 Document #: 188-1 Filed: 07/28/15 Page 2 of 19 PageID #:1953

Case: 1:14-cv-03785 Document #: 188-1 Filed: 07/28/15 Page 3 of 19 PageID #:1954

Case: 1:14-cv-03785 Document #: 188-1 Filed: 07/28/15 Page 4 of 19 PageID #:1955

Case: 1:14-cv-03785 Document #: 188-1 Filed: 07/28/15 Page 5 of 19 PageID #:1956

Case: 1:14-cv-03785 Document #: 188-1 Filed: 07/28/15 Page 6 of 19 PageID #:1957

Case: 1:14-cv-03785 Document #: 188-1 Filed: 07/28/15 Page 7 of 19 PageID #:1958

Case: 1:14-cv-03785 Document #: 188-1 Filed: 07/28/15 Page 8 of 19 PageID #:1959

Case: 1:14-cv-03785 Document #: 188-1 Filed: 07/28/15 Page 9 of 19 PageID #:1960

Case: 1:14-cv-03785 Document #: 188-1 Filed: 07/28/15 Page 10 of 19 PageID #:1961

Case: 1:14-cv-03785 Document #: 188-1 Filed: 07/28/15 Page 11 of 19 PageID #:1962

Case: 1:14-cv-03785 Document #: 188-1 Filed: 07/28/15 Page 12 of 19 PageID #:1963

Case: 1:14-cv-03785 Document #: 188-1 Filed: 07/28/15 Page 13 of 19 PageID #:1964

Case: 1:14-cv-03785 Document #: 188-1 Filed: 07/28/15 Page 14 of 19 PageID #:1965

Case: 1:14-cv-03785 Document #: 188-1 Filed: 07/28/15 Page 15 of 19 PageID #:1966

Case: 1:14-cv-03785 Document #: 188-1 Filed: 07/28/15 Page 16 of 19 PageID #:1967

Case: 1:14-cv-03785 Document #: 188-1 Filed: 07/28/15 Page 17 of 19 PageID #:1968

Case: 1:14-cv-03785 Document #: 188-1 Filed: 07/28/15 Page 18 of 19 PageID #:1969

Case: 1:14-cv-03785 Document #: 188-1 Filed: 07/28/15 Page 19 of 19 PageID #:1970

EXHIBIT B

SUBMITTED DIRECTLY TO CHAMBERS

Case: 1:14-cv-03785 Document #: 188-2 Filed: 07/28/15 Page 1 of 1 PageID #:1971

EXHIBIT C

Case: 1:14-cv-03785 Document #: 188-3 Filed: 07/28/15 Page 1 of 7 PageID #:1972

Case: 1:14-cv-03785 Document #: 188-3 Filed: 07/28/15 Page 2 of 7 PageID #:1973

Case: 1:14-cv-03785 Document #: 188-3 Filed: 07/28/15 Page 3 of 7 PageID #:1974

Case: 1:14-cv-03785 Document #: 188-3 Filed: 07/28/15 Page 4 of 7 PageID #:1975

Case: 1:14-cv-03785 Document #: 188-3 Filed: 07/28/15 Page 5 of 7 PageID #:1976

Case: 1:14-cv-03785 Document #: 188-3 Filed: 07/28/15 Page 6 of 7 PageID #:1977

Case: 1:14-cv-03785 Document #: 188-3 Filed: 07/28/15 Page 7 of 7 PageID #:1978