eccho insights 0411(6).pdf · eccho insights what’s a rule 8 ... –“where the loss has fallen,...

TRANSCRIPT

ECCHO Insights

What’s a Rule 8…What’s a Rule 9

Kevin Cranford

Vice President

BB &T

Phyllis Meyerson

Executive Vice President

ECCHO

Ap

ril 1

5,

2011

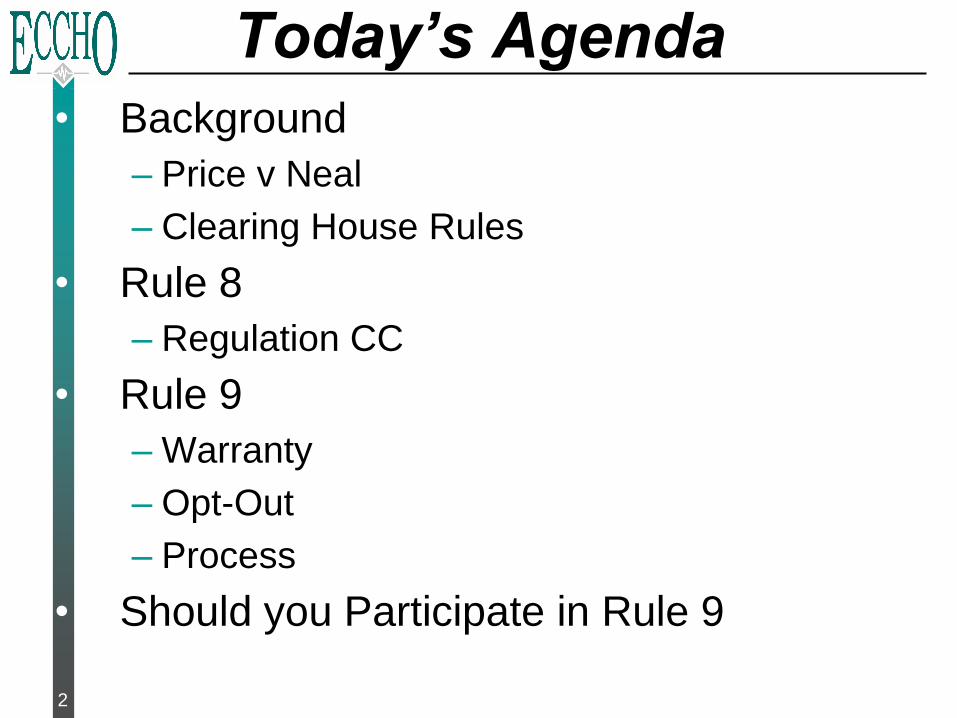

Today’s Agenda

• Background

– Price v Neal

– Clearing House Rules

• Rule 8

– Regulation CC

• Rule 9

– Warranty

– Opt-Out

– Process

• Should you Participate in Rule 9

2

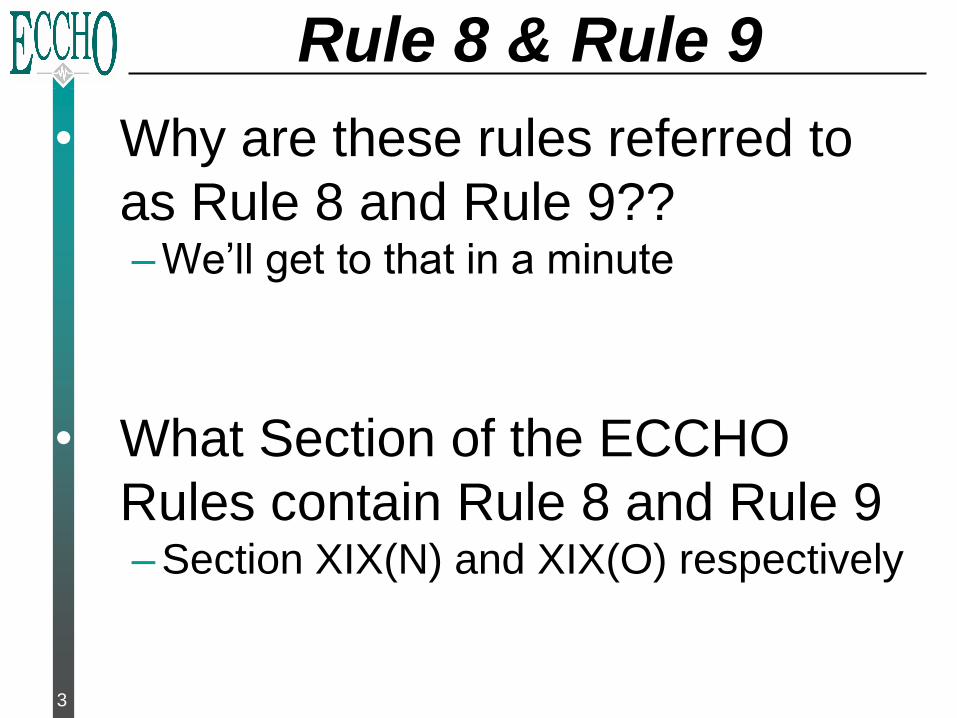

• Why are these rules referred to

as Rule 8 and Rule 9??– We’ll get to that in a minute

• What Section of the ECCHO

Rules contain Rule 8 and Rule 9– Section XIX(N) and XIX(O) respectively

3

Rule 8 & Rule 9

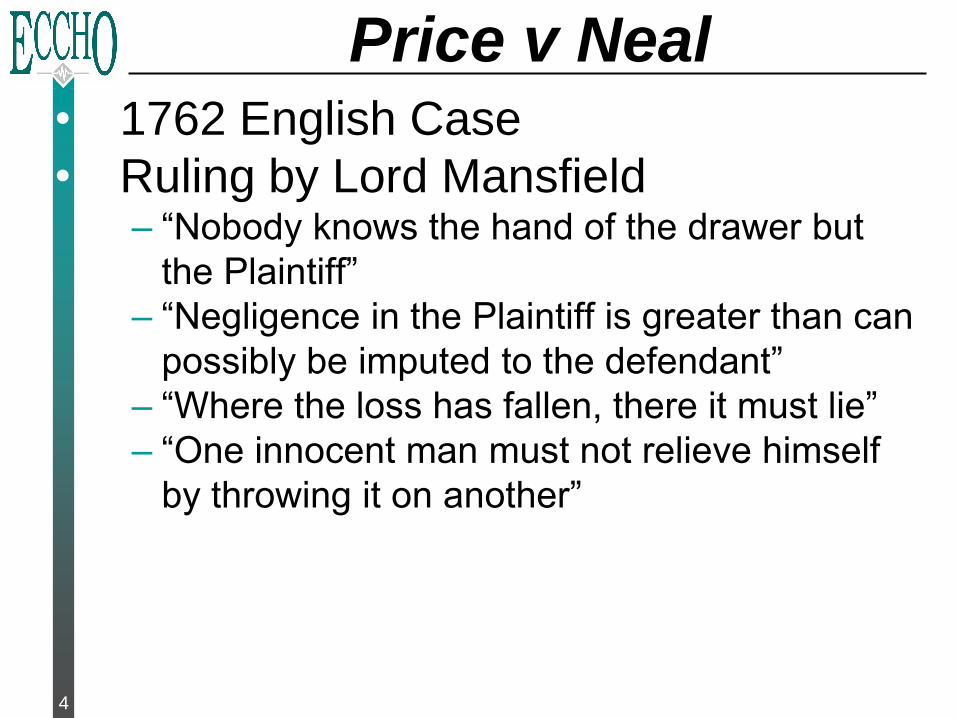

• 1762 English Case

• Ruling by Lord Mansfield– “Nobody knows the hand of the drawer but

the Plaintiff”

– “Negligence in the Plaintiff is greater than can

possibly be imputed to the defendant”

– “Where the loss has fallen, there it must lie”

– “One innocent man must not relieve himself

by throwing it on another”

4

Price v Neal

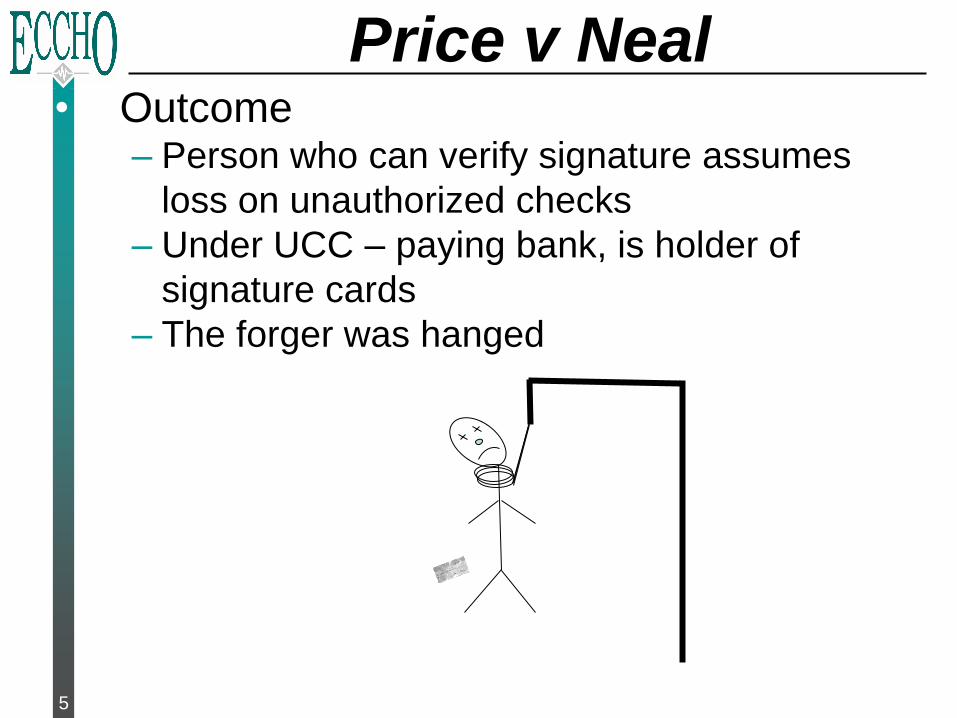

• Outcome– Person who can verify signature assumes

loss on unauthorized checks

– Under UCC – paying bank, is holder of

signature cards

– The forger was hanged

5

Price v Neal

• Depositor – Strong Incentives to take

check– Merchant in best position to verify

identification

• UCC creates risk free transaction if

forged signature since risk is

transferred to paying bank

• Depositor recoups costs, makes profit

• Depositor decision cause paying

bank losses

6

Why “Need” for Rule

• As Law – Does not reflect how society’s

payments systems operates

• Unnecessarily exposes banks (as paying

bank) to fraud losses

• Best defender is party who give value

• Underlying justification for Price v Neal is

essentially obsolete

• Fraud controls in 1762 England– Eyewitness identification

– Signature verification

– Extreme punishment

– No photo ID’s

– No thumbprint signature7

Relevance of Old Law

• Modern Check Processing– MICR encoding checks serve as carrier of

electronic data• Image only furthered electronification of check

– Subsequent to BOFD, checks rarely touched by

human hand • No human eye examines written information

– Minimum signature verification

• Signature verification has been made defunct – New technologies

• MICR

• Image

– Volume demands of business commerce

– Definition of Ordinary Care in 1990 version of UCC• “..does not require a bank to examine an instrument..”

Current Processing

8

BOFD

Intermediary/

Collecting

BankPaying Bank

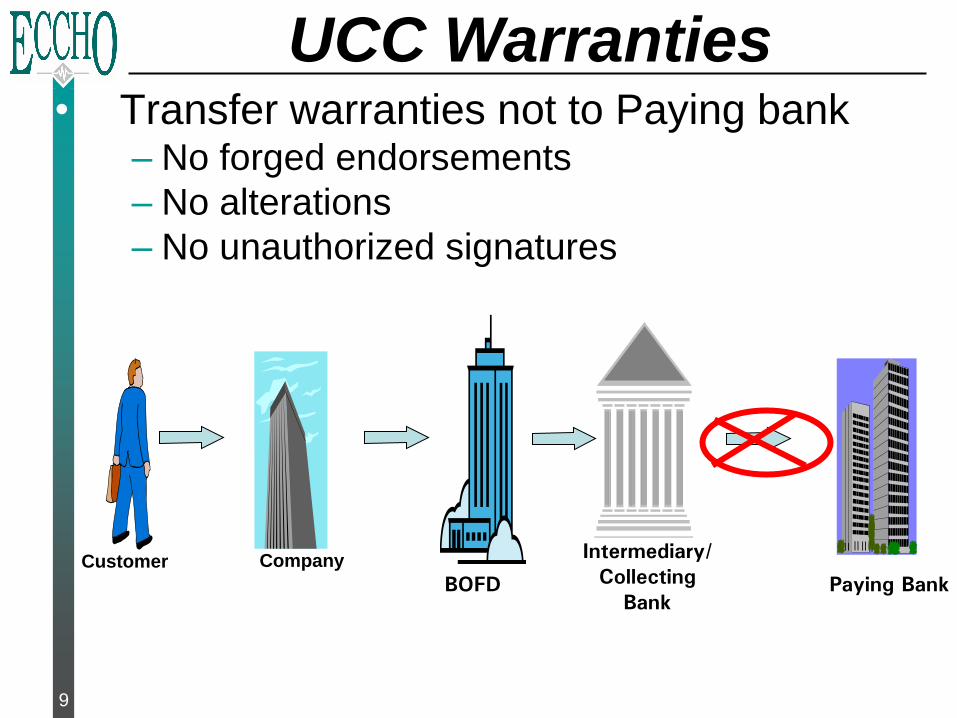

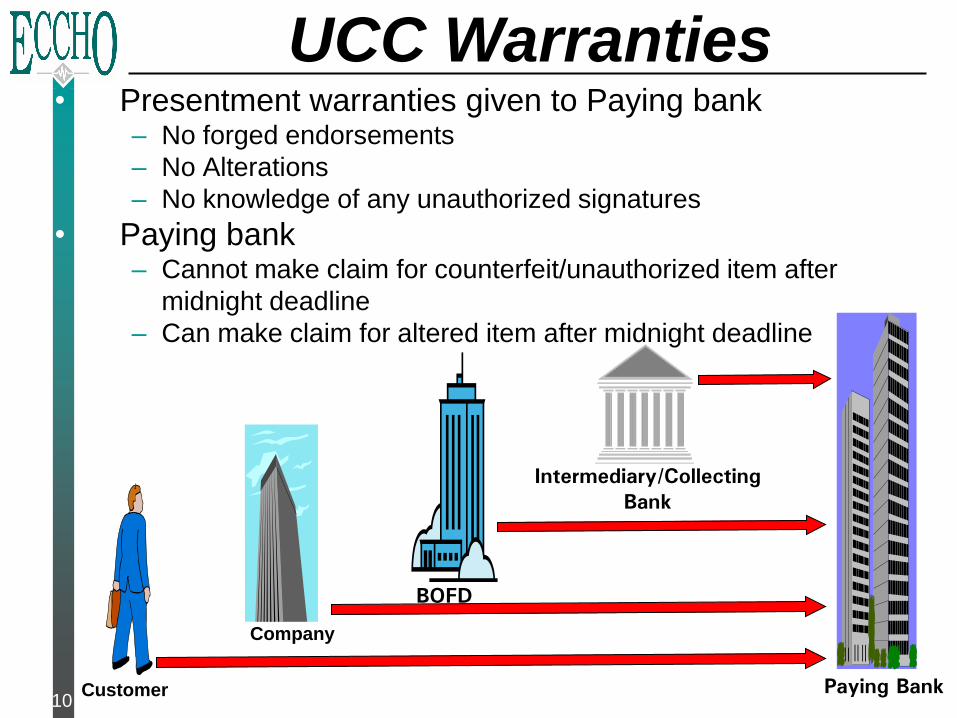

UCC Warranties

CompanyCustomer

• Transfer warranties not to Paying bank– No forged endorsements

– No alterations

– No unauthorized signatures

9

BOFD

Intermediary/Collecting

Bank

Paying Bank

UCC Warranties

Company

Customer

• Presentment warranties given to Paying bank– No forged endorsements

– No Alterations

– No knowledge of any unauthorized signatures

• Paying bank– Cannot make claim for counterfeit/unauthorized item after

midnight deadline

– Can make claim for altered item after midnight deadline

10

• Fraud personnel worked within clearing

houses to move risk– Attempted to move risk outside banking

industry

• Clearing House rules can vary UCC

• In mid 1990’s California paper clearing

house– Developed rules for unauthorized unsigned

draft (Rule 8)

– Developed claim process that mirrored ACH

– Worked with state legislator to modify UCC

11

Clearing House Rules

• Texas through its clearing house developed

similar rule for signed items (Rule 9)

• Rule 8 & 9 were implemented in clearing

houses all over the country– Eventually included in National Uniform Paper

Rules

– Incorporated in ECCHO rules for image

exchange

12

Clearing House Rules

• Remotely Created Checks

• Initially included in clearing house rules

• During RFC on Check 21 changes to Reg

CC Fed requested input on including RCC

warranty in Reg– Industry extremely supportive

– Updated Reg CC for RCC 2006

• Regulation CC– Definition of Remotely Created Check

• Check that is not created by paying bank and that

does not bear signature applied or purported to be

applied, by person on whose account check is drawn

13

Rule 8

IMAGE

BOFD Intermediary Bank

IMAGE

Unsigned Draft

Deposit

Paying BankCompany

Unsigned

Draft

Bill Pay

RCC Warranty Claim

Unauthorized

1

2

3 3 3

4

5

Consumer

Customer

Rule 8• Definition of RCC does not include

– Check created by paying bank (e.g. bill payment

service)

14

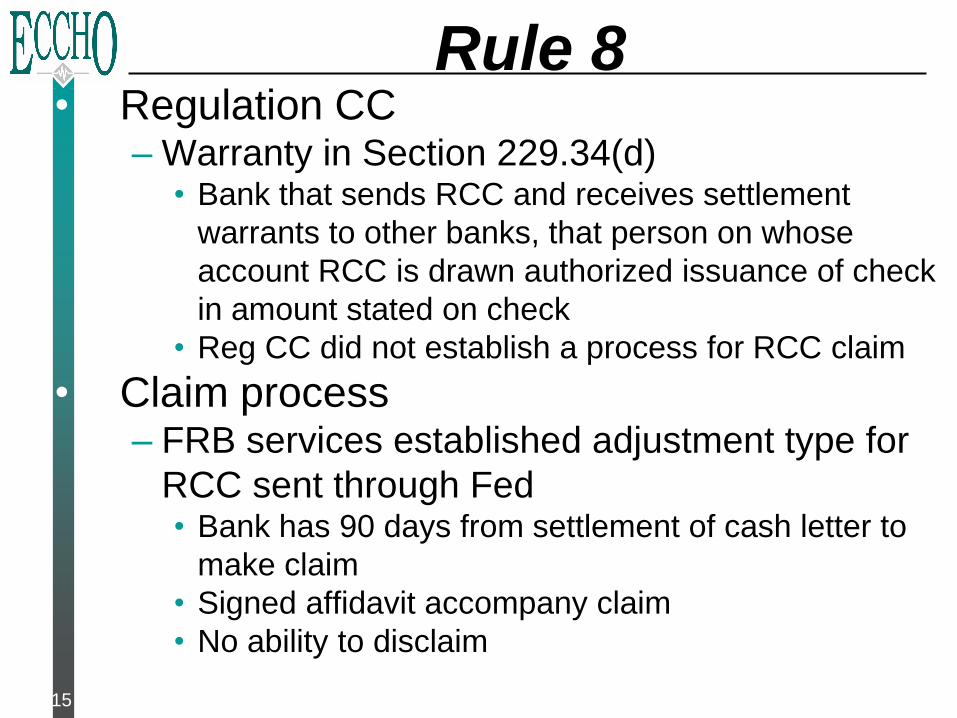

• Regulation CC– Warranty in Section 229.34(d)

• Bank that sends RCC and receives settlement

warrants to other banks, that person on whose

account RCC is drawn authorized issuance of check

in amount stated on check

• Reg CC did not establish a process for RCC claim

• Claim process– FRB services established adjustment type for

RCC sent through Fed• Bank has 90 days from settlement of cash letter to

make claim

• Signed affidavit accompany claim

• No ability to disclaim

15

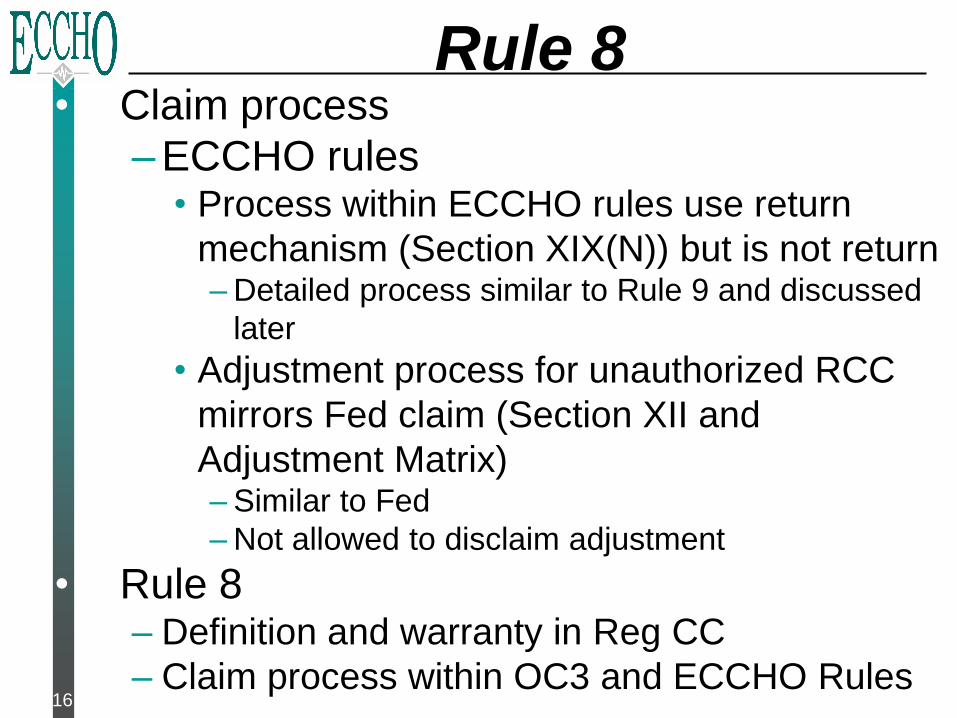

Rule 8

• Claim process

– ECCHO rules• Process within ECCHO rules use return

mechanism (Section XIX(N)) but is not return– Detailed process similar to Rule 9 and discussed

later

• Adjustment process for unauthorized RCC

mirrors Fed claim (Section XII and

Adjustment Matrix)– Similar to Fed

– Not allowed to disclaim adjustment

• Rule 8– Definition and warranty in Reg CC

– Claim process within OC3 and ECCHO Rules16

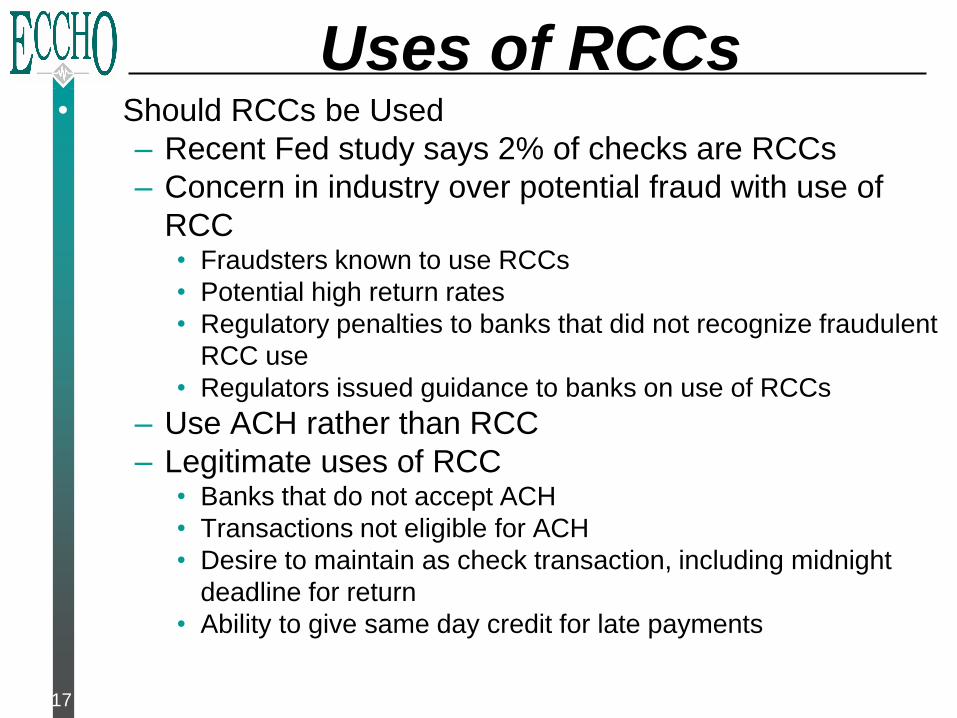

Rule 8

• Should RCCs be Used

– Recent Fed study says 2% of checks are RCCs

– Concern in industry over potential fraud with use of

RCC• Fraudsters known to use RCCs

• Potential high return rates

• Regulatory penalties to banks that did not recognize fraudulent

RCC use

• Regulators issued guidance to banks on use of RCCs

– Use ACH rather than RCC

– Legitimate uses of RCC• Banks that do not accept ACH

• Transactions not eligible for ACH

• Desire to maintain as check transaction, including midnight

deadline for return

• Ability to give same day credit for late payments

17

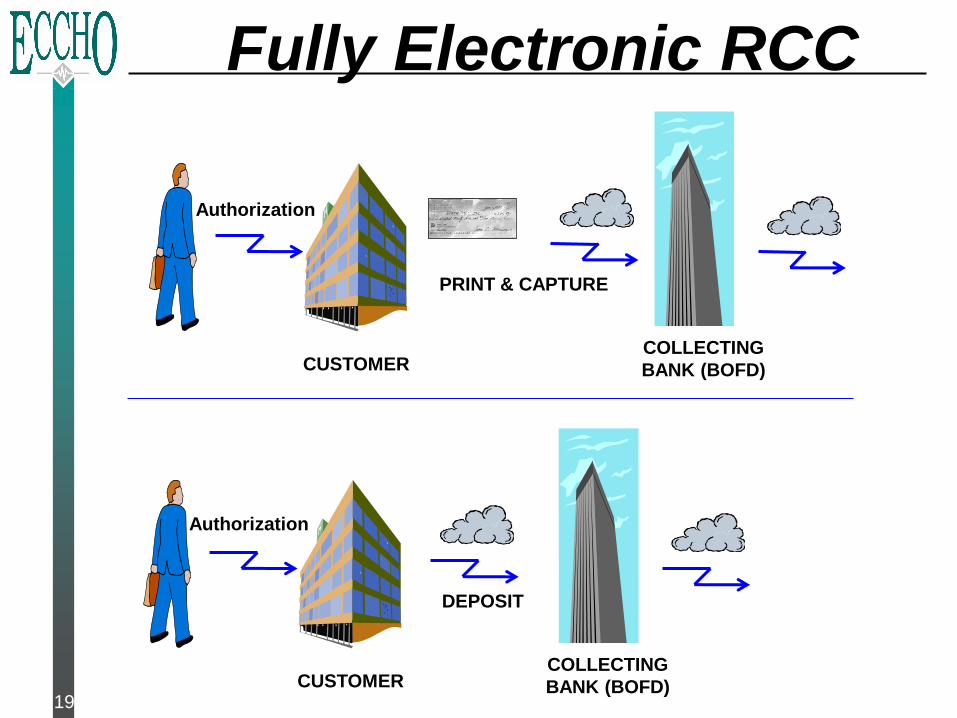

Uses of RCCs

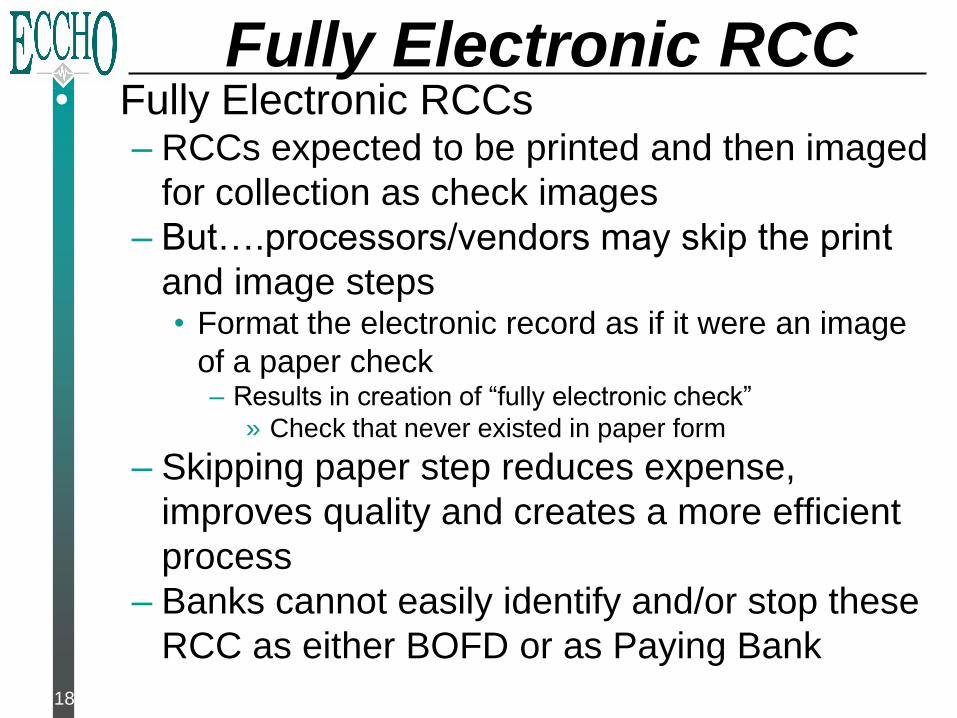

• Fully Electronic RCCs– RCCs expected to be printed and then imaged

for collection as check images

– But….processors/vendors may skip the print

and image steps• Format the electronic record as if it were an image

of a paper check– Results in creation of “fully electronic check”

» Check that never existed in paper form

– Skipping paper step reduces expense,

improves quality and creates a more efficient

process

– Banks cannot easily identify and/or stop these

RCC as either BOFD or as Paying Bank

Fully Electronic RCC

18

19

Fully Electronic RCC

COLLECTING

BANK (BOFD)CUSTOMER

PRINT & CAPTURE

COLLECTING

BANK (BOFD)CUSTOMER

DEPOSIT

Authorization

Authorization

• Poll Question #1 –Does your bank actively

participate in Rule 9?• Yes

• No

• Don’t know

20

Poll Question

• Poll Question #2

–What area of your bank handles

outgoing Rule 9 claims?• Adjustments

• Returns

• Fraud

• Customer Service

• Other

21

Poll Question

• Poll Question #3

–What area of your bank handles

incoming Rule 9 claims?• Adjustments

• Returns

• Fraud

• Customer Service

• Other

22

Poll Question

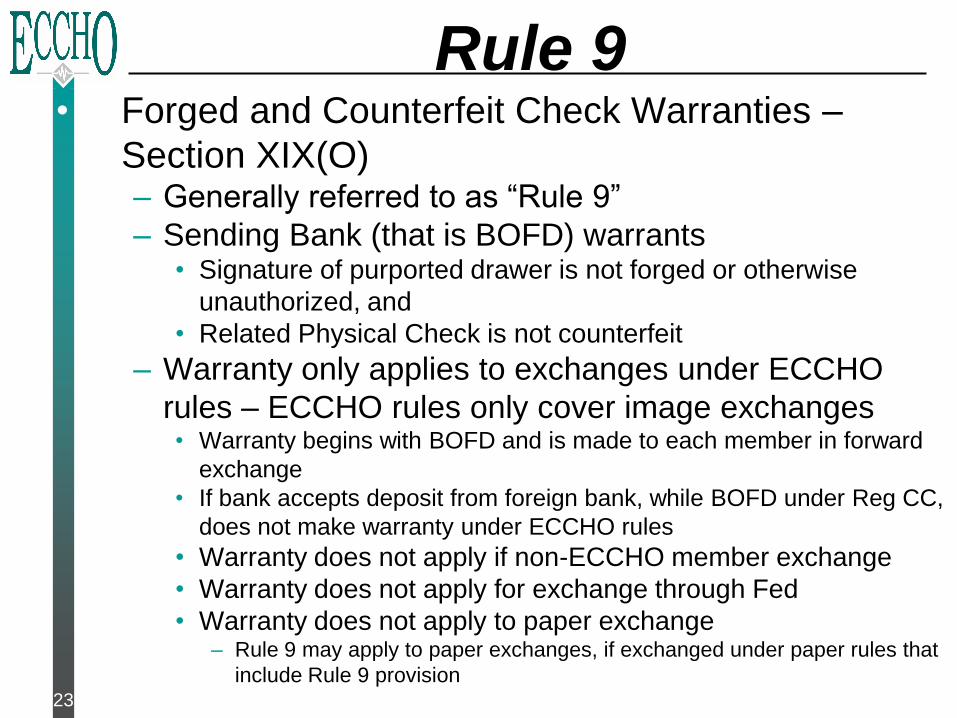

• Forged and Counterfeit Check Warranties –

Section XIX(O)– Generally referred to as “Rule 9”

– Sending Bank (that is BOFD) warrants• Signature of purported drawer is not forged or otherwise

unauthorized, and

• Related Physical Check is not counterfeit

– Warranty only applies to exchanges under ECCHO

rules – ECCHO rules only cover image exchanges• Warranty begins with BOFD and is made to each member in forward

exchange

• If bank accepts deposit from foreign bank, while BOFD under Reg CC,

does not make warranty under ECCHO rules

• Warranty does not apply if non-ECCHO member exchange

• Warranty does not apply for exchange through Fed

• Warranty does not apply to paper exchange– Rule 9 may apply to paper exchanges, if exchanged under paper rules that

include Rule 9 provision23

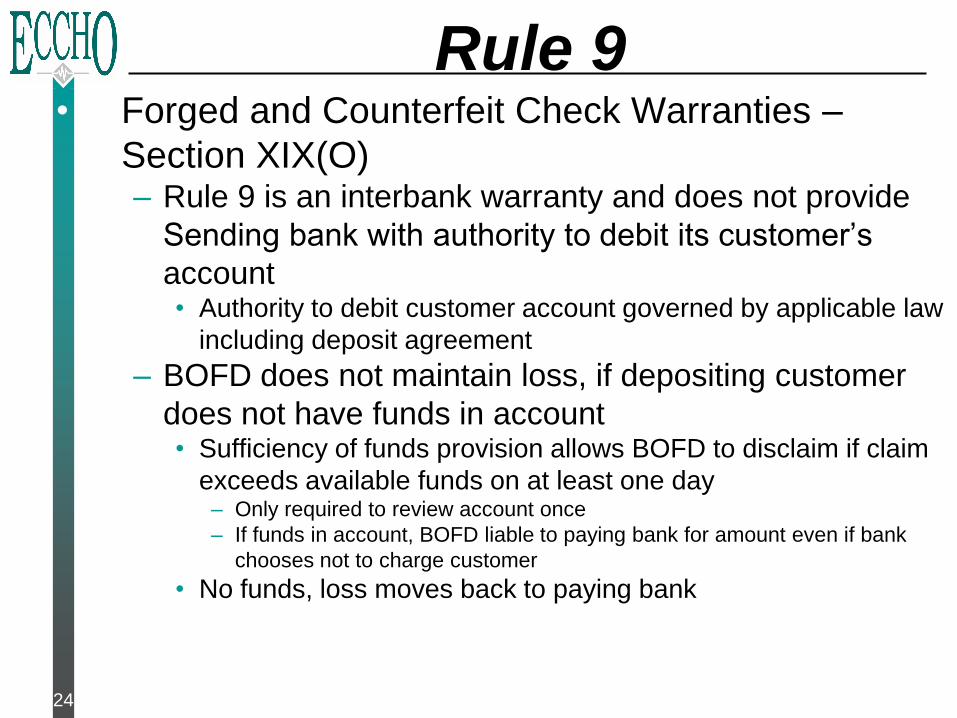

Rule 9

• Forged and Counterfeit Check Warranties –

Section XIX(O)– Rule 9 is an interbank warranty and does not provide

Sending bank with authority to debit its customer’s

account• Authority to debit customer account governed by applicable law

including deposit agreement

– BOFD does not maintain loss, if depositing customer

does not have funds in account• Sufficiency of funds provision allows BOFD to disclaim if claim

exceeds available funds on at least one day– Only required to review account once

– If funds in account, BOFD liable to paying bank for amount even if bank

chooses not to charge customer

• No funds, loss moves back to paying bank

24

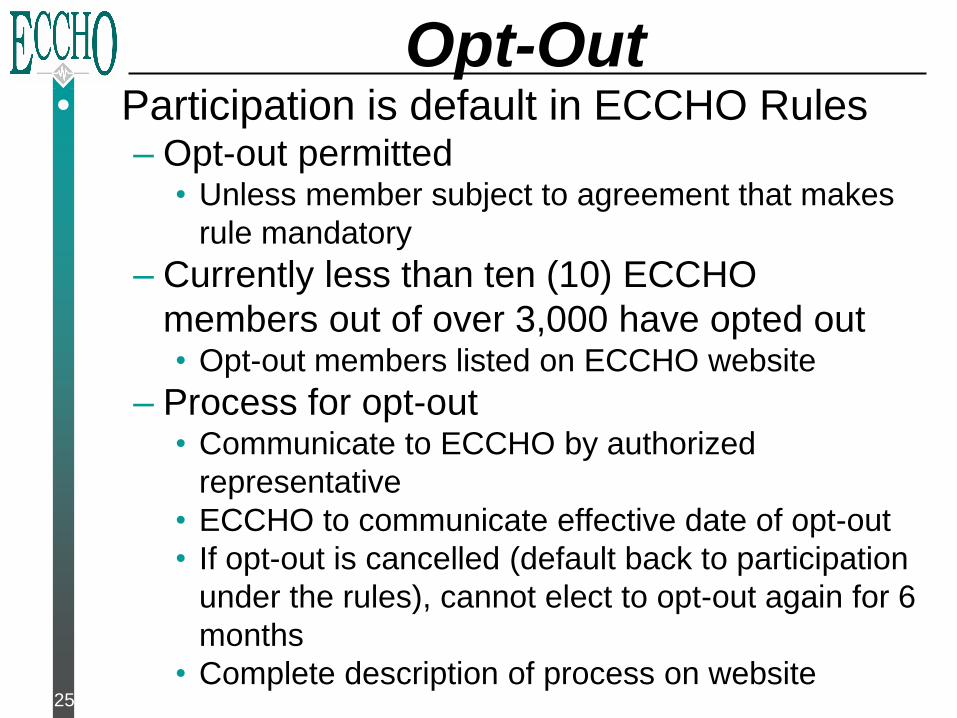

Rule 9

• Participation is default in ECCHO Rules– Opt-out permitted

• Unless member subject to agreement that makes

rule mandatory

– Currently less than ten (10) ECCHO

members out of over 3,000 have opted out• Opt-out members listed on ECCHO website

– Process for opt-out• Communicate to ECCHO by authorized

representative

• ECCHO to communicate effective date of opt-out

• If opt-out is cancelled (default back to participation

under the rules), cannot elect to opt-out again for 6

months

• Complete description of process on website25

Opt-Out

26

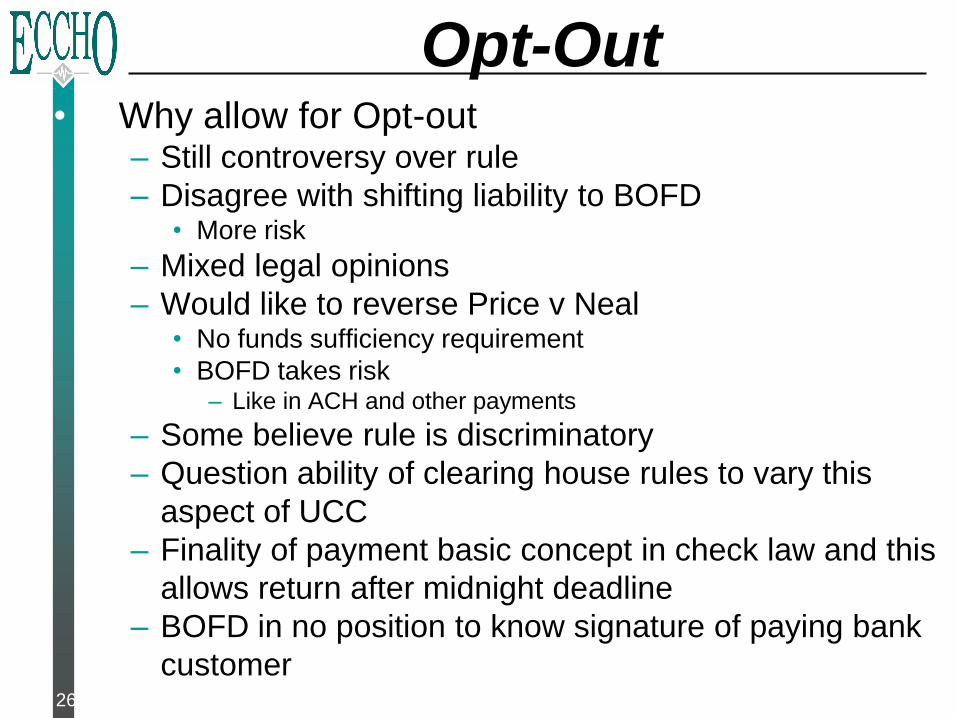

Opt-Out• Why allow for Opt-out

– Still controversy over rule

– Disagree with shifting liability to BOFD• More risk

– Mixed legal opinions

– Would like to reverse Price v Neal• No funds sufficiency requirement

• BOFD takes risk– Like in ACH and other payments

– Some believe rule is discriminatory

– Question ability of clearing house rules to vary this

aspect of UCC

– Finality of payment basic concept in check law and this

allows return after midnight deadline

– BOFD in no position to know signature of paying bank

customer

27

Mandatory Rule 9• Some Support for Mandatory Rule 9

– Rule in effect for over 15 years with no

litigation

– Original premise was paying bank had original

check• No longer case with image and IRDs

• Paying bank needs relief, since no longer has

original check

– Paying banks post from MICR data with little to

no review of check or check image

– Original rule was from risk perspective, now

should consider operational perspective

– Rule 9 is pro-image

• Similar timing/process as RCC warranty claim

(when using returns process Section XIX(N))– Paying Bank must make claim to BOFD via return

process• Use return mechanism, but actually adjustment

– Cannot send these claims through the Fed

• Return must contain notation of “Breach of Warranty”

and/or “Do Not Redposit or Re-Present” or similar

language– Paying Bank may use reason code that reflects item is sent

as warranty claim• Image standards use return reason of “3” – Warranty Breach

• Claim may be made via – Electronic image

– Paper copy of front and back of electronic image

– Substitute Check28

Claim Process

29

Disclaim - Rule 9

• Sending Bank may disclaim warranty

claim for– Account closed

– Claim amount exceeds funds in account

– Claim was not made timely as defined in

rules

– Sending Bank is not first bank to which

check was transferred

– Opt-out in effect

– Other defenses as provided by other

applicable law

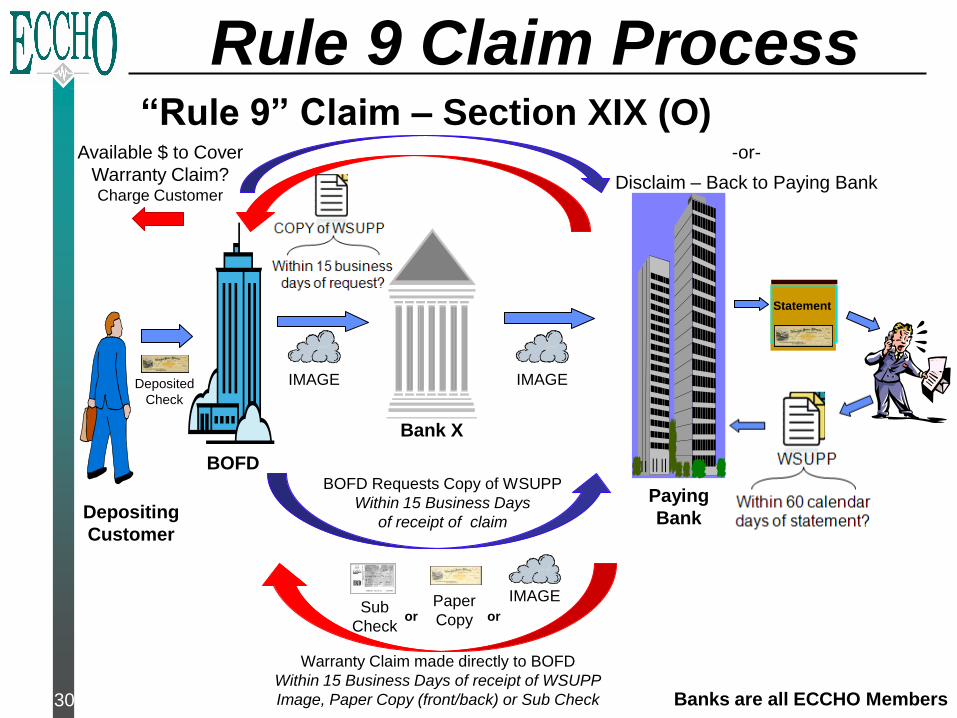

Rule 9 Claim Process“Rule 9” Claim – Section XIX (O)

Banks are all ECCHO Members

Statement

Depositing

Customer

IMAGEPaper

CopySub

Checkor or

Warranty Claim made directly to BOFD

Within 15 Business Days of receipt of WSUPP

Image, Paper Copy (front/back) or Sub Check

Paying

Bank

IMAGE IMAGEDeposited

Check

BOFD

Bank X

BOFD Requests Copy of WSUPP

Within 15 Business Days

of receipt of claim

Available $ to Cover

Warranty Claim?Charge Customer

-or-

Disclaim – Back to Paying Bank

30

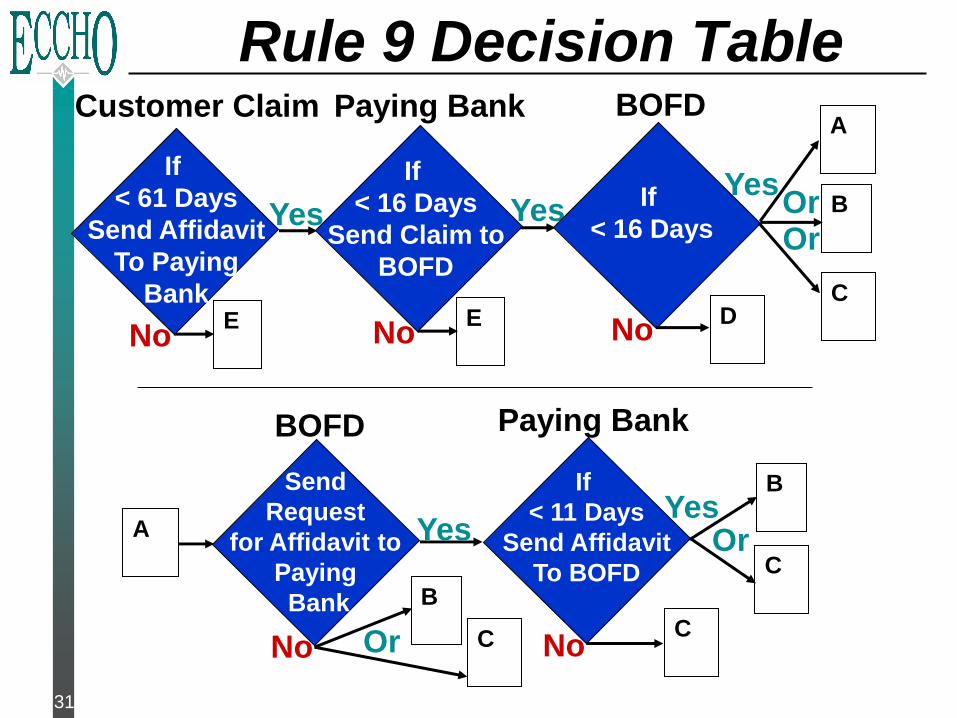

31

Yes

No

If

< 61 Days

Send Affidavit

To Paying

Bank

Yes

No

Customer Claim Paying Bank

If

< 16 Days

Send Claim to

BOFD

No

BOFD

If

< 16 DaysB

A

C

OrOr

Yes

No

BOFD

If

< 11 Days

Send Affidavit

To BOFD

Send

Request

for Affidavit to

Paying

Bank

Yes

No

Paying Bank

B

C

B

OrC

DE E

Yes

A

COr

Rule 9 Decision Table

32

If $s in

Customer’s

Account

No

Yes

Debit customer & avoid loss(if claim received without entry, settle

with Paying Bank)

BOFD

B

Receives disclaimer

Paying Bank

BOFD

Paying Bank retains loss

Or

Customer not debited

CBOFD has loss

D

E

BOFD

CSend

disclaimer

to

Paying Bank

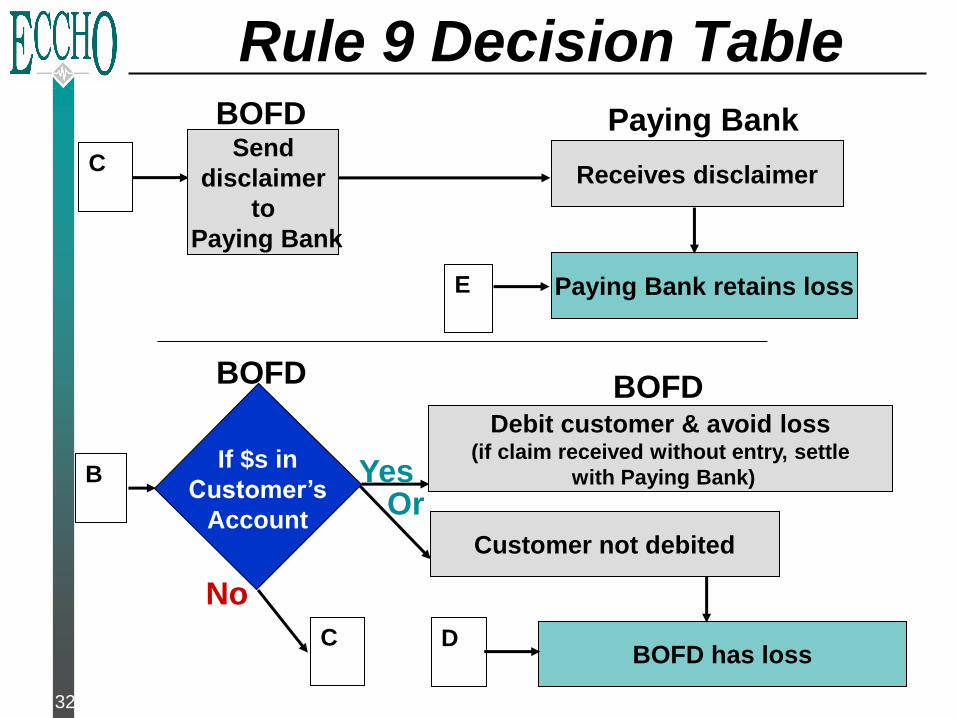

Rule 9 Decision Table

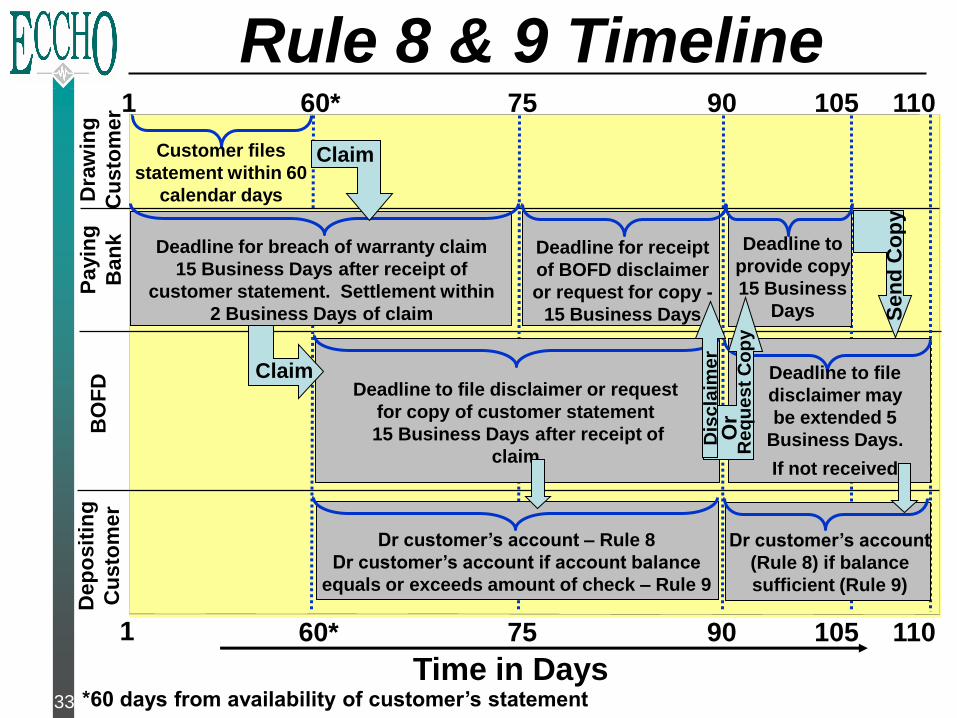

Rule 8 & 9 Timeline

Time in Days

Payin

g

Ban

kB

OF

D11060* 75 90 1051

*60 days from availability of customer’s statement

Customer files

statement within 60

calendar daysDra

win

g

Cu

sto

mer

11060* 75 90 1051

De

po

sit

ing

Cu

sto

mer

ClaimDeadline to file disclaimer or request

for copy of customer statement

15 Business Days after receipt of

claim

Deadline to

provide copy

15 Business

Days

Deadline to file

disclaimer may

be extended 5

Business Days.

If not received

Re

qu

es

t C

op

y

Deadline for receipt

of BOFD disclaimer

or request for copy -

15 Business Days

Deadline for breach of warranty claim

15 Business Days after receipt of

customer statement. Settlement within

2 Business Days of claim

Dr customer’s account – Rule 8

Dr customer’s account if account balance

equals or exceeds amount of check – Rule 9

Dr customer’s account

(Rule 8) if balance

sufficient (Rule 9)

Claim

Dis

cla

ime

r

Sen

d C

op

y

Or

33

• Paying Bank Claim must be made to BOFD as

return– Claim cannot be made through Fed

– If bank returns through Fed, no mechanism to make

claim

– Claim made through Fed may be rejected as late return

• Original rule required stamp to tell BOFD Rule 9

claim– Stamp not practical in image, so allowed for return

reason• Return reason as either customer or administrative return of “3”

– Warranty Breach (includes Rule 8 & 9 claims)

34

Challenges For Image

• Disclaim process, still needs work– Rules developed in local clearinghouses where

exchanges typically in person and in reasonable

proximity to one another• When need to disclaim was exchanged between members

– Today with national image exchange environment

members no longer in same geographic location• Image exchanged through multiple banks and/or networks

– Rule 9 claim and disclaim cannot be made to

intermediaries or Federal Reserve• Claim must be made directly to BOFD

• How to disclaim to appropriate party

35

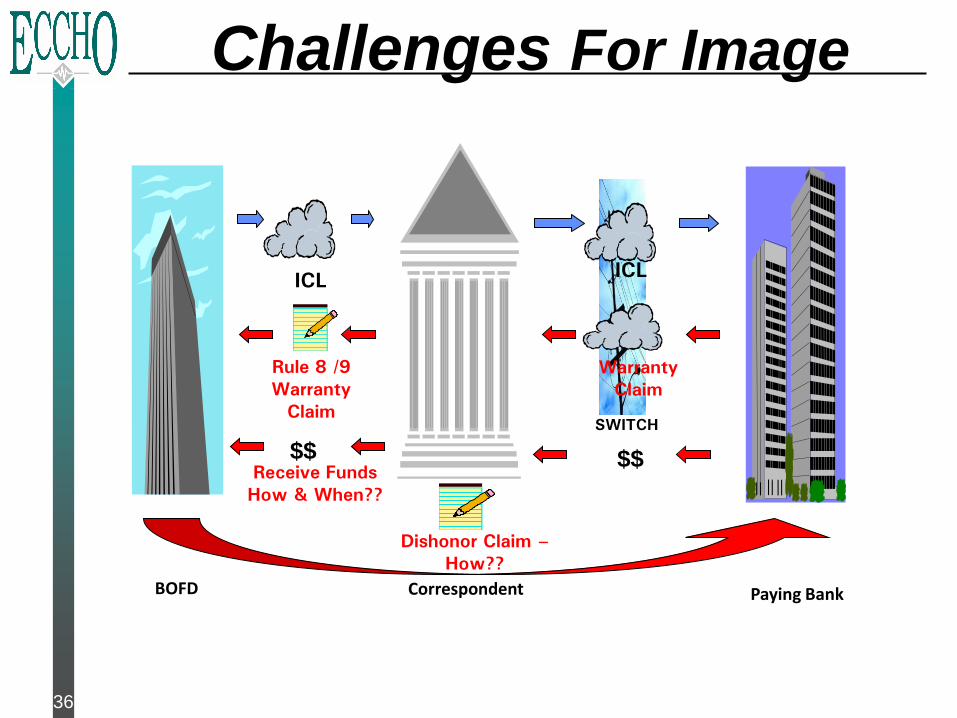

Challenges For Image

BOFD

ICL

Correspondent Paying Bank

ICL

SWITCH

Rule 8 /9

Warranty

Claim

Warranty

Claim

Dishonor Claim –

How??

$$$$Receive Funds

How & When??

Challenges For Image

36

• Banks typically act as both Paying Bank and BOFD– Both banks have opportunity to make claim or claim

made to it– Balanced and fair rules to share risks by all members

• Paying bank– Able to recover some money from the BOFD that would

have previously been a loss– Rules do not change way bank decides to reimburse

customers for forged or counterfeit checks• BOFD try to recover money from depositing

customer for Paying bank– Balance risk of customer relationship in charging back

customer for Rule 9 claim– Customer service impact has been negligible– Recovering of funds paid from fraudulent item very

positive

37

Risks vs Benefits

• Process– For paying bank claim is outgoing items– For BOFD claims are incoming items

• Returned deposited items for customer

• Average amount of items about $350• Millions of dollars savings based on Rule 9

claims over the years• Only about 5% or less are disclaimed by

BOFD• Much greater chance item will be

disclaimed if payable to individual– Fraud has occurred at both Paying Bank and

BOFD

38

Risks vs Benefits

39

Additional Information• Will be Distributed after Session

– Exhibits from ECCHO Rules• Disclaimer Form: Rule 8 and 9

• Explanatory Charts for Rule 8 and 9 Process– Events Timing

– Decisions

• Model Customer Written Statement for

Warranty Claim under Rules 8 and 9

• Coming Soon– Document on Rule 8 and 9 – by ECCHO

Questions?

40

Kevin Cranford

704-954-3645

Thank You!Phyllis Meyerson

214-273-3202

Ap

ril 1

5, 2011