econ. 338c: overview of grain marketing dr. robert wisner, university professor iowa state...

TRANSCRIPT

Econ. 338C: Overview of Econ. 338C: Overview of Grain MarketingGrain Marketing

Econ. 338C: Overview of Econ. 338C: Overview of Grain MarketingGrain Marketing

Dr. Robert Wisner, Dr. Robert Wisner, University ProfessorUniversity ProfessorIowa State UniversityIowa State University

Dr. Robert Wisner, Dr. Robert Wisner, University ProfessorUniversity ProfessorIowa State UniversityIowa State University

Spring 2007

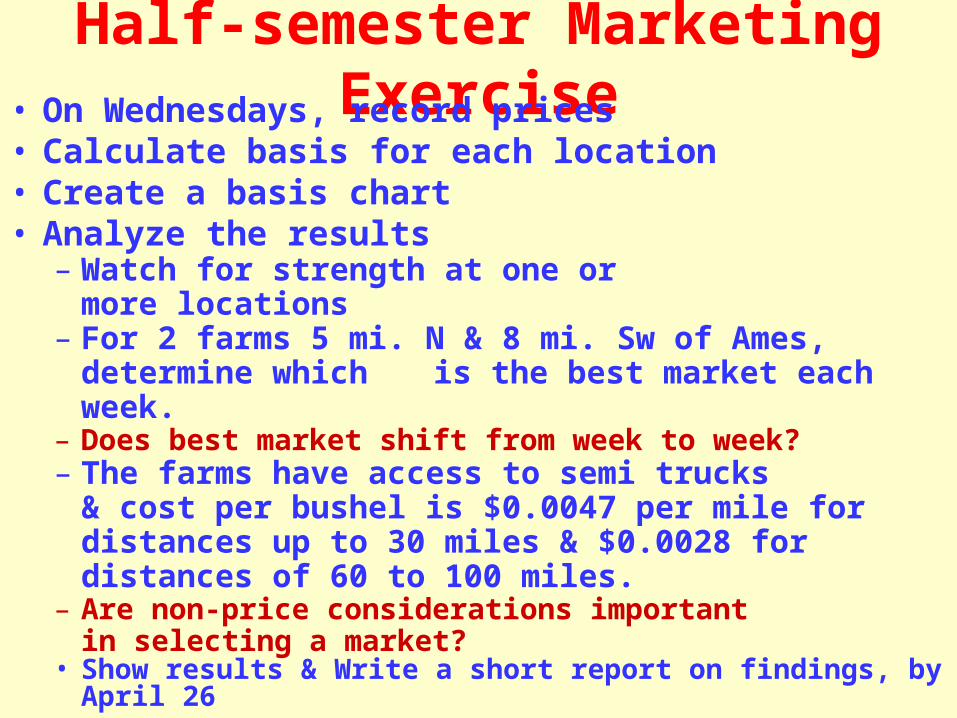

Half-semester Marketing Exercise• On Wednesdays, record prices • Calculate basis for each location• Create a basis chart• Analyze the results

– Watch for strength at one or more locations

– For 2 farms 5 mi. N & 8 mi. Sw of Ames, determine which is the best market each week.

– Does best market shift from week to week? – The farms have access to semi trucks

& cost per bushel is $0.0047 per mile for distances up to 30 miles & $0.0028 for distances of 60 to 100 miles.

– Are non-price considerations important in selecting a market?

• Show results & Write a short report on findings, by April 26

The Market’s Job: Transfering Raw Products to Consumer Products

Major Marketing Functions

• Providing time utility

• Providing form utility

• Providing space utility

• Financing

• Price/value discovery

Market Participants• Grain Producers

• Elevators

• Railroads, trucking & barge companies

• Banks & insurance cos.• Futures market traders & brokers

• Processors

• Feed Mills

• Ocean shipping firms

Key work areas for Grain Merchandisers

* Arbitrage = Maximizing return

over time & space

*Maximizing returns for available storage

*Utilizing transportation equipment efficiently * Choices heavily influenced by futures

Futures prices 3/7/07Implications?

CornMarch $4.132 May 4.24July 4.32Sept. 4.18Dec. 4.08May ‘08 4.18 July 4.23Dec. ’09 3.70

SoybeansMarch $7.34 May 7.48July 7.64Sept. 7.75Nov. 7.87May ‘08 7.97 July 8.03Nov. ’09 7.48

Futures prices 7/14/06

CornJuly $2.54 Sept. 2.61Dec. 2.77March’07 2.88May 2.97July 3.03

SoybeansJuly $6.02 Aug. 6.03Sept. 6.11Nov. 6.25Jan. ’07 6.37March ‘07 6.46

What were the markets telling farmers? Other needed information?

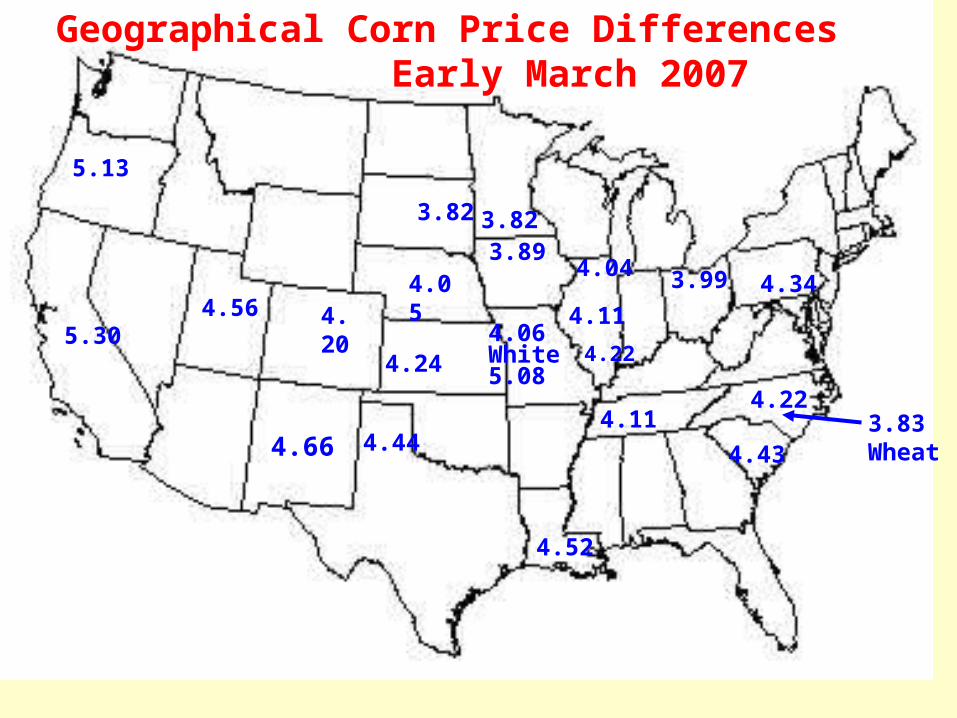

Geographical Corn Price Differences Early March 2007

4.06White 5.08

4.04 3.99

4.44

4.223.83 Wheat

3.82 3.82

4.56 4.204.05

5.30

5.13

4.343.89

4.11

4.52

4.24

4.11

4.22

4.66 4.43

0

20

40

60

80

100

120

140

160

Bu

./A

.

0

1

2

3

4

5

6

7

8

Bil

lio

n p

eo

ple

1950 1960 1970 1980 1990 2000

World Population & U.S. Corn Yield1950-1999

Population

Corn Yield

Overview of Grain Marketing , cont. • All Activities from production to final

user = Marketing• First receivers of grain-- elevators,

processors, feedlots– Pricing the grain to farmers– Offering contracts– Merchandising: finding greatest value for the

grain – Economics of transportation– Utilizing space efficiently– Segregating: specialty crops, non-GMO

Econ. 338 C: Spring 2003

Countries requiring GMO labeling

U.K.BelgiumFranceNetherlandsGermanyLuxembourgSwitzerlandDenmarkIrelandParaguaySloveniaSri LankaLatvia, Estonia, Slovakia Lithuania

Greece Portugal Spain Sweden Finland Austria Poland Australia New Zealand China Thailand Taiwan Malaysia

Italy S. Korea Japan Czech Rep. Hungary Saudi Arabia Japan Mexico Russia Ethiopia South Africa

Hungary PhilippinesBrazil

Econ. 338C: Overview of GrainU.S. & Global Marketing

From BNSF

Overview of Grain Marketing, cont. • First receivers of grain-- Continued

– Grading grain: Official & unofficial grades

– Grading standards: BCFM, Test Wt., Damage, soybeans include splits, foreign material

– Risk-management: hedging, using options

– Quality control and management ***

• Processors--soybeans– Managing & protecting processing margins:

– hedging the crush, reverse crush positions

– Merchandising products

– Sourcing the soybeans

Calculating Soybean Crush Margins 2/26/2004 2/27/03

Soybean oil price$/lb. 0.353 0.2132Oil yield, lbs./Bu. 11.06 11.2Oil value,$/Bu. 3.904 2.388

Soybean meal price, $/ton 275.00 184.00Meal yield, lbs./Bu. 45.86 43.78Meal value,$/Bu. 6.306 4.028

Total value from products 10.210 6.416Bean price, C. Illinois 9.42 5.88Gross Crush Margin 0.790 0.536

Calculating Soybean Crush Margins 3/01/20073/02/06

Soybean oil price$/lb. 0.2889 0.2450Oil yield, lbs./Bu. 11.26 11.59Oil value,$/Bu. 3.25 2.84

Soybean meal price, $/ton209.60 176.10Meal yield, lbs./Bu. 44.09 44.08Meal value,$/Bu. 4.62 3.88

Total value from products7.87 6. 72Bean price, C. Illinois 7.30 5.83Gross Crush Margin 0.58 0.90

Figure 1. Soybean Crush margins implied by futures 2004/05

0.00

0.20

0.40

0.60

0.80

1.00

1.20

Cashmargin

March May July Aug Sept Nov Jan

$ p

er

bu

sh

el

Feb 3, 04" Feb 25, 04"5-Mar-04

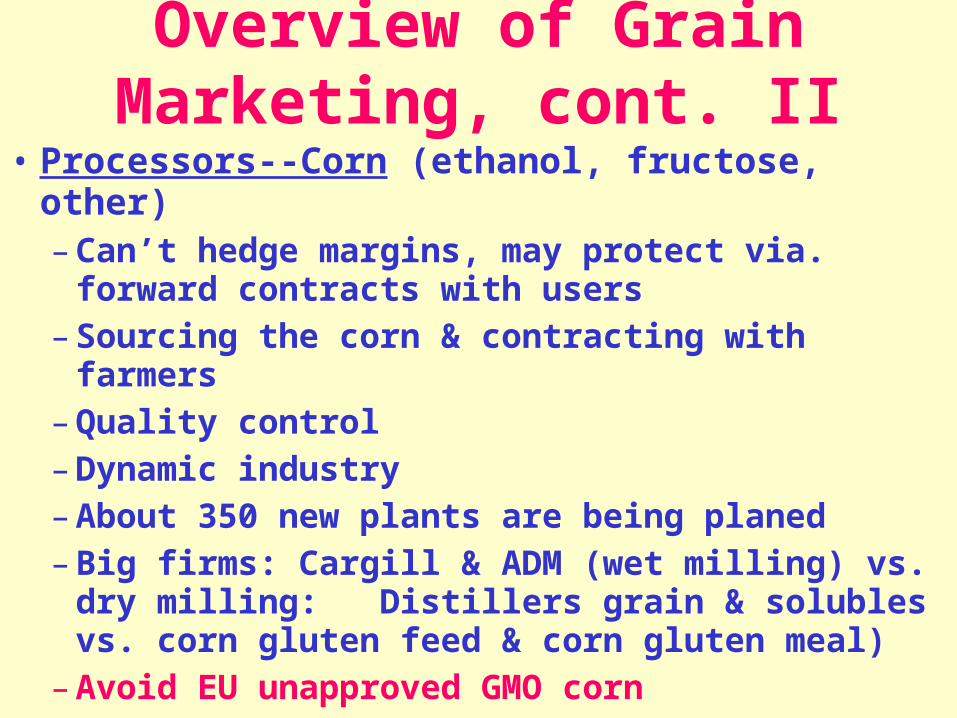

Overview of Grain Marketing, cont. II

• Processors--Corn (ethanol, fructose, other)– Can’t hedge margins, may protect via.

forward contracts with users– Sourcing the corn & contracting with farmers– Quality control– Dynamic industry– About 350 new plants are being planed– Big firms: Cargill & ADM (wet milling) vs. dry

milling: Distillers grain & solubles vs. corn gluten feed & corn gluten meal)

– Avoid EU unapproved GMO corn

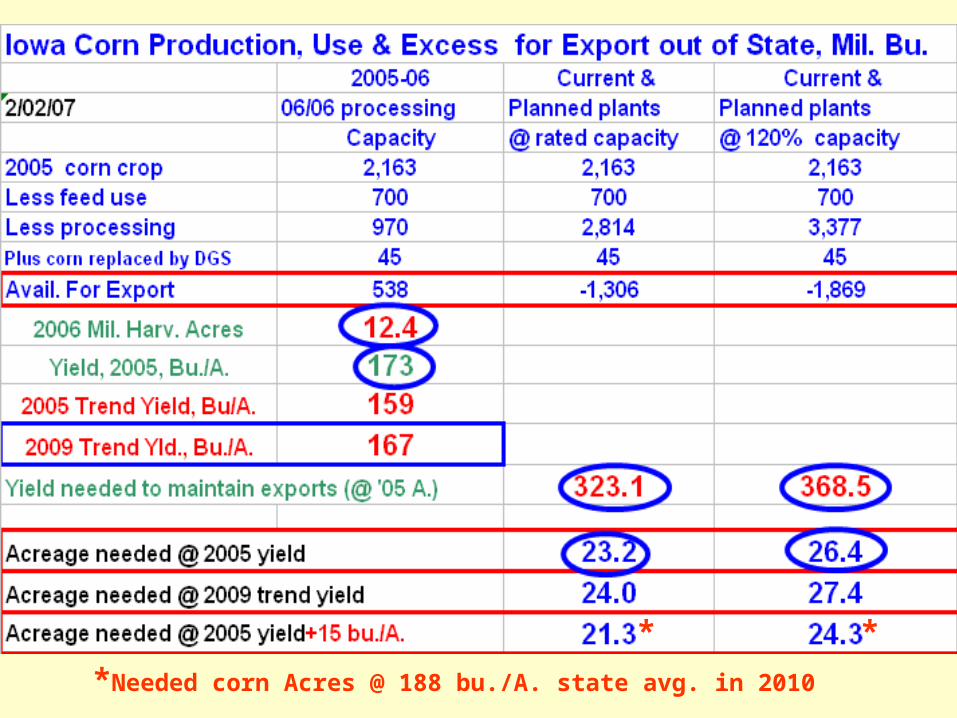

Iowa Corn Processing Plants

Annual Capacity

Operating Plants 970 mil. bu.

Expanding Plants 282

New, Under Construction 198

Planned 1,364

Potential total rated capacity 2,814 mil. bu.

Equals 137% of 2006 Iowa Corn Crop

1/29/07

Iowa corn processing & ethanol plants, current & planned, 10/26/06

63

Sac

Linn

Lee

Ida

Tama

Clay Kosuth

Jasper

Lyon

Page

StoryrJones

Fayette

Adair

Bentonn

Wapello

Pocahontas

Osceola

Jefferson

Audubon

Washington

BuenaVista

BlackHawk

Appanoose

CerroGordo

VanBuren

Mucatine

Dickenson

DesMoines

Winnebago

Montgomery

Iowa Corn Processing & Ethanol Plant Locations, Actual & Planned. 9/26/06,

PoweshiekPolk

BooneGreeneCarrollCrawford

Plymouth

O’Brien

Woodbury

Monona

Harrison Shelby

Wright Franklin

Floyd Chickasaw

Webster Hardin

Louisa

Emmet

Palo Alto

Hancock

Worth Mitchell HowardWinneshiek Allamakee

BremerButler

HamiltonGrundy

Buchanan

Delaware

Dubuque

Jackson

Clintonn

Guthrie Dallas

Johnson

Marshall

Pottawattamie

Mills

Fremont

Madison

Warren Marion Mahaska

Keokuk

Adams Union Clarke Lucas Monroe

Taylor Ringgold

Cherokee

Calhoun

Decatur Wayne Davis

Henry

Scott

Humboldt

Clayton

Cedar

Sioux

Cass

Iowa*

**

*

*

*

*

* **

*

**

*

**

*

*

*

**

*

*

*

*

*

*

*

*

**

**

*

**

*

*

**

*

* * **

Sac

Linn

Lee

Ida

Tama

Clay Kosuth

Jasper

Lyon

Page

StoryrJones

Fayette

Adair

Bentonn

Wapello

Pocahontas

Osceola

Jefferson

Audubon

Washington

BuenaVista

BlackHawk

Appanoose

CerroGordo

VanBuren

Mucatine

Dickenson

DesMoines

Winnebago

Montgomery

,

PoweshiekPolk

BooneGreeneCarrollCrawford

Plymouth

O’Brien

Woodbury

Monona

Harrison Shelby

Wright Franklin

Floyd Chickasaw

Webster Hardin

Louisa

Emmet

Palo Alto

Hancock

Worth Mitchell HowardWinneshiek Allamakee

BremerButler

HamiltonGrundy

Buchanan

Delaware

Dubuque

Jackson

Clintonn

Guthrie Dallas

Johnson

Marshall

Pottawattamie

Mills

Fremont

Madison

Warren Marion Mahaska

Keokuk

Adams Union Clarke Lucas Monroe

Taylor Ringgold

Cherokee

Calhoun

Decatur Wayne Davis

Henry

Scott

Humboldt

Clayton

Cedar

Sioux

Cass

Iowa*

**

*

*

*

*

* **

*

**

*

**

*

*

*

**

*

*

*

*

*

*

*

*

**

**

*

**

*

*

**

*

* * **

*

Sac

Linn

Lee

Ida

Tama

Clay Kosuth

Jasper

Lyon

Page

StoryrJones

Fayette

Adair

Bentonn

Wapello

Pocahontas

Osceola

Jefferson

Audubon

Washington

BuenaVista

BlackHawk

Appanoose

CerroGordo

VanBuren

Mucatine

Dickenson

DesMoines

Winnebago

Montgomery

Iowa Corn Processing & Ethanol Plant Locations, Actual & Planned. 9/26/06,

PoweshiekPolk

BooneGreeneCarrollCrawford

Plymouth

O’Brien

Woodbury

Monona

Harrison Shelby

Wright Franklin

Floyd Chickasaw

Webster Hardin

Louisa

Emmet

Palo Alto

Hancock

Worth Mitchell HowardWinneshiek Allamakee

BremerButler

HamiltonGrundy

Buchanan

Delaware

Dubuque

Jackson

Clintonn

Guthrie Dallas

Johnson

Marshall

Pottawattamie

Mills

Fremont

Madison

Warren Marion Mahaska

Keokuk

Adams Union Clarke Lucas Monroe

Taylor Ringgold

Cherokee

Calhoun

Decatur Wayne Davis

Henry

Scott

Humboldt

Clayton

Cedar

Sioux

Cass

Iowa*

**

*

*

*

*

* **

*

**

*

**

*

*

*

**

*

*

*

*

*

*

*

*

**

**

*

**

*

*

**

*

* * **

Sac

Linn

Lee

Ida

Tama

Clay Kosuth

Jasper

Lyon

Page

StoryrJones

Fayette

Adair

Bentonn

Wapello

Pocahontas

Osceola

Jefferson

Audubon

Washington

BuenaVista

BlackHawk

Appanoose

CerroGordo

VanBuren

Mucatine

Dickenson

DesMoines

Winnebago

Montgomery

,

PoweshiekPolk

BooneGreeneCarrollCrawford

Plymouth

O’Brien

Woodbury

Monona

Harrison Shelby

Wright Franklin

Floyd Chickasaw

Webster Hardin

Louisa

Emmet

Palo Alto

Hancock

Worth Mitchell HowardWinneshiek Allamakee

BremerButler

HamiltonGrundy

Buchanan

Delaware

Dubuque

Jackson

Clintonn

Guthrie Dallas

Johnson

Marshall

Pottawattamie

Mills

Fremont

Madison

Warren Marion Mahaska

Keokuk

Adams Union Clarke Lucas Monroe

Taylor Ringgold

Cherokee

Calhoun

Decatur Wayne Davis

Henry

Scott

Humboldt

Clayton

Cedar

Sioux

Cass

Iowa*

**

*

*

*

*

* **

*

**

*

**

*

*

*

**

*

*

*

*

*

*

*

*

**

**

*

**

*

*

**

*

* * **

*

*

*

* **

*

*

*

*

66 Planned + current in Iowa

11 Just across the borders

*

*

**

Figure 1.

*

*

*

Iowa corn processing & ethanol plants, current & planned, 11/20/06

63

Capacity: 129% of 2006 cropCapacity: 137% of 2006 Crop

Iowa Corn Processing Plants, Current & Planned, 2/16/07

71 Potential Iowa Plants 11 Just across IA Borders

*Needed corn Acres @ 188 bu./A. state avg. in 2010

**

Needed Yld. @ current Acres

NCGA Yield Contest 1996-2006, Irrigated and Non-Irrigated Winners, Outliers Removed

0

50

100

150

200

250

300

350

400

1995 1997 1999 2001 2003 2005 2007

Yiel

d (b

u/ac

re)

Source: Dr. Roger Elmore, ISU Agronomy Dept.

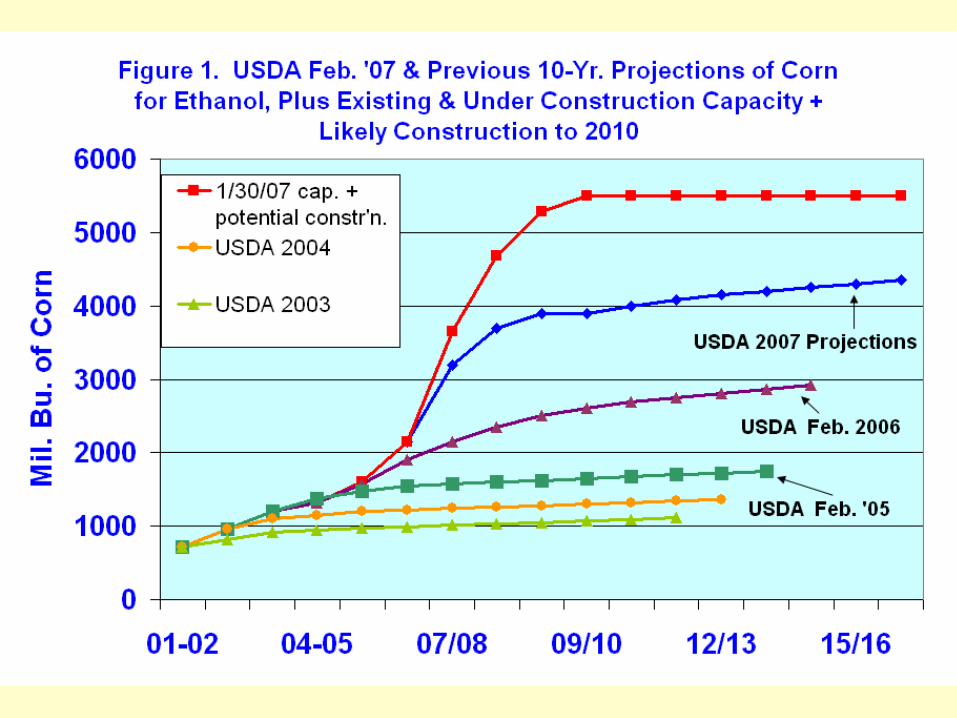

Existing & Planned U.S. Corn Processing Plants

Blue = OperatingRed = constructionGreen = plannedPink = Expansion of Existing plants

Figure 2.

8/30/06

5.5 Bil. Bu for ethanol

Crop Reporting Distr.

Illinois Corn Yields Drought Tolerant?

2004 2005

• NW 184 140

• NE 174 129

• WEST 192 141

• E.SE. 175 139

• SW 158 133

• SE 158 130

% chg.

-24

-26

-27

-21

-16

-18

‘Example’ of Exchange Rate Impact

Iowa’s Soybean Costs

Source: Embrapa Agrop. Oeste / ISU-USDA - 42 -

2000 2001 2002 2003 2004 2005 2006US$/ ha - IA, U.SR$/ ha - IA, U.S.

R$/ ha - MT, BRExchange Rate(*)

209.12%

250.50%

100.00%

155.56%

144.80%

181.91%

172.43%

145.86%139.20%

100.00%

119.16%110.91%

109.14%

100.00%

0.00%

50.00%

100.00%

150.00%

200.00%

250.00%

300.00%

US$/ha - IA, U.S R$/ha - IA, U.S.

R$/ha - MT, BR Exchange Rate(*)

+70%

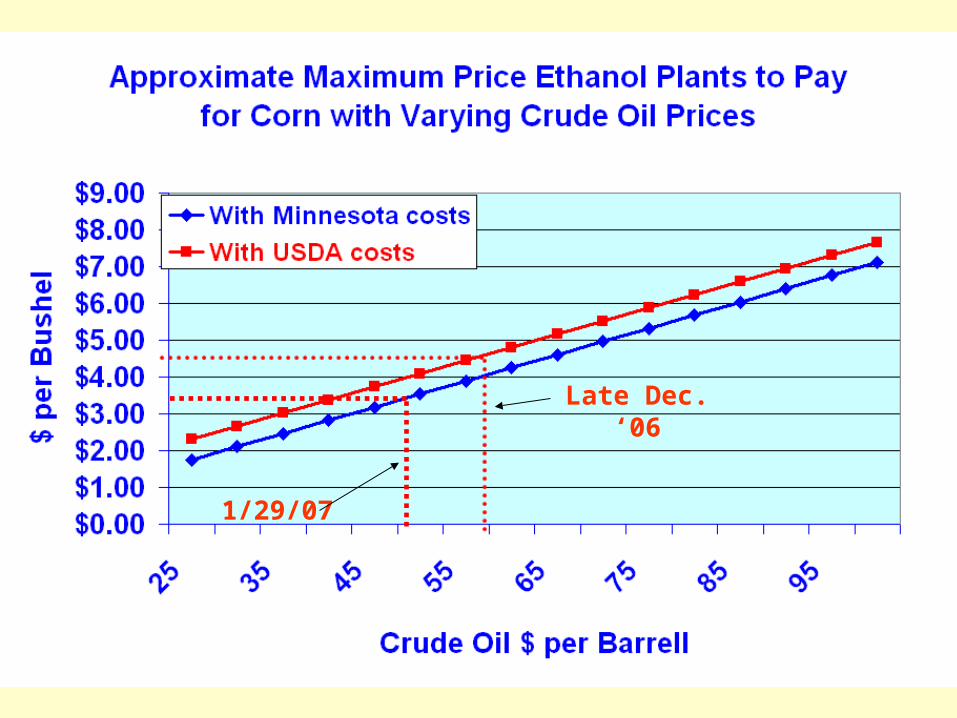

March Crude Oil Futures 2/16/07

Mar. N.Y. Gasoline Futures 2/16/07

Feb. Ethanol Futures 2/16/07

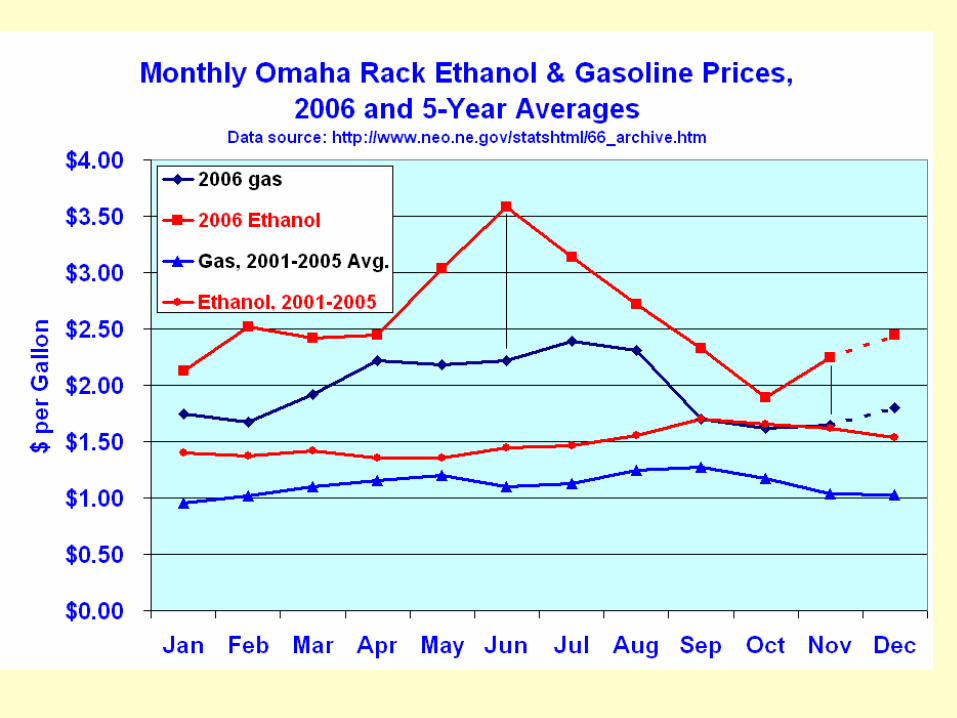

State Average Ethanol Rack Prices

http://www.axxispetro.com/ace.shtml

www.ethanol.org

Date: 2/02/07

Iowa: 1.95 Feb. 20: 2.16Illinois: 2.05

Kansas: 2.05

Michigan: 2.29

Minnesota: 1.89

Missouri: 2.24

North Dakota: 1.91

Nebraska: 2.01

South Dakota: 1.99

Wisconsin: 2.16

Averages provided by:

Ethanol Economics• $0.10 increase in ethanol price raises break-even Corn price $0.28/bu.• $1.00 rise in corn price increases cost/gal. $0.36• Ethanol prod’n cost $1.30/gal. (Minnesota- @$2 corn)

• Cost increases about $0.36/gal. for each $1 increase in corn

• 1/29/07 ethanol price: $1.91/gal.

• December 06 margins: $0.64/gal. (incl.$.51credit)

• 1/29/07: Drops to zero @ corn price of about $3.70 corn in IA ($4.10 with USDA costs) 2/20: $4.40-4.80

• Other variables: DDGS price, Natural Gas

Late Dec. ‘06

1/29/07

Monthly Unleaded GasolineFutures Prices

Gulf Hurricanes

High Prices are best cure for high prices

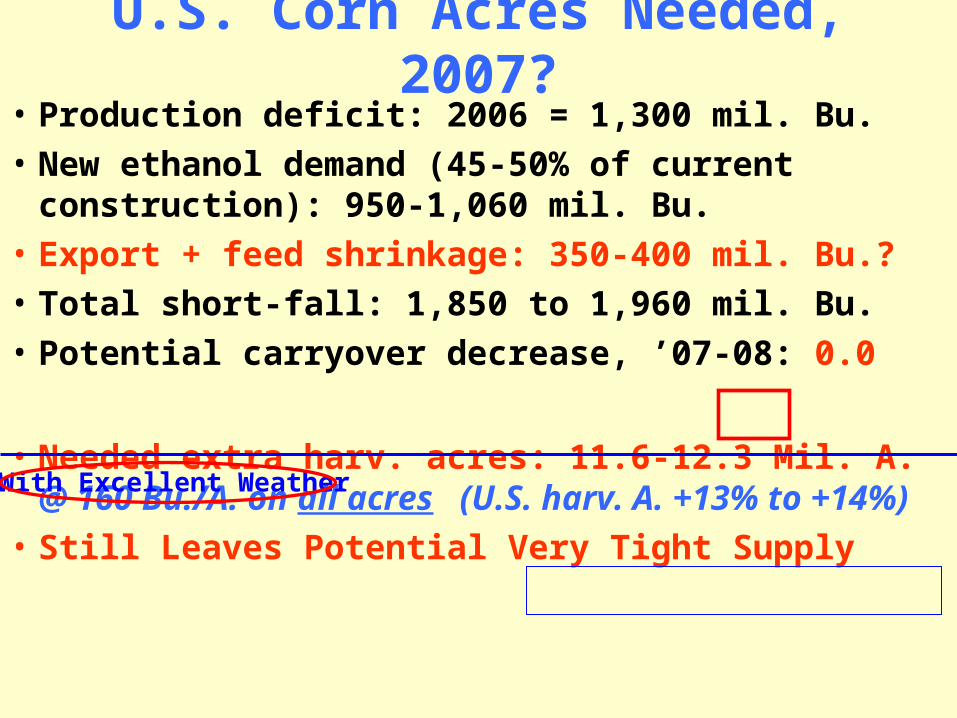

U.S. Corn Acres Needed, 2007?• Production deficit: 2006 = 1,300 mil. Bu.

• New ethanol demand (45-50% of current construction): 950-1,060 mil. Bu.

• Export + feed shrinkage: 350-400 mil. Bu.?

• Total short-fall: 1,850 to 1,960 mil. Bu.

• Potential carryover decrease, ’07-08: 0.0

• Needed extra harv. acres: 11.6-12.3 Mil. A. @ 160 Bu./A. on all acres (U.S. harv. A. +13% to +14%)

• Still Leaves Potential Very Tight Supply

With Excellent Weather

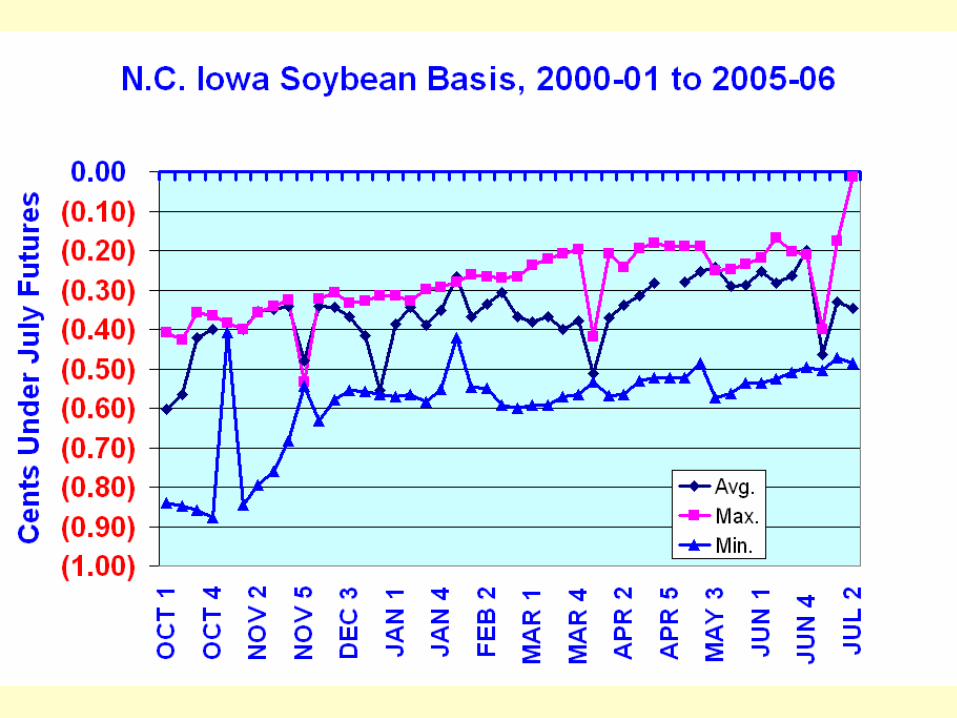

Basis for Corn, Iowa Counties

Corn Basis (cents/bu)

under near-by futures

Notes: Underlined data indicates that no data were available; averages for surrounding counties are reported.

-36.0 to -30.2

-30.2 to -28.7

-28.7 to -25.0

-25.0 to -21.6

-21.6 to -17.4 -17.4 to 0.0

Late January to late February, 2005

http://www.card.iastate.edu/ag_risk_tools/basis_maps/

Global forces to cause slowing of corn-based ethanol growth

from current 50-60% annual growth

• Corn price• Ethanol price• DDG price• Plant energy costs• Food & feed demand• Crude oil & gasoline prices• Govt. mandates & other policies

Corn Basis Under March FuturesNorthwest Iowa

Feb. 2007 -0.19Feb. 2005 -0.260Feb. 2004 -0.213Feb. 2003 -0.178 Feb. 2002 -0.276*Feb. 2001 -0.335Feb. 2000 -0.362Feb. 1999 -0.320 Avg. 1999-02 -0.323

North Central Iowa Feb. 2007 -0.20 Feb. 2005 -0.280 Feb. 2004 -0.253

Feb. 2002 -.0218Feb. 2001 -0.276Feb. 2000 -0.310Feb. 1999 -0.342Feb. 1999 -0.280Avg. 1999-02 -0.302

Mil. Bu. Change in 2002 Corn Production vs. 2001 11/12/02

+240

+255

-76 -90 -160-238-212

-101

-38

+30

-49

+45+34

+32

+6+17

+16

+17+1

-3

-24

-29

-16

-17

-16

-49-16

U.S. -504814 below 2001-02 utilization

-43

Basis Implications!

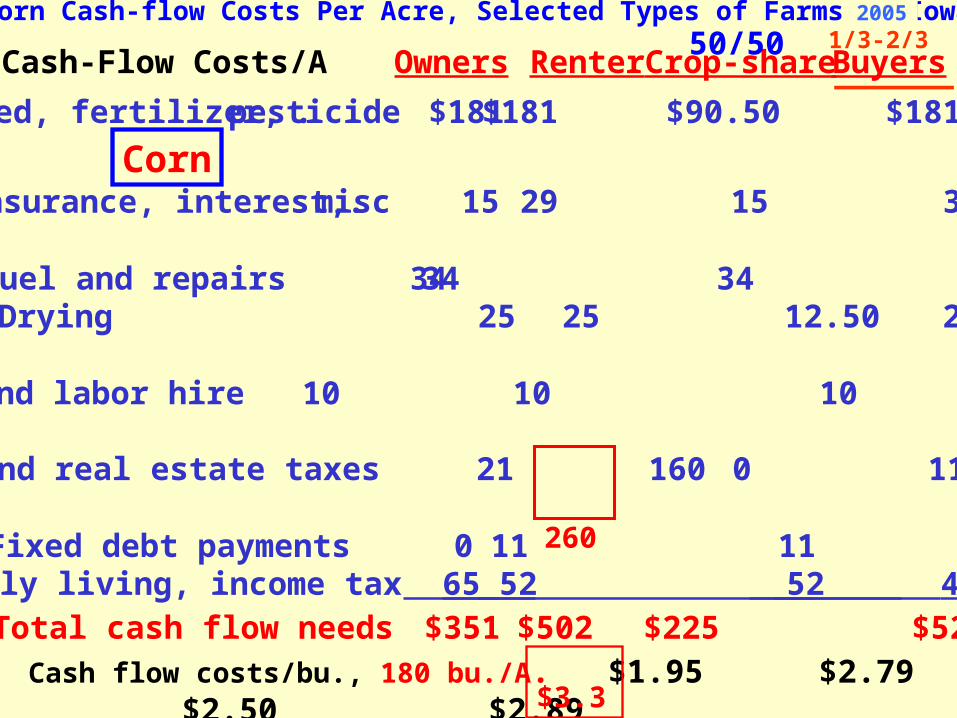

Cash-Flow Costs/A Owners Renter Crop-share Buyers

Seed, fertilizer, pesticide. $181 $181 $90.50 $181

Insurance, interest, misc. 15 29 15 36

Fuel and repairs 34 34 34 34Drying 25 25 12.50 25

Custom hire and labor hire 10 10 10 10

Rent and real estate taxes 21 160 0 115

Fixed debt payments 0 11 11 74Family living, income tax 65 52 52 45

Cash flow costs/bu., 180 bu./A. $1.95 $2.79 $2.50 $2.89Total cash flow needs

$351

$502

$225 $520

Table 1. Corn Cash-flow Costs Per Acre, Selected Types of Farms in Iowa, 20041/3-2/350/50

Corn

2005

260

$3.34

Implications of Emerging Energy Market• A lot more corn acres will be needed• Corn prices: increasingly volatile & weather-

sensitive• Basis opportunities will be greater• More storage, handling capacity needed • Winter & spring 2006-07: look for periods of

higher corn, SB prices, strong basis• Cautions about selling 2008 and later crops• Corn, biodiesel to pull bean prices up• Options may be useful in managing risks• Rent & Land Value Implications

Should you shift bean acres to corn?

• Market says yes

• How much yield drag?

• Impacts of shorter planting & harvest seasons?

• Ability to move, handle, & store more corn?

• Soil types?

• Availability of top corn seed varieties?

Go Slow in Pricing 2008 & Beyond,Especially in corn

• Prices are low relative to 2007 & new ethanol plant capacity

• Potentially explosive market with weather problems

• Uncertainty on some pricing tools in extreme mkt. volatility

Corn Prices, 2007 & Beyond2/22/07

• Dec. ’07 $4.27• Mar. ’08 4.34• Jul. ’08 4.37• Dec. ’08 3.98• Jul. ’09 4.03 • Dec. ’09 3.84• Jul. ‘10 3.88• Dec. ’10 3.72

Spreads: Narrow

Prices: low relative to likely ethanol demand & acreage needs

Concerns: 2008 & Beyond

• Potential explosive weather market• Some “New Generation” contracts

haven’t been tested in that type of market -- especially those with options sales

• With explosive market, does fine print expose farmer to margin calls?

• Could some companies exceed margin borrowing ability?

What Could Change These Prospects?

• Accelerated corn yield increases• Crude oil price collapse• Break-through in economical biomass

conversion• Ethanol import tax removed – longer term

impacts• $0.51 blending credit reduced• Declining livestock feeding

Useable Bin Size

Cleaning Conveyer Systems

Overview of Grain Marketing• Importing port: Wilmington, N.C.• The world markets

– Major grain importing countries

– Import systems & infrastructure

– Major grain exporting countries

– Ocean freight (N.Y. Journal of Commerce)

– GMO trends & preferences

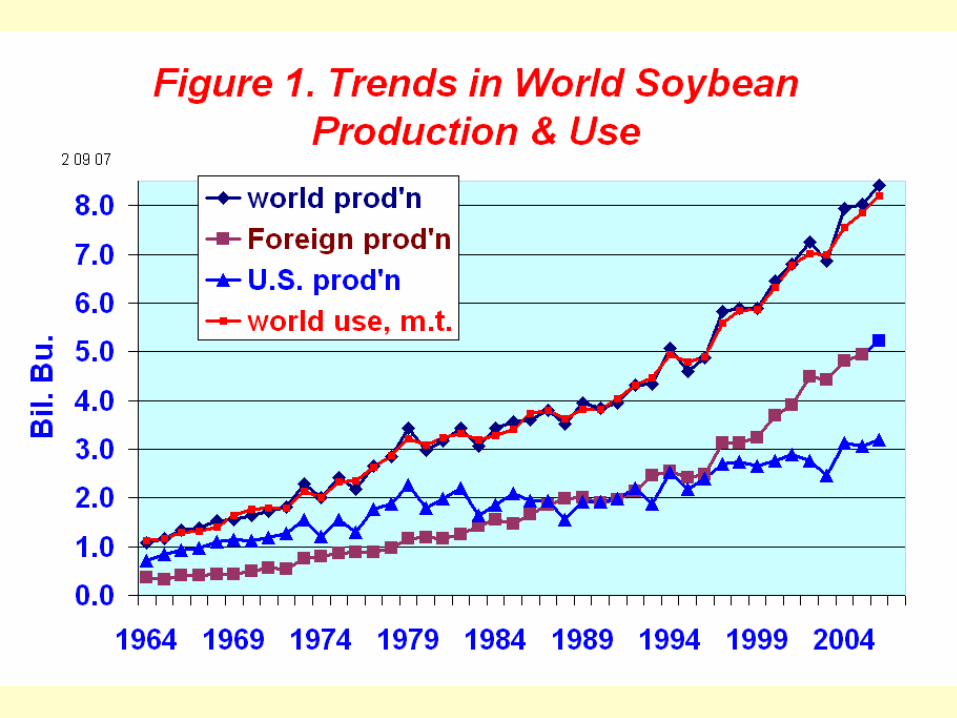

– Trends in foreign production & use

– Trade agreements: NAFTA, WTO, possible Latin American agreement

– Foreign inspection & grading

Have currencies recovered% Chg. Feb. 2003 vs. Jan. 1996

S S. Korea -51

S Hong Kong -0.9

S Japan -13.6

S Malaysia -49

S Indonesia -285

S India -33

S Argentina -218

S China +0.1

S Russia -576

S Philippines -106

S Taiwan -27

S Thailand -70

S Brazil -255

S Mexico -46

EU Euro -17

Only 2.7 mil. soy A. in highest-risk S.E. U.S.

Estimated Asian Rust Risk

% of years out of 30 that climatic conditions are expected to support Asian soy rust

Overview of Grain Marketing• World futures markets (Price Discovery)

– Chicago:corn, soft red wheat, soybeans, oats, rice

– Kansas City: hard red winter wheat

– Minneapolis: hard spring and hard white wheat, Corn & Soybean cash index markets

– Tokyo: GMO & non-GMO soybeans, corn

– Various other futures markets: Argentina, Brazil, China, Europe

– Foreign exchange futures

For March 23 Class

• Read Chapters 1 and 3 in Managing Risks and Profits, also look at Chap. 6.

• Dr. Steve Johnson, ISU Extension Management Specialist from Des Moines will teach the next two class sessions

• Focus will be on a student-participation workshop called “Winning the Game” in which you develop a grain marketing plan