economics 111.3 winter 14 march 7 th, 2014 lecture 20 ch. 10 (up to p. 231) and ch. 11

TRANSCRIPT

Economics 111.3 Winter 14

March 7th, 2014Lecture 20

Ch. 10 (up to p. 231)and Ch. 11

Firms Maximize Profit

• Profit is the difference between total revenue and total cost.

Profit = Total revenue – Total cost

Profit = Total revenue –Economic cost

Profit is the difference between total revenue and total cost.Profit = Total revenue – Total cost

Profit = Total revenue –Economic cost

• ECONOMIC COST of any resource is the value or worth it would have in its best alternative use

• FIRM’S ECONOMIC COST – those payments a firm must make, or incomes it must provide, to resource suppliers to attract the resources away from alternative production

opportunities.

Economic costs are the sum of

Explicit Costs• Money payments a firm must

make to non-owners of the firm for the resources they supplied.

Implicit Costs• Opportunity costs of firm’s own

resources or money payments the self-employed resources could have earned in their best alternative use.

Implicit Costs: examples• The firm’s opportunity cost of using the capital it owns is called the

implicit rental rate of capital

• The implicit rental rate (of capital) is the rental income that the firm forgoes by using its own capital and not renting it to another firm. The firm implicitly rents the capital from itself.

• The implicit rental rate of capital is made up of

– 1. Economic depreciation– 2. Interest forgone (rental income forgone) – Economic depreciation is the change in the market value of capital

over a given period.– Interest forgone is the return on the funds used to acquire the capital.

The same as the opportunity cost to the firm of using its own capital.

Implicit Costs: examples, cont’dA firm’s owner often supplies entrepreneurial ability, and also works for the firm. The opportunity cost of the labour supplied is the income that the owner could have earned in the best alternative job.– The return to entrepreneurship is

profit.– The profit that an entrepreneur

can expect to receive on average is called normal profit.

– Normal profit is the cost of entrepreneurship and is a cost of production.

• Normal profit is the average return for supplying entrepreneurial ability, and is an opportunity cost to the firm.

• Positive Economic Profit is earned when the return to entrepreneurial ability is greater than normal

• Negative Economic Profit (Loss) is made when the return to entrepreneurial ability is less than normal

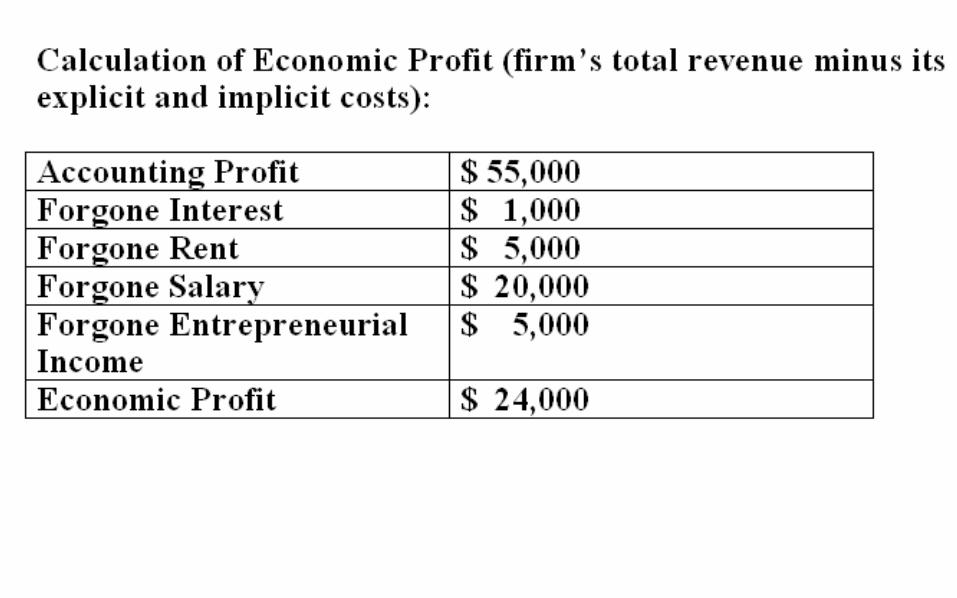

EconomicProfits

Implicit costs(including a

normal profit)

ExplicitCosts

Accountingcosts (explicit

costs only)

AccountingProfits

Ec

on

om

ic (

op

po

rtu

nit

y) C

os

ts

TotalRevenue

Profits to anEconomist

Profits to anAccountant

The Long Run and the Short Run

• Long Run – a period of time long enough to enable producers to change the quantity of all resources they employ

• In the Long Run– By definition, the firm can vary the

inputs as much as it wants. – All inputs are variable.

The Long Run and the Short Run

• Short Run is a period of time in which producers are able to change the quantities of some but not all the resources they employ

• In the short run:– Flexibility is limited.– Some factors of production cannot be

changed.– Generally, the production facility (“the

plant”) is fixed in the short run

Short-Run Production Relationship

• Total product (TP or Q) is the number of units of the good or service produced by a different number of workers.

• Marginal product is the additional output that will result from an additional worker, other inputs remaining constant.

Short-Run Production Relationship

Average product (the same as labour productivity) is calculated by dividing total output by the number of workers who produced it.