economics 306 a01: international economicsweb.uvic.ca/~bscarfe/international economics.pdf · ·...

TRANSCRIPT

Economics 306 – A01: International Economics

Summer term 2008: MTWRF 10:30-12:30 in CLEA311

Instructor: Brian L. Scarfe

Business telephone: 360-0300; e-mail: [email protected]

Office hours: MTWRF 9:15-10:15 in BEC 328; tel: 721-6520

Required Text: Paul R. Krugman and Maurice Obstfeld, International Economics:

Theory and Policy, eighth edition, Addison-Wesley, 2008, ISBN

0-321-49304-4

Given the condensed nature of summer session courses, we will only be able to cover the

main highlights of the International Economics syllabus. The course will move quickly

through the following topics. Students are strongly advised to keep their reading of the

textbook and lecture notes on pace.

Lecture outline: Text chapters

May 12-16: Part One: International Trade Theory (5 classes) Ch. 1-7

May 12: Introduction and Overview: Main Themes, Gravity Model Ch. 1 and 2

May 13: Comparative Advantage: the Ricardian Model Ch. 3

May 14: The Heckscher-Ohlin Factor Proportions Model Ch. 4

May 15: The Standard Trade Model: Growth, Terms of Trade Ch. 5

May 16: Economies of Scale, Intra-Industry Trade and Factor Mobility Ch. 6 and 7

May 20-22: Part Two: International Trade Policy (3 classes) Ch. 8-11

May 20: Instruments of Trade Policy: Tariffs Ch. 8

May 21: Other Instruments of Trade Policy: Worked Examples Ch. 9

May 22: Free Trade versus Protectionism: Customs Unions Ch. 10 and 11

May 23 (Friday): Midterm Examination (40 marks)

May 26-29: Part Three: Exchange Rates and Open-Economy

Macroeconomics (4 classes) Ch. 12-17

May 26: The Balance of Payments and Exchange Rates Ch. 12 and 13

May 27: The Asset Approach: Money, Interest Rates and Exchange Rates Ch. 14

May 28: Real Exchange Rates and Purchasing Power Parity Ch. 15

May 29: Macro-Economic Adjustment under Flexible Exchange Rates:

The Marshall-Lerner Condition and the Current Account Ch. 16

May 30-June 3: Part Four: International Macroeconomic Policy

(3 classes) Ch. 18-22

May 30: Fixed Exchange Rates and Macro-Economic Adjustment Ch. 17 and 18

June 2: External and Internal Balance: Exchange Rate Regimes and

Optimal Currency Areas Ch. 19 and 20

June 3: International Capital Markets and International Debt Problems Ch. 21 and 22

June 4 (Wednesday): Final Examination (60 marks)

Examinations and Grading Equivalencies:

Midterm examination (1 hr, 45 min): 40% Final examination (1 hr, 45 min): 60%

A+ = 90-100% A = 85-89% A- = 80-84% B+ = 75-79%

B = 70-74% B- = 65-69% C+ = 60-64% C = 55-59%

D = 50-54% F = 0-49%

Plagiarism and cheating: Students are expected to observe the same standards of scholarly

integrity as their academic and professional counterparts. Students who are found to have

engaged in unethical academic behaviour, including the practices described on pages 31-32

of the calendar, are subject to penalty by the University.

Inclusivity and diversity: The University of Victoria is committed to providing an

environment that affirms and promotes the dignity of human beings of diverse backgrounds

and needs.

Workshop Questions: Workshop questions will be taken up in class from time to time.

Students are advised to work on these questions in advance of the workshops.

Workshop One, for in class discussion on Wednesday, May 14

This question is essentially similar to problems 1 to 5 on p. 52 of the textbook.

Two countries, Home and Foreign, trade apples and bananas in a Ricardian trade world.

Home has 1,200 units of labour available, and requires 3 units of labour to produce one

tonne of apples and 2 units of labour to produce one tonne of bananas. Foreign has 800

units of labour available, and requires 5 units of labour to produce one tonne of apples and

1 unit of labour to produce one tonne of bananas.

(a) Construct graphically the world relative supply curve which relates the relative price of

apples to the relative quantity of apples produced.

(b) On the same graph, draw the world relative demand curve under the assumption that (in

both countries) expenditure is equally divided between the two goods, so that p(A) Q(A) =

p(B) Q(B), where p(A) and p(B) are the prices of apples and bananas, and Q(A) and Q(B)

are the overall quantities of apples and bananas produced (and consumed), respectively.

(c) Calculate the values of p(A)/p(B), Q(A) and Q(B) in trading equilibrium.

(d) Based upon comparative advantage theory, which country exports apples (how many

tonnes?), and which country exports bananas (how many tonnes?), in trading equilibrium?

(e) Calculate the increased volumes of apples and bananas that become available in trading

equilibrium when compared with the pre-trade situation, and thereby demonstrate that there

are consumption gains from trade (how are these gains shared between the two countries?).

Answer Guide: Workshop One

(a) The relative supply curve is horizontal at p(A)/p(B) = 3/2 (the relative cost ratio in

Home), has a vertical section at Q(A)/Q(B) = ½ (when all Home labour is allocated to

apples, and all Foreign labour is allocated to bananas), and has a further horizontal section

at p(A)/p(B) = 5/1 (the relative cost ratio in Foreign).

(b) The relative demand curve is a rectangular hyperbola which intersects the relative

supply curve in the vertical section.

(c) In trading equilibrium, p(A)/p(B) = 2, Q(A) = 400 tonnes, and Q(B) = 800 tonnes.

(d) As expected from the theory of comparative advantage, Home will export apples and

Foreign will export bananas. If D(A) and D(B) are Home’s consumption of apples and

bananas, respectively, then p(A) D(A) = p(B) D(B) and p(A) [ 400 – D(A)] = p(B) D(B). It

follows that D(A) = 200, and D(B) = 400. Thus, Home will export 200 tonnes of apples in

exchange for 400 tonnes of bananas, which are imported from Foreign.

(e) However, in the pre-trade situation at a relative cost ratio of 3/2, Home produces 200

tonnes of apples and 300 tonnes of bananas, fully employing 1,200 units of labour. In the

pre-trade situation at a relative cost ratio of 5/1, Foreign produces 80 tonnes of apples and

400 tonnes of bananas, fully employing 800 units of labour. Free trade increases the

overall production of apples from 280 tonnes to 400 tonnes, with all of the additional 120

tonnes consumed by Foreign. Free trade also increases the overall production of bananas

from 700 tonnes to 800 tonnes, with all of the additional 100 tonnes consumed by Home.

Workshop Two, for in class discussion on Wednesday, May 21

A country imports 3 billion barrels of crude oil per year and domestically produces another

3 billion barrels of crude oil per year. The world price of crude oil is $18 per barrel.

Assuming linear schedules, economists estimate the price elasticity of domestic supply to

be 0.25 and the price elasticity of domestic demand to be - 0.10 in the neighbourhood of the

current equilibrium.

(a) Assuming that the world price of crude oil does not change when the country imposes a

$6 per barrel import duty on crude oil, determine the domestic price, and the three

quantities: domestic consumption, domestic production, and import volume after the

imposition of the import duty.

(b) Calculate the impact on producer surplus, consumer surplus, and government revenues.

Also calculate the net social benefits associated with the imposition of the import duty.

(c) and (d) Redo the calculations under (a) and (b) on the assumption that the reduction in

the country’s demand for crude oil reduces the world price by $2 per barrel.

(e) By how much does the “terms of trade effect” of the import duty offset the efficiency

losses (i.e., what are the net social benefits to the importing country)? If foreign exporters

also had standing, would overall welfare be increased?

Answer Guide: Workshop Two

(a) A small open economy is a price-taker for its imports in the world market place. Since

none of the tariff incidence can be shifted backwards to foreign producers, the whole

burden of an import tariff falls on domestic consumers. In this case, the domestic price of

crude oil rises by $6 per barrel from $18 to $24. The resulting change in domestic quantity

supplied is given by 0.25 x 3 x 6/18 = 0.25 bbls (billion barrels), resulting in 3.25 bbls

being the new quantity supplied. The resulting change in domestic quantity demanded is

given by – 0.10 x 6 x 6/18 = - 0.20 bbls, resulting in 5.80 bbls being the new quantity

demanded. As a result, imports fall by 0.45 bbls to 2.55 bbls.

(b) The positive effect on producer surplus is given by area a in the diagram. This area is

equal to (3 + 3.25) x 6/2 = $18.75 b. The negative effect on consumer surplus is given by

area a+b+c+d in the diagram. This area is equal to (6 + 5.80) x 6/2 = $35.40 b. The

positive effect on net government revenues is given by area c in the diagram. This area is

equal to (5.80 – 3.25) x 6 = $15.30 b.

The net social benefits associated with the imposition of the import duty are negative,

and equal in size to area b+d in the diagram. This deadweight loss of $1.35 b. is made up

of a combination of the production side efficiency loss, area b in the diagram, which is

equal to (3.25 – 3) x 6/2 = $0.75 b, and the consumption side efficiency loss, area d in the

diagram, which is equal to (6 – 5.80) x 6/2 = $0.60 b.

(c) When the economy is no longer a price-taker in the world market place for its crude oil

imports, and the world price falls by $2 per barrel in response to the imposition of the

import duty, the domestic price rises by only $4 per barrel. As a result, the quantities

supplied, demanded, and imported all need to be recalibrated. The new quantity supplied is

3 + 0.25 x 3 x 4/18 = 3.17 bbls. The new quantity demanded is 6 – 0.10 x 6 x 4/18 = 5.87

bbls. As a result, imports fall by only 0.30 bbls to 2.70 bbls.

(d) The change in producer surplus is equal to (3 + 3.17) x 4/2 = $12.33 b. The change in

consumer surplus is equal to - (6 + 5.87) x 4/2 = - $23.73 b. The change in government

revenues is equal to (5.87 – 3.17) x 6 = $16.20 b. Notice that only 2/3s of this revenue is

raised from domestic consumers, while the remaining 1/3 is raised from foreign producers.

Thus, there is a terms of trade gain of $5.40 b. Net social benefits are equal to $4.80 b.

(e) The producer and consumer side efficiency losses are, respectively, equal to (3.17 – 3) x

4/2 = $0.34 b. and (6 – 5.87) x 4/2 = $0.26 b. The terms of trade gain exceeds the

deadweight efficiency loss by $5.40 b. - $0.60 b. = $4.80 b. or by the net social benefits.

However, the terms of trade gain to the importing country implies a terms of trade loss to

foreign exporters, so that if these exporters had standing there would be an overall welfare

loss. This loss would consist of the producer side and consumer side efficiency losses in

the importing country and two similar losses in the exporting country.

Workshop Three, for in class discussion on Thursday, May 22

Work through questions 1-4 and 7 on pp. 201-2 of the Textbook

Answer Guide: Workshop Three

Question One:

The relevant diagram is Figure 8-4, as adapted in the attached schematic. Home’s import

demand schedule is D – S = 80 – 40P. In the absence of trade, the price of wheat in Home

would be $2 per bushel.

Question Two:

Foreign’s export supply schedule is S* - D* = - 40 + 40P. In the absence of trade, the price

of wheat in Foreign would be $1 per bushel. In free trade equilibrium, one must have D – S

= S* - D*, and thus that 80 – 40P = - 40 + 40P. It follows that the world equilibrium price

of wheat is P = $1.50 per bushel. Home produces 50 bushels of wheat, consumes 70

bushels, and imports 20 bushels from Foreign. Foreign produces 70 bushels of wheat,

consumes 50 bushels, and exports 20 bushels to Home.

Question Three:

Now suppose that Home places a specific duty of $0.50 on wheat imports. This creates a

wedge between the Home and Foreign wheat prices such that P(H) = P(F) + 0.50. When

Home’s import demand is now equated to Foreign’s export supply, one has 80 – 40P(H) =

-40 + 40[P(H) - 0.50]. This equation solves for P(H) = $1.75 per bushel of wheat, so that

P(F) = $1.25 per bushel. Home now produces 55 bushels of wheat, consumes 65 bushels,

and imports 10 bushels from Foreign. Foreign produces 65 bushels of wheat, consumes 55

bushels, and exports 10 bushels to Home. The volume of trade has been cut in half by the

imposition of the import duty, as illustrated in the attached diagram. The welfare

implications for Home and Foreign are as follows:

Welfare effects for Home

Gain in producer surplus: area a (50 + 55) x 0.25/2 = $13.125

Loss in consumer surplus: area a+b+c+d (65 + 70) x 0.25/2 = $16.875

Tariff revenue gain: area c+e (65 – 55) x 0.50 = $ 5.000

Net social benefit: area e-b-d = $ 1.250

Terms of trade gain: area e (65 – 55) x 0.25 = $ 2.500

Production efficiency loss: area b (55 – 50) x 0.25/2 = $ 0.625

Consumption efficiency loss: area d (70 – 65) x 0.25/2 = $ 0.625

Welfare effects for Foreign

Gain in consumer surplus: area a* (50 + 55) x 0.25/2 = $13.125

Loss in producer surplus: area a*+b*+c*+d* (65 + 70) x 0.25/2 = $16.875

Net social loss: area b*+c*+d* = $ 3.750

Term of trade loss: area c* = area e (65 – 55) x 0.25 = $ 2.500

Consumption efficiency loss: area b* (55 – 50) x 0.25/2 = $ 0.625

Production efficiency loss: area d* (70 – 65) x 0.25/2 = $ 0.625

World welfare implications

Net social loss: area b+d+b*+d* = $ 2.500

Although Home gains at the expense of Foreign when a tariff is imposed on wheat imports,

the distortion to the world market place generates a net social loss from a world perspective.

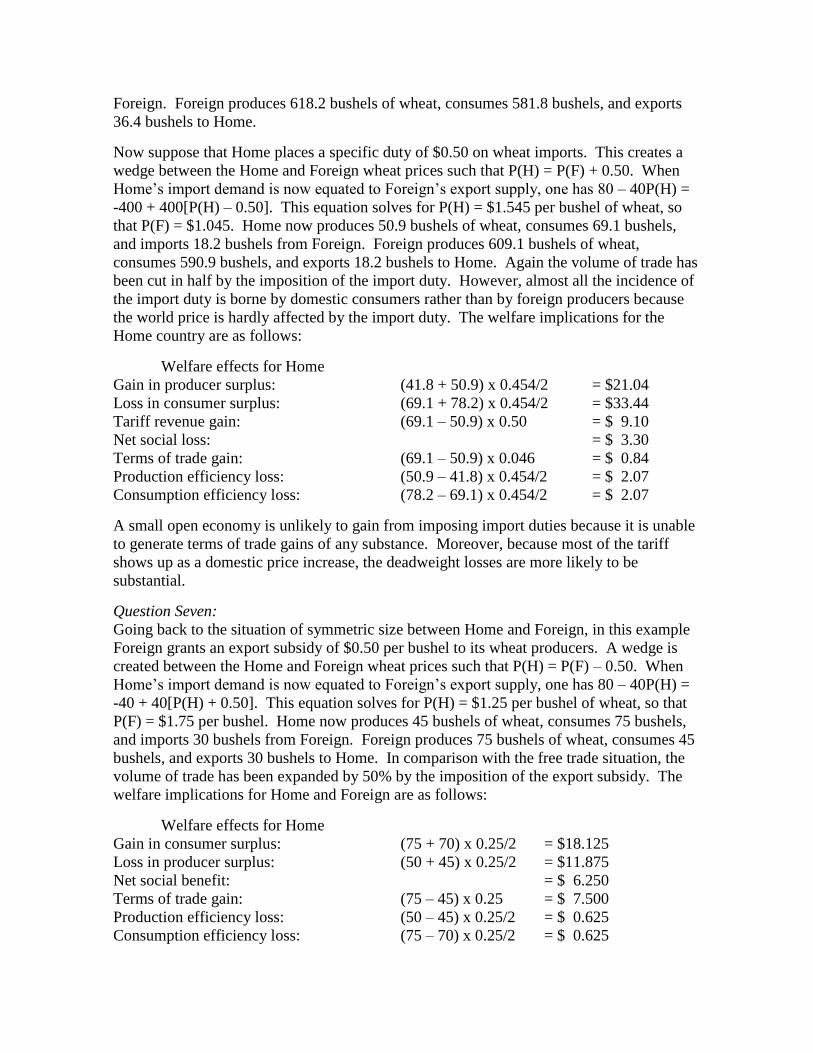

Question Four:

When Foreign is ten times as large as before, its export supply function becomes S* - D* =

- 400 + 400P. In the absence of trade, the price of wheat in Foreign would be $1 per bushel.

In free trade equilibrium, one must have D – S = S* - D*, and thus that 80 – 40P = - 400 +

400P. It follows that the world equilibrium price of wheat is P = $1.091 per bushel. Home

produces 41.8 bushels of wheat, consumes 78.2 bushels, and imports 36.4 bushels from

Foreign. Foreign produces 618.2 bushels of wheat, consumes 581.8 bushels, and exports

36.4 bushels to Home.

Now suppose that Home places a specific duty of $0.50 on wheat imports. This creates a

wedge between the Home and Foreign wheat prices such that P(H) = P(F) + 0.50. When

Home’s import demand is now equated to Foreign’s export supply, one has 80 – 40P(H) =

-400 + 400[P(H) – 0.50]. This equation solves for P(H) = $1.545 per bushel of wheat, so

that P(F) = $1.045. Home now produces 50.9 bushels of wheat, consumes 69.1 bushels,

and imports 18.2 bushels from Foreign. Foreign produces 609.1 bushels of wheat,

consumes 590.9 bushels, and exports 18.2 bushels to Home. Again the volume of trade has

been cut in half by the imposition of the import duty. However, almost all the incidence of

the import duty is borne by domestic consumers rather than by foreign producers because

the world price is hardly affected by the import duty. The welfare implications for the

Home country are as follows:

Welfare effects for Home

Gain in producer surplus: (41.8 + 50.9) x 0.454/2 = $21.04

Loss in consumer surplus: (69.1 + 78.2) x 0.454/2 = $33.44

Tariff revenue gain: (69.1 – 50.9) x 0.50 = $ 9.10

Net social loss: = $ 3.30

Terms of trade gain: (69.1 – 50.9) x 0.046 = $ 0.84

Production efficiency loss: (50.9 – 41.8) x 0.454/2 = $ 2.07

Consumption efficiency loss: (78.2 – 69.1) x 0.454/2 = $ 2.07

A small open economy is unlikely to gain from imposing import duties because it is unable

to generate terms of trade gains of any substance. Moreover, because most of the tariff

shows up as a domestic price increase, the deadweight losses are more likely to be

substantial.

Question Seven:

Going back to the situation of symmetric size between Home and Foreign, in this example

Foreign grants an export subsidy of $0.50 per bushel to its wheat producers. A wedge is

created between the Home and Foreign wheat prices such that P(H) = P(F) – 0.50. When

Home’s import demand is now equated to Foreign’s export supply, one has 80 – 40P(H) =

-40 + 40[P(H) + 0.50]. This equation solves for P(H) = $1.25 per bushel of wheat, so that

P(F) = $1.75 per bushel. Home now produces 45 bushels of wheat, consumes 75 bushels,

and imports 30 bushels from Foreign. Foreign produces 75 bushels of wheat, consumes 45

bushels, and exports 30 bushels to Home. In comparison with the free trade situation, the

volume of trade has been expanded by 50% by the imposition of the export subsidy. The

welfare implications for Home and Foreign are as follows:

Welfare effects for Home

Gain in consumer surplus: (75 + 70) x 0.25/2 = $18.125

Loss in producer surplus: (50 + 45) x 0.25/2 = $11.875

Net social benefit: = $ 6.250

Terms of trade gain: (75 – 45) x 0.25 = $ 7.500

Production efficiency loss: (50 – 45) x 0.25/2 = $ 0.625

Consumption efficiency loss: (75 – 70) x 0.25/2 = $ 0.625

Welfare effects for Foreign

Gain in producer surplus: (75 + 70) x 0.25/2 = $18.125

Loss in consumer surplus: (50 + 45) x 0.25/2 = $11.875

Government subsidy outlay: (75 – 45) x 0.50 = $15.000

Net social loss: = $ 8.750

Terms of trade loss: (75 – 45) x 0.25 = $ 7.500

Consumption efficiency loss: (50 – 45) x 0.25/2 = $ 0.625

Production efficiency loss: (75 – 70) x 0.25/2 = $ 0.625

World welfare implications:

Net social loss: = $ 2.500

Although Home gains substantially at the expense of Foreign when a subsidy is granted on

wheat exports, the distortion to the world market place generates a net social loss from a

world perspective. It should, however, be noted that an export subsidy is a particularly

perverse form of industrial protection from the perspective of the subsidising country, in

large part because an export subsidy is costly to government and turns the terms of trade

against the subsidising country. The relevant diagram is Figure 8-11.

Workshop Four, for in class discussion on Wednesday, May 28

This assignment expands upon problem 6 on page 345 of the textbook.

Suppose that the US dollar interest rate and the pound sterling interest rate are the same, 5

percent per year, but that there is a risk premium of 1 percent associated with holding

sterling rather than US dollars over the year.

(a) What is the relationship (in percentage terms) between the current equilibrium

dollar/pound exchange rate and its expected future level?

(b) If the expected future exchange rate is $1.52 per pound, what is the equilibrium

dollar/pound (spot) exchange rate?

Now suppose that the expected future exchange rate, $1.52 US per pound, remains constant

as Britain’s interest rate rises to 10 percent per year.

(c) If the US interest rate also remains constant, what is the new equilibrium dollar/pound

exchange rate?

(d) What is the expected rate of return over the year from holding a sterling deposit in a

London bank?

Now suppose that the actual exchange rate at the end of the year turns out to be $1.55 US

per pound.

(e) By how much does the actual return over the year from holding a sterling deposit in

London exceed or fall short of the expected rate of return? Would the actual dollar/pound

exchange rate rise or fall if, in response to the falsification of their expectations, currency

traders adapted their view of the expected future exchange rate towards the observed year

end outcome of $1.55 US per pound?

Answer Guide: Workshop Four

(a) The relevant formula is the uncovered interest rate parity formula:

E = E(e) (1+R*) / (1+R) (1+q),

where E is the spot exchange rate in US dollars per pound, E(e) is the expected exchange

rate at the end of the year, R* is the pound interest rate per annum in London, R is the

dollar interest rate per annum in New York, and q is the risk premium on holding pounds

rather than US dollars. Thus, when R* = R = 5% and q = 1%, the pound must be expected

to appreciate by 1% per annum. That is, E(e) must exceed E by 1%.

(b) The equilibrium spot exchange rate would be $1.505 US per pound, consistent with an

expected pound appreciation of 1% per annum, given E(e) = $1.52 US per pound.

(c) If the expected exchange rate remains at $1.52 US per pound, and the pound interest

rate rises from 5% to 10%, then the uncovered interest parity formula is satisfied only if the

current exchange rate changes such that there is an expected appreciation of the dollar equal

to approximately 4%. More precisely, this will occur when the exchange rate rises to $1.58

US per pound (a depreciation of the US dollar against the pound).

(d) The expected rate of return over the year from holding a sterling deposit in a London

bank is 6% per annum, which is the US dollar interest rate in New York plus the sterling

risk premium.

(e) If the actual exchange rate at the end of the year is $1.55 US per pound, the actual return

on holding a sterling deposit in a London bank would be approximately 8%, which exceeds

the expected rate of return by 2%. If currency traders adapt their view of the expected

future exchange rate towards the observed year end outcome of $1.55 US per pound, the

dollar/pound exchange rate would appreciate.

Economics 306: International Economics: Lecture Notes

Course Overview

International economics involves the study of the issues arising from economic interactions

among sovereign nations. This study centres around seven main themes:

The gains from international trade

Explanations of the pattern of trade

Ricardian productivity differences

The Heckscher-Ohlin factor proportions model

The standard trade model

Product differentiation and scale economies

Technological convergence and capital mobility

The impact of protectionist devices

Import duties/tariffs

Export subsidies

Quantitative restrictions/quotas

Voluntary export restraints

Customs unions and free trade areas

The balance of payments

Export and import flows and the current account

Asset transactions and the capital account

Exchange reserves and official settlements balances

Exchange rate determination

The interest rate parity relationship

Real exchange rate movements

Terms of trade effects

Macroeconomic adjustment

Flexible exchange rate regimes

Fixed exchange rate regimes

Employment fluctuations and price inflation

International policy co-ordination

The international capital market

The first three themes focus on real transactions and flows of imports and exports in the

international trading system. The final four themes relate to international monetary

economics.

The volume of trade between any two countries depends positively upon their economic

size and negatively on the distance (and therefore the associated transportation costs)

between them, as captured by the log-linear gravity equation:

ln T(i,j) = ln A + a ln Y(i) + b ln Y(j) - c ln D(i,j) + u(i,j) ,

where T(i,j) is the total trade value (exports plus imports) between countries i and j, Y(i)

and Y(j) are the gross domestic products of countries i and j, respectively, D(i,j) is the

distance between the two countries (or their central trading hubs), u(i,j) is an error term, A

is a constant, and a, b and c are positive parameters (or regression coefficients).

The gravity model has also been used to demonstrate that borders matter. That is to say,

the intensities of economic exchange within and across national borders are remarkably

dissimilar. Economic linkages are much tighter within, than among, nation-states. For

example, if the model was applied to the trade of British Columbia with other Canadian

provinces and individual US states, it would under-predict BC’s actual trade with Canadian

provinces and over-predict BC’s actual trade with most US states. The opposite effects

would be observed for the trade of Washington State.

There are many reasons why borders matter. These reasons are associated with transactions

costs, differential access to information, institutional differences, separate currencies, home

biases in preferences, and various barriers to the free flow of trade across international

boundaries. While strong, the forces of globalization do not seem to lead to a borderless

world.

Part One: International Trade Theory

Ricardo’s model of comparative advantage

The fundamental concept on which the theory of international trade is based is the principle

of comparative advantage. This principle may be defined by the statement that trade will

be mutually advantageous whenever the relative prices of various commodities differ from

country to country before trade by an amount great enough to over-offset the costs of

transferring the commodities in question from one country to another. A country will

export those goods that it produces relatively cheaply before trade in exchange for imports

of those goods that it produces relatively expensively before trade. This process of

profitable exchange leads countries to specialise (not necessarily completely) in the

production of those commodities in which they have a comparative advantage. A country

has a comparative advantage in producing a good if the opportunity cost of producing that

good in terms of other goods is lower in that country than it is in other countries.

The theory of international trade suggests that there are basically three reasons why the

relative production costs of various commodities might differ among countries. These are

(a) different resource endowments, (b) different production functions, and (c) different

scales of output. The Ricardian model of comparative advantage focuses on the second of

these reasons and, in particular, differences in relative labour-productivities in different

activities. To export those commodities in the production of which labour-productivity is

relatively high in exchange for those whose production exhibits relatively low labour-

productivity results in a gain in real income for a trading country. Thus, there are gains to

be made from international trade.

Consider an economy with a finite supply of labour that produces and consumes two

commodities, wine and cheese. The production possibility frontier may be written as:

a(L,C) Q(C) + a(L,W) Q(W) < L,

where L is labour supply, Q(C) is cheese output (measured on the horizontal axis), Q(W) is

wine output (measured on the vertical axis), a(L,C) is the unit labour requirement in the

production of cheese, and a(L,W) is the unit labour requirement in the production of wine.

Notice that a(L,C) is the reciprocal of the productivity of labour in cheese production, and

a(L,W) is the reciprocal of the productivity of labour in wine production. The absolute

slope of the production possibility frontier is the opportunity cost of cheese in terms of

wine, namely a(L,C)/a(L,W), which measures the number of litres of wine the economy

would have to give up in order to produce an extra kilogram of cheese.

If our simple economy (called Home) produces both goods, then the relative price of cheese,

p(C)/p(W), is equal to the unit labour requirement ratio, a(L,C)/a(L,W). However, if the

relative price of cheese exceeds its opportunity cost, the economy will specialise in cheese

production, while if the relative price of cheese is less than its opportunity cost, the

economy will specialise in wine production.

Now introduce a second country, called Foreign, which also has a production possibility

frontier of the form:

a*(L*,C) Q*(C) + a*(L*,W) Q*(W) < L*,

where the *-notation refers to the foreign country. Now assume that a(L,C)/a(L,W) <

a*(L*,C)/a*(L*,W) or, equivalently, that a(L,C)/a*(L*,C) < a(L,W)/a*(L*,W). This

assumption implies that the production possibility frontier for Foreign is steeper than the

production possibility frontier for Home, that Foreign has a higher opportunity cost of

cheese production than Home, that Home’s relative productivity in cheese production is

higher than it is in wine production, that Home has a comparative advantage in cheese

production, and that if trade opens up between Home and Foreign, Home will export cheese

to Foreign while importing wine. Notice that all four labour requirement coefficients are

necessary to determine comparative advantage and the direction of trade.

Demonstrate trading equilibrium in terms of the relative price and quantity of cheese

produced and consumed. See text, diagram 3-3. Note that in trading equilibrium the

relative price of cheese, p(C)/p(W) is bounded by a(L,C)/a(L,W) and a*(L*,C)/a*(L*,W).

Demonstrate also that there are gains from trade. These gains are shared between Home

and Foreign except where one of the two countries does not completely specialise, and the

relative price of cheese remains equal to that country’s labour requirement ratio.

The gains from trade depend upon comparative advantage and not upon absolute advantage.

If Home has an absolute productivity advantage in the production of both goods, it will

have a higher wage rate than Foreign. Home’s relative wage rate, w/w*, will lie between

Home’s productivity advantage in its exported good and its productivity advantage in its

imported good. The competitive advantage of an industry depends not only on its

productivity relative to the foreign industry, but also on the domestic wage rate relative to

the foreign wage rate. Finally, if there are many possible goods, j = 1…n, Home will

export all those goods for which w a(L,j) < w* a(L*,j), and import all those goods for

which w a(L,j) > w* a(L*,j). Thus, if goods are ordered by the productivity ratios,

a(L*,j)/a(L,j), then w/w* will determine where along this ordering the cut will occur

between Home’s potential exports and Home’s potential imports. Home will have a cost

advantage in any good for which its relative productivity is higher than its relative wage,

and Foreign will have a cost advantage in the other goods. However, if transport costs are

introduced, some commodities will become non-traded goods.

The Heckscher-Ohlin factor proportions model

Whereas the Ricardian model of comparative advantage focuses on differences in

production functions and, more explicitly, on differences in labour productivity as an

explanation of trade patterns, the Heckscher-Ohlin model focuses on differences in factor

endowments. A country will export those commodities which use intensively its relatively

abundant factor. Underlying this model are two key assumptions: (a) goods may be

ordered unambiguously by factor- intensities, and (b) countries have different factor

endowments.

Let there be two factors of production, land (N) and labour (L), which can be used in the

production of food (F) and cloth (C). Food production is land-intensive relative to cloth

production, which is labour-intensive. That is to say, the ratio of labour to land used in the

production of cloth is higher than the ratio of labour to land used in the production of food.

Thus,

a(L,C)/a(N,C) > a(L,F)/a(N,F),

where a(i,j) refers to the amount of factor i that is used in the production of one unit of good

j, where i = labour (L) or land (N), and j = cloth (C) or food (F). There are now two

resource constraints, which may be written as:

a(L,C) Q(C) + a(L,F) Q(F) < L, and

a(N,C) Q(C) + a(N,F) Q(F) < N,

where Q(C) and Q(F) refer to the outputs of cloth and food, respectively.

If each of the a(i,j)’s were fixed technical coefficients, the production possibilities frontier

would consist of two straight lines, one representing the labour constraint and the other

representing the land constraint. There would be a kink in the production possibilities locus

where these two constraint functions intersect. However, if there is a choice of technique,

with the a(i,j)’s depending upon relative factor input prices, then the production

possibilities frontier will be a downwards sloping line which is convex outwards from the

origin. The opportunity cost of cloth in terms of food (the absolute slope of the production

possibilities frontier) increases as the economy produces more cloth and less food. An

increase in the relative price of cloth, p(C)/p(F), would generate such a shift in production

volumes. The maximisation of production value requires that the opportunity cost of cloth

production be equated to the relative price of cloth.

Although cost minimisation implies that both a(L,C)/a(N,C) and a(L,F)/a(N,F) will

decrease if the wage paid for labour (w) rises relative to the rental price of land (r), we will

continue to assume that a(L,C)/a(N,C) > a(L,F)/a(N,F). It follows that the relative price of

cloth, p(C)/p(F) will increase as w/r increases. This is because an increase in the cost of

labour has a larger impact on the price of cloth than it has on the price of food. Taken in

reverse, an increase in p(C)/p(F) will redistribute factor income towards labour.

An increase in the supply of labour will lead to a biased expansion of production

possibilities, with the production possibilities frontier shifting outwards much more

prominently in the direction of cloth production. Indeed, if relative prices remain constant,

full employment of both factors of production would require an increase in cloth production

and a decrease in food production. However, prices may not remain constant in the face of

the increased labour supply. In particular, the relative price of labour, w/r, and the relative

price of cloth, p(C)/p(F), may fall in response to the increased availability of both labour

and cloth. It follows that a country with a relatively abundant supply of labour is likely to

be relatively effective at (and, thus, have a comparative advantage in) producing labour-

intensive goods.

Now consider a trading situation in which Home has a higher ratio of labour to land than

does Foreign. Thus, L/N > L*/N*. Home’s production possibility frontier is skewed

towards cloth production, while Foreign’s is skewed towards food production. Assuming

that Home and Foreign have similar demand functions for cloth and food, the pre-trade

relative price of cloth will be lower in Home than in Foreign. Thus, Home will begin to

export cloth and import food from Foreign. Moreover, Home’s food import quantity will

be equal to p(C)/p(F) times Home’s cloth export quantity, a fundamental budget constraint.

Countries tend to export goods whose production is intensive in factors with which they are

abundantly endowed. International trade in goods indirectly implies the international

exchange of factor services. More labour is embodied in Home’s exports than in its

imports.

On the assumption that both countries continue to produce both goods, as relative product

prices converge, relative factor prices will also tend to converge. w/r will rise in Home,

while w*/r* will fall in Foreign, implying a tendency towards international factor price

equalisation. In reality, however, factor price equalisation may be less likely than it

appears to be within the Heckscher-Ohlin model because (a) complete specialisation may

occur if factor endowments are very different, (b) production functions may differ

internationally because of technological leads and lags, and because the quality of factor

inputs may differ across countries and/or productive sectors, (c) transportation costs and

other impediments to trade may prevent full commodity price equalisation, and (d) factor-

intensity orderings may not be unambiguous.

Although there will be overall income gains from international trade, there will be changes

in income distribution that imply gains for some factors and losses for others. In particular,

each country’s abundant factor will receive an income gain, while its scarce factor will

experience an income loss. However, since trade expands a country’s overall consumption

possibilities in the sense that it would be possible to increase consumption of both goods, it

is clear that the gainers could fully compensate the losers and still have left-over gains.

Despite income distribution effects, there are gains to be achieved from international trade.

The expansion of the economy’s choices implies that it is always possible to redistribute

income in such a way that everyone gains from trade. Free trade satisfies the normal cost-

benefit criterion. Nevertheless, arguments over trade policies often reflect distributional

concerns.

The standard trade model

The standard trade model is agnostic as to whether trade patterns are determined by

Ricardian differences in production technologies or by Heckscher-Ohlinian differences in

factor endowments. The standard trade model is built on four key relationships: (a) the

relationship between the production possibility frontier and the relative supply curve; (b)

the relationship between relative prices and relative demand; (c) the determination of world

equilibrium by world relative supply and world relative demand; and (d) the effect of the

terms of trade – the price of a country’s exports divided by the price of its imports – on a

nation’s welfare.

The standard trade model proceeds in diagrammatic terms; see text figures 5-3, which

illustrates a trading equilibrium with a given terms of trade, and 5-4, which illustrates the

effects of a change in the terms of trade. The production and consumption points for a

given country must lie on an iso-value line, or budget constraint line, of the form:

p(C) Q(C) + p(F) Q(F) = p(C) D(C) + p(F) D(F),

where D(C) and D(F) are, respectively, the quantities of cloth and food consumed. The

budget constraint line may also be written as:

p(F) [D(F) – Q(F)] = p(C) [ Q(C) – D(C)],

so that import value equals export value. An increase in the terms of trade increases a

country’s welfare, while a decline in the terms of trade reduces its welfare. In trading

equilibrium, relative prices are determined by the intersection of the upward-sloping world

relative supply curve for cloth with the downward-sloping world relative demand curve for

cloth.

Export-biased growth tends to worsen a growing country’s terms of trade, to the benefit of

the rest of the world; import-biased growth tends to improve a growing country’s terms of

trade at the rest of the world’s expense. Thus, the effects of economic growth on the

welfare of the Home country will normally be as follows:

(a) Export-biased growth in Home’s production possibilities: normally positive

(b) Import-biased growth in Home’s production possibilities: positive

(c) Export-biased growth in Foreign’s production possibilities: positive

(d) Import-biased growth in Foreign’s production possibilities: normally negative

An income transfer worsens the donor’s terms of trade if the donor has a higher propensity

to spend on its export good than the recipient, i.e. if there is home country preference in

demand functions, as may be implied by the presence of non-traded goods.

For large countries, import tariffs improve the country’s terms of trade. The welfare

consequences depend upon the net effect of the terms of trade improvement when offset by

the efficiency losses associated with tariff-induced price distortions. For small price-taker

countries, import tariffs may not affect the terms of trade, while tariff-induced price

distortions generate a welfare loss. Export subsidies normally lower a country’s terms of

trade as well as generating efficiency losses; welfare is unambiguously reduced. Trade

barriers also have impacts on the internal distribution of income.

The Heckscher-Ohlin model assumes that factors are mobile between production sectors

within countries, but internationally immobile. An alternative model, the specific factors

model, separates factor inputs into three types: (a) specific resource inputs that are

immobile between production sectors, (b) generic inputs such as labour which are mobile

between sectors, but immobile internationally, and (c) capital, which is assumed to be

mobile between countries. Assume that the economy has three sectors: (a) an export sector

uses a specific natural resource (such as timber lands), labour and capital to produce a

tradable output (such as lumber), (b) an import-competing sector uses labour and capital,

plus a different specific factor, as inputs, and (c) a non-traded goods sector uses labour and

capital, but no specific factors, to produce its output. The non-traded good is taken to be

the numeraire, so that its price is unity.

There are three exogenous world prices: (a) the price of the country’s exports, (b) the price

of the country’s imports, and (c) the world price of capital funds. There are three

endogenous prices: (a) the rental price of resource inputs, (b) the price the specific factor

used in the import-competing sector, and (c) the wage of labour. Exports are resource

intensive, while imports are intensive in the use of the alternative specific factor.

Within this model, an increase in the world price of capital funds will lower the domestic

wage rate, but have ambiguous impacts on the rental price of resource inputs and the price

of the specific factor used in the import-competing sector. This ambiguity can be sorted out

if more is specified about the capital/labour ratios that pertain to these sectors in

comparison to the non-traded goods sector. Resource production often involves capital-

intensive techniques so that, in this case, the rental price of resource inputs would fall in

response to an increase in the world price of capital funds.

Also within this model, an increase in the world price of a tradable commodity will have an

impact on the associated specific factor price which is magnified in proportional terms, but

will have no impact on the price of specific factors that do not enter the cost function for

the commodity, or on the price of a generic factor such as labour. Thus, changes in the

terms of trade (the relative price of the resource-related export commodity relative to the

price of imported goods) will have important effects on internal income distribution, and

especially on the welfare of specific factor owners, while changes in the world price of

capital funds will have important effects on labour income, as well as on the level of

employment if wage rates are inflexible.

Product differentiation and scale economies

The third explanation of trade patterns is economies of scale. Scale economies are an

important explanation of intra-industry trade, whereas factor endowments and

technological differences may explain inter-industry trade. Internal economies of scale

occur at the firm level, and give rise to imperfectly competitive markets. These markets

often exhibit product differentiation, with consumers benefiting from the variety of goods

that are made available through trade. External economies of scale occur at the industry

level and are largely based upon synergistic relationships among firms. These synergistic

relationships may involve (a) specialised suppliers, (b) labour market pooling, and (c)

knowledge spill-overs.

We turn first to a model involving internal economies of scale and monopolistic

competition. Assuming that the representative firm faces a downward-sloping but linear

demand curve, one has:

Q = S/n – bS(P – P*),

where Q is quantity demanded, P is the firm’s price, P* is average price charged by the

firm’s competitors, S is total industry sales or overall market size, n is the number of firms

in the industry, and b is a positive parameter which measures the responsiveness of the

firm’s sales to its own price, given S and P*. Now let a = S/n + bSP*. It follows that PQ =

(a – Q)Q / bS, and that MR = (a – 2Q)/bS = P – Q/bS, where MR is marginal revenue.

Assuming also that the representative firm experiences both fixed costs and constant

marginal costs, the firm’s average cost (AC) function may be written as:

AC = c + F/Q,

where F is fixed costs, Q is output, and c is marginal (and average variable) costs. Setting

MR = c to maximise profits, one discovers that:

P = c + (Q / bS).

With symmetry among firms so that P = P* and Q = S/n, this expression becomes:

P = c + 1 / bn.

The larger is the number of firms competing within the industry, the smaller will each

firm’s price be. Also, with symmetry among firms, average costs may be re-written as:

AC = c + nF/S.

The larger is the number of firms in the industry, the less will scale economies be exploited,

and the higher will average costs be. If there is free entry into the industry, profits will be

driven to zero, with P = AC. Industry equilibrium thus implies that 1/bn must be equated to

nF/S, so that the equilibrium number of firms in the industry is equal to the square root of

S/bF.

The division of labour is limited by the extent of the market. However, when trade is

opened up in a monopolistically competitive industry, overall market size expands. This

increases the number of firms that can be profitably sustained within the industry, permits

these firms to take advantage of more scale economies, lowers the prices of products, and

expands the variety of products available to consumers. Because of economies of scale,

neither country is able to produce the full range of manufactured products by itself; thus,

although both countries may produce some manufactures, they will be producing different

things. Two-way trade, or intra-industry trade, occurs in manufactured goods. Whereas

inter-industry trade reflects comparative advantage, either based on Ricardian technological

differences or Heckscher-Ohlinian factor endowments, intra-industry trade reflects

economies of scale. Although there are overall gains to be made from both kinds of trade,

intra-industry trade is much less likely than inter-industry trade to have significant effects

on the distribution of income among productive factors. Examples: the formation of the

European Common Market, and the North American Auto Pact of 1964.

Dumping is a form of international price discrimination which occurs in oligopolistic

industries. Dumping occurs when it is possible for a firm to segment its markets and

proceed to sell its products at a lower price in foreign markets than in domestic markets.

Since profit maximising price discrimination requires marginal revenue to be equated in all

markets in which the firm’s output is sold, the lower price should be charged in the market

where the elasticity of demand is higher. Because greater competition is likely to exist for

a firm’s products in foreign markets than in domestic markets, the elasticity of demand is

likely to be greater in the foreign market. In terms of the linear demand curve used

previously, where MR = P – Q/bS, the lower price would be charged where Q/bS is smaller.

Given home market preference, this is most likely to be the foreign market. Thus, firms

have an incentive to dump products in the foreign market whenever the responsiveness of

quantity sold to price is greater in that market than at home.

The US International Trade Administration regards dumping as an unfair trading practice,

and often assesses anti-dumping duties against foreign firms that are alleged to be dumping

products into the US market. However, in many cases anti-dumping duties, like the

countervailing duties that are applied in the case of alleged foreign subsidies, are really

another example of trade protection.

External economies are observed when industrial clustering leads to lower costs for all

firms within the cluster. The main reasons why costs might fall when similar firms cluster

together in one location relate to the emergence of specialised suppliers, to labour market

pooling, and to knowledge spill-overs – the diffusion of new technological ideas occurs

more quickly among firms which are in close proximity to each other. All three reasons

generate synergism among firms within the cluster. Example: Silicon Valley in California.

External economies give rise to first-mover advantages, and make it more difficult for

potential competitors in other locations to break into the market. Learning-by-doing effects,

where costs fall in response to cumulative output, give rise to the phenomenon of dynamic

increasing returns. Infant-industry protection is sometimes justified on the assumption that

costs will fall as experience rises.

Technological convergence and capital mobility

International factor mobility may be either a complement to, or a substitute for,

international trade in goods and services. If the basis for the international exchange of final

commodities resides in differences in factor endowments as in Heckscher-Ohlinian trade

theory, allowing these factors to move directly between countries obviates the need for

commodity trade. However, if the basis for trade lies in other reasons (technological

differences, as in Ricardian trade theory, increasing returns to scale, etc.) trade by itself will

tend to raise the return to factors used intensively in each nation’s export sector. Factor

mobility that responds to such differences adds a factor endowment basis for expanded

commodity trade.

Sometimes the international mobility of factors is a prerequisite for the development of

commodity trade, particularly where extractive industries are concerned. On the other hand,

deliberate protectionist policies may reduce trade significantly if they encourage the flow of

capital to avoid the tariff barriers. Thus, foreign investment may serve to expand

production of a nation’s exportables, or serve to encourage production of importables.

International factor mobility responds to perceived differences in factor returns among

countries, and leads to the convergence of factor prices. International factor mobility also

increases world income, but there may be important distributional consequences. In

general, there are more important barriers to international factor mobility, perhaps with the

exception of capital mobility, than there are to the movement of goods and services in

international trade. There is limited mobility of labour between countries, and virtually no

mobility of land-based natural resources.

International capital mobility reflects borrowing and lending transactions between countries,

and gives rise to inter-temporal exchanges. Real interest rates are the key price variable

which influences these transactions. The number of units of future consumption that must

be foregone to obtain an additional unit of present consumption is equal to 1+r, where r is

the real interest rate. Alternatively, the relative price of future consumption is 1/(1+r).

Countries with a relatively low rate of interest will export capital by lending to foreign

countries. Countries with a relatively high rate of interest will import capital by borrowing.

Look at relevant diagrams.

Multinational enterprises choose to locate their operations in more than one country, and by

so doing are involved in the transfer of their core competencies and/or proprietary

technologies for use in other countries. They are, therefore, an important vehicle for

international technology transfers.

Technological convergence may be said to occur whenever the underlying technology of a

“less advanced economy” becomes more similar to that of a “more advanced economy”

through a process of technological diffusion. Recent empirical research related to (a) the

explanation of observed differences in postwar growth rates among advanced economies,

and (b) the explanation of observed changes in the pattern of international trade among

advanced economies in the postwar period, seems to suggest the following broad

generalisation, namely, that it is difficult, if not impossible, to explain either the differences

in growth rates or the changes in trade patterns if one starts from the supposition that, sector

by sector, these economies employ the same average levels of technological know-how at

any given point of time.

When the production function in any given productive sector is defined in terms of the

average degree of application of technological knowledge to production processes within

the sector, this production function will generally be observed to differ from one economy

to another. But these differences in sectoral production functions (or technological leads

and lags) among advanced economies do not remain unchanged through time. Indeed, the

effects generated by intertemporal changes in these sectoral differences are, in combination,

largely responsible for the observed differences in overall rates of economic growth and for

the observed changes in broad trading patterns.

This broad generalisation suggests that the comparative advantage positions underlying the

exchange of manufactured products are largely acquired through the combined processes of

technological change and capital accumulation. These processes are at the same time

responsible for the determination of overall rates of economic growth. Moreover, just as

comparative advantage positions can be acquired they can also be lost as the application of

technological knowledge becomes more widely diffused among trading economies. While

an original innovation may lead to a short term or medium term technological advantage,

the ensuing diffusion process tends to reduce this advantage. Such a diffusion process may

be called technological convergence.

The process of technological convergence involves the diffusion of the usage of “best-

practice techniques” across the various producers of a particular commodity, in whichever

countries these producers are located. This diffusion process normally implies some degree

of “anti-import bias” in the pattern of productivity improvements introduced by countries

which are, on the whole, importers of new techniques of production, and makes it

progressively more difficult for a country which is largely an exporter of new production

techniques to continue exporting relatively large quantities of commodities in the

production of which initially possesses a comparative advantage. Illustrate why this is

likely to be the case when diffusion processes lead to “catching up”.

Economies that grow rapidly through the reduction of an existing productivity gap

experience higher rates of return on capital investment and higher rates of capital

accumulation than a slower growing economy with a higher level of productivity. If long

term direct foreign investment responds to relative rates of return, capital will flow from a

slower growing more advanced economy to faster growing less advanced economies, this

flow tending to equalise rates of return among the countries under consideration.

International technological diffusion and international capital mobility go hand in hand,

with a major vehicle being the multinational enterprise.

In addition to the “anti-import bias” problem associated with the process of technological

convergence, an initial technological leader may also be faced with a transfer problem

associated with its long term capital outflows. The appropriate response to these two

related problems would be an overall reduction in the real exchange rate (the external value

of the technological leader’s currency adjusted for relative price levels). However,

eventually the growth rates of “catch-up” economies will slow down from their higher

levels as the process of technological convergence runs its course.

Part Two: International Trade Policy

Import duties/tariffs

A tariff is a tax levied when a good is imported. Specific duties, taxes or tariffs differ from

ad valorem duties. A specific duty involves a fixed charge for each unit of goods imported,

and tends to be independent of the point along the transportation and distribution network

at which the duty is levied. Ad valorem duties involve a percentage charge on the value of

the imported goods, and their impact depends upon where along the transportation and

distribution network the duty is levied. The cyclical impact of specific tariffs also differs

from the cyclical impact of ad valorem tariffs. An ad valorem duty that raises the same

amount of revenues as a specific duty in a normal or average market will raise larger

revenues in a buoyant market where goods prices are high, and smaller revenues in a down

market where goods prices are low. The burden of ad valorem duties on the market place is

higher than that of specific duties in buoyant markets, but is smaller than that of specific

duties in down markets. The distribution of the burden across high value products and low

value products within the same commodity class also differs between specific tariffs and ad

valorem tariffs. A blended tariff system could have the form T = a + bP, where T refers to

tariff revenues per unit, P refers to product price, and the parameters (a and b) refer to the

specific and ad valorem components, respectively. The blended tariff rate, t = T/P, would

then be equal to b + a/P.

If there are no impediments to trade, the equation of world demand to world supply

establishes an equilibrium price. In a two country world, equilibrium implies that the sum

of Home and Foreign demand must be equal to the sum of Home and Foreign supply. Thus,

the world market price is established where Home’s import demand (Home demand minus

Home supply) is equal to Foreign’s export supply (Foreign supply minus Foreign demand).

See diagrams 8-1, 8-2 and 8-3.

When Home implements an import tariff, a wedge is created between the Home and

Foreign market prices. The import tariff raises the price in Home and (except where Home

is a small price-taking country) lowers the price in Foreign. The volume traded declines.

See diagrams 8-4 and 8-5. The incidence or burden of the tariff is shared between Home

and Foreign in a manner which depends upon the elasticity of Home import demand and

the elasticity of Foreign export supply. There are also deadweight efficiency losses

associated with tariff distortions. As a result, import tariffs fail the cost-benefit test from a

world point of view. Home producers and Foreign consumers gain while Home consumers

and Foreign producers lose, but the overall net gain is negative. This negative effect is

exacerbated if Foreign retaliates to Home’s tariff by imposing protective tariffs on its

imports from Home. On the other hand, there are gains from trade from a world

perspective if one moves from tariff protection to free trade.

Whether or not Home gains or loses from implementing an import tariff depends upon the

size of the deadweight efficiency losses it incurs in relationship to the extent to which the

burden of the tariff is passed back to Foreign exporters (the terms of trade gain). Using a

cost-benefit analysis framework, Home’s net social benefits (NSB) from tariff

implementation are equal to NSB = dCS + dPS + dGR, where dCS is the change in

consumer surplus, dPS is the change in producer surplus, and dGR is the change in

government revenues associated with the tariff. The consumer surplus loss will inevitably

be larger than the producer surplus gain, and the government revenue gain may or may not

offset the difference. A small open economy will generally lose by imposing a tariff on

imports, because there will be little or no terms of trade gain. See diagrams 8-9 and 8-10.

Work through examples, including the effects of the imposition of tariffs on petroleum

imports and the impact of US countervailing duties on Canadian softwood lumber. In this

context, discuss the concept of effective protection, and why Canada needs to maintain log

export controls as long as the US continues to impose tariffs on softwood lumber imports.

Export subsidies

Export subsidies always fail the cost-benefit criterion. The wedge created between

domestic and foreign prices is associated with the diversion of production to the foreign

market. As a result, the exporting country creates a consumer surplus loss for domestic

consumers and a producer surplus gain for domestic producers, accompanied by a drain

from government revenues. There are again deadweight losses from the subsidy distortion,

to which must be added a terms of trade loss. See diagram 8-11.

On the other hand, an export tax can generate a terms of trade gain for an exporting country.

The effects of an export tax are similar to the effects of an import duty, but with the

important difference that the tax revenues accrue to the government of the exporting

country rather than to the government of the importing country.

Quantitative restrictions/quotas

Like a tariff, an import quota raises the domestic price of the imported good. However,

rather than generating tariff revenues for government, an import quota generates quota rents

for those companies who hold import licences, or quota rights. If these licences are held by

domestic importers, then the importing country may experience a gain or a loss from

imposing quotas depending upon the balance between efficiency losses and terms of trade

gains. However, if the import licences are held by foreign exporters, the importing country

suffers a net loss from a cost-benefit perspective. See diagram 8-13.

Voluntary export restraints

Voluntary export restraints are usually imposed at the request of an importing country.

However, from a cost-benefit perspective the request makes little sense because the

importing country suffers a terms of trade loss as well as the usual efficiency losses from

market distortion. The exporting country may enjoy a terms of trade gain, with its

exporters enjoying rents that arise from the restraints. Indeed, voluntary export restraints

operate like import quotas where the quota rights (or import licences) are assigned to

foreign exporters. As one form of managed trade, multilateral export restraints are often

called orderly marketing agreements.

Other trade policy instruments include local content requirements and national procurement,

regulated product standards and red-tape barriers, and export credit subsidies. The

summary table, 8-1, should be studied in detail. Although the effects on national welfare of

tariffs and import quotas are ambiguous (except for small countries where national welfare

falls), the effects on national welfare of export subsidies and voluntary export restraints are

negative. From a cost-benefit perspective, free trade should be preferred to protectionism.

Moreover, when monopoly power exists within a country, free trade can help to reduce this

power. Free trade is therefore a useful form of industrial policy.

Free trade versus protectionism

The case for free trade is based upon (a) economic efficiency gains through the harnessing

a comparative advantage and the avoidance of market distortions, (b) scale economies,

longer production runs, and enhanced product variety, (c) greater opportunities for learning

and innovation, and (d) the fact that retaliatory trade protection is a negative sum game.

The case against free trade is based upon (a) the terms of trade argument (optimum tariff

argument) for protection, (b) domestic market failure (second best arguments, including

infant industry arguments for protection), and (c) income distribution concerns. However,

it is always preferable to deal with market failures as directly as possible, because indirect

policy responses lead to unintended distortions of incentives elsewhere in the economy.

Thus, trade policies justified by domestic market failure are never the most efficient

response; they are always “second best” rather than “first best” policies. Indeed, most

deviations from free trade are adopted not because their benefits exceed their costs but

because the public fails to understand their true cost.

Movements towards free trade normally require international negotiation in which import

protection is traded off for export access, and the avoidance of trade wars. This process

mobilises the collective support of exporters and the general public to overcome the

concentrated lobbies of import competing industries and the workers they employ.

Customs unions and free trade areas

Trade liberalisation rounds under the General Agreement of Tariffs and Trade (GATT), and

now the World Trade Organisation (WTO) normally involve multilateral tariff reductions

based upon most favoured nation clauses. However, preferential trading agreements in the

form of customs unions and free trade areas are also permitted under the GATT/WTO.

Whereas a customs union involves a common set of external tariffs, which must be

determined by prior negotiation, a free trade area does not. The management of a free trade

area therefore requires a elaborate set of “rules of origin”. The European Community is a

customs union, while NAFTA is a free trade area. Preferential trading agreements involve

trade creation among the members of the customs union or free trade area, and trade

diversion from non-members of the preferential trading agreement. Welfare implications

involve balancing the gains from trade creation against the losses from trade diversion. The

gains are likely to exceed the losses if most of the trade creation effects involve intra-

industry trade based upon economies of scale, longer production runs, and increased

consumer choice.

Miscellaneous trade issues

The rationale for strategic trade policy in industrialised countries is based upon two kinds

of market failure. One of these is the inability of firms in high-technology industries to

capture or appropriate the externality benefits of contributions to knowledge that spill-over

to other firms. The other is the presence of monopoly profits in highly concentrated

oligopolistic firms. However, entry deterrence (i.e. a head start) seems to be required if a

subsidy is to generate an addition to oligopoly profits that exceed the subsidy, and the

whole strategy risks retaliatory activity (e.g. Boeing vs. Airbus, Embraer vs Bombardier).

Import-substituting industrialisation based upon the infant industry argument, which was

popular in developing countries during the first 30 postwar years, has largely been

superseded by export-orientated industrialisation during later years due to the example set

by a group of high performance Asian economies. The pre-conditions for rapid growth

through technological convergence appear to be: (a) the existence of a productivity gap to

be exploited, (b) the ability to invest in new capital equipment of the latest vintage (which

itself requires a high rate of savings), (c) the existence of a reasonable infrastructure of

social overhead facilities, including educational facilities, (d) a labour force with a

reasonably high level of education and skills, (e) the ability to release labour resources from

less productive sectors, including agriculture, (f) wage rates and labour income at a level

which creates a market for mass produced goods, (g) alert entrepreneurs and dynamic

management, and (h) respect for international comparative advantages and openness to

international trade. A threshold level of per capita income may be required before take-off

can occur.

The effects of globalisation on the real incomes of low-wage workers in both developing

and industrialised countries have given rise to various concerns. However, some of these

concerns are not well founded in economic logic. In developing countries, low-wage

workers would be worse off without the ability to work in growing export industries (e.g.

Mexico’s maquiladoras). In industrialised countries, it is technological change rather than

international trade which appears to be the main driving force behind labour market duality

(high wage, high skilled jobs versus low wage, low skilled jobs). Debate continues to

occur over whether labour standards and environmental standards should be included as a

component in trade negotiations.

Part Three: Exchange Rates and Open-Economy Macroeconomics

Export and import flows and the current account of the balance of payments

The national income accounting identity for an open economy may be written as:

Y = C + I + G + EX – IM,

where Y stands for gross national product, I for investment, G for government expenditure,

EX for exports and IM for imports. Within this identity, the difference between the value

of goods and services that are exported, EX, and the value of goods and services that are

imported, IM, equals the current account balance, CA = EX – IM. If EX > IM, the current

account is said to be in surplus, while if EX < IM, the current account is said to be in deficit.

A current account deficit implies that domestic absorption, or C + I + G, exceeds gross

national product, Y, and that the economy is spending more on imports than it is earning

from its exports. The economy is therefore borrowing from foreigners and reducing its net

foreign wealth. A current account surplus implies that domestic absorption is smaller than

gross national product, and that the economy is spending less on imports than it is earning

on exports. The economy is therefore lending to foreigners and increasing its net foreign

wealth.

Now define national saving, S, as the sum of private sector saving, SP = Y – T - C, and

public sector saving, SG = T – G, where T refers to tax revenues. Public sector saving will

be negative if government expenditure, G, exceeds tax revenues, T, so that the

government’s fiscal accounts are in deficit. It follows that national saving is the difference

between gross national product and the sum of private and public consumption

expenditures. Thus, S = Y – C – G, from which it follows that:

S = I + CA, where CA = EX – IM.

A country that saves more than it invests at home will be building up its stock of net

foreign wealth by running a current account surplus. A country whose domestic investment

exceeds national savings will be running a current account deficit and thereby financing

part of its investment needs by borrowing foreign savings.

Another way of looking at these accounting identities is to note that:

CA = SP – I – (G – T),

from which it becomes evident that, depending upon its private saving and investment

decisions, an economy that runs a large government sector deficit may find that deficit

mirrored in a current account deficit. The large US current account deficit reflects a

deficiency in national saving relative to investment. Part of the explanation of the shortfall

in national saving is the size of the government sector deficit. This is known as the twin

deficits problem. On the other side of the Pacific, China and Japan are generating large

current account surpluses because their national savings exceed their domestic investments.

In a sense, they are currently financing the US government deficit.

Asset transactions and the capital account of the balance of payments

The balance of payments records all transactions that occur between the Home country and

foreign countries. All transactions that result in a payment to foreigners (for example,

import purchases) are recorded as a debit (or negative) item in the balance of payments,

while all transactions that result in receipts from foreigners (for example, export sales) are

recorded as a credit (or positive) item in the balance of payments. Since export values and

import values are recorded in the balance of payments, the balance of payments includes

the current account.

Notice, however, that export values include exports of both goods and services, where

services include tourist services provided to foreign visitors and income receipts that

represent a return on the Home country’s foreign asset holdings. Similarly, import values

include imports of both goods and services, where services include the tourist services

provided when Home country residents visit foreign lands and income payments that

represent a return on foreign investments in the Home country. It follows that the current

account balance is a more inclusive concept than the merchandise trade balance, which

usually refers to the difference between the value of goods exports and the value of goods

imports.

The balance of payments also includes a capital account. (Although the textbook follows

US guidelines and distinguishes a capital account from an asset account, Canada does not

follow this classification, so we will treat the two accounts as merged.) The capital

account includes all exchanges of capital assets between the Home country and foreign

countries. If Canadians purchase US government bonds, or a condominium in the French

Riviera, this represents a capital outflow and would be recorded as a debit item in the

capital account. If foreigners purchase shares in well known Canadian companies, or a

chalet at Whistler, BC, the associated capital inflow would be recorded as a credit item in

the capital account. More generally, capital outflows are associated with an increase in

foreign assets held by residents of the Home country, while capital inflows are associated

with an increase in Home country assets held by residents of foreign countries.

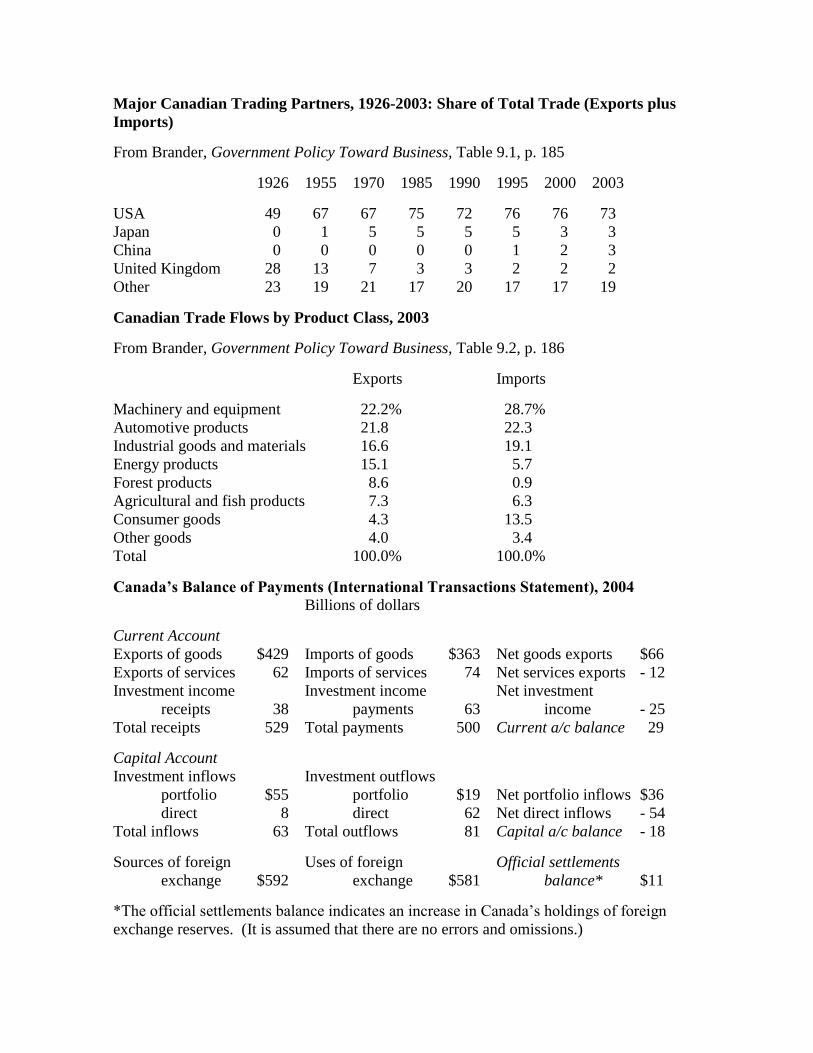

Exchange reserves and official settlements balances

The balance of payments includes both the current account and the capital account. Double

entry accounting principles ensure that a current account surplus implies a capital account

deficit and that a current account deficit implies a capital account surplus. Current account

surpluses are lent back to foreign countries through capital outflows. Current account

deficits are covered by borrowing from foreign countries through capital inflows. In this

accounting sense, the balance of payments always balances.

However, included within the capital account are official settlement transactions. Central

banks hold exchange reserve accounts which are comprised of short term money market

instruments (such as Treasury bills) denominated in foreign currencies, normally US dollars,

euros, pounds, or yen. Thus, official settlements transactions involve the purchase or sale

of foreign exchange reserves by a country’s central bank. Official purchases of foreign

exchange reserves imply that the balance of payments would otherwise have been in overall

surplus had these purchases not occurred. Official sales of foreign exchange reserves imply

that the balance of payments would otherwise have been in overall deficit had these sales

not occurred. Thus, one may write:

dRH = CA + NF,

where dRH is the change in official holdings of foreign exchange reserves, CA is the

current account balance, and NF is net capital inflows excluding official settlement

transactions. If there is no official intervention in the foreign exchange market, dRH = 0,

and thus CA = - NF. A current account surplus, CA > 0, is associated with a net capital