economics for healthcare managers, third edition

TRANSCRIPT

Copyright 2015 Health Administration Press

Economics for Healthcare Managers, Third Edition

Instructor’s Manual

Robert H. Lee Department of Health Policy and Management

University of Kansas

Copyright 2015 Health Administration Press

Contents Chapter 1: Why Health Economics? ............................................................................................... 5

Key Concepts .............................................................................................................................. 5

Solved Exercises ......................................................................................................................... 5

Case 1.1: An Upset Customer ..................................................................................................... 7

Case 1.2: Questions About Tax Exemptions .............................................................................. 8

Case 1.3: Why Is the Pressure to Reduce Healthcare Costs So Strong? ..................................... 8

Chapter 2: An Overview of the US Healthcare System .................................................................. 9

Key Concepts .............................................................................................................................. 9

Solved Exercises ......................................................................................................................... 9

Case 2.1: A Pain in the Back .................................................................................................... 11

Chapter 3: An Overview of the Healthcare Financing System ..................................................... 12

Key Concepts ............................................................................................................................ 12

Solved Exercises ....................................................................................................................... 12

Case 3.1: Federal Employees Health Benefits Program as the Model for Marketplace Plans . 14

Case 3.2: Group Health Cooperative’s Patient-Centered Medical Home ................................. 15

Chapter 4: Describing, Evaluating, and Managing Risk............................................................... 16

Key Concepts ............................................................................................................................ 16

Solved Exercises ....................................................................................................................... 16

Case 4.1: Betting on Medicare Advantage ............................................................................... 19

Case 4.2: Investing in Cardiology Services .............................................................................. 20

Case 4.3: Diversification by Joint Venture ............................................................................... 20

Chapter 5: Cost ............................................................................................................................. 22

Key Concepts ............................................................................................................................ 22

Solved Exercises ....................................................................................................................... 22

Case 5.1: Virginia Mason Medical Center ................................................................................ 27

Case 5.2: Improving Performance ............................................................................................ 28

Case 5.3: The Costs of Nonurgent Care in the Emergency Department ................................ 288

Chapter 6: Bending the Cost Curve .............................................................................................. 30

Key Concepts ............................................................................................................................ 30

Solved Exercises ....................................................................................................................... 30

Chapter 7: The Demand for Healthcare Products ......................................................................... 33

Key Concepts ............................................................................................................................ 33

Economics for Healthcare Managers, Third Edition – Instructor’s Manual 3

Copyright 2015 Health Administration Press

Solved Exercises ....................................................................................................................... 33

Case 7.1: MinuteClinic ............................................................................................................. 39

Chapter 8: Elasticities ................................................................................................................... 40

Key Concepts ............................................................................................................................ 40

Solved Exercises ....................................................................................................................... 40

Case 8.1: Mental Health Parity ................................................................................................. 43

Case 8.2: Reducing Waiting Time ............................................................................................ 43

Chapter 9: Forecasting .................................................................................................................. 45

Key Concepts ............................................................................................................................ 45

Solved Exercises ....................................................................................................................... 45

Case 9.1: Building a New Urgent Care Center ......................................................................... 52

Case 9.2: Forecasting the Demand for Transfusions ................................................................ 52

Chapter 10: Supply and Demand Analysis ................................................................................... 53

Key Concepts ............................................................................................................................ 53

Solved Exercises ....................................................................................................................... 53

Case 10.1: Worrying About Demand Shifts ............................................................................. 59

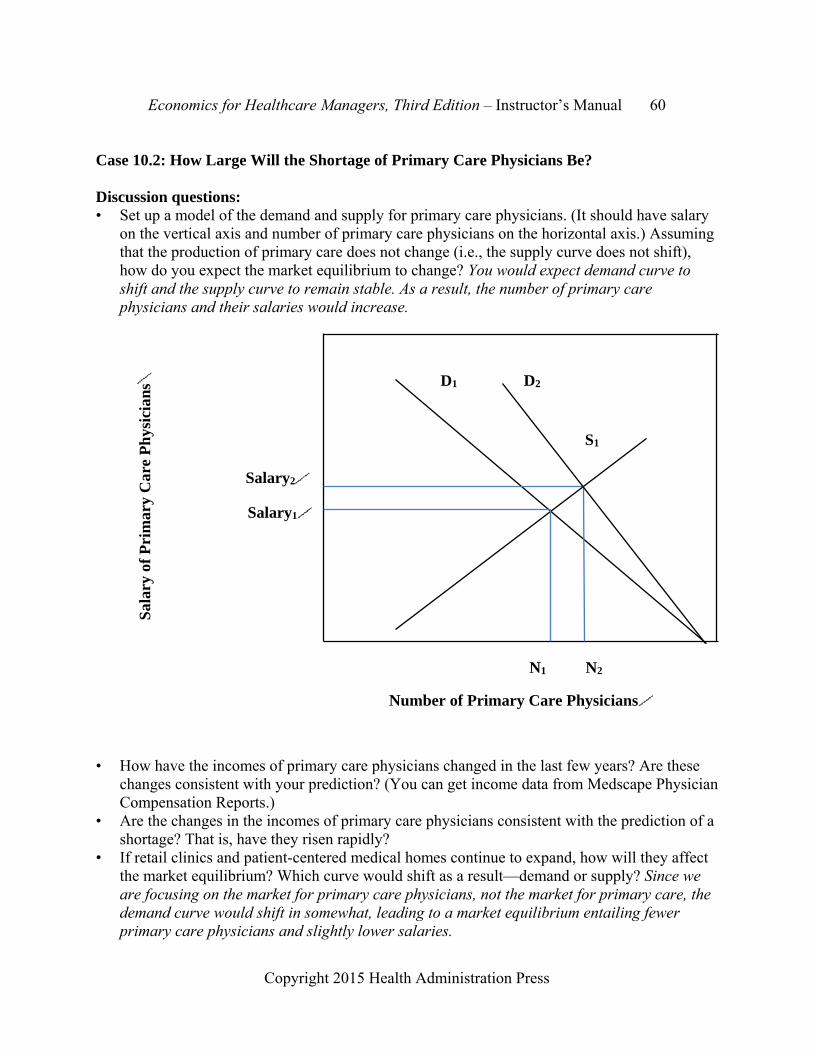

Case 10.2: How Large Will the Shortage of Primary Care Physicians Be? ............................. 60

Chapter 11: Maximizing Profits.................................................................................................... 62

Key Concepts ............................................................................................................................ 62

Solved Exercises ....................................................................................................................... 62

Case 11.1: Perfecting Patient Care ............................................................................................ 65

Case 11.2: Tax Exemption for Not-for-Profit Hospitals ........................................................... 66

Chapter 12: Pricing ....................................................................................................................... 67

Key Concepts ............................................................................................................................ 67

Solved Exercises ....................................................................................................................... 67

Case 12.1: Price Discrimination in Practice ............................................................................. 70

Case 12.2: What Should You Charge? ..................................................................................... 71

Case 12.3: Should My Firm Accept This Contract? ................................................................. 72

Chapter 13: Asymmetric Information and Incentives ................................................................... 73

Key Concepts ............................................................................................................................ 73

Solved Exercises ....................................................................................................................... 73

Case 13.1: Improving Safety..................................................................................................... 77

Economics for Healthcare Managers, Third Edition – Instructor’s Manual 4

Copyright 2015 Health Administration Press

Case 13.2: Improving Total Knee Replacement at Brigham and Women’s Hospital .............. 78

Chapter 14: Economic Analysis of Clinical and Managerial Interventions ................................. 79

Key Concepts ............................................................................................................................ 79

Solved Exercises ....................................................................................................................... 79

Case 14.1: Teledermatology ..................................................................................................... 82

Chapter 15: Profits, Market Structure, and Market Power ........................................................... 83

Key Concepts ............................................................................................................................ 83

Solved Exercises ....................................................................................................................... 83

Case 15.1: Deregulating Pharmaceutical Advertising .............................................................. 86

Chapter 16: Government Intervention in Healthcare Markets ...................................................... 88

Key Concepts ............................................................................................................................ 88

Solved Exercises ....................................................................................................................... 88

Case 16.1: Setting Prices for Walkers ....................................................................................... 92

Case 16.2: To Vaccinate or Not ................................................................................................ 92

Case 16.3: Diagnosing Chest Pains .......................................................................................... 93

Chapter 17: Regulation ................................................................................................................. 94

Key Concepts ............................................................................................................................ 94

Solved Exercises ....................................................................................................................... 94

Case 17.1: Monks, Caskets, and the Supreme Court ................................................................ 96

Case 17.2: Self-Regulation ....................................................................................................... 97

Case 17.3: Changing Consumer Information ............................................................................ 97

Chapter 18: Behavioral Economics .............................................................................................. 99

Key Concepts ............................................................................................................................ 99

Solved Exercises ....................................................................................................................... 99

Economics for Healthcare Managers, Third Edition – Instructor’s Manual 5

Copyright 2015 Health Administration Press

Chapter 1: Why Health Economics? Key Concepts Economics helps managers focus on key issues.

Economics helps managers understand goal-oriented decision making.

Economics helps managers understand strategic decision making.

Economics gives managers a framework for understanding costs.

Economics gives managers a framework for understanding market demand.

Economics gives managers a framework for assessing profitability.

Healthcare managers must deal effectively with risk and uncertainty.

Healthcare managers must contend with the management problems that insurance presents.

Information asymmetries create a number of problems for healthcare managers.

Not-for-profit organizations create unique problems for managers.

Rapid change in the healthcare system forces managers to lead their organizations into unfamiliar territory on a routine basis.

Solved Exercises1 1.1. Why is the idea that value depends on consumers’ preferences radical? The idea that “the

customer is always right” is not widely held in healthcare. Insisting that consumers’ preferences define value challenges the belief system of many professionals.

1.2. Mechanics usually have better information about how to fix automobiles than their customers do. What problems does this advantage create? Do mechanics or their customers do anything to limit these problems? In some cases mechanics take advantage of their customers. In other cases customers are reluctant to take their car to a mechanic or follow his advice. Customers try to use information from associates to identify reliable mechanics and try to patronize one mechanic, understanding that taking good care of repeat customers is in the self-interest of mechanics. Mechanics seek certification programs, develop brand names, and offer guarantees.

1 The discussion questions in this guide can be analyzed in some length. The answers provided here are merely illustrative. An instructor who chooses to focus on the answer to a question will surely develop a more detailed response.

Economics for Healthcare Managers, Third Edition – Instructor’s Manual 6

Copyright 2015 Health Administration Press

1.3. A mandatory health insurance plan costs $4,000. One worker earns $24,500 in employment income and $500 in investment income. Another worker earns $48,000 in employment income and $2,000 in investment income. A third worker earns $68,000 in employment income and $7,000 in investment income. A premium-based system would cost each worker $4,000. A wage tax–based system would cost each worker 8.5 percent of wages. An income tax–based system would cost each worker 8 percent of income. For each worker, calculate the cost of the insurance as a share of total income.

E = Employment Income $24,500 $48,000 $68,000

I = Investment Income $500 $2,000 $7,000

P = Premium cost of insurance $4,000 $4,000 $4,000

Premium as a percentage of income = P/(E + I) 16.0% 8.0% 5.3%

W = Wage tax cost of insurance = 0.085 E $2,083 $4,080 $5,780

Wage tax as a percentage of income = W/(E + I) 8.3% 8.2% 7.7%

T = Income tax cost of insurance = 0.085 (E + I) $2,000 $4,000 $6,000

Income tax as a percentage of income = T/(E + I) 8.0% 8.0% 8.0%

1.4. Which of the payment systems in Exercise 1.3 would impose the largest burden on those with incomes under $25,000: a plan financed via premiums, via the income tax, or via a payroll tax? The easiest way to look at this is to compare the cost as a percentage of income. The premium cost is 16 percent of income for those with incomes under $25,000, so it poses the greatest burden.

1.5. Which of the plans in Exercise 1.3 would be fairest? To answer this question requires a definition of fairness, and different individuals will have different definitions. For example, one definition could be that the price was the same for everyone. Only the premium-based plan meets this test. Another definition of fairness might be having cost be the same percentage of income for everyone. Only the income tax–based plan meets this test.

1.6. Which of these questions can you answer using positive economics? For which of the preceding questions must you use normative economics? “Which plan would be fairest?” clearly involves normative decisions. It is tempting, but not entirely correct, to say that the analysis of the burden of health insurance costs involves no normative judgments. Making the decision to analyze spending as a percentage of income also reflects the analyst’s belief that this is the best way to describe spending. What one chooses to analyze often reflects one’s values, even if the analysis that follows is completely positive.

Economics for Healthcare Managers, Third Edition – Instructor’s Manual 7

Copyright 2015 Health Administration Press

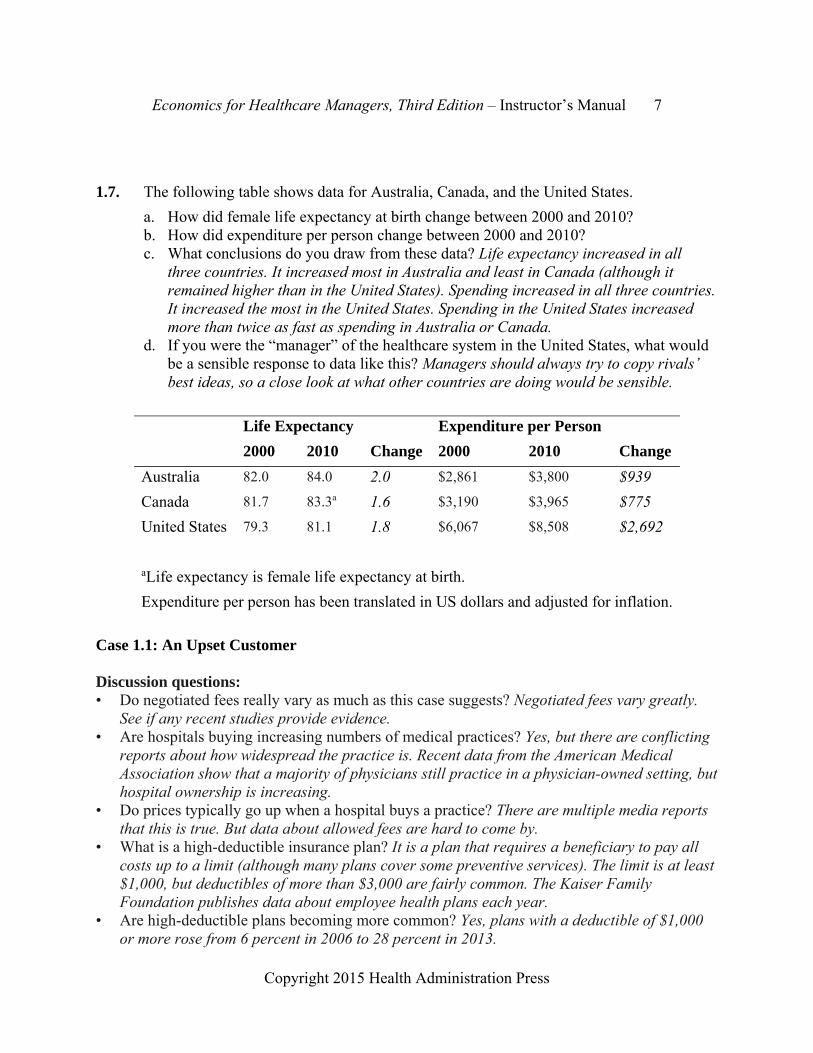

1.7. The following table shows data for Australia, Canada, and the United States.

a. How did female life expectancy at birth change between 2000 and 2010? b. How did expenditure per person change between 2000 and 2010? c. What conclusions do you draw from these data? Life expectancy increased in all

three countries. It increased most in Australia and least in Canada (although it remained higher than in the United States). Spending increased in all three countries. It increased the most in the United States. Spending in the United States increased more than twice as fast as spending in Australia or Canada.

d. If you were the “manager” of the healthcare system in the United States, what would be a sensible response to data like this? Managers should always try to copy rivals’ best ideas, so a close look at what other countries are doing would be sensible.

Life Expectancy Expenditure per Person

2000 2010 Change 2000 2010 Change

Australia 82.0 84.0 2.0 $2,861 $3,800 $939

Canada 81.7 83.3a 1.6 $3,190 $3,965 $775

United States 79.3 81.1 1.8 $6,067 $8,508 $2,692

aLife expectancy is female life expectancy at birth.

Expenditure per person has been translated in US dollars and adjusted for inflation.

Case 1.1: An Upset Customer Discussion questions: • Do negotiated fees really vary as much as this case suggests? Negotiated fees vary greatly.

See if any recent studies provide evidence. • Are hospitals buying increasing numbers of medical practices? Yes, but there are conflicting

reports about how widespread the practice is. Recent data from the American Medical Association show that a majority of physicians still practice in a physician-owned setting, but hospital ownership is increasing.

• Do prices typically go up when a hospital buys a practice? There are multiple media reports that this is true. But data about allowed fees are hard to come by.

• What is a high-deductible insurance plan? It is a plan that requires a beneficiary to pay all costs up to a limit (although many plans cover some preventive services). The limit is at least $1,000, but deductibles of more than $3,000 are fairly common. The Kaiser Family Foundation publishes data about employee health plans each year.

• Are high-deductible plans becoming more common? Yes, plans with a deductible of $1,000 or more rose from 6 percent in 2006 to 28 percent in 2013.

Economics for Healthcare Managers, Third Edition – Instructor’s Manual 8

Copyright 2015 Health Administration Press

• Is buying medical practices a profitable strategy for hospitals? Hospitals lose money on most practices that they buy. They may offset this via increased referrals.

• If you were this customer, how would you react? Case 1.2: Questions About Tax Exemptions Discussion questions: • What do hospitals have to do to qualify for tax-exempt status? The answer varies. In some

states there are specific requirements. In others there are not. The Affordable Care Act (ACA) sets some standards, but does not set dollar or percentage amounts.

• How much charity care do hospitals provide on average? No national data are available, but a 2010 study found that California not-for-profit hospitals provide $1,428,513,583 in charity care.

• How much is tax-exempt status worth to hospitals? The same study found that these hospitals saved $3,271,614,090 by being tax exempt.

• Should the University of Pittsburgh Medical Center be required to pay Pittsburgh taxes? Case 1.3: Why Is the Pressure to Reduce Healthcare Costs So Strong? Discussion questions: • Why is spending so much more than other countries on healthcare a problem? More

resources would be available for other goals. • What can Americans not buy due to high spending on healthcare? Examples would include

education (because of pressure on state budgets from Medicaid) or transportation (because of pressure on the federal budget from Medicaid).

• What factors other than healthcare affect population health? Nutrition, neighborhood safety, clean water, and many more factors affect health.

• Does this evidence suggest that the American healthcare system is not efficient? Spending more and getting poorer results does suggest inefficiency.

Economics for Healthcare Managers, Third Edition – Instructor’s Manual 9

Copyright 2015 Health Administration Press

Chapter 2: An Overview of the US Healthcare System Key Concepts Healthcare products are inputs into health.

Healthcare products are also outputs of the healthcare sector.

The usefulness of healthcare products varies widely.

Marginal analysis helps managers focus on the right questions.

Life expectancies have increased sharply in the United States in recent years.

Other wealthy countries have seen larger health gains with smaller cost increases.

The healthcare sector may change radically in response to technology and policy changes.

Solved Exercises 2.1. Identify a product that is one organization’s output and another organization’s input.

Among the possible examples are pharmaceuticals. They are produced in one organization and used in another.

2.2. Can you think of any initiatives that reflect the input view of healthcare? Corporate wellness programs are good examples. The belief is that better nutrition and exercise will result in healthier, more productive employees. Moreover, advocates believe that increasing the use of these nonmedical inputs will reduce the use of medical inputs.

2.3. What’s wrong with spending 17.2 percent of GDP on healthcare? Nothing, unless consumers and their representatives believe that this healthcare spending is not giving them enough value.

2.4. Americans spend more on smartphones than the citizens of other countries, yet this type of spending is seldom described as a problem. Why is spending more on healthcare different? The biggest difference is that Americans have directly voted with their dollars to increase spending on smartphones. Their decisions about healthcare spending seldom reflect the true cost of the resources involved (because of extensive subsidies). When it comes to healthcare, Americans usually feel they are spending “someone else’s money.” More accurately, they are paying indirectly for healthcare by paying taxes, by accepting lower wages, or by paying insurance premiums. Indirect payment creates an incentive to spend too much.

2.5. US national health expenditure was $7,026 per person in 2006 and $4,790 in 2000. The Consumer Price Index had a value of 201.6 in 2006 and a value of 172.2 in 2000. Adjusted for inflation, how much was spending in 2000? To adjust spending in 2000 for inflation simply multiply actual spending by the Consumer Price Index for 2006 and divide by the Consumer Price Index for 2000. This gives $5,608 = $4,790 201.6/172.2.

2.6. US national health expenditure was $148 per person in 1960 and $4,790 in 2000. The Consumer Price Index had a value of 29.6 in 1960 and a value of 172.2 in 2000. In 1960

Economics for Healthcare Managers, Third Edition – Instructor’s Manual 10

Copyright 2015 Health Administration Press

dollars, how much was spending in 2000? To adjust spending in 1960 for inflation simply multiply actual spending by the Consumer Price Index for 2006 and divide by the Consumer Price Index for 1960. This gives $1,008 = $148 201.6/29.6.

2.7. How did the state and local government share of national health expenditures change between 2000 and last year? What accounts for this change? Go to the “Actuarial Studies” page on the website of the Centers for Medicare & Medicaid Services (www.cms.gov/Research-Statistics-Data-and-Systems/Research/ActuarialStudies/index.html) to get data. Between 2000 and 2012, state and local government spending on health doubled, meaning that it fell from 10.4percent of the total to 10.3 percent.

2.8. When was the last year that GDP grew faster than national health expenditure? Go to the “Actuarial Studies” page on the website of the Centers for Medicare & Medicaid Services (http://www.cms.gov/Research-Statistics-Data-and-Systems/Research/ActuarialStudies/index.html) to get data. Gross Domestic Product grew faster than health spending in 2010, 2011, and 2012.

2.9. Your accountants tell you that it costs $400 to set up an immunization program at a preschool and immunize one child against polio. It will cost $460 to immunize 20 more children. What is the cost per child for the first child? What is the cost per child for these additional 20 children? What is the average cost per child? What concepts do these calculations illustrate? These calculations illustrate the ideas of average and incremental (marginal) values. The cost for the first child is $400. The incremental cost for the next 20 is $23 = $460/20. Average cost for the 21 children is $43 = (400 + 460)/21.

2.10. A new treatment of cystic fibrosis costs $2 million. The life expectancy of 1,000 patients who were randomly assigned to the new treatment increased by 3.2 years. What is the cost per life year of the new treatment? The added cost is $2 million. The increase in life years is 3.2 1,000 = 3,200. So, the cost per life year is $625 = $2 million/3,200.

2.11. Setting up nurse practitioner clinics to serve 20,000 newborns in Georgia would cost $6 million. This program would increase life expectancy at birth from 75.1 years to 75.3 years. How many life years would be gained? What is the cost per life year? Should this program be started? The added cost is $6 million. The increase in life years is 0.2 20,000 = 4,000. So, the cost per life year is $1,500 = $6 million/4,000.

2.12. Why has the share of healthcare output produced by hospitals fallen? Will this trend continue? Can you think of a policy or technology change that would further reduce hospital use? Can you think of a policy or technology change that would increase hospital use? What implications do these changes have for the careers of healthcare managers? The main reason is that changes in technology allow more and more care to be delivered in an outpatient setting. The implication is that much of the growth in opportunities for healthcare managers will be in sectors other than hospitals. An example of a technology that will reduce hospital use is DNA testing, which will allow identification of effective, ineffective, and dangerous drugs for individuals. By getting patients the right drugs in a timely fashion a significant number of hospitalizations can be omitted. I cannot think of a policy or technology change that would increase hospital use.

Economics for Healthcare Managers, Third Edition – Instructor’s Manual 11

Copyright 2015 Health Administration Press

Case 2.1: A Pain in the Back Discussion questions: • If imaging followed by surgery is as effective as conservative therapy, what’s wrong with

letting physicians and patients do what they want? Imaging followed by surgery will cost much more than conservative therapy, so it drives up costs.

• What explains this rise of imaging and surgery for back pain? It is not completely clear, but imaging and surgery are usually quite profitable for physicians and health systems. Some physicians may order imaging studies because of malpractice concerns.

• Who makes decisions about surgery? Patients decide on surgery, based on the recommendations of their physicians.

• Should insurers take action to reduce surgery rates? Should individuals? Insurers are in a better position to reduce rates than individuals, who may be poorly informed.

• How do providers’ revenues change if imaging and surgery rates rise? They go up. • How do patients’ costs change if imaging and surgery rates rise? They go up. • How do current incentive systems affect physicians’ and patients’ decisions? If they are paid

per procedure, imaging followed by surgery will be much more profitable for physicians than conservative therapy. Increasingly, though, high rates of imaging studies are being used as an indicator of poor quality, which makes imaging studies less attractive for physicians. For well-insured patients in a standard PPO, imaging followed by surgery will not entail very large out-of-pocket spending. For the increasing number of patients in high-deductible plans, the cost of imaging followed by surgery will be quite high.

Economics for Healthcare Managers, Third Edition – Instructor’s Manual 12

Copyright 2015 Health Administration Press

Chapter 3: An Overview of the Healthcare Financing System Key Concepts Consumers pay for most medical care indirectly, through taxes and insurance premiums. Direct payments for healthcare are often called out-of-pocket payments. Insurance pools the risks of high healthcare costs. Moral hazard and adverse selection complicate risk pooling. About 85 percent of the US population has medical insurance. Most consumers obtain coverage through an employer- or government-sponsored plan. Receiving insurance as a benefit of employment has significant tax benefits. Managed care has largely replaced traditional insurance. Managed care plans differ widely. Solved Exercises 3.1. Why is health insurance necessary? Health insurance is necessary because healthcare

costs are so skewed. Most people spend relatively little, but an unfortunate few spend huge amounts. People often want insurance to protect them from large, uncommon losses.

3.2. Explain how adverse selection and moral hazard are different, and give an example of each. Adverse selection involves individuals with different risks sorting themselves into different insurance pools. For example, young, healthy workers who do not have a personal physician are more likely to join an HMO than are older or less healthy workers who have an established relationship with a physician. So, average spending will be lower for the HMO group, even if the HMO does nothing to reduce costs. Moral hazard involves purchasing a product or purchasing more of a product because it is covered by insurance (and the consumer bears only part of the cost). For example, a consumer with coverage for flu shots is more likely to get them than a consumer without coverage.

3.3. “The United States is the land of the overinsured, the underinsured, and the uninsured.” What do you think that these concepts mean? Why might this comment be true? About 48 million Americans lacked health insurance as of 2014, so the third part of the comment is clear. Many Americans with insurance are overinsured because they have coverage for “uninsurable” expenses. A small expense that occurs with high probability, such as routine dental examinations or replacement of eyeglasses, costs much more to buy via insurance than it does directly and is said to be uninsurable. Insurance benefits are just ways of reducing taxes. These same consumers may have very limited coverage for uncommon, expensive services (which are precisely the sorts of expenses that insurance should cover). Consumers like these are underinsured, because they are at risk for catastrophic expenses. These first two comments are true largely because the tax code gives very large subsidies to high-income employees who get health insurance benefits at work and no subsidies to low-income employees who do not. Why so many people are left

Economics for Healthcare Managers, Third Edition – Instructor’s Manual 13

Copyright 2015 Health Administration Press

at risk for catastrophic expenses is not clear.

3.4. Private health insurers have been slow to develop and adopt proven cost containment innovations (e.g., case rates or disease management programs). Why do you think that is the case? Most have such a small market share that it is difficult to get providers to accept unfamiliar payment systems. In addition, a company that spent its resources to develop a successful program would find that other companies that did not would quickly copy it. The payoff to innovation is apt to be small. In addition, until recently many companies lacked the analytic capacity to assess cost containment strategies.

3.5. A radiology firm charges $2,000 per exam. Uninsured patients are expected to pay list price. How much do they pay? Usually they will pay $2,000.

3.6. A radiology firm charges $2,000 per exam. An insurer’s allowed fee is 80 percent of charges. Its beneficiaries pay 25 percent of the allowed fee. How much does the insurer pay? How much does the beneficiary pay? The allowed fee is $1,600 = 0.8*$2,000. Of this beneficiaries pay $400 and the insurer pays $1,200.

3.7. If the radiology firm raised its charge to $3,000, how much would the insurer pay? How much would the beneficiary pay? The allowed fee would rise $2,400 = 0.8 $3,000. Of this, beneficiaries pay $600 and the insurer pays $1,800.

3.8. A surgeon charges $2,400 for hernia surgery. He contracts with an insurer that allows a fee of $800. Patients pay 20 percent of the allowed fee. How much does the insurer pay? How much does the patient pay? The allowed fee is $800, of which patients pay $160 and the insurer pays $640.

3.9. You have incurred a medical bill of $10,000. Your plan has a deductible of $1,000 and coinsurance of 20 percent. How much of this bill will you have to pay directly? You will pay $2,800. The deductible is $1,000 and the coinsurance is $1,800 = 0.2 ($10,000 - $1,000).

3.10. Why do employers provide health insurance coverage to their employees? Employees want insurance coverage, so employers offer it to attract and retain them.

3.11. Your practice offers only a PPO with a large deductible, high coinsurance, and a limited network. You pay $400 per month for single coverage. Some of your employees have been urging you to offer a more generous plan. Who would you expect to choose the more generous plan and pay any extra premium? Such a plan would be most attractive to those who anticipate high expenditures, primarily those with pre-existing conditions.

3.12. What are the fundamental differences between HMO and PPO plans? PPO plans usually have larger provider networks and less restrictive coverage of out-of-network providers.

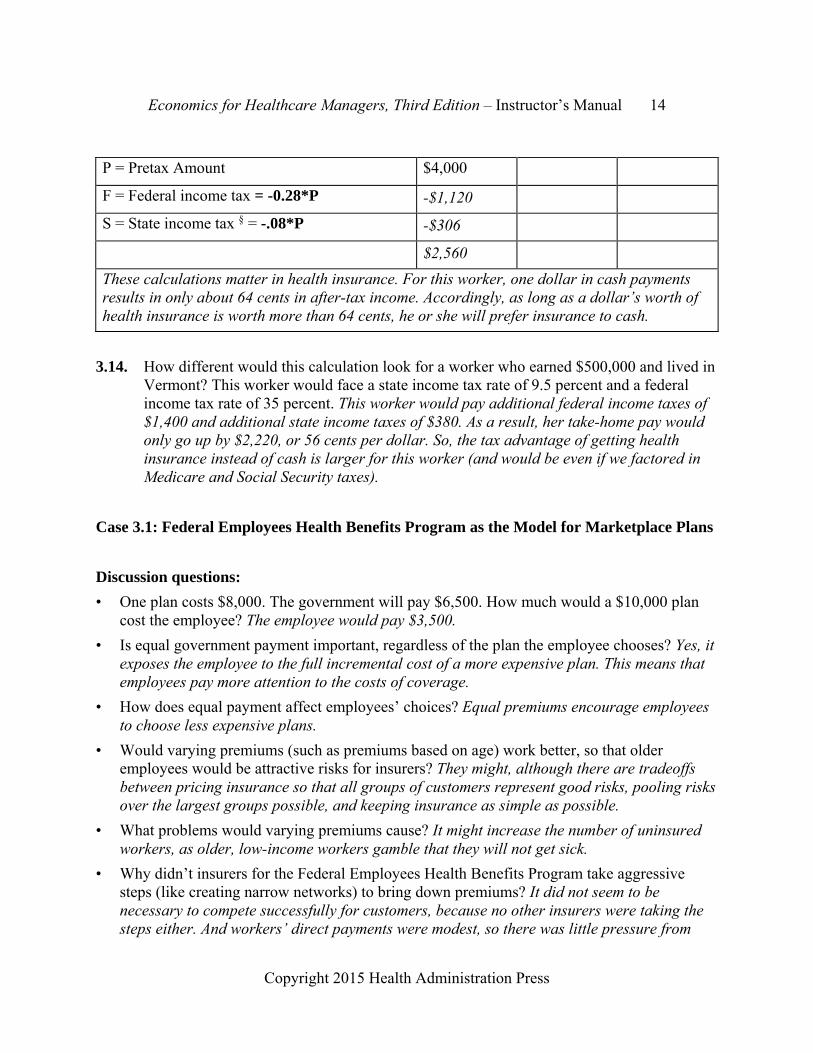

3.13. Suppose that your employer offered you $4,000 in cash instead of health insurance coverage. Health insurance is excluded from state and federal income taxes. (To keep the problem simple we will ignore Social Security and Medicare wage taxes.) The cash would be subject to state income taxes (8 percent) and federal income taxes (28 percent). How much would your after-tax income go up if you took the cash rather than the insurance?

Economics for Healthcare Managers, Third Edition – Instructor’s Manual 14

Copyright 2015 Health Administration Press

P = Pretax Amount $4,000

F = Federal income tax = -0.28*P -$1,120

S = State income tax § = -.08*P -$306

$2,560

These calculations matter in health insurance. For this worker, one dollar in cash payments results in only about 64 cents in after-tax income. Accordingly, as long as a dollar’s worth of health insurance is worth more than 64 cents, he or she will prefer insurance to cash.

3.14. How different would this calculation look for a worker who earned $500,000 and lived in Vermont? This worker would face a state income tax rate of 9.5 percent and a federal income tax rate of 35 percent. This worker would pay additional federal income taxes of $1,400 and additional state income taxes of $380. As a result, her take-home pay would only go up by $2,220, or 56 cents per dollar. So, the tax advantage of getting health insurance instead of cash is larger for this worker (and would be even if we factored in Medicare and Social Security taxes).

Case 3.1: Federal Employees Health Benefits Program as the Model for Marketplace Plans

Discussion questions:

• One plan costs $8,000. The government will pay $6,500. How much would a $10,000 plan cost the employee? The employee would pay $3,500.

• Is equal government payment important, regardless of the plan the employee chooses? Yes, it exposes the employee to the full incremental cost of a more expensive plan. This means that employees pay more attention to the costs of coverage.

• How does equal payment affect employees’ choices? Equal premiums encourage employees to choose less expensive plans.

• Would varying premiums (such as premiums based on age) work better, so that older employees would be attractive risks for insurers? They might, although there are tradeoffs between pricing insurance so that all groups of customers represent good risks, pooling risks over the largest groups possible, and keeping insurance as simple as possible.

• What problems would varying premiums cause? It might increase the number of uninsured workers, as older, low-income workers gamble that they will not get sick.

• Why didn’t insurers for the Federal Employees Health Benefits Program take aggressive steps (like creating narrow networks) to bring down premiums? It did not seem to be necessary to compete successfully for customers, because no other insurers were taking the steps either. And workers’ direct payments were modest, so there was little pressure from

Economics for Healthcare Managers, Third Edition – Instructor’s Manual 15

Copyright 2015 Health Administration Press

customers to take these steps.

• Why do the high incomes of federal employees affect their choices? Consumers with high incomes tend to be less price sensitive than consumers with low incomes. In the context of insurance, they tend to buy more generous plans that offer better protection against financial and medical risks. Because their tax rates are higher, they may also want coverage that turns predictable after-tax spending into pre-tax spending on insurance premiums.

Case 3.2: Group Health Cooperative’s Patient-Centered Medical Home Discussion questions: • Why would it make sense to become a network model HMO? By becoming a network model

HMO (one that signs contracts with some of its providers rather than owning them), Group Health could expand at lower cost.

• Would you like to get your primary care at a patient-centered medical home? This depends on personal preferences, so no right answer is possible. It may be a useful way to explore the features of patient-centered medical homes.

• Did it make sense for Group Health to support the patient-centered medical home transition? Group Health is an insurer as well as a provider of care. For an insurer, a patient-centered medical home offers a way of reducing medical costs. For a provider, a patient-centered medical home offers a practice environment that patients, doctors, and nurses prefer. This makes it easier to add patients and attract staff.

• Could an independent practice afford to become a patient-centered medical home? Perhaps it could if most of its competitors were patient-centered medical homes. Being a patient-centered medical home might be required to be an effective competitor. Otherwise, a patient-centered medical home adds costs and may reduce revenue, making it a problematic choice for an independent practice.

• Why is Medicare sponsoring patient-centered medical home demonstrations? Medicare wants to save money, improve beneficiaries’ experience of care, and improve beneficiaries’ health. A patient-centered medical home helps with all of these goals.

• How would a 6 percent reduction in hospitalization rates affect hospitals? They would become less profitable. As much as half of a hospital’s costs do not vary with volume, so a reduction in volume reduces revenue more than cost.

Economics for Healthcare Managers, Third Edition – Instructor’s Manual 16

Copyright 2015 Health Administration Press

Chapter 4: Describing, Evaluating, and Managing Risk Key Concepts Clinical and managerial decisions typically entail uncertainty about what will happen.

Decision makers often have imprecise estimates of the probabilities of various outcomes.

Decision making about risk involves describing, evaluating, and managing potential outcomes.

Insurance and diversification are two ways to manage risk.

Solved Exercises 4.1. Five of ten people earn $0, four earn $100, and one loses $100. What is the expected

payoff? What is the variance of the payoff? An average is just the sum of the earnings divided by the number of observations. In this case there are ten people with total earnings of $300, so the average is $30. A variance is the squared difference between each observation and the average, weighted by the share of observations with a value.

Person Earnings p*(Earnings – Average) 2 1 $0 $90 Average = $30.00 2 0 $90 Variance = 4,100 3 0 $90 4 0 $90 5 0 $90 6 100 $490 7 100 $490 8 100 $490 9 100 $490 10 (100) $1,690

4.2. There is a 50 percent chance of making $0, a 40 percent chance of making $100, and a 10 percent chance of losing $100. Calculate the expected value and variance of the payoff. How does your estimate compare to the previous problem? Your answer is the same, since 0.5 $0 + 0.4 $100 - 0.1 $100 = $30. The variance is 4,100 = 0.5 ($0 - $30)2 + 0.4 ($100 - $30)2+ 0.1 (-$100 - $30)2

Economics for Healthcare Managers, Third Edition – Instructor’s Manual 17

Copyright 2015 Health Administration Press

4.3. There is a 1 percent chance that you will have healthcare bills of $100,000, a 19 percent chance that you will have healthcare bills of $10,000, a 60 percent chance that you will have healthcare bills of $500, and a 20 percent chance that you will have healthcare bills of $0. What is your expected healthcare spending? In this case your expected spending is $3,200, which is equal to 0.01 $100,000 + 0.19 $10,000 + 0.60 $500 + 0.20 $0.

4.4. There is a 1 percent chance that you will have healthcare bills of $100,000, a 19 percent chance that you will have healthcare bills of $10,000, a 60 percent chance that you will have healthcare bills of $500, and a 20 percent chance that you will have healthcare bills of $0. What will your expected insurance benefits be? Would you be willing to buy complete insurance coverage if it cost $3,712? Explain. In this case your expected spending is $3,200, which is equal to 0.01 $100,000 + 0.19 $10,000 + 0.60 $500 + 0.20 $0. Because the insurance premium is larger than your expected spending, you would buy insurance only if you are risk averse.

4.5. Instead of complete insurance as in Exercise 4.4, you have a policy with a $5,000 deductible. What will your expected out-of-pocket spending be? What will your expected insurance benefits be? Assuming that the premium equals 116 percent of expected insurance benefits, do you prefer the policy with a $5,000 deductible or complete coverage? Your expected out-of-pocket spending will be $1,300 = 0.01 $5,000 + 0.19 $5,000 + 0.60 $500. Your expected insurance benefits will be $1,900 = 0.01 $95,000 + 0.19 x $5,000. Your premium will be $2,204 = 1.16 $1,900. Which policy you will choose is not clear. The policy with a $5,000 deductible costs a lot less, but it also exposes you to more risk.

Out-of-

Probability Spending Benefits Spending

1% $100,000 $95,000 $5,000

19% $10,000 $5,000 $5,000

60% $500 $0 $500

20% $0 $0 $0

4.6. Your firm, which operates a nationwide system of cancer clinics, has annual profits of $800 million and cash reserves of $500 million. Your clinics have a replacement value of $200 million, and fire insurance for them would cost $5 million per year. Actuarial data show that your expected losses due to fire are $4 million. Should you buy insurance? Assuming that your firm is risk neutral, you would not buy fire insurance. Insurance would cost $5 million, and your expected loss is $4 million. Even multiple fires would not significantly reduce your profits or exhaust your firm’s reserves, so not buying insurance makes sense.

Economics for Healthcare Managers, Third Edition – Instructor’s Manual 18

Copyright 2015 Health Administration Press

4.7. Your firm rents a supply management system to hospitals. You have received a buyout offer of $5 million. You forecast a 25 percent chance that you will have profits of $10 million, a 35 percent chance that you will have profits of $6 million, and a 40 percent chance that you will have profits of $2 million. Should you accept the offer? Explain. Your expected profit is $5.4 million = 0.25 $10 + 0.35 $6 + 0.4 $2. Since expected profits exceed the offer, you would accept it only if you were risk averse. Risk aversion means preferring a sure $5 million to a risky $5.4 million.

4.8. You were given a lottery ticket. The drawing will be held in five minutes. You have a 0.1 percent chance of winning $10,000. You refuse an offer of $11 for your ticket. Are you risk averse? Explain. You are not risk averse. The expected value of your ticket is $10 = 0.001 $10,000. By refusing a sure offer with a higher expected value, you have revealed that you are a risk seeker.

4.9. Your house is worth $200,000. Your risk of a catastrophic flood is 0.5 percent. Such a flood would destroy your house and would not be covered by homeowner’s insurance. Although you grumble, you buy flood coverage for $1,200. Are you risk averse or risk seeking? Your expected loss is $1,000 = 0.005 $200,000. Since you prefer a sure loss of $1,200 to a risky loss of $1,000, you must be risk averse.

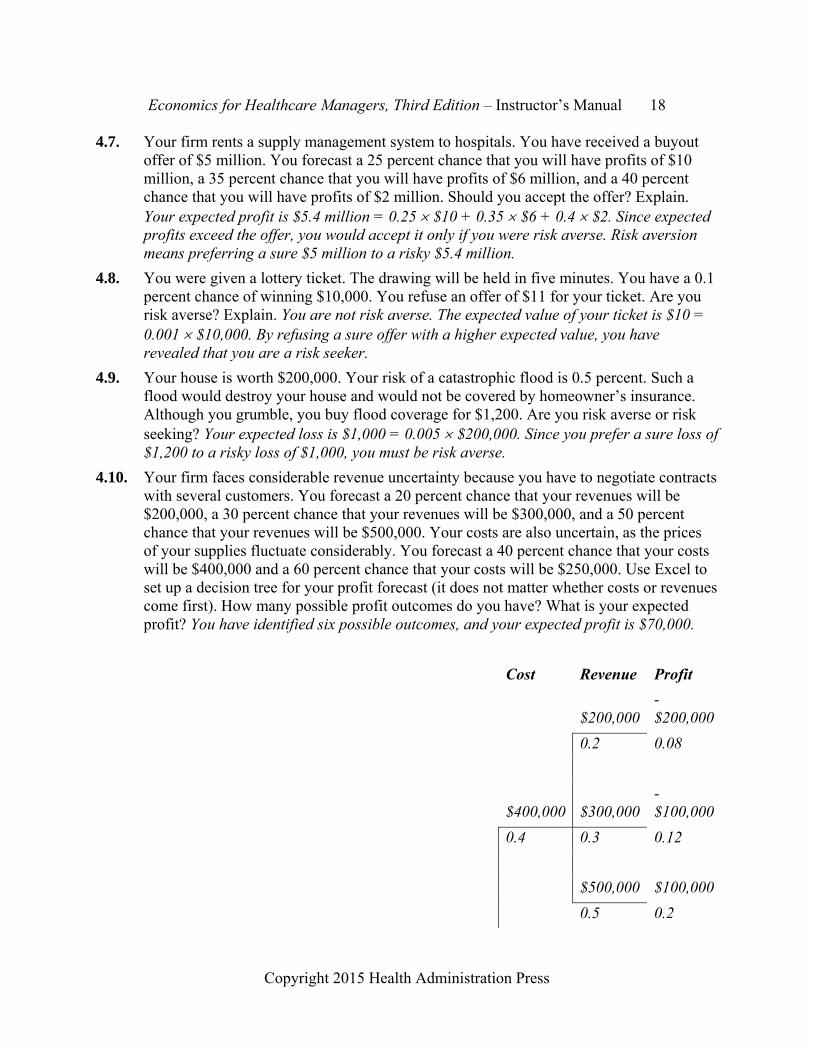

4.10. Your firm faces considerable revenue uncertainty because you have to negotiate contracts with several customers. You forecast a 20 percent chance that your revenues will be $200,000, a 30 percent chance that your revenues will be $300,000, and a 50 percent chance that your revenues will be $500,000. Your costs are also uncertain, as the prices of your supplies fluctuate considerably. You forecast a 40 percent chance that your costs will be $400,000 and a 60 percent chance that your costs will be $250,000. Use Excel to set up a decision tree for your profit forecast (it does not matter whether costs or revenues come first). How many possible profit outcomes do you have? What is your expected profit? You have identified six possible outcomes, and your expected profit is $70,000.

Cost Revenue Profit

$200,000 -$200,000

0.2 0.08

$400,000 $300,000 -$100,000

0.4 0.3 0.12

$500,000 $100,000

0.5 0.2

Economics for Healthcare Managers, Third Edition – Instructor’s Manual 19

Copyright 2015 Health Administration Press

Expected Profit = $70,000

$200,000 -$50,000

0.2 0.12

$250,000 $300,000 $50,000

0.6 0.3 0.18

$500,000 $250,000

0.5 0.3

4.11. Your firm has been sued for $3 million by a supplier for breach of contract. Your lawyers believe that there are three possible outcomes if the suit goes to trial. One, which the lawyers term “highly improbable,” is that your supplier will win the lawsuit and be awarded $3 million. Another, which the lawyers term “unlikely,” is that your supplier will win the lawsuit and be awarded $500,000. The third, which the lawyers term “likely,” is that your supplier will lose the lawsuit and be awarded $0. You have to decide whether to try to settle the case. To do so you need to assign probabilities to “highly improbable,” “unlikely,” and “likely.” What probabilities correspond to these statements? Going to trial will cost you $100,000 in legal fees. One of your lawyers believes that your supplier will settle for $100,000 (plus your legal fees of $25,000). Should you settle? It is not clear what probabilities correspond to these statements, and different people will have different ideas about what they are. Settling will cost you $125,000. Going to court will cost you $100,000. Assume for the moment that a “highly improbable” outcome is half as likely as an “unlikely” outcome. If an “unlikely” outcome has more than a 0.005 chance of happening, settling will be less expensive.

Case 4.1: Betting on Medicare Advantage Discussion questions: • What has happened to Medicare Advantage enrollment since 2012? A good source of current

information is State Health Facts at kff.org. • What has happened to Medicaid managed care enrollment since 2012? A good source of

current information is State Health Facts at kff.org. • Have any insurers pulled out of Medicaid managed care markets during the past year? This

Economics for Healthcare Managers, Third Edition – Instructor’s Manual 20

Copyright 2015 Health Administration Press

will require an internet search, as sources will vary. • Medicare Advantage contracts last a year. What is Aetna risking by betting that Medicare

Advantage will be an attractive opportunity? The main risk is that Medicare Advantage will stop being a profitable product. The company also could lose its initial investments.

• Is Medicare Advantage riskier than other forms of private health insurance? Medicare Advantage may be a little riskier, in that Congress can change the rules. However, companies and other insurance plan sponsors change their requirements too.

• What other healthcare firms also face risks due to changes in government policy? Virtually all healthcare firms face risks due to changes in policy. That includes firms that do little Medicare or Medicaid business.

Case 4.2: Investing in Cardiology Services Discussion questions: • How likely is a change in Medicare payment? What probability should you assign to it? You

certainly cannot assign an objective probability to it. This will be a subjective probability based on your understanding of the situation.

• What will happen to hospital profits if Medicare does switch to bundled payments? They will probably go down, because the organization that gets the bundled payment will have incentives to eliminate low-value services.

• How likely is a failure to recruit three excellent cardiologists? What probability should you assign to this endeavor? What will happen to profits if you are able to recruit only two excellent cardiologists? Again, this will be a subjective probability based on your understanding of the situation. Shea is “confident” that cardiologists can be recruited. That certainly means a probability in excess of 0.50.

• If you set up this scenario as a decision tree, which of your assumptions become clear to other decision makers? The probabilities and the profit forecasts become explicit.

• What are the advantages of making your assumptions clear? What are the disadvantages? The advantages are primarily that others can assess whether the assumptions are reasonable. Being forced to defend your assumptions (and sometimes changing them) will improve decision making. Having to defend your assumptions will add to your preparation time, which may be a disadvantage.

Case 4.3: Diversification by Joint Venture Discussion questions: • Why is expansion outside the United States an attractive form of diversification? Overseas

risks are likely to be uncorrelated with domestic risks. Different political and economic forces are likely to be at work. So, if things are going badly in the United States, they may be

Economics for Healthcare Managers, Third Edition – Instructor’s Manual 21

Copyright 2015 Health Administration Press

going well overseas. • What are the pitfalls of international expansion? An ongoing concern is that you may not

fully appreciate the risks you are accepting. Unfamiliarity with the history and culture may lead you to take on more risky projects than you anticipate.

• What are the potential pitfalls of other diversification efforts? See the answer to the pitfalls of international expansion. Another pitfall is that opportunities that you understand may have risks that are correlated with the risks in your core market. This means that things go well in the new markets when things go well in the core market, so you are not diversifying in a way that really reduces risk.

• What are the main risks that UPMC faces in its Pittsburgh operations? New competition and changes in insurance markets are the main ones.

Economics for Healthcare Managers, Third Edition – Instructor’s Manual 22

Copyright 2015 Health Administration Press

Chapter 5: Cost Key Concepts Costs depend on perspective.

Costs can be hard to measure.

Good managers have an accurate understanding of costs.

Goods and services an organization produces are called outputs.

Goods or service an organization uses in production are called inputs.

Incremental cost equals the change in cost resulting from a change in output.

Average cost equals the total cost of a process divided by the total output of a process.

Large firms have a cost advantage if there are economies of scale.

Multiproduct firms have a cost advantage if there are economies of scope.

Higher quality should mean higher costs. If not, the organization is inefficient.

Higher input prices mean higher costs.

Costs depend on outputs, technology, input prices, and efficiency.

Opportunity cost is the value of a resource in its best alternative use.

Sunk costs, which are costs you cannot change, should be ignored.

Solved Exercises 5.1. Why is it important to distinguish between fixed and variable costs? It is important

because increasing or reducing output only changes variable costs. A common mistake is to lump together fixed and variable costs, thus overestimating the cost of expanding output and overestimating the savings from reducing output.

5.2. Explain how a decrease in input prices or an increase in efficiency would affect costs. The effects would be the same.

5.3. You spent $500,000 on staff training last year. Why should this cost be treated as a sunk cost? Why should this cost be ignored in making a decision whether to switch coding software? Nothing that you can do this year will change what was spent on last year’s staff training. So it is a sunk cost and should be ignored in your software decision.

5.4. Your president bought two acres of land for $200,000 ten years ago. Although it is zoned for commercial use, it currently holds eight small, single-family houses. A property management firm that wants to continue leasing the eight houses has offered you $400,000 for the property. A developer wants to build a 12-story apartment building on

Economics for Healthcare Managers, Third Edition – Instructor’s Manual 23

Copyright 2015 Health Administration Press

the site and has offered $600,000. What value should you assign to the property? The next best (i.e., highest valued) use of the land is for an apartment building. Therefore, you should assign a value of $600,000.

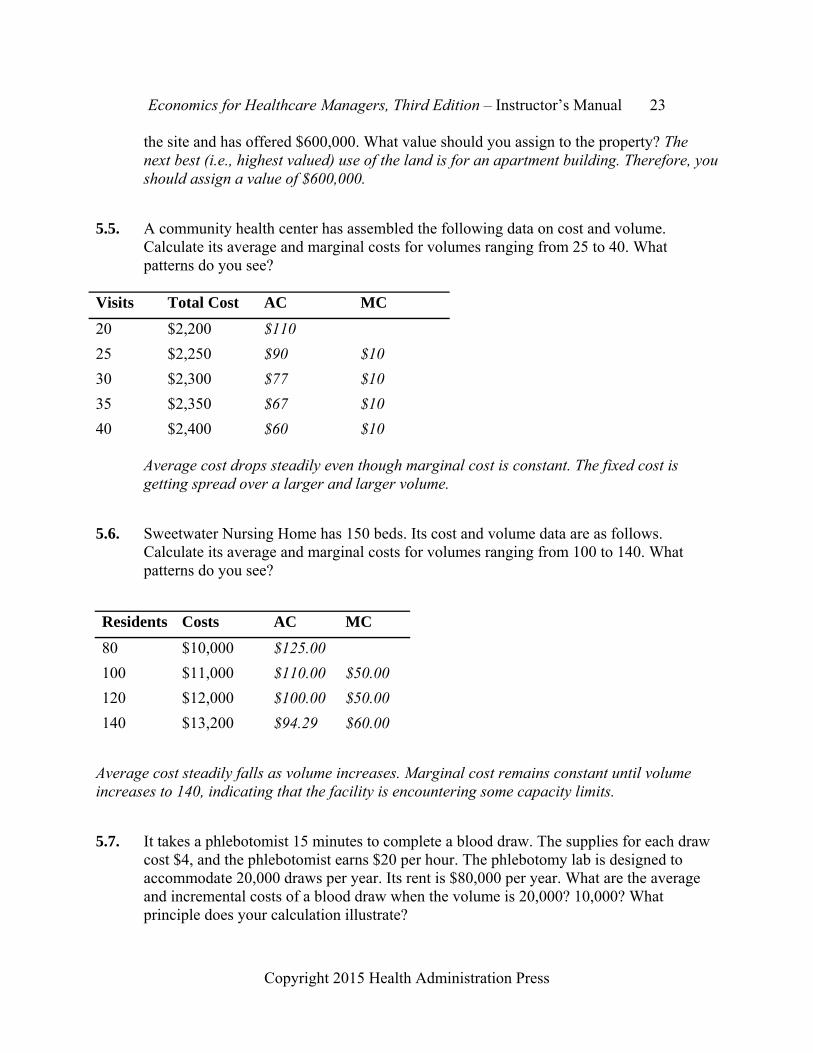

5.5. A community health center has assembled the following data on cost and volume. Calculate its average and marginal costs for volumes ranging from 25 to 40. What patterns do you see?

Average cost drops steadily even though marginal cost is constant. The fixed cost is getting spread over a larger and larger volume.

5.6. Sweetwater Nursing Home has 150 beds. Its cost and volume data are as follows. Calculate its average and marginal costs for volumes ranging from 100 to 140. What patterns do you see?

Residents Costs AC MC

80 $10,000 $125.00

100 $11,000 $110.00 $50.00

120 $12,000 $100.00 $50.00

140 $13,200 $94.29 $60.00

Average cost steadily falls as volume increases. Marginal cost remains constant until volume increases to 140, indicating that the facility is encountering some capacity limits.

5.7. It takes a phlebotomist 15 minutes to complete a blood draw. The supplies for each draw cost $4, and the phlebotomist earns $20 per hour. The phlebotomy lab is designed to accommodate 20,000 draws per year. Its rent is $80,000 per year. What are the average and incremental costs of a blood draw when the volume is 20,000? 10,000? What principle does your calculation illustrate?

Visits Total Cost AC MC

20 $2,200 $110

25 $2,250 $90 $10

30 $2,300 $77 $10

35 $2,350 $67 $10

40 $2,400 $60 $10

Economics for Healthcare Managers, Third Edition – Instructor’s Manual 24

Copyright 2015 Health Administration Press

Costs with a Wage of $20

Volume Total Cost AC MC

0 $80,000

20,000 $260,000 $13.00 $9.00

10,000 $170,000 $17.00 $9.00

The average cost of a blood draw when the volume is 20,000 is $13. The AC is $17 when the volume is 10,000. At smaller volumes the $80,000 in fixed costs results in higher average costs, even though marginal costs are constant.

5.8. How would the average and marginal costs change if the phlebotomist’s wage rose to $24 per hour? What principle does your calculation illustrate?

Costs with a Wage of $24

Volume Total Cost AC MC

0 $80,000

20,000 $280,000 $14.00 $10.00

10,000 $180,000 $18.00 $10.00

The marginal cost of a blood draw is $9 when the wage is $20. It rises to $10 when the wage is $24. The average cost rises by $1 as well. This shows that marginal (and average) costs rise when input prices rise.

5.9. A new computer lets a phlebotomist complete a blood draw in 10 minutes. The supplies for each draw cost $4, and the phlebotomist earns $20 per hour. The phlebotomy lab is designed to accommodate 20,000 draws per year. Its rent is $80,000 per year. What is the marginal cost of a blood draw? What principle does your calculation illustrate?

Costs with a Wage of $20 and a Time of 10 Minutes

Volume Total Cost AC MC

0 $80,000

20,000 $240,000 $12.00 $8.00

10,000 $160,000 $16.00 $8.00

Economics for Healthcare Managers, Third Edition – Instructor’s Manual 25

Copyright 2015 Health Administration Press

The marginal and average costs both fall by $1. This illustrates that an improvement in efficiency has effects much like a reduction in input costs.

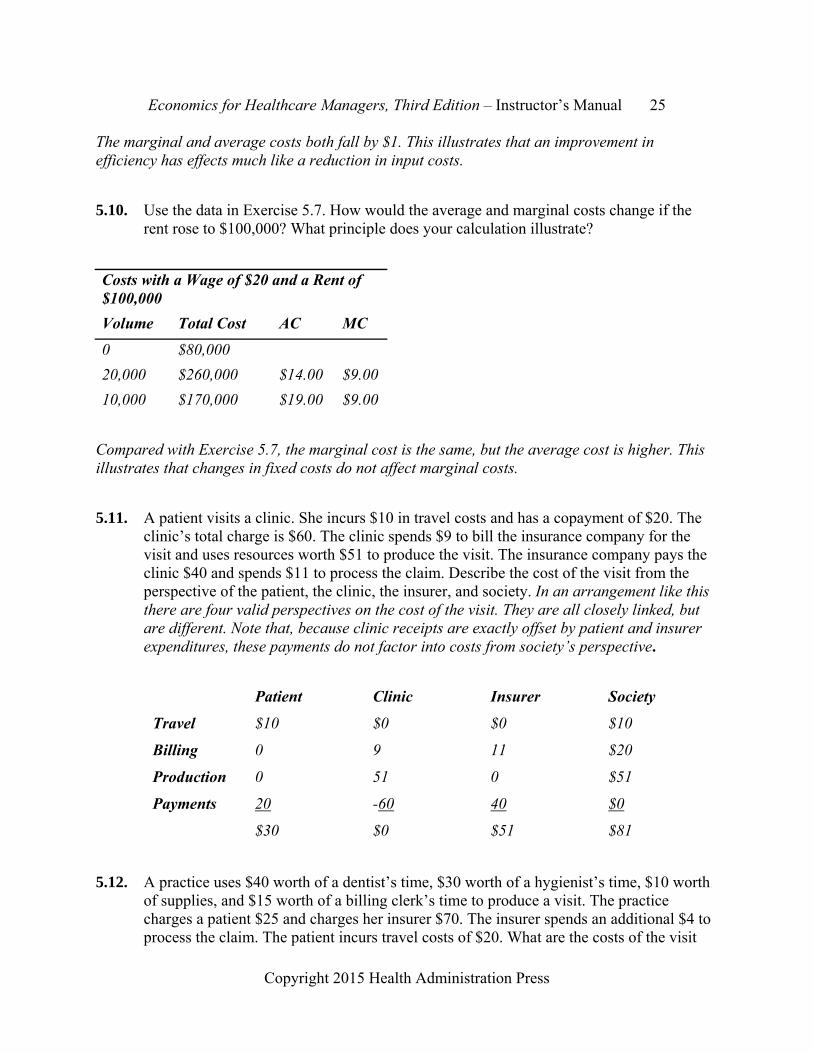

5.10. Use the data in Exercise 5.7. How would the average and marginal costs change if the rent rose to $100,000? What principle does your calculation illustrate?

Costs with a Wage of $20 and a Rent of $100,000

Volume Total Cost AC MC

0 $80,000

20,000 $260,000 $14.00 $9.00

10,000 $170,000 $19.00 $9.00

Compared with Exercise 5.7, the marginal cost is the same, but the average cost is higher. This illustrates that changes in fixed costs do not affect marginal costs.

5.11. A patient visits a clinic. She incurs $10 in travel costs and has a copayment of $20. The clinic’s total charge is $60. The clinic spends $9 to bill the insurance company for the visit and uses resources worth $51 to produce the visit. The insurance company pays the clinic $40 and spends $11 to process the claim. Describe the cost of the visit from the perspective of the patient, the clinic, the insurer, and society. In an arrangement like this there are four valid perspectives on the cost of the visit. They are all closely linked, but are different. Note that, because clinic receipts are exactly offset by patient and insurer expenditures, these payments do not factor into costs from society’s perspective.

Patient Clinic Insurer Society

Travel $10 $0 $0 $10

Billing 0 9 11 $20

Production 0 51 0 $51

Payments 20 -60 40 $0

$30 $0 $51 $81

5.12. A practice uses $40 worth of a dentist’s time, $30 worth of a hygienist’s time, $10 worth of supplies, and $15 worth of a billing clerk’s time to produce a visit. The practice charges a patient $25 and charges her insurer $70. The insurer spends an additional $4 to process the claim. The patient incurs travel costs of $20. What are the costs of the visit

Economics for Healthcare Managers, Third Edition – Instructor’s Manual 26

Copyright 2015 Health Administration Press

from the perspective of society, the patient, the practice, and the insurer?

Patient Patient Insurer Society

Dentist’s time -$40 -$40

Hygienist’s time -$30 -$30

Supplies -$10 -$10

Claims processing -$4 -$4

Clerk’s time -$15 -$15

Travel cost -$20 -$20

Fee $95 -$25 -$70 $0

$0 -$45 -$74 -$119

5.13. Kim and Pat underwrite insurance. Each underwrites 50 accounts per month. Each account takes four hours to underwrite. The value of their time is $40 per hour. Monthly costs for each are $1,500 for an office, $2,000 for a receptionist, and $2,400 for a secretary. Calculate the average and incremental cost per case for Kim and Pat. Since costs are the same for Kim and Pat, we will only calculate Kim’s costs. Average cost simply equals total cost divided by total output. There are two ways to calculate incremental cost. One would be to add up the cost that each additional account requires. The only variable input is Kim or Pat’s time. Since each account takes four hours and time costs $40 per hour, incremental cost is $160. One could also calculate total costs at a volume of 50 and calculate the incremental cost of producing one more. This also finds an incremental cost of $160. Because there are fixed costs and incremental costs are constant, average cost goes down as volume goes up.

Volume 50 51

Kim's Time $8,000 $8,160

Rent $1,500 $1,500

Receptionist $2,000 $2,000

Secretary $2,400 $2,400

Total Cost $13,900 $14,060

Average cost $278 $276

Incremental cost $160

Economics for Healthcare Managers, Third Edition – Instructor’s Manual 27

Copyright 2015 Health Administration Press

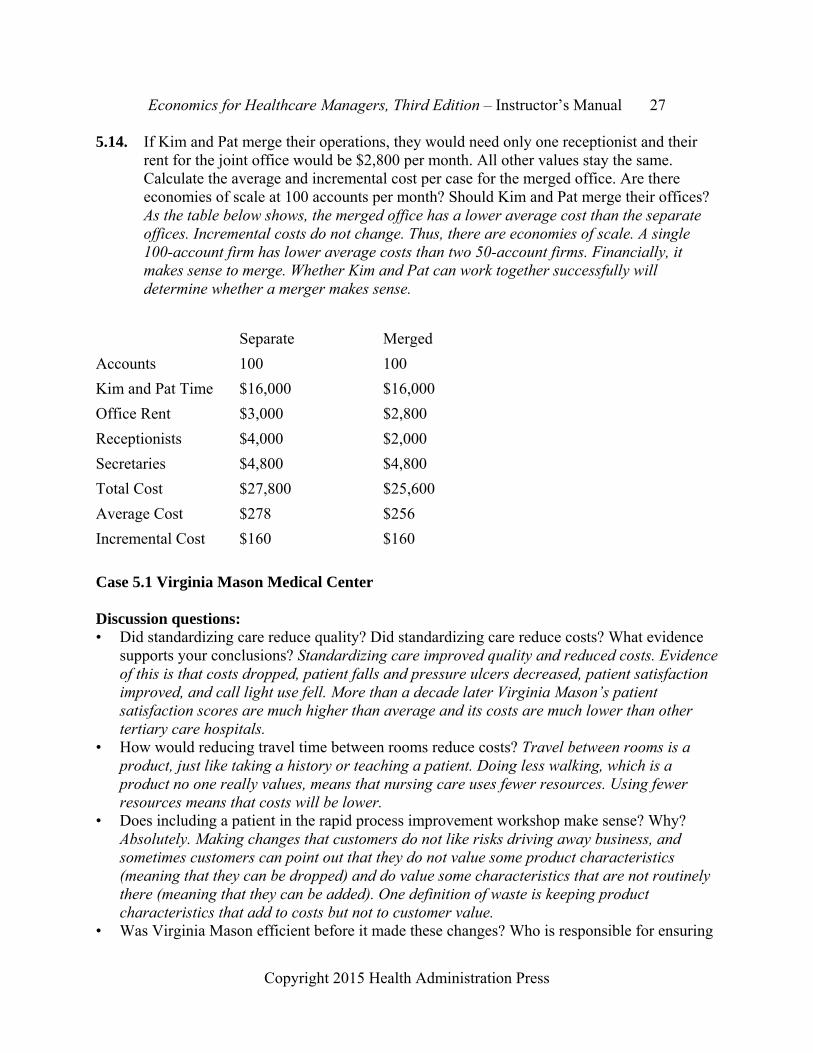

5.14. If Kim and Pat merge their operations, they would need only one receptionist and their rent for the joint office would be $2,800 per month. All other values stay the same. Calculate the average and incremental cost per case for the merged office. Are there economies of scale at 100 accounts per month? Should Kim and Pat merge their offices? As the table below shows, the merged office has a lower average cost than the separate offices. Incremental costs do not change. Thus, there are economies of scale. A single 100-account firm has lower average costs than two 50-account firms. Financially, it makes sense to merge. Whether Kim and Pat can work together successfully will determine whether a merger makes sense.

Separate Merged

Accounts 100 100

Kim and Pat Time $16,000 $16,000

Office Rent $3,000 $2,800

Receptionists $4,000 $2,000

Secretaries $4,800 $4,800

Total Cost $27,800 $25,600

Average Cost $278 $256

Incremental Cost $160 $160

Case 5.1 Virginia Mason Medical Center Discussion questions: • Did standardizing care reduce quality? Did standardizing care reduce costs? What evidence

supports your conclusions? Standardizing care improved quality and reduced costs. Evidence of this is that costs dropped, patient falls and pressure ulcers decreased, patient satisfaction improved, and call light use fell. More than a decade later Virginia Mason’s patient satisfaction scores are much higher than average and its costs are much lower than other tertiary care hospitals.

• How would reducing travel time between rooms reduce costs? Travel between rooms is a product, just like taking a history or teaching a patient. Doing less walking, which is a product no one really values, means that nursing care uses fewer resources. Using fewer resources means that costs will be lower.

• Does including a patient in the rapid process improvement workshop make sense? Why? Absolutely. Making changes that customers do not like risks driving away business, and sometimes customers can point out that they do not value some product characteristics (meaning that they can be dropped) and do value some characteristics that are not routinely there (meaning that they can be added). One definition of waste is keeping product characteristics that add to costs but not to customer value.

• Was Virginia Mason efficient before it made these changes? Who is responsible for ensuring

Economics for Healthcare Managers, Third Edition – Instructor’s Manual 28

Copyright 2015 Health Administration Press

that care is efficient? No, Virginia Mason was not efficient before the changes. Managers are responsible for making care more efficient. Managers are also responsible for making sure that frontline workers are engaged in improving efficiency.

• Why did the nurses resist the changes? Would you expect to encounter resistance in other departments? Resistance to change is common, especially when those involved are concerned that change will affect their professional roles. You should expect to encounter resistance in other departments as well.

Case 5.2 Improving Performance Discussion questions: • Could limiting the number of prostheses improve the quality of care? Yes, it simplifies what

other team members have to master. • Why was a team needed to choose the best way of doing knee replacements? The process

involves many people, and changes at any point can have major effects elsewhere. For example, changes in anesthesia could make recovery care easier or harder. Most performance improvement efforts seek input from those involved in the whole process.

• Is standardization like this common? Should it be? It is not common. Many argue it should be.

• Some of your staff object to standardizing care, calling it “cookbook nursing.” How do you respond? Focus on the benefits for patients. You are trying to improve their care and reduce their financial burdens. You are trying to make sure that your teams offer patients the best care possible.

• What would happen to your organization if insurers started steering patients to the most efficient providers and you were not one of them? Your volumes would drop. Most likely, profits would drop too, because fixed costs are very high for hospitals.

• Was Brigham and Women’s Hospital efficient before it made the changes described in this case? No.

Case 5.3 The Costs of Nonurgent Care in the Emergency Department

Discussion questions:

• Why do patients who are not critically ill go to emergency departments? Emergency departments are open whenever patients want to seek care. Many other providers offer very few weekend or evening visits. In addition, you do not need an appointment, and emergency departments must see anyone, whether they have insurance or not.

• Why do the variety of services emergency departments produce and the amount of overhead to be allocated make cost finding difficult? Overhead costs are very difficult to tie to particular services, so allocations are largely arbitrary. More overhead generally means cost estimates are more subjective. More overhead also means that average costs will be much higher than marginal costs. When many services get produced cost finding is more

Economics for Healthcare Managers, Third Edition – Instructor’s Manual 29

Copyright 2015 Health Administration Press

complex. You have fewer cases to work with, so estimates become less reliable. • Why was Morgan confident that costs could be reduced while quality could be improved? Is

this conclusion supported in the literature? The literature generally supports the conclusion that healthcare providers are not very efficient, meaning that they can increase quality while reducing costs.

• Thinking as a consumer, what would constitute higher quality in the emergency department? This is subjective.

• What options should the hospital consider? Obvious ones are expanded same-day appointments, expanded hours for primary care clinics, and urgent care clinics. Why would you be confident that these options would incur lower costs than an emergency department? These alternatives are open fewer hours, have less sophisticated equipment, have fewer personnel, have less skilled personnel, and generally treat simpler cases. Do you think quality would be higher? There is no right answer to this question, but most observers would argue that more patients being seen by their usual sources of care and less emergency department crowding would mean higher quality.

• If the hospital creates one or more urgent care clinics and adds evening and weekend hours to its primary care clinics, what will happen to emergency department volumes? What effect will that have on emergency department costs? Volumes will drop, probably by 15 percent or more. Overall costs will drop, but cost per visit will probably rise (without active cost reduction efforts). The drop in volume will increase fixed cost per visit, and the likely increase in the complexity of cases seen (as patients with simpler problems go elsewhere) will increase variable cost per visit.

Economics for Healthcare Managers, Third Edition – Instructor’s Manual 30

Copyright 2015 Health Administration Press

Chapter 6: Bending the Cost Curve Key Concepts The Triple Aim includes improving the experience of care for patients, improving population

health, and reducing healthcare costs per person.

The Affordable Care Act (ACA) has changed incentives for insurers and providers in a number of ways.

The ACA has already increased hospitals’ incentives to reduce readmissions.

Medicare Advantage HMOs are growing.

Multiple trials of Medicare accountable care organizations (contracts with potential gains for providers if cost and quality goals are met) are underway.

Private insurers are also testing accountable care organizations and simpler variants called narrow networks.

The prices that private insurers pay for similar products vary a great deal.

Private insurers are testing ways of steering patients to less expensive providers.

Multiple trials of bundled payments (fixed payments for an episode of care) are underway.

Multiple trials of medical homes are underway.

A number of states are shifting Medicaid beneficiaries to HMOs.

Some states have expanded Medicaid; some have not.

Some evidence indicates that the ACA’s initiatives have had positive effects.

The full effects of the ACA’s initiatives will not be known for years.

Solved Exercises 6.1. An insurance market consists of high-risk patients, who average $40,000 in spending per

year, and low-risk patients, who average $1,000 per year. Overall, low-risk patients represent 90 percent of the population. What would average spending be for a population

like this? Average spending would be $4,900, which equals 0.10 $40,000 + 0.90 $1,000.

6.2. Refer to Exercise 6.1. What would average spending be if low-risk patients were 92

percent of the population? Average spending would be $4,120, which equals 0.08

$40,000 + 0.92 $1,000.

6.3. Refer to Exercise 6.1. If an insurer sold 100,000 policies at $6,000, what would revenue be? What would medical costs be if the insurer paid for everything and low-risk patients were 90 percent of the population? How would that change if low-risk patients were 92

Economics for Healthcare Managers, Third Edition – Instructor’s Manual 31

Copyright 2015 Health Administration Press

percent of the population? Revenue would equal $600 million. If low-risk patients were 90 percent of the population, the insurer would spend $490 million, leaving $110 million to split between other costs and profit. If low-risk patients were 92 percent of the population, the insurer would spend $412 million, leaving $188 million to split between other costs and profit.

6.4. Why did hospitals have limited incentives to reduce readmissions prior to the ACA? Hospitals got paid for readmissions.

6.5. Refer to the box titled “Steering Patients to Less Expensive Providers” in this chapter. What would happen in the market for colonoscopies with a reference price of $500? What would happen in the market for colonoscopies with a reference price of $25? You would anticipate that some patients would switch to providers with lower prices. You would also expect some providers with high prices to reduce their prices. If the reference price fell to $25, you would anticipate that some patients would switch to initial fecal immunochemical tests followed by colonoscopies if there were abnormal results. You would also expect more patients to get tested, as fecal immunochemical tests are less trouble.

6.6. Go to the CMS Innovation Center http://innovation.cms.gov/index.html and see what ideas are being tested in a state of your choice.

6.7. Why would a system like John Muir Health launch a medical home that is intended to reduce its revenues? One reason is a conviction that a medical home is the right way to structure primary care. Another is the suspicion that the market is moving toward medical homes and the system would not want to be a late adopter.

6.8. How are a narrow network and an ACO different? Narrow networks are much simpler, as they do not usually incorporate all the requirements of an ACO. A narrow network is just an insurance plan with a limited number of providers.

6.9. What recent evidence about the performance of ACOs can you find? Are they growing? Are they saving money? Do enrollees seem to like the care they get? Is the quality of care good? The answers to Questions 6.9–6.14 can be found via Internet searches. The Centers for Medicare and Medicaid Services maintain a listing of ACOs, but it is not always up-to-date.

6.10. What recent evidence about the performance of medical homes can you find? Are they growing? Are they saving money? Do enrollees seem to like the care they get? Is the quality of care good?

6.11. What recent evidence about bundled payment can you find? Are they growing? Are they saving money? Do enrollees seem to like the care they get? Is the quality of care good?

Economics for Healthcare Managers, Third Edition – Instructor’s Manual 32

Copyright 2015 Health Administration Press

6.12. What recent evidence about Medicare Advantage HMOs can you find? Are they growing? Are they saving money? Do enrollees seem to like the care they get? Is the quality of care good?

6.13. How much did cost per Medicare beneficiary go up last year? (The Kaiser Foundation publishes these data on its website [http://kff.org/state-category/medicare/]).

6.14. Why would a health system want to participate in a trial of bundled payment?

6.15. What risk does a health system bear when it agrees to a bundled payment? The only risk is that costs will be higher than expected, meaning that profit per episode will be lower than expected.

6.16. What risk does a health system bear when it agrees to accept capitation? Capitation includes the risk of costs being higher than expected plus the risk that the number of episodes will be higher than expected.

Economics for Healthcare Managers, Third Edition – Instructor’s Manual 33

Copyright 2015 Health Administration Press

Chapter 7: The Demand for Healthcare Products Key Concepts The quantity demanded is the amount of a good or service purchased at a specific price when

all other factors are held constant.

When a product’s price rises, the quantity demanded usually falls.

Demand (a demand curve) describes the amounts of a good or service that will be purchased at different prices when all other factors are held constant.

An increase or decrease in demand reflects a shift in the entire list of amounts purchased at different prices. An increase or a decrease in demand results when another factor that influences consumer decisions changes.

Other factors that influence demand for healthcare products include consumer income, insurance coverage, perceptions of health status, perceptions of the productivity of other goods and services, and tastes.

The amount of money that a consumer pays directly for a product is called the out-of-pocket price for that good or service.

Because of insurance, the total price and the out-of-pocket price can differ quite a bit.

A complement is a good or service used instead of another good or service. Demand for a good falls if the price of a complement increases.

A substitute is a good or service used instead of another good or service. Demand for a good rises if a substitute rises in price.

Solved Exercises 7.1. Is the idea of demand is useful in healthcare, given the important role of agents? Study

after study finds that the demand for healthcare products is much like the demand for other products. Higher prices usually reduce consumption of healthcare products; lower prices usually increase consumption. Managers should not ignore possible reactions by agents. Neither should they ignore standard demand responses. Healthcare is not alone in having an important role for agents.

7.2. Should medical services be free? Justify your answer. For most consumers medical services should not be free. Consumers will tend to use free services until either the services have no added value or until other rationing devices (such as waits) curb demand.

7.3. Why might a consumer be “rationally ignorant” about the proper therapy for gallstones? Getting information takes time and energy that could be used in other ways (like fishing, working, or going to church). Because the probability of using this information is low for most consumers, the expected benefit of information is likely to be less than its expected cost.

Economics for Healthcare Managers, Third Edition – Instructor’s Manual 34

Copyright 2015 Health Administration Press