economics@anz anz international economics monthly...• given the anticipated slow progress on...

TRANSCRIPT

Inside:

Main article...............................1

Financial Markets Update............7

FX and Policy Rate Forecasts.......9

Macro Economic Forecasts ........10

LT FC Govt. Bond Ratings .........11

Country Updates .....................12

Authors:

Amy Auster Head of International Economics +61 3 9273 5417 [email protected]

Jasmine Robinson Senior Economist International +61 3 9273 6289 [email protected]

Alex Joiner Economist, International +61 3 9273 6123 [email protected]

Mark Rodrigues Senior Economist, Australia +61 3 9273 6286 [email protected]

Cameron Bagrie Chief Economist, New Zealand +64 4 802 2212 [email protected]

June 2006

ANZ International Economics Monthly

China : High liquidity, rapid loan growth - and the banks that depend on it

Economics@ANZ

Economics@ANZ undertook a short research trip to China in mid-June. Discussions with government policymakers and private sector experts focused on developments in monetary policy, the exchange rate and the banking system. The main themes and ideas generated by the meetings are as follows:

• China’s Big Four state-owned banks remain highly dependent upon their deposit base to provide the liquidity for their loan book, which in turn is still dominated by state-owned enterprises. A large proportion of that deposit base is believed to be held by a very small percentage of the population. The potential for loss of deposits is a major risk for these banks, leading to concerns about any source of competition.

• There are two imminent potential sources of competition. The first is the opening of the domestic banking system to foreign institutions under WTO in December 2006. The second is the gradual opening of the capital account to allow for easier transfer of savings out of China. Although the government has committed to liberalisation of the banking sector and the capital account, concerns about banking system stability ensure that progress will be slow.

• The government will correctly resist pressures to free the exchange rate for several years, for as long as significant capital controls are in place. However, the authorities will continue with the development of the domestic market infrastructure, such as the introduction of new hedging instruments, in order to facilitate the transition to greater currency volatility. Currency volatility may also be increased via a widening the RMB trading band.

• Given the anticipated slow progress on opening the capital account, we do not anticipate that the RMB will appreciate beyond USD/RMB7.0 in the near or medium term. Indeed, on a fundamental basis, the magnitude of potential capital outflows as against current and relatively stable inflows leads us to believe that the RMB is not necessarily undervalued, and certainly not to the extent that many market participants would seem to believe. Whether the government believes the currency is significantly undervalued is also debatable.

• We put forward the argument that high domestic liquidity is problematic in China not because of foreign capital inflows, as is commonly perceived, but because of the growth-target strategy of local governments and their financiers. Foreign direct investment has been static at roughly US$60 bn per annum for several years, as against US$200 bn in domestic loans written last year. From this vantage point, China’s rapid pace of FX reserve accumulation may be occurring because it is required by investors (local and foreign) to cover a minimum percentage of the monetary base, such that investors feel at ease with their ability to hedge against future currency volatility and convert future profits to foreign currencies.

Data flow for April and May suggest that the economy accelerated in the second quarter, raising the possibility that real GDP growth may be 10.5% YOY after 10.3% growth in the first quarter. More measures aimed at cooling the economy should be anticipated. The measures should remain concentrated in certain sectors such as coastal property markets and heavy manufacturing, although there could (and should) be greater efforts to slow down credit growth.

Economics@ANZ ANZ International Economics Monthly – June 2006

Page 2

China’s banks and future competition

Over the next six months, state-owned banks in China are meant to be preparing for a new world in which they will compete with foreign banks for the Chinese market. This process has been in the works for some time, with significant reforms undertaken over the past five years to get the banks ready for this new environment. The reforms – which have focused on improving asset quality, advancing the supervisory and regulatory framework, and restructuring ownership including via the introduction of foreign partners – have improved banks’ balance sheets significantly, as seen in the chart below.

Profile of major banks’ balance sheets

Sources: CBRC, National Bureau of Statistics, China

0.0

0.5

1.0

1.5

2.0

2.5

3.0

2002 2003 2004 20050

5

10

15

20

25

30

NPL Ratio (RHS)

Total NPLs (LHS)% of total loansRMB tr

Nonetheless, there are ongoing concerns as to how ready China’s banks really are for competition, which in the next 12 months is meant to come from two primary sources. The first is increased competition in the domestic market, which is taking place under the umbrella of the Qualified Foreign Institutional Investor Act (QFII) passed in 2002. In its initial phase, QFII allowed licensed foreign financial institutions to provide financial services to Chinese enterprises, as well as limited investments in the domestic equities and bond markets. At the end of this year, that license will extend so that QFII-licensed firms will be able to offer services to all Chinese clients, including at the retail level. As at the end of last year, 138 foreign banks had been approved to conduct RMB-related business in China, but their assets at US$85 bn amounted to only 2% of total assets in the banking sector.1

The second source of competition is from the global capital market, with the advent of the Qualified Domestic Institutional Investor (QDII) program under which licensed Chinese financial institutions will be able to convert RMB deposits to invest offshore in foreign currency assets.

1 Ding Lu, “China’s Banking Sector: Meeting the WTO Agenda,” April 2006.

Challenges posed by competition

There are two key challenges facing China’s largest banks in an environment of increased competition.

On the liability side, there is significant risk of a shrinking deposit base. China’s Big Four state-owned banks are still heavily reliant upon the deposit base that funds their loan book.2 The volume of deposits is huge; bank deposits are 160% of GDP in China as against 77% in the US, 78% in Korea, and 119% in Singapore. Moreover, 72% of Chinese residents’ net wealth is held in bank deposits, where the average real return is 0.3% per annum, thanks in part to controlled interest rates. This is also potentially very high velocity money, as it is estimated that up to half of the Big Four’s deposits are held by 2% of the population – the wealthiest and most sophisticated class of savers.

Big Four still reliant on high velocity deposits

Sources: McKinsey Global Institute, Putting China’s Capital to Work, May 2006

2

18

25

55

0 20 40 60

Affluent Mass affluentMiddle income Mass retail

2% of households are responsible for more than half of state-owned banks’ deposits and profits

Customers by segment (%) % branch profitability

55

48

8

-11

-50 0 50 100

Affluent Mass affluentMiddle income Mass retail

On the asset side, the Big Four banks are still oriented toward the large state-owned enterprises. While many SOEs have improved their financial performance and balance sheets, there is no question that some SOEs are not competitive. OECD studies suggest that SOE productivity overall is half that of private enterprise in China.3 Yet, loan growth is still high. Thus, concern remains as to the quality of new assets that the Big Four are writing. Indeed, a number of credit rating agencies and other observers have published research reports that indicate the current level of problem loans is US$160 bn, or as much as the current US$164 bn in official NPLs among all commercial banks.4

2 China’s large four state-owned banks are International Commercial Bank of China (ICBC); Bank of China (BOC); China Construction Bank (CCB); and Agricultural Bank of China (ABC) 3 Dougherty and Herd, 2005, OECD 4 China: Taking stock of Banking System NPLs, Fitch Ratings, May 2006

Economics@ANZ ANZ International Economics Monthly – June 2006

Page 3

Loan growth to SOEs is still high

Sources: McKinsey Global Institute, Putting China’s Capital to Work, May 2006

0%

20%

40%

60%

80%

100%

# of e

nter

prise

s

Cont

rib to

GDP

Shar

e of lo

ans

Local private SMEsQuasi-private/foreign/large localSOEs

% of total

Profile of bank loans (2002)

0

50

100

150

200

250

300

350

2001 2002 2003 20040

5

10

15

20

25

New loans issued

RMB tr

Nominal (LHS)

% GDP (RHS)

% GDP

Controlled competition

It is clear that the Chinese authorities intend to increase the level of competition in the banking system by opening up both the domestic and foreign markets. Indeed, some local observers have characterised the introduction of the QDII legislation as “aggressive”, with a scope and timetable well in advance of what many were expecting. It is also clear, however, that ensuring stability in the banking system is a much higher policy priority. This is why we expect that the ongoing process of liberalising the banking sector, the capital account, interest rates and the exchange rate regime will continue to proceed very cautiously and slowly; there will be no “Big Bang” in China.

First, the authorities will continue to exert control over the banking system through opaque regulation, which allows for plenty of administrative intervention. Licensing to qualify for the QDII or QFII programs is not straightforward. Even after licenses have been approved, interpretation of regulations remains a major challenge for most firms. Market participants, and particularly foreign institutions, generally err on the side of caution in order to avoid punitive action by the regulators.

Second, enabling regulations have numerous exemptions. For example, although commercial banks licensed under QDII can convert RMB to foreign currency and invest offshore, those investment choices are limited to the fixed income market. On the other hand, fund managers (who operate under different licenses to banks) can only raise foreign currency funds, but can invest in both fixed income and equity.

Third, existing regulations change frequently. For example, starting last year existing foreign banks operating in China encountered new restrictions on their use of so-called foreign debt quotas, otherwise known as overseas funding sources. This has restricted the ability of foreign banks to bring foreign currency onshore, and has forced an increased reliance on funding from local banks.

We expect regulatory mechanisms such as licensing and quotas to continue to hamper competition in the financial market in China until the authorities are comfortable about the position of the major banks.

Implications for FX policy

The above scenario has important medium-term implications for the Chinese economy, including potentially lower productivity growth, a long-term build-up of contingent liabilities and a continued excessively high domestic savings rate (with lower household consumption). In the short term, however, the main macro implications are for the exchange rate and monetary policy because of the expected slow pace of capital account liberalisation.

The bottom line is that we believe that the government will continue to resist pressure to free the exchange rate for several years – not because the authorities are dedicated to maintaining a fixed exchange rate, but because it is unwise and probably impossible for any government to attempt to have both a floating exchange rate and a closed capital account.

The RMB can only find its market-clearing rate when all capital is free to move across China’s borders, both into and out of the country. However, some regulatory bodies are extremely hesitant to allow capital to leave the country unabated, for fear of a surge of outflows that could destabilise the banking system and/or reduce interest in the domestic capital markets. Although it is hard to envision it now, as recently as 2002 the authorities were far more concerned about capital outflows than capital inflows. The chart below shows net capital flows on commercial bank debt were negative for 5 consecutive years following the Asian crisis, which presented a far greater risk at the time given the smaller current account surplus.

China’s foreign capital inflows

-40

-20

0

20

40

60

80

100

120

140

160

1990 1993 1997 2000 2004

US$ bn

Source: IIF

-20

0

20

40

60

199019931996199920022005

FDIPortfolio equityCommercial bank debtOther creditors

US$ bn

Current account balance Net foreign capital flows

The chart above also highlights the skew of cross-border capital flows to China. Because of the concern about the possibility of outflows and a long-standing focus on promoting foreign investment, the

Economics@ANZ ANZ International Economics Monthly – June 2006

Page 4

implementation of the capital account regulation is more heavily weighted to preventing outflows than preventing inflows. Conversion of foreign currency to RMB requires documented proof of an underlying transaction for trade or purchase of a real asset; conversion from RMB to foreign currency faces a higher threshold and in many cases is simply not allowed. If a financial institution has documentary evidence from a local government that they have agreed to purchase a real (eg, non-financial) asset in China, the State Administration of Foreign Exchange (SAFE) as the regulator must allow the conversion of funds.

As a result of uneven regulation, the bias in terms of capital flows tends to be inflows over outflows – that is, China’s economy is facing surging foreign capital inflows, while outflows are minimal.

Is the RMB undervalued?

The massive ever-increasing foreign capital inflows into China have given rise to a commonly-held view that the currency is undervalued. Speculation, to the limited extent that it exists, has put some upward pressure on the currency. The weight of real and speculative inflows has brought foreign exchange reserves to US$925 billion as at May 2006.

However, in our view it cannot be assumed that the exchange rate is undervalued. If the Chinese government were to lift all capital controls tomorrow, what percentage of the banks’ US$2.5 trillion deposit base would be at risk of moving offshore? Taking a step back, M2 (currency in circulation + deposits + short-term liquid assets) is currently roughly US$4 trillion, or four times the level of foreign exchange reserves. As shown in the chart below, M2 has also been growing at a rapid rate, with a nominal increase of US$590 bn over the year to May as against a US$233 bn increase in FX reserves over the same period. A mere 10% shift in the monetary base to offshore right now would represent a loss of 43% loss of FX reserves.

FX reserves and monetary base

0

1

2

3

4

5

Jan-01 May-02 Sep-03 Jan-05 May-060

2

4

6

8

10

12US$ trillion M2/reserves

M2/FX reserves ratio(RHS)

M2 (LHS)

FX reserves (LHS)

Sources: Datastream, IMF, Economics@ANZ

Why would some funds move offshore? To put it simply, the rate of return on investment assets in China remains very low due to the lack of domestic financial market development. The chart below shows why the weighted average real return on household wealth across all assets in China is 1.3% pa as against 3.0% pa in the United States.

Real return on household wealth

Sources: McKinsey Global Institute, Putting China’s Capital to Work, May 2006

0.3

0.3

1.6

4.5

1.6

4.9

2.5

3.4

1.0

1.9

2.4

4.8

1.3

3.0

0 1 2 3 4 5 6

China

US

Bank deposits Pension and insuranceFixed income EquityMutual funds Real estateWeighted average

Over time, as China’s capital markets develop, rates of return should increase. This would reduce the risk of capital outflows when the capital account is liberalised – but since this process will take time, it is another argument in favour of a slow liberalisation of the capital account.

Meanwhile, as long as the capital account remains closed, and the exchange rate unable to equilibrate between the real demand and supply for RMB onshore and offshore, we believe the authorities will resist allowing the exchange rate to appreciate significantly.

We do not believe that the exchange rate will appreciate past USD/RMB7.0 for at least several years, if at all. First, the authorities are aware of the potential downward pressure on the RMB as the capital account is liberalised. Second, PPP-based models for the RMB suggest a fair value of around USD/RMB7.0-7.5. These models are skewed by the measures of relative prices in China, but still do not suggest the RMB is far off fair value at the current USD/RMB7.998. Third, a relatively weak exchange rate helps to attract investment and promote Chinese exports, although in our view the exchange rate is by far less important vis-à-vis China’s cost base than the relative costs of labour and capital. Fourth, the government has come to the view – to which we agree – that allowing slight currency appreciation simply signals that more appreciation is on its way, tending to fuel speculation. Finally, and most importantly, the authorities simply do not appear to believe that the exchange rate is significantly undervalued.

While we anticipate that the government will maintain a fixed or nearly-fixed exchange rate

Economics@ANZ ANZ International Economics Monthly – June 2006

Page 5

regime for some time, we expect continued measures aimed at building up the infrastructure for an eventual on-shore foreign currency market. The forward market opened in September, and the first licenses in the onshore swap market were issued in April. In June, the government announced it would trial some currency deregulation mechanisms in the Binhai province, with Tianjin as its major city. Currency volatility may be allowed to increase, for example by widening the intraday trading band from its current +/-0.3% margin.

The cause of rising FX reserves

Is the level of the exchange rate and expectations of ongoing appreciation principally responsible for rising foreign exchange reserves in China? FX reserves reached US$925 bn as of May, implying that reserves have been rising by an average of US$21 bn per month for the first five months of the year as against an average of US$18 bn per month in the second half of 2005. Reserve accumulation has accelerated even as capital flows and reserve accumulation in other Asian economies has slowed in the first half of this year.

At first glance, the cause of rising FX reserves appears to be the trade surplus and high FDI. However, trade and FDI do not tell the whole story. In 2005, the trade surplus plus FDI totalled US$160 bn, while FX reserves rose by US$210 bn, leaving 24% of the reserve accumulation unaccounted for by regulated inflows. In the 5 months to May 2006, trade + FDI was US$69 bn vs US$106 bn of reserve accumulation, or a 35% gap.

Conventional wisdom blames the gap to speculative inflows arising from currency appreciation plays, and blames high M2 growth on inflow-driven liquidity and incomplete sterilisation. There is, however, another potential explanation – that reserve accumulation is required by investors to cover a minimum percentage of M2, such that investors feel comfortable with their ability to convert future profits to foreign currencies. The chart below highlights the magnitude of difference in the monthly accumulation rates of M2 and reserves.

Liquidity driven by high loan growth

0

20

40

60

80

100

Oct-02 Apr-04 Oct-05

M2 Reserves

US$bn

M2 and FX accumulation

Sources: Datastream, IMF, Economics@ANZ

1.11.226,835Sing

3.53.31,259Indon

3.1

3.0

4.9

4.3

M2 / reserves current

3.1

2.9

4.4

4.7

M2 / reserves 2005 average

25,444Hong Kong

15,119Taiwan

2,576Thai

1,702China

GDP per capitaUS$

High liquidity

The reason why M2 is expanding so rapidly is not because of high foreign capital inflows, but rather because of high domestic loan growth, which is in turn the result of the growth-target strategy of local governments and their financiers. Local and provincial governments are quite powerful entities that enjoy both very soft budget constraints and strong relationships with local and regional banks. While the national authorities have announced measures aimed at stemming loan growth – first in 2004 and again this year – they have not reduced the growth and employment targets against which local government performance is measured. Targets aside, provincial governments are all keen to attract investment and boost growth. It is not surprising, therefore, that the tightening measures appear to have had little affect thus far.

If the above argument is correct, then it must be expected that China’s foreign exchange reserves will continue to rise as long as credit expansion continues at such a rapid pace in China. Comparing China to other economies as in the table above, which appears to put a benchmark for the M2/reserves at about 3, one of two things will happen. Either M2 will shrink by 25% to reach US$3 trillion or – more likely – reserves will rise to about US$1.4 trillion in the next year. While sterilising those reserves represent an ongoing cost to the People’s Bank of China, this is a cost that the authorities have proven they are willing to bear.

Liquidity also driving strong growth

Rapidly expanding credit is also driving high growth rates in China. Data flow for April and May suggest that the economy accelerated in the second quarter, raising the possibility that real GDP growth may be 10.5% YOY after 10.3% growth in the first quarter – results should be announced later in July. More measures aimed at cooling the economy should be anticipated, including higher interest rates, potentially higher reserve requirements, more guidance on lending criteria and perhaps measures to impose greater budget discipline at the local government level.

Domestic economy still accelerating

Sources: UN Statistics Database, Datastream, Economics@ANZ

Gross fixed capital formation

10

15

20

25

30

35

40

45

50

1970 1978 1986 1994 2002

Contribution to GDP ( )

US

AustraliaJapan

China

India

Real GDP growth

0

3

6

9

12

15

Q4 92 Q2 97 Q4 01 Q2 06

% ANZforecasts

Trend

Economics@ANZ ANZ International Economics Monthly – June 2006

Page 6

Although we suspect that foreign investment is not what is driving China’s burgeoning credit growth, there is still concern among regulators about the stability of foreign capital inflows and their impact on monetary policy. As such, efforts to cool lending growth could extend to foreign companies and financial institutions if the government chooses to wind back the favourable tax treatment that has to date been extended to foreign investment in China.

Amy Auster Head of International Economics Email: [email protected] Ph: +61 3 9273 5417 References: Lu, D (April 2006) “China’s Banking Sector Meeting the WTO Agenda” China Policy Institute The University of Nottingham McKinsey & Company (May 2006) “Putting China’s Capital to Work: The Value of Financial System Reform” McKinsey Global Institute

Economics@ANZ ANZ International Economics Monthly – June 2006

Page 7

Financial Markets Update

Exchange rates, US$ per local currency unit, indexed

80

85

90

95

100

105

110

115

Jan-06 Mar-06 Jun-06

03 Jan 2005 = 100

Korea

Australia

Japan

Taiwan

China

New Zealand

95

98

100

103

105

108

110

113

Jan-06 Mar-06 Jun-06

03 Jan 2005 = 100

Singapore

Indonesia

Malaysia

Thailand

Philippines

Vietnam

Exchange rates

• US dollar weakness, subsequent to the latest hike in the Fed Funds rate in late June, has provided some respite to currencies across the region. Nominal exchange rates had been in free fall since mid-May as investors withdrew from Asian markets amidst expectations of a US rate hike in late June, which became a reality.

• Volatility in exchange rates in the ASEAN region has increased significantly over the past few months. Strong regional appreciation over the first part of the year unwound significantly throughout May and June. However, the upward trend has seemingly now resumed post the Fed Funds rate hike in late June.

• The Indonesian rupiah climbed by around 6% from February to May only to drop the same amount in some turbulent days in mid-May. The rupiah has rallied 3% since mid-June, posting the largest gains in the region.

90

95

100

105

110

115

120

125

130

135

140

Jan-04 Jul-04 Jan-05 Jul-05 Jan-06

Jan 2003=100

NZ

Taiwan

Australia

Korea

Japan

Real exchange rates, US$ per local currency unit, indexed

90

100

110

120

Jan-04 Jul-04 Jan-05 Jul-05 Jan-06

Jan 2003=100

Indonesia

Thailand

Philippines

Malaysia

Singapore

Real Exchange rates

• The latest data in this chart, which is May, shows real exchange rates of the Philippines and Indonesia depreciating amidst moderating inflation and weak nominal exchange rates.

• Further evidence of a pick-up in economic activity and expectations of higher inflation as well as a stronger yen led to a sharp appreciation in Japan’s real exchange rate in May.

• Higher inflation in Australia has exaggerated the appreciation of the real exchange rate beyond its nominal rate of increase. The decline in New Zealand’s real exchange rate halted in May assisted by an appreciating nominal exchange rate.

Policy rates

0

1

2

3

4

5

6

7

8

Mar-05 May-05 Aug-05 Nov-05 Feb-06 May-06

Hong Kong

Korea

Taiwan

%

US

Australia

New Zealand

0

2

4

6

8

10

12

14

Mar-05 May-05 Aug-05 Nov-05 Feb-06 May-06

Thailand

Malaysia

Philippines

%

Singapore

Indonesia

Policy rates

• We still forecast the Fed Funds rate to peak at 5.5% in 2006 from the current 5.25%, with the next hike expected at the August meeting.

• Policy rates in the economies of North Asia and Australia are still firmly on an upward trend. Rates in the ASEAN region, however, seem to be reaching the top of their tightening cycles. In the case of Indonesia, the central bank has begun to adopt a loosening stance. After the impact of reduced fuel subsidies on petrol prices eases off in the second half of 2006, inflation is expected to broadly moderate across ASEAN.

• Another 25 bps rate hike is expected for Australia later in 2006 as core inflation edges closer to the top of the target band.

Economics@ANZ ANZ International Economics Monthly – June 2006

Page 8

Government Bond Index

1

2

3

4

5

6

Sep-05 Nov-05 Jan-06 Apr-06 Jun-06

Korea

Yield (on traded index)

Australia

Hong Kong

China

Japan

1

3

5

7

9

11

13

15

17

Sep-05 Nov-05 Jan-06 Apr-06 Jun-06

Indonesia

Thailand

Yield (on traded index)

Philippines

Malaysia

Singapore

Source: JPMorgan

Philippines’ index is the 10-year bond yield as there is no GBI index.

Bond markets

• Trends in the fixed income markets have been mixed over recent months. A gradual upward drift in yields is apparent across North Asia due to rising inflation expectations. Markets closely linked to the US, in Hong Kong and Australia, have climbed the most rapidly as US yields continue to rally on accelerating inflation expectations and higher cash rates.

• Yields in Japan have moderated in recent months. The upward trend in yields in the first quarter was based on inflation expectations that were buoyed by positive momentum in both the core and headline measures. However, yields now appear to be in pause mode, awaiting BOJ’s exit from its zero interest rate policy.

• Significant upward movements in yields were experienced in the Philippines and Indonesia as investors removed funds from these lower-rated debt markets. The higher-rated markets in the rest of the ASEAN region remained relatively insulated from these capital outflows.

Foreign exchange reserves

0

100

200

300

400

500

600

700

800

900

1,000

2001 2002 2003 2004 2005 2006

China

US$ bn

Korea

Japan

Taiwan

0

20

40

60

80

100

120

140

160

180

2001 2002 2003 2004 2005 2006

Singapore

Hong Kong

US$ bn

Malaysia

Thailand

India

Indonesia

Source: Bloomberg

International reserves

• Reserve accumulation in China showed no signs of letting up with a US$20 bn increase in April followed by a US$30 bn rise in May. Reserves now stand at US$925 bn, surging well above the second highest reserves holder Japan at US$842 bn. At this pace, China’s reserves will reach US$1 tr before year’s end. Reserves growth was again driven by strong trade and investment flows. China's trade surplus hit a record high of US$13bn in May, bringing the surplus for the first five months of the year to around US$47bn. China has also attracted US$23bn in foreign direct investment in the five months to May.

• India’s foreign reserves have resumed their upward trend bolstered by strong remittance flows and FDI in recent months, and despite a local equity market sell-off.

Share price indices

60

80

100

120

140

160

180

Jan-05 Jun-05 Dec-05 May-06

1 Jan 2004 = 100

HK

Japan

Korea

Taiwan

China

50

75

100

125

150

175

200

225

Jan-05 Jun-05 Dec-05 May-06

1 Jan 2004 = 100

Singapore

Malaysia

Indonesia

Philippines

Thailand

Source: Datastream

Equity markets

• Stockmarkets edged up in the final week of June after the sharp correction which began in mid-May. For North Asia, the indices were still above that recorded at the start of the year. However, for Southeast Asia, the May fall-out has led to serious erosion of gains made through the year.

• In contrast to other North Asian markets, the rally in China’s stockmarket in 2006 has been rapid, reflecting ample liquidity.

• Thailand’s financial markets have been fairly resilient given the current uncertain political backdrop that has put a cloud on investment prospects.

Economics@ANZ ANZ International Economics Monthly – June 2006

Page 9

Foreign Exchange and Policy Rate Forecasts May-06 Jun-06 Sep-06 Dec-06 Mar-07 Jun-07 Sep-07

China

USD/CNY, eop 8.02 7.99 7.91 7.79 7.73 7.67 7.61 AUD/CNY, eop 6.03 5.91 5.69 5.45 5.33 5.21 5.17 One year base lending rate 5.85 5.85 6.12 6.12 6.12 6.12 5.85 Hong Kong USD/HKD, eop 7.76 7.79 7.78 7.78 7.77 7.76 7.75 AUD/HKD, eop 5.84 5.76 5.60 5.45 5.36 5.28 5.27 HKMA discount rate 6.25 6.75 7.00 7.00 7.00 6.50 6.00 India USD/INR, eop 46.4 45.5 45.0 44.5 44.3 44.0 43.5 AUD/INR, eop 34.9 33.7 32.4 31.2 30.5 29.9 29.6 Reverse Repo rate 5.50 5.75 6.00 6.00 6.00 5.75 5.50 Indonesia USD/IDR, eop 9,255 9,000 8,900 8,750 8,700 8,650 8,600 AUD/IDR, eop 6,962 6,660 6,408 6,125 6,003 5,882 5,848 BI rate 12.75 12.50 11.50 10.25 9.50 8.50 7.25 Korea USD/KRW, eop 946 970 960 950 960 970 980 AUD/KRW, eop 711 718 691 665 662 660 666 Overnight call rate 4.00 4.25 4.50 4.75 4.75 4.50 4.50 Malaysia USD/MYR, eop 3.63 3.62 3.59 3.57 3.55 3.54 3.52 AUD/MYR, eop 2.73 2.68 2.58 2.50 2.45 2.40 2.39 Overnight policy rate 3.50 3.50 3.75 3.75 3.50 3.25 3.25 Philippines USD/PHP, eop 52.9 52.0 51.5 50.8 50.5 50.3 50.0 AUD/PHP, eop 39.8 38.5 37.1 35.5 34.8 34.2 34.0 Overnight Reverse Repo rate 7.50 7.50 7.75 7.75 7.50 7.25 7.25 Singapore USD/SGD, eop 1.58 1.57 1.56 1.55 1.55 1.54 1.54 AUD/SGD, eop 1.19 1.16 1.12 1.09 1.07 1.05 1.05 3-month interbank rate 3.44 3.50 3.60 3.60 3.60 3.50 3.40 Taiwan USD/TWD, eop 32.0 31.8 30.5 30.0 29.8 29.5 29.3 AUD/TWD, eop 24.1 23.5 22.0 21.0 20.5 20.1 19.9 Discount rate 2.38 2.50 2.63 2.50 2.50 2.40 2.40 Thailand USD/THB, eop 38.1 38.0 38.5 37.8 37.0 36.8 36.5 AUD/THB, eop 28.7 28.1 27.7 26.5 25.5 25.0 24.8 14-day repo rate 4.75 5.00 5.00 5.00 4.75 4.50 4.25 Vietnam USD/VND, eop 15,958 16,015 16,047 16,079 16,122 16,154 16,186 AUD/VND, eop 12,003 11,851 11,554 11,255 11,124 10,985 11,007 Japan USD/JPY, eop 112.7 115.0 110.0 105.0 102.0 100.0 98.0 AUD/JPY, eop 84.7 85.1 79.2 73.5 70.4 68.0 66.6 Overnight call rate 0.01 0.00 0.25 0.5 0.50 0.75 1.0 Australia AUD/USD, eop 0.75 0.74 0.72 0.70 0.69 0.68 0.68 Cash rate 5.50 5.75 5.75 6.00 6.00 6.00 6.00 New Zealand NZD/USD, eop 0.63 0.62 0.60 0.58 0.55 0.53 0.53 AUD/NZD, eop 1.19 1.19 1.20 1.21 1.25 1.28 1.28 Overnight call rate 7.25 7.25 7.25 7.00 6.50 6.50 6.00

Economics@ANZ ANZ International Economics Monthly – June 2006

Page 10

Macro Economic Forecasts Real GDP Growth (%)

2004 2005 2006f 2007f

Australia 3.6 2.5 2.9 3.1

Cambodia 7.7 9.6 7.9 7.6

China 10.1 9.9 9.8 8.9

Hong Kong 8.6 7.3 4.8 3.5

India+ 7.5 8.4 7.5 7.2

Indonesia 5.0 5.6 4.8 6.4

Japan 2.3 2.6 2.4 2.0

Korea 4.7 4.0 5.0 3.2

Malaysia 7.1 5.3 5.4 5.0

New Zealand 4.3 2.3 1.5 1.4

Philippines 6.0 5.1 4.5 4.3

Singapore 8.7 6.3 7.0 5.0

Taiwan 6.1 4.1 5.1 3.0

Thailand 6.2 4.6 4.5 4.3

Vietnam 7.7 8.4 7.8 7.4

Nominal GDP (US$ bn)

2004 2005 2006f 2007f

Australia 637.4 705.4 725 715.9

Cambodia 4.9 5.2 5.4 5.6

China 1931.0 2175.6 2437.4 2680.8

Hong Kong 165.7 173.6 185.7 196.8

India+ 670 753 845 935

Indonesia 257.6 300 345 390

Japan 4674.7 4672.3 4765.7 4813.4

Korea 681.5 799.7 847.7 890.1

Malaysia 117.7 125 136 146

New Zealand 97.8 108.6 99.4 89.9

Philippines 86.1 98 110 122

Singapore 106.8 114 123 130

Taiwan 305.4 330.7 350.6 368.1

Thailand 161.7 177 195 208

Vietnam 45.3 53.1 61.3 69.6

Inflation (%)

2004 2005 2006f 2007f

Australia 2.3 2.7 2.9 2.7

Cambodia 3.8 5.8 5.3 5.0

China 3.9 1.8 2.5 3.0

Hong Kong 0.0 0.8 1.8 1.5

India+ 3.8 4.1 4.5 3.5

Indonesia 6.1 10.4 12.7 7.7

Japan 0.0 -0.2 0.2 0.9

Korea 3.6 2.8 3.1 3.8

Malaysia 1.4 3.1 4.0 3.0

New Zealand 2.7 3.2 3.7 2.7

Philippines 5.9 7.7 7.5 6.0

Singapore 1.7 0.5 1.5 0.9

Taiwan 1.6 2.3 3.0 2.5

Thailand 2.8 4.5 4.8 3.0

Vietnam 7.8 8.2 6.0 4.5

Fiscal Balance (% of GDP)*

2004 2005 2006f 2007f

Australia 1.2 1.7 1.0 1.0

Cambodia -5.4 -5.6 -5.8 -6.0

China -2.1 -1.1 -2.0 -1.9

Hong Kong -0.4 -0.4 -0.4 -0.7

India+ -4.5 -4.2 -3.8 -3.6

Indonesia -1.6 -0.5 -1.4 -0.8

Japan -6.5 -6.2 -6.0 -5.8

Korea 0.7 -0.3 -0.8 -0.2

Malaysia -4.3 -3.3 -3.0 -2.3

New Zealand 5.2 4.1 5.8 3.3

Philippines -3.9 -2.8 -2.1 -1.5

Singapore -0.1 0.2 -1.3 0.1

Taiwan -2.5 -2.5 -2.2 -2.4

Thailand 0.1 -1.2 -1.7 -1.4

Vietnam -1.7 -2.1 -2.3 -2.9

Current Account (% of GDP)

2004 2005 2006f 2007f

Australia -6.3 -6.0 -5.4 -6.0

Cambodia -10.1 -10.9 -10.6 -10.3

China 4.0 6.7 4.4 4.0

Hong Kong 9.5 9.3 5.6 2.1

India+ -0.1 -2.1 -2.5 -2.5

Indonesia 1.2 0.5 1.2 1.6

Japan 3.8 3.9 4.0 3.5

Korea 4.1 2.4 1.7 1.2

Malaysia 12.5 11.7 8.9 6.6

New Zealand -6.7 -8.9 -10.2 -8.3

Philippines 2.6 2.0 2.0 1.8

Singapore 26.1 28.5 24.0 22.0

Taiwan 5.8 3.4 3.1 2.5

Thailand 4.1 -1.4 -1.1 -1.0

Vietnam -2.1 -2.7 -3.6 -4.0

Foreign Exchange Reserves (US$ bn)

2004 2005 2006f 2007f

Australia 33.9 43.3 n.a. n.a.

Cambodia 0.94 0.95 0.94 0.96

China 609 818 925 850

Hong Kong 123 123 125 127

India 126.5 138 150 155

Indonesia 34.9 33 35 40

Japan 833 828 815 800

Korea 198 215 230 220

Malaysia 66.6 70.5 75 80

New Zealand 6.9 9.1 n.a. n.a.

Philippines 13.1 16 17.5 18.5

Singapore 112.2 117 122 125

Taiwan 241 253 265 270

Thailand 48.7 50.7 52 54

Vietnam 7.0 8.9 9.6 10.2

+: Fiscal year beginning April; *:Fiscal balance for Australia, New Zealand, Malaysia and Singapore corresponds to fiscal year

Economics@ANZ ANZ International Economics Monthly – June 2006

Page 11

Long Term Foreign Currency Government Bond Ratings

Investment Grade Sub-Investment Grade

Moody’s S&P Moody’s S&P

Aaa AAA Ba1 BB+ Australia Australia Costa Rica Egypt Canada Canada Egypt El Salvador France France Morocco India

Germany Germany Panama Morocco Japan Singapore Romania

New Zealand United Kingdom Singapore United States Ba2 BB

United Kingdom Colombia Colombia United States Fiji Costa Rica

Guatemala Jordon Aa1 AA+ Jordan Panama

Belgium Belgium Peru Brazil New Zealand Ba3 BB-

Aa2 AA Peru Cook Islands Italy Vietnam Guatemala Aa3 AA- Brazil Philippines

Cayman Islands Hong Kong Turkey Serbia Taiwan Italy Turkey

Japan Venezuela Taiwan Ukraine

A1 A+ Vietnam Czech Republic Qatar

Hong Kong Kuwait B1 B+ Hungary Papua New Guinea Ghana Macau Philippines Indonesia Qatar Suriname Pakistan UAE Ukraine A2 A Indonesia

China Chile B2 B Cyprus Cyprus Honduras Papua New Guinea Israel Korea Pakistan Uruguay Kuwait Saudi Arabia Venezuela Argentina Poland

A3 A- B3 B- Korea China Argentina Bolivia

Malaysia Czech Republic Bolivia Lebanon Saudi Arabia Hungary Lebanon Paraguay

Israel Uruguay Suriname Malaysia

Baa1 BBB+ Caa1 and below CCC and below Chile Oman Cuba Belize

Mexico Poland Ecuador Ecuador South Africa Thailand Nicaragua Thailand South Africa Paraguay

Oman Belize Baa2 BBB

Mauritius Mexico Tunisia Tunisia Russia Bulgaria

Russia Baa3 BBB-

El Salvador Romania India

Bulgaria

At the end of May, Moody’s changed its ratings methodology and established new country ceilings that are 1 or 2 notches above the sovereign credit rating for many countries rated A and below. Bloomberg’s CSDR page now shows the new country ceilings rather than the old sovereign bond ratings. We are evaluating the change and how we will interpret the new ratings.

Economics@ANZ ANZ International Economics Monthly – June 2006

Page 12

Country Update: Australia Growth back to trend

0

1

2

3

4

5

03 04 05 06

% change

Quarterly

Year-ended

Retail sales remain solid, but petrol is beginning to bite

60

70

80

90

100

110

120

130

140

03 04 05 060

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

Retail Sales (RHS) Petrol price(LHS)

cents per litre % ch trend

Sources: Australian Bureau of Statistics

• GDP grew by 0.9% in the March quarter, lifting theannual rate to 3.1% - the first time it has been above 3%since the September quarter 2004. Householdconsumption was the primary driver of growth in thequarter, providing the first ‘hard’ evidence that thecaution that has characterised consumer spending overthe past year is beginning to recede.

• Retail sales eased by 0.3% in May, following a strong1.1% surge in April. Trend growth in retail spending hasslowed marginally this year, providing some evidence thatthe rise in petrol prices over this period has begun to bite.Nevertheless, at 0.6%, trend monthly growth in retailspending in the first five months of 2006 is around doublethe pace of the final five months of 2005, confirming thesolid underlying path of consumer demand.

• Private sector credit grew by a robust 1.1% in May, withbusiness credit up 1.1% and household credit up 1.0%.The ongoing robust credit growth is indicative of theunderlying strength of domestic economic conditions andrefutes the view that the household sector is facing animminent balance sheet correction. Our analysissuggests that both the business and household sectorsretain ample capacity for further debt accumulation.

• The labour market also strengthened further, withemployment up by a massive 56,000 jobs in May, and theunemployment rate falling to 4.9% - the lowest level inaround 30 years.

• Recent data suggest underlying momentum in theeconomy may be a little stronger than we had thought.However, we expect the RBA will proceed cautiously.These data pre-date the May rate rise. We expect theRBA will wait to gauge the effects of these factors beforemoving again, opening the door for a 25bp rate risetoward the end of the year.

Mark Rodrigues

Economic data – Australia Monthly data Oct 05 Nov 05 Dec 05 Jan 06 Feb 06 Mar 06 Apr 06 May 06 Building Approvals, 000’s 12.3 12.7 12.3 12.1 12.2 12.7 12.3 12.7 Retail Sales, % YOY 3.1 3.1 3.9 4.6 4.6 5.0 7.3 5.2 Exports, % YOY 14.3 15.8 24.1 13.4 24.4 19.3 14.6 n/a Imports, % YOY 5.6 11.6 11.2 13.0 10.1 9.9 13.1 n/a Trade Balance, AUD bn -1.33 -2.40 -0.98 -2.40 -0.43 -1.51 -1.09 n/a Foreign Exchange Reserves, US$ bn 41.2 42.9 43.3 43.7 41.4 44.3 48.5 51.3 Quarterly data Jun 04 Sep 04 Dec 04 Mar 05 Jun 05 Sep 05 Dec 05 Mar 06 Real GDP, % YOY 4.7 3.3 2.0 2.0 2.7 2.6 2.9 3.1 - Private consumption 6.4 5.7 4.5 3.6 3.3 2.8 2.7 2.9 - Government consumption 3.3 4.0 3.9 3.1 3.8 1.8 2.6 1.9 - Gross fixed capital expenditure 10.8 6.9 5.2 3.0 7.9 9.1 9.7 12.0 Consumer Price Index, % YOY (nsa) 2.5 2.3 2.6 2.4 2.5 3.0 2.8 3.0 Current Account, AUD bn -12.1 -14.1 -16.0 -15.3 -12.1 -13.5 -14.3 -14.0 Capital Account, AUD bn (nsa) 11.3 15.5 15.4 14.6 10.8 15.7 13.3 13.7

Sources: Australian Bureau of Statistics, RBA. Note: data seasonally adjusted unless otherwise stated

Economics@ANZ ANZ International Economics Monthly – June 2006

Page 13

Country Update: Cambodia

Cambodia: Exports to US, Imports from Asia

0

50

100

150

200

250

300

350

00 01 02 03 04 05 06

Imports from

Exports to

January-00 to December 05

$US mn

Asia Trade

0

20

40

60

80

100

120

140

160

180

200

00 01 02 03 04 05 06

$US mn

Exports to

Imports from

January-00 to Dec 05

US Trade

Source: IMF Direction of Trade Statistics

Heavily reliant on US as key exports market

0 15 30 45 60

US

Germany

Vietnam

UK

Canada

Japan

2004

2005

% of Total Exports

0 15 30

Thailand

China

HongKong

Vietnam

Singapore

Japan

2004

2005

% of Total imports

Exports Imports

Source: IMF Direction of Trade Statistics

• Cambodian GDP growth surprising on the upside for 2005 was in no small part due to significant improvements in trade performance. Strong export growth has been sustained despite increased competition in Cambodia’s only significant export industry, the garments trade. Significant liberalisation of this sector has occurred after the expiration of both the Agreement on Textiles and Clothing at the end of 2004 and the Multi-fibre Agreement at the end of 2005. Cambodia’s overall merchandise exports increased by 10.2% in 2005, with significant growth in the key market of the US. Exports to the US grew by 18.2% in 2005 as Cambodia continues to pick up market share in US garment sector. In other key markets, fortunes were mixed, with exports to the EU down by 11.1%. However, much of this fall was offset by a 21.3% increase in exports to Asia. Exports to close neighbours Vietnam and Thailand both increased significantly as Cambodia seeks to forge closer relations with these countries. Crackdowns on border smuggling, particularly in petrol, may have also assisted these bilateral trade relationships. Exports to the US accounted for around 60% of Cambodia’s total exports in 2005 followed by 21% to the EU and 10% to Asia.

• Virtually all of Cambodia’s exports to the US are garments (averaging around 97% over the last 3 years). US trade data indicates that Cambodia’s exports to the US have increased around 29% in the first four months of 2006 (c/w same period in 2005). This performance has been supported by the US (and EU) continuing to contain garment imports from China and Vietnam. In addition, the “Better Factories Cambodia” project, funded by the ILO, has boosted productivity and improved labour conditions. Both of which have assisted export performance and encouraged the manufacturing base to expand significantly. Ministry of Commerce figures for April indicate an 11% increase in the number of employees in the garments sector, to 293,600, since January 2005. The number of garment manufacturing factories also increased by around 13% during 2005.

Alex Joiner

Economic data – Cambodia Monthly data Oct 05 Nov Dec 05 Jan 06 Feb 06 Mar 06 Apr 06 May Consumer Price Index, % YOY 6.4 6.7 6.7 6.3 6.2 5.9 4.8 4.9 -Transport & Communication 11.4 10.0 9.1 10.2 9.9 8.9 9.5 10.5 -Food & Beverages 10.0 10.8 11.1 10.8 10.7 10.2 7.4 7.2 Exports, % YOY 10.8 13.8 23.1 30.6 n/a n/a n/a n/a Imports, % YOY 16.8 11.2 21.0 18.7 n/a n/a n/a n/a Trade Balance, US$ mn -89.2 -83.8 -117.7 -28.4 n/a n/a n/a n/a Foreign Exchange Reserves, US$ mn 942.2 929.2 952.7 959.1 981.9 1,002.7 n/a n/a Tourist Arrivals, % YOY 41.9 26.8 34.5 17.5 21.1 14.3 23.1 n/a GDP Composition 2004 Trading Partners Exports Imports Real GDP, % YOY 7.7 2004 % share US 55.9 Viet’m 10.9 - Agriculture, % YOY -2.0 Germany 11.7 Thail’nd 22.5 - Industry, % YOY 16.1 UK 6.9 Sing 10.8 - Services, % YOY 9.2 Vietnam 4.4 China 13.6 Nominal GDP, US$ bn 4.89 Japan 3.5 HK 14.1

Sources: Datastream, National Institute of Statistics of Cambodia

Economics@ANZ ANZ International Economics Monthly – June 2006

Page 14

Country Update: China

CPI accelerating as base effect of 2004 grain spike wear off and liquidity expands

-10

0

10

20

Jan-01 Jul-02 Jan-04 Jul-05-30

-20

-10

0

10

20

30

40% YOY

Grain

Food

House lease

CPI

CPI

Sources: Bloomberg, Datastream

M2 growth

0

5

10

15

20

25

30

Jan-01 Jul-02 Jan-04 Jul-05

% YOY

Fixed asset investment is still growing strongly

-20

-10

0

10

20

30

40

50

60

70

80

90

100

Feb-05 Jun-05 Oct-05 Feb-06

% YOY

Metal products

Transportequip

Food and beverage

All manuf

Fixed asset investment – by manufacturing sector

Sources: Bloomberg, Datastream

-20

-10

0

10

20

30

40

50

60

Feb-03 Jun-04 Oct-05

% YOY

Total urban

Secondaryindustry

Local projects

Tertiary industry

Fixed asset investment – by economic sector

• The economy shows no sign of slowdown. Activity in fact appears to have accelerated in the second quarter, raising the possibility that GDP growth will exceed the 10.3% YOY recorded in the first quarter. Industrial production rose 23% YOY in May, with heavy industry growth still outpacing that of light industry, as exports rose 25% YOY. Perhaps more surprising, consumption data appears to have ticked upward with retail sales rising 14.2% YOY after average annual growth of 12.8% in the first quarter. Imports, perhaps the most reliable high frequency indicator of total domestic demand, rose 21.7% YOY in May after growth of 24.8% in the first quarter.

• In addition to strong activity, CPI has recorded its first strong increase in May, rising 1.4% YOY as against an average of 1.2% YOY in the first quarter. The uptick is no doubt related to the wearing off of the base effect of the 2004 grain price spike, with grain prices rising 2.9% YOY (nsa) in April and 3.4% YOY (nsa) in May after recording significant deflation for the past 18 months. The cost of rent and house leasing also turned positive – in the case of rental prices, it is the first positive annual price rise since the series was introduced in 2002.

• As expected, the authorities continued to announce measures to cool the economy by raising the reserve requirement to tighten liquidity in the banking system. Three powerful central agencies issued further warnings to local governments on the need to rein in investment spending – though, as the charts show, fixed asset investment in manufacturing is also strong. Some observers have suggested that an upcoming reshuffle of provincial-level leadership is a key cause of the flood of investment, making it akin to election-year spending. However, we forecast ongoing tightening measures including another rise in lending rates as of August.

• The RMB appreciated by 0.25% in nominal terms in June after depreciating slightly in May. It is now trading at USD/RMB7.998 and is likely to continue to remain below the USD/RMB8.0 level.

Amy Auster

Economic data – China Monthly data Oct 05 Nov 05 Dec 05 Jan 06 Feb 06 Mar 06 Apr 06 May 06 Retail Sales, % YOY 12.8 12.4 12.5 15.5 9.4 13.5 13.6 14.2 Consumer Price Index, % YOY 1.2 1.3 1.6 1.9 0.9 0.8 1.2 1.4 Exports, % YOY 29.6 18.6 18.2 28.4 22.2 28.3 23.9 25.1 Imports, % YOY 23.4 21.0 22.2 25.3 29.5 21.1 15.3 21.7 Trade Balance, US$ bn 12.0 10.5 11.0 9.7 2.44 11.19 10.46 13 Foreign Exchange Reserves, US$ bn 784.9 794.2 818.9 845.2 853.7 875.1 895.0 925.0 Quarterly data Jun 04 Sep 04 Dec 04 Mar 05 Jun 05 Sep 05 Dec 05 Mar 06 Real GDP, % YOY 9.6 9.1 9.5 9.9 10.1 9.8 9.9 10.3 - Primary sector 4.9 5.5 6.3 4.6 5.0 5.0 5.2 4.5 - Secondary sector 11.5 11.1 11.1 10.9 11.0 10.9 11.4 12.5 - Tertiary sector 8.1 8.1 10.0 9.7 9.8 10.0 9.6 8.9 Nominal GDP, US$ bn 455.1 473.8 567.8 565.1 580.2 608.5 470.1 n/a Current Account, US$ bn 51.6 76.1 100.8 125.7 137.8 154.1 174.0 184.2 FDI (actual), US$ bn* 19.1 14.8 15.3 13.4 15.2 14.7 17.7 14.3 Sources: Datastream, Bloomberg * - Quarterly sum

Economics@ANZ ANZ International Economics Monthly – June 2006

Page 15

Country Update: Hong Kong

Tourism and retail sales softening but labour market tightness contributing to CPI rises

Tourism and retail

-8

-6

-4

-2

0

2

4

6

8

10

00 01 02 03 04 05 06

%

CPI, YOY

Unemployment

CPI and unemployment

Source: Datastream, Economics@ANZ

-20

0

20

40

60

01 02 04 05-100

-50

0

50

100

150

200

250% YOY

Visitor arrivals (RHS)

Retail sales , volume (LHS)

% YOY

Hang Seng rally contributing to local high liquidity

M2 growth

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

01 02 03 04 05 060

20

40

60

80

100

120Index

Hang Seng (LHS)

Index

Property prices (RHS)

Market prices

Source: Datastream, Economics@ANZ

-10

-5

0

5

10

15

20

25

30

01 02 04 05

% YOY

• The economy continues to benefit from its expanding ties to the mainland. Chinese IPOs on the Hang Seng are increasing its capitalisation and generating capital inflows, while rising visitor arrivals from China continue to outpace growth from other geographies. The government remains keen to benefit from the mainland’s boom, and this month signed off on the fourth phase of the Closer Economic Partnership Agreement to reduce cross-border restrictions in the areas of legal services, construction, tourism and air transport.

• Growing activity between Hong Kong and China is allowing the economy to absorb what would otherwise be dampening effects on growth. Exports have slowed to annual growth of only 8% as of May, while the property sector has softened with sharp declines in mortgage approvals and a softening of what had been strong rises in property prices. Retail sales have also softened, to an annual increase of only 2.0%, in volume terms, in May after rising at more than 8% in the first four months of the year. Nonetheless, unemployment reached a five-year low of 4.9% in May.

• Some of the overflow of China’s high liquidity can be seen in the Hong Kong economy, where M2 growth accelerated to 17.6% in May after average growth of 8.6% over the first four months of the year and despite ongoing official interest rate increases. The Hong Kong base rate rose to 6.75% in June, following the 17th US Federal Reserve hike. However, the prime lending rate offered by commercial banks has remained at 8% since March, in effect ignoring two official rate hikes. The CPI accelerated to 2.1% YOY in May, the highest rate since before the Asian crisis.

• Some of the costs associated with close proximity to the mainland are also becoming apparent; a report released last month by three local universities estimated that air pollution now brings economic losses equivalent to US$2.6 bn (1.5% of GDP) per year.

Amy Auster

Economic data – Hong Kong Monthly data Oct 05 Nov 05 Dec 05 Jan 06 Feb 06 Mar 06 Apr 06 May 06 Visitor Arrivals, %YOY 6.2 5.6 5.5 15.6 10.6 14.8 9.5 7.0 Retail Sales, % YOY 4.8 4.1 6.8 11.6 -3.2 9.1 9.4 5.3 Consumer Price Index, % YOY 1.3 1.2 1.4 1.8 1.3 1.7 1.9 2.1 Exports, % YOY 12.1 11.8 7.0 4.7 21.1 15.3 10.0 n/a Imports, % YOY 10.1 13.9 11.0 1.2 28.9 16.6 11.8 n/a Trade Balance, US$ bn 0.4 -0.5 -2.2 0.6 -3.0 -2.4 -1.9 n/a Foreign Exchange Reserves, US$ bn 121.9 122.4 124.3 127.8 125.7 125.9 127.0 126.5 Quarterly data Jun 04 Sep 04 Dec 04 Mar 05 Jun 05 Sep 05 Dec 05 Mar 06 Real GDP, % YOY 12.3 7.0 7.5 5.5 7.3 8.4 7.8 8.0 - Private consumption 11.2 5.7 6.0 4.1 2.4 3.6 3.4 4.5 - Government consumption 0.0 -1.3 -1.7 -4.6 -2.3 -1.6 -3.8 1.3 - Gross fixed capital expenditure 10.3 0.8 -2.4 0.4 4.9 2.8 8.4 8.5 Nominal GDP, US$ bn 41.5 41.1 42.1 42.7 44.3 44.9 45.8 n/a Current Account, US$ bn 0.6 6.5 7.5 4.2 4.1 5.6 6.4 4.6 Capital Account, US$ bn 0.0 -0.2 -0.1 -0.3 -0.2 -0.1 -0.1 n/a Source: Datastream

Economics@ANZ ANZ International Economics Monthly – June 2006

Page 16

Country Update: India Inflation picks up

Wholesale prices

4

5

6

03 04 05 06

% pa.

Policy rate

Sources: Bloomberg,Datastream

0

2

4

6

8

10

12

14

16

03 04 05

Annual % change

Reverse repo rateTotal WPI

Fuel

Current account reverts to surplus in Q1 2006

-20000

-15000

-10000

-5000

0

5000

10000

98 99 00 01 02 03 04 05

Sources: Bloomberg and Reserve Bank of India

US$ mn

Trade

Services

Transfers

Current account

• The central bank’s unexpected inter-meeting interest rate hike signals growing concerns over inflation risks. The RBI lifted its key reverse-repurchase rate by 25 bps to 5.75% on 8 June, three days after the government lifted gasoline and diesel prices. The wholesale price index, which is used as an inflation benchmark, has begun to gather momentum. It rose by 5.44% in the week ended 17 June, the fastest pace since 14 May 2005. Higher fuel costs together with increases in fruit and vegetable prices have lifted inflation. However, the government has recently taken steps to reduce import duties on essential commodities to help stem price increases. The import duty on wheat has been reduced to 5% from 50% with effect from 28 June till 31 December and pulses and sugar have been allowed in duty-free. Exports of pulses have also been banned.

• The RBI has maintained its inflation target of 5-5.5%. We expect that the central bank will lift its policy rate by another 25 bps to 6% at its next meeting on 25 July and the risk of a further rate hike has increased especially in the climate of global monetary tightening.

• The current account recorded a surplus of US$1.8 bn in the March quarter, underpinned by strong remittance inflows from Indians working abroad and revenue from software exports. For FY2005/06, the current account deficit widened to US$10.6 bn, compared with a shortfall of US$5.4 bn in FY2004/05. Foreign direct investment was a stronger US$2.04 bn in the March quarter compared with an average of US$1.2 bn over the past three quarters and portfolio investment Was US$4.3 bn.

• On the political front, the agreement between India and China to resume trade through the Himalayan Nathula Pass, which has been closed for more than 40 years, signals a further thawing of bilateral relations. India’s trade with China reached US$18.7 bn in 2005 or 7.8% of India’s total trade.

Jasmine Robinson

Economic data – India Monthly data Oct 05 Nov 05 Dec 05 Jan 06 Feb 06 Mar 06 Apr 06 May 06 Industrial Production, %YOY 9.4 5.9 5.9 8.9 8.9 8.8 9.1 n/a Passenger car sales, % YOY 2.3 0.0 1.3 8.5 7.7 19.1 21.0 27.7 Consumer Price Index, % YOY 4.2 5.4 5.6 4.4 4.6 4.6 4.6 n/a Exports, % YOY 30.3 22.7 26.9 25.7 12.3 20.6 12.1 21.6 Imports, % YOY 32.6 20.5 16.0 14.1 21.4 18.7 16.7 8.0 Trade Balance, US$ bn -3.2 -2.5 -2.7 -2.9 -3.2 -2.9 -4.2 -3.8 Foreign Exchange Reserves, US$ bn 137.0 137.0 131.0 134.0 136.0 145.0 154.0 n/a Quarterly data Jun 04 Sep 04 Dec 04 Mar 05 Jun 05 Sep 05 Dec 05 Mar 06 Real GDP, % YOY (at factor cost) 7.9 6.7 7.0 8.4 8.5 8.3 7.5 9.3 - Agriculture 6.6 8.0 8.1 6.8 9.5 6.3 7.0 7.9 - Industry 3.5 -0.2 -1.2 1.0 3.4 4.0 2.9 5.5 - Services 10.1 8.4 9.4 11.4 9.6 9.7 8.2 10.8 Nominal GDP, US$ bn 144.2 142.0 171.9 175.9 168.4 168.3 191.1 196.4 Current Account, US$ bn 3.4 -3.5 -5.5 0.2 -4.6 -5.1 -3.9 n/a Capital Account, US$ bn 4.5 3.1 11.7 12.4 5.4 9.9 -0.6 n/a Source: Datastream, Bloomberg

Economics@ANZ ANZ International Economics Monthly – June 2006

Page 17

Country Update: Indonesia Foreign reserves and debt indicators improve

20

25

30

35

40

45

00 01 02 03 04 05

US$ bn

Source: Datastream

Foreign reserves Debt Indicators

40

60

80

100

120

140

160

180

200

96 97 98 99 00 01 02 03 04 05

ratios

Debt to GDP

Short-term debt to reserves

Inflation moderates, lifting prospects for further interest rate cuts

Annual % change

Inflation

-8

-6

-4

-2

0

2

4

6

8

01 02 03 04 05

% pa

Real interest rates

Sources: Datastream, Bank Indonesia

-5

0

5

10

15

20

01 02 03 04 05

Total CPI

CPI-Food

• The government has indicated that its plans to pay US$3.7 bn of the US$7.8 bn owed to the IMF shortly. The partial repayment, which is ahead of its 2010 schedule, highlights the improvement in Indonesia’s external position with foreign reserves exceeding US$40 bn as at May 2006. The early payment will also alleviate the government’s debt servicing burden and offers scope for the reallocation of spending.

• The government is committed to maintaining fiscal discipline, having made inroads in containing the deficit in recent years. The fiscal deficit for 2006 is now estimated to reach 1.4% of GDP, up from the initial budget estimate of 0.7% of GDP. The government is expected to use funds left over from the 2005 budget to help mitigate the economic impact of high interest rates. However, the GDP growth estimate of 5.9% for 2006 appears optimistic.

• Partial indicators suggest that private consumption remains weak. Motor-cycle sales are still down by more than 20%. An expected easing in inflation will prompt further cuts in the BI rate in the months ahead and this will also help to lift both consumption and investment. Inflation continued its decline in June, moderating to 15.5% YOY, compared with 17% YOY at the start of the year. We expect a 50 bps cut in July, bringing the BI rate to 12%.

• The rupiah has weakened since early May, largely reflecting US dollar strength on the back of expectations of further US interest rate hikes. While a fall in Indonesian rates will also contribute to a further narrowing of interest rate differentials, Indonesian rates are still at a relatively high level and the current negative real interest rate gap will narrow and, we expect it to become positive in the second half of the year, giving some support to the currency.

Jasmine Robinson

Economic data – Indonesia Monthly data Oct 05 Nov 05 Dec 05 Jan 06 Feb 06 Mar 06 Apr 06 May 06 Industrial Production, %YOY -5.4 0.2 -4.7 -3.3 0.07 0.17 n/a n/a Motor cycle sales, % YOY 28.5 35.4 -3.0 -31.1 -9.0 -31.0 -33.5 -23.1 Consumer Price Index, % YOY 17.9 18.4 17.1 17.0 17.9 15.74 15.4 15.6 Exports, % YOY 4.8 11.5 22.1 22.5 15.18 1.14 11.89 n/a Imports, % YOY 15.3 3.7 -3.7 3.6 5.33 -12.93 -5.4 n/a Trade Balance, US$ bn 3.0 2.8 3.3 3.3 2.84 3.11 2.85 n/a Foreign Exchange Reserves, US$ bn 31.0 31.6 33.0 33.2 33.66 38.17 40.69 n/a Quarterly data Jun 04 Sep 04 Dec 04 Mar 05 Jun 05 Sep 05 Dec 05 Mar 06 Real GDP, % YOY 4.4 4.7 7.0 6.3 5.6 5.8 4.8 4.6 - Private consumption 5.3 5.1 3.9 3.4 3.8 4.4 4.2 3.2 - Government consumption 7.1 -1.6 -0.9 -8.1 -6.3 14.4 33.2 13.8 - Gross fixed capital expenditure 14.3 17.0 16.2 14.3 15.0 9.4 1.8 2.5 Nominal GDP, US$ bn 62.1 63.3 66.1 67.8 69.1 69.5 74.8 82.8 Current Account, US$ bn 2.2 2.8 0.3 1.0 0.9 -0.1 1.3 n/a Capital & Financial Account, US$ bn -0.7 0.9 1.1 0.1 -0.2 1.7 4.7 n/a Sources: Bloomberg, Datastream, Bank Indonesia

Economics@ANZ ANZ International Economics Monthly – June 2006

Page 18

Country Update: Japan

Leading indicators continue upward climb Leading indicators

-65

-55

-45

-35

-25

-15

-5

5

15

25

95 98 01 04

Index levelLarge enterprises

All businesses

Manufacturing

Tankan – business conditions

Source: Datastream, Economics@ANZ

30

40

50

60

70

80

90

100

110

Oct-01 Oct-03 Oct-05

Leadingeconomic

index

Index level

Purchasing managers' index

Market participants anticipating BOJ move Inflation

-15

-10

-5

0

5

10

00 01 02 03 04 05 06

% YOY

Industrial production

Retail sales

IP and retail sales

Source: Datastream, Economics@ANZ

-3

-2

-1

0

1

2

3

Oct-01 Oct-03 Oct-05

10-yr bondyield, % pa

%

Headline CPI, % YOY

Core CPI, % YOY

• The long-awaited Tankan survey report for June confirmed suspicions that business activity has continued to increase and the outlook to improve. Overall business conditions scored a 6, a level not seen since 1992. The diffusion index (DI) for large manufacturers rose by one point to 21, while the diffusion index for large non-manufacturers rose by 2 points to 20. The DI is a ratio of those who express a positive outlook as against a negative outlook for the economy.

• The Tankan survey led to increased speculation that the Bank of Japan will imminently end its zero interest rate policy and raise its overnight call rate to above zero at its 13-14 July meeting. We have pencilled in a rate hike for August, as we believe the BOJ will await second quarter GDP data before determining whether deflationary pressures have been vanquished.

• There are data that support a more cautious BOJ approach, such as an unemployment rate that is still above 4%; declining unit labour costs in the manufacturing sector; the failure of disposable income to rise despite tightening labour markets; and a lack of clear direction on consumption indicators such as retail sales. Most importantly, the GDP deflator remained in negative territory on a MOM and YOY basis in the first quarter, likely representing domestic productivity gains and a lack of pass through of higher input prices to end users by manufacturers.

• Another reason why the BOJ can afford to wait is because, unlike the US bond market, the Japanese bond market is already doing the central bank’s work. Yields on long-term bonds have risen by roughly 50 bps since the start of the year, or roughly the same amount as core inflation. In other words, the removal of quantitative easing and transmission of BOJ’s policy intentions are already tightening liquidity conditions in Japan and leading to a more neutral monetary policy stance. Under these conditions, the BOJ can afford to wait until it is convinced that deflation has left the building.

Amy Auster

Economic data – Japan Monthly data Oct 05 Nov 05 Dec 05 Jan 06 Feb 06 Mar 06 Apr 06 May 06 Industrial Production, %YOY 2.5 3.4 4.9 2.8 2.5 3.1 3.3 3.1 Retail Sales, % YOY -0.5 0.6 1.3 -0.4 1.1 1.1 -0.8 0.1 Consumer Price Index, % YOY -0.7 -0.8 -0.1 0.5 0.4 0.3 0.4 n/a Exports, % YOY 2.3 1.4 2.9 1.4 7.5 5.9 2.0 13.5 Imports, % YOY 11.7 3.1 11.6 13.4 16.0 12.5 10.2 12.6 Trade Balance, US$ bn 7.1 5.0 7.7 -3.1 8.0 8.2 5.6 3.4 Foreign Exchange Reserves, US$ bn 823.2 824.3 828.8 832.9 831.6 832.7 839.2 842.8 Quarterly data Jun 04 Sep 04 Dec 04 Mar 05 Jun 05 Sep 05 Dec 05 Mar 06 Real GDP, % YOY 2.6 2.3 0.5 1.1 2.7 2.7 4.0 3.5 - Private consumption 2.5 2.4 0.6 1.1 1.8 2.0 3.3 2.4 - Government consumption 2.2 1.6 1.4 1.9 1.4 2.1 1.6 0.8 - Gross fixed capital formation 0.9 1.5 -1.1 1.0 3.4 5.1 3.9 4.8 Nominal GDP, US$ bn 4643.7 4525.6 4515.0 4676.0 4766.3 4821.9 4771.2 4766.1 Current Account, US$ bn 179.1 171.4 170.2 170.9 167.9 165.5 167.4 200.4 Capital Account, US$ bn 2.7 2.3 0.5 1.1 2.7 2.7 4.0 3.0 Source: Datastream

Economics@ANZ ANZ International Economics Monthly – June 2006

Page 19

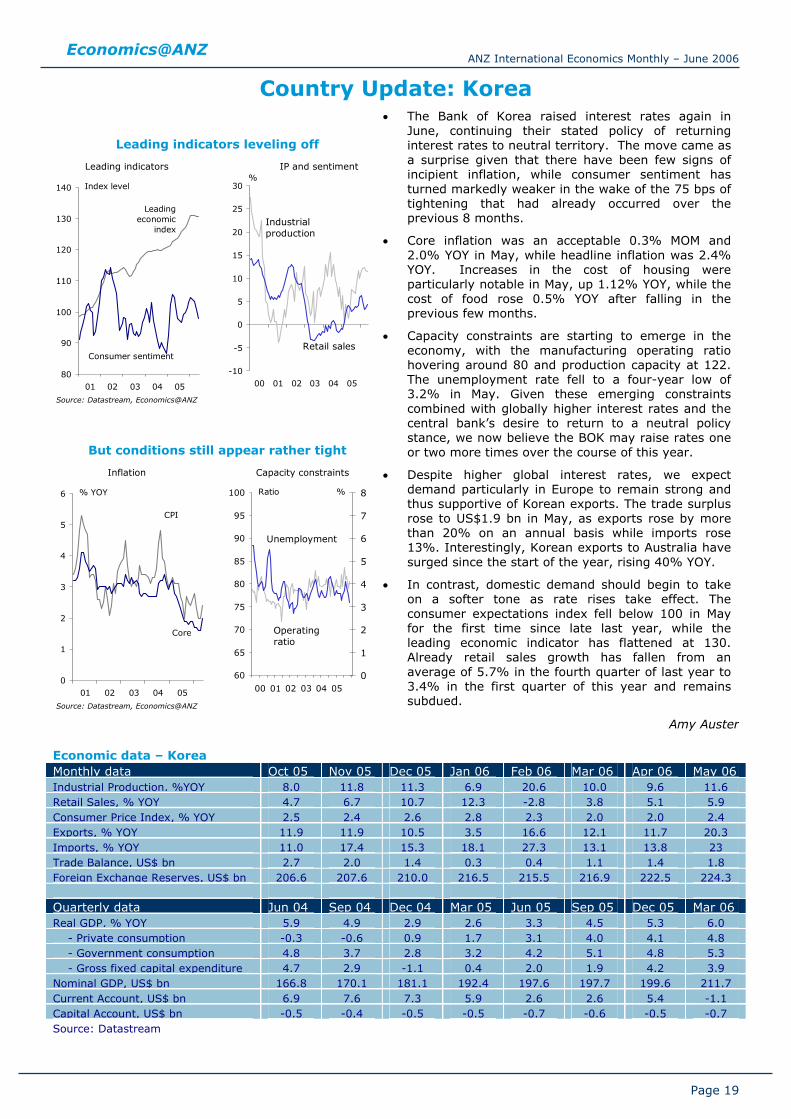

Country Update: Korea

Leading indicators leveling off

80

90

100

110

120

130

140

01 02 03 04 05

Leadingeconomic

index

Index level

Consumer sentiment

-10

-5

0

5

10

15

20

25

30

00 01 02 03 04 05

%

Industrial production

Retail sales

Leading indicators IP and sentiment

Source: Datastream, Economics@ANZ

But conditions still appear rather tight

0

1

2

3

4

5

6

01 02 03 04 05

CPI

% YOY

Core

60

65

70

75

80

85

90

95

100

00 01 02 03 04 050

1

2

3

4

5

6

7

8Ratio

Operating ratio

Unemployment

%

Inflation Capacity constraints

Source: Datastream, Economics@ANZ

• The Bank of Korea raised interest rates again in June, continuing their stated policy of returning interest rates to neutral territory. The move came as a surprise given that there have been few signs of incipient inflation, while consumer sentiment has turned markedly weaker in the wake of the 75 bps of tightening that had already occurred over the previous 8 months.

• Core inflation was an acceptable 0.3% MOM and 2.0% YOY in May, while headline inflation was 2.4% YOY. Increases in the cost of housing were particularly notable in May, up 1.12% YOY, while the cost of food rose 0.5% YOY after falling in the previous few months.

• Capacity constraints are starting to emerge in the economy, with the manufacturing operating ratio hovering around 80 and production capacity at 122. The unemployment rate fell to a four-year low of 3.2% in May. Given these emerging constraints combined with globally higher interest rates and the central bank’s desire to return to a neutral policy stance, we now believe the BOK may raise rates one or two more times over the course of this year.

• Despite higher global interest rates, we expect demand particularly in Europe to remain strong and thus supportive of Korean exports. The trade surplus rose to US$1.9 bn in May, as exports rose by more than 20% on an annual basis while imports rose 13%. Interestingly, Korean exports to Australia have surged since the start of the year, rising 40% YOY.

• In contrast, domestic demand should begin to take on a softer tone as rate rises take effect. The consumer expectations index fell below 100 in May for the first time since late last year, while the leading economic indicator has flattened at 130. Already retail sales growth has fallen from an average of 5.7% in the fourth quarter of last year to 3.4% in the first quarter of this year and remains subdued.

Amy Auster

Economic data – Korea Monthly data Oct 05 Nov 05 Dec 05 Jan 06 Feb 06 Mar 06 Apr 06 May 06 Industrial Production, %YOY 8.0 11.8 11.3 6.9 20.6 10.0 9.6 11.6 Retail Sales, % YOY 4.7 6.7 10.7 12.3 -2.8 3.8 5.1 5.9 Consumer Price Index, % YOY 2.5 2.4 2.6 2.8 2.3 2.0 2.0 2.4 Exports, % YOY 11.9 11.9 10.5 3.5 16.6 12.1 11.7 20.3 Imports, % YOY 11.0 17.4 15.3 18.1 27.3 13.1 13.8 23 Trade Balance, US$ bn 2.7 2.0 1.4 0.3 0.4 1.1 1.4 1.8 Foreign Exchange Reserves, US$ bn 206.6 207.6 210.0 216.5 215.5 216.9 222.5 224.3 Quarterly data Jun 04 Sep 04 Dec 04 Mar 05 Jun 05 Sep 05 Dec 05 Mar 06 Real GDP, % YOY 5.9 4.9 2.9 2.6 3.3 4.5 5.3 6.0 - Private consumption -0.3 -0.6 0.9 1.7 3.1 4.0 4.1 4.8 - Government consumption 4.8 3.7 2.8 3.2 4.2 5.1 4.8 5.3 - Gross fixed capital expenditure 4.7 2.9 -1.1 0.4 2.0 1.9 4.2 3.9 Nominal GDP, US$ bn 166.8 170.1 181.1 192.4 197.6 197.7 199.6 211.7 Current Account, US$ bn 6.9 7.6 7.3 5.9 2.6 2.6 5.4 -1.1 Capital Account, US$ bn -0.5 -0.4 -0.5 -0.5 -0.7 -0.6 -0.5 -0.7 Source: Datastream

Economics@ANZ ANZ International Economics Monthly – June 2006

Page 20

Country Update: Malaysia Inflation pressures likely to persist in second

half of 2006

Inflation Money supply

Source: Datastream

-10

-5

0

5

10

15

01 02 03 04 05

% YOY

PPI

CPI

0

5

10

15

20

25

30

35

01 02 03 04 05

% YOY

M2

Trade trends

Source: Datastream

-15

-10

-5

0

5

10

15

20

25

30

35

2002 2003 2004 2005

3-month mvg avg, %YOY

imports

exports

• Malaysia’s inflation rate eased in May to 3.9% YOY after staying above 4.5% YOY in March and April. Money supply (M2) has also slowed from over 30% YOY in July 2005 to 14.8% YOY in May 2006. However, we still expect inflation to remain elevated in the second half of the year. The impact of utility rate hikes (domestic electricity and water tariffs lifted in June and July respectively), recovery in chicken and meat prices and still-high petrol prices are expected to filter through to consumer prices.

• Against the backdrop of rising global interest rates, relatively healthy economic growth and inflation concerns, Bank Negara is expected to continue on the path of policy normalisation. We have forecast another 25 bps hike in the overnight policy rate (OPR) when the central bank meets at the end of July. The OPR is currently at 3.5%.

• Export trends have eased in recent months while imports have outpaced export expansion. Imports of capital goods have stayed strong but the outlook for exports is for some slowing as global growth decelerates. We therefore expect real GDP to expand by around 5.4% this year, slower than the government’s forecast of 6%.

• After the steady appreciation track of the ringgit since the new exchange rate regime was adopted in July 2005, the currency has retreated over the past month and is heading towards USD/MYR3.70 from a high of USD/MYR3.57 in early May. While this largely reflects US dollar strength underpinned by expectations of further US interest rate hikes, the recent fluctuations in the MYR signal greater flexibility in exchange rate management on the part of the central bank. We continue to expect the MYR, along with other Asian currencies, to appreciate against the US dollar in the second half of the year, riding on the back of JPY and CNY strength. Expectations of higher domestic interest rates will also support a ringgit appreciation.

Jasmine Robinson

Economic data – Malaysia Monthly data Oct 05 Nov 05 Dec 05 Jan 06 Feb 06 Mar 06 Apr 06 May 06 Industrial Production, %YOY 6.3 8.5 2.2 4.7 7.9 3.6 4.7 n/a Motor Vehicle sales, % YOY 29.1 7.7 4.9 2.9 -8.7 -9.4 -5.4 -0.5 Consumer Price Index, % YOY 3.1 3.3 3.2 3.2 3.2 4.8 4.6 3.9 Exports, % YOY 13.8 12.5 13.8 11.6 17.1 12.6 10.3 n/a Imports, % YOY 9.5 6.6 8.7 10.3 20.1 17.2 15.6 n/a Trade Balance, US$ bn 2.8 2.3 2.5 2.3 2.0 2.6 2.0 n/a Foreign Exchange Reserves, US$ bn 76.9 72.6 70.2 71.3 72.7 73.2 75.9 80.1 Quarterly data Jun 04 Sep 04 Dec 04 Mar 05 Jun 05 Sep 05 Dec 05 Mar 06 Real GDP, % YOY 8.4 6.8 5.9 5.9 4.1 5.4 5.2 5.2 - Private consumption 11.9 11.2 10.2 10.1 7.4 10.4 9.0 7.5 - Government consumption 9.5 1.3 4.4 1.0 0.6 4.7 12.6 0.1 - Gross fixed capital expenditure 3.5 3.2 2.3 2.0 6.7 9.6 0.4 11.4 Nominal GDP, US$ bn 29.4 30.1 30.7 31.2 32.0 33.6 34.0 35.2 Current Account, US$ bn 3.3 4.4 3.4 5.8 4.8 4.9 4.5 5.3 Capital & Financial Account, US$ bn 0.2 -0.9 2.9 0.9 0.1 1.5 -12.4 -1.4 Sources: Datastream, Bloomberg

Economics@ANZ ANZ International Economics Monthly – June 2006

Page 21

Country Update: New Zealand

Gross Domestic Product

-0.2

0

0.2

0.4

0.6

0.8

1

1.2

1.4

Jun-04 Dec-04 Jun-05 Dec-05 Jun-06 Dec-06

QOQ% Change

Rebound

Easing for remainder of 2006

Current Account Deficit

-10

-9

-8

-7

-6

-5

-4

-3

-2

-1

0

93 94 95 96 97 98 99 00 01 02 03 04 05 06

% of GDP

Source: Statistics NZ

• As expected, the New Zealand economy recorded a pick-up in economic activity in the March quarter, following a flat second half of 2005. Gross Domestic Product increased 0.7% over the quarter, taking annual growth to 2.2%, from 2.3% in December.

• But just as we believed growth was understated in the second half of 2005, there were influences that inflated the March outturn. A rebound in inventories, which alone contributed 1.2 percentage points to growth, overstated the level of economic activity in the March quarter, just as a massive stock run-down overstated the weakness in the December quarter.

• With close to 70% of the economy being domestic and spending dominated, slow consumer spending leaves a massive void to fill. A weaker currency is laying the platform for a strong up-tick in export performance although the lag between the two is typically 18 months. In the interim, there is a glaring absence of an engine to drive the economy, leaving growth decidedly sluggish into 2007. This foreshadows a two-sided economy during this period as a rebalancing takes place from the domestic to the export orientated sectors.

• New Zealand recorded a current account deficit of 9.3% of GDP during the year ended March 2006, the worst since 1975. However, the composition does not look as bad as the headline implies with the deterioration largely driven by a high investment income deficit, which is heavily linked to a strong domestic profitability cycle.

• The Reserve Bank left the Official Cash Rate unchanged at 7.25% at the review on the 8th of June. While acknowledging a backdrop of slowing economic activity, the Bank continues to talk tough in an attempt to maintain policy traction along the yield curve and keep a lid on inflation expectations.

Cameron Bagrie

Economic data – New Zealand Monthly data Oct 05 Nov 05 Dec 05 Jan 06 Feb 06 Mar 06 Apr 06 May 06 Retail Sales, % YOY 7.0 6.7 6.4 6.4 6.3 6.1 5.7 n/a Residential building consents (% -17.5 -17.8 -17.2 -15.1 -13.6 -16.0 -13.6 -10.7 Exports, % YOY 1.6 0.8 0.3 -0.5 -1.2 0.0 0.4 4.1 Imports, % YOY 8.0 7.9 6.8 8.5 8.1 7.7 7.6 8.7 Annual Trade Balance, US$ bn -4.3 -4.6 -4.5 -4.9 -4.9 -4.5 -4.3 -4.4 Quarterly data Jun 04 Sep 04 Dec 04 Mar 05 Jun 05 Sep 05 Dec 05 Mar 06 Real GDP, % YOY 4.1 4.3 4.3 3.7 3.1 2.7 2.3 2.2 - Private consumption 6.5 6.7 6.5 5.8 5.7 5.1 4.7 4.1 - Government consumption 4.8 5.3 5.6 5.2 5.0 5.9 5.7 5.6 - Gross fixed capital expenditure 15.6 15.4 13.2 7.8 4.9 4.0 4.3 5.6 Nominal GDP, US$ bn 89.5 93.6 97.8 100.5 105.0 107.8 108.6 107.6 Annual Current Account, US$ bn -4.4 -5.6 -6.5 -7.4 -8.4 -9.1 -9.6 -10.1 Consumer Price Index, annual % 2.4 2.5 2.7 2.8 2.8 3.4 3.2 3.3 Sources: Statistics NZ, ANZ National Bank

Economics@ANZ ANZ International Economics Monthly – June 2006

Page 22

Country Update: Philippines Inflation moderates keeping interest rates

unchanged

Inflation

6

7

8

9

10

03 04 05 06

% pa.Policy rates

Sources: Bloomberg, Datastream

0

1

2

3

4

5

6

7

8

9

10

03 04 05 06

%YOY