economy - valuewalk.com · an illustrated executive summary the election of modi (m), the...

TRANSCRIPT

ECONOMY

Research Analysts:

October 2016

M+R+T resets = A revolution in 'access'

Ritika Mankar Mukherjee, [email protected]

Tel: +91 22 3043 3175

MARKET

SME

India's transformation in 'access’

Foreign Investor

Ports & Roads

Domestic Investor

Sumit [email protected]

Tel: +91 22 3043 3229

Nitin [email protected]

Tel: +91 22 3043 3241

Economy

October 04, 2016 Ambit Capital Pvt. Ltd. Page 2

CONTENTS

Section 1: The three ‘access’ related transformations ……………………9 underway in India

Section 1.1: Transformation#1: Access to end-markets ………………………..9

Section 1.2: Transformation#2: Access to capital ……………………………..17

Section 1.3: Transformation#3: Access to physical infrastructure ……………29

Section 2: Macroeconomic Implications …………………………………….34

Impact#1: Improved market access and access to …………………………….34 inputs of production is likely to yield gradual improvements in GDP growth in India

Impact#2: Cost of debt capital is set to fall over the next 5 years …………..36

Articulating our GDP forecast for FY18 ………………………………………….41

Section 3: Investment Implications …………………………………………..44

Investment theme 1: Plays on enhanced consumption ……………………….44

Investment theme 2: Plays on a more competitive financial system …………45

Investment theme 3: Plays on an improved transport network ………………46

Ambit Capital and / or its affiliates do and seek to do business including investment banking with companies covered in its research reports. As a result, investors should be aware that Ambit Capital may have a conflict of interest that could affect the objectivity of this report. Investors should not consider this report as the only factor in making their investment decision.

THEMATIC October 04, 2016

Economy

Exhibit A: GDP growth recovery to be U-shaped

Source: CEIC, Ambit Capital research

Exhibit B: Stocks in focus

Stock Ticker MCap (USD mn) Upside

Plays on enhanced consumption

Asian Paints APNT IN 17,198 3%

Havells HAVL IN 4,049 -4%

TTK Prestige TTKPT IN 938 6%

Trent TRENT IN 1,114 0%

Plays on a more competitive financial system

Axis Bank AXSB IN 19,761 9%

Cholamandalam CIFC IN 2,772 10%

City Union Bank CUBK IN 1,216 7%

Plays on an improved transport network

Ashok Leyland AL IN 3,554 23%

Sadbhav Infrastructure SINP IN 569 20%

Ashoka Buildcon ASBL IN 492 29%

Source: Bloomberg, Ambit Capital research

Research Analysts

Ritika Mankar Mukherjee, CFA +91 22 3043 3175 [email protected]

Sumit Shekhar +91 22 3043 3329 [email protected]

Nitin Bhasin +91 22 3043 3241 [email protected]

5.6%

6.6%

7.2%

6.8% 6.8%

7.3%

5%

6%

7%

8%

FY13

FY14

FY15

FY16

FY17

E

FY18

E

Rea

l GD

P g

row

th(Y

oY

cha

ng

e, in

%)

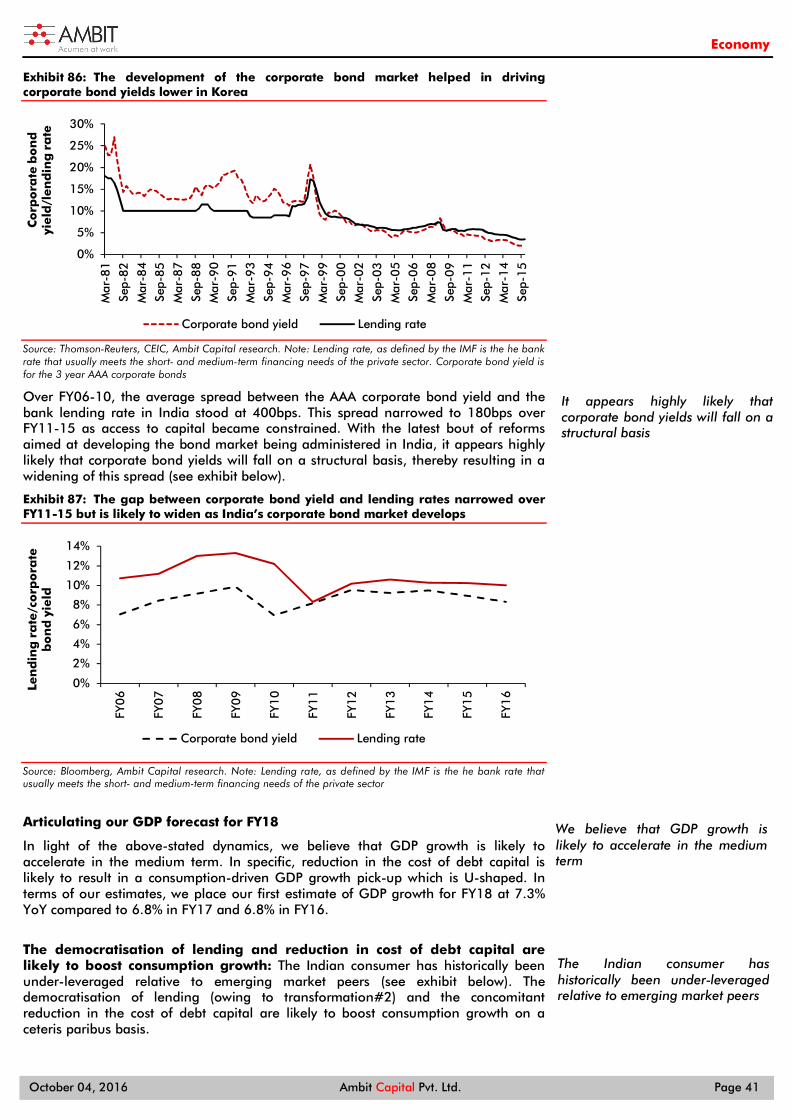

M+R+T resets = A revolution in ‘access’ The election of Modi (M), the appointment of Rajan (R) and the advent of Technology (T) set off a collapse in earnings growth in India from FY14 (refer to our note titled ‘M+R+T = Earnings recession in India’ for details). Whilst the M+R+T resets have been disruptive in the short run, in this note we describe how the policy decisions triggered by M+R+T have propelled a silent revolution in ‘access’ to end-markets, capital and physical infrastructure. We expect the resultant reduction in cost of debt capital and slow but sure productivity boost to trigger a consumption-driven U-shaped economic recovery in India in FY18 (Ambit GDP est. for FY18 is 7.3% vs 6.8% in FY16). Hence, we urge investors to BUY plays on enhanced consumption, plays on a more competitive financial system and plays on the improved transport network in India.

M+R+T = Earnings recession in India in the short term In our note dated December 16, 2015 we highlighted that earnings growth for India Inc is set to stay under pressure owing to three sets of structural changes, namely “…(1) PM Modi (M) who is calling time on the traditional model of crony capitalism driven capex growth; (2) Governor Rajan (R) who is increasing competition for traditional banks, deepening of corporate bond markets and reducing regulatory arbitrage between banks and NBFCs; and (3) Technology which is weakening the traditional offering of Indian IT services firms whilst increasing competition for retail lenders and B2C companies”.

M+R+T = A silent revolution in ‘access’ in the long term Whilst the M+R+T resets have been disruptive in the short run, in this note we describe how the range of policy decisions triggered by Modi, Rajan and Technology has set off a silent revolution in ‘access’. In specific, we highlight: Transformation#1: Access to ‘end-markets’: The advent of e-commerce

and the potential implementation of a single Goods and Services Tax (GST) hold the potential of transforming access to end-markets for producers of goods as well as services in India.

Transformation#2: Access to ‘capital’: Three sets of changes are set to improve cost and accessibility of finance, namely: (1) increased competition ‘amongst banks’ and ‘to banks’ (from NBFCs, corporate bonds and other financial technology driven offerings), (2) improved access to capital for SMEs (through schemes like MUDRA and credit extended by e-commerce majors), and (3) improvement in access to consumer finance (through schemes like PMJDY and lenders competing to provide retail credit).

Transformation#3: Access to ‘physical infrastructure’: The Modi-led NDA administration’s focus on improving physical connectivity (via roads, railways, air and waterways) holds the potential of dramatically improving mobility of labour as well as raw materials.

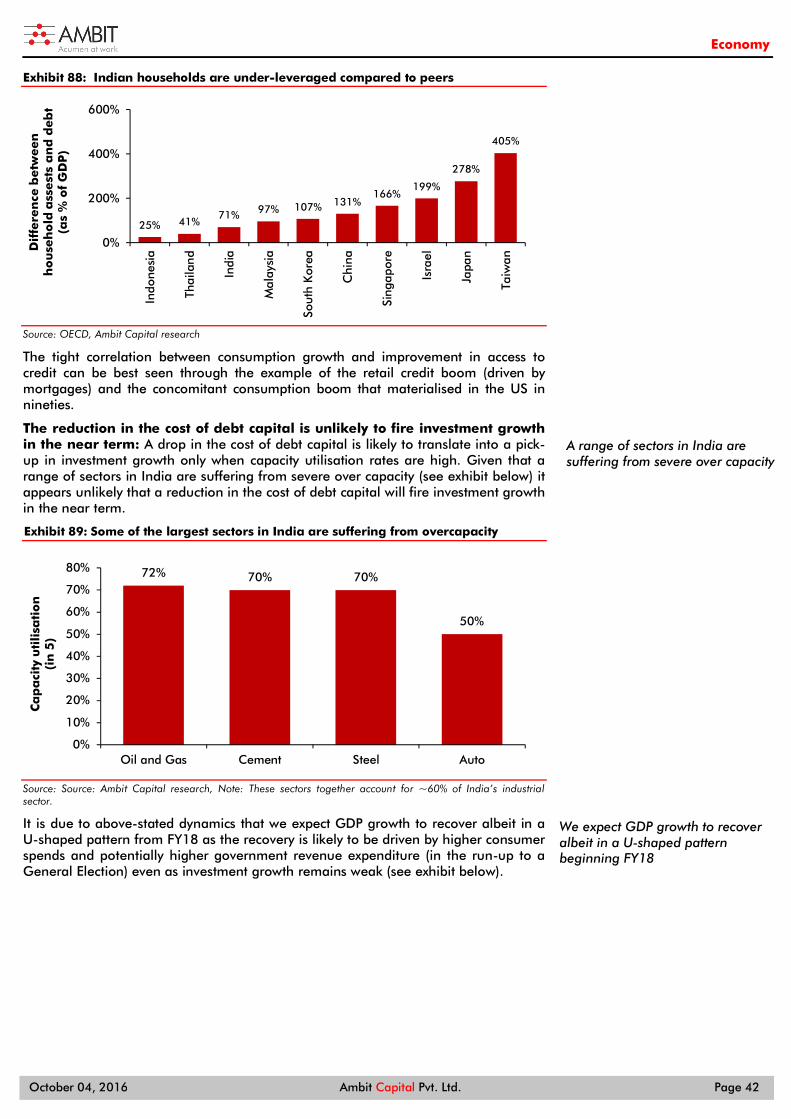

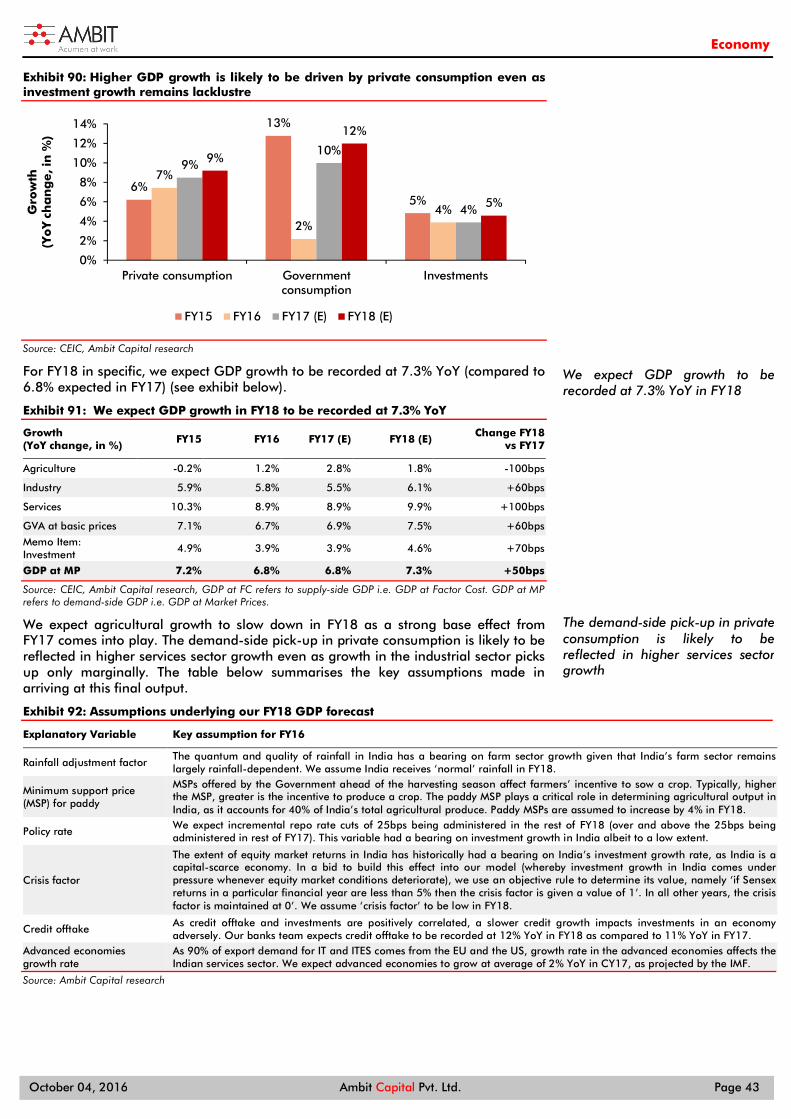

Macroeconomic and investment implications The combination of superior physical infrastructure and rollout of GST will boost access to end-markets as well as inputs. Cross-country experience suggests that such reforms boost productivity in a gradual manner. Furthermore, Modi’s black money crackdown is likely to result in a reduction in the cost of debt capital in India. We expect the cost of debt capital in India (proxied by the SBI lending rate) to fall by ~360bps by FY20. Based on these two macro impacts, we expect GDP to undergo a U-shaped improvement and expect GDP growth in FY18 to be recorded at 7.3% YoY (see exhibit in the right hand margin). Hence, we urge investors to BUY plays on enhanced consumption (Asian Paints, Havells, TTK prestige, Trent), plays on a more competitive financial system (Axis bank, Cholamandalam and City Union bank) and plays on the improved transport network in India (Ashok Leyland, Sadbhav Infrastructure and Ashoka Buildcon).

Economy

October 04, 2016 Ambit Capital Pvt. Ltd. Page 4

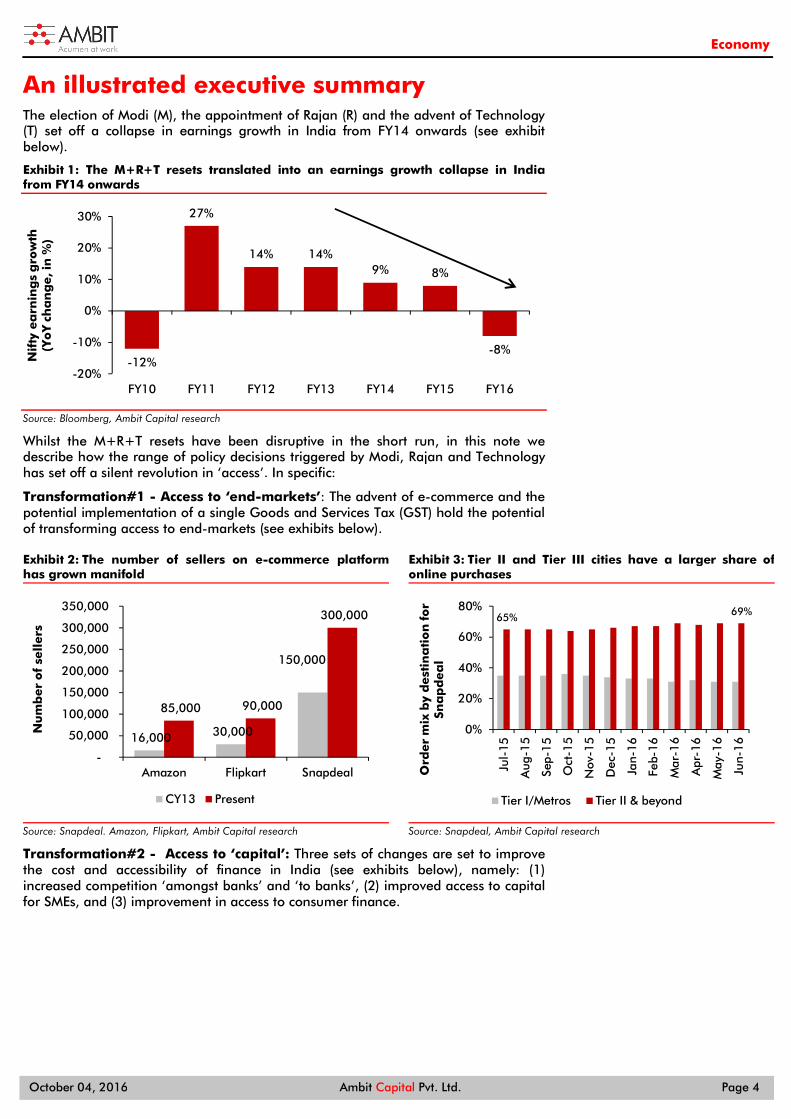

An illustrated executive summary The election of Modi (M), the appointment of Rajan (R) and the advent of Technology (T) set off a collapse in earnings growth in India from FY14 onwards (see exhibit below).

Exhibit 1: The M+R+T resets translated into an earnings growth collapse in India from FY14 onwards

Source: Bloomberg, Ambit Capital research

Whilst the M+R+T resets have been disruptive in the short run, in this note we describe how the range of policy decisions triggered by Modi, Rajan and Technology has set off a silent revolution in ‘access’. In specific:

Transformation#1 - Access to ‘end-markets’: The advent of e-commerce and the potential implementation of a single Goods and Services Tax (GST) hold the potential of transforming access to end-markets (see exhibits below).

Exhibit 2: The number of sellers on e-commerce platform has grown manifold

Source: Snapdeal. Amazon, Flipkart, Ambit Capital research

Exhibit 3: Tier II and Tier III cities have a larger share of online purchases

Source: Snapdeal, Ambit Capital research

Transformation#2 - Access to ‘capital’: Three sets of changes are set to improve the cost and accessibility of finance in India (see exhibits below), namely: (1) increased competition ‘amongst banks’ and ‘to banks’, (2) improved access to capital for SMEs, and (3) improvement in access to consumer finance.

-12%

27%

14% 14%9% 8%

-8%

-20%

-10%

0%

10%

20%

30%

FY10 FY11 FY12 FY13 FY14 FY15 FY16

Nif

ty e

arn

ing

s g

row

th(Y

oY c

ha

ng

e, i

n %

)

16,000 30,000

150,000

85,000 90,000

300,000

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

Amazon Flipkart Snapdeal

Nu

mb

er

of

sell

ers

CY13 Present

65% 69%

0%

20%

40%

60%

80%

Jul-

15

Aug

-15

Sep-

15

Oct

-15

Nov

-15

Dec

-15

Jan-

16

Feb-

16

Mar

-16

Apr

-16

May

-16

Jun-

16

Ord

er

mix

by

dest

ina

tio

n fo

r Sn

ap

dea

l

Tier I/Metros Tier II & beyond

Economy

October 04, 2016 Ambit Capital Pvt. Ltd. Page 5

Exhibit 4: The RBI has taken a range of measures to increase competition ‘amongst banks’ and ‘to banks’

Steps to increase competition ‘amongst banks’

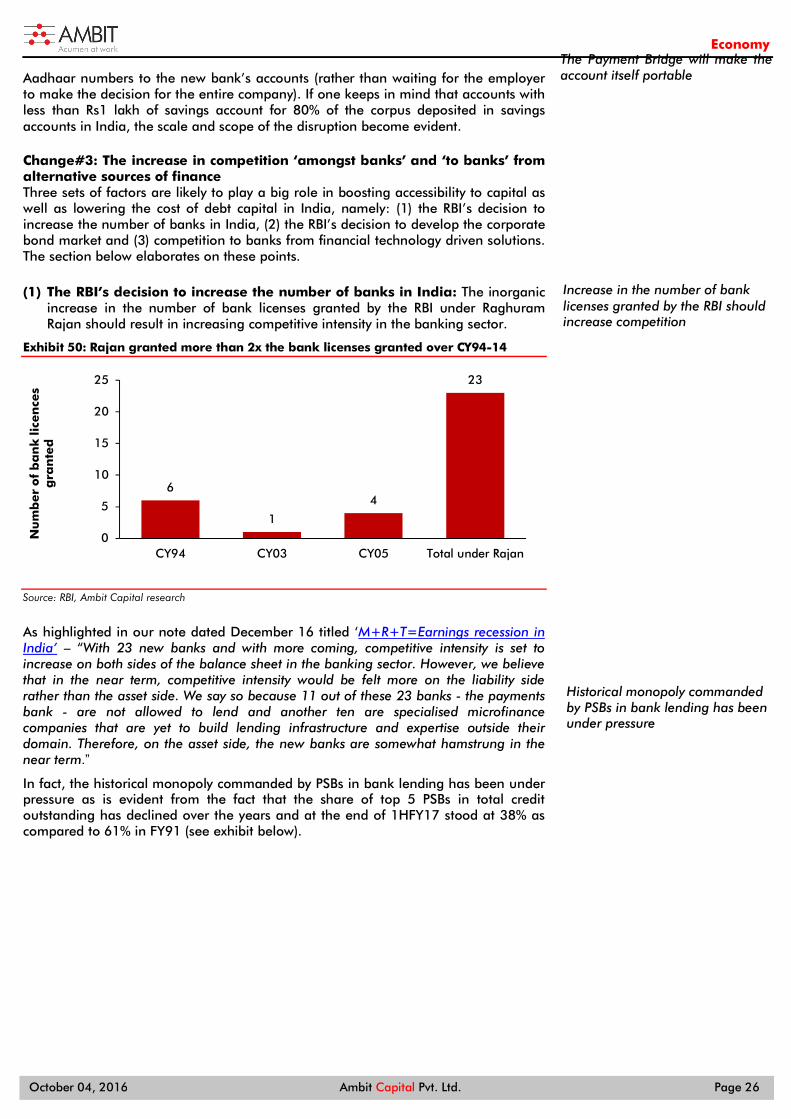

The inorganic increase in the number of bank licenses granted by the RBI under Raghuram Rajan should result in increasing competitive intensity in the banking sector The advent of financial technology is set to disrupt the financial industry as a whole. Specifically, it will induce more competition in the banking system. Fintech can potentially make low-value, high-volume transactions cheaper and, hence, will pose a threat to the banking system.

Steps to increase competition ‘to banks’

Raghuram Rajan approved a slew of measures in August 2016 to promote the growth of corporate bond markets. From FY19, accessing bank credit beyond certain thresholds will become costlier for large corporates. The RBI has also addressed various market impediments to promote participation and improve liquidity in secondary bond market. Source: mudra.org.in, Ambit Capital research

Transformation#3 - Access to ‘physical infrastructure’: The Modi-led NDA administration’s focus on improving physical connectivity holds the potential of dramatically improving mobility of labour as well as raw material (see exhibits below).

Exhibit 5: The NDA Government has boosted spending on infrastructure…

Source: Union budget documents, Ambit Capital research

Exhibit 6: … with a special focus on road building

Source: Ministry of Roads, Transport and Highways, Ambit Capital research

Exhibit 7: The Government has ambitious targets for infrastructure development

Head Target

Roads

Government think tank NITI Aayog has set ambitious targets of doubling the network of national highways and hiking the railway track length by almost eight times between now and CY20 as it aims to create world-class infrastructure to boost the economy. The total network of highways — including single and intermediate lanes and 4 & 6 lanes — is set to more than double to 96,000 km in 2020 from 45,406 km in FY16-end.

Railways The target for total track length, including commissioning of new lines, has been set at 130 lakh km for FY20 from 17.8 lakh km in FY17 and 16.5 lakh km achieved in FY16. At the same time, the government aims to reduce the empty freight wagon return ratio from an abysmal 39% during the current and last fiscal to 30% by CY20.

Airways The targets for passenger and cargo capacity have been set at 440 million passengers per year and 6 million tonnes a year, respectively. For the current fiscal, the passenger capacity target is set at 270 million, higher than the 250 million passenger capacity during last fiscal, while the cargo capacity has been maintained flat at four million tonnes for FY17.

Ports The target for FY20 has been fixed at 2,331 million tonnes per annum (mtpa) as against the current capacity of 1602 mtpa.

Source: NITI Aayog, Ambit Capital research

Macroeconomic implications

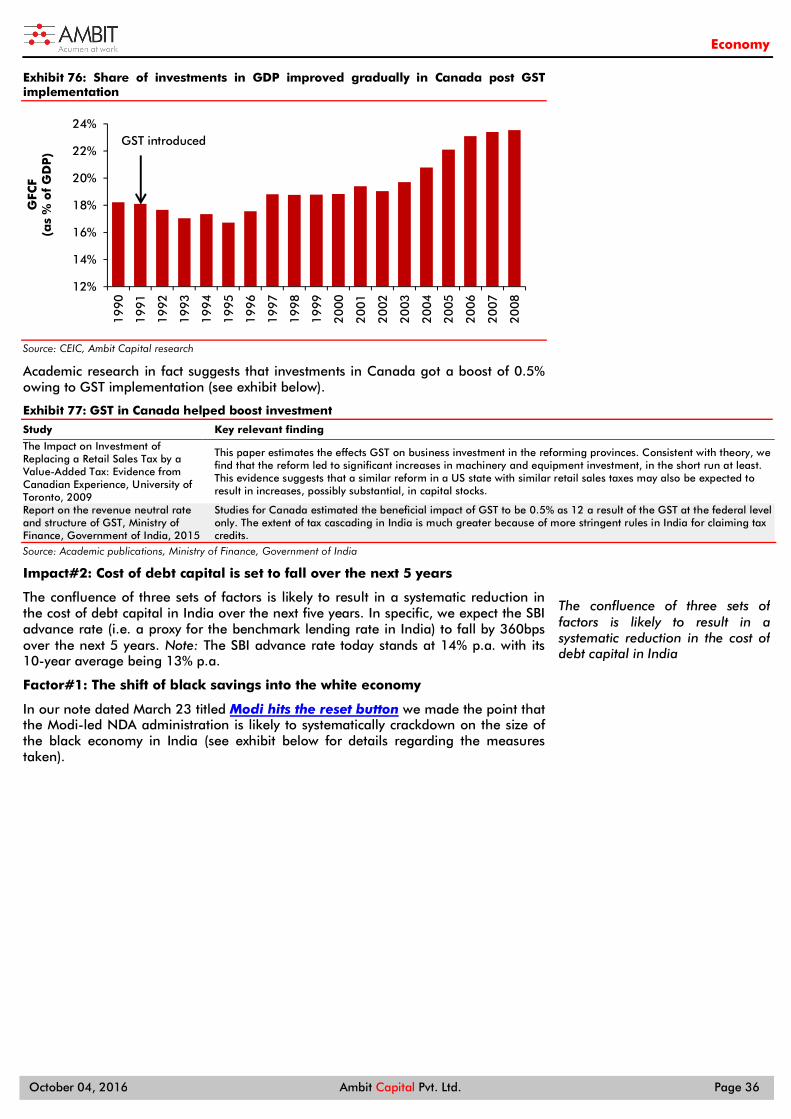

The combination of superior physical infrastructure and the rollout of GST will boost access to end-markets as well as inputs. Cross-country experience suggests that such reforms boost productivity in a gradual manner. Furthermore, Modi’s black money crackdown is likely to result in a reduction in the cost of debt capital in India. We expect the cost of debt capital in India (proxy is the SBI lending rate) to fall by ~360bps by FY20.

2.0%

3.1% 3.0%

3.6%

0%

1%

2%

3%

4%

FY14 FY15 FY16 FY17 (BE)

Go

vt. sp

en

din

g o

n

infr

ast

ruct

ure

(as

% o

f G

DP

)

7

24

810

25

0

5

10

15

20

25

30

FY12 FY13 FY14 FY15 FY16RE

FY17BE

Ro

ad

aw

ard

s(i

n '0

00

s o

f K

Ms)

Economy

October 04, 2016 Ambit Capital Pvt. Ltd. Page 6

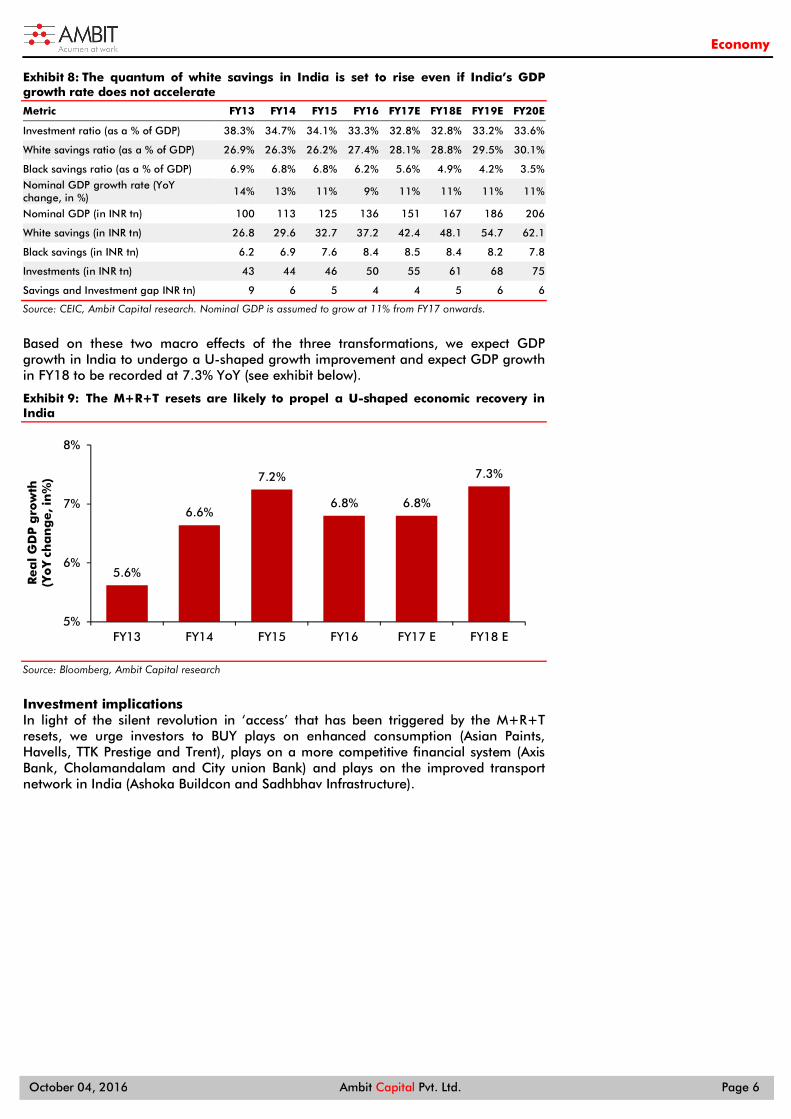

Exhibit 8: The quantum of white savings in India is set to rise even if India’s GDP growth rate does not accelerate

Metric FY13 FY14 FY15 FY16 FY17E FY18E FY19E FY20E

Investment ratio (as a % of GDP) 38.3% 34.7% 34.1% 33.3% 32.8% 32.8% 33.2% 33.6%

White savings ratio (as a % of GDP) 26.9% 26.3% 26.2% 27.4% 28.1% 28.8% 29.5% 30.1%

Black savings ratio (as a % of GDP) 6.9% 6.8% 6.8% 6.2% 5.6% 4.9% 4.2% 3.5%

Nominal GDP growth rate (YoY change, in %)

14% 13% 11% 9% 11% 11% 11% 11%

Nominal GDP (in INR tn) 100 113 125 136 151 167 186 206

White savings (in INR tn) 26.8 29.6 32.7 37.2 42.4 48.1 54.7 62.1

Black savings (in INR tn) 6.2 6.9 7.6 8.4 8.5 8.4 8.2 7.8

Investments (in INR tn) 43 44 46 50 55 61 68 75

Savings and Investment gap INR tn) 9 6 5 4 4 5 6 6

Source: CEIC, Ambit Capital research. Nominal GDP is assumed to grow at 11% from FY17 onwards.

Based on these two macro effects of the three transformations, we expect GDP growth in India to undergo a U-shaped growth improvement and expect GDP growth in FY18 to be recorded at 7.3% YoY (see exhibit below).

Exhibit 9: The M+R+T resets are likely to propel a U-shaped economic recovery in India

Source: Bloomberg, Ambit Capital research

Investment implications In light of the silent revolution in ‘access’ that has been triggered by the M+R+T resets, we urge investors to BUY plays on enhanced consumption (Asian Paints, Havells, TTK Prestige and Trent), plays on a more competitive financial system (Axis Bank, Cholamandalam and City union Bank) and plays on the improved transport network in India (Ashoka Buildcon and Sadhbhav Infrastructure).

5.6%

6.6%

7.2%

6.8% 6.8%

7.3%

5%

6%

7%

8%

FY13 FY14 FY15 FY16 FY17 E FY18 E

Rea

l G

DP

gro

wth

(Yo

Y c

ha

ng

e, i

n%

)

Economy

October 04, 2016 Ambit Capital Pvt. Ltd. Page 7

Prologue: M+R+T = Earnings recession in India in the short term “After a decade of ossification, the landscape is changing at a rapid rate for India Inc as: (1) An unconventional PM calls time on the traditional model of subsidy funded consumption growth and crony capitalism driven capex growth in India; (2) A gutsy RBI Governor brings about multiple policy changes to radically increase competition in the Financial Services sector; and (3) Technology lowers the barriers to entry into B2C sectors such as lending, consumer goods and auto.”

‘M+R+T=Earnings recession in India’, December 16, 2015

In our note dated December 16, 2016 we said that the resets engineered by PM Modi, the changes instituted by Governor Rajan, and the technology-induced resets will entail short-term pain in India. In specific, we pointed to three set of resets: some engineered by the PM, some by the then RBI Governor, and some due to the spread of new technology.

Reset #1: Modi hits the ‘reset’ button

In our note dated 23 March 2015, “Modi hits the ‘reset’ button”, we highlighted that Modi (who is essentially a man driven by personal goals and searing political ambition) has sensed the need to deliver three structural changes to perpetuate his political success.

“Our discussions with the policy ecosystem in Delhi as well as our understanding of the key policy measures announced by the NDA Government suggest that the Prime Minister is seeking to engineer three structural resets: (1) shift India’s savings landscape away from gold and land and towards the formal financial system, (2) disrupt the Indian model of crony capitalism, and (3) redefine India’s subsidy mechanism”.

In other words, Prime Minister Modi has been calling time on the traditional model of black money funded consumption growth and crony capitalism driven capex growth.

Reset #2: Rajan’s resets

Dr. Raghuram Rajan, who served as the Governor of the RBI from September 2013 to September 2016, played a pivotal role in transforming the Indian financial landscape. He increased competition for traditional private banks through the introduction of a record number of new banks, deepened the corporate bond market, worked to resurrect PSU banks, and reduced the regulatory arbitrage between banks and NBFCs.

Reset #3: The ‘technology’ induced resets

The rise of e-commerce over the past few years was termed as ‘disruptive’ in nature by media and practitioners alike.

The growing penetration of smartphone and internet combined with an increasing propensity of Indian consumers to transact online has led to firms like Flipkart and Snapdeal being considered a serious threat to existing brick and mortar players. While the success of these dot com firms cannot be labelled as ‘disruptive’ in nature, the radical improvements achieved by them using technology over the traditional model cannot be overlooked.

‘Modi’, ‘Rajan’ and ‘Technology’ resets to entail short-term pain

In conclusion, we thus made the point that the interplay of the above stated resets is likely to result in powerful pressure on corporate earnings in the short run (see exhibit below).

Three resets driven by Modi, Rajan and Technology led to an earnings recession

Prime Minister Modi has been calling time on the traditional model of black money funded consumption growth

Rajan increased competition for traditional private banks through the introduction of a record number of new banks

The rise of e-commerce over the past few years was termed as ‘disruptive’ in nature

Economy

October 04, 2016 Ambit Capital Pvt. Ltd. Page 8

Exhibit 10: Earnings growth for the Nifty has tapered over the last four years

Source: Bloomberg, Ambit Capital research

This is because incumbents who had enjoyed high earnings growth on the back of corruption and artificial suppression of competition under the UPA Government are now facing increasing pressure on their revenues and earnings.

‘Modi’, ‘Rajan’ and ‘Technology’ resets to revolutionise ‘access’ in the long term

Whilst the M+R+T resets have been disruptive in the short run, in this note we describe how the range of policy decisions triggered by Modi, Rajan and Technology are transforming access to ‘end-markets’, access to ‘capital’ as well as access to ‘physical infrastructure’ from a long-term perspective. The subsequent note is divided into three sections, namely:

Section 1 elaborates on three dimensions along which ‘access’ is being transformed in India.

Section 2 endeavors to eke out the macroeconomic implications of these unique changes while drawing from cross-country experience in this regard.

Section 3 focusses on highlighting the investment implications of these changes.

-12%

27%

14% 14%

9% 8%

-8%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

FY10 FY11 FY12 FY13 FY14 FY15 FY16

Nif

ty e

arn

ing

s g

row

th

Incumbents are facing increasing pressure on their revenues and earnings.

Economy

October 04, 2016 Ambit Capital Pvt. Ltd. Page 9

Section 1: The three ‘access’ related transformations underway in India India has historically been a supply-constrained economy mainly owing to the existence of barriers that prevent easy access to the three basic inputs of production, namely capital, labour and technology. As highlighted in the preceding section, the MRT resets have been disruptive in the short run as incumbents are forced to deal with an inorganic rise in competition and/or a breakdown in the old ways of doing business (which was centered on leveraging political connectivity). In this note, we highlight that despite the short-term pain triggered by the MRT resets, these resets have inadvertently triggered a silent revolution that is likely to transform access to ‘capital’, ’end-markets' and ‘physical infrastructure’.

Even as no solution appears to be on the horizon with respect to India’s problem of providing jobs to its large and youthful demographic structure (which is largely uneducated and unemployed: refer to our note titled ‘Sizing India’s demographic bomb’ for details), these three ‘access’ related transformations are likely to enhance the pace of output growth in India.

In the subsequent section, we elaborate on each of the three transformations that are currently underway in India, namely: Transformation #1: Access to end-markets,

Transformation #2: Access to capital, and

Transformation #3: Access to physical and virtual infrastructure.

Section 1.1: Transformation#1: Access to end-markets

“Our main finding is that market access is indeed an important determinant of Sub-Saharan Africa’s (SSA’s) economic development. This effect is still lower than that found for other parts of the world, but our results do show that the importance of market access has increased markedly in SSA over the last two decades….These findings are robust after controlling for many other variables affecting economic development (most notably human capital, institutions, natural resource dependence, and other more standard measures of a country’s geography). In our most conservative specification, we find that a 1% increase in a SSA country’s market access is associated with a 0.03% increase in its GDP per worker. “

- Garretsen, ‘Market Access: A Key Determinant of Economic Development in Sub-Saharan Africa’ (2012)

The advent of e-commerce in India and the potential implementation of a single Goods and Services Tax (GST) hold the potential of transforming access to end-markets for producers of goods as well as services in India.

One of the main reasons responsible for the small scale of operations of Indian firms has been the high cost of access and creation of pan-India distribution networks. The advent of e-commerce has helped producers find an inorganic solution to this problem as sellers have the option of simply tying up with one or more e-commerce majors and, thereby, creating access to the whole of India overnight. Concomitantly, manufacturers and retailers across India are increasingly moving towards selling products online as the number of Indians with access to the internet rises systematically.

Section 1.1.1: Improved access for small companies to end-markets through e-commerce According to the Economic Survey for 2016, “With 3.6 crore [36mn] units spread across the country, that employ 8.05 crore [80.5mn] people, Micro, Small and Medium Enterprises (MSME) have a contribution of 37.5% to the country’s GDP. The sector has huge potential for helping address structural problems like unemployment, regional imbalances, unequal distribution of national income and wealth across the country.” MSMEs account for 37% of India’s total manufacturing output and generate employment for nearly a tenth of India’s total population (see exhibit below).

India has historically been a supply-constrained economy owing to the existence of barriers that prevent easy access to the three basic inputs of production

The advent of e-commerce and GST hold the potential of transforming access to end-markets

Manufacturers and retailers across India are increasingly moving towards selling products online

MSMEs account for 37% of India’s total manufacturing

Economy

October 04, 2016 Ambit Capital Pvt. Ltd. Page 10

Exhibit 11: MSMEs contribute 37% of India’s manufacturing sector GDP…

Source: Ministry of MSME, Ambit Capital research

Exhibit 12: …and employ about one-tenth of the total population

Source: Ministry of MSME, Ambit Capital research

However, as is evident from the chart above, MSMEs’ share in manufacturing has been declining (even as the total share of manufacturing in India’s GDP remains stagnant) mainly because MSMEs in India must contend with the challenge of poor access to end-markets. The ministry of MSME, in its annual report for FY15, has noted that “MSMEs in India face constraints such as high cost of credit, low access to new technology and lack of access to national and international markets”.

MSMEs in India are defined as firms with investment in plant and machinery under US$2.5mn. MSMEs in India typically remain small as market access is limited to a particular locality or a small region owing to a range of constraints, including weak physical infrastructure and the high cost of creating a widespread distribution network.

This, in turn, prevents MSMEs from organically growing into larger firms that can exploit economies of scale. For instance, India’s manufacturing sector is characterised by significantly smaller firms as compared to China (see exhibit below).

Exhibit 13: About 88% of Indian factories have less than 100 workers each

Source: EPW, Ambit Capital research. Note data pertains to CY13

42% 42%41%

40%39%

37% 37%

33%

36%

39%

42%

45%FY

07

FY0

8

FY0

9

FY1

0

FY1

1

FY1

2

FY1

3

MSM

E m

an

ufa

ctu

rin

g(a

s %

of

tota

l m

an

ufa

ctu

rin

g

81 84 88 92 97 101 106 111 117

0

20

40

60

80

100

120

140

FY0

7

FY0

8

FY0

9

FY1

0

FY1

1

FY1

2

FY1

3

FY1

4

FY1

5

MSM

E em

plo

ymen

t(i

n m

illi

on

s)

25 26 2317

5 2 1 0

77

11 6 4 2 1 0 00

20

40

60

80

100

0-4

9

50-

99

100

-199

200

-499

500

-999

100

0-1

99

9

200

0-4

99

9

500

0-Sh

are

of

fact

ori

es

wit

h s

peci

fied

nu

mb

er

of

wo

rkers

(in

%)

Number of workers hired

China India

MSMEs in India must contend with the challenge of poor access to end-markets

India’s manufacturing sector is characterised by significantly smaller firms as compared to China

Economy

October 04, 2016 Ambit Capital Pvt. Ltd. Page 11

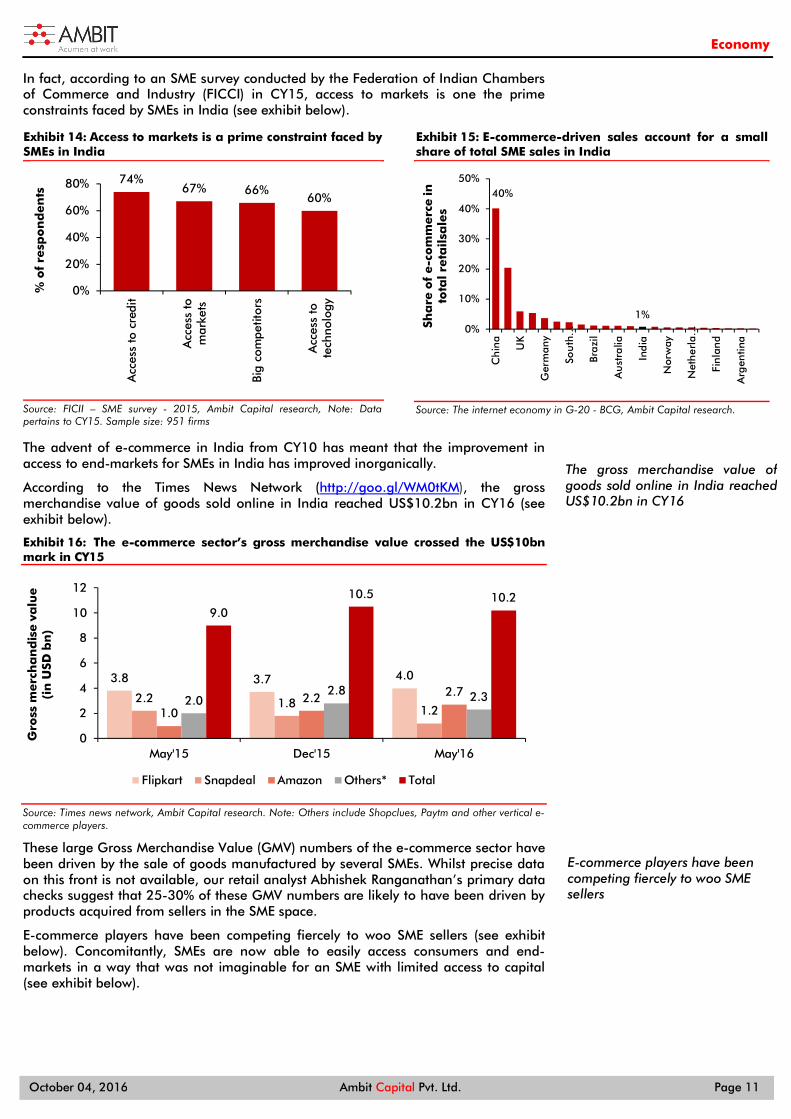

In fact, according to an SME survey conducted by the Federation of Indian Chambers of Commerce and Industry (FICCI) in CY15, access to markets is one the prime constraints faced by SMEs in India (see exhibit below).

Exhibit 14: Access to markets is a prime constraint faced by SMEs in India

Source: FICII – SME survey - 2015, Ambit Capital research, Note: Data pertains to CY15. Sample size: 951 firms

Exhibit 15: E-commerce-driven sales account for a small share of total SME sales in India

Source: The internet economy in G-20 - BCG, Ambit Capital research.

The advent of e-commerce in India from CY10 has meant that the improvement in access to end-markets for SMEs in India has improved inorganically.

According to the Times News Network (http://goo.gl/WM0tKM), the gross merchandise value of goods sold online in India reached US$10.2bn in CY16 (see exhibit below).

Exhibit 16: The e-commerce sector’s gross merchandise value crossed the US$10bn mark in CY15

Source: Times news network, Ambit Capital research. Note: Others include Shopclues, Paytm and other vertical e-commerce players.

These large Gross Merchandise Value (GMV) numbers of the e-commerce sector have been driven by the sale of goods manufactured by several SMEs. Whilst precise data on this front is not available, our retail analyst Abhishek Ranganathan’s primary data checks suggest that 25-30% of these GMV numbers are likely to have been driven by products acquired from sellers in the SME space.

E-commerce players have been competing fiercely to woo SME sellers (see exhibit below). Concomitantly, SMEs are now able to easily access consumers and end-markets in a way that was not imaginable for an SME with limited access to capital (see exhibit below).

74%67% 66%

60%

0%

20%

40%

60%

80%

Acc

ess

to c

redi

t

Acc

ess

tom

arke

ts

Big

com

petit

ors

Acc

ess

tote

chno

logy

% o

f re

spo

nd

en

ts 40%

1%0%

10%

20%

30%

40%

50%

Ch

ina

UK

Ger

man

y

Sou

th…

Bra

zil

Au

stra

lia

Ind

ia

Nor

way

Net

her

la…

Fin

lan

d

Arg

entin

a

Sha

re o

f e-c

om

merc

e in

to

tal re

tail

sale

s

3.8 3.7 4.0

2.2 1.81.21.0

2.2 2.72.0

2.8 2.3

9.0

10.5 10.2

0

2

4

6

8

10

12

May'15 Dec'15 May'16

Gro

ss m

erc

ha

nd

ise v

alu

e(i

n U

SD b

n)

Flipkart Snapdeal Amazon Others* Total

The gross merchandise value of goods sold online in India reached US$10.2bn in CY16

E-commerce players have been competing fiercely to woo SME sellers

Economy

October 04, 2016 Ambit Capital Pvt. Ltd. Page 12

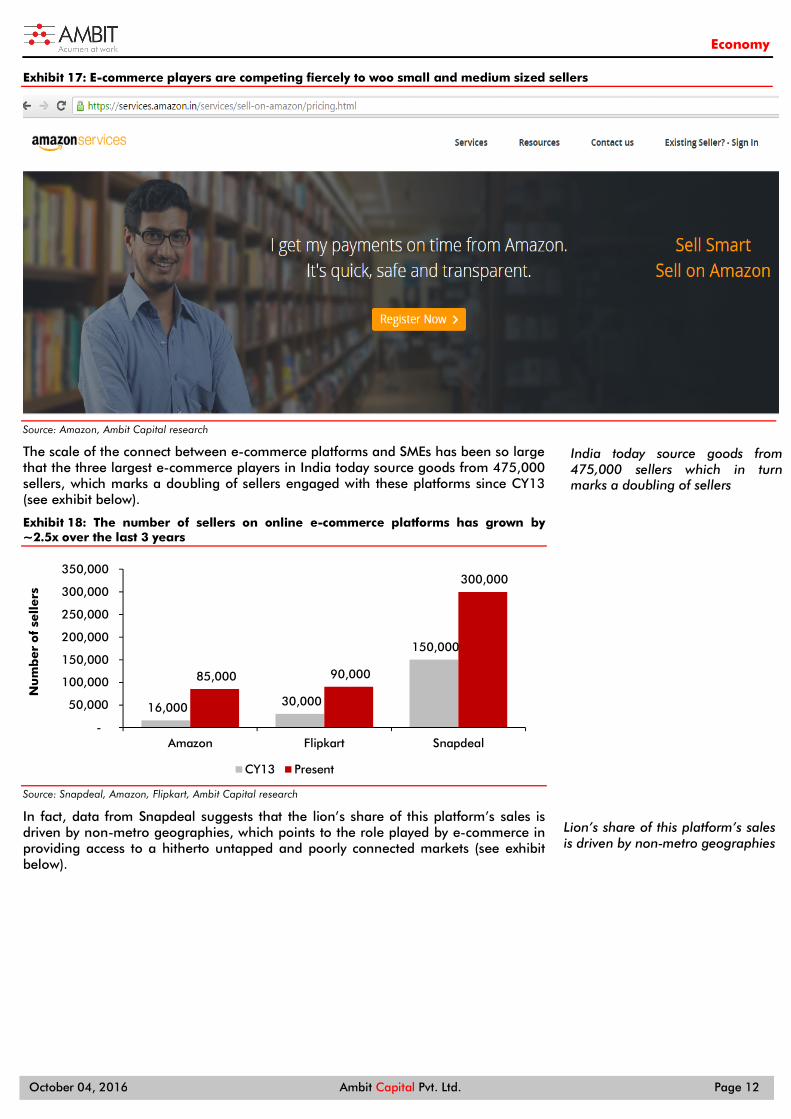

Exhibit 17: E-commerce players are competing fiercely to woo small and medium sized sellers

Source: Amazon, Ambit Capital research

The scale of the connect between e-commerce platforms and SMEs has been so large that the three largest e-commerce players in India today source goods from 475,000 sellers, which marks a doubling of sellers engaged with these platforms since CY13 (see exhibit below).

Exhibit 18: The number of sellers on online e-commerce platforms has grown by ~2.5x over the last 3 years

Source: Snapdeal, Amazon, Flipkart, Ambit Capital research

In fact, data from Snapdeal suggests that the lion’s share of this platform’s sales is driven by non-metro geographies, which points to the role played by e-commerce in providing access to a hitherto untapped and poorly connected markets (see exhibit below).

16,000 30,000

150,000

85,000 90,000

300,000

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

Amazon Flipkart Snapdeal

Nu

mb

er

of

sell

ers

CY13 Present

India today source goods from 475,000 sellers which in turn marks a doubling of sellers

Lion’s share of this platform’s sales is driven by non-metro geographies

Economy

October 04, 2016 Ambit Capital Pvt. Ltd. Page 13

Exhibit 19: More than 60% of Snapdeal’s sales are driven by non-metropolitan geographies

Source: Snapdeal, Ambit Capital research

However, the most striking feature of e-commerce players reaching out to small sellers/manufacturers is that they are providing this access to the market place at a fairly reasonable cost amounting to ~5% of the product price (see exhibit below).

Exhibit 20: E-commerce majors are offering a selling platform to sellers at a very minimal rate

Category Mobile

Product Price Rs5,000 (including shipping charge to buyers)

Referral Fee Rs175 (3.5% of Rs5000)

Closing Fee/Unit Sold Rs10

Easyship Fee Rs30

Sub-Total Rs215

Service Tax on Fee Rs32.25 (15% inclusive of Swachh Bharat and Krishi Kalyan Cess)

Total Fee Rs247.25

The seller makes Rs4,752.75

Source: Amazon India, Ambit Capital research

In fact, a survey conducted by industry body FICCI explicitly highlights that SMEs find internet platforms to be a cost-effective medium to grow sales (see exhibit below).

Exhibit 21: Most SMEs highlight that e-commerce is a cost-effective medium to grow sales

Source: FICCI SME survey – 2015, Ambit Capital research. Sample size: 951 firms

65% 65% 65% 64% 65% 66% 67% 67% 69% 68% 69% 69%

0%

20%

40%

60%

80%Ju

l-15

Aug

-15

Sep-

15

Oct

-15

Nov

-15

Dec

-15

Jan-

16

Feb-

16

Mar

-16

Apr

-16

May

-16

Jun-

16

Ord

er

mix

by

dest

ina

tio

n fo

r Sn

ap

dea

l

Tier I/Metros Tier II & beyond

44%

43%

37%

35%

32%

0% 10% 20% 30% 40% 50%

Employment

Increase in profits

Increase in sales

Geographic reach

Increase in customers

Reasons given by SMEs for purpose of internet usage

Access to the market place is provided at a fairly reasonable cost amounting to ~5%

SMEs find internet platforms to be cost effective

Economy

October 04, 2016 Ambit Capital Pvt. Ltd. Page 14

The advent of online platforms has indeed transformed the ‘access to end-markets’ of SME manufacturers and retailers. In fact, our primary data checks suggest that sales have increased manifold after these producers started selling their products online (see exhibit below).

Exhibit 22: Small traders/manufacturers have been able to grow sales dramatically by using online platforms

Business Testimony

Seller of multiple products, including toys and electronic items -Area of operations: Central and North India -Size of business: Medium

How has selling on online retail platforms helped your business? The scale of operations has increased manifold since we started doing business with one of the leading online marketplaces in India. We are now selling on a pan-India basis with effectively no marketing cost. How have sales improved after tying up with e-commerce majors? When we started in CY14 we were selling 50 products, but today we are selling 4000 products and 18 different categories.

Manufacturer of antique furniture -Area of operations: Jodhpur -Size of business: Medium

What is your business model? We are an antique furniture manufacturer based in Jodhpur. We have historically been an export oriented business with very little domestic sales till a few years ago. What has been your experience with respect to online selling? We built our own online platform four years ago and have also started selling on major Indian online portals. With minimal domestic sales a few years back, today I am getting 300-500 orders every day. Hence, domestic sales now account for nearly 15-20% of my total sales.

Jewellery Manufacturer -Area of operations: Jaipur -Size of business: Medium

How has tying up with the large e-commerce companies helped your business? There is no doubt that tying up with online retailers has increased hassles with respect to return orders and payments. However, the hassle is completely worth it as we have increased our sales manifold. Can you give us some quantification regarding the increase in sales? Online sales now accounts for 20-25% of our total sales. In the absence of online portals, we actually did very little business outside Jaipur. So the entire online sales piece is over and above what we used to do earlier and, hence, is a big add-on.

Manufacturer of snacks -Area of operations: Pan India -Size of business: Medium

How did you start your business? We felt that there is a market for healthy snacks at reasonable prices. This is the core idea that led us to start our business. What has been the role of online marketplace in your business? Our entire model has no brick and mortar selling component and we sell online only. The technology has allowed us to access a wider marketplace beyond our physical location. What has been your overall experience in selling online? We initially struggled to create space for ourselves as we were new and had to deal with limited customer awareness. Whilst we are still dealing with this issue, the reach we have for our size is disproportionately large. A lot of start-ups are using the online platform as their main selling platform because of this reach that it offers.

Source: Ambit Capital research.

It is also critical to note that manufacturers and retailers across India are increasingly moving towards online business models as they offer a cost-effective way to distribute goods (see exhibit below).

Exhibit 23: SMEs are also setting up websites to directly sell online

Name/Organisation Testimony

Karan Chugh, Proprietor, Florence Clothing

“We will close all our stand-alone stores as soon as the rental deals are over. The overhead operating costs are high and we will save Rs1.5 lakh per store per month if we close them as we save on rentals, utilities and other costs” (https://goo.gl/S5uFKW\).

Chirag Pavecha, MK Synthetics

“Our brick and mortar retail business is credit based and has low returns. Whereas online, we get the order first and then fulfil it, giving us a better view of our inventory and return on investment.” (https://goo.gl/S5uFKW).

Amit Sharda, MD, Soulflower India Pvt. Ltd

“The return on investment in standalone stores is not worth our time. We can double our sales if we put that same money and focus on e-commerce as compared to standalone stores” (https://goo.gl/S5uFKW).

Source: Media reports, Ambit Capital research

Whilst e-commerce players and websites being directly set up by manufacturers for online selling are boosting access to end-markets in India, the improvement in access to end-markets has been mainly driven by the rapid rise in the number of Indians with access to the internet (see exhibit below).

Sales have increased manifold after these producers started selling their products online

Manufacturers and retailers across India are increasingly moving towards online business models

The improvement in access to end-markets has been driven by the rapid rise in the number of Indians with access to the internet

Economy

October 04, 2016 Ambit Capital Pvt. Ltd. Page 15

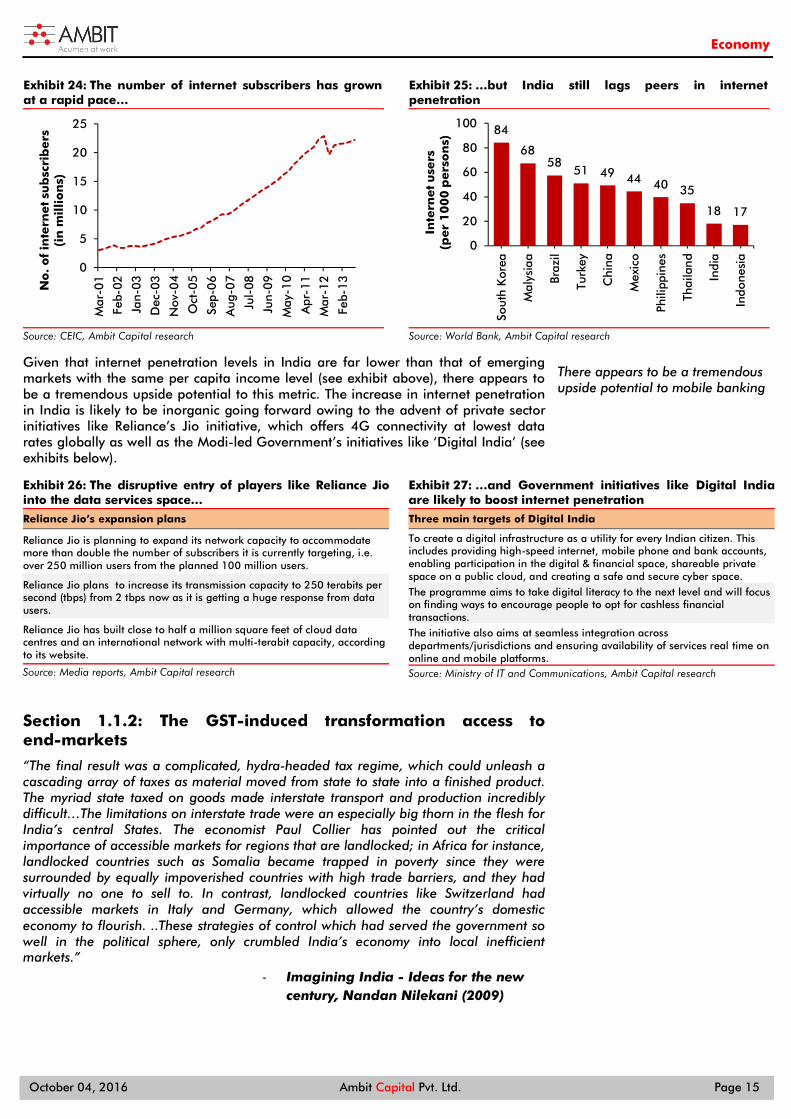

Exhibit 24: The number of internet subscribers has grown at a rapid pace…

Source: CEIC, Ambit Capital research

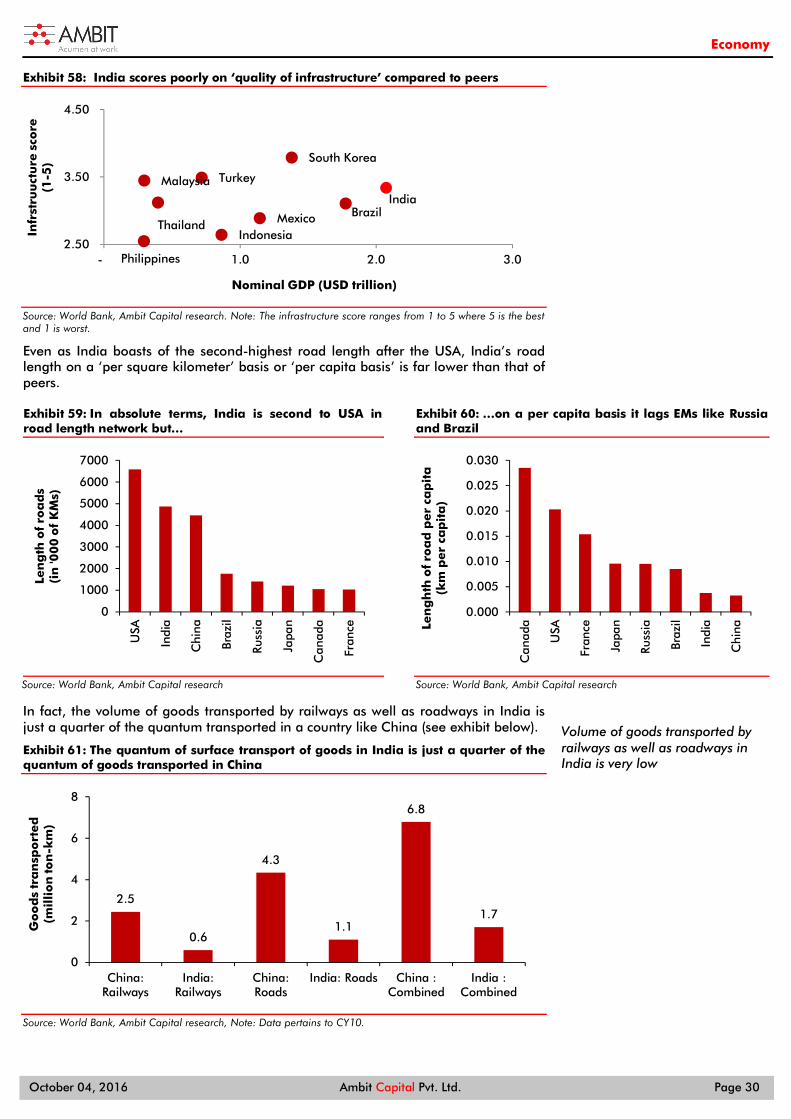

Exhibit 25: …but India still lags peers in internet penetration

Source: World Bank, Ambit Capital research

Given that internet penetration levels in India are far lower than that of emerging markets with the same per capita income level (see exhibit above), there appears to be a tremendous upside potential to this metric. The increase in internet penetration in India is likely to be inorganic going forward owing to the advent of private sector initiatives like Reliance’s Jio initiative, which offers 4G connectivity at lowest data rates globally as well as the Modi-led Government’s initiatives like ‘Digital India’ (see exhibits below).

Exhibit 26: The disruptive entry of players like Reliance Jiointo the data services space…

Reliance Jio’s expansion plans

Reliance Jio is planning to expand its network capacity to accommodate more than double the number of subscribers it is currently targeting, i.e. over 250 million users from the planned 100 million users.

Reliance Jio plans to increase its transmission capacity to 250 terabits per second (tbps) from 2 tbps now as it is getting a huge response from data users.

Reliance Jio has built close to half a million square feet of cloud data centres and an international network with multi-terabit capacity, according to its website.

Source: Media reports, Ambit Capital research

Exhibit 27: …and Government initiatives like Digital Indiaare likely to boost internet penetration

Three main targets of Digital India

To create a digital infrastructure as a utility for every Indian citizen. This includes providing high-speed internet, mobile phone and bank accounts, enabling participation in the digital & financial space, shareable private space on a public cloud, and creating a safe and secure cyber space. The programme aims to take digital literacy to the next level and will focus on finding ways to encourage people to opt for cashless financial transactions. The initiative also aims at seamless integration across departments/jurisdictions and ensuring availability of services real time on online and mobile platforms. Source: Ministry of IT and Communications, Ambit Capital research

Section 1.1.2: The GST-induced transformation access to end-markets

“The final result was a complicated, hydra-headed tax regime, which could unleash a cascading array of taxes as material moved from state to state into a finished product. The myriad state taxed on goods made interstate transport and production incredibly difficult…The limitations on interstate trade were an especially big thorn in the flesh for India’s central States. The economist Paul Collier has pointed out the critical importance of accessible markets for regions that are landlocked; in Africa for instance, landlocked countries such as Somalia became trapped in poverty since they were surrounded by equally impoverished countries with high trade barriers, and they had virtually no one to sell to. In contrast, landlocked countries like Switzerland had accessible markets in Italy and Germany, which allowed the country’s domestic economy to flourish. ..These strategies of control which had served the government so well in the political sphere, only crumbled India’s economy into local inefficient markets.”

- Imagining India - Ideas for the new century, Nandan Nilekani (2009)

0

5

10

15

20

25

Mar

-01

Feb-

02

Jan-

03

Dec

-03

Nov

-04

Oct

-05

Sep-

06

Aug

-07

Jul-

08

Jun-

09

May

-10

Apr

-11

Mar

-12

Feb-

13No

. o

f in

tern

et su

bsc

rib

ers

(in

mil

lio

ns)

84

6858

51 49 44 40 35

18 17

0

20

40

60

80

100

Sout

h K

orea

Mal

ysia

a

Braz

il

Turk

ey

Chi

na

Mex

ico

Phili

ppin

es

Thai

lan

d

Indi

a

Indo

nesi

a

Inte

rnet u

sers

(per

10

00

pers

on

s)

There appears to be a tremendous upside potential to mobile banking

Economy

October 04, 2016 Ambit Capital Pvt. Ltd. Page 16

The introduction of GST will ensure that indirect tax structures are common and uniform across the country. This will eliminate the ‘tax risk’ or make the entire country tax-neutral irrespective of the choice of the geographic location of the business’ operation. In the current framework, three sets of issues are particularly problematic.

A Central Sales Tax (CST) of 2% is levied on inter-state transactions, which creates inefficiencies in the supply chain as goods produced for local consumption attract lower tax rates than those produced for consumption in other states. This creates a cost for the free movement of goods across states as a producer is likely to be able to sell at a more competitive price in the state that he produces in.

Secondly, differential tax regimes across states add to the already elevated cost of movement of goods in India. For instance, according to a study conducted by National Council for Applied Economic Research (NCAER), trucks in India travel only ~200km in a day as opposed to ~800km in the US as 25% of the total travel time is taken by check points and other official stoppages. This raises direct costs in the form of wages to drivers as well as the cost of holding inventory.

Thirdly, according to the Chief Economic Advisor’s report on the revenue-neutral rate, inter-state trade costs exceed intra-state trade costs by a factor of 7x to 16x. This points to the clear existence of border barriers to inter-state movement of goods. Further, inter-state trade costs in India exceed inter-state costs in the US by a factor of 6, suggesting that India’s border effects are large by international comparison. Bringing India’s inter-state trade costs down to the US level could increase welfare by 15%; conversely, completely eliminating intra-state trade frictions could raise welfare by 5%.

The introduction of GST will ensure that indirect tax structures are common and uniform across the country

Central Sales Tax (CST) of 2% creates inefficiencies

Differential tax regimes across states add to the already elevated cost of movement of goods in India

There is a clear existence of border barriers to inter-state movement of goods

Economy

October 04, 2016 Ambit Capital Pvt. Ltd. Page 17

Section 1.2: Transformation#2: Access to capital

“Finance thrives when financial infrastructure is strong. The RBI has been working hard to improve the financial infrastructure of the country - it has made tremendous advances, for example, in strengthening the payment and settlement systems in the country. Similarly, it has been working on improving information sharing through agencies such as credit bureaus and rating agencies. I propose to carry on such work, which will be extremely important to enhance the safety and speed of flows as well as the quality and quantity of lending in the country. On the retail side, I particularly want to emphasise the use of the unique ID, Aadhaar, in building individual credit histories. This will be the foundation of a revolution in retail credit.”

-Dr. Raghuram Rajan’s first speech as the 23rd Governor of the RBI delivered on 4 September 2013

Three powerful sets of changes underway in India are dramatically transforming ‘access to finance’ in India namely, (1) Improvement in access to capital for SME’s (through schemes like MUDRA and credit being extended by e-commerce majors), (2) improvement in access to consumer finance (through schemes like PMJDY and lenders competing to provide retail credit) and (3) system-level improvements in the lending landscape in India owing to increased competition ‘amongst banks’ and ‘to banks’ (from NBFCs, corporate bonds and other financial technology driven sources). India’s lending landscape has been ‘closed’ and ‘oligopolistic’ thus far

“Normally manufactures in India face real capital costs (nominal lending charges minus inflation) exceeding 4-5% compared with 1-2% costs for their global competitors...It is reported that in a survey, that more than two-thirds of SMEs preferred not to utilise commercial bank credit because of the long and complicated processing times and large volume of collateral demanded by banks.”

- Revisiting manufacturing policy, Rajiv Kumar Senior Fellow at The Centre for Policy Research, 2014

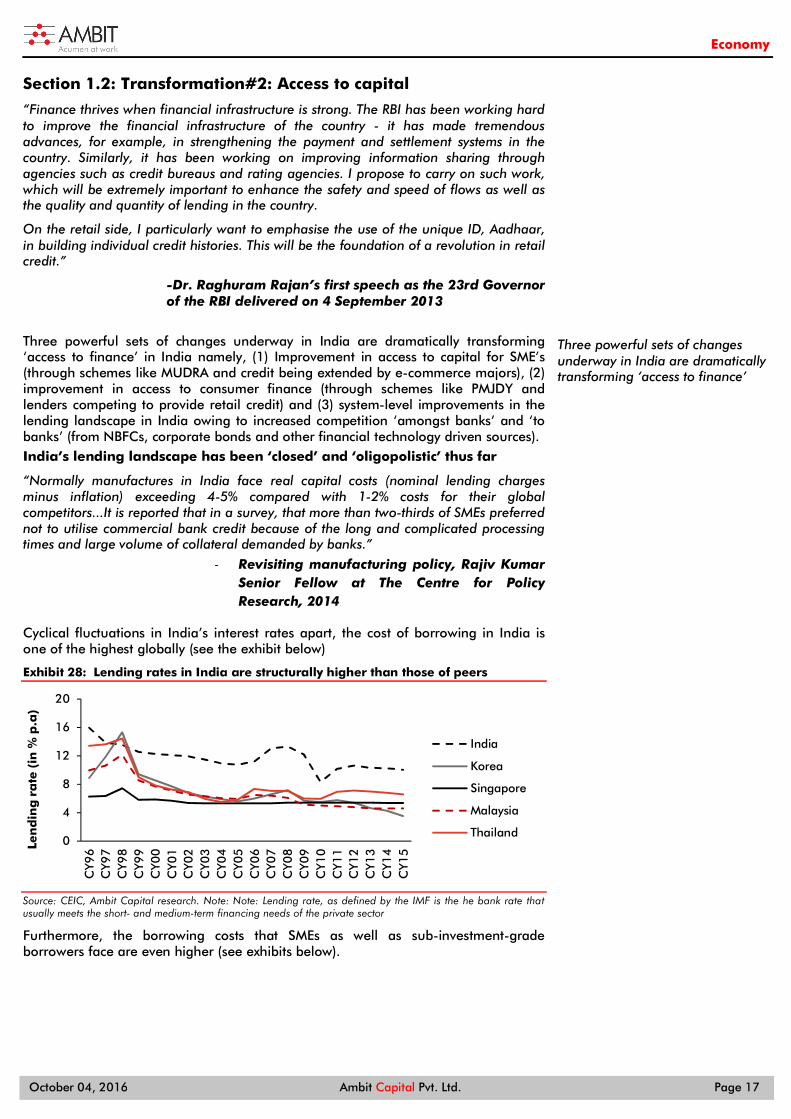

Cyclical fluctuations in India’s interest rates apart, the cost of borrowing in India is one of the highest globally (see the exhibit below)

Exhibit 28: Lending rates in India are structurally higher than those of peers

Source: CEIC, Ambit Capital research. Note: Note: Lending rate, as defined by the IMF is the he bank rate that usually meets the short- and medium-term financing needs of the private sector

Furthermore, the borrowing costs that SMEs as well as sub-investment-grade borrowers face are even higher (see exhibits below).

0

4

8

12

16

20

CY9

6C

Y97

CY9

8C

Y99

CY0

0C

Y01

CY0

2C

Y03

CY0

4C

Y05

CY0

6C

Y07

CY0

8C

Y09

CY1

0C

Y11

CY1

2C

Y13

CY1

4C

Y15Le

nd

ing

ra

te (

in %

p.a

)

India

Korea

Singapore

Malaysia

Thailand

Three powerful sets of changes underway in India are dramatically transforming ‘access to finance’

Economy

October 04, 2016 Ambit Capital Pvt. Ltd. Page 18

Exhibit 29: SMEs in India face higher borrowing costs from banks

Source: RBI, Ambit Capital research. Note: The lending rate used is the average of the rate offered by the 5 largest banks in India.

Exhibit 30: BBB borrowers face borrowing costs in excess of 10% in India

Source: CEIC, Ambit Capital research

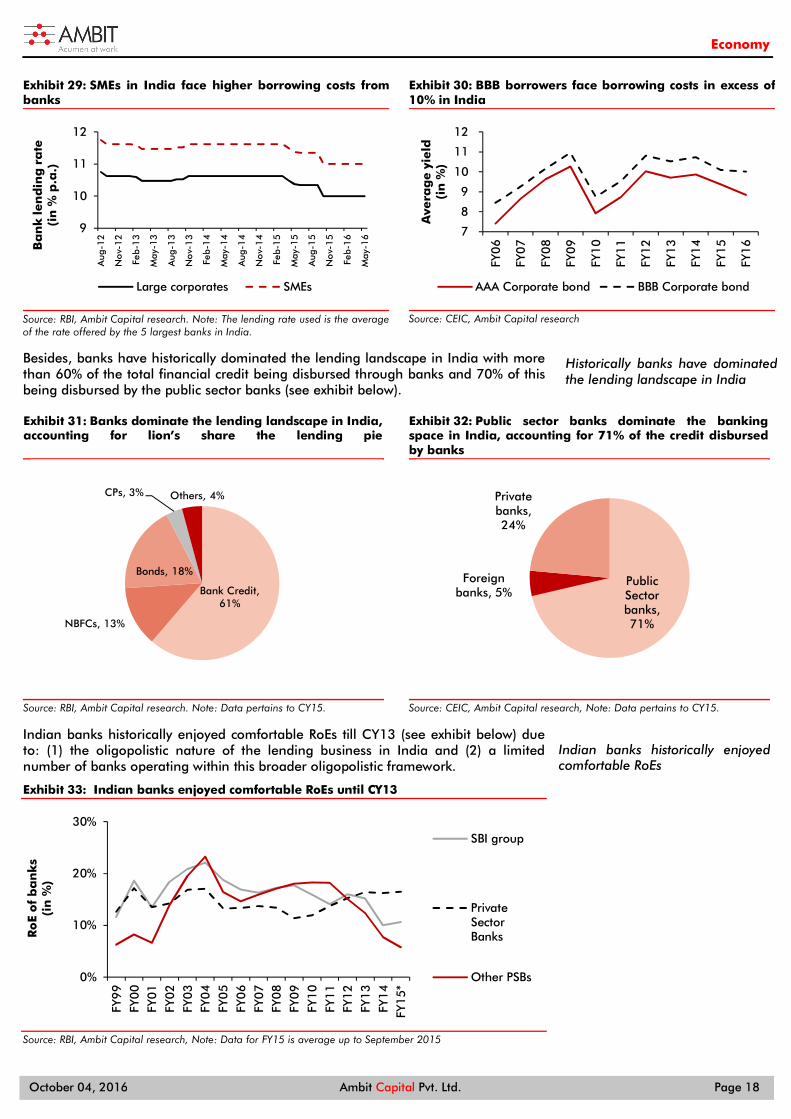

Besides, banks have historically dominated the lending landscape in India with more than 60% of the total financial credit being disbursed through banks and 70% of this being disbursed by the public sector banks (see exhibit below).

Exhibit 31: Banks dominate the lending landscape in India, accounting for lion’s share the lending pie

Source: RBI, Ambit Capital research. Note: Data pertains to CY15.

Exhibit 32: Public sector banks dominate the banking space in India, accounting for 71% of the credit disbursed by banks

Source: CEIC, Ambit Capital research, Note: Data pertains to CY15.

Indian banks historically enjoyed comfortable RoEs till CY13 (see exhibit below) due to: (1) the oligopolistic nature of the lending business in India and (2) a limited number of banks operating within this broader oligopolistic framework.

Exhibit 33: Indian banks enjoyed comfortable RoEs until CY13

Source: RBI, Ambit Capital research, Note: Data for FY15 is average up to September 2015

9

10

11

12

Aug

-12

No

v-1

2

Feb-

13

May

-13

Aug

-13

No

v-1

3

Feb-

14

May

-14

Aug

-14

No

v-1

4

Feb-

15

May

-15

Aug

-15

No

v-1

5

Feb-

16

May

-16

Ba

nk

len

din

g r

ate

(i

n %

p.a

.)

Large corporates SMEs

7

8

9

10

11

12

FY0

6

FY0

7

FY0

8

FY0

9

FY1

0

FY1

1

FY1

2

FY1

3

FY1

4

FY1

5

FY1

6

Ave

rag

e y

ield

(in

%)

AAA Corporate bond BBB Corporate bond

Bank Credit, 61%

NBFCs, 13%

Bonds, 18%

CPs, 3% Others, 4%

Public Sector banks, 71%

Foreign banks, 5%

Private banks, 24%

0%

10%

20%

30%

FY9

9FY

00

FY0

1FY

02

FY0

3FY

04

FY0

5FY

06

FY0

7FY

08

FY0

9FY

10

FY1

1FY

12

FY1

3FY

14

FY1

5*

Ro

E o

f b

an

ks

(in

%)

SBI group

PrivateSectorBanks

Other PSBs

Historically banks have dominated the lending landscape in India

Indian banks historically enjoyed comfortable RoEs

Economy

October 04, 2016 Ambit Capital Pvt. Ltd. Page 19

Not only did Public Sector Banks (PSBs) dominate the lending landscape in India until CY13, but the model of lending dominated by PSBs often favoured large corporates with political patronage. The clear advantage that access to capital yielded in a capital-scarce economy was evident from the fact that politically connected companies used to outperform the overall markets until CY10 (see exhibit below).

Exhibit 34: Politically connected companies outperformed the broader market until CY10

Source: Bloomberg, Ambit Capital research

This structure in which a handful of banks dominated the lending landscape in India (typically lending to their cronies with less than ideal due diligence) was the root cause of the lending binge that transpired between FY04-08. During this period, GDP growth was recorded at an average pace of 9% YoY, gross capital formation (GFCF) grew at a multi-decadal high pace of 19% YoY (in real terms), and non-food credit grew at 28% YoY (see exhibit below).

Exhibit 35: The lending binge spanning FY04-08 was funded by indiscriminate bank lending

Source: Bloomberg, Ambit Capital research

This indiscriminate lending by banks to politically connected companies resulted in bad loans piling up to record levels in the Indian banking system, thereby compromising the traditional banking system’s ability to lend (see exhibits below).

-

500

1,000

1,500

2,000

2,500

3,000

Jan-

04

May

-04

Sep-

04

Jan-

05

May

-05

Sep-

05

Jan-

06

May

-06

Sep-

06

Jan-

07

May

-07

Sep-

07

Jan-

08

May

-08

Sep-

08

Jan-

09

May

-09

Sep-

09

Jan-

10

May

-10

Sep-

10

Ambit Connected Cos Index BSE 500

20% 20%

9%

27% 28%

16%17% 17%

7%

0%

5%

10%

15%

20%

25%

30%

Bank-Credit Non-food GFCF

Ave

rag

e Y

oY g

row

th

20 yr average FY04-08 FY09-13

The model of lending dominated by PSBs often favoured large corporates with political patronage.

Banks typically lent money to their cronies with less than ideal due diligence

This indiscriminate lending by banks to politically connected companies resulted in bad loans

Economy

October 04, 2016 Ambit Capital Pvt. Ltd. Page 20

Exhibit 36: Gross NPAs have increased in public sector banks…

Source: RBI, Ambit Capital research.

Exhibit 37: …as also in private sector banks

Source: RBI, Ambit Capital research.

Resets induced by Modi, Rajan and Technology are disrupting the old system of lending

Three powerful sets of changes underway in India are dramatically transforming ‘access to finance’ in India, namely: (1) Improvement in access to capital for SMEs (through schemes like MUDRA and credit being extended by e-commerce majors), (2) improvement in access to consumer finance (through schemes like PMJDY and lenders competing to provide retail credit), and (3) system-level improvements in the lending landscape in India owing to increased competition ‘amongst banks’ and ‘to banks’ (from NBFCs, corporate bonds and other financial technology driven sources).

Change#1: Improvement in access to capital for SMEs

“Small businesses are run by smart businessmen but their growth currently is being limited by a shortage of capital; this is why we are launching the Growth Capital programme”

- Ankit Nagotri, Chief Business Officer, Flipkart [July 17, 2015]

Access to capital for SMEs is set to improve dramatically going forward owing to three sets of forces springing to life, namely:

The end of an era whereby large companies foreclosed supply of credit for SMEs by virtue of their political connectivity,

E-commerce majors extending loans to SMEs, and

Government-driven schemes like Micro Units Development and Refinance Agency (MUDRA) boosting access to capital.

E-commerce majors are now extending credit to the tune of Rs500bn-600bn, or ~0.4% of GDP, annually to SME sellers (according to our retail team) and MUDRA-driven credit disbursements are projected to increase to Rs1.8tn, or ~1.2% of GDP, by FY17-end. This compares to the credit of Rs4.9tnn or 3.6% of GDP extended by banks to SME in FY16.

In the section below, we elaborate on each of these three strands that are improving access to capital for SMEs.

The end of the crony-capitalist centered lending era: Thus far, politically linked companies had privileged access to capital; hence, SMEs ended up paying unusually high cost for debt with the supply of credit being foreclosed by the politically-linked large companies. The resets engineered by PM Modi are now breaking the crony capitalists’ privileged access to capital. The fall of politically linked companies is evident from the fact that the index of politically connected companies has underperformed the overall markets since CY10 (see exhibit below).

0%

4%

8%

12%

16%

FY1

1

FY1

2

FY1

3

FY1

4

FY1

5

1H

FY16

PSUsRestructuredLoansPSUs GrossNPAs

0%

2%

4%

6%

FY1

1

FY1

2

FY1

3

FY1

4

FY1

5

1H

FY16

PrivateRestructuredLoans

Private GrossNPAs

Three powerful sets of changes underway in India are dramatically transforming ‘access to finance’

Access to capital for SMEs is set to improve dramatically

E-commerce majors are now extending credit to the tune of Rs500-600bn, or ~0.4% of GDP,annually to SME sellers

SMEs ended up paying unusually high costs for debt

Economy

October 04, 2016 Ambit Capital Pvt. Ltd. Page 21

Exhibit 38: P-75 index has underperformed the broader market since CY10

Source: Bloomberg, Ambit Capital research

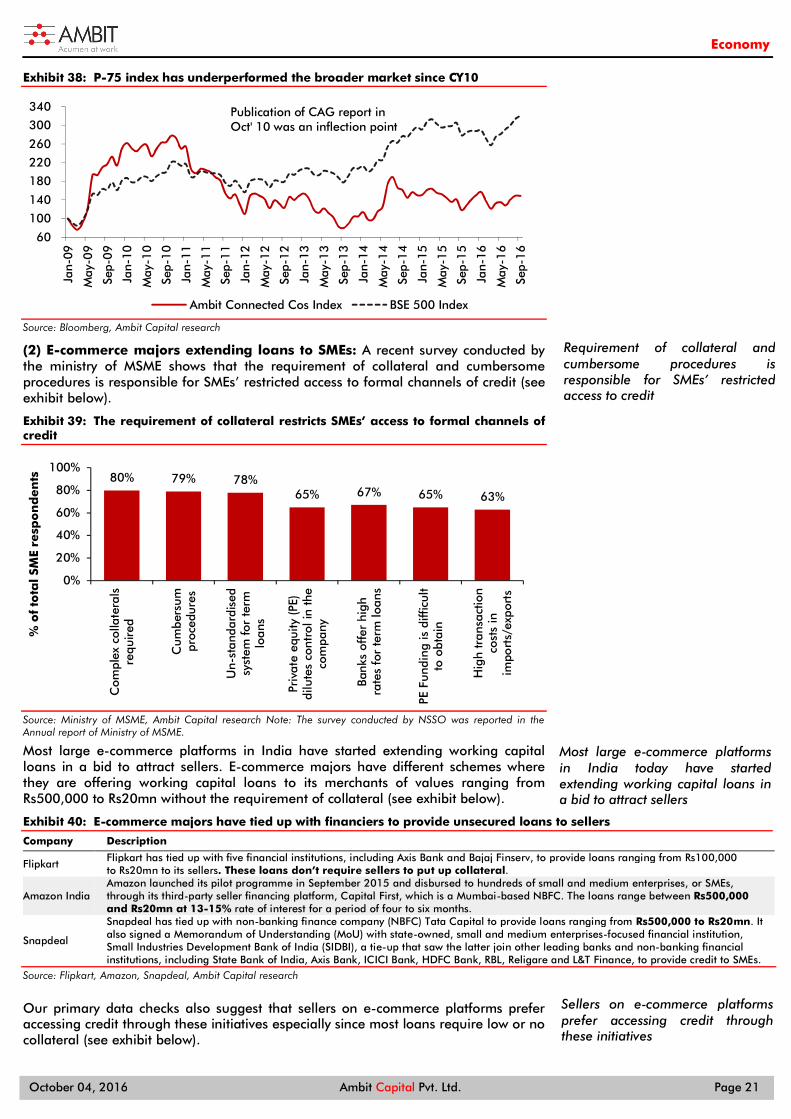

(2) E-commerce majors extending loans to SMEs: A recent survey conducted by the ministry of MSME shows that the requirement of collateral and cumbersome procedures is responsible for SMEs’ restricted access to formal channels of credit (see exhibit below).

Exhibit 39: The requirement of collateral restricts SMEs’ access to formal channels of credit

Source: Ministry of MSME, Ambit Capital research Note: The survey conducted by NSSO was reported in the Annual report of Ministry of MSME.

Most large e-commerce platforms in India have started extending working capital loans in a bid to attract sellers. E-commerce majors have different schemes where they are offering working capital loans to its merchants of values ranging from Rs500,000 to Rs20mn without the requirement of collateral (see exhibit below).

Exhibit 40: E-commerce majors have tied up with financiers to provide unsecured loans to sellers

Company Description

Flipkart Flipkart has tied up with five financial institutions, including Axis Bank and Bajaj Finserv, to provide loans ranging from Rs100,000 to Rs20mn to its sellers. These loans don’t require sellers to put up collateral.

Amazon India Amazon launched its pilot programme in September 2015 and disbursed to hundreds of small and medium enterprises, or SMEs, through its third-party seller financing platform, Capital First, which is a Mumbai-based NBFC. The loans range between Rs500,000 and Rs20mn at 13-15% rate of interest for a period of four to six months.

Snapdeal

Snapdeal has tied up with non-banking finance company (NBFC) Tata Capital to provide loans ranging from Rs500,000 to Rs20mn. It also signed a Memorandum of Understanding (MoU) with state-owned, small and medium enterprises-focused financial institution, Small Industries Development Bank of India (SIDBI), a tie-up that saw the latter join other leading banks and non-banking financial institutions, including State Bank of India, Axis Bank, ICICI Bank, HDFC Bank, RBL, Religare and L&T Finance, to provide credit to SMEs.

Source: Flipkart, Amazon, Snapdeal, Ambit Capital research

Our primary data checks also suggest that sellers on e-commerce platforms prefer accessing credit through these initiatives especially since most loans require low or no collateral (see exhibit below).

60

100

140

180

220

260

300

340

Jan-

09

May

-09

Sep-

09

Jan-

10

May

-10

Sep-

10

Jan-

11

May

-11

Sep-

11

Jan-

12

May

-12

Sep-

12

Jan-

13

May

-13

Sep-

13

Jan-

14

May

-14

Sep-

14

Jan-

15

May

-15

Sep-

15

Jan-

16

May

-16

Sep-

16

Ambit Connected Cos Index BSE 500 Index

80% 79% 78%65% 67% 65% 63%

0%

20%

40%

60%

80%

100%

Com

plex

col

late

rals

requ

ired

Cum

bers

umpr

oced

ures

Un-

stan

dard

ised

syst

em fo

r te

rmlo

ans

Priv

ate

equi

ty (

PE)

dilu

tes

cont

rol i

n th

eco

mpa

ny

Bank

s of

fer

high

rate

s fo

r te

rm lo

ans

PE F

undi

ng is

diff

icul

tto

obt

ain

Hig

h tr

ansa

ctio

nco

sts

inim

port

s/ex

port

s

% o

f to

tal SM

E re

spo

nd

en

ts

Requirement of collateral and cumbersome procedures is responsible for SMEs’ restricted access to credit

Most large e-commerce platforms in India today have started extending working capital loans in a bid to attract sellers

Sellers on e-commerce platforms prefer accessing credit through these initiatives

Publication of CAG report in Oct' 10 was an inflection point

Economy

October 04, 2016 Ambit Capital Pvt. Ltd. Page 22

Exhibit 41: Sellers and manufacturers are availing credit facilities extended by e-commerce majors

Business Testimony

Seller of multiple products including toys and electronic items Area of operations: Central and North India Size of business: Medium

“All the major e-commerce majors have offered me credit without collateral and on simple terms. This is a huge relief as obtaining loans from the banks is difficult without a collateral. I have used this platform to get credit once in the past year and plan to use it in future as well.”

Seller of apparels Area of operation: Central India Size of business: Medium

“I have not used the credit facilities myself but had availed it for my manufacturer who is a supplier. The process was easy and they got a loan of Rs800,000 within few days of registering and applying for the same.”

Source: Ambit Capital research

Globally, advances made in analytics have helped e-commerce players develop full-fledged lending businesses that are a source of easily accessible and affordable credit to SME sellers (see exhibit below for a case study on China).

Exhibit 42: Case study of the rise of Alibaba in China

Head Description

E- commerce major Alibaba’s financial arm, Ant Financial

In China, Alibaba’s financial arm, Ant Financial, within a span of 4 years has scaled up a range of financial products varying from online payments to lending to credit scoring

Carved out in 2011, Ant Financial and its flagship product, Alipay, commands more than 82% share in China’s online payment market (although part of this could be because of the protection from competitive forces that Alibaba has received from the Chinese authorities)

This combined with other services such as wealth management, provides Ant Financial access to rich data (e.g. shopping history, utility bills, work & home addresses, property, family links

Financial access to rich data (e.g. shopping history, utility bills, work & home addresses, property, family links). Analytics on this data has enabled Ant’s lending business to cater to small businesses which were previously neglected by the banks due to sub-par credit scores

Source: iresearch global, Ambit Capital research

Among the online marketplaces in India, Flipkart, Snapdeal and Amazon, have begun offering working capital loans to their merchants using merchants’ selling patterns, ratings, customer feedback and social media profile for credit scoring. This sub-activity undertaken by e-commerce players in India has the potential of growing into a full-fledged business in India thereby alleviating the acute problem of access to capital to India’s small borrowers. In fact early signs of such businesses taking off can already be seen in India (see exhibit below).

Exhibit 43: Online e-commerce majors have started providing working capital loans to sellers

Title/Source Description

Paytm starts offering collateral-free loans for merchants on its platform (Livemint, July 11, 2016 http://goo.gl/cNvLKW).

Payments services and e-commerce firm Paytm on July 11 said it has started offering collateral-free working capital loans for merchants on its platform. These small loans would be in the range of Rs10,000 to Rs100,000 thousand, which can be increased later based on the eligibility criteria and the working capital needs of merchants, Paytm said.

Flipkart to arrange easy working capital loans to vendors to ensure loyalty (The Economic Times, Dec 09, 2015 http://goo.gl/Xc9RKa).

Flipkart has started providing easy working capital loans to its sellers. Merchant loyalty and engagement have become key factors in India's cut-throat e-commerce industry. Snapdeal and Amazon, too, have launched similar loan schemes for their merchants, seeking to lock in key sellers and encourage them to sell more. Flipkart, India's largest online marketplace by sales, said its loan scheme will give its vendors easier access to loans with basic documentation in 2-5 days.

Shopclues plans to disburse Rs50bn worth loan to sellers ( Livemint, August 23, 2016 http://goo.gl/CTw4DR)

Shopping portal ShopClues (Clues Network Pvt. Ltd) on August 23 said it plans to disburse Rs50bn worth of loans to merchants selling on its platform under its financing initiative Capital Wings. Of this, Rs2bn will be disbursed ahead of this year's Diwali festival.

Source: Media reports, Ambit Capital research

(3) Government driven schemes like MUDRA: PM Modi introduced the Micro Units Development and Refinance (MUDRA) scheme in CY15 under which small ticket loans of various sizes are offered to the small and medium entrepreneurs without any collateral. MUDRA is set to partner with Banks, Micro Finance Institutions (MFIs) and other lending institutions in a bid to boost access to capital for SMEs (see exhibit below).

Advances made in analytics have helped e-commerce players develop full-fledged lending businesses

Among the online marketplaces in India, Flipkart, Snapdeal and Amazon, have begun offering working capital loans

MUDRA is set to partner with Banks, Micro Finance Institutions (MFIs) and other lending institutions in a bid to boost access to capital for SMEs

Economy

October 04, 2016 Ambit Capital Pvt. Ltd. Page 23

Exhibit 44: MUDRA will partner banks/MFIs to provide financial assistance to the MSME sector

Source: mudra.org.in, Ambit Capital research

The MUDRA scheme incentivises SME lending by the banking and MFI sectors mainly because the financial institutions can get refinance from MUDRA and also a Government guarantee in which 50% of the bad loans will be covered by National Credit Guarantee Corporation (NCDC).

Our discussions with the Chief Financial Officer (CFO) of MUDRA suggest that the Government has actually put the MUDRA scheme on priority and the progress is monitored regularly through the Prime Minister’s Office (PMO).

A similar scheme was run in Indonesia (see exhibit below for details) and its success points to the upside potential of such a scheme.

Exhibit 45: Indonesia’s KUR is similar to MUDRA

Scheme Details

Microfinance Program: Kredit Usaha Rakyat (KUR)

The Indonesian government intends to disburse IDR 30 trillion (USD 2.2 billion) in small business loans under its Kredit Usaha Rakyat (KUR) program, which is intended to provide credit to micro-, small and medium-sized enterprises (MSMEs) and cooperatives. The aims of KUR include boosting economic growth in 2015 and decreasing microcredit interest rates.

The Government would subsidise state banks so they could cut their microcredit interest rate from 21 to 12% starting in 2015

The government reduced the cap on the annual interest rate of loans under KUR from 22% to 21% and set the maximum amount of each collateral-free loan at IDR 15 million (USD 1,150) as of March 2015.

Source: Media reports, Ambit Capital research

50% of the NAPs will be covered by National Credit Guarantee Corporation (NCDC).

Economy

October 04, 2016 Ambit Capital Pvt. Ltd. Page 24

Change#2: The improvement in access to consumer finance

Given the fact that there is no sign of an investment recovery materialising in India, within bank credit growth the main component that has been growing at a rapid pace is retail credit (see exhibit below).

Exhibit 46: Retail credit has been growing at a faster pace than overall credit

Source: RBI, Ambit Capital research

The combination of the Pradhan Mantri Jan-Dhan Yojna (PMJDY), the JAM trinity (i.e. Jan Dhan-Aadhaar-Mobile) and Unified Payments Interface (UPI) possesses the potential of vastly democratising access to capital in a country where 40% of consumer finance is raised from informal sources. PM Modi launched the Pradhan Mantri Jan-Dhan Yojna (PMJDY) scheme in August 2015 and, as a result of this scheme, every Indian household today has a bank account (see exhibit below). As per the latest data, 1.03bn Indians possess Aadhaar cards and this unique number is being linked to their bank accounts to transfer various Government subsidies directly into the account of the beneficiaries (see exhibit below).

Exhibit 47: Aadhaar and bank accounts have been used to transfer various Government subsidies

Item

Number of Aadhaar cards seeded (in millions

Status as on May 31, 2014

Status as on Mar 31, 2016

LPG connections 28.2 122.8

Food & Public Distribution (No. of ration cards) 12 113.9

MNREGA Job cards NA 59

National Social assistance program (Pension Scheme) NA 9.5

Voter ID cards NA 310

PMJDY NA 93.2

Passport NA 2.4

CBDT(Income TAX) Returns NA 4.5

Jeevan Pramaan (Pension certificate) NA 1.4

Source: Ministry of Communication and Information technology, Ambit Capital research. Note: The Government has started seeding Aadhaar cards to various beneficiaries’ identities to remove duplication.

The JAM trinity (i.e. Jan Dhan-Aadhaar-Mobile) has helped boost mobile banking in India in a big way (see exhibits below). In FY16, Rs625bn (or 0.5% of GDP) of credit was disbursed via mobile banking (see exhibit below).

0%

5%

10%

15%

20%

25%

Jul-

15

Jul-

15

Aug

-15

Sep-

15

Sep-

15

Oct

-15

Nov

-15

Nov

-15

Dec

-15

Jan-

16

Jan-

16

Feb-

16

Mar

-16

Mar

-16

Apr

-16

May

-16

Jun-

16

Jun-

16

Jul-

16

Yo

Y g

row

th(i

n %

)

Retail credit Overall credit

The main component that has been growing at a rapid pace is retail credit

As per the latest data, 1.03bn Indians possess an Aadhaar card

JAM trinity (i.e. Jan Dhan-Aadhaar-Mobile) has helped boost mobile banking in India in a big way

Economy

October 04, 2016 Ambit Capital Pvt. Ltd. Page 25

Exhibit 48: Mobile banking has grown at a rapid pace in the recent past

Source: RBI, Ambit Capital research

The launch of the Unified Payments Interface (UPI) by the National Payments Corporation of India (NPCI) is likely to act as a catalyst to dramatically increase mobile banking because: (1) the UPI plays the critical role of being the central registry which can convert detailed account information into a one word address, (2) UPI acts as a payment “bridge” between all Indian individuals as well as firms, and (3) UPI allows people to request for payments.

With the UPI, one might simply need to enter details and get a billing request on the phone. This request can then be accepted or rejected right away. For example, a local grocery shop from which you purchase grocery items frequently could take your UPI details and then at the end of each month can send you a bank request for the money owed. You simply have to accept or reject the request. This is revolutionary in the sense that it eliminates use of personal details such as bank account number or credit card details (see exhibit below).

Exhibit 49: The UPI payments interface is likely to dramatically boost the prospects of mobile banking in India

Head Description

What is UPI and what can a user do with the app?

UPI is a payment system that allows money transfer between any two bank accounts by using a smartphone. UPI allows a customer to pay directly from a bank account to different merchants, both online and offline, without the hassle of typing credit card details, IFSC code, or net banking/wallet passwords.

How can one download the UPI app?

The UPI app of 19 banks -- Andhra Bank, Axis Bank, Bank of Maharashtra, Bhartiya Mahila Bank, Canara Bank, Catholic Syrian Bank, DCB Bank, Federal Bank, ICICI Bank, TJSB Sahakari Bank, Oriental Bank of Commerce, Karnataka Bank, UCO Bank, Union Bank of India, United Bank of India, Punjab National Bank, South Indian Bank, Vijaya Bank and YES Bank -- will be available on the Google Play Store of Android phones in the next few days for customers to download.

What is revolutionary about the concept?

People can send money using virtual ID - they do not have to give other details. They just have to enter the virtual ID on the payments page of the vendor and they will receive an alert on the mobile asking them to authorise the transaction. Secondly, a vendor can use UPI to “pull” the payment from the customer’s account.

Source: Media reports, Ambit Capital research

As Nandan Nilekani put it on the date of the launch of UPI on April 11, 2016, “Payments have evolved in different ways. You had a card system, mobile money, Internet e-wallets. But completely mobile interoperable person-to-person instant real time with push and pull really didn’t exist anywhere. So I think that is where UPI is a leapfrog”.

In fact, the combination of UPI and JAM can spur liability-side innovation in a big way. Using the UPI-NPCI bridge, the payment banks and the small finance banks licensed by the RBI in 2015 can extend their reach into the wallets of the 300 million Indians who receive subsidy payments from the Government. Using mobile phones, rather than branches, these new types of banks can hoover up the savings of not just the currently financially excluded constituency but also of salaried middle class workers who at present receive sub-par interest rates from their banks. Such savings account portability will become easy if employers pay salaries to employees’ Aadhaar numbers from where UPI-NPCI directs the payment to the account chosen by the employee. In effect, the UPI will make the money in savings accounts fungible between accounts. The Payment Bridge will make the account itself portable. Thus, if a new upstart bank offers better savings rates, employees can individually map their

0

100

200

300

400

500

600

700A

pr-0

4O

ct-0

4A

pr-0

5O

ct-0

5A

pr-0

6O

ct-0

6A

pr-0

7O

ct-0

7A

pr-0

8O

ct-0

8A

pr-0

9O

ct-0

9A

pr-1

0O

ct-1

0A

pr-1

1O

ct-1

1A

pr-1

2O

ct-1

2A

pr-1

3O

ct-1

3A

pr-1

4O

ct-1

4A

pr-1

5O

ct-1

5Mo

bil

e b

an

kin

g tra

nsa

ctio

ns

(in

IN

R b

illi

on

)

The launch of the UPI by the NPCIis likely to act as a catalyst to dramatically increase mobile banking

Combination of UPI and JAM can spur liability-side innovation in a big way

Economy

October 04, 2016 Ambit Capital Pvt. Ltd. Page 26

Aadhaar numbers to the new bank’s accounts (rather than waiting for the employer to make the decision for the entire company). If one keeps in mind that accounts with less than Rs1 lakh of savings account for 80% of the corpus deposited in savings accounts in India, the scale and scope of the disruption become evident.