economy in good shape

TRANSCRIPT

BUSINESS

Economy in Good Shape Forecasts for 1956 business indicate peak year but some let-down in activity after midyear

A HE BUSINESS PICTURE looks very good for 1956. Economists look for 1956 to top 1955, but al l display conservatism about prospects for activity during the latter half of the current year. Whatever the predictions, the facts of the matter are that 1956 is a presidential election year, and much depends on congressional "politicking" and particularly on t h e identity of the presidential candidates. Also, there will be continual upward pressure on prices and especially strong pressure for wage increases. Politicians will have many fits between now and election day resolving trie influences on voters of higher prices versus higher wages. In a boiling election year, the August Federal Reserve Board will be hard pressed to follow the bare dictates of good, sound economic policy which may require strict controls on credit and the supply of money.

some signs of economic indigestion perhaps around midyear. At that point, the FRB will probably be willing to relax austerity in the money market and, in fact, provide some stimulus to the economy, within the limits of its ability to do so.

• NICB Report. The National Industrial Conference Board predicted a breakthrough in gross national product to better than $400 billion, possibly as high as $410 billion during the first half of the year, unemployment of 2.5 million, a rise of 1.5 points in the wholesale price index but no change in the consumer products price index. Elements of strength as we enter 1956, according to the report, are the hard core for expansion, further accumulation of inventories, pressures of population resulting in increased state and local spending, and the possibility of tax relief. The NICB economist •^ointed to increasin0" si^ns of strain

and stress in the economy, and thought the second half of 1956 would bear careful watching.

A Du Pont economist at the meeting predicted a 5 % decline in textile production in the second half. Such a decline may serve to cool, for a time, d ie boom in synthetic fiber expansion.

• Declme of !%* An estimate of $398 billion for gross national product in 1956, starting higher and ending lower, is made by Fortune. The decline during the year in CNP is estimated at only 1%, and expectations are for a completion of this "high-level readjustment" by the end of the year. Business will turn up in 1957. Basic considerations governing these projections involve a rapid rise in business inventories coupled with some limitations in consumer spending as debt repayments mount. Industrial production now seems to be at a peak, and a downturn seems inevitable. Fortunately, capital outlays are increasing to what appears to be a record high. The latest Department of Commerce survey shows that businessmen expect a continuation in the rise in new plant and equipment expenditures from seasonally adjusted rates of $29.5 billion in the third quarter of 1955 to estimated rates of $31 billion and $31.5 billion in the fourth quarter and first quarter of 1956, respectively. Unadjusted rates for the chemicals and allied products industries were $239 million, $300 million, and $294 million resOectiveh7.

2 7 8 C & E N J A N . 16, 1956

fGmeNmtf&£TS3

PROCESS

imDMBTfajesf TlSfeNDiS

PHENOLIC PLASTICS l a n d Other Tar Ariel Resincl

V INYL RESINS CELLULOSE ACETATE PLASTICS

Production, Millions o f Pounds Production Millions o f Pounds

Production, Molding and Extrusion Materiols , Sheets, Rods, a n d Tube, Millions of Pounds

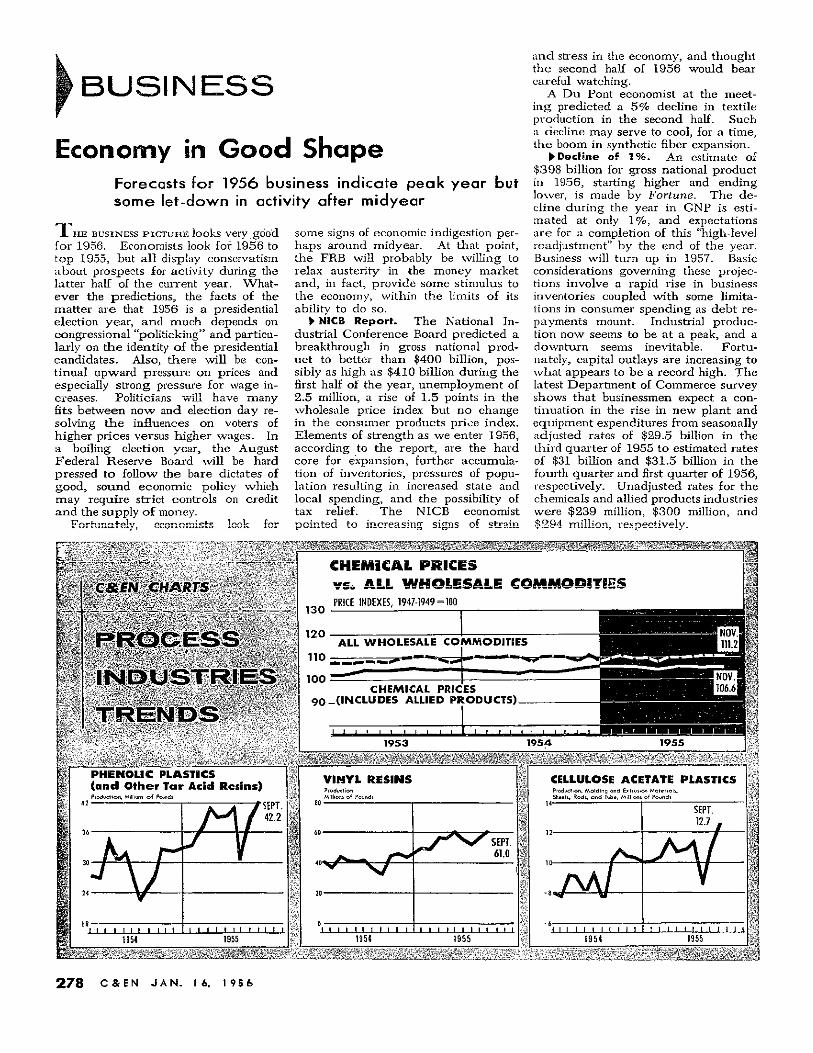

CHEMICAL I»K1€ES

~£* AtL WHOLESALE COMMODITIES PRICE INDEXES. 1947-1949 = 100

NOV. 111.2

NOV. 106.6

130

120

no 100

90

ALL WHOLESALE COMMODITIES

CHEMICAL PRICES (INCLUDES ALLIED PRODUCTS)

1953 1954 1955

1954 1955 1954 1955

SEPT. 42.2

SEPT. 61.0

SEPT. 12.7

1954 1955

Larger unemployment is predicted up to the level of 4 million by- the year end, and relatively stable prices and wage costs.

• Automobiles. It is hard to visualize production and disappearance (into owner channels) of almost 8 million automobiles last year. Certainly, the fortunes of the auto industry mean a great deal to chemical process industries as paint, glass, rubber, metals, etc. For the current year, car production will taper off to the level of 7 million cars, predicted by General Motors, while Fortune estimates new car sales at 6,250,000 versus 7.4 million last year. The Secretary of Commerce figures auto production at 4,250,000 during the first half year.

Economists are saying that t h e cyclic durable goods industries will fare poorly in 1956. These industries would include autos, tires, and appliances for the most part. Notwithstanding their reduced consumption of steel, the steel industry looks for very good business, aided by record construction expenditures for new plant and equipment The nation's steel-making capacity is rated at 128 million tons, a gain of only 2 % over a year ago. Tlie industry's per capita capacity is now up to 1547 pounds versus 1320 in 1950, and it does not appear to be sufficient. Certainly the chemical industry is feeling the pinch today as steel requirements for new plant capacity are not readily forthcoming.

• Chemicals. Progress in rJhe chemical industry in 1956 will probably not be up to standard, and certainly will not come anywhere near matching the amazing recovery of 1955. The industry moves ahead of the economy as a whole, but it is so closely integrated to the economy that progress is distinctly affected by the economic outlook and climate. In the absence of another durable goods boom, the chemical industry will have to make up for some lost business in these segments of the economy by gains in sales to capital goods industries (users of plastics, for example) and to consumer goods industries as petroleum, textile, food, and tobacco. Last >^ear, construction expenditures for chemicals and allied products were at a low ebb, reaching just over $1 billion. Consequently, capacity additions will not provide a relatively large increment of sales gains. As a result, sales gains for the chemical industry may be very modest at an average of 5% t o produce an estimated industry total of about $24.5 billion for 1956.

CHART CREDITS: Chemical Prices vs. All Wholesale Commodities—Department of Labor; Vinyl Resins, Cellulose Acetate Plastics, Phenolic Plostics-Department of Commerce.

if Your Filter Medium Is Blinding Or Clogging

The Use Ot E&D Filter Paper As A Cover

May Be Inukated!

Many commercial filtration processes are troubled with slurry that contains slimy fines, gelatinous or minute particles. In a large number of such cases the use of E & D filter paper as a "cover" over the filter medium will p r o v i d e finer filtration while protecting the medium. The cost of the paper is sufficiently low to warrant peeling it off and discarding after use leaving the medium underneath relatively clean. Savings in production time can be substantial.

Write for our FILTRATION ANALYSIS REPORT. We will recommend the proper grade for your use and send free samples for testing.

THE EATON-DIKEMAN CO. FILTERTOWN

MT. HOLLY S P R I N G S . PENNA.

The only company in America exclusively devoted to the manufacture of f i l ter^

"paper for science and industry. - F I L T E R P A P E R -

KEEP YOUR MERCURY CLEAN

This radical improvement is a fast, economical method of purifying mercury for any laboratory or plant.

The motor-driven OXIFIER separates by air oxidation the dissolved base metals from the body of contaminated mercury. (2 to 4 hrs. per 25-Ib. batch.) The TYPE " F " FILTER removes the resultins oxide-dusl and scum, as well as water, oil and all other floating materials, leaving the mercury bright and lively with a mirror-like surface. ( 2 5 lbs. per 6 min.)

This OXIFIER-FILTER process renders low-cost prime virgin or accumulated scrap mercury equal, and in important respects superior, to expensive triple-distilled. It is entirely suitable for use in meters, instruments, and electrical apparatus.

Also available: Large Industrial and Small Sets. Write for Catalog No. 54.

OXIFIER, 26-lb. capacity $198.00 FILTER, Type F $50.00 5-Ib. u 85.00 " Û 20.00

150-lb. " 660.00 " H 160.00

&etdee4e#t s4frfra*atccé (^umfeaetfy 810 FRONT ST., HELLERTOWN, PA.

J A N . 16, 19 5 6 C & Ε Ν 2 7 9

BY THE

^let&ieÂem l^toceéé,