education finances...financial advisors. this presentation is not individual investment advice. if...

TRANSCRIPT

EDUCATION FINANCESQ4 2019 Participant Webinar

2CAPTRUST

Information about Today’s Session

• Select “Computer audio” to join via VOIPOR Select “Phone call” to dial in

• All attendee’s lines are muted

• Questions can be asked by typing them into the questions pane on the control panel, and there will be time at the end of the session to answer questions

• Submitted questions will not be visible to other audience members

• All attendees will receive a copy of the presentation after the webinar

• Today’s session is being recorded

3CAPTRUST

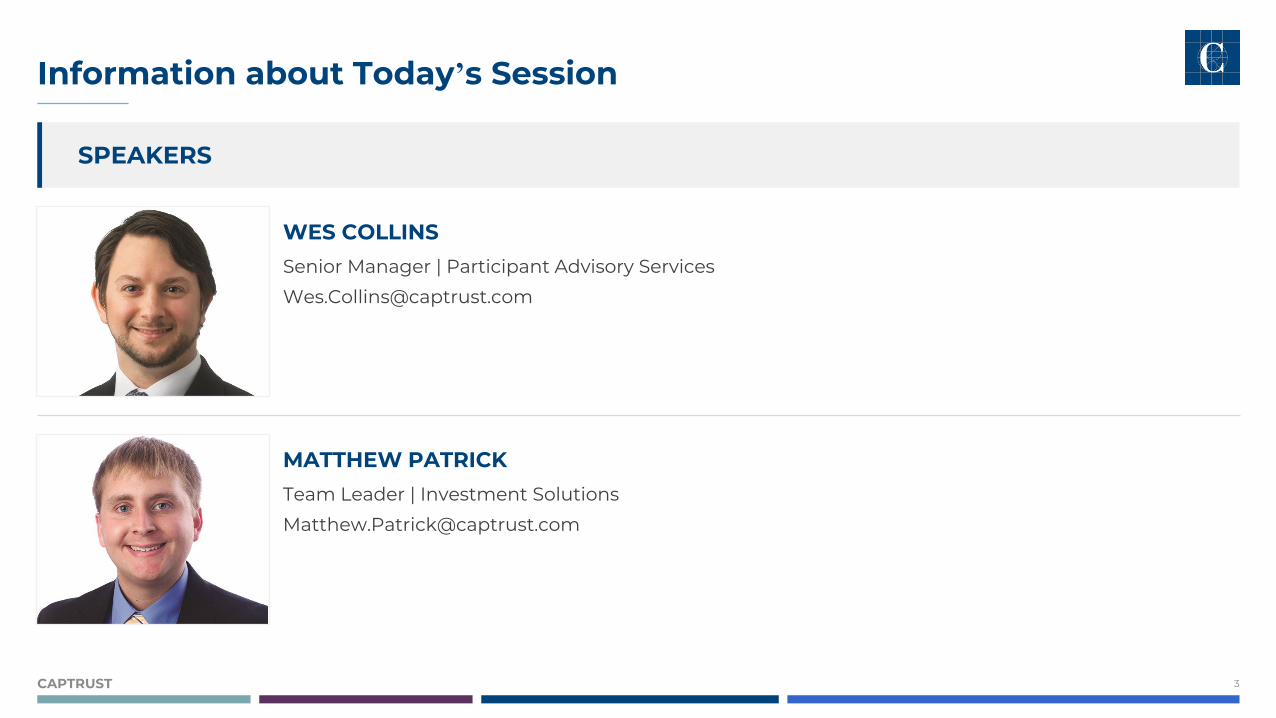

Information about Today’s Session

SPEAKERS

WES COLLINS

MATTHEW PATRICK

Team Leader | Investment Solutions

Senior Manager | Participant Advisory Services

4CAPTRUST

Legal Disclaimers

Individual investors have particular needs in planning for retirement. No single solution fits every investor.

YOUR INDIVIDUAL NEEDS AND GOALS ARE JUST AS UNIQUE AS YOU ARE.

This presentation is intended as a visual component to a broad educational program presented by CAPTRUST Financial Advisors. This presentation is not individual investment advice. If you have questions or concerns regarding your own individual retirement needs, please contact a CAPTRUST representative for further assistance.

CAPTRUST does not render legal, accounting, or tax advice. This material has been prepared solely for informational purposes and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any performance data quoted represents past performance. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Past performance is no guarantee of future results.

5CAPTRUST

Poll #1

Which financial situation do you currently have going on in your life?

A. Saving for a child’s education

B. Managing student loan debt (for yourself or a child)

C. Saving for retirement

6CAPTRUST

Agenda

Financial Aid and Student Loans

Saving for Education

Managing Student Loan Debt

01

02

03

7CAPTRUST

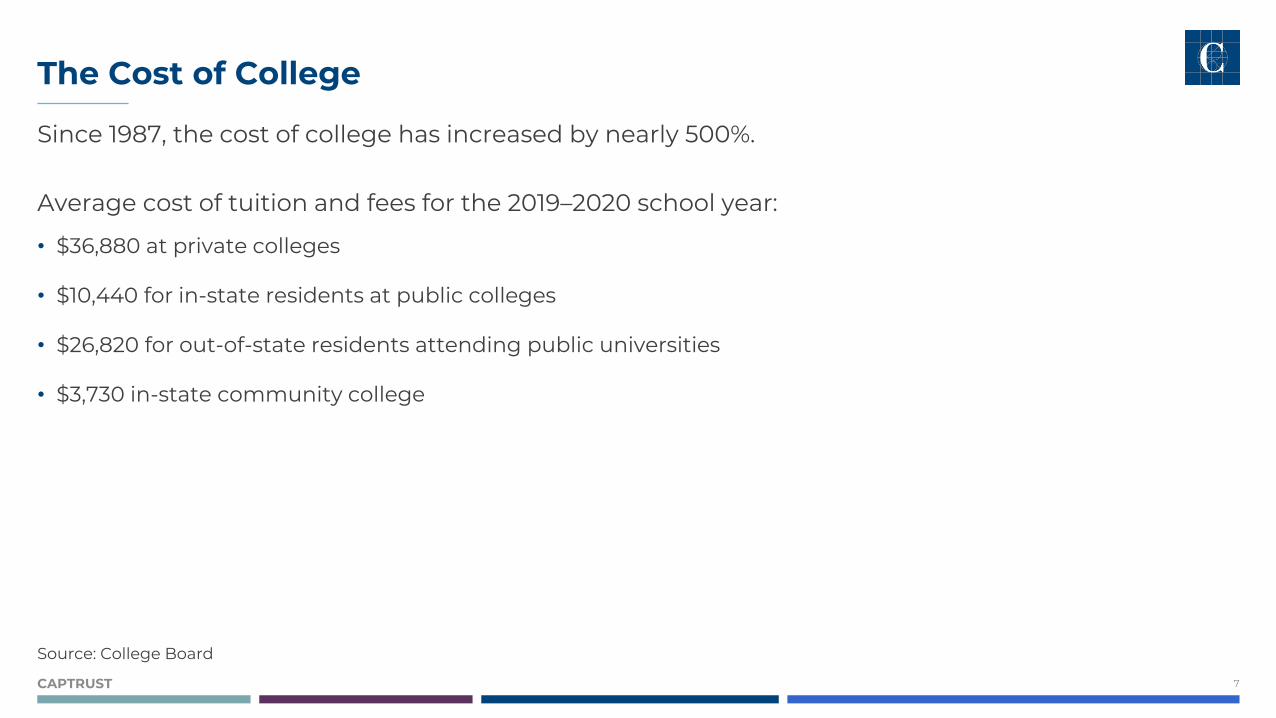

The Cost of College

Since 1987, the cost of college has increased by nearly 500%.

Average cost of tuition and fees for the 2019–2020 school year:

• $36,880 at private colleges

• $10,440 for in-state residents at public colleges

• $26,820 for out-of-state residents attending public universities

• $3,730 in-state community college

Source: College Board

8CAPTRUST

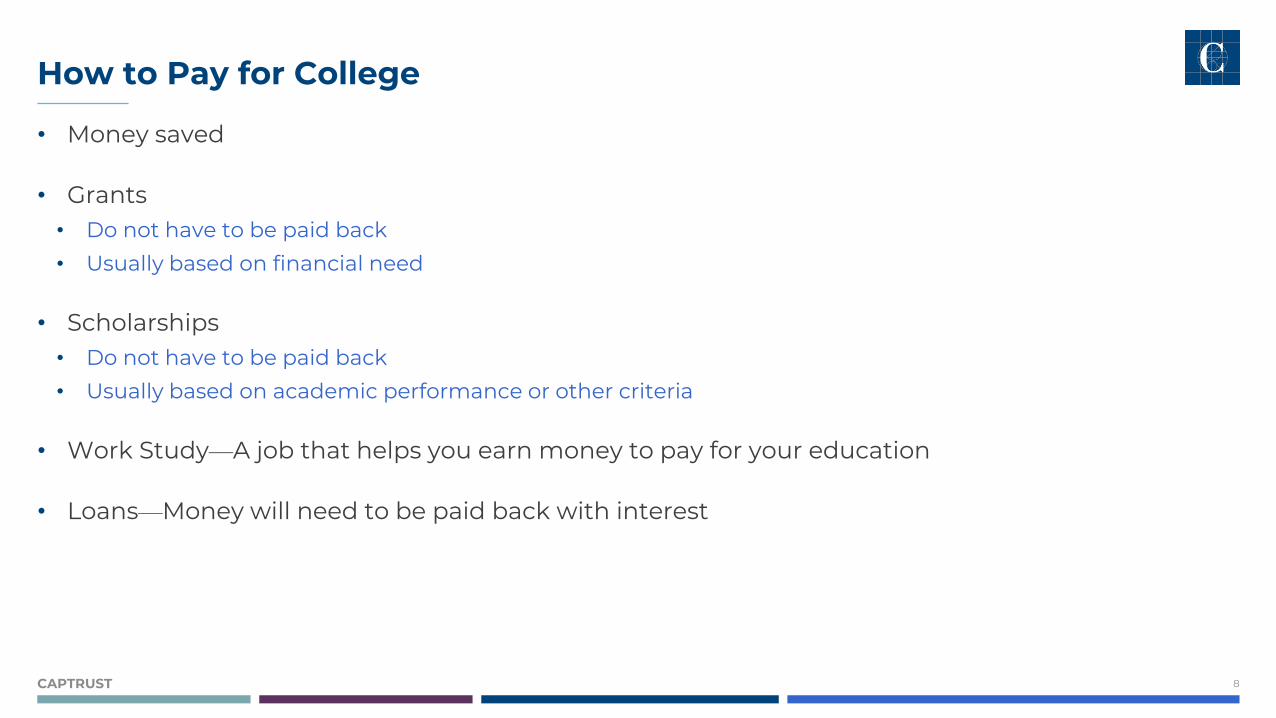

How to Pay for College

• Money saved

• Grants• Do not have to be paid back

• Usually based on financial need

• Scholarships • Do not have to be paid back

• Usually based on academic performance or other criteria

• Work Study—A job that helps you earn money to pay for your education

• Loans—Money will need to be paid back with interest

FINANCIAL AID AND STUDENT LOANS

71%Source: U.S. Department of Education

10CAPTRUST

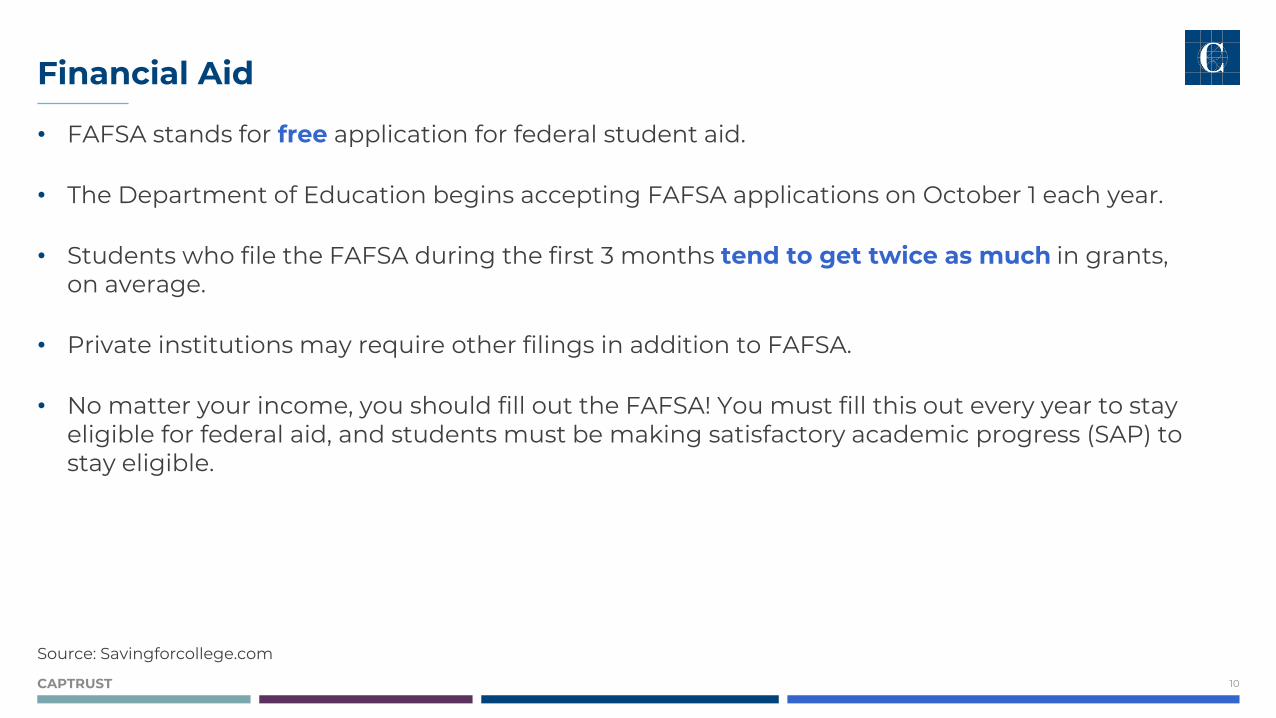

Financial Aid

• FAFSA stands for free application for federal student aid.

• The Department of Education begins accepting FAFSA applications on October 1 each year.

• Students who file the FAFSA during the first 3 months tend to get twice as much in grants, on average.

• Private institutions may require other filings in addition to FAFSA.

• No matter your income, you should fill out the FAFSA! You must fill this out every year to stay eligible for federal aid, and students must be making satisfactory academic progress (SAP) tostay eligible.

Source: Savingforcollege.com

11CAPTRUST

Financial Aid

Footer

Do you know what your state offers?

Tuition assistance (or free tuition):

• Fees, room, and board will still need to be funded

• Typically only for participating in-state community colleges, associate-degree programs, and vocational schools

• If considering these programs, make sure to research all requirements

• Helpful resource: www.nasfaa.org/State_Financial_Aid_Programs

12CAPTRUST

Federal and Private Student Loans

Federal—Loans from the U.S. government

• Direct Subsidized—Based on financial need • Up to $5,500, for undergraduates

• Interest is delayed

• Direct Unsubsidized—Financial need not required • Up to $20,500 (less subsidized amounts) for undergraduates and graduate students

• Borrower responsible for interest at all times

• Direct PLUS—Financial need not required, but required to credit check • For parents of undergraduate students, or for graduate students

• Maximum amount is cost of attendance minus financial aid

Private—Loans through banks and other financial institutions

• Not based on financial need

• Credit checks will be required

13CAPTRUST

How Do You Know How Much You Might Spend?

Source: Valuepenguin.com

Calculating loan repayment amounts

Repayment ratios

What a job might pay and what might be required: www.studentaid.gov/careersearch

LOAN TYPE BORROWER INTEREST RATE LOAN FEE

Direct Subsidized Undergraduate 4.53% 1.059%

Direct Unsubsidized Undergraduate 4.53% 1.059%

Direct Unsubsidized Graduate or Professional 6.08% 1.059%

Direct PLUS Parents, Graduate, or Professional 7.08% 4.236%

14CAPTRUST

College Savings Calculator

Use the calculator on CAPTRUSTadvice.com to determine your needs.

What do you need to run a calculation?

• Child’s age and expected age to start college

• Current savings balance (if any)

• Monthly contributions (if any)

• Expected college cost

• Estimated inflation and investment return

SAVING FOR EDUCATION

16CAPTRUST

Investing for Education

Most common options:

• 529 plans

• Coverdell Educational Savings Accounts (ESA)

• Prepaid tuition plans

• Uniform Gifts to Minors Act (UGMA) and Uniform Transfers to Minors Act (UTMA)

17CAPTRUST

Poll #2

If you are currently saving for an education, what account types are you using?

A. 529 plan

B. UGMA/UTMA

C. Coverdell ESA

D. Personal savings/investment accounts

18CAPTRUST

Investing for Education

529 Saving Plan—A state-sponsored educational savings option

• After-tax way to save

• Typically no residency requirements; some states provide in-state tax benefits

• Menu of investments to choose from

• Up to $15,000 per year without gift tax issues; up to $75,000 using a 5-year treatment

• Distributions for qualified education expenses are tax-free

• Distributions for nonqualified expenses usually incur a 10 percent penalty, taxes on earnings

• Accounts can be reassigned

• As of 2017, up to $10,000 per year can be used at private, public, and religious K-12 schools

19CAPTRUST

Investing for Education

529 Pre-Paid Tuition Plan—A state-sponsored education option

• Typically has residency requirements, age limitations, and enrollment periods

• Locking in tuition at today’s rates

• Buy units or credits at participating universities for future tuition and fees

• No investment options

• Typically do not cover other costs like room and board

• May not get full benefit if deciding to go to an out-of-state school

• Typically transferable

Helpful resource: https://www.Morningstar.com/articles/947035/a-primer-on-prepaid-529-plans

20CAPTRUST

Investing for Education

COVERDELL ESA UGMA/UTMA ACCOUNTS

• Can be used to pay for qualified K-12 and higher education expenses

• Earnings can grow tax-free

• Contributions limited to $2,000 a year (not tax deductible)

• Withdrawals for qualified expenses are free from federal tax

• Can contribute until beneficiary is 18 years of age

• Distribution must occur prior to age 30

• Income restrictions

• Custodial account for a minor

• No income or contribution limits, but gift tax can apply above limit

• Irrevocable gift

• Beneficiary gains control at age of majority

• Withdrawal for any reason at age of majority

• Varied taxation based on minor

• Counted as student’s assets; heavier impact on financial aid eligibility

21CAPTRUST

Other Savings

Will using money from retirement accounts impact your ability to retire?

• Using a Roth IRA• Income limitations

• After-tax account

• Up to $6,000 per year

• Contributions can be withdrawn without taxes or penalties

• Tapping into pre-tax accounts• Taxes on distributions

• Exception to 10% penalty if used for college tuition and other qualified expenses

• Borrowing from employer-sponsored plan• Many plans allow for loans

• Pay yourself back with interest

• What are the costs?

• What if I leave employment?

MANAGING STUDENT LOAN DEBT

23CAPTRUST

Poll #3

If you currently have student loan debt, approximately how much do you have?

A. Less than $25,000

B. $25,000 - $50,000

C. $50,000 - $75,000

D. $75,000 - $100,000

E. $100,000 +

24CAPTRUST

Student Debt

Sources: Federal Reserve Bank of NY; The Brookings Institute, “Borrowers with Large Balances: Rising Student Debt and Falling Repayment Rates”, Feb 2018; The Institute for College Access and Success

• Over 44 million Americans have some sort of student debt.

• Total outstanding student loan debt measures in at $1.5 trillion, making it the second highest category of consumer debt behind mortgage debt.

• Borrowers in the class of 2018, on average, owe $29,200.

• According to the TD Banks “Student Debt Impact Survey”, $1 of every $5 of take-home pay is spent repaying student loan debt.

25CAPTRUST

Student Debt

Source: Consumer Financial Protection Bureau

Student debt is not only an issue for the young.

• Around 2.8 million American adults over the age of 60 carry student loan debt.

• Since 2005, the number of older adults with student loan debt has quadrupled. The average amount owed jumped from around $12,000 to $23,000.

• Three-quarters of adults over 60 with student loan debt said they borrowed for their children’s education.

• Thirty-nine percent said they had gone without meeting healthcare needs to afford their student loan payments.

26CAPTRUST

Social Impact of Student Debt

• Student loan debt negatively impacts ability to save for other goals.

• Fifty-four percent of respondents to a TD Bank survey said they maxed out credit lines.

• Millennials are delaying buying homes, contributing towards retirement, building rainy day fund, marrying, and starting families.

• Financial stress has health impacts—stress-induced headaches, insomnia, anxiety, and isolation.

• Financial stress leads to lost productivity in the workplace.

Source: TD Bank Student Debt Impact Survey

27CAPTRUST

Managing Debt

• Get organized.

• Prioritize spending and budget.

• Accelerate payments.

• Consolidate or refinance.

• Investigate income-driven repayment.

• Consider deferment/forbearance.

• Get counseling. The National Foundation for Credit Counseling and American Student Assistance offer advice on how to tackle your debt. These two nonprofit organizations can provide online or in-person help.

28CAPTRUST

Public Service Loan Forgiveness Program

If you are employed by a government or not-for-profit organization, you may be able to receive loan forgiveness

Teacher Loan Forgiveness Program

If you teach full-time for five complete and consecutive academic years in a low-income school or educational service agency, and meet other qualifications, you may be eligible for forgiveness of up to $17,500

Both programs have numerous requirements including length of service, types of loans, and staying current on payments

As of September 30, 2018:

Total number of applications: 49,669

Number of applications denied: 32,409

Borrowers who have received student loan forgiveness: 206

Helpful Resource: https://blog.ed.gov/2019/09/public-service-loan-forgiveness-tips

Student Loan Forgiveness

29CAPTRUST

Taxes and Education

There may be tax credits or deductions for an education.

• Credits—Reduce the amount of income tax you may have to pay• Lifetime Learning Credit

• American Opportunity Tax Credit

• Deductions—Reduce the amount of your income that is subject to tax; thus, generally reducing the amount of tax you may have to pay

• Student loan interest deduction—Income limitations and must be a qualified student loan used for qualified education expenses

30CAPTRUST

Key Takeaways

Save early and often:

• Open 529 plan and encourage gifts for the future

• Understand impact of using retirement funds for a child’s education

Investigate loans available privately and/or via the federal government, so that you know:

• what is available;

• who is eligible;

• when interest begins; and

• the repayment terms.

6th

Grade

9th

Grade

12th

Grade

Discuss with children as early as 6th grade whether they are considering higher education

By 9th grade, discuss with children how you may be able to support them financially for college

Senior year, make sure they apply for FAFSA on October 1

31CAPTRUST

Key Takeaways

Tips for managing loans post-graduation.

• Get organized.

• Investigate options; ask for help because this is complicated.

• Do not miss payments or default.

• Develop a plan and write it down.

32CAPTRUST

Resources and Articles

• www.savingforcollege.com/

• www.collegeboard.org/

• studentaid.ed.gov/sa/

• www.morningstar.com/save-for-college

• www.nfcc.org

(National Foundation for Credit Counseling)

33CAPTRUST

Schedule an Appointment or Call Directly

CAPTRUST Advice Desk Hours

Monday–Thursday 8:30AM–5:30PM ET

Friday 8:30AM–4:00PM ET

Evening appointments available.

captrustadvice.com

Online

800.967.9948

Call

THANK YOU!

Please take a moment to share your thoughts with us and fill out our survey.