eg-ach quick reference guide - egyptianbanks.com reference guide v1.1.pdf · this reference guide...

TRANSCRIPT

EG-ACH QUICK

REFERENCE GUIDE

Version 1.0

Issued: September 2012

1 0 T A L A A T H A R B S T – E V E R G R E E N T O W E R

F I F T E E N T H F L O O R – C A I R O 1 1 5 2 2 E G Y P T

T : + 2 0 ( 2 ) 2 5 7 9 3 0 7 0 F : + 2 0 ( 2 ) 2 5 7 9 3 0 7 1

W W W . E G Y P T I A N B A N K S . C O M

Document: EG-ACH Quick Reference Guide Page No. 1 of 12

02/09/12

Version 1.0

©EBC 2012

Confidential and Proprietary Information to EBC Not to be disclosed without written permission from Egyptian Banks Company for Technological Advancement

Table of Contents

1 INTRODUCTION ......................................................................................................................... 2

2 DIRECT DEBIT ............................................................................................................................. 2

WHAT IS A DIRECT DEBIT? ............................................................................................................. 2 2.1

WHAT COMPANIES USE THE DIRECT DEBIT SCHEME? ......................................................................... 2 2.2

WHO IS INVOLVED? ...................................................................................................................... 2 2.3

WHAT IS A DIRECT DEBIT MANDATE? .............................................................................................. 3 2.4

MANDATE TYPES: ........................................................................................................................ 3 2.5

2.5.1 Irrevocable Mandate .......................................................................................................... 3

2.5.2 Revocable Mandate ............................................................................................................ 5

HOW LONG DOES IT TAKE FOR A TRANSACTION TO GO THROUGH ........................................................... 6 2.6

HOW TO BECOME A REGISTERED BILLER ........................................................................................... 6 2.7

HOW TO INITIATE A DIRECT DEBIT TRANSACTION ............................................................................... 6 2.8

WHO COULD COLLECT THE MANDATES? .......................................................................................... 6 2.9

DIRECT DEBIT FULL CYCLE .............................................................................................................. 7 2.10

IS IT SAFE? .................................................................................................................................. 7 2.11

SEEKING REFUNDS........................................................................................................................ 7 2.12

3 DIRECT CREDIT ........................................................................................................................... 8

WHAT IS A DIRECT CREDIT? ........................................................................................................... 8 3.1

BENEFITS FOR SENDERS/RECEIVERS ................................................................................................. 8 3.2

WHAT COMPANIES USE DIRECT CREDIT? ......................................................................................... 8 3.3

WHO IS INVOLVED? ...................................................................................................................... 8 3.4

HOW THE DIRECT CREDIT SCHEME WORKS ....................................................................................... 8 3.5

DIRECT CREDIT WINDOW TIMING ................................................................................................... 9 3.6

3.6.1 Same Day Settlement Windows .......................................................................................... 9

3.6.2 Forward Value Settlement Window .................................................................................. 10

IS IT SAFE? ................................................................................................................................ 11 3.7

Document: EG-ACH Quick Reference Guide Page No. 2 of 12

02/09/12

Version 1.0

©EBC 2012

Confidential and Proprietary Information to EBC Not to be disclosed without written permission from Egyptian Banks Company for Technological Advancement

1 Introduction The Automated Clearing House System (ACH) is established for bulk processing of individual

and recurrent electronic credit and debit transfers initiated by commercial banks or by their

customers. Such recurrent fund transfers include direct credit of salary payments by

employers, regular remittances by individuals, direct debits from utility companies to collect

amounts due from their customers and direct debits from finance companies to collect

installments due on consumer loans, etc. This electronic processing of direct credit and

direct debit transactions will reduce the economy’s reliance on costly check processing.

This reference guide is intended for use and reference by banks and their business and

private customers, and is divided into two sections, direct debit, and direct credit.

2 Direct Debit

What is a Direct Debit? 2.1A direct debit is a quick, easy and convenient method of making regular payments (e.g. bills,

installments, subscriptions, etc…) without having to visit a bank. Direct Debit is used

throughout the world and is acknowledged as one of the most cost effective and efficient

methods of processing regular and periodic payments.

What Companies Use the Direct Debit Scheme? 2.2Direct Debits are used for bill collection throughout the world, by insurance, utilities,

finance, service suppliers, automobile, and other companies that receive regular and

periodic payments. It is generally acknowledged by Originators to be the most cost effective

and efficient method of bill collection.

Who is involved? 2.3 The Creditor (Biller or Originator), i.e. The Company that provides the goods or

services.

The Creditor Bank, where the originator maintains its accounts.

The Debtor (Customer or Payer), i.e. the Bank customer who wishes to pay the bills

and whose account is to be debited.

Mandate Processor, In charge of collecting the mandates from the banks and

converting them to electronic mandates

Mandate Portal, portal where mandates are hosted

The Debtor Bank, i.e. the Bank holding the Payer’s account, which is to be debited.

The ACH Network, i.e. the operator of the ACH network, who will perform routing,

clearing, and dispute resolution.

Document: EG-ACH Quick Reference Guide Page No. 3 of 12

02/09/12

Version 1.0

©EBC 2012

Confidential and Proprietary Information to EBC Not to be disclosed without written permission from Egyptian Banks Company for Technological Advancement

What is a Direct Debit Mandate? 2.4A Direct Debit Mandate is an instruction from a customer to his bank authorizing a specific

organization, known as the Originator, to collect varying amounts from his account in

settlement of outstanding bills for goods or services provided.

Mandate Types: 2.5Currently there are two types of EG-ACH Direct Debit Mandate. Both Mandate types are

standard and governed by the scheme, the form of standard Mandate is approved and

published by EBC to all participants as they will be obliged to use EG-ACH Direct Debit

standard Mandate form in order use the Direct Debit Service.

The Debtor could sign any type of Mandate form based on his agreement with the Creditor:

Irrevocable Mandate

Revocable Mandate

In the event of an inconsistency between the Mandate terms and condition stated in the

Rulebook, and the Mandate terms and conditions stated in the latest version of the

Mandate announced and officially published by EBC, the provisions of the latest terms and

conditions stated in the Mandate shall prevail the Mandate terms and condition stated in

this Rulebook.

2.5.1 Irrevocable Mandate The irrevocable Mandate has the following characteristics:

All Debit transactions initiated by the Creditor based on the Irrevocable Mandate

shall be irrevocable transaction and could not be subject to refund upon Debtor

request.

Payment frequency as per the underlying payment terms and conditions stated in

the signed contract between the Creditor and the Debtor, such contract is not

governed by the scheme.

Mandate shall not be cancelled without mutual agreement between the Debtor and

the Creditor.

In the event that the Creditor has misused the Irrevocable Mandate, the Debtor

could submit a claim to EBC through the Debtor bank.

EBC shall provide dispute service to EG-ACH Participants. Dispute process may be

used for resolving Unresolved Issues that arise in respect of the Irrevocable Mandate

and relevant Direct Debit transactions between the Debtor/Debtor Bank and the

Creditor/Creditor Bank, the following issues shall be subject to dispute:

o The Debtor decides to dispute Direct Debit transaction due to a breach

occurs by the Creditor to the Mandate terms and conditions.

o The Debtor submits an Irrevocable Mandate cancellation request.

Dispute is applicable for the Irrevocable Mandate and relevant Direct Debit

transactions only under the terms and conditions stated in the Dispute rules

document shared and announced by EBC.

Document: EG-ACH Quick Reference Guide Page No. 4 of 12

02/09/12

Version 1.0

©EBC 2012

Confidential and Proprietary Information to EBC Not to be disclosed without written permission from Egyptian Banks Company for Technological Advancement

Document: EG-ACH Quick Reference Guide Page No. 5 of 12

02/09/12

Version 1.0

©EBC 2012

Confidential and Proprietary Information to EBC Not to be disclosed without written permission from Egyptian Banks Company for Technological Advancement

2.5.2 Revocable Mandate The Revocable Mandate has the following characteristics:

All Debit transactions initiated by the Creditor based on the Revocable Mandate

shall be subject to refund upon Debtor request.

Payment frequency should be defined in the Mandate; the debtor must specify the

payment frequency upon signing the Mandate.

Mandate could be cancelled upon Debtor request from the Debtor Bank

Document: EG-ACH Quick Reference Guide Page No. 6 of 12

02/09/12

Version 1.0

©EBC 2012

Confidential and Proprietary Information to EBC Not to be disclosed without written permission from Egyptian Banks Company for Technological Advancement

How long does it take for a transaction to go through 2.6The Direct Debit Scheme works with a window timing session where the Creditor has the

power to send/receive any transaction and/or reverse/cancel it if he wishes, while the

debtor could easily reject any incoming transactions due to any technical obstructions.

How to Become a Registered Biller 2.7The biller submits a request to his bank in order to become his sponsor bank and if the bank

accepts to sponsor the biller, the bank will assist the biller to fill the registration form and

submit it to EBC then the biller will receive his unique OIN.

How to initiate a Direct Debit Transaction 2.81) Become a registered biller

a) Only a biller could initiate a Direct Debit Transaction through the sponsor bank

(Creditor Bank)

2) Collect Mandates

3) Activate collected mandates through Debtor Bank

4) Initiate Direct Debit Transaction

5) Represent uncollected transaction

Who Could Collect the Mandates? 2.9Mandate processors who were authorized by the biller to collect their customer’s mandates

Document: EG-ACH Quick Reference Guide Page No. 7 of 12

02/09/12

Version 1.0

©EBC 2012

Confidential and Proprietary Information to EBC Not to be disclosed without written permission from Egyptian Banks Company for Technological Advancement

Direct Debit Full Cycle 2.10 The Creditor invites the Payer to pay his bills by using the automated Direct Debit

Scheme.

The Debtor agrees to use the scheme, completes and signs a Direct Debit mandate

form.

Creditor dematerialize the physical Mandate into electronic Mandate on the

Centralized Mandate Portal System.

The Creditor sends the completed physical Direct Debit Mandate to the Debtor

Bank.

The Debtor Bank then records the fact that the Debtor has given permission to the

Creditor to debit his account subject to the terms of the Mandate he has signed and

activate the relevant electronic Mandate

The Creditor starts presenting Direct Debits to the customer’s account

The Debtor Bank debits the Payer’s account (the account nominated in the

mandate), and the Originator’s account is credited

Direct Debits can be presented for payment for as long as the Mandate remains

valid

The Creditors Direct Debit File should contain the following info per collection

(name, bank account, UMR, amount of collection and purpose transaction reason)

Is it Safe? 2.11Yes, the scheme is completely safe and is sponsored and governed by EBC. Customers need

not be concerned about signing a Mandate allowing bills to be paid directly from their

accounts, as the scheme rules guarantee a refund if any incorrect amounts are deducted. In

fact, it is safer paying by direct debit than by cash or checks because of the scheme

guarantee. Originators are bound by the Direct Debit scheme rules, and consequently may

only submit debits to a customer account strictly in accordance with the terms of their

contracts with them.

Seeking Refunds 2.12Payers can at any time question the validity of a direct debit applied to their accounts. If a

customer wishes to make a claim, he should contact his bank and provide them with the

relevant details. He should also complete the Direct Debit claim form, which will be available

at the bank. If it is proven that an error has been made by the Originator or the bank, the

Payer will receive a full and immediate refund under the terms of the Direct Debit scheme

rules.

Document: EG-ACH Quick Reference Guide Page No. 8 of 12

02/09/12

Version 1.0

©EBC 2012

Confidential and Proprietary Information to EBC Not to be disclosed without written permission from Egyptian Banks Company for Technological Advancement

3 Direct Credit

What is a Direct Credit? 3.1 A direct credit is a quick, easy and convenient method of making deposits into a beneficiary's account (e.g. pensions, dividend payments, inward remittance credit, etc…) without having to visit a bank. Direct Credit is used throughout the world as well and is acknowledged as one of the most cost effective and efficient methods of sending funds to a customer's account

Benefits for Senders/Receivers 3.2 Cash Concentration in only one bank

The ability to transfer money throughout the 38 banks of Egypt

No need to wait for a check from your bank or financial/brokerage institution.

No need to wait in line to receive your pension payment.

Fast and convenient and the money moves instantly between accounts.

What Companies Use Direct Credit? 3.3Direct Credits are used by the government, banks, corporates and financial and stock brokerage institutions to deposit pensions, wire transfers, and stock dividends to beneficiaries. It is generally acknowledged by Originators to be the most cost effective and efficient method of bill collection.

Who is involved? 3.4 The Originator: The initiator of the credit payment instruction (Governmental.

Corporate. Financial institution.)

The Originating Bank: Bank of the originator.

The ACH Operator: The ACH Network, i.e. the operator of the ACH network, who

will perform routing, clearing, and dispute resolution. Provider of the inter-bank

clearing of the payment instruction

The Beneficiary Bank: Bank of the receiver

The Beneficiary: The receiver of the credit payment instruction

How the Direct Credit Scheme Works 3.5The originator submits a request to its bank to initiate a Direct Credit transaction to credit

the beneficiary account in any working bank in Egypt. The Banks uses the EG-ACH to send

and receive electronic funds transfer.

Document: EG-ACH Quick Reference Guide Page No. 9 of 12

02/09/12

Version 1.0

©EBC 2012

Confidential and Proprietary Information to EBC Not to be disclosed without written permission from Egyptian Banks Company for Technological Advancement

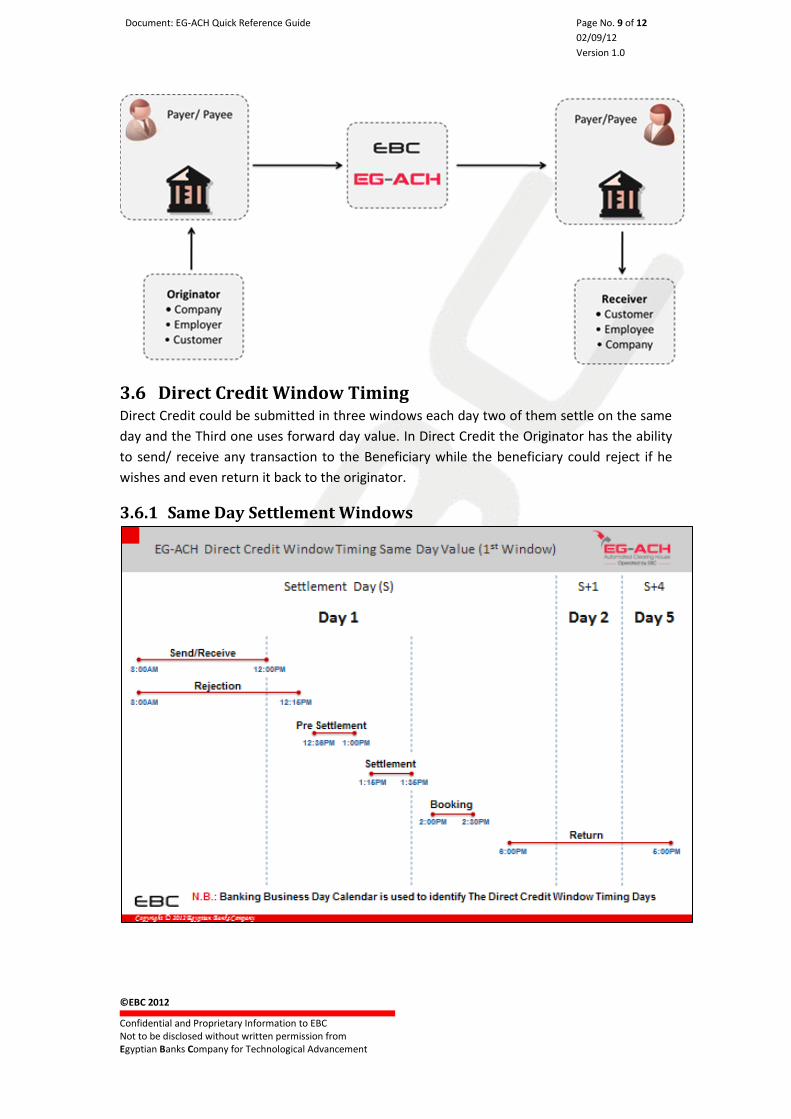

Direct Credit Window Timing 3.6Direct Credit could be submitted in three windows each day two of them settle on the same

day and the Third one uses forward day value. In Direct Credit the Originator has the ability

to send/ receive any transaction to the Beneficiary while the beneficiary could reject if he

wishes and even return it back to the originator.

3.6.1 Same Day Settlement Windows

Document: EG-ACH Quick Reference Guide Page No. 10 of 12

02/09/12

Version 1.0

©EBC 2012

Confidential and Proprietary Information to EBC Not to be disclosed without written permission from Egyptian Banks Company for Technological Advancement

3.6.2 Forward Value Settlement Window

Document: EG-ACH Quick Reference Guide Page No. 11 of 12

02/09/12

Version 1.0

©EBC 2012

Confidential and Proprietary Information to EBC Not to be disclosed without written permission from Egyptian Banks Company for Technological Advancement

Is it safe? 3.7 Direct Credit transactions are very safe as long as the account numbers the money is being deposited into are accurate.