eiuglobal commodity forecast (1)

TRANSCRIPT

Global economics

World commodity forecasts: industrial raw materials

January 2012

Economist Intelligence Unit 26 Red Lion Square London WC1R 4HQ United Kingdom

Economist Intelligence Unit

The Economist Intelligence Unit is a specialist publisher serving companies establishing and managing operations across national borders. For 60 years it has been a source of information on business developments, economic and political trends, government regulations and corporate practice worldwide.

The Economist Intelligence Unit delivers its information in four ways: through its digital portfolio, where the latest analysis is updated daily; through printed subscription products ranging from newsletters to annual reference works; through research reports; and by organising seminars and presentations. The firm is a member of The Economist Group.

London Economist Intelligence Unit 26 Red Lion Square London WC1R 4HQ United Kingdom Tel: (44.20) 7576 8000 Fax: (44.20) 7576 8500 E-mail: [email protected]

New York Economist Intelligence Unit The Economist Group 750 Third Avenue 5th Floor New York, NY 10017, US Tel: (1.212) 554 0600 Fax: (1.212) 586 0248 E-mail: [email protected]

Hong Kong Economist Intelligence Unit 60/F, Central Plaza 18 Harbour Road Wanchai Hong Kong Tel: (852) 2585 3888 Fax: (852) 2802 7638 E-mail: [email protected]

Geneva Economist Intelligence Unit Boulevard des Tranchées 16 1206 Geneva Switzerland Tel: (41) 22 566 2470 Fax: (41) 22 346 93 47 E-mail: [email protected]

This report can be accessed electronically as soon as it is published by visiting store.eiu.com or by contacting a local sales representative.

The whole report may be viewed in PDF format, or can be navigated section-by-section by using the HTML links. In addition, the full archive of previous reports can be accessed in HTML or PDF format, and our search engine can be used to find content of interest quickly. Our automatic alerting service will send a notification via e-mail when new reports become available.

Copyright © 2012 The Economist Intelligence Unit Limited. All rights reserved. Neither this publication nor any part of it may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic, mechanical, by photocopy, recording or otherwise, without the prior permission of The Economist Intelligence Unit Limited.

All information in this report is verified to the best of the author's and the publisher's ability. However, the Economist Intelligence Unit does not accept responsibility for any loss arising from reliance on it.

ISSN 1351-8976

Symbols for tables �0 or 0.0� means nil or negligible; �n/a� means not available; ��� means not applicable

Printed and distributed by IntypeLibra, Units 3/4, Elm Grove Industrial Estate, Wimbledon, SW19 4HE, UK

Contents 1

World commodity forecasts: industrial raw materials January 2012 www.eiu.com © The Economist Intelligence Unit Limited 2012

Contents

2 Economist Intelligence Unit commodity price index

5 Aluminium

13 Coal

22 Copper

31 Cotton

41 Crude oil

49 Gold

57 Lead

63 Natural gas

72 Natural rubber

78 Nickel

84 Steel

90 Tin

97 Wool

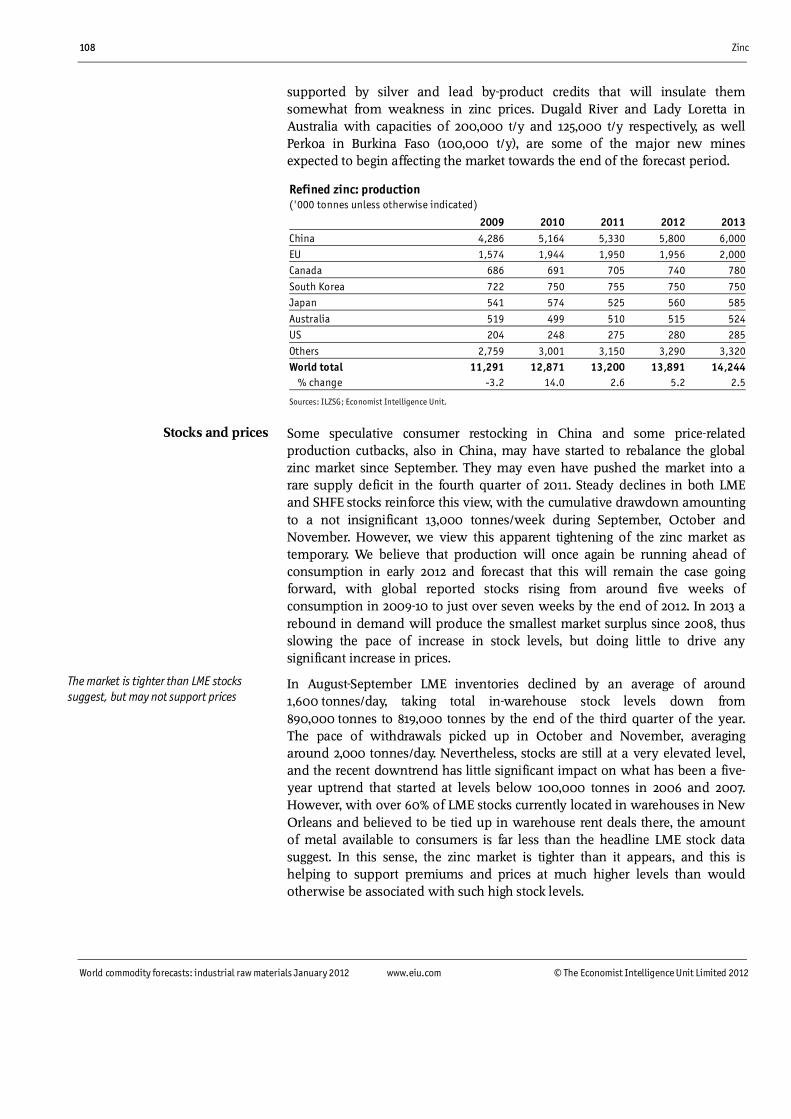

104 Zinc

111 Statistical appendix

Editors: Caroline Bain (editor); Danny Richards (consulting editor)

Editorial closing date: December 13th 2011

All queries: Tel: (44.20) 7576 8000 E-mail: [email protected]

Next report: To request the latest schedule, e-mail [email protected]

2 Economist Intelligence Unit commodity price index

World commodity forecasts: industrial raw materials January 2012 www.eiu.com © The Economist Intelligence Unit Limited 2012

Economist Intelligence Unit commodity price index

The prices of most commodities fell sharply in late September-early October 2011 amid a broader sell-off of more risky financial assets. Prices fell amid increasing concerns about a slowdown in the global economy in 2012 and uncertainty surrounding the eventual outcome of the ongoing sovereign debt crisis in the euro zone. Signs of somewhat slower growth in China, by far the largest single market for base metals, also unsettled commodity markets. Prices of a few commodities�particularly crude oil�regained some ground during October and November, but for the most part industrial raw material prices remained at these lower levels. Towards the end of November and in early December markets started to reflect optimism about the possibility of a comprehensive package of measures to support European sovereigns and the single currency being announced after a "make or break" summit of EU leaders in early December. Early indications are that the measures announced have failed to shore up market confidence, and by mid-December commodity prices were easing back.

Prices will continue to weaken in 2012 owing to slower consumption growth and, depending on the commodity, some improvement on the supply front. However, low global interest rates and a loss of confidence in sovereign creditworthiness, which is encouraging investors to seek return in real assets, will offer support to prices.

Our overall commodity price index rose by 24% in 2010, boosted by a surge in prices of over 45% for industrial raw materials (IRM). Continued investor interest in commodities in an environment of ultra-low interest rates and ample liquidity pushed the IRM index up sharply in the first half of 2011 (by around 42% year on year), but lower prices in the second half of the year are estimated to have pulled the annual average rise in the index down to 23%. This weaker momentum will carry through into 2012, when the WCF index is expected to fall by around 10%, before prices stabilise in 2013.

Gold (which is not included in the IRM index) is perhaps the one metal that is likely to benefit from the prevailing global economic uncertainty. Investor demand�both physical and speculative�is expected to continue to support prices in the short term, as investors seek a "safe haven" in an environment of low interest rates (and negative real interest rates), further quantitative easing (at least in Europe) and concerns about the stability of the global financial system. Central banks, which had been net sellers of gold for decades, turned net buyers in 2010, and this is expected to continue in 2012-13 as part of efforts to diversify reserve asset holdings away from an over-reliance on the US dollar. However, we expect investor interest in gold to start to decline in late 2012 owing to the prospect of some normalisation of monetary conditions moving into 2013 and somewhat stronger global growth, leading to a marked weakening of gold prices.

International demand for metals will be supported to some extent in the coming months by the recovery in manufacturing and by reconstruction work in Japan in the wake of last year's March earthquake and tsunami. However,

Disappointing supply outlooks will support some metals prices

Gold prices will start to slip in late 2012 as global growth prospects improve

Economist Intelligence Unit commodity price index 3

World commodity forecasts: industrial raw materials January 2012 www.eiu.com © The Economist Intelligence Unit Limited 2012

this will be counterbalanced by weak demand in the EU and the US and somewhat slower growth in China's consumption. Following the sharp drop in base metals prices in late September, we now expect the base metal index to rise by only 14% in 2011. Metals prices are expected to remain weak and to fall by 2.6% on an annual average basis in 2012, before starting to recover in 2013 in tandem with stronger economic growth. Even so, supply fundamentals in some base metal markets, particularly tin and copper, suggest that the markets will remain tight. Were consumption growth to surprise on the upside in 2012, then industrial raw material prices would move higher (particularly as copper has a heavy weighting in the IRM index).

We expect China to remain the primary source of demand growth during the forecast period, but in the next two years Chinese consumption growth will ease as a result of government measures to cool the property market, efforts to curb emissions and weaker external demand, which will lead to slower output growth. These negative trends will, however, be partially offset by the return of looser monetary conditions as inflationary pressures subside. In the medium to longer term metals prices will remain volatile, given that mine output can easily be hampered by inclement weather, energy shortages, transport bottlenecks, union activity or a difficult regulatory environment. However, robust growth in the developing world and ongoing urbanisation will limit the annual average drop in industrial raw materials prices in 2012-13 to barely 1%. There is a risk that prices could weaken more markedly if investors were to lose faith in the long-term prospect for commodity prices.

Price forecast summary (US$ index, 1990=100; % change year on year)

Index % 2009 2010 2011 2012 2013 2009 2010 2011 2012 2013WCF 154.0 190.6 242.8 216.3 207.6 -22.3 23.8 27.4 -10.9 -4.0IRM 132.7 192.9 236.9 212.9 215.1 -25.6 45.4 22.8 -10.1 1.0 Base metals 143.4 200.9 229.5 223.7 231.8 -28.5 40.1 14.2 -2.6 3.6 Fibres 86.0 122.3 175.5 128.3 115.8 -11.5 42.2 43.5 -26.9 -9.7 Rubber 209.9 379.9 522.2 427.4 430.8 -25.6 81.0 37.5 -18.2 0.8Crude oil 277.3 357.0 497.6 425.8 437.1 -36.7 28.7 39.4 -14.4 2.6

Note. WCF (World commodity forecasts) is an index of 21 hard and soft commodities. IRM (Industrial raw materials) is a price index of nine hard commodities. The metals sector has a weighting of 65.1% in the IRM index, fibres 27.4% and rubber 7.5%. IRM has

Source: Economist Intelligence Unit.

The price of Brent (dated Blend) dropped sharply in the wake of the broad commodities sell-off in late September, falling from a range of US$110-US$115/barrel in the middle of the month to well below US$105/barrel. Prices subsequently rallied in November, as the publication of a report by the International Atomic Energy Agency (IAEA) sparked renewed concerns about Iran's uranium enrichment programme. However, disappointment following the lacklustre EU summit in early December saw prices slipping back again. Uncertainty surrounding the extent of the global economic slowdown and the risk of a deterioration in the sovereign debt crisis in the euro zone will continue to weigh on the oil market in the first half of 2012.

Oil prices will be supported by non-OECD consumption

4 Economist Intelligence Unit commodity price index

World commodity forecasts: industrial raw materials January 2012 www.eiu.com © The Economist Intelligence Unit Limited 2012

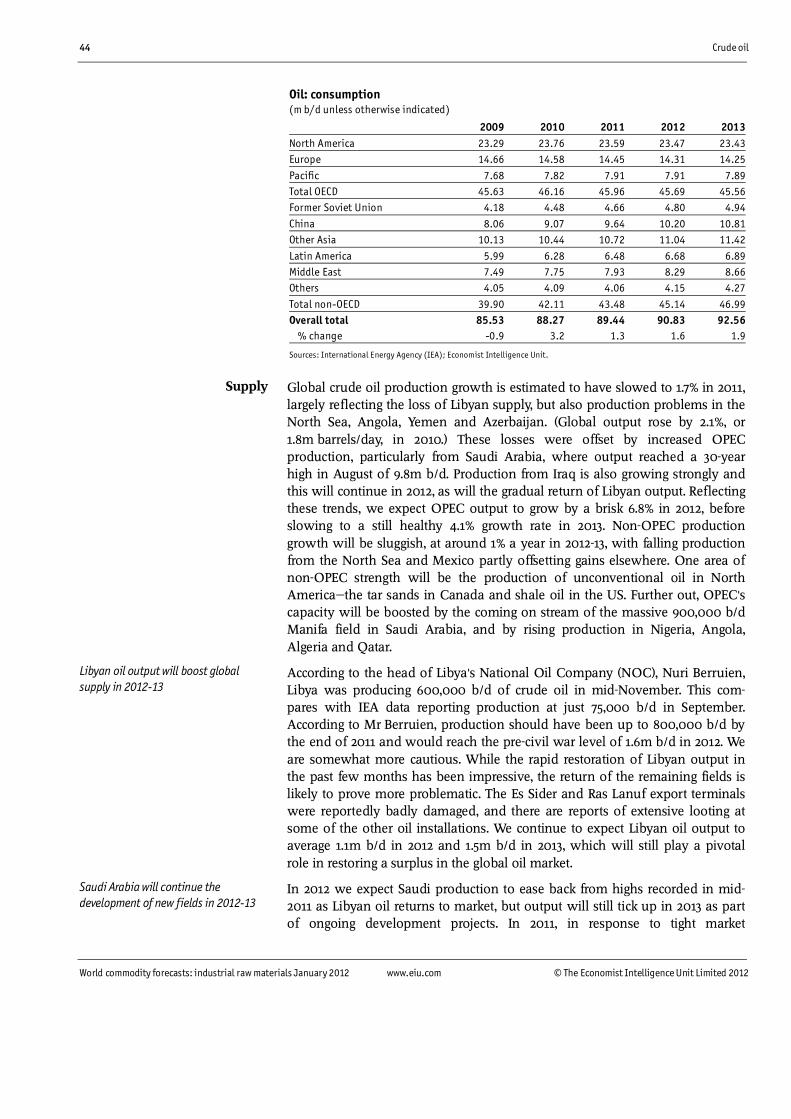

We expect OECD oil consumption to decline steadily throughout the forecast period, reflecting heightened efforts at energy efficiency and conservation, the increased use of biofuels and subdued economic growth. In contrast, the ongoing trends of urbanisation and rising disposable incomes in the developing world, particularly China, will continue to prop up demand, thereby supporting prices. The supply picture, meanwhile, is set to improve, with additional output expected to come on stream in OPEC member states, particularly Iraq, and the gradual resumption of Libyan production.

Given that we now expect a return to a market surplus in 2012 and some building of stocks, we expect oil prices to move lower at an annual average of US$95/barrel. Somewhat stronger economic growth prospects in 2013 will lead to some recovery in prices, but the expected market surplus in that year will prevent a significant increase.

Economist Intelligence Unit commodity price index (1990=100)

2011 2012 2013 2014 1 Qtr 2 Qtr 3 Qtr 4 Qtr 1 Qtr 2 Qtr 3 Qtr 4 Qtr 1 Qtr 2 Qtr 3 Qtr 4 Qtr 1 QtrUS$ index WCF 259.8 255.5 239.0 217.1 219.9 217.6 213.1 214.6 212.7 210.7 204.8 202.1 203.9IRM 264.2 253.6 228.4 201.2 208.7 212.7 212.8 217.6 218.7 220.4 212.9 208.4 210.1 Base metals 247.4 240.7 229.4 200.7 213.2 221.9 224.1 235.5 236.4 238.4 228.8 223.7 227.7 Fibres 214.4 202.9 148.6 136.3 136.6 131.4 127.2 117.8 118.1 120.0 114.7 110.2 107.0 Rubber 589.8 548.8 509.4 440.8 431.0 428.1 425.2 425.2 430.1 429.1 431.0 433.0 431.0Crude oil 470.2 525.0 504.2 490.8 448.3 425.8 412.4 416.9 425.8 434.8 439.3 448.3 448.3

% change, year on year WCF 48.1 49.7 25.6 -3.8 -15.4 -14.8 -10.8 -1.2 -3.3 -3.2 -3.9 -5.8 -4.1IRM 44.6 39.7 24.5 -10.2 -21.0 -16.1 -6.9 8.2 4.8 3.6 0.0 -4.2 -3.9 Base metals 25.5 27.3 19.1 -10.8 -13.8 -7.8 -2.3 17.3 10.9 7.4 2.1 -5.0 -3.7 Fibres 103.2 83.2 29.5 -13.8 -36.3 -35.2 -14.4 -13.6 -13.5 -8.7 -9.9 -6.4 -9.4 Rubber 74.4 46.8 44.2 -3.0 -26.9 -22.0 -16.5 -3.6 -0.2 0.2 1.4 1.8 0.2 Crude oil 36.9 48.9 47.2 26.2 -4.7 -18.9 -18.2 -15.1 -5.0 2.1 6.5 7.5 5.3

Note. WCF (World commodity forecasts) is an index of 21 hard and soft commodities. IRM (Industrial raw materials) is a price index of nine hard commodities. The metals sector has a weighting of 65.1% in the IRM index, fibres 27.4% and rubber 7.5%. IRM has a weighting of 44.4% in the WCF index.

Source: Economist Intelligence Unit.

Economist Intelligence Unit commodity price index(US$ index; 1990=100)

Source: Economist Intelligence Unit.

0

50

100

150

200

250

300

0

100

200

300

400

500

600Oil; right scaleWCF; left scaleIRM; left scale

141312111009080706050403022001

Aluminium 5

World commodity forecasts: industrial raw materials January 2012 www.eiu.com © The Economist Intelligence Unit Limited 2012

Aluminium

The Economist Intelligence Unit estimates global aluminium consumption at 5.2% in 2011, a marked slowdown from 2010, when consumption expanded by 14.1%. Global primary aluminium consumption was up by 6% year on year in January-September 2011, according to the World Bureau of Metal Statistics (WBMS). China's apparent consumption was relatively modest during this nine-month period, rising by 7.8% year on year, partly offsetting the strong perform-ance in the EU (particularly in Germany, where consumption swelled by 11.3%). However, the EU is expected to struggle to maintain this pace in the final quarter, owing to the persistent economic turmoil that continues to undermine business confidence and investment. Despite weak global economic growth in 2012, our forecast of only a moderate slowdown in growth in global aluminium consumption, to 4.4%, is based on the assumption that supply chains, particularly in the automotive sector, will have recovered fully by the early part of the year (having been disrupted by the March 2011 earthquake in Japan and recent heavy flooding in Thailand). Global aluminium consumption growth will improve in 2013, to 4.8%, supported by demand in the developing world underpinned by increasing car ownership in countries such as China and India. Alongside its use in the construction, consumer goods and packaging sectors, the metal's lightweight properties also ensure that it will remain in considerable demand in terms of producing fuel-efficient cars and aircraft.

Consumption in Japan, which accounted for 5.1% of world aluminium con-sumption in 2010, is estimated to have shrunk in 2011 owing to the severe disruptions to the manufacturing supply chain and consumer sentiment as a result of the earthquake and nuclear disaster in March. Although supply chain disruptions appeared to have eased early in the second half of the year, industrial production fell by a revised 3.3% year on year in September and was also 3.3% lower than the previous month, the first monthly decline since March, suggesting that the recovery momentum had slowed. Supply-chain disruptions to the automotive sector stemming from severe floods in Thailand in October-November will have further hampered car production in Japan. Before the floods worsened, Toyota had claimed that its automotive output had returned to normal levels in September, aided by a temporary workforce that helped to make up for the post-earthquake decline in output. However, the Thai floods forced the firm to stop production at three Thai assembly plants (producing parts needed in Japan's manufacturing process) at the beginning of October. Global production for other Japanese carmakers, including Nissan and Mitsubishi Motors, was also affected, but by mid-November most carmakers, with the exception of Honda, had restarted operations. We expect Japan's aluminium consumption to drop by 8% in 2011 as a whole. A combination of base effects and higher demand stemming from the post-quake reconstruction phase will boost aluminium consumption, by 7.5% in 2012. Growth is forecast to slow to 3.5% in 2013 as the effect of the reconstruction-based recovery wanes and higher base effects kick in. However, the effect from the reconstruction effort may be more constrained, given the possibility that large amounts of aluminium scrap from the disaster could be recycled.

Demand

Thai floods dampen aluminium demand in Japan and further afield

6 Aluminium

World commodity forecasts: industrial raw materials January 2012 www.eiu.com © The Economist Intelligence Unit Limited 2012

US automotive production (and aluminium demand) in the fourth quarter of 2011 will also be constrained by disruption to supply chains as some materials are sourced from Thailand. Apparent aluminium consumption growth in the US had already averaged a lacklustre 3.4% in the first nine months of 2011, with this sluggish growth in part reflecting the fact that Japanese carmakers in the US had to cut production owing to the problem of sourcing parts from Japan earlier in the year. Subdued economic growth means that only a marginal improvement is likely in 2012-13�we expect that aluminium consumption will rise by an average of just 1% over the next two years, down from 2.2% in 2011. The risk is also on the downside, given the potential for further disruption in the euro zone to constrain growth in the US, with particularly negative conse-quences for the automotive sector.

Year-on-year growth in apparent consumption in the EU was robust in the first nine months of 2011 (standing at 8.9% year on year), fuelled by continued expansion in Germany's automotive sector. However, consumer and business confidence has been severely damaged by the further deterioration in the outlook for the euro zone, and we have revised down again slightly our estimate of aluminium consumption growth in 2011 to 7%. Our forecast for growth in 2012 stands at 0.5%, with consumption of aluminium constrained by weak regional GDP growth, moribund property markets, fiscal tightening and the end of the restocking cycle. We forecast that aluminium consumption growth will strengthen somewhat in 2013, to 1.5%, but the risk is on the downside given the potential for the sovereign debt crisis to deepen, depressing regional economic growth for longer.

We expect aluminium consumption growth in China, which accounts for around 40% of global demand, to slow to 6.7% in 2011, following an increase of 10.5% in 2010. Apparent consumption growth stood at 7.8% in the first nine months of 2011, in part owing to the high base period and also probably some inventory drawdown. We expect that growth during the final quarter of the year will have been held back by still-tight monetary policy, more restrained investment and relatively weak demand for new cars. Given the weak global economic outlook, which will restrict China's exports of manufactured pro-ducts, we expect aluminium consumption to continue to grow at a rate of around 6% a year in 2012-13. The expansion of the country's high-speed rail infrastructure will support consumption, although there are some doubts about the future of the project following the high-speed train crash in Zheijang province in eastern China in July. However, the current leadership appears determined to keep the economy on track before a leadership transition in 2012.

In Brazil, aluminium consumption rose by an estimated 11.7% in 2011, supported by the government's growth acceleration programme (PAC), which focuses on infrastructure development. Consumption was fuelled further by continued rapid growth in car ownership, the start of a construction boom ahead of the football World Cup in 2014 and the Olympic Games in 2016, and further expansionary fiscal policies (the latest of which was a cut in tax on petrol that was announced in late September). The country is having to rely increasingly on imports to satisfy its growing demand, owing in part to capacity constraints. Although demand for aluminium will be curbed somewhat by the fact that

Consumption growth in Brazil will stay strong, despite slowing GDP growth

EU consumption growth will slow amid economic weakness

China's demand will continue to drive global consumption growth

US demand will remain lacklustre

Aluminium 7

World commodity forecasts: industrial raw materials January 2012 www.eiu.com © The Economist Intelligence Unit Limited 2012

Brazil's economy has begun to slow, the authorities appear intent on easing policy, and the ongoing construction work in preparation for the World Cup and the Olympic Games will provide sufficient support, such that aluminium consumption growth will average more than 15% a year in 2012-13.

Under India's 12th five-year plan, which commences in April 2012, the govern-ment plans to invest heavily in the country's urbanisation and infrastructure development. This should support demand for aluminium during the five years of the plan, although the pace of growth in consumption may be relatively slow in the early part of this period. There will be large-scale investments to tackle energy shortages, which will involve the use of aluminium for power transmission lines, while the government's tax breaks for wind-farm projects and renewable energy sources will boost demand for aluminium for use in the production of wind turbines. According to the latest data from the WBMS, apparent consumption rose by 7.4% year on year in January-September 2011, but reflecting the slowdown in car production growth in recent months, we expect consumption growth of 6.8% for the year as a whole. Although we do not expect car production growth to return to the high of around 30% recorded in 2010, it will be fairly strong in the coming years, and we therefore expect aluminium consumption to expand by around 9% a year in 2012-13.

Primary aluminium: consumption ('000 tonnes unless otherwise indicated)

2009 2010 2011 2012 2013China 14,300 15,805 16,864 17,835 18,836EU 5,100 6,767 7,241 7,302 7,412

US 3,854 4,242 4,340 4,361 4,428Japan 1,523 2,025 1,863 2,003 2,073

India 1,458 1,475 1,575 1,714 1,868South Korea 1,038 1,255 1,306 1,350 1,420

Brazil 799 985 1,100 1,270 1,472Russia 750 685 689 702 741Canada 571 577 585 602 620

Others 5,371 5,846 6,150 6,423 6,792World total 34,764 39,661 41,713 43,562 45,662 % change -5.8 14.1 5.2 4.4 4.8

Sources: World Bureau of Metal Statistics (WBMS); Economist Intelligence Unit.

Global primary aluminium production growth is estimated to slow to 5% in 2011, following an expansion of 11.2% recorded in 2010, when independent Chinese smelters restarted idle capacity and large smelters in the Gulf Co-operation Council (GCC) came on stream. Although slowing, domestic demand growth in China is likely to have encouraged local producers to operate at high levels in 2011, leaving little room for the restart of production at idle smelters in North America or western Europe. High-cost aluminium producers are likely to cut back capacity if aluminium prices remain at their current lows�Aluminium Corp of China has stated that prices are now close to the costs of production. Meanwhile, environmental issues and energy constraints will also act to limit output growth both in China and globally. In the light of these restrictions, alongside the rising cost of bauxite, there will be an increased focus on boosting the use of recycled aluminium in place of refining new metal. Given all these

Supply

India's 12th five-year plan will spur demand for aluminium

8 Aluminium

World commodity forecasts: industrial raw materials January 2012 www.eiu.com © The Economist Intelligence Unit Limited 2012

trends, we forecast that global primary aluminium production will stand at 4.1% a year in 2012-13.

In 2010 China's output expanded by 25.6%, totalling 16.2m tonnes, equivalent to around 40% of global output. Restrictions on electricity usage and high energy costs hampered aluminium production in 2011, so that output growth is estimated at just 7%. Under its five-year plan, the government has committed to lowering energy usage by 16% in 2015 from 2010 levels. The expansion of the industry will also be constrained by regulation over the next few years: the government has instructed local authorities to stop approving the construction of new aluminium smelting capacity, as part of efforts to reduce growth in energy-intensive industries. Furthermore, the government is reportedly plan-ning to reduce export tax rebates for semi-finished aluminium products (the current level of this rebate for some producers is 13%). The appreciation of the renminbi is also eroding the competitiveness of China's aluminium exports.

Nevertheless, new capacity is being built. Alcoa (US) and the China Power Investment Corporation signed a Memorandum of Understanding in January 2011, agreeing to work together on US$7.5bn worth of clean aluminium and energy projects. In July the National Development and Reform Commission (NDRC), China's senior economic planner, also approved a 1m-tonne alumina project based in the north-western Shanxi province. Meanwhile, the Baiyun district intends to increase its aluminium capacity to 450,000 tonnes/year (t/y) during the 12th five-year plan. On balance, however, we forecast that pro-duction growth will slow to an annual average of 3.2% in 2012-13. (Data from China�s National Bureau of Statistics show that aluminium output was only up by 0.3% year on year in October.) Limited supplies of raw materials could also hamper output growth in the medium term, as reportedly Indonesia's government may limit exports for bauxite from 2014�Indonesia accounts for 80% of China's bauxite imports. Nevertheless, Chinalco's planned increase in bauxite production, alongside further mineral discoveries, are expected to ensure that China's domestic bauxite production should maintain a respectable rate of growth over the next two years.

In India, aluminium production growth is estimated to slow to 6.3% in 2011, from 8.9% in 2010, as environmental concerns remaining an obstacle to some of India's aluminium producers. However, as companies gear up to meet the expected increase in domestic demand, plans for new projects continue to be put forward. We therefore expect output growth to average 7.1% a year in 2012-13. Hindalco (India) has stated that it is commissioning a series of projects to boost aluminium smelting capacity to 1.8m t/y from 600,000 t/y currently, but has said that it is struggling to commission projects because of uncertainty regarding the country's regulatory environment. India's National Aluminium Company Limited (Nalco) still plans to build a 500,000-t/y aluminium smelter in Orissa, despite being refused approval for setting up the project in Jharsuguda on environmental grounds, with the company looking into alternative sites. However, it has not ruled out the possibility of locating the smelter outside Orissa.

The issue of energy conservation and efficiency continues to gain importance globally, not only in response to environmental concerns, but also because of

China's output will be constrained by shortages of energy and raw materials

India will increase supply to meet expanding demand

EC plans to increase emphasis on environmental impact of production

Aluminium 9

World commodity forecasts: industrial raw materials January 2012 www.eiu.com © The Economist Intelligence Unit Limited 2012

the high cost of energy and energy shortages in some countries. Conversely, although aluminium boasts environmentally friendly features because of its lightweight properties for cars, the production of the metal is hugely energy-intensive, accounting for around 50% of the aluminium industry's production costs. In September the European Commission (EC) launched its roadmap for a resource-efficient Europe, and this will result in a reassessment of the environmental impact of aluminium production. There have been calls for the assessment to consider not only the environmental damage from the production of a material, but also the environmental benefits stemming from the use of that material, including not only its use but also its capabilities for recycling. The EC's roadmap also calls for increased investment in recycling. Given that prevailing high energy prices are behind shutdowns and the holding back of new primary aluminium projects, it is unsurprising that the market for recycled aluminium is already gaining ground.

Production of aluminium in Latin America is estimated to remain weak in 2011, dropping by 3.5% (mainly owing to a sluggish performance in Brazil), following a contraction of 8.1% in 2010. We expect output to rise in 2012-13, by 1.7% a year, owing to a low base of comparison and continued economic growth in the region that encourages investment, but the risk to our forecast is on the downside. Brazil accounts for around 60% of production in the region, but the country has not increased capacity since 1985, and production capacity has now fallen to 1.5m t/y. Brazil's primary aluminium production was 1.07m tonnes in the first nine months of 2011, a decline of 7.1% year on year, according to the WBMS. Reportedly, aluminium companies want the government to abol-ish import duties because of the tight supply conditions in the domestic market. Although it has depreciated recently, the relatively strong Real makes importing aluminium more favourable, while hurting exporters. Nevertheless, a Norweg-ian firm, Norsk Hydro, has boosted its capacity in Brazil, increasing output at the Alunorte refinery, the world's largest refinery, to 6.3m tonnes this year.

Elsewhere in Latin America, Venezuelan output is being held back by insufficient investment in capacity, and the country has had to import large amounts of the metal. The building of the Serlaca aluminium rolling plant in Venezuela, which began in 2008, has come to a halt; the plant had been scheduled to start operations in 2013. Reportedly, this was because of financial issues.

Data from the WBMS suggest that Russia's aluminium output rose by only 1.2% year on year in January-September 2011. However, Rusal is reportedly making progress on projects for new smelters and modernisation of existing plants�the 600,000-t/y smelter at the Boguchanskoya energy and metals complex on the Angara river is expected to start producing aluminium by the end of the first quarter of 2013. Rusal also recently received loan approval to finance the construction of its 750,000-t/y Taishet smelter near Irkutsk in September; it aims to commence operations in 2013.

Nevertheless, in line with this apparent weak performance, and also reflecting the recent announcement by Rusal that it had cut its planned output increase to 1% for 2011 as a whole (from 2% previously), we estimate that supply increased by a mere 0.8% in 2011. However, we forecast that Russia's output will grow by

Capacity constrains could limit growth in production in Brazil

Output in Russia is expected to rise as new capacity comes on stream

10 Aluminium

World commodity forecasts: industrial raw materials January 2012 www.eiu.com © The Economist Intelligence Unit Limited 2012

just under 4% a year in 2012-13, as increased capital expenditure improves existing plants and new projects.

Production in the Middle East remains strong, and there are plans for major capacity expansion. Production capacity in the Gulf region was not directly affected by the unrest in parts of the Middle East and North Africa, and we expect output growth in the region to reach 8.2% in 2011, to around 3.5m tonnes, driven by rapid growth in Qatar. We forecast that aluminium production growth will rise in the next two years, with output reaching 4.1m tonnes in 2013 as new capacity comes on stream. Plans for new plants in the region continue to make progress. Although the Qatalum project in Qatar has faced delays, production capacity has reached 585,000 t/y (the target for the first phase of development), according to reports published at the end of September. Emal-Emirates Aluminium in Abu Dhabi (Dubai Aluminium and Mubadala Group) has completed its first phase of development, with a capacity of 750,000 tonnes, which will rise to close to 1.5m t/y on completion of the second phase, which is scheduled for end-2014. Financing for the second phase of the development has now been secured. Similarly, Ma'aden Bauxite and Alumina Company (a joint venture between Ma'aden and Alcoa) has signed funding contracts for the second phase of their joint-venture project in Saudi Arabia. The first phase, comprising an aluminium smelter (with a capacity of 740,000 t/y) and rolling mill, will begin operating in 2013, and the second, comprising a mine and refinery (with a capacity of 1.8m t/y), will come on stream in 2014.

We estimate strong growth in US production in 2011, following a year of flat growth in 2010 and a contraction of 35% in 2009. Growth will remain positive in 2012-13, with new capacity coming on stream. For example, Noranda Aluminium Holding has announced plans to expand production at its 263,000-t/y New Madrid plant by 6% in 2013. Canadian production fell by 2.2% in 2010, but output is expected to grow by 1.8% in 2011 and to expand by an annual average of over 5% in 2012-13, as more capacity comes on stream. Rio Tinto has invested more than US$1bn to expand and modernise its operations in Saquenay-Lac-Saint-Jean Quebec and its Kitimat smelter in British Colombia.

Primary aluminium: production ('000 tonnes unless otherwise indicated)

2009 2010 2011 2012 2013China 12,891 16,194 17,328 17,900 18,450

Russia 3,815 3,947 3,979 4,129 4,287Canada 3,030 2,963 3,017 3,205 3,349Middle East 2,745 3,188 3,449 3,750 4,100

EU 2,399 2,654 2,712 2,739 2,835Latin America 2,510 2,307 2,226 2,253 2,300

Australasia 2,214 2,272 2,317 2,401 2,461US 1,727 1,727 1,921 1,980 2,080Africa 1,690 1,742 1,822 1,910 2,005

India 1,479 1,610 1,711 1,823 1,965Others 2,699 2,766 2,940 3,050 3,177

World total 37,198 41,371 43,423 45,139 47,009 % change -6.2 11.2 5.0 4.0 4.1

Sources: WBMS; International Aluminium Institute (IAI); Economist Intelligence Unit.

North American production is expected to continue to grow

Growth in output in the Middle East will be rapid

Aluminium 11

World commodity forecasts: industrial raw materials January 2012 www.eiu.com © The Economist Intelligence Unit Limited 2012

Stocks of aluminium at the London Metal Exchange (LME) and the International Aluminium Institute (IAI) picked up in the first quarter of 2011, reaching nearly 6.2m tonnes at the end of March. Stocks then dipped to 6m tonnes at the end of June, edged up to 6.1m tonnes by end-August before dipping again to just under 6m tonnes by end-September. Excess stocks still weigh on the market. Indeed, we expect stocks to rise in 2012-13, albeit at a slower pace towards the latter part of the forecast period, as the market will be in oversupply. It is possible that stocks could be released if investors expect aluminium prices to fall or if rising interest rates increase the costs of financing the stocks, but there have been significant delays in accessing stocks owing to the concentration of holdings in LME-registered warehouses in Detroit. Although the market surplus is set to shrink over the next two years, the stock picture will remain healthy, with total reported market stocks providing more than 50 days' consumption. However, the market appears tighter than the stock picture suggests, owing to the fact that access to these warehoused stocks remains difficult.

Primary aluminium: supply and demand ('000 tonnes unless otherwise indicated)

2009 2010 2011 2012 2013Global production 37,198 41,371 43,423 45,139 47,009

Global consumption 34,764 39,661 41,713 43,562 45,662Balance 2,434 1,710 1,711 1,578 1,347Total reported market stocks 5,833 5,669 6,280 6,700 6,750Days' consumption 61 52 55 56 54

Sources: WBMS; Economist Intelligence Unit.

Prices for aluminium have remained on a general downward trend since May 2011. During the heavy sell-off in late September aluminium prices dropped below US$2,200/tonne for the first time in 12 months, and in October they averaged US$2,171/tonne before slipping below the US$2,000/tonne level in late November. The recent selling activity was a reflection of deepening fears of a slowdown in the US economy as well as uncertainty about the fate of the euro zone and the increasing fragility of economic growth within the region. Amid the current economic environment, aluminium prices are being influenced less by the traditional supply and demand factors than by investor sentiment.

Meanwhile, the delays at LME warehouses have created concerns about metal availability, which, coupled with uncertainties about the market environment and prices, have been deterring investors from purchasing forward contracts. We expect prices to average US$2,420/tonne in 2011, and we forecast that they will fall in 2012 to US$2,300/tonne in response to the gloomy economic outlook and easing energy prices. Certainly, the market for the metal is tight and prices have already dropped to what is deemed to be a breakeven point for many producers, which could prevent a sharper downturn in prices. In 2013 prices will edge upwards, reflecting an improvement in global demand and higher production costs, both in terms of energy and for raw materials (with bauxite being in tight supply).

Stocks and prices

Prices will hold up relatively well, despite market surpluses

12 Aluminium

World commodity forecasts: industrial raw materials January 2012 www.eiu.com © The Economist Intelligence Unit Limited 2012

Primary aluminium: stocks and prices 2010 2011 2012 2013 2014Stocksa 1 Qtr 5,769 6,142 6,350 6,740 6,6502 Qtr 5,612 5,960 6,489 6,800 -3 Qtr 5,641 5,978 6,648 6,720 -4 Qtr 5,669 6,280 6,700 6,750 - % change -2.8 10.8 6.7 0.7 -

Pricesb 1 Qtr 2,163 2,500 2,250 2,400 2,4002 Qtr 2,096 2,603 2,300 2,400 -3 Qtr 2,089 2,400 2,225 2,350 -4 Qtr 2,343 2,178 2,425 2,370 -Year 2,173 2,420 2,300 2,380 - % change 30.5 11.4 -5.0 3.5 -

a Total reported producer and LME stocks, end-period; '000 tonnes rounded. b LME cash price, US$/tonne.

Sources: London Metal Exchange (LME); Economist Intelligence Unit.

Primary aluminium: stocks and prices

Sources: London Metal Exchange; Economist Intelligence Unit.

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Prices (US$/tonne); right scaleStocks ('000 tonnes); left scale

141312111009080706052004

Coal 13

World commodity forecasts: industrial raw materials January 2012 www.eiu.com © The Economist Intelligence Unit Limited 2012

Coal

Growth in global demand for coal is forecast to average 4.3% per year in 2012-13, down from an estimated 5.4% in 2011. Demand growth will ease in 2012 as the global economy slows, before picking up moderately in 2013. The Economist Intelligence Unit currently does not expect a sharper slowdown because, to date, the worsened outlook for the EU and the US has not had a substantial impact on our forecasts for China and India. Nevertheless, these economies are expected to slow, and the ongoing crisis in the euro zone means that risks are to the downside. China will continue to provide by far the largest spur to coal demand during the period (although efforts to curtail emissions are likely to have some impact). India will be another important driver of demand, as it continues to pursue its rural electrification plans. Demand in the EU is forecast to ease in 2012, owing to a sharp deterioration in economic performance in the euro zone. US consumption is also forecast to decline in 2012, owing to the increasing use of natural gas in electricity generation and as the economy slows in that year.

Developments in China, which accounted for around 46% of global coal consumption in 2010, will remain central to global coal demand in 2012-13. China relies on coal for more than 80% of its power generation. The country became a net importer of thermal coal in 2007, and the world�s second-largest importer (after Japan) in 2010, when it imported 90m tonnes of thermal coal. Consumption growth is estimated at 8% in 2011, as the Chinese economy continued to expand rapidly.

There are already signs of a slowing of economic activity in China. However, a recent decline in inflation has boosted expectations that the government will raise electricity tariffs to help the country�s power plants. These are struggling with very high coal prices, threatening renewed power shortages, and face a tightening of emission standards in January 2012. Higher electricity tariffs would support demand for coal, especially imports. Despite rapid growth in recent months, thermal coal imports were down by 12.7% year on year in January-October 2011, to 38m tonnes, partly owing to a steep fall in early 2011 on the back of high international prices.

We continue to expect a moderate easing of coal demand growth in 2012-13, in line with a cooling of the wider economy. Efforts to curtail emissions may also constrain coal consumption, but ongoing expansion in coal-fired power-generating capacity will mean that growth will still notch up an annual average rate of 6.3% in 2012-13.

In the US, coal consumption bounced back by 5% in 2010, after a sharp 11% fall in 2009. However, unfavourable base effects, only slight growth in electricity generation owing to subdued economic growth, and increased electricity gener-ation from natural gas, hydropower and other renewables mean that coal con-sumption is estimated to decline by 1.5% in 2011. The presence of relatively cheap, readily available and "cleaner" natural gas is leading to a shift away from coal-fired power generation, while coal consumption is likely to be constrained by efforts to curtail carbon emissions. With US economic growth forecast to slow sharply

Demand

Chinese coal demand growth will ease in tandem with economic growth

US consumption will decline

14 Coal

World commodity forecasts: industrial raw materials January 2012 www.eiu.com © The Economist Intelligence Unit Limited 2012

again in 2012, we expect electricity demand to be lower, and for coal consumption to decline by 3.5% in that year, followed by a stabilisation in 2013, as economic growth picks up and gas prices rise.

Data from the EU's statistical body, Eurostat, show that growth in coal con-sumption in the EU picked up sharply to 8.1% year in January-May 2011. Coal demand is expected to be boosted in 2011 by sharply higher gas prices.

Much of the growth in coal consumption is accounted for by Poland, the EU's second-largest coal consumer. Polish coal consumption rose by 15.5% year on year in January-June 2011. Surprisingly, Poland avoided a contraction in economic output during the global crisis in 2008-09, and has been one of the EU�s fastest-growing economies since then.

Consumption is also growing (albeit much more modestly) in Germany, the EU's largest consumer of coal�by 1.3% year on year in January-June 2011. Economic growth remained relatively strong in Germany in 2011. Moreover, despite Germany�s environmental credentials, its decision, in the wake of the Japanese nuclear crisis, to close eight of its 17 nuclear power stations (the remaining plants are to be closed by 2022) is likely to provide some support to coal consumption.

We expect growth in EU coal consumption to ease in the second half of 2011, in line with a slowdown in the EU economy. Nevertheless, growth is likely to have been relatively strong for the year as a whole, at a revised 5%. Economic performance in both Poland and Germany, as in the wider EU, is forecast to worsen considerably in 2012, when real GDP in the EU as a whole is forecast to contract slightly. We therefore expect coal demand to slip in 2012, before posting limited growth in 2013 as the European economy picks up. The subdued demand outlook will be further constrained by concerns about carbon emis-sions, with some countries turning to gas or renewables for new power-generation capacity.

Coal consumption in the robust Indian economy has grown rapidly in recent years, averaging 8.5% per year in 2006-10 according to Energy Information Administration (EIA) data, including growth of 10.8% in 2010. With a relatively closed economy, India should be fairly well protected from the global downturn. Coal consumption is therefore expected to continue to rise strongly, boosted by the long-term plan to raise thermal power-generation capacity in an effort to increase access to electricity in rural areas. In its five-year plan for the period 2012-17, the Indian government envisages that the rate of annual demand growth could stay at around 8%.

Problems with accessing sufficient domestic coal supplies to meet demand are likely to remain the main constraint on consumption; in October 2011 there were power outages (blamed on a shortage of coal) in a number of states and in the capital, New Delhi, leading to public protests in some areas. The Ministry of Coal estimates that there will be a production shortfall of 142m tonnes in fiscal year 2011/12 (April-March), and the country�s Planning Commission has cautioned that the gap could rise to as much as 200m tonnes by 2016/17. Coal imports have risen strongly�they were up by 51% year on year in April-October 2011�and private Indian companies and Coal India, the state-owned

The demand profile in the EU is weak

Indian consumption should be relatively protected from global woes

Coal 15

World commodity forecasts: industrial raw materials January 2012 www.eiu.com © The Economist Intelligence Unit Limited 2012

coal producer, are increasingly interested in acquiring coal assets overseas to fill the domestic supply gap. However, there is a technical limit to the share of imported coal that can be used by domestic power-plant boilers. Moreover, the failure of domestic electricity tariffs to keep pace with the high cost of imports is now reported to be limiting demand for the latter.

In Japan, coal consumption grew by 14% in 2010, as the wider economy bounced back from recession. The Japanese economy is expected to post a small contraction in 2011, owing to the devastating earthquake and tsunami in March, which also damaged several thermal power stations. Coal consumption is therefore estimated to decline in 2011. However, with these plants now coming back into operation, coal demand is likely to be boosted in the medium term by the impact of the nuclear crisis.

The contribution of nuclear power to electricity generation is now expected to fall over the next ten years, owing to public safety concerns. Partly for energy security reasons, coal is viewed as an important alternative to oil for electricity generation, and will continue to account for a substantial share of Japan's total energy supply well into the future, despite concerns about its damaging environmental impact. In a sign of renewed interest in coal, in June Japan's Itochu trading house agreed to pay US$1.5bn for a 20% stake in a new Colombian mining partnership with Drummond (US). After jumping in 2011, the share of coal in total electricity generation is forecast to remain significantly higher in 2012-13 than before the nuclear crisis. A bounce-back in Japanese economic activity in 2012 following the slowdown in 2011 should also support energy demand.

Elsewhere in Asia, which is expected to remain the fastest-growing of the main global regions in 2012-13, coal-fired generation features as a key element of economic development plans, despite the associated environmental concerns. This is the case, for example, in Indonesia, which is in the process of imple-menting an intensive programme of coal-fired power plant construction, as part of plans to electrify rural areas. PLN, the state electricity supplier, projects that its coal consumption could rise to 95m tonnes in 2015, up from 41m tonnes in 2010. In Vietnam, the state-run PetroVietnam has plans for five new coal-fired plants to become operational by 2015 and to build 90 by 2025, leading to a sharp rise in coal consumption, including imports. Even South Korea�the world�s third-largest importer of coal�is finding it a challenge to implement its "green growth" policy announced in 2008, and is likely to remain heavily reliant on coal-fuelled power stations.

Australian coal consumption is expected to grow in 2012-13, with the carbon tax due to be introduced in July 2012 unlikely to have a major impact over the forecast period. The tax will be introduced at A$23/tonne (around US$25/tonne), and will apply to 500 businesses with the highest emission levels, including power stations and coal mines. It will rise by 2.5% per year until it is replaced in 2015 by an emissions trading scheme. One of the aims of the new system is to encourage a switch in power generation away from coal towards natural gas and renewables.

Australian carbon tax will have a limited impact

Japanese demand for coal to benefit from nuclear troubles

Indonesia and Vietnam see coal as the way forward

16 Coal

World commodity forecasts: industrial raw materials January 2012 www.eiu.com © The Economist Intelligence Unit Limited 2012

Coal: consumption (m tonnes unless otherwise indicated)

2009 2010 2011 2012 2013China 3,152 3,387 3,658 3,896 4,130US 905 951 937 904 904

EU 719 718 754 746 750India 622 689 748 810 875Russia 202 206 209 213 219

Japan 165 188 186 193 198South Africa 181 183 188 193 199

Australia 136 109 111 113 116Turkey 93 100 105 109 114South Korea 103 114 121 128 136

World total 6,874 7,289 7,681 7,995 8,355 % change 3.2 6.0 5.4 4.1 4.5

Sources: Energy Information Administration (EIA); Economist Intelligence Unit.

Global coal production is estimated to have rebounded strongly in 2010, growing by 6.2%, as high prevailing prices and a recovery in consumption encouraged the growth in supply. China and Indonesia led the way in output growth in 2010, with increases of 9% and 19% respectively. We expect global output growth to remain at around this rate in 2011, despite a continued dis-appointing performance in India and some disruptions to supply in other key producers, owing to continued rapid growth in Chinese output. Production growth is forecast to ease to an annual average of 4.5% in 2012-13, in line with slower demand growth.

China has hiked coal output in recent years�by an average of 9% per year in 2007-10�although this has not been enough to keep pace with growing domestic demand. Output continued to grow robustly in 2011: coal production increased by 12.2% year on year in January-October 2011, according to the China Coal Transportation and Distribution Association, including 7.3% year-on-year growth in October.

A considerable amount of new capacity is expected to come on stream by the end of the forecast period, which should partly offset the loss of output from mines considered dangerous or environmentally damaging. There are ongoing efforts to improve safety standards, particularly at smaller mines (which account for around 30% of production). The process of mergers and acquisitions in the coal mining industry should lead to a marked reduction in the number of mines in China, but efficiency gains will support output growth. In 2010 China shut down 2,173 mines with a total capacity of 231m tonnes/year, and the 12th five-year plan for the coal industry, which is expected to be released soon, targets further consolidation of the mining sector in 2011-15.

The government is showing some signs of seeking to constrain coal output. This is partly owing to concerns that reserves are being used up too quickly, but also to environmental considerations. The country's 2011-15 five-year plan for the first time sets climate change targets and envisages a decline in coal's share in energy consumption. However, this will still see the addition of an extra 260 gw in coal-fired power generation (albeit with part of this being to help

Supply

Solid domestic demand will support China's output growth

Coal 17

World commodity forecasts: industrial raw materials January 2012 www.eiu.com © The Economist Intelligence Unit Limited 2012

compensate for the closure of older facilities, which will be replaced with lower-emission plants). Other factors could also limit supply, including safety concerns, depleting mines, particularly in eastern China, and infrastructure constraints, although plans are in place to improve rail and port transport in the coming years. On the whole, given the requirements of the still rapidly developing economy, China's production is expected to grow at a steady pace in 2012-13, albeit at a somewhat slower rate than in recent years as demand growth eases.

US production grew by just 1% in 2010, following a drop of around 8% in 2009, according to the EIA. We expect output to decline in 2011 as domestic con-sumption eases, partly because of the availability of cheap and plentiful natural gas. Even though US coal exports rose sharply in 2011, coal production fell by 0.1% year on year in January-October, according to EIA data. Such factors are expected to continue to constrain output in 2012-13. Given our forecast of slower US growth in 2012, we expect production to ease again in that year.

After growing rapidly in 2005-09, by an annual average of 6.5% according to EIA data, growth in coal production in India slowed sharply to 2.5% in 2010. According to the Indian authorities, output was down by 2.5% year on year in the first five months of the current fiscal year (April-August), and performance is estimated to have weakened further in September-October. State-owned Coal India (the largest coal producer in the world, accounting for over 85% of total Indian output) has blamed the production shortfall since 2009 mainly on delays in obtaining environmental clearances for more than 150 projects. In 2011 output was also hit by heavy rains and industrial action in October.

India has ambitious coal output targets in its five-year plan covering the period 2012-17, which foresees output rising by 7% annually to 770m tonnes by 2017 (although even this growth would see a rising import requirement). The govern-ment is finally moving on overcoming the regulatory obstacles to greater coal production. On the assumption that substantial progress on this is nevertheless likely to take time, we forecast only a moderate pick-up in annual production growth during our forecast period, to 5% by 2013.

In the early part of 2011 Australia's production was disrupted by severe flood-ing in Queensland, with the mines only slowly coming back into production over the course of the year. Growth in Australian production should pick up in 2012-13, assuming no further weather-related disruptions to supply. Output will be supported by the opening of new mines in New South Wales and Queensland. Progress is also being made in addressing infrastructure shortcomings with, for example, work on boosting coal export capacity at the Port of Newcastle in New South Wales making good progress. The country's carbon tax, which is due to come into effect in July 2012, has caused a great deal of controversy and given rise to dire warnings of the impact on the coal industry, but government projections envisage coal production more than doubling by 2050.

Ramped up Indonesian coal production has accounted for much of the growth in global coal supplies in recent years, encouraged by burgeoning demand from China and especially India, which is expected to supplant Japan in 2011 as

US production is forecast to fall

Australian production will benefit from new mine openings

Indonesian growth to continue despite unfavourable government policy

India's output is expected to continue to underperform

18 Coal

World commodity forecasts: industrial raw materials January 2012 www.eiu.com © The Economist Intelligence Unit Limited 2012

Indonesia's largest coal market. However, there is persistent uncertainty about the operating environment, particularly as the government is seeking to guarantee domestic supply to meet the country's growing power needs. The possible introduction in 2014 of a ban on exports of coal with an energy value of below 5,100 kilocalories/kg has emerged as a key concern for domestic producers. The government has also suggested that it might introduce a moratorium on new mining permits, in order to settle existing disputes over permits. These uncertainties, together with a growing environmental lobby and concern about deforestation, have clouded the investment environment at a time of rising domestic and external demand.

Nevertheless, although production was down by around 1% year on year in the first quarter of 2011 as a result of wet weather, the Indonesian association of coal miners, APBI, expects output to grow by up to 14% in 2011. Given expect-ations of robust domestic and external demand, output is forecast to grow by an average of 6% per year in 2012-13.

Output in Russia was hit hard by a serious accident in May 2010, which closed main coal mine belonging to Raspadskaya, the country's largest underground mine and coking coal producer. Output has been growing in year-on-year terms since April 2011 and has accelerated since then, supported by base effects. Output was up by 3.2% year on year in January-October 2011, including 10.5% year-on-year growth in October.

Russian output growth is expected to continue to recover in 2012-13, posting annual average growth of over 4% during the period, as Raspadskaya restores output. Russian coal output will also be supported in the coming years by external demand. Russia's long-term coal development plans envisage a diversification away from traditional Western export markets towards the fast-growing Asia-Pacific region. China is set to become an increasingly important export market.

Increased domestic consumption and a strategic shift away from gas towards coal in thermal power plants should also support coal output. The govern-ment's energy strategy to 2030 envisages substituting coal for gas in thermal power stations, raising coal's share in electricity generation to 34-36% by 2030 from 26% in 2008. Kemerovo region in western Siberia, which accounts for more than one-half of the country's total output, has announced investment plans totalling US$28bn in 2011-25, with 22 new coal mines to be launched, helping to raise the region's output by 41% by the end of the period, from 186m tonnes in 2010.

South Africa has seen only sluggish growth in coal output for a number of years. Coal production is reported to have grown by just 1.3% in 2010. The industry is facing a myriad of problems that will continue to constrain output. South Africa's state-owned Eskom�the largest electricity producer in Africa�has complained that a lack of new coal mine development in the country during the last several years has put pressure on its coal supplies. The rail network is also proving inadequate, having suffered years of underinvestment. Plans to increase the capacity of Transnet, the state-owned railroad operator, to

Russian output will continue to recover

South Africa's coal industry will disappoint amid myriad constraints

Coal 19

World commodity forecasts: industrial raw materials January 2012 www.eiu.com © The Economist Intelligence Unit Limited 2012

81m tonnes of coal for export by 2015, from 62m tonnes in fiscal year 2010/11 (April-March), look ambitious.

According to the latest data from Statistics South Africa, coal output was 0.2% lower year on year in January-September 2011, partly owing to strike action in July. We forecast annual average growth of just 1.3% in 2012-13.

In the EU, latest Eurostat data show coal production rebounding in 2011 after falling by 5.1% in 2009 and a further 1.7% in 2010. Output across the EU was up by 6.2% year on year in January-May 2011. Output in Germany, the EU�s largest coal producer, was up by 1.1% year on year in January-June. Growth was higher in Poland (the bloc�s second-largest producer), at 4.9% year on year in January-June. EU-wide output growth was driven higher by rapid (in some cases double-digit) year-on-year growth in Bulgaria, Romania, Greece, the Czech Republic and the UK. EU output growth is forecast to ease in 2012-13 on the back of weaker demand.

Coal output in Colombia�the world�s fourth-largest coal exporter�bounced back in the third quarter of 2011 after rains and flooding earlier in the year, and was up by 11% year on year in January-September, according to Ingeominas, the mining regulator. With rising Asian demand and the expansion of the Panama Canal opening up Asian markets to Colombian exports, companies investing in Colombia have ambitious output targets. Colombia's largest coal mine, Cerrejon, which is owned by BHP Billiton, Xstrata and Anglo American, aims to boost annual capacity from 32m tonnes to 40m tonnes in the short term, and eventually to 60m tonnes. Prodeco, the Colombian coal operation of Swiss-based Glencore International, plans to double annual output to 20.7m tonnes by 2015, while Drummond (US) plans to raise annual output to 35m tonnes in 2014, from 25m currently.

Coal: production (mine output; m tonnes unless otherwise indicated)

2009 2010 2011 2012 2012China 3,050 3,321 3,687 3,945 4,201

US 975 985 980 950 955India 555 569 557 574 603

Australia 399 407 415 432 447Russia 297 311 322 335 350Indonesia 302 359 398 426 447

South Africa 247 251 251 254 257Germany 185 184 185 186 186

Kazakhstan 102 111 115 119 124Colombia 73 75 82 86 91

World total 6,967 7,401 7,861 8,207 8,586 % change 2.3 6.2 6.2 4.4 4.6

Sources: EIA; Economist Intelligence Unit.

A strong rebound in production will have been more than adequate to meet the increase in demand in 2010. As a result, the market surplus is estimated to have risen to 112m tonnes, with a further rise to 180m tonnes in 2011 owing to continued strong output growth. Steady growth in production should enable the market to remain in surplus throughout 2012-13.

Stocks and prices

Leading producers in Colombia have ambitious output targets

The outlook for the EU is weaker owing to the poor economic forecast

20 Coal

World commodity forecasts: industrial raw materials January 2012 www.eiu.com © The Economist Intelligence Unit Limited 2012

Coal: supply and demand (m tonnes)

2009 2010 2011 2012 2013Production 6,967 7,401 7,861 8,207 8,586Consumption 6,874 7,289 7,681 7,995 8,355

Balance 93 112 180 211 231

Sources: EIA; Economist Intelligence Unit.

Thermal coal prices rose sharply in the first quarter of 2011, to an average of US$129/tonne (their highest level since the third quarter of 2008), owing to concerns about supply from Australia following severe flooding in Queensland and sustained strength in consumption. The early and severe start to winter in the northern hemisphere offered further support to prices, as did the prospect of reduced nuclear power in Japan and a switch to coal-fired electricity. Prices eased somewhat in the second quarter, to US$120/tonne, as coal participated in the sell-off in commodities in May. Despite the deteriorating global economic picture and falls in other commodity prices, coal prices held up, averaging US$120.6/tonne in the third quarter of 2011. However, prices have been gradually easing since early October, reaching around US$113/tonne in mid-November. Prices are expected to remain supported against any steep fall in the remainder of 2011 by still-robust consumption growth and the high price of alternative fuels�crude oil and liquefied natural gas (LNG) in the Pacific region. With signs already emerging that global economic growth is rapidly losing steam, in addition to a widening market surplus, prices are forecast to decline in 2012-13, but to remain high by historical standards.

Coal: prices 2010 2011 2012 2013 2014Pricesa 1 Qtr 95.19 128.99 110.00 100.00 110.002 Qtr 99.49 120.00 107.00 105.00 -3 Qtr 93.55 120.61 105.00 105.00 -4 Qtr 107.63 115.00 105.00 110.00 -Year 98.97 121.15 106.75 103.25 - % change 37.8 22.4 -11.89 -3.28 -

a Australian, thermal, Newcastle/Port Kembla, US$/metric tonne.

Sources: World Bank; Economist Intelligence Unit.

Coal prices are forecast to ease, but to remain high by historical standards

Coal 21

World commodity forecasts: industrial raw materials January 2012 www.eiu.com © The Economist Intelligence Unit Limited 2012

Coal: prices(Australian, thermal, Newcastle/Port Kembla, US$/m tonne)

Sources: World Bank; Economist Intelligence Unit.

0

20

40

60

80

100

120

140

160

180

141312111009080706052004

22 Copper

World commodity forecasts: industrial raw materials January 2012 www.eiu.com © The Economist Intelligence Unit Limited 2012

Copper

The Economist Intelligence Unit estimates that growth in global copper consumption in 2011 slowed to 2.8%, from 5.6% in 2010. In addition to weak demand in the EU and US, the main restraining factor for copper demand in 2011 was monetary tightening in China, reflected in a slowdown in growth in manufacturing activity and construction (particularly residential) as well as a lack of access to credit, which has seen copper fabricators struggle to finance working inventories. The improvement witnessed in apparent Chinese demand since early in the third quarter was not necessarily driven by real consumption but by restocking, the bulk of which is mainly being done by merchants, with fabricators still largely reliant on hand-to-mouth strategies until credit market conditions improve. Therefore, the steady drawdown of stocks on the London Metal Exchange (LME) in October-November was a case of merchants exploiting low prices and arbitrage opportunities to build inventories in anticipation of future demand from consumers rather than an improvement in real consumption.

World refined copper consumption is forecast to grow by 3.2% in 2012, as policy loosening in China leads to restocking at fabricators and underpins an acceleration in growth in that country, even though export-related demand will be subdued owing to weakness in the US and EU. We also expect a return to growth in India, South Korea and Taiwan in 2012. World consumption is expected to increase by 4.6% in 2013, as the US and EU recover, but China and emerging Asian markets will continue to be the main drivers of global copper demand growth.

China's copper buyers ran down their working inventories to low levels during 2010, and many manufacturers continued to destock or, at best, adopt hand-to-mouth strategies during much of 2011. (Most did not engage in the usual restocking activity that tends to characterise the peak demand period between March and June.) However, restocking finally began in late 2011 (reflected in an increase in imports), and it took a significant fall in prices to trigger it. The broad-based sell-off that affected many markets in early August and again in late September saw copper prices on the LME fall faster than those on the Shanghai Futures Exchange (SHFE), and the resulting price differential made importing copper into China viable. Chinese buying activity picked up accordingly, with premiums strengthening in Shanghai and Singapore and LME cancelled warrants and physical withdrawals at Asian warehouses increasing as metal was shipped into China.

Arbitrage activity became more sporadic in November compared with October and September, and premiums, although still elevated, came off their recent highs. This suggests that buying appetite has waned slightly, although activity is still fairly robust and imports for November and December are likely to have remained above the 250,000-tonne level. It is important to clarify the origins of the stronger import demand since the middle of the year. We believe that merchants exploiting price dips and arbitrage opportunities are the dominant buyers, not genuine consumers of physical metal. China's copper fabricators still do not have access to sufficient credit lines to finance significant restocking,

Demand

Bargain hunting has led to a surge inChinese imports

Copper 23

World commodity forecasts: industrial raw materials January 2012 www.eiu.com © The Economist Intelligence Unit Limited 2012

so much of the metal arriving is destined, at least in the first instance, for merchants' stockpiles and not necessarily for consumption.

Merchants are confident that consumers� inventories are low and will need replenishing at some point in the coming few months, even against a back-ground of concerns about the outlook for demand in overseas markets, such as the EU. Worries about the outlook for growth could result in Chinese monetary policy being loosened, which would provide a boost to downstream demand for refined copper in China, and merchants will get the increase in demand they are anticipating. We therefore maintain a fairly optimistic view of Chinese copper demand, despite the knock-on effect of economic slowdowns in the US and EU. Growth remains on track to meet our full-year estimate in 2011 of 5.5%, and we expect an acceleration to 6% in 2012 and 8% in 2013. Indeed, at this point, we believe that the risks to these forecasts are on the upside.

There is some concern in the copper market that a slowdown in European and US economic growth will act as a drag on China and other emerging-market economies with significant trade exposure to the West. However, the vast majority of China's copper demand is driven by the domestic economy. In any case, China's government has the motivation and the means to stimulate the domestic economy if external demand falls too sharply, and recent develop-ments suggest that it is indeed starting to tinker with its policy balance in some areas. We therefore believe that Chinese copper demand is fairly well insulated from a slowdown in the Western economies. In fact, it tends to be negatively correlated, with lower copper prices associated with a Western economic slow-down triggering a pick-up in Chinese apparent demand through price-related restocking. This was the case in 2009.

Despite the estimated contraction in Japan's economy in 2011, copper consumption is expected to have recorded positive growth following a relatively swift recovery by copper fabricators from the devastating earthquake and tsunami of March 11th. The latest World Bureau of Metal Statistics (WBMS) estimates show that growth was down in year-on-year terms by just 2.5% in the nine months to September. However, production of semi-fabricated copper products increased by 0.6% year on year over the same period (to 800,623 tonnes) and imports of semis rose by 44.4% to 30,813 tonnes. These data point to good demand from copper-consuming sectors during the second and third quarters and minimal disruptions from rolling power shortages in the summer. Overall, our forecast for refined copper consumption in 2011 remains at 1.07m tonnes, which is an increase of 1.2% from 2010. We continue to forecast an acceleration in growth in 2012-13 to an annual average of 2.5%, driven by reconstruction spending.

Elsewhere in Asia, refined copper consumption growth has been surprisingly weak this year, according to WBMS data. In the nine months to September, year-on-year declines were reported in India (down by 18.8%), South Korea (down by 9%) and Taiwan (down by 13.6%). We attribute this to the effects of consumer destocking in these countries. This means that we can expect some restocking to occur following the price falls in September, which should have improved year-on-year comparisons in the final few months of the year. We

Stronger growth will come from Japan owing to reconstruction spending

Low prices have ended consumer destocking in some parts of Asia

Chinese apparent demand is negatively correlated with Western demand

Chinese consumers will take their turn restocking in 2012 and 2013

24 Copper

World commodity forecasts: industrial raw materials January 2012 www.eiu.com © The Economist Intelligence Unit Limited 2012

forecast a return to growth in all three countries in 2012-13, as stocks return to more normal levels and as the economies stabilise.

The latest data from the WBMS suggest that copper consumption in the EU contracted by 0.6% year on year in the first nine months of 2011. This is down from positive growth of 1.4% in January-August. Copper consumption is being negatively affected by the slowdown in economic growth in the region and an escalation of concerns about the stability of the euro zone. Confidence has collapsed throughout the copper supply chain and downstream orders for copper products have shrivelled against a background of uncertainty and pessimism. Our expectations are still for refined copper consumption growth of just 0.8% in 2011, with a contraction of around 2% forecast for 2012, before a return to growth, albeit of only 1%, in 2013. The risks, particularly to our shorter-term view, are on the downside, but we are reluctant to make downgrades to our forecasts, not least because data from the International Copper Study Group (ICSG) still indicate that growth is positive and comments from a leading producer, Aurubis (Germany), point to underlying consumption being better than prevailing bearish economic sentiment suggests.

WBMS figures suggest that US copper consumption growth has turned negative, reportedly contracting by 1.6% in the nine months to September. This is in line with a fall in the production of semi-fabricated copper and brass products, of 1.1% year on year over the same period. We maintain our recently revised forecast for US refined copper consumption, of a contraction this year overall of 0.5% and growth in 2012 of 1%. However, the recovery will accelerate in 2013, and we forecast growth of 2% in consumption for that year.

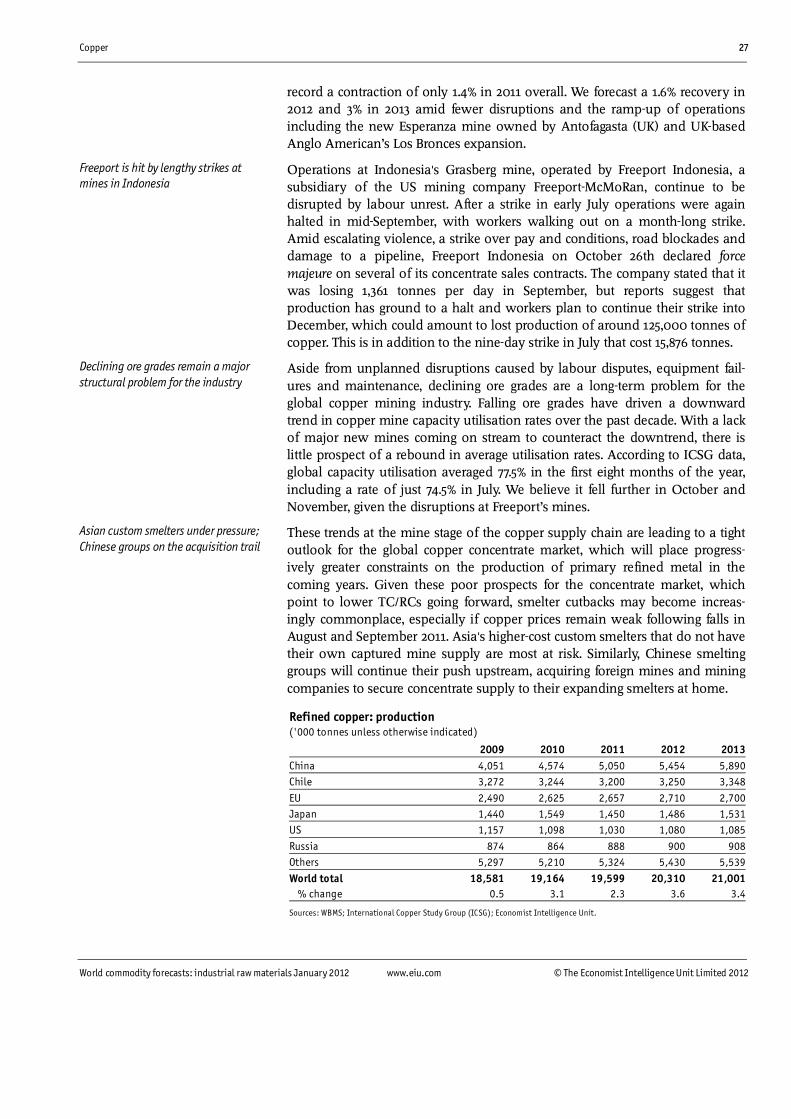

Refined copper: consumption ('000 tonnes unless otherwise indicated)

2009 2010 2011 2012 2013China 7,086 7,419 7,827 8,297 8,960EU 3,090 3,432 3,459 3,390 3,424

US 1,637 1,751 1,742 1,760 1,795Japan 875 1,060 1,073 1,101 1,127

South Korea 933 856 805 843 869Latin America 517 666 699 727 756Taiwan 494 532 484 494 509

Others 3,510 3,450 3,623 3,731 3,843World total 18,142 19,166 19,712 20,343 21,283 % change 0.0 5.6 2.8 3.2 4.6

Sources: World Bureau of Metal Statistics (WBMS); Economist Intelligence Unit.

Global production of refined copper rose by 3.1% in 2010, held back by tightness in the global concentrate market owing to low ore grades at ageing mines and unplanned disruptions. The same constraints were still evident in 2011, and constrained global refined production growth. Reflecting an escalation of labour disputes affecting some of the world's largest copper mines in Chile, Indonesia and Peru, we now estimate growth in global copper mine production in 2011 to be flat at best, with output falling short of targets by around 1m tonnes. In an effort to protect themselves to some extent from the disruptions to concentrate supply, smelters and refineries have increased their reliance on

Supply

EU consumption is slowing and growth may already have turned negative

Consumption growth has turned negative in the US too

Copper 25

World commodity forecasts: industrial raw materials January 2012 www.eiu.com © The Economist Intelligence Unit Limited 2012

scrap as a raw material. However, low prices in recent months have seen scrap supplies dwindling as well. In 2012-13 new investments in primary capacity, particularly in China, will underpin further modest growth in global refined copper output, which is forecast to expand by an average of 3.5% a year, providing mine supply also recovers. However, the tendency for copper mines to be disrupted by labour issues, accidents, low ore grades and other factors means that the risk of disruptions in the copper supply chain will remain high. Nevertheless, we expect that growth will be achieved by a recovery to record-high prices and falling inventories in the refined market, incentivising higher rates of scrap collection and utilisation and encouraging smelters and refineries to maximise output and run down raw material inventories.

Data for Chinese production in October from the National Bureau of Statistics (NBS) showed that output of refined copper declined for the third consecutive month, to 469,000 tonnes, compared with a record high level of 518,000 tonnes in August. With the temporary improvement in availabililty in the spot copper concentrate market owing to the shutdowns of Japanese smelters following the earthquake and tsunami in March, treatment and refining charges (TC/RCs) earned by smelters for processing the material doubled to US$150/tonne and 15 US cents/lb, respectively. This encouraged Chinese smelters to maximise capacity utilisation in the wake of the Japanese disaster. However, Japanese smelters have been returning to normal operations in more recent months, and as a result spot TC/RCs have retreated in line with a renewed tightening of the spot concentrate market. They were last reported at around US$30-40/tonne and 3-4 US cents/lb in November, from US$50/tonne and 5 US cents/lb, respectively, in September and October. The correction back to lower levels has been accelerated somewhat by mine strikes in Chile, Indonesia and Peru, which have further reduced the availability of concentrate in the spot market. This is reflected by Chinese smelters reining in capacity utilisation again. Output growth is expected to continue moderating in the coming months.