emba presentation november 17,2012. cost allocations involve: common costs joint costs

TRANSCRIPT

COST ALLOCATION

EMBA PresentationNovember 17,2012

Cost Allocations Involve:

Common Costs Joint Costs

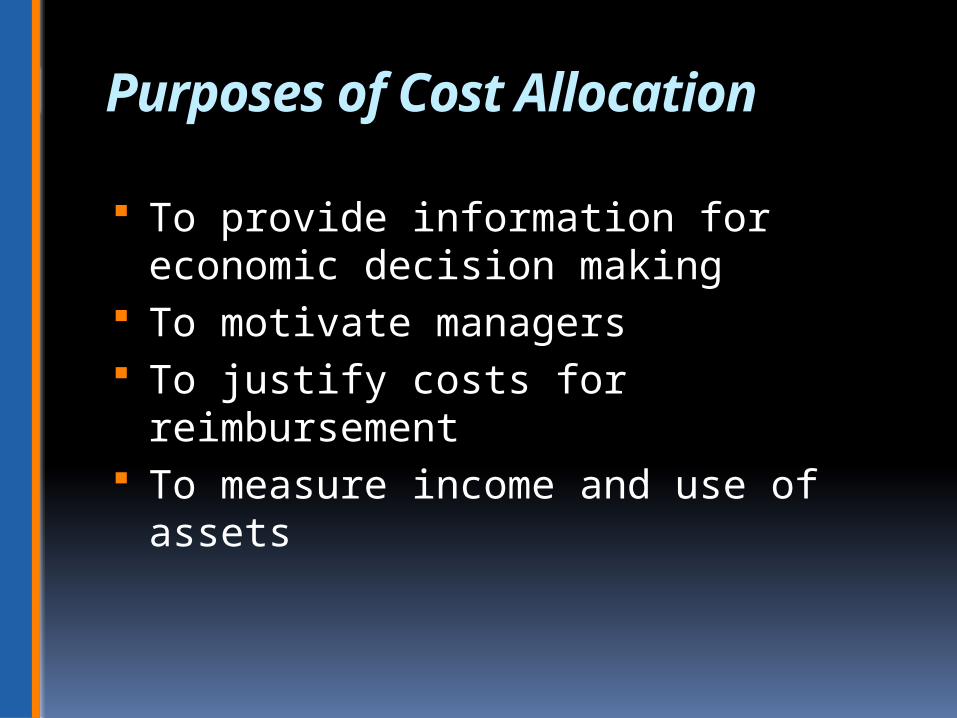

Purposes of Cost Allocation To provide information for economic

decision making To motivate managers To justify costs for reimbursement To measure income and use of assets

Criteria for Allocation of Costs

Cause and effect Benefits received Fairness or equity Ability to bear

Steps in Cost Allocation

Define the cost objects Accumulate common costs Choose a method for assigning costs

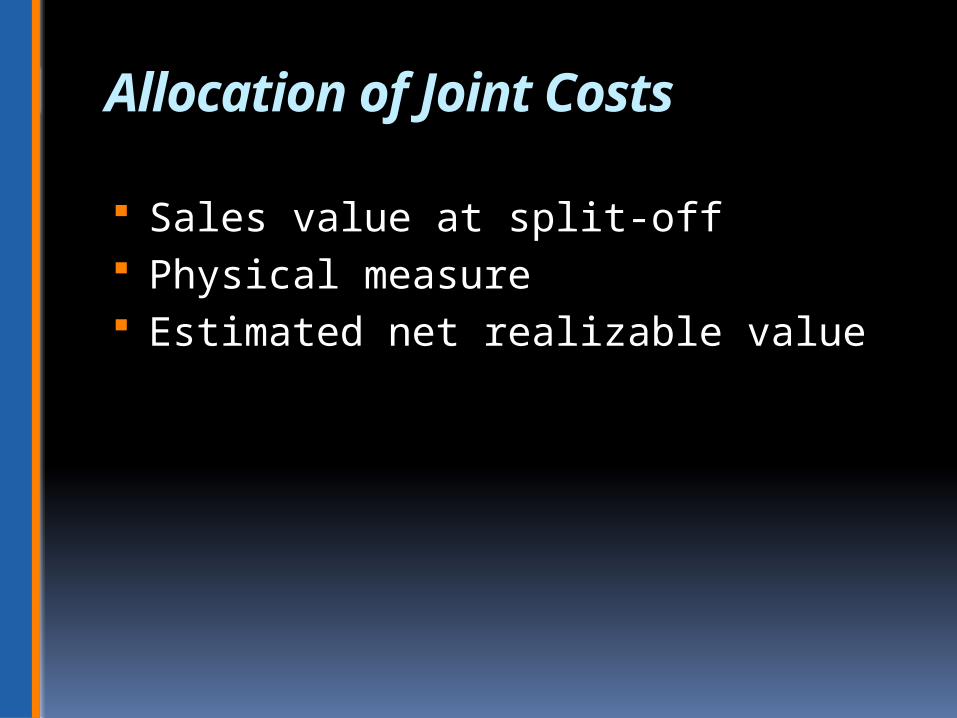

Allocation of Joint Costs

Sales value at split-off Physical measure Estimated net realizable value

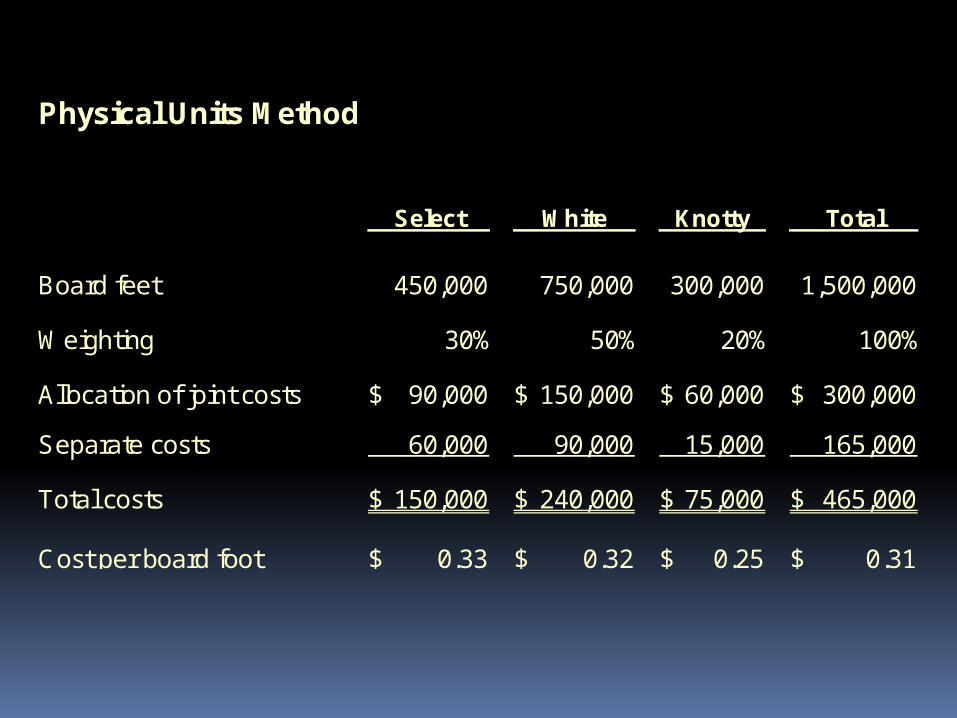

Physical Units Method

Select White Knotty Total

Board feet 450,000 750,000 300,000 1,500,000

Weighting 30% 50% 20% 100%

Allocation of joint costs 90,000$ 150,000$ 60,000$ 300,000$

Separate costs 60,000 90,000 15,000 165,000

Total costs 150,000$ 240,000$ 75,000$ 465,000$

Cost per board foot 0.33$ 0.32$ 0.25$ 0.31$

Sales Value at Spin Off Method

Select White Knotty Total

(450,000 x..35)(750,000 x.40)(300,000 x .19) 157,500$ 300,000$ 75,000$ 532,500$

Weighting 30% 56% 14% 100%

Allocation of joint costs 88,732$ 169,014$ 42,254$ 300,000$

Separate costs 60,000 90,000 15,000 165,000

Total costs 148,732$ 259,014$ 57,254$ 465,000$

Cost per board foot 0.33$ 0.35$ 0.19$ 0.31$

Net Realizable Value Method

Select White Knotty Total

(405,000 x.40)(675,000 x.55)(270,000 x .25) 162,000$ 371,250$ 67,500$ 600,750$

Less separate costs 60,000 90,000 15,000 165,000

NRV at split off 102,000$ 281,250$ 52,500$ 435,750$

Weighting 23% 65% 12% 100%

Allocated joint costs 70,224$ 193,632$ 36,145$ 300,000$

Add separate costs 60,000 90,000 15,000 165,000

Total costs 130,224$ 283,632$ 51,145$ 465,000$

Cost per board foot 0.29$ 0.38$ 0.17$ 0.31$

Method Select White

Knotty Total

Physical units .33 .32 .25 .31

Split off .33 .35 .19 .31

NRV .29 .38 .17 .31

Comparison of the Three Methods

So, which is the best

method?

None . . .

they are all arbitrary

Pros and Cons

Physical units – is easy to calculate Split-off – may not be appropriate if

there is no market at the split-off point

NRV – assumes that the greater the end sales dollars, the better it can bear the joint cost

Allocation of Common Costs Direct Method Step-down Method Reciprocal Method

Direct Method Allocations

Head Percent Hours PercentAdmin/HR - - - - Information Services - - - - Government 40 0.53333 3,000 0.33333 Corporate 35 0.46667 6,000 0.66667

Total 75 1.00000 9,000 1.00000

Administrative Information Services

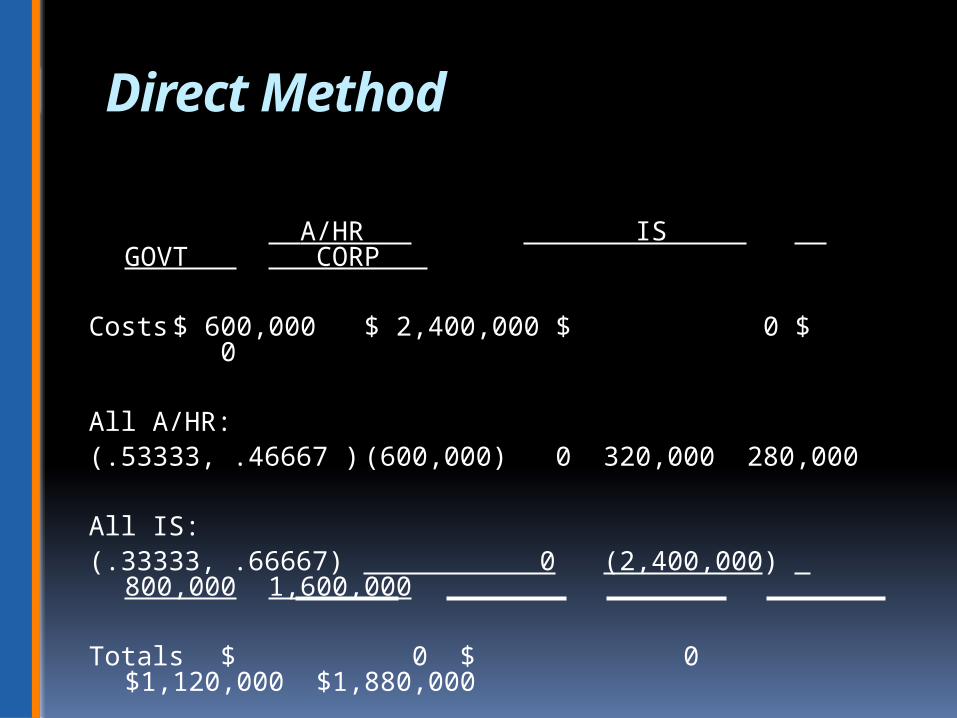

Direct Method

A/HR IS GOVT CORP

Costs $ 600,000 $ 2,400,000 $ 0 $ 0

All A/HR:(.53333, .46667 ) (600,000) 0 320,000 280,000

All IS:(.33333, .66667) 0(2,400,000) 800,000

1,600,000

Totals $ 0 $ 0 $1,120,000$1,880,000

Step Down Allocations

Head Percent Hours PercentAdmin/HR - - - - Information Services 25 0.25000 - - Government 40 0.40000 3,000 0.33333 Corporate 35 0.35000 6,000 0.66667

Total 100 1.00000 9,000 1.00000

Administrative Information Services

Step Down Method – A/HR First

A/HR IS GOVT CORP

Cost $ 600,000 $ 2,400,000 $ 0 $ 0

A/HR

(.25, .40, .35) (600,000) 150,000 240,000210,000

IS

(.33333. .66667) 0(2,550,000) 850,000 1,700,000

Totals $ 0 $ 0 $1,090,000$1,910,000

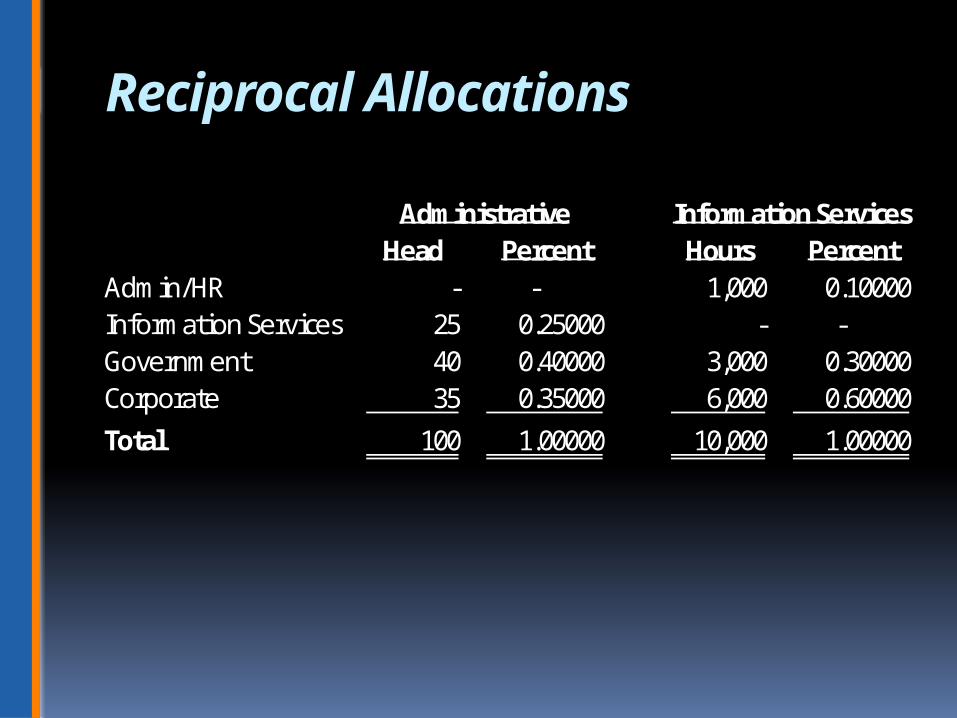

Reciprocal Allocations

Head Percent Hours PercentAdmin/HR - - 1,000 0.10000 Information Services 25 0.25000 - - Government 40 0.40000 3,000 0.30000 Corporate 35 0.35000 6,000 0.60000

Total 100 1.00000 10,000 1.00000

Administrative Information Services

Reciprocal Method A/HR IS GOVT CORP

Costs $ 600,000 $2,400,000

A/HR (.25, .40, .35) (861,538) 215,385 344,615

301,538

IS (.10, .30, .60) 261,538 (2,615,385) 784,615

1,569,231

Totals $ 0 $ 0 $1,129,230 $1,870,769

A = 600,000 + .10 ISIS = 2,400,000 + .25 AIS = 2,400,000 +1 50,000 + .025 IS.9750 IS = 2,550,000IS = 2,615,385A = 600,000+.10 (2,615,385)A = 861,538

Comparison of Results

Method Government Corporate

Direct $1,120,000 $1,880,000

Stepdown Adm first $1,098,000

$1,910,000

Stepdown IT first $1,128,000

$1,892,000

Reciprocal $1,129,230 $1,870,769

Pros and Cons of Methods

Direct method – easy but ignores how support departments use each other

Step down – widely accepted but requires designation of a “first” department

Reciprocal – most accurate but not well understood or widely used

Summary

Reason for cost allocations Allocating joint costs Allocating common costs

Copyright by Frank Ilett, 2012