emea insurers snapshot - regional snapshot

TRANSCRIPT

LIMITED ACCESS

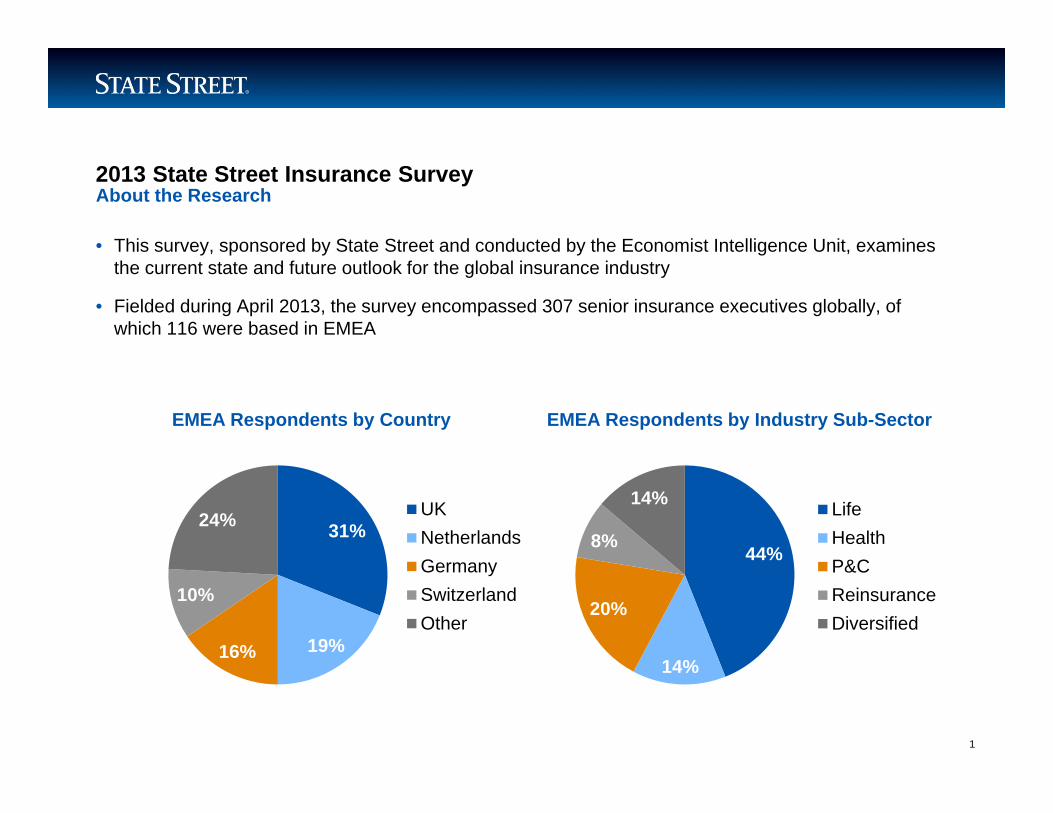

2013 State Street Insurance Survey

• This survey, sponsored by State Street and conducted by the Economist Intelligence Unit, examines the current state and future outlook for the global insurance industry

• Fielded during April 2013, the survey encompassed 307 senior insurance executives globally, of which 116 were based in EMEA

About the Research

1

44%

14%

20%

8%

14% LifeHealthP&CReinsuranceDiversified

31%

19%16%

10%

24% UKNetherlandsGermanySwitzerlandOther

EMEA Respondents by Country EMEA Respondents by Industry Sub-Sector

LIMITED ACCESS

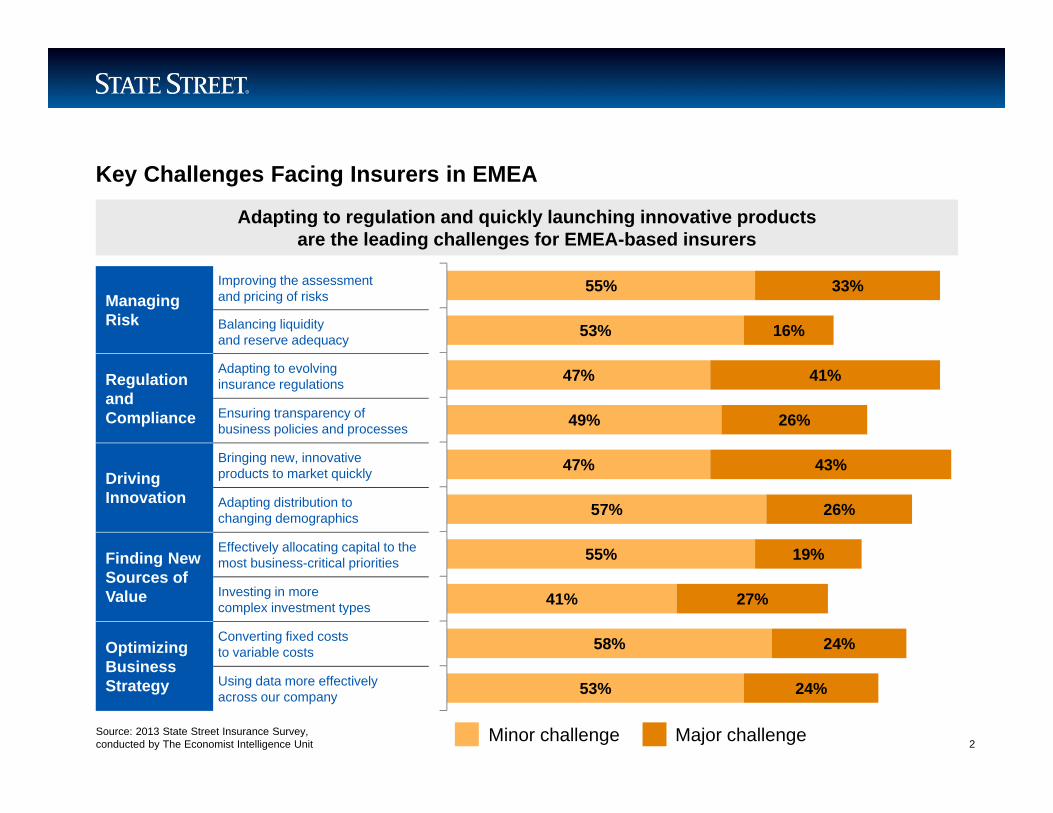

Key Challenges Facing Insurers in EMEA

Managing Risk

Improving the assessment and pricing of risks

Balancing liquidity and reserve adequacy

Regulationand Compliance

Adapting to evolving insurance regulations

Ensuring transparency of business policies and processes

Driving Innovation

Bringing new, innovative products to market quickly

Adapting distribution to changing demographics

Finding New Sources of Value

Effectively allocating capital to the most business-critical priorities

Investing in more complex investment types

Optimizing BusinessStrategy

Converting fixed costs to variable costs

Using data more effectively across our company

55%

53%

47%

49%

47%

57%

55%

41%

58%

53%

33%

16%

41%

26%

43%

26%

19%

27%

24%

24%

Minor challenge Major challengeSource: 2013 State Street Insurance Survey, conducted by The Economist Intelligence Unit 2

Adapting to regulation and quickly launching innovative products are the leading challenges for EMEA-based insurers

LIMITED ACCESS

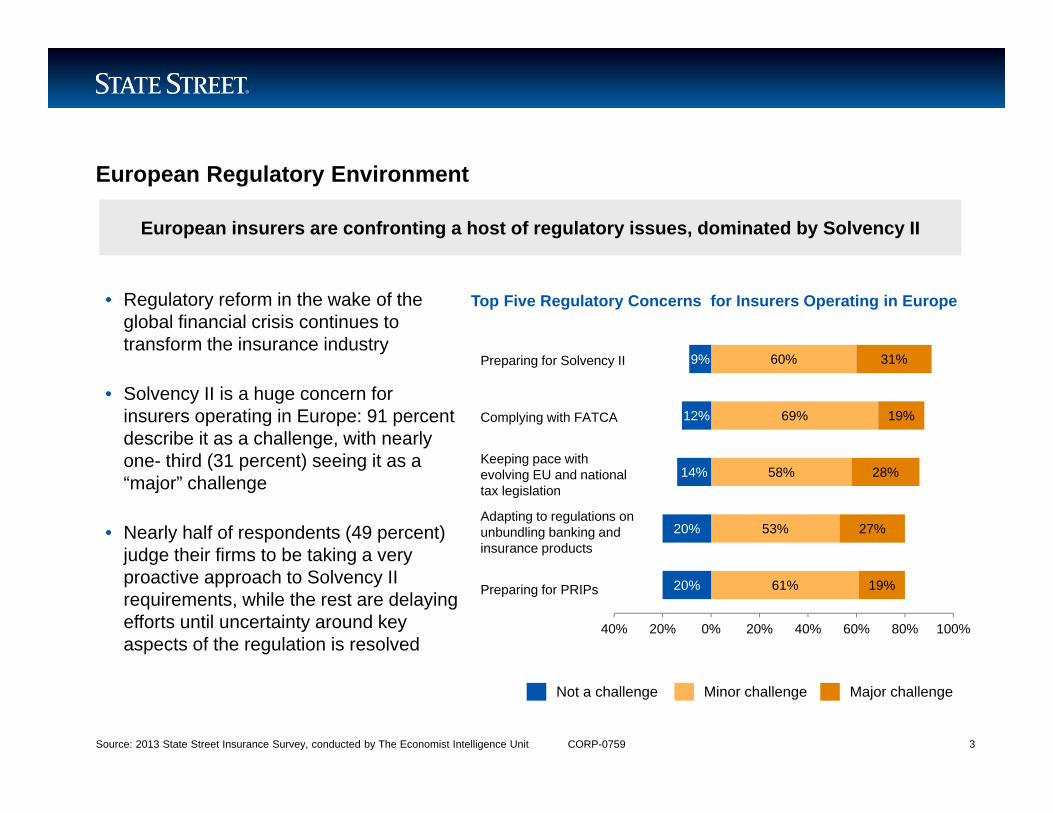

60%

69%

58%

53%

61%

31%

19%

28%

27%

19%

9%

12%

14%

20%

20%

40% 20% 0% 20% 40% 60% 80% 100%

European Regulatory Environment

Top Five Regulatory Concerns for Insurers Operating in Europe

Source: 2013 State Street Insurance Survey, conducted by The Economist Intelligence Unit CORP-0759 3

• Regulatory reform in the wake of the global financial crisis continues to transform the insurance industry

• Solvency II is a huge concern for insurers operating in Europe: 91 percent describe it as a challenge, with nearly one- third (31 percent) seeing it as a “major” challenge

• Nearly half of respondents (49 percent) judge their firms to be taking a very proactive approach to Solvency II requirements, while the rest are delaying efforts until uncertainty around key aspects of the regulation is resolved

European insurers are confronting a host of regulatory issues, dominated by Solvency II

Preparing for Solvency II

Complying with FATCA

Keeping pace with evolving EU and national tax legislation

Adapting to regulations onunbundling banking and insurance products

Preparing for PRIPs

Not a challenge Minor challenge Major challenge