emerging issues in finance what keeps me up at night? philip livingston december 20, 2005 emerging...

Post on 21-Dec-2015

218 views

TRANSCRIPT

Emerging Issues in Finance

What Keeps Me Up At Night?

Philip LivingstonDecember 20, 2005

Emerging Issues in Finance

What Keeps Me Up At Night?

Philip LivingstonDecember 20, 2005

Issues Around 404Issues Around 404

COST, COST, COSTNew FASB standards and other regulatory obligations

Outpouring of concern when ED on Uncertain Tax Provisions was proposed for year endComplexity of standards and impact on 404 processes

Companies continue to modify their installations of IT systems late in the year due to concerns of AS2 implicationsContinuing lack of judgment in evaluation of deficiencies

More leadership needed from companies and accounting firmsInexperienced staff need guidance and sense of scope and risk

COST, COST, COSTNew FASB standards and other regulatory obligations

Outpouring of concern when ED on Uncertain Tax Provisions was proposed for year endComplexity of standards and impact on 404 processes

Companies continue to modify their installations of IT systems late in the year due to concerns of AS2 implicationsContinuing lack of judgment in evaluation of deficiencies

More leadership needed from companies and accounting firmsInexperienced staff need guidance and sense of scope and risk

FEI “SOX 404 Implementation – Practices of Leading Companies”FEI “SOX 404 Implementation – Practices of Leading Companies”

Organization StructureEnterprise-wide initiative through tone at the topStart early, involve many and communicateFinance takes the lead – controllership or internal auditClearly define roles and responsibilitiesSeparate documentation and testingRobust training and education

Scope, Documentation and TestingSelf-assessment as the foundationRisk-based approach to scopeFormalize and standardize documentation and testingIncorporate internal controls reviews in M&A due diligence

Organization StructureEnterprise-wide initiative through tone at the topStart early, involve many and communicateFinance takes the lead – controllership or internal auditClearly define roles and responsibilitiesSeparate documentation and testingRobust training and education

Scope, Documentation and TestingSelf-assessment as the foundationRisk-based approach to scopeFormalize and standardize documentation and testingIncorporate internal controls reviews in M&A due diligence

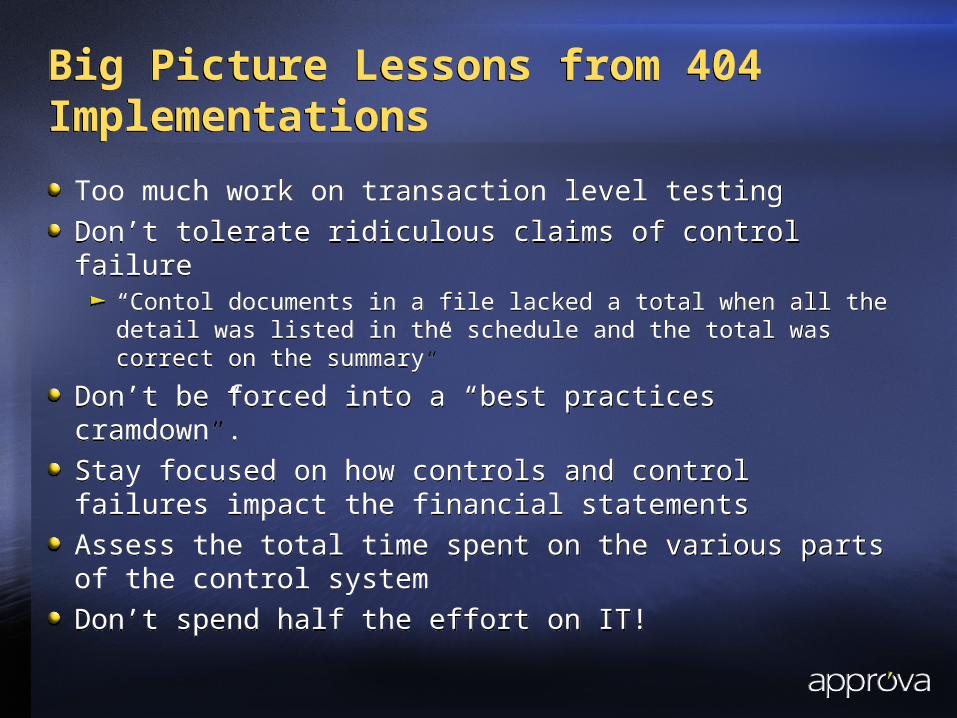

Big Picture Lessons from 404 ImplementationsBig Picture Lessons from 404 Implementations

Too much work on transaction level testingDon’t tolerate ridiculous claims of control failure

“Contol documents in a file lacked a total when all the detail was listed in the schedule and the total was correct on the summary”

Don’t be forced into a “best practices cramdown”. Stay focused on how controls and control failures impact the financial statementsAssess the total time spent on the various parts of the control systemDon’t spend half the effort on IT!

Too much work on transaction level testingDon’t tolerate ridiculous claims of control failure

“Contol documents in a file lacked a total when all the detail was listed in the schedule and the total was correct on the summary”

Don’t be forced into a “best practices cramdown”. Stay focused on how controls and control failures impact the financial statementsAssess the total time spent on the various parts of the control systemDon’t spend half the effort on IT!

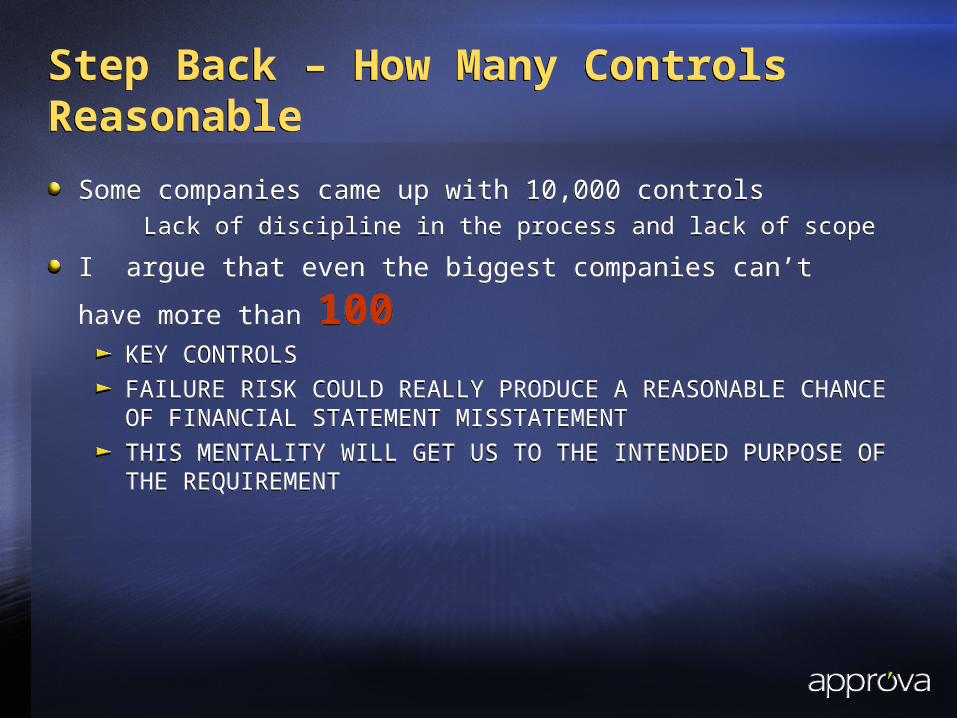

Step Back – How Many Controls ReasonableStep Back – How Many Controls Reasonable

Some companies came up with 10,000 controlsLack of discipline in the process and lack of scope

I argue that even the biggest companies can’t have more

than 100 KEY CONTROLS FAILURE RISK COULD REALLY PRODUCE A REASONABLE CHANCE OF FINANCIAL STATEMENT MISSTATEMENTTHIS MENTALITY WILL GET US TO THE INTENDED PURPOSE OF THE REQUIREMENT

Some companies came up with 10,000 controlsLack of discipline in the process and lack of scope

I argue that even the biggest companies can’t have more

than 100 KEY CONTROLS FAILURE RISK COULD REALLY PRODUCE A REASONABLE CHANCE OF FINANCIAL STATEMENT MISSTATEMENTTHIS MENTALITY WILL GET US TO THE INTENDED PURPOSE OF THE REQUIREMENT

How to Make Internal Control Compliance Sustainable and Efficient

How to Make Internal Control Compliance Sustainable and Efficient

AUTOMATE, AUTOMATE, AUTOMATE! Focus on STRENGTHENING INTERNAL CONTROL

Move beyond a compliance mentality2004 proved that a pure compliance mentality is a disaster

“Build it in, don’t bolt it on!”Focus on testing ONLY key controls, do less transaction testingBuild a “Sensitive Transaction” monitoring process

Define high risk transactions in a policy that leaves little to judgmentDefine an extended approval and sign off process for these

– Like “deal desk” in the software worldCertain transactions – related parties and those involving executives may need to be elevated to the external auditor and audit committee

Consider Harvey Pitt’s idea – forensic audits every three years

AUTOMATE, AUTOMATE, AUTOMATE! Focus on STRENGTHENING INTERNAL CONTROL

Move beyond a compliance mentality2004 proved that a pure compliance mentality is a disaster

“Build it in, don’t bolt it on!”Focus on testing ONLY key controls, do less transaction testingBuild a “Sensitive Transaction” monitoring process

Define high risk transactions in a policy that leaves little to judgmentDefine an extended approval and sign off process for these

– Like “deal desk” in the software worldCertain transactions – related parties and those involving executives may need to be elevated to the external auditor and audit committee

Consider Harvey Pitt’s idea – forensic audits every three years

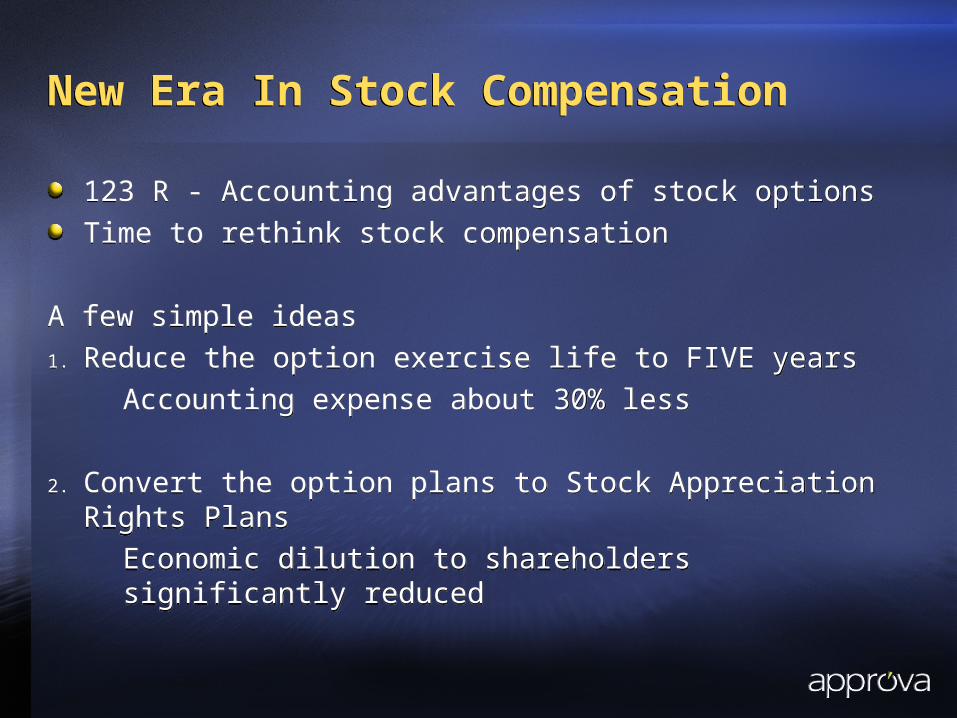

New Era In Stock CompensationNew Era In Stock Compensation

123 R - Accounting advantages of stock options Time to rethink stock compensation

A few simple ideas1. Reduce the option exercise life to FIVE years

Accounting expense about 30% less

2. Convert the option plans to Stock Appreciation Rights Plans

Economic dilution to shareholders significantly reduced

123 R - Accounting advantages of stock options Time to rethink stock compensation

A few simple ideas1. Reduce the option exercise life to FIVE years

Accounting expense about 30% less

2. Convert the option plans to Stock Appreciation Rights Plans

Economic dilution to shareholders significantly reduced

Simplifying Financial ReportingSimplifying Financial Reporting

Need to make financial statements READABLE and FUNCTIONAL for the INVESTORTables and charts, not textNo elevator music!Real business issues and trendsEnd of hard copy reports is in sight

TECHNOLOGY! TECHNOLOGY! TECHNOLOGY!

Need to make financial statements READABLE and FUNCTIONAL for the INVESTORTables and charts, not textNo elevator music!Real business issues and trendsEnd of hard copy reports is in sight

TECHNOLOGY! TECHNOLOGY! TECHNOLOGY!

Escalating Audit Fees and Quality of AuditsEscalating Audit Fees and Quality of Audits

Escalating Audit FeesQuality of audits not improvingConcentration of audit firmsTalent pool severely strained by systemic changes

Escalating Audit FeesQuality of audits not improvingConcentration of audit firmsTalent pool severely strained by systemic changes

Transactions with ExecutivesTransactions with Executives

Recent charges filed against Conrad Black allege:

An acquisition “required non-compete payments” be paid to the top executives

Many of these cases are simply low-tech theft. No better than the guy that robs the local Seven Eleven. They should be treated that way.

Recent charges filed against Conrad Black allege:

An acquisition “required non-compete payments” be paid to the top executives

Many of these cases are simply low-tech theft. No better than the guy that robs the local Seven Eleven. They should be treated that way.

Revenue RecognitionRevenue Recognition

60% of restatements historically from revenue recognition issuesUsually, silly timing issues brought about by earnings pressureLack of PRACTICAL, but formalized, policiesSoftware industry particularly difficult

60% of restatements historically from revenue recognition issuesUsually, silly timing issues brought about by earnings pressureLack of PRACTICAL, but formalized, policiesSoftware industry particularly difficult

Other High Risk AreasOther High Risk Areas

Financial Close ProcessRelated Party TransactionsAccount ReconciliationsTransactions Centered in Critical Accounting PoliciesSegregation of DutiesCapitalization policiesVariances in budget and forecasts to actuals

Financial Close ProcessRelated Party TransactionsAccount ReconciliationsTransactions Centered in Critical Accounting PoliciesSegregation of DutiesCapitalization policiesVariances in budget and forecasts to actuals

SEC’s List of Common Fraud SchemesSEC’s List of Common Fraud Schemes

Premature revenue recognitionExcess reserves to smooth earningsImproper accounting for vendor rebatesImproper capitalized costsChanging estimates “to make the numbers”Top-side and period end manual journal entries“Earnings management”

Premature revenue recognitionExcess reserves to smooth earningsImproper accounting for vendor rebatesImproper capitalized costsChanging estimates “to make the numbers”Top-side and period end manual journal entries“Earnings management”

Real Promotion of Ethical Conduct Real Promotion of Ethical Conduct

We still aren’t doing enough hereEmployees need to know we are serious about snuffing out unacceptable behaviorCommunication must be repeated and come from the topCompanies largely doing the least amount required

We still aren’t doing enough hereEmployees need to know we are serious about snuffing out unacceptable behaviorCommunication must be repeated and come from the topCompanies largely doing the least amount required

Capital AllocationCapital Allocation

AcquisitionsDo they hit the pre-deal projections?Do we get the synergies we projected?Does the return generate net shareholder value or destroy shareholder value?

Capital expendituresNew capacity really needed?Cost savings really materialize?Positive or negative IRR

Share BuybacksGreat balancer in capital allocation equation

AcquisitionsDo they hit the pre-deal projections?Do we get the synergies we projected?Does the return generate net shareholder value or destroy shareholder value?

Capital expendituresNew capacity really needed?Cost savings really materialize?Positive or negative IRR

Share BuybacksGreat balancer in capital allocation equation

Bottom LineBottom Line

Clean, crisp financial reporting more valuable than ever

Investors clearly avoiding messy, complicated companies.

Premium valuations for companies that have clear business models and clear financial reporting.

Ability of financial officers to impact shareholder value, greater than ever.

Clean, crisp financial reporting more valuable than ever

Investors clearly avoiding messy, complicated companies.

Premium valuations for companies that have clear business models and clear financial reporting.

Ability of financial officers to impact shareholder value, greater than ever.