emirates telecommunications corporation - etisalat · emirates telecommunications corporation...

TRANSCRIPT

April 2010 1

Emirates Telecommunications Corporation

„Etisalat‟

April 2011

Analyst Day

1Q 2011

April 2011 2

Notice to Recipients

Emirates Telecommunications Corporation Etisalat and its subsidiaries (“Etisalat” or the

“Company”) confirms that, to the best of its knowledge and belief (having made all reasonable

enquiries), the factual information contained in this presentation is at its date true and accurate

in all material respects, has been prepared with all reasonable care and that the opinions

expressed herein were, at the time they were given, honestly held.

Unless otherwise stated the source of all information provided in this Presentation is the

Company and its subsidiaries.

Where this Presentation contains summaries of documents, those summaries should not be

relied upon and the actual documentation must be referred to for its full effect.

The contents of this presentation, which may include non-public price sensitive information, are

and must remain confidential. This Presentation may not be reproduced or used in whole or in

part for any other purpose, nor should it be disclosed to any other party.

3

Agenda

• 1Q 2011 Result1

• Group Overview2

• Etisalat UAE 1Q 2011 Result3

• International Operations 1Q 2011 Result4

• Key Takeaways5

April 2011

4

1. 1Q 2011 Result

April 2011

5

1Q 2011 Result

Consolidated revenue amounted to AED 8,040m, a 2% increase over the prior

corresponding period

International revenue amounted to AED1,867m, a 15% increase over the prior

corresponding period

Profit after royalty amounted to AED 1,817m a decrease of 9% over the prior

corresponding period

Continued investments with capital expenditure of AED 1,113m representing 14% of

revenue

Consolidated subscribers increased 19% to 45m from 38m in the prior corresponding

period

April 2011

6

2. Group Overview

April 2011

7

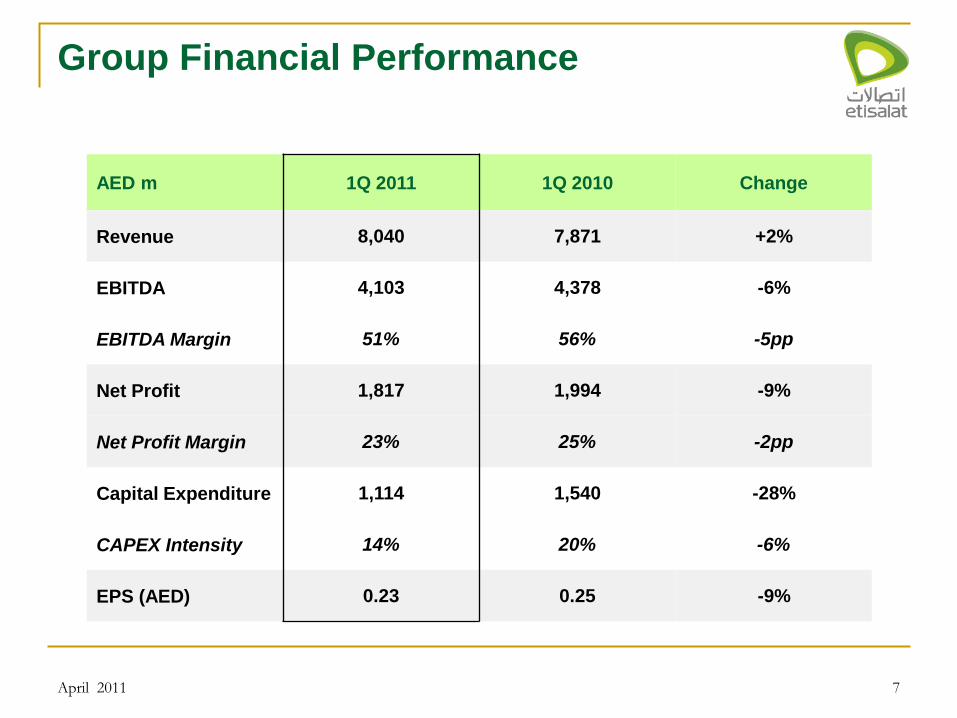

Group Financial Performance

AED m 1Q 2011 1Q 2010 Change

Revenue 8,040 7,871 +2%

EBITDA 4,103 4,378 -6%

EBITDA Margin 51% 56% -5pp

Net Profit 1,817 1,994 -9%

Net Profit Margin 23% 25% -2pp

Capital Expenditure 1,114 1,540 -28%

CAPEX Intensity 14% 20% -6%

EPS (AED) 0.23 0.25 -9%

April 2011

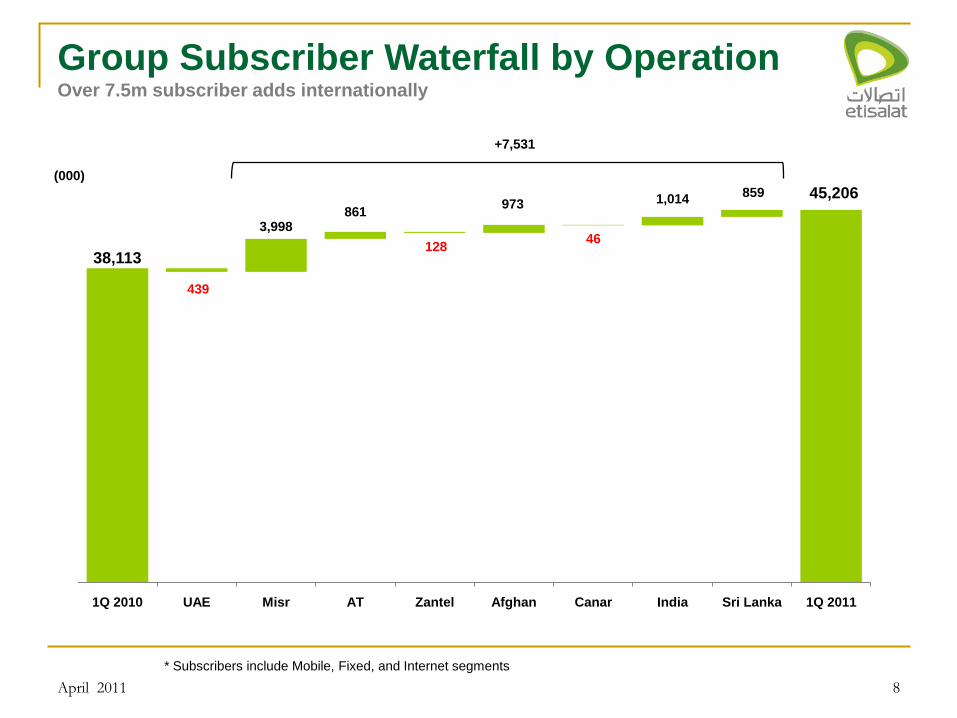

38,113

45,206

3,998 861

128

973 1,014 859

439

46

1Q 2010 UAE Misr AT Zantel Afghan Canar India Sri Lanka 1Q 2011

8

Group Subscriber Waterfall by OperationOver 7.5m subscriber adds internationally

* Subscribers include Mobile, Fixed, and Internet segments

+7,531

April 2011

(000)

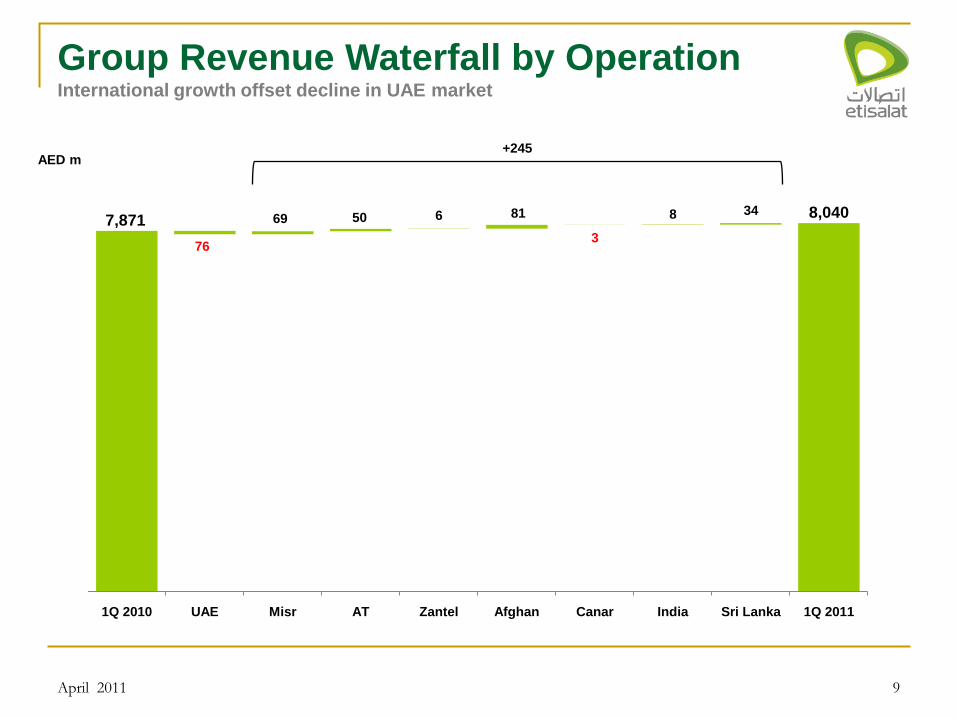

7,871 8,040 69 50 6 81 8 34

76 3

1Q 2010 UAE Misr AT Zantel Afghan Canar India Sri Lanka 1Q 2011

9

Group Revenue Waterfall by OperationInternational growth offset decline in UAE market

+245AED m

April 2011

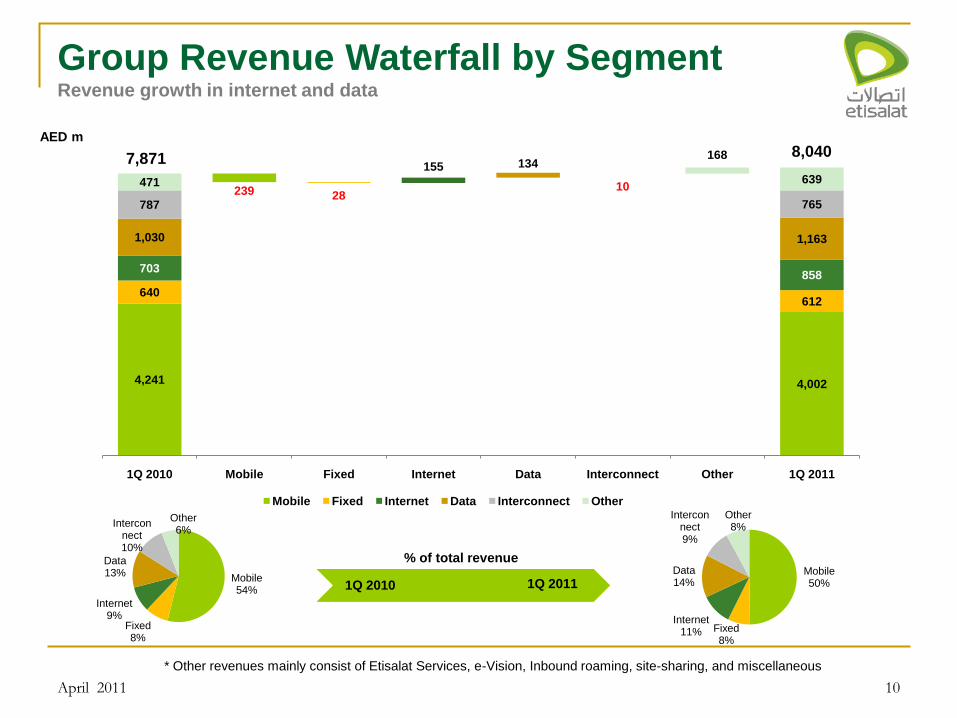

4,241 4,002

640612

703858

1,030 1,163

787 765

471 639155 134

10

168

239 28

1Q 2010 Mobile Fixed Internet Data Interconnect Other 1Q 2011

Mobile Fixed Internet Data Interconnect Other Previous Positive Negative

10

Group Revenue Waterfall by SegmentRevenue growth in internet and data

Mobile54%

Fixed8%

Internet9%

Data13%

Interconnect10%

Other6%

Mobile50%

Fixed8%

Internet11%

Data14%

Interconnect9%

Other8%

1Q 2010 1Q 2011

7,871

% of total revenue

AED m

* Other revenues mainly consist of Etisalat Services, e-Vision, Inbound roaming, site-sharing, and miscellaneous

April 2011

8,040

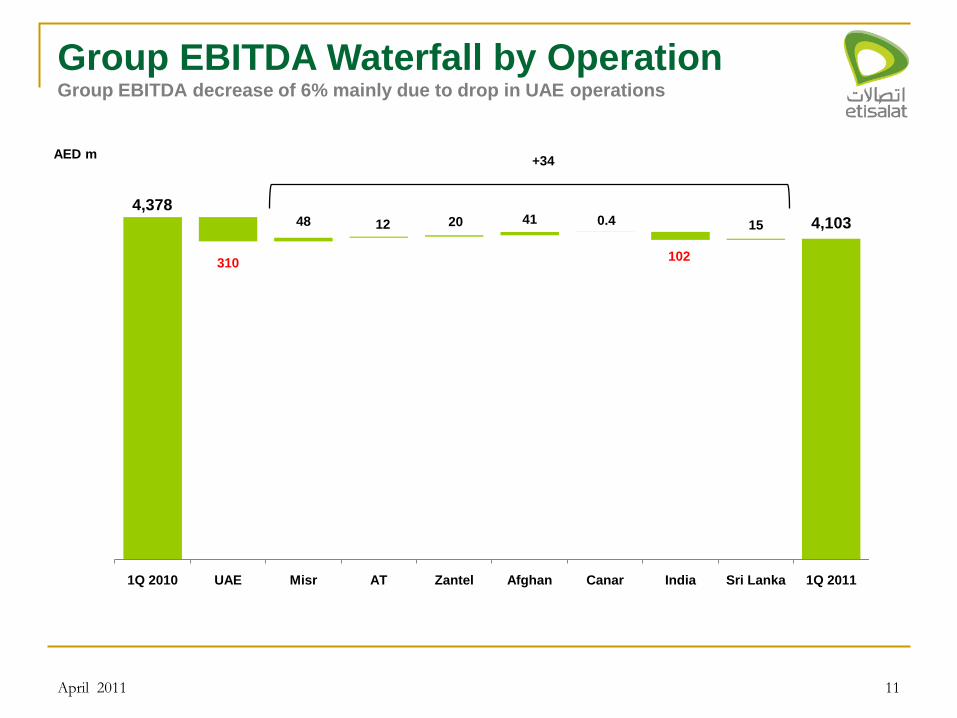

48 12 20 41 0.4 15

310 102

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

1Q 2010 UAE Misr AT Zantel Afghan Canar India Sri Lanka 1Q 2011

11

Group EBITDA Waterfall by OperationGroup EBITDA decrease of 6% mainly due to drop in UAE operations

+34AED m

4,3784,103

April 2011

12

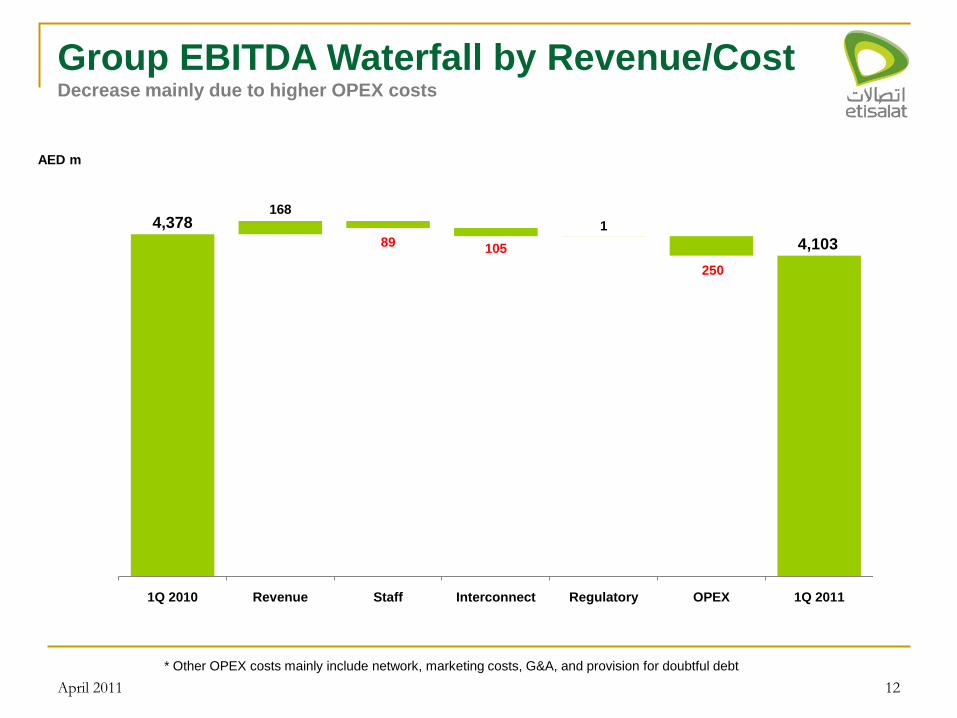

Group EBITDA Waterfall by Revenue/CostDecrease mainly due to higher OPEX costs

* Other OPEX costs mainly include network, marketing costs, G&A, and provision for doubtful debt

AED m

4,378

April 2011

4,103

4,378

4,103

168

1

89105

250

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

1Q 2010 Revenue Staff Interconnect Regulatory OPEX 1Q 2011

13

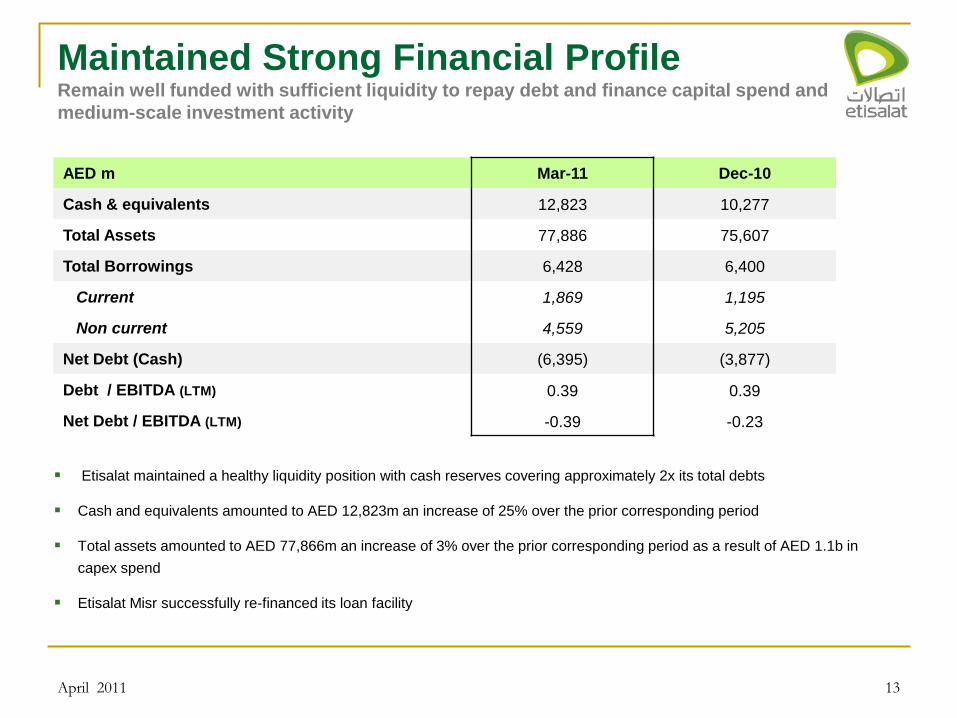

Maintained Strong Financial ProfileRemain well funded with sufficient liquidity to repay debt and finance capital spend and

medium-scale investment activity

AED m Mar-11 Dec-10

Cash & equivalents 12,823 10,277

Total Assets 77,886 75,607

Total Borrowings 6,428 6,400

Current 1,869 1,195

Non current 4,559 5,205

Net Debt (Cash) (6,395) (3,877)

Debt / EBITDA (LTM) 0.39 0.39

Net Debt / EBITDA (LTM) -0.39 -0.23

Etisalat maintained a healthy liquidity position with cash reserves covering approximately 2x its total debts

Cash and equivalents amounted to AED 12,823m an increase of 25% over the prior corresponding period

Total assets amounted to AED 77,866m an increase of 3% over the prior corresponding period as a result of AED 1.1b in

capex spend

Etisalat Misr successfully re-financed its loan facility

April 2011

14

3.Etisalat UAE

April 2011

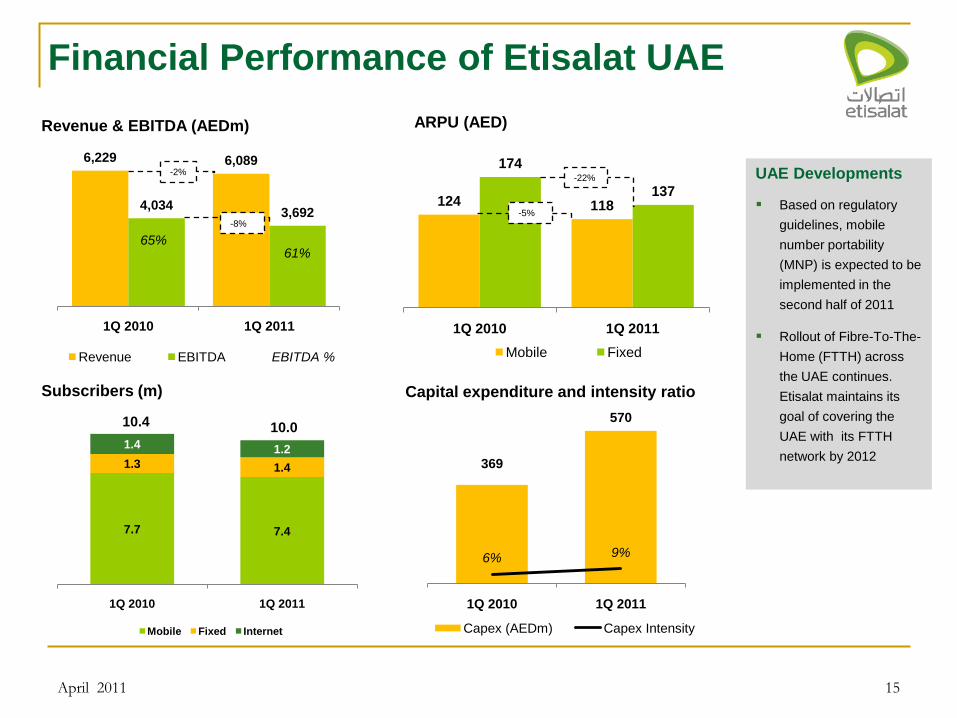

7.7 7.4

1.3 1.4

1.4 1.2

1Q 2010 1Q 2011

Mobile Fixed Internet

15

Financial Performance of Etisalat UAE

ARPU (AED)Revenue & EBITDA (AEDm)

Subscribers (m) Capital expenditure and intensity ratio

10.4 10.0

6,229 6,089

4,034 3,692

65%61%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

1Q 2010 1Q 2011

Revenue EBITDA EBITDA %

124 118

174

137

1Q 2010 1Q 2011

Mobile Fixed

369

570

6% 9%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

100

200

300

400

500

600

1Q 2010 1Q 2011

Capex (AEDm) Capex Intensity

-2%

-5%-8%

April 2011

UAE Developments

Based on regulatory

guidelines, mobile

number portability

(MNP) is expected to be

implemented in the

second half of 2011

Rollout of Fibre-To-The-

Home (FTTH) across

the UAE continues.

Etisalat maintains its

goal of covering the

UAE with its FTTH

network by 2012

-22%

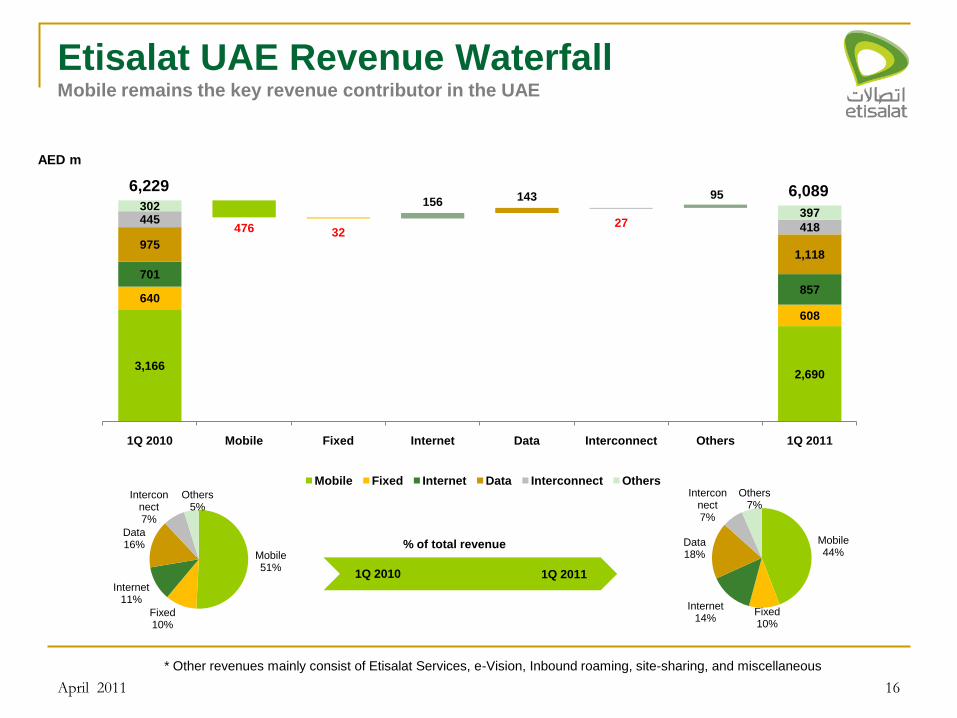

3,1662,690

640

608

701

857

9751,118

445418

302 397

156 143

476 32 27

95

1Q 2010 Mobile Fixed Internet Data Interconnect Others 1Q 2011

Mobile Fixed Internet Data Interconnect Others Previous Positive Negative

16

Etisalat UAE Revenue WaterfallMobile remains the key revenue contributor in the UAE

Mobile51%

Fixed10%

Internet11%

Data16%

Interconnect7%

Others5%

Mobile44%

Fixed10%

Internet14%

Data18%

Interconnect7%

Others7%

1Q 2010 1Q 2011

6,089

% of total revenue

AED m

* Other revenues mainly consist of Etisalat Services, e-Vision, Inbound roaming, site-sharing, and miscellaneous

April 2011

6,229

17

4.International Operations

April 2011

18

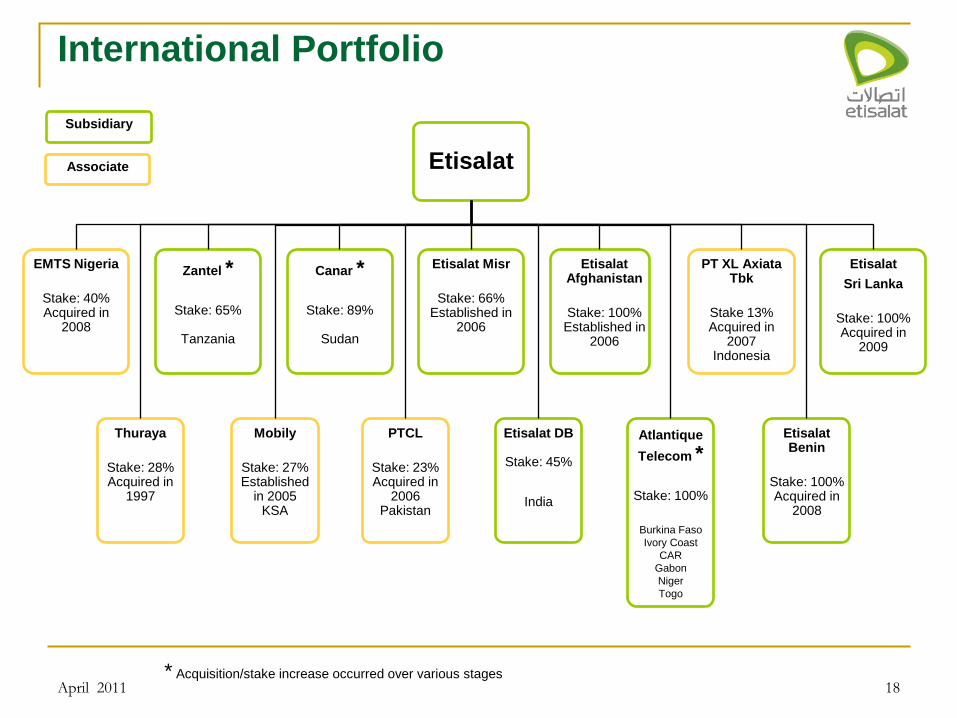

International Portfolio

Etisalat

EMTS Nigeria

Stake: 40%Acquired in

2008

Thuraya

Stake: 28%Acquired in

1997

Zantel *

Stake: 65%

Tanzania

Mobily

Stake: 27%Established

in 2005KSA

Canar *

Stake: 89%

Sudan

PTCL

Stake: 23%Acquired in

2006Pakistan

Etisalat Misr

Stake: 66%Established in

2006

Etisalat DB

Stake: 45%

India

Etisalat Afghanistan

Stake: 100%Established in

2006

Atlantique

Telecom *

Stake: 100%

Burkina Faso

Ivory Coast

CAR

Gabon

Niger

Togo

PT XL AxiataTbk

Stake 13%Acquired in

2007Indonesia

Etisalat Benin

Stake: 100%Acquired in

2008

Etisalat

Sri Lanka

Stake: 100%Acquired in

2009

* Acquisition/stake increase occurred over various stages

Associate

Subsidiary

April 2011

19

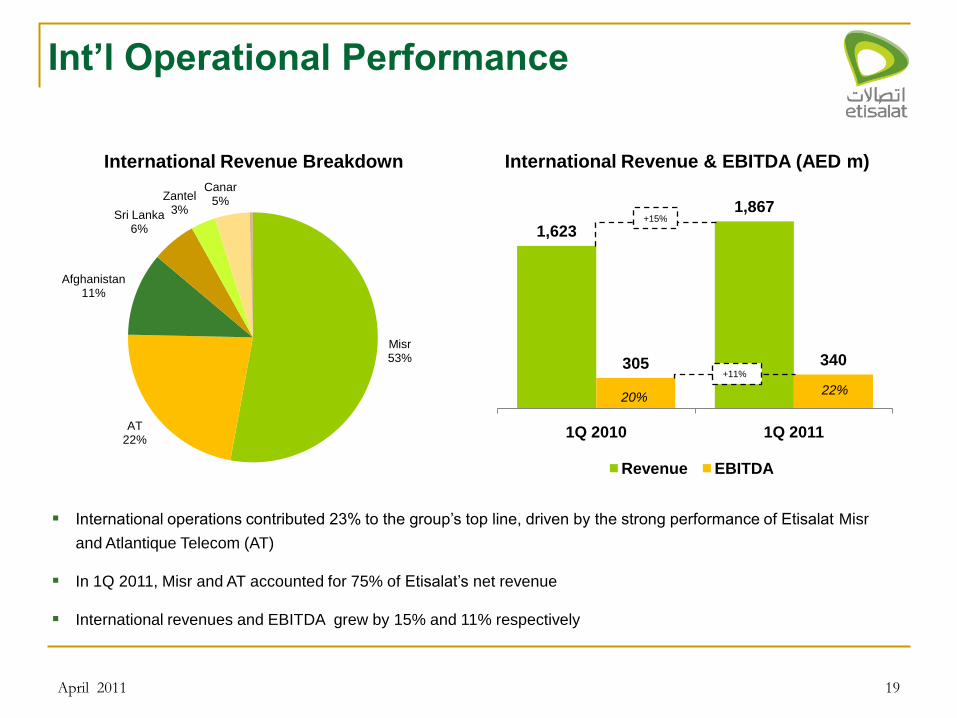

Int‟l Operational Performance

International operations contributed 23% to the group’s top line, driven by the strong performance of Etisalat Misr

and Atlantique Telecom (AT)

In 1Q 2011, Misr and AT accounted for 75% of Etisalat’s net revenue

International revenues and EBITDA grew by 15% and 11% respectively

International Revenue Breakdown International Revenue & EBITDA (AED m)

Misr53%

AT22%

Afghanistan11%

Sri Lanka6%

Zantel3%

Canar5%

1,623

1,867

305 340

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

1Q 2010 1Q 2011

Revenue EBITDA

+15%

+11%

20%22%

April 2011

16,720

20,718

0

5,000

10,000

15,000

20,000

25,000

1Q 2010 1Q 2011

20

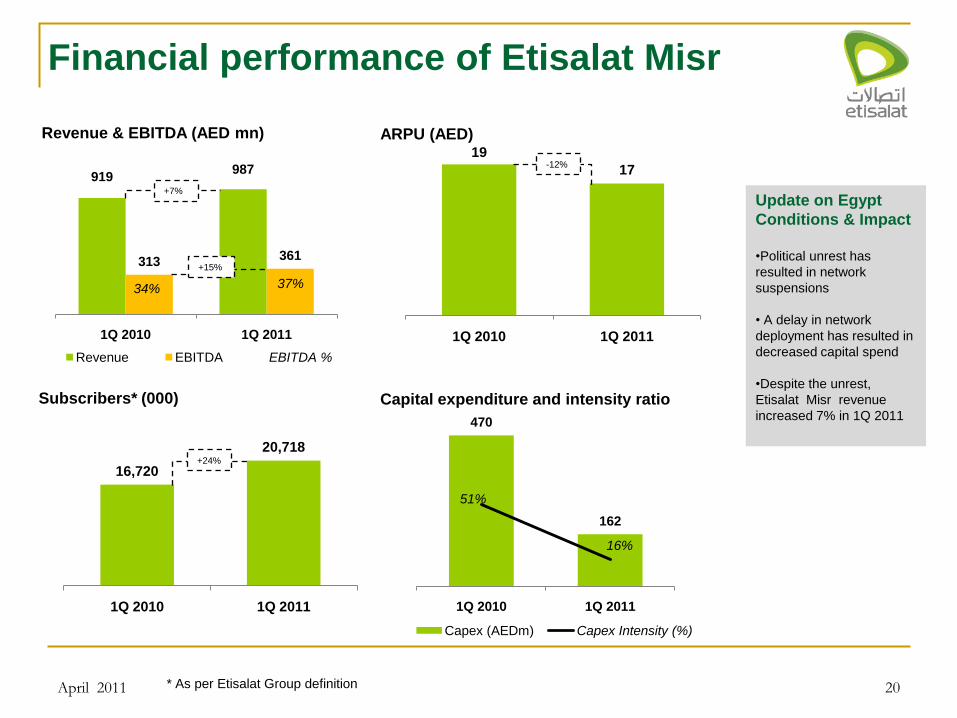

Financial performance of Etisalat Misr

919 987

313 361

34% 37%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

200

400

600

800

1,000

1,200

1Q 2010 1Q 2011

Revenue EBITDA EBITDA %

Revenue & EBITDA (AED mn) ARPU (AED)

Subscribers* (000) Capital expenditure and intensity ratio

19

17

0

2

4

6

8

10

12

14

16

18

20

1Q 2010 1Q 2011

470

162

51%

16%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

50

100

150

200

250

300

350

400

450

500

1Q 2010 1Q 2011

Capex (AEDm) Capex Intensity (%)

+7%

-12%

+24%

+15%

April 2011

Update on Egypt

Conditions & Impact

•Political unrest has

resulted in network

suspensions

• A delay in network

deployment has resulted in

decreased capital spend

•Despite the unrest,

Etisalat Misr revenue

increased 7% in 1Q 2011

* As per Etisalat Group definition

369 419

62 74

17% 18%0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

50

100

150

200

250

300

350

400

450

1Q 2010 1Q 2011

Revenue EBITDA EBITDA %

21

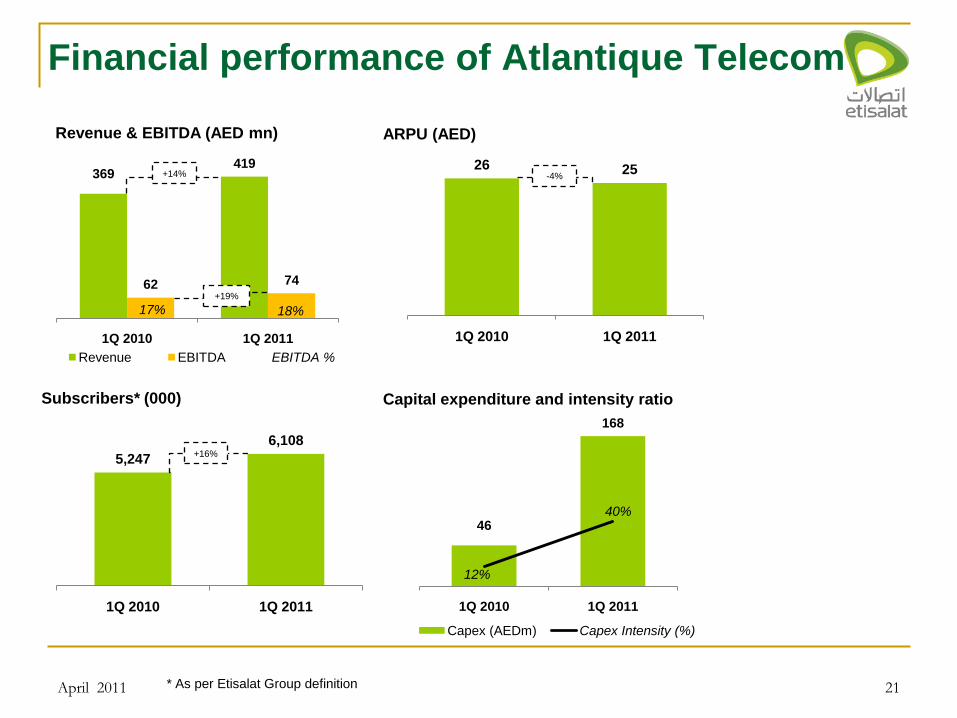

Financial performance of Atlantique Telecom

Revenue & EBITDA (AED mn) ARPU (AED)

Subscribers* (000) Capital expenditure and intensity ratio

26 25

0

5

10

15

20

25

30

1Q 2010 1Q 2011

46

168

12%

40%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

20

40

60

80

100

120

140

160

180

1Q 2010 1Q 2011

Capex (AEDm) Capex Intensity (%)

+14% -4%

5,247

6,108

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

1Q 2010 1Q 2011

+16%

+19%

April 2011 * As per Etisalat Group definition

22

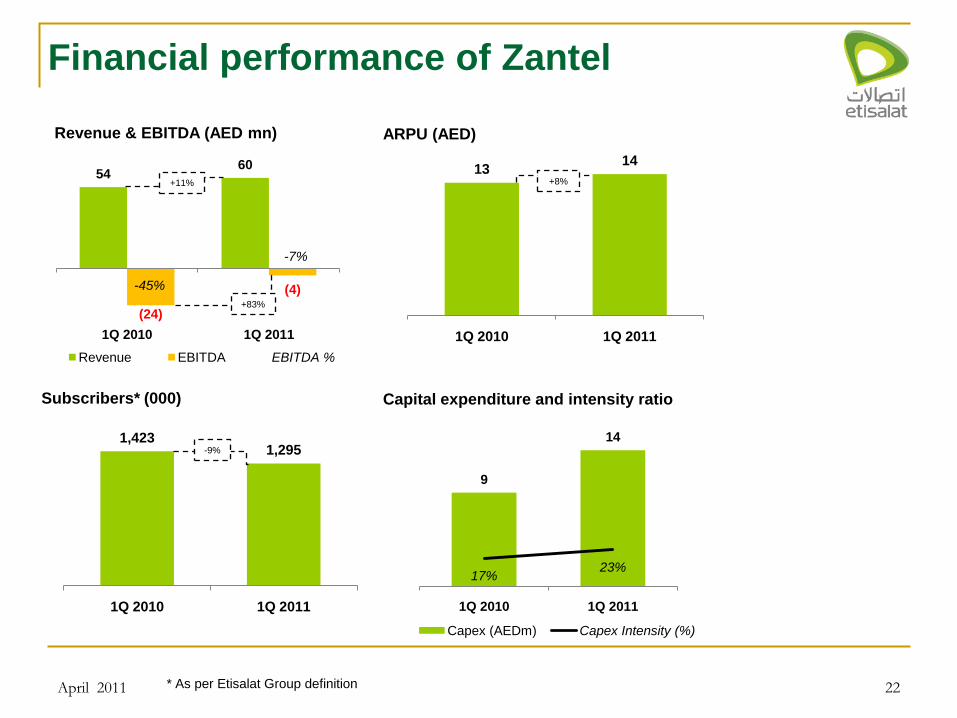

Financial performance of Zantel

1,423 1,295

0

200

400

600

800

1,000

1,200

1,400

1,600

1Q 2010 1Q 2011

54 60

(24)

(4)-45%

-7%

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

-30

-20

-10

0

10

20

30

40

50

60

70

1Q 2010 1Q 2011

Revenue EBITDA EBITDA %

Revenue & EBITDA (AED mn) ARPU (AED)

Subscribers* (000) Capital expenditure and intensity ratio

1314

0

2

4

6

8

10

12

14

16

1Q 2010 1Q 2011

+11% +8%

-9%

9

14

17%23%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

2

4

6

8

10

12

14

16

1Q 2010 1Q 2011

Capex (AEDm) Capex Intensity (%)

+83%

April 2011 * As per Etisalat Group definition

23

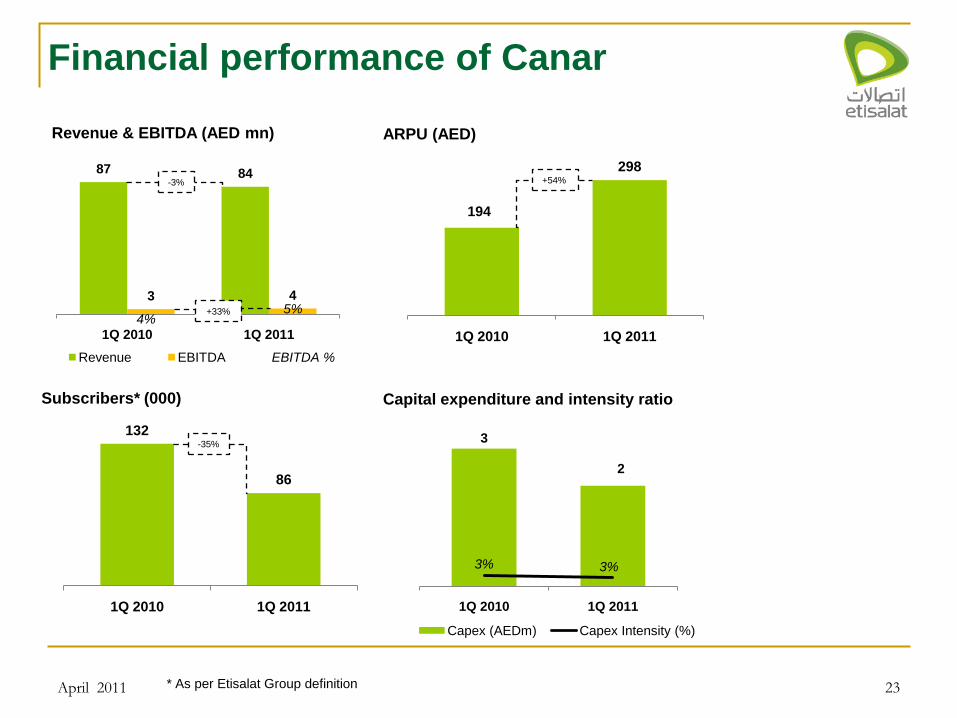

Financial performance of Canar

132

86

0

20

40

60

80

100

120

140

1Q 2010 1Q 2011

87 84

3 4

4%5%

-5%

15%

35%

55%

75%

95%

0

10

20

30

40

50

60

70

80

90

100

1Q 2010 1Q 2011

Revenue EBITDA EBITDA %

Revenue & EBITDA (AED mn) ARPU (AED)

Subscribers* (000) Capital expenditure and intensity ratio

194

298

0

50

100

150

200

250

300

350

1Q 2010 1Q 2011

-3% +54%

-35%3

2

3% 3%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

0

1

1

2

2

3

3

4

1Q 2010 1Q 2011

Capex (AEDm) Capex Intensity (%)

+33%

April 2011 * As per Etisalat Group definition

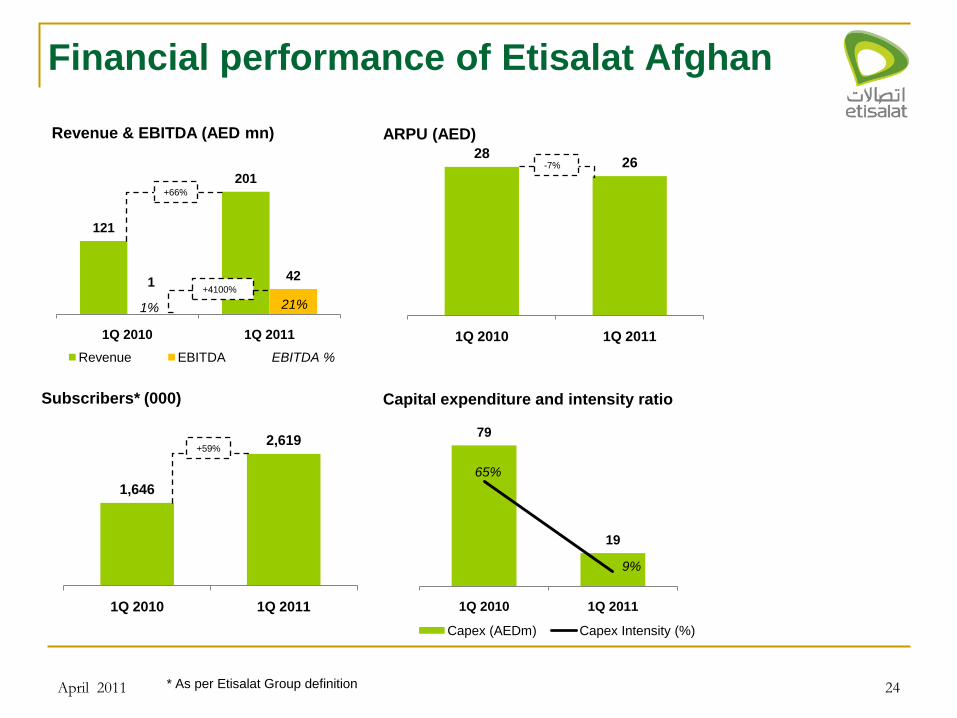

24

Financial performance of Etisalat Afghan

1,646

2,619

0

500

1,000

1,500

2,000

2,500

3,000

1Q 2010 1Q 2011

121

201

1 42

1% 21%0%

5%

10%

15%

20%

25%

0

50

100

150

200

250

1Q 2010 1Q 2011

Revenue EBITDA EBITDA %

Revenue & EBITDA (AED mn) ARPU (AED)

Subscribers* (000) Capital expenditure and intensity ratio

2826

0

5

10

15

20

25

30

1Q 2010 1Q 2011

+66%

-7%

+59%

79

19

65%

9%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

10

20

30

40

50

60

70

80

90

1Q 2010 1Q 2011

Capex (AEDm) Capex Intensity (%)

+4100%

April 2011 * As per Etisalat Group definition

74

108

9

24

12%22%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

20

40

60

80

100

120

1Q 2010 1Q 2011

Revenue EBITDA EBITDA %

25

Financial performance of Etisalat Sri Lanka

2,547

3,406

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

1Q 2010 1Q 2011

Revenue & EBITDA (AED mn) ARPU (AED)

Subscribers* (000) Capital expenditure and intensity ratio

10 11

0

2

4

6

8

10

12

1Q 2010 1Q 2011

April 2011

+34%

+10%+46%

+167%

16

57

21%

53%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

10

20

30

40

50

60

70

1Q 2010 1Q 2011

Capex (AEDm) Capex Intensity (%)

* As per Etisalat Group definition

26

5. Key Takeaways

April 2011

27

Key Takeaways

April 2011

Maintained revenue growth due to Etisalat’s diversified geographic and product

portfolio

Despite competitive pressure, Etisalat UAE posted high operating margins after

royalties

Etisalat UAE is witnessing rebalancing of its product portfolio with mobile to Internet &

data revenue substitution

Continue to address cost optimization in the UAE operation

International operations to lead growth

Maintained a robust financial position with flexibility to potentially finance future

acquisitions

28

Q&A

April 2011