empirical and behavioural finance

DESCRIPTION

Behavioural FinanceTheoriesFinanceTRANSCRIPT

Chapter 9 – Empirical Evidence on Exchange Rates

9.1 – Intro

9.2 – What is an Efficient Market?

Following Eugene Fama (1970), an efficient market is conventionally defined as one in which prices always fully reflect available information.

In the specific application to the foreign exchange market, this implies that market participants use all relevant available information bearing on the appropriate value of the exchange rate to produce a set of exchange rates – spot and forward – that does not provide an opportunity for unusual ex ante profit opportunities.

o In other words, unusual profit cannot be made by speculators who make exchange rate forecasts on a similar information set.

Two concerns: (1) Is new information instantaneously and fully reflected in the exchange rate? (2) What is relevant and what is irrelevant information?

Page 201

Problem with exchange market efficiency tests: Even if one were to discover that the forward rate systematically over or underpredicted the future

spot rate, this discrepancy is not necessarily a sign of foreign exchange market inefficiency – It could be indicative of the existence of a risk premium in the foreign exchange market.

If the forward rate of a currency were systematically to underpredict its future spot exchange rate, as in the example above, this may be due to the existence of a positive risk premium attached to the foreign currency.

In the example above: The difference between the forward rate £0.60/$1 and the actual/expected future spot rate of

£0.63/$1 may be viewed as a £0.03 risk premium on the dollar.o In other words, speculators will only buy dollars forward if they expect to be able to sell

them in the future and make £0.03 profit.o This profit represents the compensation required by speculators to buy dollars forward

which are regarded as more risky than pounds.

Any expected excess profits to be earned on buying the foreign currency forward are merely the compensation required by n efficient foreign exchange market to compensate for the risks associated with holding the foreign currency forward.

If the forward exchange rate of the foreign currency is systematically under valued in relation to the future spot exchange rate, this may be evidence of the existence of a positive risk premium attached to the foreign currency.

o That is, international investors require a higher expected return on the foreign currency as compared to the domestic currency because they regard it as a relatively risky asset to hold compared to the domestic currency.

A positive risk premium on the foreign currency corresponds to a negative risk premium on the domestic currency, and vice versa.

9.3 – Exchange Market Efficiency Tests

(Levich/Frankel regression)

According to this test, if the foreign exchange market is efficient in the sense that the exchange rate (spot and forward) incorporates all currently available information and there is no risk premium in the foreign exchange market.

o If this is the case, then the forward rate will be an unbiased predictor of the future spot exchange rate.

o The expected sign of a1, therefore, is zero (a1 = 0). If a1 was non-zero then the forward exchange rate would systematically over or underpredict the

future spot exchange rate and rational economic agents could use this information to make systematic profits.

The coefficient a2 will be equal to unity (a2 = 1) showing that the forward exchange rate on average correctly predicts the future spot exchange rate.

The error term (ut) will possess OLS properties and will be serially uncorrelated.o No serial correlation implies that there is no statistically significant relationship between

the errors of one period and errors made in other periods.o One cannot forecast future errors on the basis of past errors – if agents could predict

future errors on the basis of past errors, this would be a sign of foreign exchange market inefficiency, which would suggest the presence of unexploited profit opportunities.

Results of tests in table 9.1 on page 204.

The regression (equation 9.6) is inappropriate if exchange rates follow a non-stationary process – that is, there is some trend exchange rate appreciation or depreciation.

o It is thus necessary to detrend the data in order for the regression estimates to be unbiased.

Cumby and Obstfied – equation (9.7) on page 204.

Equation (9.7) states that a currency that is at a forward discount (ft – st) of x% should on average depreciate by x%, whereas a currency that is at a forward premium (ft – st) of x% should on average appreciate by x%.

If the foreign exchange market is efficient and characterised by rational expectations, so that we can substitute the actual exchange rate for the expected exchange rate, along with the assumption that there is no risk premium, one would again expect a1 to be zero and the coefficient a2 not to differ significantly from unit, indicating that, on average, the realised change in the exchange rate is correctly forecasted by the forward premium/discount.

Results of equation (2.7) suggest that, on average, currencies that were at a forward discount actually appreciated, while those at a forward premium actually depreciated.

This is a clear rejection of the joint market efficiency test because it suggests that there exists a fairly simple rule for investors to make excessive profits – simply put your money in a currency that is at a forward discount (because of the relatively high interest rate in that country) and you

will not only benefit from the higher interest rate but also an exchange rate appreciation. This is a clear violation of UIP.

Problem with decisive rejections: joint test of exchange market efficiency (rational expectations) and the non-existence of a risk premium => no clear-cut interpretation.

o It may be evidence of exchange market inefficiency (REH does not hold) or be indicative of the existence of a risk premium in the foreign exchange market means that we cannot gain a clear-cut interpretation.

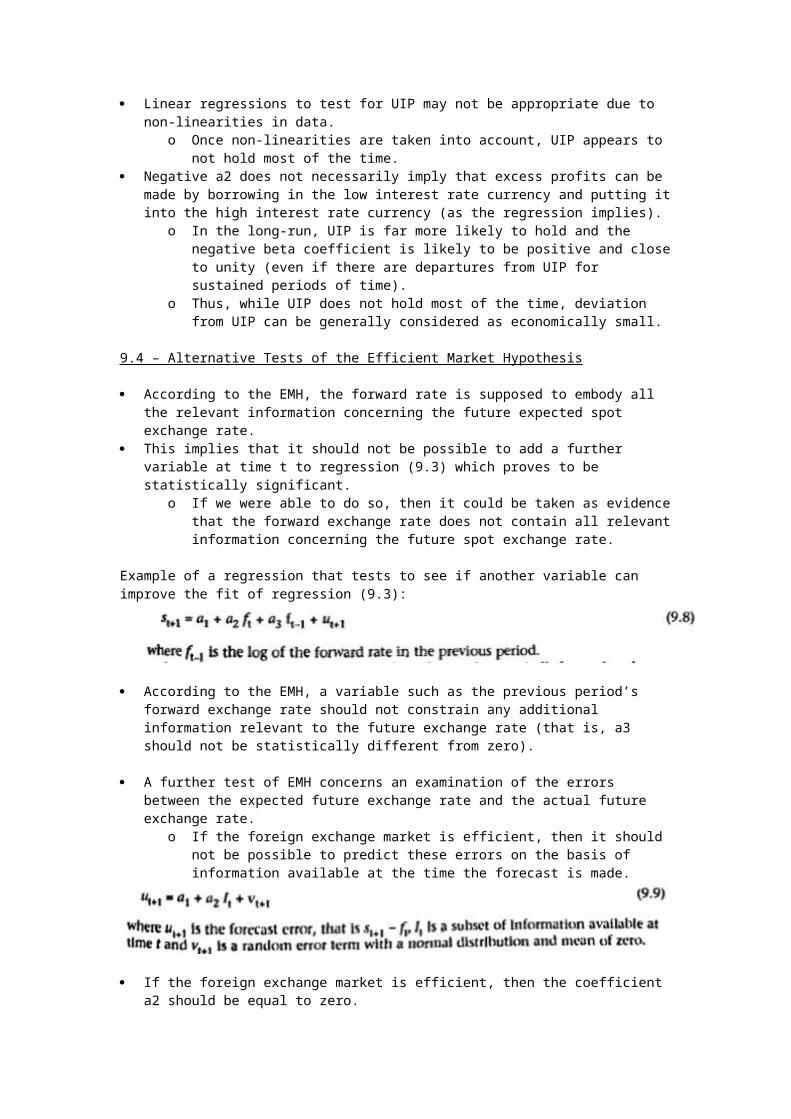

Called-forward discount puzzle. Linear regressions to test for UIP may not be appropriate due to non-linearities in data.

o Once non-linearities are taken into account, UIP appears to not hold most of the time. Negative a2 does not necessarily imply that excess profits can be made by borrowing in the low

interest rate currency and putting it into the high interest rate currency (as the regression implies).o In the long-run, UIP is far more likely to hold and the negative beta coefficient is likely to

be positive and close to unity (even if there are departures from UIP for sustained periods of time).

o Thus, while UIP does not hold most of the time, deviation from UIP can be generally considered as economically small.

9.4 – Alternative Tests of the Efficient Market Hypothesis

According to the EMH, the forward rate is supposed to embody all the relevant information concerning the future expected spot exchange rate.

This implies that it should not be possible to add a further variable at time t to regression (9.3) which proves to be statistically significant.

o If we were able to do so, then it could be taken as evidence that the forward exchange rate does not contain all relevant information concerning the future spot exchange rate.

Example of a regression that tests to see if another variable can improve the fit of regression (9.3):

According to the EMH, a variable such as the previous period’s forward exchange rate should not constrain any additional information relevant to the future exchange rate (that is, a3 should not be statistically different from zero).

A further test of EMH concerns an examination of the errors between the expected future exchange rate and the actual future exchange rate.

o If the foreign exchange market is efficient, then it should not be possible to predict these errors on the basis of information available at the time the forecast is made.

If the foreign exchange market is efficient, then the coefficient a2 should be equal to zero. This efficiency test is known as the ‘orthogonality property’ and implies that agents use all

relevant information in making their forecasts so as to avoid predictable forecast errors. The EMH holds that the forecast error ut+1 is due to unpredictable shocks and will be unrelated to

any information available at time t, where t is the previous period’s forecast errors ut.

According to the EMH, if there is no risk premium and the foreign exchange market uses all information efficiently, then a1 = 0, a2 = 0, and a3 = 1.

Other tests: proxies for the future expected exchange rate.

9.5 – Summary of Finding on Market Efficiency

Testing of foreign exchange market efficiency and the non-existence of risk premium. The problem with all these tests is that even when the joint hypothesis is rejected, there is no

means of knowing whether this is due to the existence of a risk premium or due to the failure of foreign exchange market efficiency.

Mixed results depending upon the currency and the particular test considered. Evidence suggesting that for certain periods and certain rates, the joint hypothesis does not hold. Tests of EMH using the forward premium/discount as a prediction for the future

appreciation/deprecation of the currency convincingly reject the joint hypothesis. Accepting that the joint hypothesis does not hold, the big issue left to resolve is whether or not the

rejection is due to the existence of a risk premium or the existence of inefficiency/non-rational expectations in the foreign exchange market.

Risk premium likely to be too small to account for the failure of exchange market tests.o Behaves as predicted by the portfolio balance model – it increases with the supply of

domestic bonds and decreases with the supply of foreign bonds (Frankel 1984 and Rogoff 1984)

Failure is more likely to be due to non-rational expectation in the foreign exchange market rather than the existence of a risk premium.

o Neither rational expectations nor alternative expectations hypothesis correctly specify exchange market expectations (Frankel and Froot 1987).

MacDonald and Torrance (1989) – both the existence of a risk premium and non-rational expectations are to blame.

Clarida and Taylor (1997) and Clarida et al. (2003) – there may be information in the series of forward exchange rates that is useful for predicting the future path of the spot exchange rate, suggesting non-rational use of information.

9.6 – Empirical Tests of Exchange Rate Models Pp. 209 – 210

9.7 – Exchange Rate Models: A forecasting Analysis

Pp. 210 – 214

9.8 – Explaining the Poor Results of Exchange Rate Models

Box 9.1 on page 206

9.9 – The ‘News’ Approach to Modelling Exchange Rates

An attractive feature of the news approach is that it combines the concept of exchange market efficiency with modern models of exchange rate determination.

Dornbusch (1980) and Frenkel (1982) suggested that the correct way to model exchange rate movements us to presume that the foreign exchange market is efficient implying that all ex ante profit opportunities are eliminated.

Movements in exchange rates will be due to the arrival of new information. Any difference between the forward rate and the corresponding rate that later transpires must, in an

efficient market (with no risk premium), be due to the arrival of new information.o Unanticipated exchange rate movements are due to unexpected changes in the

fundamentals.

The expected spot rate is given by the forward exchange rate in the previous period.o Use as a proxy for the unexpected change in the exchange rate we can turn to the EMH.

Results: the unexpected changes in the fundamentals (news items) were found to be significant determinants of the unexpected change in the exchange rate and the coefficients expected sign – Refer to page 218 for regression.

Some mixed results regarding the direction of exchange rates following new information – not robust across different currencies and information may be statistically significant but wrong signed.

Edwards (1983) and MacDonald (1983) – past news (lagged news terms) can have a significant effect on the unexpected exchange rate change.

o Incompatible with the concept of exchange market efficiency.

Example on page 219

Mixed empirical support.

9.10 – The Longer-Run Predictability of Exchange Rate Movements

Pp. 219 – 223

Long-run exchange rates can in large part be modelled on the basis of economic fundamentals such as the monetary model of exchange rate determination.

It is becoming a stylised fact that economic fundamentals are proving better for both modelling and forecasting the long-run exchange rate than the short-run exchange rate.

9.11 – Modelling Exchange Rate Expectations

Pp. 223 – 227

Static, adaptive, and extrapolative expectation mechanisms are somewhat arbitrary because they state that the future exchange rate can be predicted entirely on the basisi of current and past values of the exchange rate.

o No attention is paid to other information that may be relevant for the future exchange rate (e.g. domestic and foreign inflation, interest rates, fiscal and monetary policy).

Regressive expectations, rational expectations, and perfect foresight models seem better suited to dealing with exchange rates (from a theoretical viewpoint) because they all allow for economic agents to use a wider set of information.

Regressive expectation requires economic agents to form a view concerning the appropriate long-run equilibrium exchange rate.

Rational expectations suggests that although agent do not always get the exact exchange rate correct, they nevertheless do not systematically get things wrong.

The perfect foresight model implies that economic agents actually have the correct model of exchange rate determination and thereby do not make errors with regard to the future exchange rate.

o Unrealistic but the advantage of the approach is the structure of the model and not because of an arbitrary specification of exchange rate expectations.

9.12 – Empirical Tess of Different Expectations Mechanisms

Pp. 227 – 228

9.13 – Alternative Approaches to Modelling Exchange Rates: The Role of Chartists and Fundamentalists

Pp. 228 – 230

Chartists claim that certain patterns of behaviour repeat themselves and that, by detecting the relevant pattern in play, considerable success can be had in predicting the future exchange rate.

The important point about chartists is that the only information they require to predict exchange rates is the recent past behaviour of the exchange rate itself.

o Economic fundamentals are not required.

Fundamentalists argue that the best way to predict the future course of exchange rates is to look at the prospective for underlying economic fundamentals such as future interest rates, balance of payments prospects, and inflation for example.

The important thing about fundamentalist is that they believe that the foreign exchange market is efficient which means that (for them) past behaviour of the exchange rate will be of little use in predicting its course.

o What matters for the exchange rate is the prospective development of economic fundamentals.

Chartists – come up with different forecasts merely by using past movements of the exchange rate to forecast the future exchange rate.

Fundamentalists – use different exchange rate models for forecasting the future exchange rate: (1) the flexibly-price monetary model, (2) the frankel sticky-price monetary model, and (3) the portfolio balance model.

Experiment/test on page 229