end review report

TRANSCRIPT

8/18/2019 End Review Report

http://slidepdf.com/reader/full/end-review-report 1/44

1

Title:- A comparative study of housing loan and education loan of

public and private sector bank in India.

Date-29/!/2"#

2014-16$%$-%&'

(ubmitted by- (ubmitted to-

Avish )ain*2++, Dr .eha $arashar

(aarmal (aran*229,

$%$-%&' *'0$,

8/18/2019 End Review Report

http://slidepdf.com/reader/full/end-review-report 2/44

CHAPTER-1

BREIF SCOPE OF THE PROJECT:

Appraisal of Credit Proposals: Home Loans, education loan (private and public

sector bank) Tradin process

To Learn credit proposals

To Compare banks credit product

8/18/2019 End Review Report

http://slidepdf.com/reader/full/end-review-report 3/44

CHAPTER-2

LITERATURE REVIEW

Literature revie! provides available researc" !it" respect to t"e selected topic of t"e pro#ect

or t"e researc" findins b$ an aut"or !"ic" "as been done !it" respect to t"e researc"

topic. T"is c"apter provides t"e overall vie! of t"e available literature !it" respect to t"e

topic of t"e pro#ect. T"e revie! of t"e related researc" !orks are described as under:%

1&erstain 'avid (*) e+amined in "is stud$ taken from 1 to t"at in t"is period

t"ere is increasin use of "ome loans as compared to private mortae insurance (P-). He

"as divided "is stud$ into four sections.

./andell, 0err$ ' () anal$ses t"e s"arp rise and t"en suddenl$ drop do!n "ome pricesfrom t"e period 1**% . C"anes in prices are for t"e reasons as suc" economicfundamentals , t"e problem !as not subprime lendin per se, but t"e ed2s dramaticreductions, t"en increases in interest rates durin t"e earl$% mid% , t"e "ousin 3boom!as concentrated in t"ose markets !it" sinificant suppl$%side restrictions, !"ic" tend to bemore price%volatile4 "e problem !as not in t"e e+cess suppl$ of credit in areate, or t"eincrease in subprime per se, but rat"er in t"e increased or reduced presence of certain ot"er mortae products.

5.La courr, -ic"eal (6) anal$sis in "is stud$ t"e factors affected t"e increase in t"e levelof Annual percentae rates (AP7) spread reportin durin 8 over 9.T"e t"ree mainfactors are (1) c"anes in lender business practices4 () c"anes in t"e risk profile ofborro!ers4 and (5) c"anes in t"e $ield curve environment. T"e result s"o!s t"at aftercontrollin for t"e mi+ of loan t$pes, credit risk factors, and t"e $ield curve, t"ere !as nostatisticall$ sinificant increase in t"e reportable volume for loans oriinated directl$ b$lenders durin 8, t"ou" indirect, !"olesale oriinations did sinificantl$ increase.inall$, iven a model of t"e factors affectin results for 9%8, !e predict t"at

results !ill continue to s"o! an increase in t"e percentae of loans t"at are "i"er priced

!"en final numbers are released in ;eptember 6. La cour -ic"eal ()

e+amined t"e "ome purc"ase mortae product preferences of L- "ouse"olds. <b#ectives

of "is stud$ !ere to anal$sis t"e factors t"at determined t"eir c"oice of mortae product.

T"e role pricin and product substitution pla$ in t"is sement of t"e market and do results

var$ !"en loans are oriinated t"rou" mortae brokers= or t"is t"e$ "ave use t"e

reression anal$sis and results t"at "i" interest risk reduces loan value.

9.'r. 7anara#an C. (1) said t"at t"e financial s$stem of ndia built a vast net!ork offinancial institutions and markets over times and t"e sector is dominated b$ bankin sector !"ic" accounts for about t!o%t"ird of t"e assets of orani>ed financial sector.

8.Haavio, 0auppi () stated t"at countries !"ere a lare proportion of t"e population livesin o!ner? occupied "ousin is e+periencin "i"er unemplo$ment rates. T"an countries!"ere t"e ma#orit$ of people live in private rental "ousin, !"ic" mi"t suest t"at rental"ousin en"ances labour mobilit$. n t"is paper, t"e$ develop a simple inter temporal t!oreion model t"at allo! us to compare o!ner occupied "ousin markets to rental marketsand to anal$>e "o! t"ese alternative arranements allocate people in space and time. Announced t"at it !ill offer loans for 7s. %1 lak" at 1.8 percent t"e lo!est rate

8/18/2019 End Review Report

http://slidepdf.com/reader/full/end-review-report 4/44

offered b$ an$ "ousin finance provider, bi brot"er ;& "as taken t"e rate !ar in t"e "ome

loans cateor$ to ne! "ei"ts. @arasim"am Committee (1**1) points out t"at alt"ou" t"e

bankin s$stem in our countr$ "as made rapid proress durin t"e last t!o decades, t"ere

is decline in productivit$ and efficienc$ and erosion of profitabilit$.

.Collee e+perience and success variables are t"ose t"at occur in collee and !"ic" t"e

collee, t"e borro!er, or bot" "ave some abilit$ to affect. T"ese c"aracteristics include

collee ma#or, academic ac"ievement, transfer status, educational oals of t"e student,

financial support, and deree completion (/olk!ein et al. 1**).

6.T"e reason for t"e correlation bet!een collee success and default be"avior is unkno!n4

"o!ever, it is possible t"at t"e "ard !ork and responsibilit$ t"at result in collee success are

establis"ed "abits t"at carr$ over to ot"er responsibilities in students lives, suc" as loanrepa$ment. Also, borro!ers !"o ac"ieve success in collee !ill most likel$ obtain better

positions in t"e #ob market and be in a better position to repa$ t"eir loans after t"e$ leave

sc"ool (;teiner and Tes>ler 5).

8/18/2019 End Review Report

http://slidepdf.com/reader/full/end-review-report 5/44

CHAPTER-3

BANKING INDUSTRY ANALYSIS

T"e &ankin industr$ comprises of sements t"at provide financial assistance and advisor$

services to its customers b$ means of varied functions suc" as commercial bankin,!"olesale bankin, personal bankin, internet bankin, mobile bankin, credit unions,

investment bankin and t"e like.

Bit" $ears, banks are also addin services to t"eir customers. T"e ndian bankin industr$

is passin t"rou" a p"ase of customers market. T"e customers "ave more c"oices in

c"oosin t"eir banks. A competition "as been establis"ed !it"in t"e banks operatin in

ndia.

Bit" stiff competition and advancement of tec"nolo$, t"e services provided b$ banks "ave

become more eas$ and convenient. T"e past da$s are !itness to an "our !ait before

!it"dra!in cas" from accounts or a c"eue from nort" of t"e countr$ bein cleared in one

mont" in t"e sout".

&anks are amon t"e main participants of t"e financial s$stem in ndia. &ankin offers

several facilities D <pportunities. T"is section provides compre"ensive and updated

information, uidance and assistance in all areas of bankin in ndia.

&ank of Hindustan, set up in 16, !as t"e earliest ndian &ank . &ankin in ndia on

modern lines started !it" t"e establis"ment of t"ree presidenc$ banks under Presidenc$

&ankEs act 16 i.e. &ank of Calcutta, &ank of &omba$ and &ank of -adras.

T"e commercial bankin structure in ndia consists of: ;c"eduled Commercial &anks D

Fnsc"eduled &anks. &ankin 7eulation Act of ndia, 1*9* defines &ankin as Gacceptin,

for t"e purpose of lendin or investment of deposits of mone$ from t"e public, repa$able on

demand or ot"er!ise and !it"dra!able b$ c"eues, draft, order or ot"er!ise.G

T"e arrival of forein and private banks !it" t"eir superior state%of%t"e%art tec"nolo$%based

services pus"ed ndian &anks also to follo! suit b$ oin in for t"e latest tec"noloies so as

to meet t"e t"reat of competition and retain customer base.

T"e evolution of T services outsourcin in t"e ndian banks "as presentl$ moved on to t"elevel of acilities -anaement (-). &anks no! lookin at business process manaement

(&P-) to increase returns on investment, improve customer relations"ip manaement

(C7-) and emplo$ee productivit$.

or, t"ese entities sustainin lon%term customer relations"ip manaement (C7-) "as

become a c"allene !it" almost ever$one in t"e market !it" similar products.

8/18/2019 End Review Report

http://slidepdf.com/reader/full/end-review-report 6/44

3.1-His!"i#$% B$#&'"!()*

T"e first bank in ndia, t"ou" conservative, !as establis"ed in 16. rom 16 till toda$,

t"e #ourne$ of ndian &ankin ;$stem can be sereated into t"ree distinct p"ases. T"e$ are

as mentioned belo!:

PHA;I ? Iarl$ p"ase from 16 to 1** of ndian &anks

PHA;I ? @ationali>ation of ndian &anks and up to 1**1

PHA;I ? ndian inancial D &ankin ;ector 7eforms after 1**1.

PHASE I:

T"e Jeneral &ank of ndia !as set up in t"e $ear 16. @e+t came &ank of Hindustan and

&enal &ank. T"e Iast ndia Compan$ establis"ed &ank of &enal (1*), &ank of &omba$

(19) and &ank of -adras (195) as independent units and called it Presidenc$ &anks.

T"ese t"ree banks !ere amalamated in 1* and mperial &ank of ndia !as establis"ed

!"ic" started as private s"are"olders banks, mostl$ Iuropeans s"are"olders. 'urin t"e

first p"ase t"e ro!t" !as ver$ slo! and banks also e+perienced periodic failures bet!een

1*15 and 1*9. T"ere !ere appro+imatel$ 11 banks, mostl$ small. To streamline t"e

functionin and activities of commercial banks, t"e Jovernment of ndia came up !it" T"e

&ankin Companies Act, 1*9* !"ic" !as later c"aned to &ankin 7eulation Act 1*9* asper amendin Act of 1*8 (Act @o. 5 of 1*8). 7eserve &ank of ndia !as vested !it"

e+tensive po!ers for t"e supervision of bankin in ndia as t"e Central &ankin Aut"orit$.

'urin t"ose da$s public "as lesser confidence in t"e banks. As an aftermat" deposit

mobili>ation !as slo!. Abreast of it t"e savins bank facilit$ provided b$ t"e Postal

department !as comparativel$ safer. -oreover, funds !ere larel$ iven to t"e traders.

PHASE II:

Jovernment took ma#or steps in t"is ndian &ankin ;ector 7eform after independence. n

1*88, it nationali>ed mperial &ank of ndia !it" e+tensive bankin facilities on a lare scale

especiall$ in rural and semi%urban areas. ;econd p"ase of nationali>ation ndian &ankin

;ector 7eform !as carried out in 1* !it" seven more banks. T"is step brou"t K of t"e

bankin sement in ndia under Jovernment o!ners"ip.

T"e follo!in are t"e steps taken b$ t"e Jovernment of ndia to 7eulate &ankin

nstitutions in t"e Countr$:

1*9*: Inactment of &ankin 7eulation Act.

1*88: @ationali>ation of ;tate &ank of ndia.

1*8*: @ationali>ation of ;& subsidiaries.

1*1: nsurance cover e+tended to deposits.

8/18/2019 End Review Report

http://slidepdf.com/reader/full/end-review-report 7/44

8/18/2019 End Review Report

http://slidepdf.com/reader/full/end-review-report 8/44

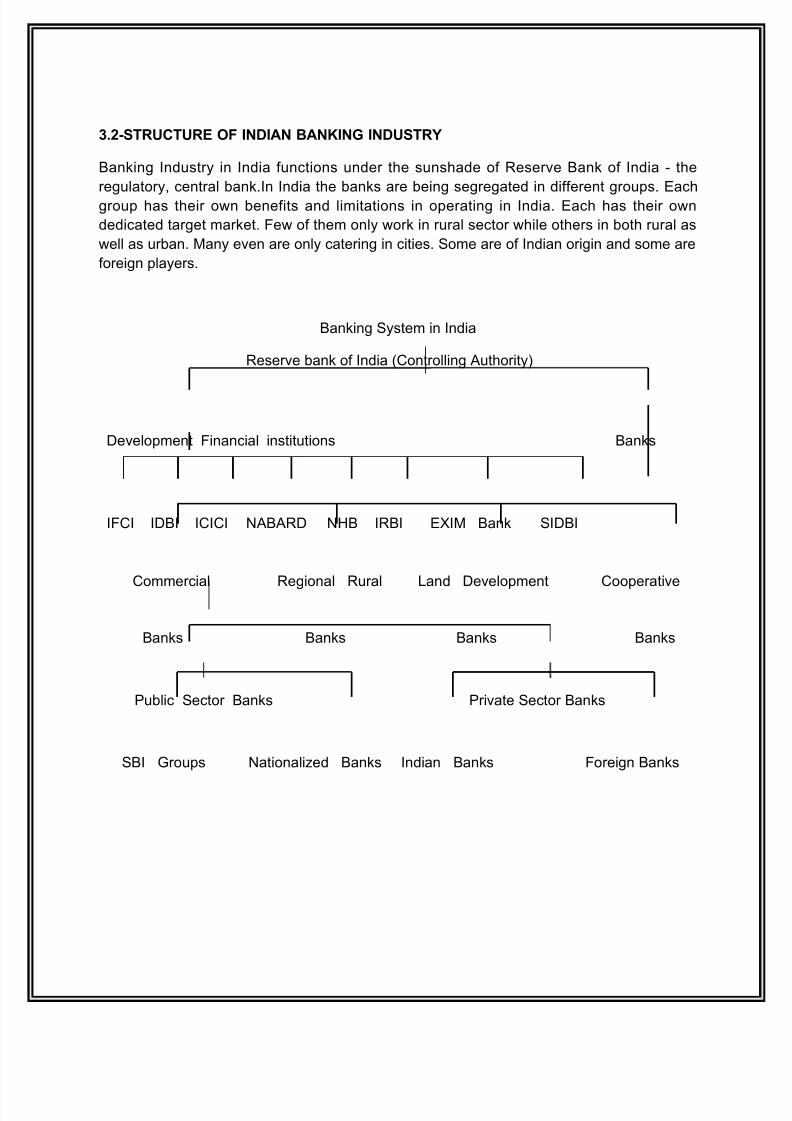

3.2-STRUCTURE OF INDIAN BANKING INDUSTRY

&ankin ndustr$ in ndia functions under t"e suns"ade of 7eserve &ank of ndia % t"e

reulator$, central bank.n ndia t"e banks are bein sereated in different roups. Iac"

roup "as t"eir o!n benefits and limitations in operatin in ndia. Iac" "as t"eir o!n

dedicated taret market. e! of t"em onl$ !ork in rural sector !"ile ot"ers in bot" rural as

!ell as urban. -an$ even are onl$ caterin in cities. ;ome are of ndian oriin and some are

forein pla$ers.

&ankin ;$stem in ndia

7eserve bank of ndia (Controllin Aut"orit$)

'evelopment inancial institutions &anks

C '& CC @A&A7' @H& 7& I- &ank ;'&

Commercial 7eional 7ural Land 'evelopment Cooperative

&anks &anks &anks &anks

Public ;ector &anks Private ;ector &anks

;& Jroups @ationali>ed &anks ndian &anks orein &anks

8/18/2019 End Review Report

http://slidepdf.com/reader/full/end-review-report 9/44

3.3-P(+%i# S,#!" B$)&s

Public sector banks are t"ose banks !"ic" are o!ned b$ t"e Jovernment. T"e Jovt. runs

t"ese &anks. n ndia 19 banks !ere nationali>ed in 1** D in 1* anot"er banks !ere

also nationali>ed. T"erefore in 1* t"e number of nationali>ed bank . At present t"ere

are total Public ;ector &anks in ndia (As on %*%*). <f t"ese 1* are nationalised

banks, (;TATI &A@0 < @'<7I AL;< -I7JI' 7ICI@TLM) belon to ;& D

associates roup and 1 bank ('& &ank) is classified as ot"er public sector bank. Belfare is

t"eir primar$ ob#ective.

Almost K of t"e business are still controlled b$ Public ;ector &anks (P;&s). P;&s are still

dominatin t"e commercial bankin s$stem. ;"ares of t"e leadin P;&s are alread$ listed

on t"e stock e+c"anes

Nationalised banks

• Alla"abad &ank

• And"ra &ank• &ank <f &aroda• &ank <f ndia•

&ank <f -a"arastra• Canara &ank• Central &ank <f ndia• Corporation &ank• 'ena &ank• ndian &ank• ndian <verseas &ank

• <riental &ank <f Commerce

• Pun#ab D ;ind &ank• Pun#ab @ational &ank•

;$ndicate &ank• FC< &ank• Fnion &ank <f ndia• Fnited &ank <f ndia• /i#a$a &ank

Other

Public

Secto

r

Banks

IDBI(ndustrial

'evelopment

&ank <f

ndia)Ltd.

SBI & its Associates

;tate &ank of ndia

;tate &ank of H$derabad

;tate &ank of -$sore

;tate &ank of Patiala

;tate &ank of Travancore

;tate &ank of &ikaner And Naipur

(;tate &ank of ;aurastra mered !it"

;& in t"e $ear and ;tate &ank of

ndore n 1)

8/18/2019 End Review Report

http://slidepdf.com/reader/full/end-review-report 10/44

1

3.-P"i$, S,#!" B$)&s

T"e 7& "as iven licenses to ne! private sector banks as part of t"e liberalisation process.

T"ese banks are o!ned and run b$ t"e private sector. /arious banks in t"e countr$ suc" as

CC &ank, H'C &ank etc. An individual "as control over t"ere banks in preparation to t"e

s"are of t"e banks "eld b$ "im.

Private bankin in ndia !as practiced since t"e beinnin of bankin s$stem in ndia. T"e

first private bank in ndia to be set up in Private ;ector &anks in ndia !as ndusnd &ank. t

is one of t"e fastest ro!in &ank Private ;ector &anks in ndia. '& ranks t"e tent" larest

development bank in t"e !orld as Private &anks in ndia and "as promoted !orld class

institutions in ndia.

T"e first Private &ank in ndia to receive an in principle approval from t"e 7eserve &ank of

ndia !as Housin 'evelopment inance Corporation Limited, to set up a bank in t"e private

sector banks in ndia as part of t"e 7&Es liberali>ation of t"e ndian &ankin ndustr$. t !as

incorporated in Auust 1**9 as H'C &ank Limited !it" reistered office in -umbai and

commenced operations as ;c"eduled Commercial &ank in Nanuar$ 1**8. @J /$s$a, $et

anot"er Private &ank of ndia !as incorporated in t"e $ear 1*5

Private sector banks "ave been subdivided into follo!in cateories:%

Old Private Sector Banks

•

&ank of 7a#ast"an Ltd.• Cat"olic ;$rian &ank Ltd.• Cit$ Fnion &ank Ltd.• '"analaks"mi &ank Ltd.• ederal &ank Ltd.• @J /$s$a &ank Ltd.

• Nammu and 0as"mir &ank Ltd.• 0arnataka &ank Ltd.• 0arur /$s$a &ank Ltd.• Laks"mi /ilas &ank Ltd.• @ainital &ank Ltd.•

7atnakar &ank Ltd.• ;& Commercial and nternational

&ank Ltd.• ;out" ndian &ank Ltd.• Tamilnad -ercantile &ank Ltd.• Fnited Bestern &ank Ltd.

New Private Sector Banks

• &ank of Pun#ab Ltd. (since mered!it" Centurian &ank)

• Centurian &ank of Pun#ab (sincemered !it" H'C &ank)

• 'evelopment Credit &ank Ltd.• H'C &ank Ltd.• CC &ank Ltd.• ndusnd &ank Ltd.• 0otak -a"indra &ank Ltd.• A+is &ank (earlier FT &ank)• Mes &ank Ltd.

8/18/2019 End Review Report

http://slidepdf.com/reader/full/end-review-report 11/44

11

3./-G"!0 ",)*s

T"e ro!t" of bankin in t"e comin $ears is likel$ to be more ualitative t"an uantitative,

accordin to t"e report. &ased on t"e pro#ections made in t"e Gndia /ision G prepared

b$ t"e Plannin Commission and t"e 'raft 1t" Plan, t"e report forecasts t"at t"e pace of

e+pansion in t"e balance%s"eets of banks is likel$ to decelerate

T"e ndian bankin market is ro!in at an astonis"in rate, !it" assets e+pected to reac"

F;O1.8 trillion b$ 19. An e+pandin econom$, middle class, and tec"noloical innovations

are all contributin to t"is ro!t". T"e countr$s middle class accounts for over 58 million

people. n correlation !it" t"e ro!t" of t"e econom$, risin income levels, increased

standard of livin, and affordabilit$ of bankin products are promisin factors for continued

e+pansion. T"e ndian bankin ndustr$ is in t"e middle of an T revolution, focusin on t"e

e+pansion of retail and rural bankin. Pla$ers are becomin increasinl$ customer%centric in

t"eir approac", !"ic" "as resulted in innovative met"ods of offerin ne! bankin products

and services. &anks are no! reali>in t"e importance of bein a bi pla$er and are

beinnin to focus t"eir attention on merers and acuisitions to take advantae of economies of scale andor compl$ !it" &asel reulation. ndian bankin industr$ assets

are e+pected to reac" F;O1.8 trillion b$ 19 and are poised to receive a reater infusion of

forein capital. T"e bankin industr$ s"ould focus on "avin a small number of lare pla$ers

t"at can compete loball$ rat"er t"an "avin a lare number of framented pla$ers.

3.-L,'$% R,'(%$!"4 Iss(,s R,%$,* T! B$)&i)'

&anks !orks under various leal frame!orks most important of t"em are, t"e &ankin

reulation act 1*9*, &asel norms, 7& act, @eotiable nstruments act.

&ankin 7eulation Act 1*9*

T"e bankin reulation act !as passed as bankin companies act and it came into force in

159*. ;ubseuentl$ it !as c"aned to &ankin reulation act on 15.

&A;IL @orms

&asel is t"e second of t"e &asel accords !"ic" are recommendation on t"e bankin la!s

and reulations issued b$ bankin committee on bankin supervision. T"e purpose of &asel

norms is to create international standards t"at bankin reulators can use !"en creatin

reulations about "o! muc" capital does banks needs to put aside to uard aainst t"e

t$pes of financial and operational risks banks face. Advocates of &asel believe t"at suc"

an international s$stem can "elp protect t"e international financial s$stem from man$ t$pes

of problem t"at arise s"ould a bank or a series of banks collapse. n practice &asel

attempts to accomplis" t"is b$ settin up riorous risks and capital manaement

8/18/2019 End Review Report

http://slidepdf.com/reader/full/end-review-report 12/44

reuirement desined to ensure t"at t"e banks "old capital reserves appropriate to t"e risks

t"e banks e+poses itself to t"rou" its investment and lendin practices. Jenerall$ speakin

t"is rules sa$s t"at t"e reater t"e risk t"e bank e+poses itself, t"e reater t"e capital bank

reuires to safeuard its solvenc$ and overall economic stabilit$.

3.5-O66!"()ii,s $)* C$%%,)',s 7!" P%$4,"s

T"e bar for !"at it means to be a successful pla$er in t"e sector "as been raised. our

c"allenes must be addressed before success can be ac"ieved. irst, t"e market is seein

discontinuous ro!t" driven b$ ne! products and services t"at include opportunities in

credit cards, consumer finance and !ealt" manaement on t"e retail side, and in fee%based

income and investment bankin on t"e !"olesale bankin side.

T"ese reuire ne! skills in sales D marketin, credit and operations. ;econd, banks !ill no

loner en#o$ !indfall treasur$ ains t"at t"e decade%lon secular decline in interest rates

provided. T"is !ill e+pose t"e !eaker banks. T"ird, !it" increased interest in ndia,

competition from forein banks !ill onl$ intensif$. ourt", iven t"e demorap"ic s"ifts

resultin from c"anes in ae profile and "ouse"old income, consumers !ill increasinl$

demand en"anced institutional capabilities and service levels from banks.

3.8-PEST A)$%4sis !) , B$)&i)' I)*(s"4 F$#!"s A77,#i)' , I)*(s"4:-

Political actors -onetar$ Polic$

7eulator$ rame!ork &udet D &udet -easures

C"anes in interest rates

Iconomic actors -ore savins

-ore Capital ormation

ncrease in production of oods and ;ervices %&ankin C"annels

;ocial actors ncrease in population

C"anes in lifest$le

Ias$ !a$ of lendin mone$

I+plorin bankin facilities in rural areas

Tec"noloical actors nternet &ankin

T ;ervices D -obile &ankin

Credit Cardsmprovement in efficienc$

8/18/2019 End Review Report

http://slidepdf.com/reader/full/end-review-report 13/44

PI;T Anal$sis on t"e &ankin ndustr$ Political actors Affectin t"e ndustr$:% T"e ndian bankin ndustr$ is mostl$ dependent on t"e monetar$ polic$ decided b$ t"e

7&

;tricter reulations !it" respect to capital and liuidit$ directl$ affects t"e business of

banks

&anks need to ad#ust t"eir interest rates accordinl$, !"ic" ma$ or ma$ not favor t"em

&anks are forced to lend as per t"e uidelines of 7&, t"at includes credit ro!t" in all

sectors

&udetar$ -easures announced b$ t"e overnment at t"e beinnin of ever$ financial

$ear also la$ do!n uidelines to banks to lend or accept deposits

T"e overnment can also increase credit in particular sectors suc" as increase in farm

credit, increase in infrastructure credit etc.(priorit$ lendin)

;ometimes t"e overnment ives debt !aivers to certain sections of t"e societ$ t"at need

to be ad"ered to b$ banks as !ell

PI;T Anal$sis on t"e &ankin ndustr$ Iconomic actors Affectin t"e ndustr$:% Iconomic factors in t"e countr$ also effect t"e &ankin ndustr$ bot" favorabl$ or

unfavourabl$

B"en t"e econom$ is in ood s"ape in terms of "i" per capita income, ood ariculture

"arvest and normal inflation, banks "ave an ede as people are left !it" more mone$ to

deposit t"em !it" banks T"is "elps in more capital formation as more deposits can be reali>ed

Also n t"e times of economic boom, more and more ' is brou"t into ndia t"rou"

bankin c"annels, t"at actuall$ improves business for banks and t"e

econom$ in eneral Iconomic prosperit$ encouraes lendin business for t"e banks but in

times of recession banks face tou" times to recover t"eir mone$, issue fres" credit and

@-s are lo!er too

8/18/2019 End Review Report

http://slidepdf.com/reader/full/end-review-report 14/44

PI;T Anal$sis on t"e &ankin ndustr$ ;ocial actors Affectin t"e ndustr$:%

T"e ndian bankin s$stem "as been proressin rapidl$. T"ere are still several untapped

rural markets, despite t"e lare number of banks in ndia

-an$ farmers still take loans from mone$lenders at a ver$ "i" interest rate and small%

scale industries continue to remain important for banks

Ho!ever c"anes could be e+pected in t"e near future for t"e unorani>ed sector

T"e ro!in population of ndia is a reat opportunit$ for ndian banks as a lot of people in

t"e countr$ !ant to open a bank account and develop ood savins "abits

C"anin lifest$le of t"e ndian urban population !"o !ants eas$ !a$s of financin to t"eir

desires

PI;T Anal$sis on t"e &ankin ndustr$ Tec"noloical actors Affectin ndustr$:%

ndian bankin "as been consistentl$ !orkin to!ards t"e development of tec"noloical

c"anes and its usae in its operations

Bit" t"e application of ne! and improved tec"noloies banks are e+pected to reduce

costs, time and provide "i"er customer satisfaction

nternet bankin or bankin via t"e p"one can be considered a remarkable development in

t"e bankin industr$

-obile bankin enables customers to c"eck t"eir account balance, transfer funds 9+6, bill

pa$ments, bookin of busfli"t tickets, rec"are prepaid mobile and do a lot more

effortlessl$ and securel$

&ankin t"rou" cell p"one benefits t"e banks too. t cuts do!n on t"e cost of in%person

bankin and "elps reduce "eadcount at branc"es

3.19-SWOT A)$%4sis !7 B$)&i)' I)*(s"4:;T7I@JTH; /aluable contributor to J'P

7eulator$ environment

Jovernment ;upport

8/18/2019 End Review Report

http://slidepdf.com/reader/full/end-review-report 15/44

BIA0@I;;I; ncreasin @PA

Lo! penetration

Lack of product differentiation

<PP<7TF@TI; -odern Tec"nolo$

Fntapped 7ural -arket

Jlobali>ation

TH7IAT; Fnorani>ed mone$ lendin market

Customer dissatisfaction

7ise of monopolistic structures

3.11-PORTERS FIVE FORCES ;ODEL

&u$er Po!er:

Hi" barainin po!er of customers on account of banks renders uniform services to t"eclients. @o! a da$s almost all banks !ould like to provide reuisite information ver$ easil$ b$!a$ to nternet, -obile bankin to t"e clients ;upplier Po!er:

Lo! barainin po!er of suppliers on account of 7& reulator$ benc"marks. &anks "ave tomeet numerous reulator$ standards created b$ 7&

Competitive 7ivalries:

Hi" competition of account of number of prominent public, private, forein alon !it"cooperative banks Availabilit$ of ;ubstitutes:

Hi" menace from substitutes like @&Cs, -utual funds, Jovernment securities and T%bills

T"reat of ne! entrants:

Lo! t"reat of ne! entrants on account of bankin reulations. &efore settin up of a ne! bank,it is essential to take t"e consent of 7&.

8/18/2019 End Review Report

http://slidepdf.com/reader/full/end-review-report 16/44

8/18/2019 End Review Report

http://slidepdf.com/reader/full/end-review-report 17/44

CHAPTER-

RESEARCH ;ETHODOLOGY

.1R,s,$"# P("6!s,:- A comparative stud$ of "ousin loan and education loan of publicand private sector bank in ndia.

9.R,s,$"# O+<,#i,:-

To stud$ t"e policies and procedure for t"e Credit Appraisal of "ousin and education

loan

To bride a ap bet!een practical life and t"e t"eor$ t"at !e "ave learnt in our courses.

To understand t"e business and competitive environment of public sector bank , private

sector bank

To find t"e bank sector t"at is larel$ availed b$ t"e customer.

n durin pro#ect to take intervie! of top five bank manaer (8 manaer public and 8

private bank) basis of ratin aenc$ in "ousin and education loan sector

.3-R,s,$"# =,!*!%!'4:

P!6(%$i!): public(6) and private(5) sector bank

S$=6%, si>,:-18 credit manaer intervie!

S$=6%, 46,: ;imple random samplin

S$=6%, $",$: A"medabad cit$

T!!% (s,s 7!" $)$%4s,s:

1.)Jrap"ical 7epresentation of Anal$sis:

%Pie c"arts

%;P;;

.- S!("#,s !7 *$$

P"i=$"4 D$$-

<bservation and personal discussion !it" credit appraisal manaers Questionnaire

SECONDARY DATA1. -AJAR@I;.. @IB;PAPI7;

5. BI&;TI;9. &<<0;

./-TYPE OF RESEARCH&ased on t"e ob#ectives of t"e stud$, t"e descriptive researc" met"od is used .

.?-SURVEY ;ETHOD A surve$ !ill be conducted amonst t"e banks in A"medabad. T"e

7esearc"er !ill personall$ meet t"e credit manaer and intervie! t"em.

8/18/2019 End Review Report

http://slidepdf.com/reader/full/end-review-report 18/44

Building Up of a Proposal 1 GATHERING CREDIT INFOR;ATION:%

An appraisal of a proposal beins !it" t"e at"erin of adeuate backround kno!lede

about borro!ers c"aracter and credit !ort"iness. n t"e concept of appraisal, muc"

reliance is placed on t"e credentials of t"e borro!er. T"erefore, t"ere is a necessit$ for

evaluation of t"e borro!er in reard to "is standin in t"e business, means and

respectabilit$. T"e result of t"e elaborate scrutin$ concernin all t"ese aspects is reuired

to be put into a precise credit report !"ic" "elps in takin decision on a credit proposal.

Iac" individual case "as to be e+amined in t"e li"t of its o!n circumstances and

#udment e+ercised on issues enumerated above and a final decision "as to be arrived at

on t"e basis of scrutin$ of all t"e issues.

nformation b$ definition is t"at data !"ic" is relevant and meaninful for makin decisions.

An information s$stem is an aid to t"e decision makin, carr$in out and alterin decisions.

All information reuired b$ t"e banker in t"e pre%sanction period s"ould become part of a

s$stem. t s"ould flo! into t"e information s$stem from various sources, suc" as t"e

borro!er, banks o!n record, environment etc. A sinificant basis of banker%borro!er

relations"ip is overned b$ t"e information !"ic" flo!s bet!een t"e t!o parties. After

ascertainin t"e credit needs of t"e borro!er, t"e banker looks to!ards information about

"is borro!ers credit !ort"iness. He seeks out t"e credit information etc. from "is co%

bankers, ot"er borro!ers and market information.

. VARIOUS SOURCES OF CREDIT INFOR;ATION

nformation reardin c"aracter, "onest$, and financial position "as to be discreetl$

at"ered from follo!in sources:

a. T, +!""!0," : t"e bank s"ould develop as muc" credit information as possible

durin t"e initial intervie! !it" t"e borro!erpartners of firm directors of compan$

proposed uarantor co%obliator and principal officials of firmscompan$, nature of itsbusiness, past and e+pected profitabilit$, t"e deree of competition t"at t"e

firmcompan$ faces and !"et"er or not it "as "ad or anticipated an$ difficult$ etc.

nformation reardin its principal officers s"ould be collected durin suc" intervie!.

b. B!""!0,"s 7i)$)#i$% s$,=,)s: for lendin decisions, financial information is a

sinificant part of t"e total information s$stem. t is derived basicall$ from borro!ers:

• Tradin and profit and loss statement

• &alance s"eet

• Cas" and fund flo! statements

8/18/2019 End Review Report

http://slidepdf.com/reader/full/end-review-report 19/44

c. B$)&s !0) ",#!"*s: f "e is an e+istin borro!er, banks o!n records are a ric"

source of additional information. <perations in t"e borro!ers account and ot"er

dealins at t"e bank level in reard to collections, discountinretirement of bills etc.

often useful clues to borro!ers operatin and financial transactions. A revie! of t"e

previous $ears operations in t"e account and assessments of borro!ers financial

statements relatin to t"at period !ill provide a ric" source of information about t"e

borro!er.

d. O6i)i!)s: &ank s"ould compile opinions on t"eir borro!ers. T"e$ s"ould contain

full and reliable records of t"e c"aracter, estimated means and business activities of

all firms and individuals !"o are under an$ form of liabilit$ to t"e bank, !"et"er asdirect borro!ers or as co%obliators. ull particulars of parties immovable properties

!"ere t"e$ are situated, !"et"er t"e$ are free from encumbrance and in t"e case of

land, acreae s"ould be recorded toet"er !it" fair estimates of t"eir value. As far as

possible !ritten statements of t"eir properties s"ould be taken in evaluatin

properties o!ned b$ parties #ointl$ !it" ot"ers and as a rule suc" properties s"ould

be disrearded in arrivin at t"e net means.

e. F"!= !," +$)&s: in respect of fres" proposals, enuiries !it" local banks s"ould

be made before entertainin t"e proposal to avoid multiple financin !it"out our full

kno!lede. n case of ne! customer "avin dealins !it" ot"er banks, confidential

opinion of "is banker "as to be obtained.

f. I)#!=, $@ $ss,ss=,) !"*," % ncome ta+ assessment orders aricultural income

ta+ assessment orders ive an insi"t into t"e borro!ers account and t"e e+tent to

!"ic" it is profitable. Comments t"ereon b$ t"e income ta+ office s"all indicate t"e

s"ortcomins (lacunae) in t"e business. n t"e case of estate o!ners aricultural ta+

assessment orders to be obtained to arrive at parties credit !ort"iness.

. S$%,s $@ $ss,ss=,) !"*,"s: ;ales ta+ assessment orders !ill reveal t"e turnover

in business and !"en read !it" tradin manufacturin and profit D loss account, it

ma$ be possible to "ave a fair assessment of tendencies in trade i.e., !"et"er over%

tradin or carefull$ tradin !it"in recourses at command or tradin entirel$ on t"e

borro!ed funds.

8/18/2019 End Review Report

http://slidepdf.com/reader/full/end-review-report 20/44

". W,$% $@ $ss,ss=,) !"*,"s: !ealt" ta+ assessment order !ill indicate t"e net

!ort" of individuals and reveals t"e liuid source available to brin t"e reuired

marin mone$ for t"e venture.

i. ;$"&, s!("#,s: Constant touc" !it" t"e market !ill "elp to "ave first "and

information about t"e ains or losses in particular business transactions of t"e

borro!ers.

#. P"!6,"4 s$,=,)s: T"e propert$ statement of borro!er !ill ive an idea of "is

!ort", liabilities and "is income from real estates (immovable properties).

k. ;()i#i6$% 6"!6,"4 ",'is,"s: reference to municipal propert$ reisters !ill ive anidea of buildin o!ned !it"in t"e municipalit$, 7ental /alues and "ouse ta+ pa$able.

t ma$ be noted t"at t"e said reisters are open for reference to all persons.

l. O," ,@,")$% s!("#,s: ot"er e+ternal sources, if an$, like stock e+c"ane

director$, business periodicalsmaa>ines#ournals etc.

!"#UI!"$"N%S AS P"! ONS%I%U%ION O' BO!O("!)

ollo!in 7euirements as per constitution of borro!er s"ould be collected for proposals

emanatin from%

1. P$"),"si6:

• Cop$ of partners"ip deed

• Cop$ of certificate of reistration of firm (if reistered)

. C!=6$)4 :

• -emorandum and articles of association

• Certificate of incorporation

• Certificate of commencement of business

• ;earc" report indicatin subsistin c"ares on t"e assets of t"e compan$.

• &oard resolution for borro!ins, creation on t"e assets of t"e compan$ and

e+ecution of t"e documents.

3. C!!6,"$i, s!#i,i,s

• &$la!s

8/18/2019 End Review Report

http://slidepdf.com/reader/full/end-review-report 21/44

• Permission from reistrar for t"e borro!ins, creation of c"are on t"e assets

of t"e societ$ and e+ecution of documents.

. T"(ss• Trust deed

• 7esolution for t"e borro!ins and e+ecution of documents.

/. I)*(s"i$% ()is :

• Pro#ect report !it" cas" flo!, fund flo! statements etc.

• ndustrial licenses;; reistration certificate.

• License from local aut"orit$, compliance of leal reuirements or conditions

as applicable and clearance from reulator$ bodies.

'INANIA* APP!AISA*

<n receipt of a loan application t"e banker beins t"e process of financial appraisal. T"e

first t"in done is to anal$>e t"e financial statements. T"erefore, an understandin of t"ese

financial statements is important for t"e appraiser.

<nce balance s"eet is taken for anal$sis t"e follo!in items are c"ecked up:

1. Fi@,* $ss,s: To find out an$ revaluation of fi+ed assets done b$ t"e compan$ to

improve t"eir net !ort".

• T"e sc"edules of t"e fi+ed assets s"ould be c"ecked up.

• ;tud$ notes on accounts and comments of auditors s"ould be c"ecked.

• ;c"edule for reserve s"ould be studied

• An$ c"ane in t"e accountin procedure of depreciation s"ould be c"ecked

. C("",) $ss,s: to find out !"et"er t"e assets stated are reall$ liuid or

not.

• T"e sc"edules under current liabilities and current assets to ascertain an$

obsolete or slo! movin ra! material or finis"ed ood and old debtors or

receivables s"ould be c"ecked

• T"e auditors report s"ould be read and understood properl$.

•

T"e claims loded aainst receivables must be studied

• T"e receivables due from sisterassociate concerns must be studied.

8/18/2019 End Review Report

http://slidepdf.com/reader/full/end-review-report 22/44

5. O," C("",) Ass,s: T"eir reasonableness and t"eir need to maintain t"em for

t"e business.

• /arious components of ot"er current assets and if t"e same is more t"an 8K

%1K, ascertain t"e nature and need for maintainin suc" amount 4 an$assets !"ic" is not used in t"e into da$ business activit$ s"all be removed

and proper treatment is to be made accordinl$.

• &ank uarantee or letter of credit marin s"all be s"o!n as non% current

assets.

9. C!)i)',) %i$+i%ii,s: To find out an$ unreconi>ed liabilities or losses if an$.

• T"e C'''&' ot"er bills discounted liabilit$, if an$ ,is reported in t"e

auditors report , t"en increase t"e bank borro!in to t"e e+tent liabilit$ !as

not taken in t"e balance s"eet and also increases t"e debitsreceivables to

t"at e+tent.

8. T,"= %i$+i%ii,s: To find out !"et"er t"e liabilities are lon term or s"ort term, and

its needs and reularit$

• T"is s"all be decreasin $ear after $ear4 if it "as increased, t"en t"e reason

for t"e same is to be looked into (ma$ be irreular or ne! term loan availed

for e+pansion etc.)

• T"e term liabilities !it" repa$ment of t"e same and t"e amount pa$able

durin t"e $ear s"all be deducted from t"e term liabilities as current liabilities

for findin out liuidit$ position of t"e compan$ s"ould be c"ecked.

?. S!#&s:

• T"e stock statements and Q; forms to find t"e aut"enticit$ of t"e fiures

reported under stockreceivables.• C"ane in t"e valuation of t"e stockfinis"ed oods, if an$, is to be verified to

find out its effect on t"e profitabilit$ of t"e compan$.

6. I)$)'i+%, $ss,s :

• An$ abnormal increase in t"is fiure s"all be studied to find out t"e reasons

for t"e same4 t"is ma$ be due to take over b$ ot"ers also.

. A##!()i)' N!"=s:

8/18/2019 End Review Report

http://slidepdf.com/reader/full/end-review-report 23/44

• An$ c"ane in t"e accountin norms from t"e past s"all be studied to find

out t"e reasons for t"e same4 its effect on t"e net profit, net !ort" of t"e

compan$ is to be ascertained.

BA*AN" S+""% ANA*,SIS

1. C!==,)s !) , 6,"7!"=$)#, !7 , ()i vis%S%vis last $ear sales%

• ncreased in last $ear sales are al!a$s ood4 if t"e net profit also "as

increased correspondinl$ t"e performance can be noted as satisfactor$.

• f t"e sales "as come do!n or t"e net profit "as also come do!n t"en t"e

reason "as to be ascertained. f t"e unit earned at least cas" profit t"en t"e

position ma$ be considered as satisfactor$.

• I7 , NP ! Ns$%,s is 6!sii, $ is s(77i#i,) 7!" $##,6i)' $s

s$is7$#!"44 but as per t"e credit ratin c"art ma+imum marks are assined

if t"e borro!er ac"ieves K as percentae of net profitnet sales.

• 7eturn on investment or 7eturn on euit$ ma$ also be used to find out t"e

return on capital invested.

. L!)' ,"= S",)' !7 $ #!=6$)4 is calculated based on t"e level of t"e net

!ort" of t"e compan$ promoters stakeloans from close relatives%

• f t"e net !ort" "as increased due to infusion of fres" capital or plou" back

of profit, it can be termed as satisfactor$4 even increase of loan from friends

D relatives is a ood sin.

•

f t"e net !ort" is decreasin, reason ma$ due to net loss or diversion4 truereason needs to be ascertained.

• f t"e DE ratio is less t"an :1 t"e same is ood4 furt"er if t"e T<LT@B is

less t"an 8:1 t"en t"e units solvenc$ is noted to be satisfactor$. T"e ratio

indicates t"at borro!er "as not borro!ed muc" and t"e outside debts !it"in

a reasonable limit.

3. Li(i*i4 6!sii!) !7 , 6$"4-C("",) "$i!

• f t"e current ratio is increasin and nearer to 1.8 and above t"en !e can

note t"e position is satisfactor$.

8/18/2019 End Review Report

http://slidepdf.com/reader/full/end-review-report 24/44

• I+pected Current ratio is 1.:1 and above4 if t"e ratio is less t"an 1.:1

t"en t"e promoters marin (@et !orkin capital) to!ards Borkin Capital

ma$ not be sufficient to cover t"e !orkin capital limit4 care s"all be taken to

ensure t"at sufficient @et !orkin capital for t"e !orkin capital en#o$ed isavailable.

• B"en t"e Current ratio is poor and t"e @et !orkin capital is not sufficient to

cover t"e e+istin limit, no furt"er term loan s"all be sanctioned and t"e

part$ is to be advised not to take up an$ fres" investment in fi+ed assets.

9. ($%i4 !7 #("",) $ss,s :

• T"e current assets "oldin period must be less t"an 5 mont"s for traders

and t"e 8 mont"s for t"e industries dependin upon t"e t$pe of industr$

4"oldin level more t"an t"e above needs proper #ustification.

• t s"ould be ensured t"at t"e current assets turnover is at least more t"an

four times in a $ear.

8. C!)i)',) %i$+i%i4:

• T"e effect of t"is liabilit$ on t"e net !ort" of t"e compan$4 if its effect is

less t"an 8%1 K of t"e net !ort" of t"e compan$ ,t"e same ma$ be noted4

but if it t"reatens t"e e+istence of t"e compan$ t"en t"e position needs

serious anal$sis.

?. Di,"si!) 7"!= , +(si),ss ),,*s ! +, i,0,* #$",7(%%4.

• 7eduction in @et !orkin capital position( belo! t"e reuired level) !"en

t"e unit "as earned cas" profit and clearin of term loan installments !"en

t"e unit is makin cas" loss needs to be vie!ed seriousl$.

•

7eduction in t"e net !ort" of t"e firm (!"en t"e$ "ave s"o!n net profitneeds furt"er probin.

APP!AISA* %"+NI#U"S 'O! !"%AI* *OANS

I. EDUCATION LOANS

Till some $ears back "i"er education and ualit$ education !as not affordable to some

illustrious students because of t"e financial constraints. T"ere !as no an$ alternative but to #ump in t"e #ob market prematurel$. And t"is led to untimel$ end of buddin talents and

t"eir forceful transformation into to t"e mediocrit$. ;c"olars"ips !ere t"ere, but t"ose !ere

so less in numbers t"at onl$ luckier fe! could avail t"em. &ut no! t"e scene "as c"aned

8/18/2019 End Review Report

http://slidepdf.com/reader/full/end-review-report 25/44

drasticall$. T"e boom in t"e bankin sector "as led to release of lare amount of funds for

education loans

S(*,) %!$)s in ndia (popularl$ kno!n as E*(#$i!) %!$)s) "ave become a popular

met"od of fundin "i"er education in ndia !it" t"e cost of educational derees oin

"i"er. T"e spread of self%financin institutions(!"ic" "as less to no fundin from t"e

overnment) for "i"er education in fields of enineerin, medical and manaement !"ic"

"as "i"er fees t"an t"eir overnment aided counterparts "ave encouraed t"e trend in

ndia. -ost lare public sector and private sector banks offer educational loans.

Fnder section (e) of t"e ndian ncome ta+ act, a person can e+empt t"e amount paid

aainst t"e interest of t"e education loan % eit"er for self or for "is"er spouse or c"ildren %

for ei"t $ears from t"e $ear (s)"e starts to repa$ t"e loan or for t"e duration t"e loan is in

effect, !"ic"ever is lesser.

Iducation loan is becomin popular da$ b$ da$ because of t"e risin fee structure of

"i"er education. t came into e+istence in 1**8 started first b$ ;& bank and after t"at

man$ banks started offerin stud$ loan.

T"e education loan provided b$ Pun#ab @ational bank is kno!n as / i*4$%$&s4$6("i

sc"eme. T"e details reardin its eliibilit$, processin, documentation etc. are iven as

follo!s:%

C!)#,6 VIDYALAKSHYAPURTI ;c"eme is t"e main sc"eme and its variantP@& ;arvotam ;"iks"a sc"eme stands mered !it" t"e mainsc"eme !it" effect from .1.

C!("s,s,%i'i+%,

S(*i,s i) I)*i$;c"ool level includin. , Jraduation, Post raduation, Professionalcourses, Computer courses and Ivenin courses, ot"er coursesleadin to diploma deree approved b$ FJC, Jovt, ACTI, A&-;,C-7 etc. and Advance diploma in &ankin Tec". t includesprofessional D commercial D pilot trainin courses in ndia and

abroad. or stud$ in ndia. nstitutes approved b$ 'JCA areincluded.

S(*i,s A+"!$*Jraduation, PJ and Courses offered b$ C-A London , CPA in F;A

E%i'i+i%i4 • ndian @ational

• ;ecured Admission;ecured pass marks in ualif$in e+am. &ranc"es need not o intotec"nicalities of admission process (selection t"rou" manaementuota etc.) and ma$ consider loan based on admission advice. RBD Ci". N!. ?995 *. 29.12.2995

;!", $) !),%!$) i) $ 7$=i%4

n case of more t"an one loan in a famil$, t"e famil$ as a unit is to betaken into account for considerin t"e loan and securit$ taken inrelation to total uantum of loan sub#ect to marin and repa$incapacit$ of t"e parents.

T!6 (6 L!$)s Top up loans ma$ be sanctioned to students for pursuin furt"er

8/18/2019 End Review Report

http://slidepdf.com/reader/full/end-review-report 26/44

studies !it"in overall eliibilit$ limits !it" appropriate resc"edulementof e+istin loans and reuired permission b$ t"e CH

A', !7 s(*,) T"ere is no restriction !it" reard to ae of student for bein eliiblefor t"e loan.

I)#!=, C"i,"i$ @o ncome criteria are prescribed for t"e parents. Ho!ever amount of

loan be decided b$ #udin ncome of t"e parents.A=!() !7%!$)

7s. 1. lac in ndia and . lac for abroad. CH can e+ercise"i"er po!ers.

P"i!"i4 S,#!" 7s. 1. lac in ndia and 7s. . lac for abroad.C$6i$%R,(i",=,)

7isk Bei"t as per &A;IL% 1K7isk Bei"t as per &A;IL% 68K

;$"'i) @L Fp to 7s. 9. lac

8K Above 7s. 9. lac in ndia

18K Above 7s. 9. lac abroad

(;c"olars"ipassistance ma$ be included in t"e marin)S,#("i4 @L Fp to 7s. 9. lac

5rd

part$ uarantee for loans above 9. lac upto 7s. 6.8 lac(I+emption from takin uarantee for loan up to 6.8 lak" for students of T, -, L7 etc.I- of P or ot"er Coll. ;ecurit$ for loans above 6.8 lac (s!(%* +,i),"6",,* $s %!$) $=!() !7 Rs. ./1 %$# $)* $+!, i) ,"=sH$pot"ecation of assets if created out of loan amount.Co%obliation of students parents as !ell as assinment of futureincome of student in loan above 7s. 6.8 lac. or married persons, co%obliator can be spouse or parents or parents%in%la!. Jrand parentscan also become co%obliants.

S,#("i4 7!"s$77 =,=+,"s

Lien on Terminal dues

I+tension of I- of P

res" -ortae if t"ere is no HL Co%obliation of emplo$ee

P,)$% I),",s Fp to 8% %%%%@L , Above 8% U K on </I7'FI A-<F@TU67"!) 7,, @L

.8K (-a+imum 8%) for studies abroad !"ic" is eliible for

refund on availment of loan.D!#(=,)$i!)C$"',s

Fpto 9. lac % 7s. 6% plus service ta+

Above 9. lac 7s. 98% plus service ta+

R,6$4=,) 8 to 6 $ears !it" moratorium period eual to Course period 1 $ear or mont"s after ettin #ob !"ic"ever is earlier. &- is empo!ered topermit e+tension in moratorium period up to $ears as aainst

present provision of ma+. 1 $ear in deservin cases under reportinto circle "ead.

C$%#(%$i!) !7i),",s

;imple interest is to be c"ared durin moratorium period and kept ina separate account. T"e accrued interest durin repa$ment "olida$!ill be added to Principal for fi+in of I-.

I),",s#!)#,ssi!)

1K interest concession is allo!ed if it is serviced durin "olida$period. T"e concession !ill be iven at start of repa$ment and I-!ill be fi+ed accordinl$.7ebate of .8K is allo!ed to students of Ts, -s etc.

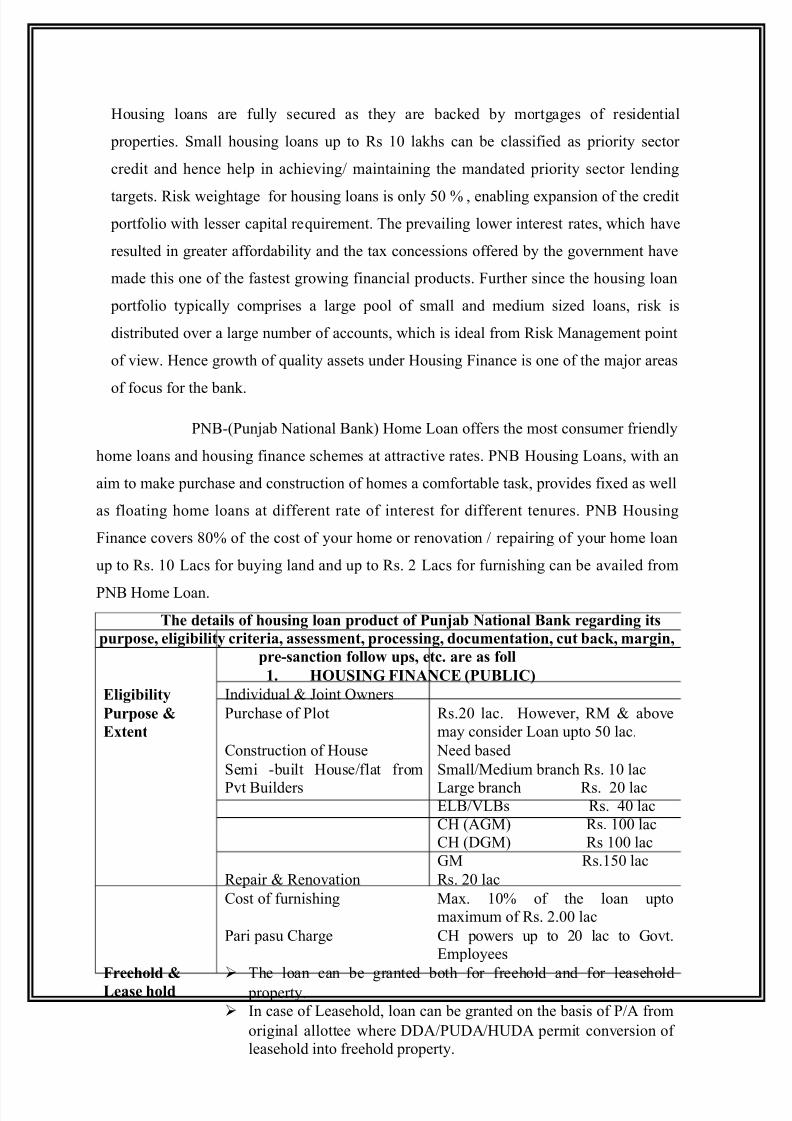

II 13(I.% 4A.(

Housing loans have emerged as an attractive avenue for credit deployment for banks in

the recent past. Industry level statistics reveal that !"s in this segment is relatively lo#.

8/18/2019 End Review Report

http://slidepdf.com/reader/full/end-review-report 27/44

Housing loans are fully secured as they are backed by mortgages of residential

properties. $mall housing loans up to %s 10 lakhs can be classified as priority sector

credit and hence help in achieving& maintaining the mandated priority sector lending

targets. %isk #eightage for housing loans is only '0 ( ) enabling e*pansion of the credit

portfolio #ith lesser capital re+uirement. ,he prevailing lo#er interest rates) #hich have

resulted in greater affordability and the ta* concessions offered by the government have

made this one of the fastest gro#ing financial products. urther since the housing loan

portfolio typically comprises a large pool of small and medium sied loans) risk is

distributed over a large number of accounts) #hich is ideal from %isk /anagement point

of vie#. Hence gro#th of +uality assets under Housing inance is one of the maor areas

of focus for the bank.

!-!unab ational ank3 Home oan offers the most consumer friendly

home loans and housing finance schemes at attractive rates. ! Housing oans) #ith an

aim to make purchase and construction of homes a comfortable task) provides fi*ed as #ell

as floating home loans at different rate of interest for different tenures. ! Housing

inance covers 50( of the cost of your home or renovation & repairing of your home loan

up to %s. 10 acs for buying land and up to %s. 2 acs for furnishing can be availed from

! Home oan.

The details of housing loan product of $un5ab .ational &ank regarding its

purpose6 eligibility criteria6 assessment6 processing6 documentation6 cut back6 margin6

pre-sanction follo ups6 etc are as foll

" 13(I.% 7I.A.8 *$3&4I8,

ligibility Individual 7oint 8#ners

$urpose

;tent

!urchase of !lot %s.20 lac. Ho#ever) %/ above

may consider oan upto '0 lac.

9onstruction of House eed based

$emi -built House&flat from

!vt uilders

$mall&/edium branch %s. 10 lac

arge branch %s. 20 lac:&;s %s. 40 lac

9H "</3 %s. 100 lac

9H =</3 %s 100 lac

</ %s.1'0 lac

%epair %enovation %s. 20 lac

9ost of furnishing /a*. 10( of the loan upto

ma*imum of %s. 2.00 lac

!ari pasu 9harge 9H po#ers up to 20 lac to <ovt.

:mployees

7reehold

4ease hold

,he loan can be granted both for freehold and for leasehold

property.

In case of easehold) loan can be granted on the basis of !&" from

original allottee #here =="&!>="&H>=" permit conversion of

leasehold into freehold property.

8/18/2019 End Review Report

http://slidepdf.com/reader/full/end-review-report 28/44

8ther#ise advance is not permitted against plots purchased on

!o#er of "ttorney basis.

8apital

0e<uirementoan limit up to ?0 lac %isk @eight is '0(

oan limit above ?0 lac %isk @eight is A'(

,; %atio more than A'( %isk @eight is 100('argin and&!lot 40(

9onstruction&repair&addition 2'(

0ate of Interest %ate of Interest as per " 9irculars issued from time to time.

0.'0 ( e*tra #ill be charged on H& for ?rd House.

,he interest can be fi*ed or floating

8ption can be changed from fi*ed to floating and vice versa #ith

flat charges of 2( fee on alance outstanding

i*ed Interest rate be revie#ed&reset after a block of ' years in

respect of loans disbursed on or after 1.5.2006.

8oncessional

0ate of Interest

for Defense

mployees

ank has decided to e*tend concessions to =efense personnel #ho are

raising Housing oans under bankBs regular Housing oan scheme for

public as underC

2' bps rela*ation in interest rates

'0 bps rela*ation in processing fee

,hese rela*ations are to be made applicable in all ne# cases #here

defense personnel avail housing loan either in single name or along

#ith spouse.

0&D 8ir .o ""/2" dt "#22",

0epayment /a*imum 2' years including /oratorium period of 15 months

Installment can be fi*ed up to ma*imum age of 6' years. HubIncharge of $cale-I; and above besides 9ircle Head can rela* the

age up to A0 years)

%epayment of loan for repair&renovation&addition&alteration

restricted to 10 years including moratorium period of 6/.

"ll deductions should not e*ceed '0( of <ross monthly income.

Ho#ever #here gross monthly salary is above '0000&-) the

deduction can be up to 60( and if gross monthly salary is above

100000&-) the deduction can be up to A0( #ith the permission of

9H. ,he income of earning spouse and children can be taken into

account.

,he Income of spouse and earning children can be taken into

account provided they are made co-borro#ers.

ather&mother can also be made co-borro#ers in cases #here

property is in the single name of his&her son and also clubbing of

their income is permitted for determining eligibility criteria.

/inimum 24 advance che+ues should be obtained. "s and #hen) 6

che+ues remain) fresh lot be obtained. 8ut of 24) 2? che+ues

should be of installments and 1 che+ue should be of the amount

e+ual to the balance amount.

%raduated

'I

! offers benefit of graduated :/I. ,his means that the customer

has the option of choosing :/I that can increase or decrease duringrepayment period rather than being given a fi*ed :/I over repayment

tenor.

8/18/2019 End Review Report

http://slidepdf.com/reader/full/end-review-report 29/44

3pfront fee 0.D0 ( of loan amount E service ta* education cess 10.?0(3 on

loans above ?00 crore.

!rocessing fees F 0.'0( of loan amount ma*. 200003 Eservice ta*

for loans up to ?00 crore.

Documentationcharges %s.1?'0 E service ta*

(ecurity :+uitable&%egistered /ortgage of Immovable !roperty

,ripartite agreement be e*ecuted amongst Housing oard&=ev

"uthority&9oop $ociety&uilder) the borro#er and the bank #here

mortgage cannot be created immediately. In such cases) ? rd party

guarantee is also to be obtained.

:/ of other I! or pledge of $9 etc. up to 12'( of loan amount

if property is being purchased from 1st !&" holder and #here there

is delay in e*ecution of ,ripartite agreement or #here themortgage of property is not possible being an ancestral property

#ithout title deeds3 or al =ora and.

;erification of security is re+uired once in 2 years. In case of !"s

accounts) security is to be verified on Half yearly basis.

%uarantee In general6 no guarantee is to be asked for &ut hile preparing

0&4 score sheet6 if score is less than =>6 then !rd party guarantee

can be obtained to raise score of the applicant .

Insurance In case of building at 0e-construction cost.

$riority (ector

inclusion

%epair %enovation %s.1.00 lac %ural $emi&>rban3

%s.2.00 lac >rban3

8thers %s. 20.00 lacther features oan can be sanctioned by the branch&hub near to the present place

of #ork&posting&residence of the borro#er. Ho#ever) if the

property is situated at other place) services of branch&hub located

at that center may be availed for verification of $ecurity and

:9&;aluation etc.

oan can be granted even if property is in the name of #ife&parents

provided that the o#ner is made co-borro#er.

oan can be granted for 2nd house in the same city.

oan can be granted for purchase of house for rental purpose.

or take over) permission of higher authority is not re+uired

Important

conditions

oan cannot be granted

or construction in >n-authoried colonies

If property is to be used for commercial purpose

@ithout approved /ap

* In 8ompliance of Delhi 1igh 8ourt rders,

!re-payment charges of 2( be recovered on account being

taken over by another bank. In case) the loan is pre-paid out of

o#n sources or the loan is taken over by another bank #ith in

?0 days from date of circular by #hich either the interest is

raised or any important term or condition is changed) there #ill

be no pre-payment charges. lat pre-payment charges of 2( be recovered from borro#ers

#ho pre-pay #ithout construction on the plot before ' years.

!o#ers of concessions in rate of interest&other charges stand

8/18/2019 End Review Report

http://slidepdf.com/reader/full/end-review-report 30/44

#ithdra#n vide %= cir no. '2&0A dt. 1?.11.0A.

In case6 the construction of house is not completed ithin ! years

or in case the plot is sold6 penal interest ?2> over and above the

applicable rate be charged

;pression ofInterest It is a letter issued by the bank&branch #herein the lender e*pressesintention to make advance to the intended borro#er on the basis of

eligibility criteria subect to the fulfillment of terms and conditions.

%rih 0aksha

@avach

It is /ortgage %educing ,erm "ssurance !olicy issued in ,ie up

arrangement #ith ,","-"I<. ,here is one-time premium of 2.'(

appro*3 and that amount can also be financed. ,he coverage of the

scheme is 1-20 years. ,he sum assured is bet#een %s.10000 to %s.

1.00 crore. In case of death of the borro#er) receipt from insurance

company can be utilied to#ards adustment of loan amount as per

amortiation table. !rior permission of ,","-"I< is re+uired if

amount is over %s. 50.00 lac.

Iffco Tokyogeneral

insurance co

,he coverage for accidental death and permanent total disability dueto accident3 along #ith mandatory insurance Gire !olicy including

earth+uake is offered in tie up arrangement #ith Iffco ,okyo <eneral

Insurance 9o. td. ,o all e*isting as #ell as ne# borro#ers.

arnest 'oney

Deposit

(cheme

,o meet the re+uirement of earnest money to apply for

plot&flat&house from $tate Housing oards and >rban

=evelopment authorities.

,hese authorities undertake to refund or issue allotment letter to

the bank subect to eligibility of the bank for proposed loan and

future re+uirement of Housing oan.

:*tent of loan is D0( of :/= or ma*. %s 2.00 lac in the shape of

=emand oan

%8I is !% 1.A'(

%epayment through %efund order&Housing oan&ullet !ayment.

<uarantee clause deleted

D 7acility to

e;isting 1/4

borroers

8= facility can be allo#ed to e*isting Housing oan borro#ers there

is no I% irregularity. 8ther features of the scheme are as underC

/inimum '0000&- and /a*imum %s. '.00 lac.

"dditional limit and present o&s should not e*ceed A'( of

current market price of the house so as to maintain margin of

2'(.

>pfront fees is I and documentation charges are %s. '00&-. ,ake home salary should not be less than 40( of gross salary.

oaning po#ers are $-il) /- %s.4.00 lac) ) :

;

%s. '.00 lac.

%8I is e+ual to !%

"fter H is repaid) 8= can be continued& rene#ed provided

the sanctioning authority is satisfied about repaying capacity of

the borro#er and ;alue of security

D facility for personal use should not be sanctioned to the

borroers6 ho have availed loan for plot 6 construction onhich is yet to be completed in terms of 0&D cir no +!

dt2"//9

8n revie#) it has been decided to do a#ay #ith the condition of

minimum 2 year of repayment track record of the borro#er for

8/18/2019 End Review Report

http://slidepdf.com/reader/full/end-review-report 31/44

considering 8= facility up to ' lac. Ho#ever this is subect to

compliance of all other terms and conditions such as JK9 norms)

9II database) takeover guidelines) security norms) maintenance of

margin etc.

,his facility is outside the purvie# of GHub and $pokeG model in the

accounts of e*isting H borro#ers.

*0&D 8ir .o #+ dt "9"229,

$.& 7le;ible

1ousing 4oan

(cheme

,his is an attractive variant of Housing oan $cheme offered by the

! for its customers. >nder this scheme) 8= facility is made

available to the H borro#er. He can deposit his savings and #ithdra#

the same as per his re+uirement. ,he features of the scheme are as

underC

:ligibility "ge of the applicant must be less than =

:*isting H borro#ers can also apply provided their loan account is regular and no I% irregularity persists.

!urpose "ll purposes as per original scheme e;cept $urchase of

4and / $lot

:*tent ,erm oan 50(

8verdraft 20(

"fter lapse of ? years) enhancement in 8= #ill be

allo#ed e+ual to reduction in ,erm oan and

thereafter on yearly basis.

"fter lapse of ' years) 20( increase in original

limit is allo#ed in the shape of ,&8= for personal needs.

/arket ;alue of !roperty should be sufficient to

cover the margin of 2'(

"fter attaining age of '' years) 8= facility #ill be

reduced on monthly basis so that #hole limit and

,& are adusted by the end of 6' years.

/a*imum 8= limit should not e*ceed '0( of

,otal limit.

H can be sanctioned by the branch&hub situated

near the #orkplace&posting&residence.

$ecurity verification can be done by nearby

branch.

%ate of Interest as given above in the table in

Housing oan scheme general3

or 8verdraft portion) %&I is e+ual to !%

8/18/2019 End Review Report

http://slidepdf.com/reader/full/end-review-report 32/44

C!)si(,s !7%!$)

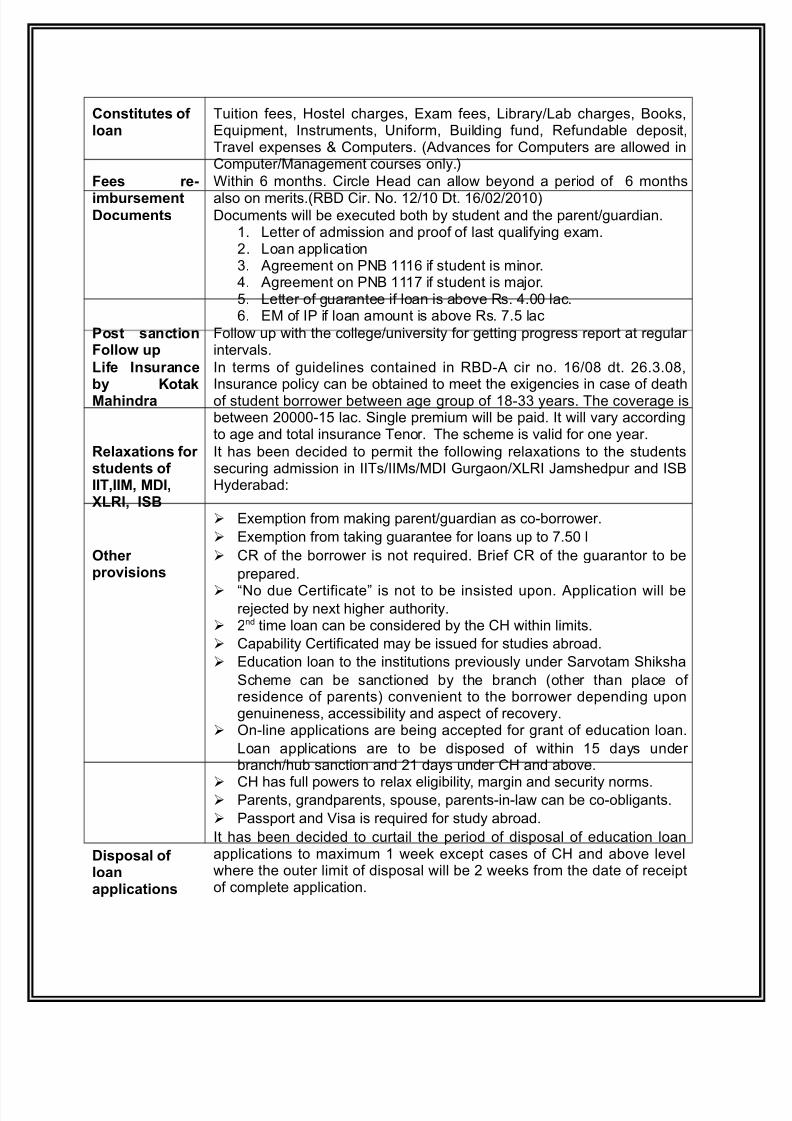

Tuition fees, Hostel c"ares, I+am fees, Librar$Lab c"ares, &ooks,Iuipment, nstruments, Fniform, &uildin fund, 7efundable deposit,Travel e+penses D Computers. (Advances for Computers are allo!ed inComputer-anaement courses onl$.)

F,,s ",-

i=+("s,=,)

Bit"in mont"s. Circle Head can allo! be$ond a period of mont"s

also on merits.(7&' Cir. @o. 11 't. 11)D!#(=,)s 'ocuments !ill be e+ecuted bot" b$ student and t"e parentuardian.

1. Letter of admission and proof of last ualif$in e+am.. Loan application5. Areement on P@& 111 if student is minor.9. Areement on P@& 1116 if student is ma#or.8. Letter of uarantee if loan is above 7s. 9. lac.. I- of P if loan amount is above 7s. 6.8 lac

P!s s$)#i!)F!%%!0 (6

ollo! up !it" t"e colleeuniversit$ for ettin proress report at reular intervals.

Li7, I)s("$)#,+4 K!$&;$i)*"$

n terms of uidelines contained in 7&'%A cir no. 1 dt. .5.,nsurance polic$ can be obtained to meet t"e e+iencies in case of deat"of student borro!er bet!een ae roup of 1%55 $ears. T"e coverae isbet!een %18 lac. ;inle premium !ill be paid. t !ill var$ accordinto ae and total insurance Tenor. T"e sc"eme is valid for one $ear.

R,%$@$i!)s 7!" s(*,)s !7IITII; ;DILRI ISB

t "as been decided to permit t"e follo!in rela+ations to t"e studentssecurin admission in Ts-s-' JuraonL7 Nams"edpur and ;&H$derabad:

I+emption from makin parentuardian as co%borro!er.

I+emption from takin uarantee for loans up to 6.8 l

O,"6"!isi!)s

C7 of t"e borro!er is not reuired. &rief C7 of t"e uarantor to be

prepared.

V@o due CertificateW is not to be insisted upon. Application !ill bere#ected b$ ne+t "i"er aut"orit$.

nd time loan can be considered b$ t"e CH !it"in limits.

Capabilit$ Certificated ma$ be issued for studies abroad.

Iducation loan to t"e institutions previousl$ under ;arvotam ;"iks"a

;c"eme can be sanctioned b$ t"e branc" (ot"er t"an place of residence of parents) convenient to t"e borro!er dependin uponenuineness, accessibilit$ and aspect of recover$.

<n%line applications are bein accepted for rant of education loan.

Loan applications are to be disposed of !it"in 18 da$s under branc""ub sanction and 1 da$s under CH and above.

CH "as full po!ers to rela+ eliibilit$, marin and securit$ norms. Parents, randparents, spouse, parents%in%la! can be co%obliants.

Passport and /isa is reuired for stud$ abroad.

Dis6!s$% !7%!$)$66%i#$i!)s

t "as been decided to curtail t"e period of disposal of education loanapplications to ma+imum 1 !eek e+cept cases of CH and above level!"ere t"e outer limit of disposal !ill be !eeks from t"e date of receiptof complete application.

8/18/2019 End Review Report

http://slidepdf.com/reader/full/end-review-report 33/44

FACTS AND FINDINGS

1. 98K customers are prefer t"e Public &ank !"en takin personal loan and onl$ 5K

customers prefer Private &ank.

. amil$ members are creatin more effect on decisions reardin "ousinl loan.

5. nterest rate is main factor consider b$ customers !"en takin loan.

9. -ost of t"e customer prefers t"e repa$ment of loan in "i"er duration.

8. -ost of t"e customers consider t"e policies of bank reardin "ousin loan.

. 8 K customers ive t"e "i"er ratin to ;& &ank.

6. n H'C &ank onl$ 5 K customers ive t"e "i"er ratin to H'C &ank

<nl$ overnments emplo$ees are prefer t"e public &ank.

*. ;imilarl$ self emplo$ed D businessmans are prefer t"e private &ank.

1 Lo! income class people face difficult$ to takin personal loan

ANALYSIS AND INTERPRETATION

S$=6%, si>, 199

.1 T46, !7 #(s!=,"s.

SBI HDFC

$ B(si),ss=$) 12 29

+ S,%7 ,=6%!4,* 29 29

#W!"&i)'6"!7,ssi!)$% 25 3/

*G!.s,"i#,,=6%!4,, 9 2/

8/18/2019 End Review Report

http://slidepdf.com/reader/full/end-review-report 34/44

I),"6",$i!):- As per t"e stud$ t"e ovt. emplo$ees are main customers of public bank

and businessman are less minimum. <n t"e ot"er side !orkin professional are main

customers of private bank.

.2 B$)& 6",7,",)#, 7!" 6,"s!)$% %!$).

$ HDFC 39

+ SBI /

# OTHERS 2/

8/18/2019 End Review Report

http://slidepdf.com/reader/full/end-review-report 35/44

I),"6",$i!):-

-a+imum number of customers prefer ;& bank for takin personal

loan compare to H'C bank bco> of lo! interest rate, ood imae, and public sector bank.

8K customers prefer ot"er bank like CC, P@&, and &ank of &road.

.3 S!("s !7 #!==()i#$i!) F"!= 0,", #(s!=,"s ', ,I)7!"=$i!) $+!( +$)&.

$ A*,"is,=,) 39

+ F"i,)* 2/

# F$=i%4 =,=+," 3/

* O,"s 19

8/18/2019 End Review Report

http://slidepdf.com/reader/full/end-review-report 36/44

I),"6",$i!):- As per as m$ t"e stud$ t"e famil$ members are t"e main sources of

Communication about bank and advertisement is ot"er sources. amil$ members influence

t"e decision related to takin personal loan.

. F$#!"s #!)si*," +4 #(s!=,"s 0i%, $&i)' %!$).

$ I),",s "$, 9

+ S#,=, 29

# D("$i!) 5

* O,"s 2

8/18/2019 End Review Report

http://slidepdf.com/reader/full/end-review-report 37/44

6K

K

K K

I),"6",$i!):-

B"en an$ customers plannin for takin personal loan from an$

bank t"e$ mainl$ consider t"e interest rate of t"e particular bank and t"e$ ive second

preference to duration D sc"emes.

Q.8 Loan duration preferred b$ customers.

$ 2 4,$"s 12

+ 3 4,$"s 25

# 4,$"s 2

* ;!", $) / 4,$"s 3?

8/18/2019 End Review Report

http://slidepdf.com/reader/full/end-review-report 38/44

I),"6",$i!):- -a+imum customers prefer t"e more t"an 8 $ears duration for personal

loan because of lon duration mont"l$ installment can be affordable b$ t"e customers.

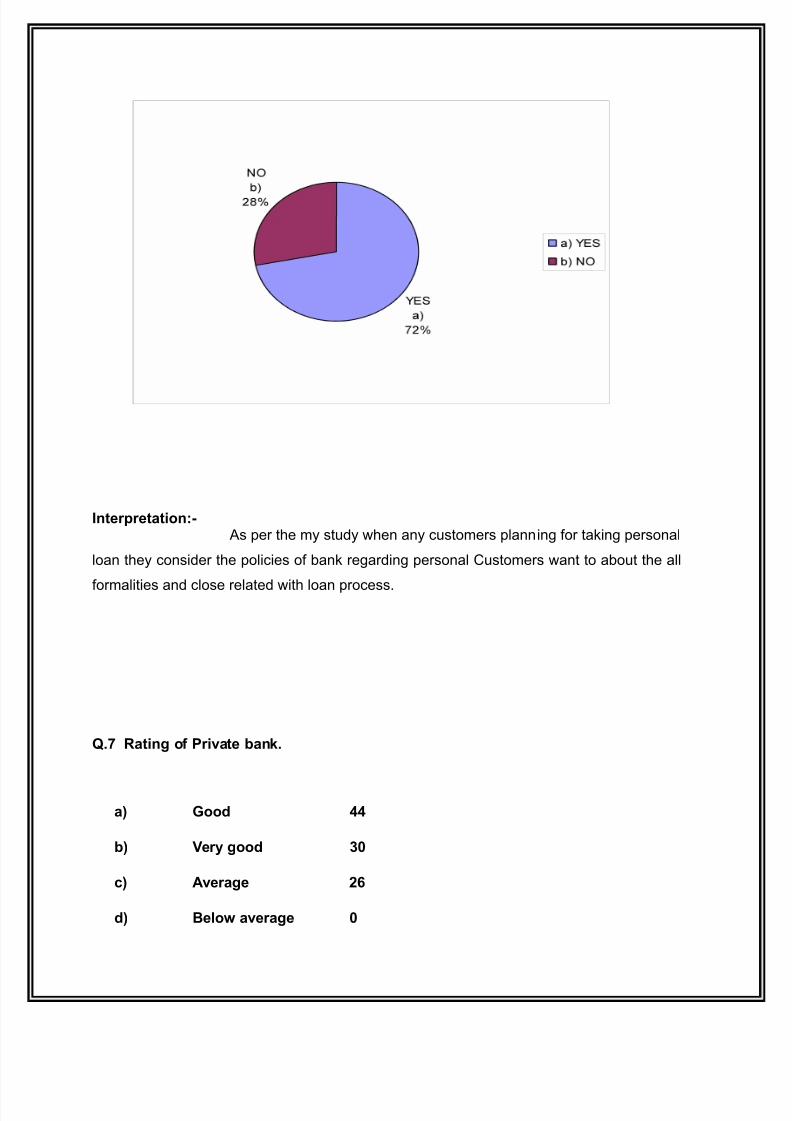

Q. Consideration on policies of bank reardin personal loan b$ customers.

$ YES 2

+ NO 25

8/18/2019 End Review Report

http://slidepdf.com/reader/full/end-review-report 39/44

I),"6",$i!):- As per t"e m$ stud$ !"en an$ customers plannin for takin personal

loan t"e$ consider t"e policies of bank reardin personal Customers !ant to about t"e all

formalities and close related !it" loan process.

. R$i)' !7 P"i$, +$)&.

$ G!!*

+ V,"4 '!!* 39

# A,"$', 2?

* B,%!0 $,"$', 9

8/18/2019 End Review Report

http://slidepdf.com/reader/full/end-review-report 40/44

I),"6",$i!):-

Accordin to m$ stud$ 68K customers are aree t"at private bank isver$ ood D ood because of ood services, more numbers of sc"eme.

Q. 7atin t"e Public bank.

$ G!!* /9

+ V,"4 '!!* 9

# A,"$', 19

* B,%!0 $,"$', 9

8/18/2019 End Review Report

http://slidepdf.com/reader/full/end-review-report 41/44

I),"6",$i!):- *K of customers aree t"at public bank is ver$ ood D ood.

because of ood imae, public sector bank, lo! interest rate. Compression to privtae bank

more customers aree t"at public bank is ver$ ood.

.8 O," $%% 6",7,",)#, !) , +$sis !7 i),",s "$, i=$', $)* s#,=,.

$ HDFC 3/

+ SBI ?/

8/18/2019 End Review Report

http://slidepdf.com/reader/full/end-review-report 42/44

I),"6",$i!):- 8K of customers prefer t"e ;& bank and 58 K prefer H'C bank

on t"e basis of interest rate, imae and sc"emes. T"e main reason is t"at t"e ;& bank is

public sector bank so customers trust on ;& bank more t"an H'C bank.

X

8/18/2019 End Review Report

http://slidepdf.com/reader/full/end-review-report 43/44

APPENDI

P,"s!)$% D,$i%s:

@ame: % YYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYY

Address: %

YYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYY

YYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYY

Ae: % YYYYYYYYYYYYYYYYYY contact no: % YYYYYYYYYYYYYYYYYY

1 P"!7i%, !7 ",s6!)*,)

(a) &usinessman (b) ;elf emplo$ed

(c) Borkin professional (d) Jovernment ;ervice Implo$ee

2 Wi# +$)& 0!(%* 4!( 6",7," 7!" 6,"s!)$% %!$)

(a) private &ank

(b) public &ank (c) <t"ers

3 W$ =$&, 4!( +,%i,, ! $&, , 6,"s!)$% %!$) 7"!= $)4 6$"i#(%$" +$)&

(a) Advertisement (b) friend

(c) amil$ member (d) ot"ers

W$ 0i%% 4!( #!)si*," 0i%, $&i)' %!$)

(a) nterest rate (b) sc"eme

(c) 'uration (d) ot"ers

/ F!" 0$ i=, i),"$% 4!( $, $&,) %!$)

(A) 1% $ears (b) %5 $ears

(c) 5%9 $ears (d) more t"an 9 $ears

8/18/2019 End Review Report

http://slidepdf.com/reader/full/end-review-report 44/44