energy investment ideas for growth, inflation and deflationmcdep.com/contraryenergy42.pdf ·...

TRANSCRIPT

www.mcdep.com 1

Energy Investment Ideas for Growth, Inflation and Deflation

Presentation by Kurt H. WulffThe 41st Contrary Opinion ForumBasin Harbor, VermontOctober 2, 2003

www.mcdep.com 2

Summary and Recommendation

Invest in Energy for Real Return with Inflation Protection, Deflation Resistance and Tax EfficiencyOil is Underpriced and Natural Gas is CleanValue Stocks for Energy Resources on Unlevered BasisBuy Canadian Oil Sands Trust (COSWF), Anadarko (APC) and Marathon Oil (MRO)Sell Kinder Morgan (KMI, KMR, KMP)

www.mcdep.com 3

Outline

Investment StrategyIndustry OutlookValuation MethodBuy IdeasSell Ideas

www.mcdep.com 4

Investment Strategy

Real Return Bond BenchmarksReal Rates Trend Lower

Inflation ProtectionInflation Expectations Trend HigherFree Money Spawns InflationTwin Deficits Are Back to Spawn Inflation

Deflation ResistanceChronic Deflation Concerns WaneAccidental Deflation Possible Any Time

Tax Efficiency

www.mcdep.com 5

Bond Benchmarks

4.84.0Nominal BondReturn (%/yr)

3.22.0Implied Inflation (%/yr)

1.62.0Real Bond Return (%/yr)

20th Century Actual

(Dimson, Marsh & Staunton)

Current Ten-Year Expectation

U.S. Treasury Securities

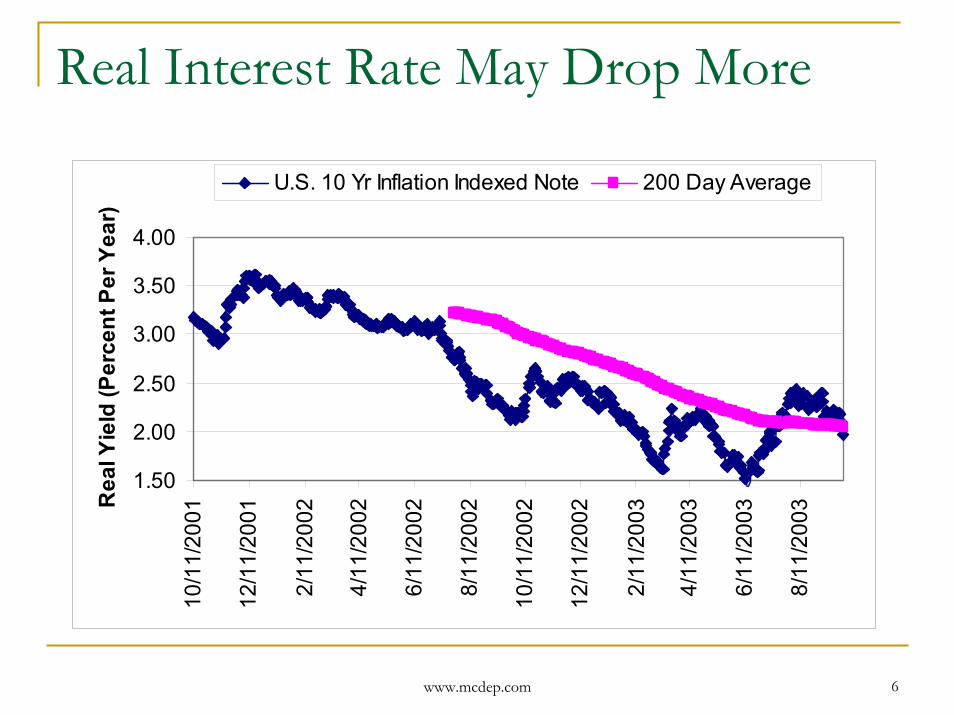

www.mcdep.com 6

Real Interest Rate May Drop More

1.50

2.00

2.50

3.00

3.50

4.00

10/1

1/20

01

12/1

1/20

01

2/11

/200

2

4/11

/200

2

6/11

/200

2

8/11

/200

2

10/1

1/20

02

12/1

1/20

02

2/11

/200

3

4/11

/200

3

6/11

/200

3

8/11

/200

3Rea

l Yie

ld (P

erce

nt P

er Y

ear)

U.S. 10 Yr Inflation Indexed Note 200 Day Average

www.mcdep.com 7

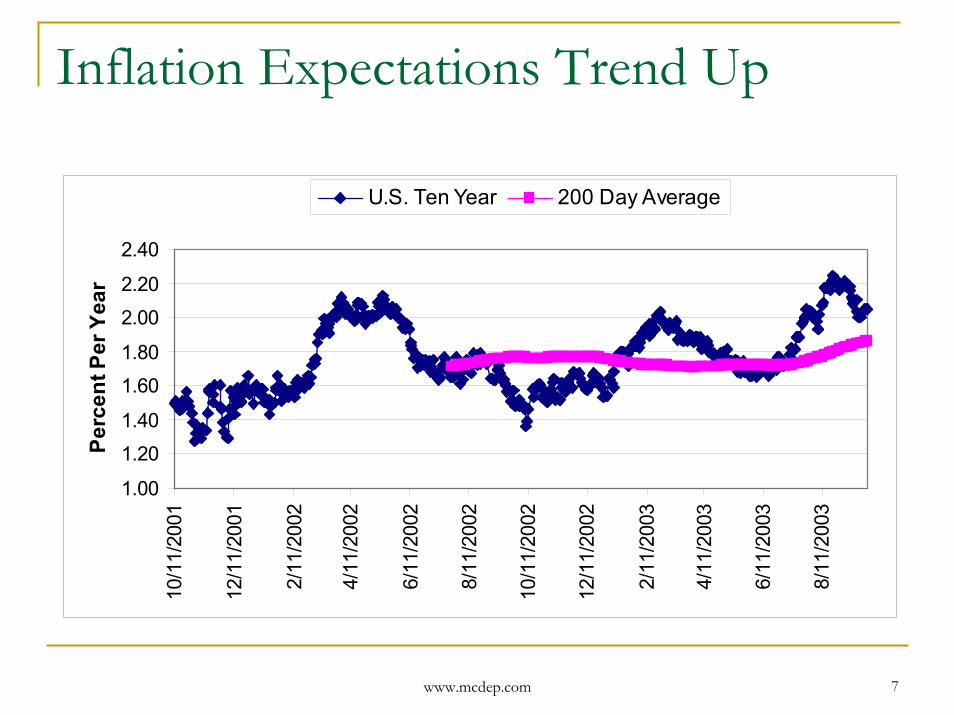

Inflation Expectations Trend Up

1.00

1.20

1.40

1.60

1.80

2.00

2.20

2.40

10/1

1/20

01

12/1

1/20

01

2/11

/200

2

4/11

/200

2

6/11

/200

2

8/11

/200

2

10/1

1/20

02

12/1

1/20

02

2/11

/200

3

4/11

/200

3

6/11

/200

3

8/11

/200

3

Perc

ent P

er Y

ear

U.S. Ten Year 200 Day Average

www.mcdep.com 8

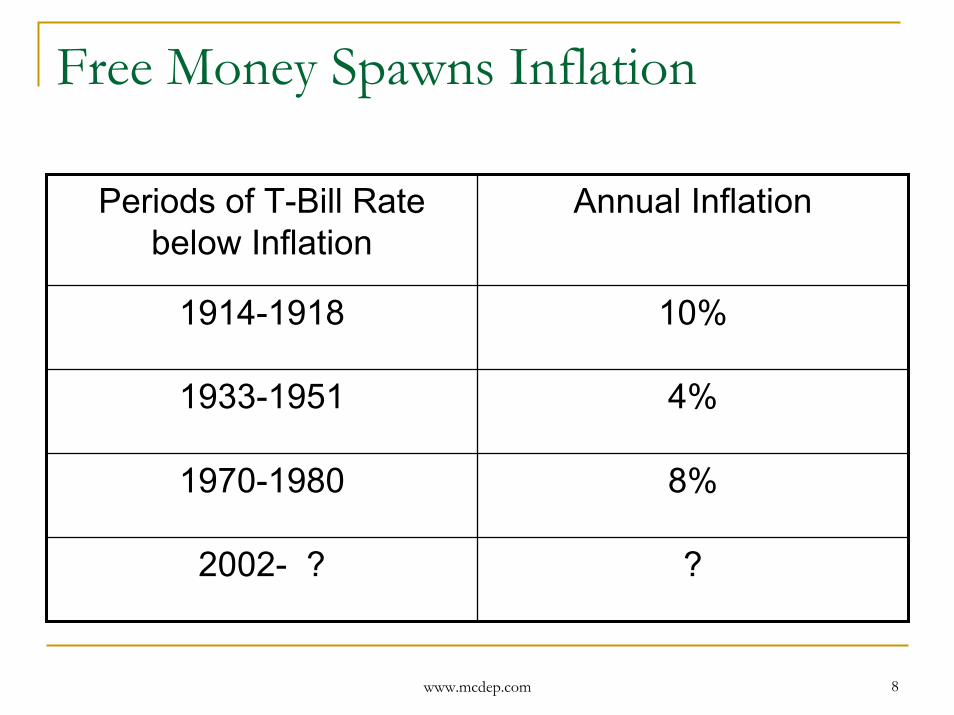

Free Money Spawns Inflation

?2002- ?

Annual InflationPeriods of T-Bill Rate below Inflation

8%1970-1980

4%1933-1951

10%1914-1918

www.mcdep.com 9

Twin Deficits are Back to Spawn Inflation

Trade deficit on the order of a half trillion dollars may signal weaker dollar and higher priced importsDollar exchange rate decline limited by inflation in other currenciesFederal budget deficit also on the order of a half trillion dollars

Military spendingSocial spending

www.mcdep.com 10

Resistance to Chronic Deflation Builds

3.00

3.50

4.00

4.50

5.00

5.50

6.00

10/1

1/20

01

12/1

1/20

01

2/11

/200

2

4/11

/200

2

6/11

/200

2

8/11

/200

2

10/1

1/20

02

12/1

1/20

02

2/11

/200

3

4/11

/200

3

6/11

/200

3

8/11

/200

3

Yiel

d (P

erce

nt P

er Y

ear)

U.S. Ten Year Note 200 Day Average

www.mcdep.com 11

Deflation Accidents Possible Any Time

High debt carries high riskMortgage market?Derivatives abuse?Securities fraud?Hedge fund speculation?Country defaults?Utility deregulation?

Be wary of high-leverage entities

www.mcdep.com 12

New Tax-Efficiency Favors Equity

Investors taxed at half or less the rate on stocks compared to bondsReducing tax on dividends and capital gains reduces tax on inflation which logically should not be taxedImprovement in relative appeal of equity helps overly leveraged companies to substitute equity for debt

www.mcdep.com 13

Industry Outlook – Natural Gas and Oil Most Valuable Energy Resources

OilDemand, Supply and PricePrice Cycle Turning Up2006 Oil Rising 10% Per YearSix-Year and One-Year Futures for Price Forecast

Natural GasReliable and CleanConvenient and EconomicDiscount to oil historical pricesPremium to oil in futures prices

Refining/MarketingPower

www.mcdep.com 14

Oil is Cheap

Demand linked to economic growthDemand artificially suppressed

Fuel taxesRationingAcceptance of dirtier fuels

Spare production capacity minimalMiddle East Religion and PoliticsFutures prices low

www.mcdep.com 15

Oil Price Cycle Turning UpLight Sweet Crude Oil, 1969-2003

0.0010.0020.0030.0040.0050.0060.0070.0080.00

1969

1971

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

Dol

lars

Per

Bar

rel

Inflation Adusted Current

www.mcdep.com 16

2006 Oil Rising 10% Per YearLight Sweet Crude Oil Futures

17.00

18.00

19.00

20.00

21.00

22.00

23.00

24.00

25.00

26.00

2/18

/200

0

4/18

/200

0

6/18

/200

0

8/18

/200

0

10/1

8/20

00

12/1

8/20

00

2/18

/200

1

4/18

/200

1

6/18

/200

1

8/18

/200

1

10/1

8/20

01

12/1

8/20

01

2/18

/200

2

4/18

/200

2

6/18

/200

2

8/18

/200

2

10/1

8/20

02

12/1

8/20

02

2/18

/200

3

4/18

/200

3

6/18

/200

3

8/18

/200

3

Dolla

rs P

er B

arre

l

December 2006 40 Week Average

www.mcdep.com 17

Rolling Six-Year and One-Year Futures Input to Fundamental Analysis

2.002.503.003.504.004.505.005.506.006.50

12/28

/2001

1/25/2

0022/2

2/2002

3/22/2

0024/1

8/2002

5/16/2

0026/1

3/200

27/1

1/200

28/8

/2002

9/5/200

210

/3/20

02

10/31

/2002

11/27

/2002

12/26

/2002

1/22/2

0032/1

9/200

33/1

9/200

34/1

6/200

35/1

4/200

36/1

1/2003

7/9/200

38/6

/2003

9/3/200

3

Dol

lars

Per

Mill

ion

BTU

12.0015.0018.0021.0024.0027.0030.0033.0036.0039.00

Dol

lars

Per

Bar

rel

72 Month Natural Gas 12 Month Natural Gas 72 Month Oil 12 Month Oil

www.mcdep.com 18

Natural Gas Reliable and Clean

No blackouts because of primitive transmission along wires strung on unsightly polesNo discharge of excessive waste heat into rivers and waterways, especially during hot monthsNo windless days or bird kills from whirring turbine blades on polesNo particulates or sulfur dioxide and far less carbon dioxide than from coalNo flooding of human or wildlife habitat behind dams

www.mcdep.com 19

Natural Gas Convenient and Economic

Turbine driven with waste heat recovery (combined cycle) most efficient generation of electricity from heatDistributable underground to point of use

Coal and nuclear like obsolescing mainframe computersNatural gas like personal computers

Highly refined oil most competitive alternative turbine and heating fuelStrong demand drives up natural gas priceOil a backup for natural gas

www.mcdep.com 20

Natural Gas Historical Discount to Oil

Natural Gas Price Discount, 1969-2003

0.00

0.20

0.40

0.60

0.80

1.00

1.20

196919711973197519771979198119831985198719891991199319951997199920012003

Nat

ural

Gas

/Oil

(6:1

= 1

.0)

www.mcdep.com 21

Natural Gas Futures PremiumNatural Gas/Oil Futures

0.70

0.80

0.90

1.00

1.10

1.20

1.30

1.40

1.50

12/2

8/20

01

1/28

/200

2

2/28

/200

2

3/28

/200

2

4/28

/200

2

5/28

/200

2

6/28

/200

2

7/28

/200

2

8/28

/200

2

9/28

/200

2

10/2

8/20

02

11/2

8/20

02

12/2

8/20

02

1/28

/200

3

2/28

/200

3

3/28

/200

3

4/28

/200

3

5/28

/200

3

6/28

/200

3

7/28

/200

3

8/28

/200

3

Nat

ural

Gas

/Oil

(6:1

=1.0

) Six-Year One-Year

www.mcdep.com 22

Refining Margin Improving

Refining Crack One-Year Futures and 40 Week Average

4.00

4.50

5.00

5.50

6.00

6.50

7.00

12/2

8/20

01

1/28

/200

2

2/28

/200

23/

28/2

002

4/28

/200

25/

28/2

002

6/28

/200

27/

28/2

002

8/28

/200

2

9/28

/200

210

/28/

2002

11/2

8/20

02

12/2

8/20

02

1/28

/200

3

2/28

/200

33/

28/2

003

4/28

/200

3

5/28

/200

3

6/28

/200

37/

28/2

003

8/28

/200

3

Dol

lars

Per

Bar

rel

www.mcdep.com 23

Power Underpriced – Dirt for DollarsElectricity vs. Natural Gas

-60-50-40-30-20-10

010203040

6/24

/200

2

7/24

/200

2

8/24

/200

2

9/24

/200

2

10/2

4/20

02

11/2

4/20

02

12/2

4/20

02

1/24

/200

3

2/24

/200

3

3/24

/200

3

4/24

/200

3

5/24

/200

3

6/24

/200

3

7/24

/200

3

8/24

/200

3

9/24

/200

3

Spar

k Sp

read

(Dol

lars

/Meg

awat

t Hou

r) East West

www.mcdep.com 24

McDep Ratio measures unlevered value

Market Cap and Debt to Present ValueUnlevered – counters the distortion of debtPresent value depends on interest rates, inflation, commodity prices, reserve life, investment requirements, operating costs

Weekly calculations for natural gas royalty trustsPeriodic reconciliation of cash flow multiple assessments with reserve life

www.mcdep.com 25

Weight Portfolio Positions onUnlevered Basis - Example

CNOOC Limited Kinder Morgan, Inc.Symbol CEO KMIRating Buy SellPrice Change 2003 31% 27%Debt/Present Value - 0.80 Portfolio Weight (Equal Unlevered PV) 83% 17%Weighted Gain 26% -5%

Portfolio Gain = 21%

www.mcdep.com 26

Buy energy producers

Mega Cap – CVX, RDDividends above TIPS real returnDividends likely to adjust for inflationLow debt offers deflation resistanceNew lower tax rate makes dividends more valuable

Producer/Refiners – COP, MRO, PTRNorth Am Natural Gas – ECA, BR, APC, XTO, SJTOil – CEO, EAC, COSWF

www.mcdep.com 27

Mega Cap Energy ProducersDominant Market Cap, Attractive Value

Price($/sh) Market Debt/

Symbol/ 24-Sep Cap Present McDepRating 2003 ($mm) Value Ratio

Exxon Mobil CorpoXOM 36.90 247,000 0.10 1.05 Total S.A. TOT 76.84 98,000 0.19 0.92 BP plc BP 42.65 158,000 0.15 0.87 Royal Dutch/Shell RD B 45.00 156,000 0.18 0.85 ChevronTexaco CorCVX B 72.33 77,000 0.22 0.82

www.mcdep.com 28

Energy Producer/RefinersPotential to Outperform Mega Caps

Price($/sh) Market Debt/

Symbol/ 24-Sep Cap Present McDepRating 2003 ($mm) Value Ratio

Murphy Oil Corporation MUR 59.83 5,530 0.26 1.34 Imperial Oil Limited (30%) IMO 37.81 4,290 0.12 1.04 Petro-Canada PCZ 40.35 10,690 0.19 0.92 Norsk Hydro ASA (49%) NHY 52.74 6,670 0.27 0.91 OAO Lukoil LUKOY 77.60 16,000 0.12 0.88 ConocoPhillips COP B 55.75 38,000 0.38 0.87 Marathon Oil Corporation MRO B 28.35 8,790 0.31 0.80 Suncor Energy SU 18.66 8,880 0.14 0.78 PetroChina Company Ltd (10%) PTR B 32.85 5,780 0.11 0.70

www.mcdep.com 29

Opportunity in Marathon Oil (MRO) About Every Ten Years

Double oil production from Yates Field in Texas free from price controls – DLJ Action Recommendation, October 1973Leading candidate for financial restructuring –DLJ Action Recommendation, April 1, 1981Vote for Spinoff – McDep Action Recommendation, March 19, 1990Set It Free from U.S. Steel– McDep Stock Idea, April 16, 2001

www.mcdep.com 30

Opportunity in Marathon (MRO) Today

Acquirable, efficient producer/refinerLow multiple of cash flow – EV/Ebitda = 5.4Value split approximately

45% oil and overseas natural gas35% U.S. Midwest refining/marketing20% North American natural gas

Competent managementStock should trade like peers and offer additional possible upside surprise

www.mcdep.com 31

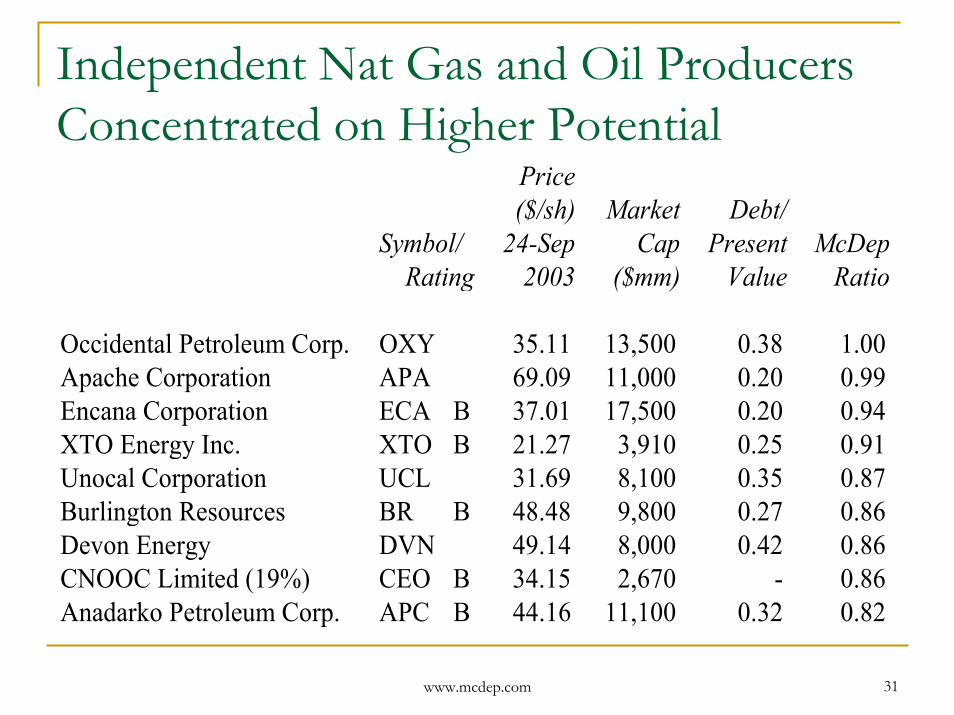

Independent Nat Gas and Oil Producers Concentrated on Higher Potential

Price($/sh) Market Debt/

Symbol/ 24-Sep Cap Present McDepRating 2003 ($mm) Value Ratio

Occidental Petroleum Corp. OXY 35.11 13,500 0.38 1.00 Apache Corporation APA 69.09 11,000 0.20 0.99 Encana Corporation ECA B 37.01 17,500 0.20 0.94 XTO Energy Inc. XTO B 21.27 3,910 0.25 0.91 Unocal Corporation UCL 31.69 8,100 0.35 0.87 Burlington Resources BR B 48.48 9,800 0.27 0.86 Devon Energy DVN 49.14 8,000 0.42 0.86 CNOOC Limited (19%) CEO B 34.15 2,670 - 0.86 Anadarko Petroleum Corp. APC B 44.16 11,100 0.32 0.82

www.mcdep.com 32

Anadarko (APC) – Acquirable Producer

Management ready to sellDisenchanted ownersStrategic complement to LNG

56% North American natural gasPremier Rockies acres (Union Pacific land grant)

Cost savings in overhead and hedgingMarketable reservesOpportune time in energy commodity cycle

www.mcdep.com 33

Income Buys

Price($/sh) Market Annual

Symbol/ 24-Sep Cap Income McDepRating 2003 ($mm) (%) Ratio

San Juan Basin Royalty Trust SJT B 17.88 830 10.6 1.03 CNOOC Limited (19%) CEO B 34.15 2,670 4.7 0.86 Royal Dutch/Shell RD B 45.00 156,000 4.4 0.85 ChevronTexaco Corporation CVX B 72.33 77,000 4.0 0.82 Marathon Oil Corporation MRO B 28.35 8,790 3.5 0.80 Canadian Oil Sands Trust (US$) COSWF B 28.95 2,500 5.0 0.71 PetroChina Company Ltd (10%) PTR B 32.85 5,780 6.2 0.70

www.mcdep.com 34

Canadian Oil Sands Trust (COSWF)Premium Characteristics

Sole asset 35% Syncrude Oil Sands PlantEqual economic partner Exxon et alLow fee, efficient, administrationVolume growth – 260mbd, 350mbd, plusReserves last practically foreverEnvironmentally desirable productDividend double by 2006, triple by 2007Dividend qualifies for 15% U.S. rate

www.mcdep.com 35

Canadian Oil Sands Trust (COSWF)Potential Ten-Bagger (10x in 10 years)

Ten-bagger growth rate: 26%/yearCanadian Oil Sands Trust Multipliers

Volume: 2xEV/Ebitda: 2xOil Price: 2x, 3x, 4x Dividend/Ebitda: 3x,4x

Downside: Cash Breakeven at US$13/barrel

www.mcdep.com 36

Sell pipeline partnerships– EEP, EEQ, EPN, KMI, KMR, KMPReal growth valued two to three times buy recommendationsMost inflation protection usurped by general partnerLimited deflation resistance because of high leverageAccounting misrepresents debt and high compensation to general partnerTax change expands competitive income opportunities

www.mcdep.com 37

Pipeline PartnershipsUnattractive Valuation

Price($/sh) Market Debt/

Symbol/ 24-Sep Cap Present McDepRating 2003 ($mm) Value Ratio

Kinder Morgan Energy Partners, L.P. KMP S 42.09 5,790 0.47 2.07 Kinder Morgan Management, LLC KMR S 37.20 1,710 0.47 1.88 Kinder Morgan, Inc. KMI S 53.63 6,600 0.80 1.56 Enbridge Energy Partners, L.P. EEP S 48.99 1,910 0.57 1.68 Gulfterra Energy Partners GTM S 40.38 2,220 0.56 1.68 Enbridge Energy Management, L.L.C EEQ S 44.39 420 0.57 1.58

www.mcdep.com 38

KMP/COS Side by Side

Arizona Pipe Failure

Notoriety

5.0%6.2%DistributionYield

.311.61Distribution/Equity Ebitda

.19.47Debt/PV

718EV/Ebitda

Canadian Oil Sands Trust

Kinder Morgan Energy Partners

www.mcdep.com 39

Moral Hazard in Pipeline Partnerships

General Partner takes up to 50% of cash flow for no capital outlay exploiting moral hazard

Partnerships skimp on debt servicePartnerships skimp on maintenance and safety

Failure of 48-year old Arizona pipeline triggered gasoline shortages in August 2003

Rating agencies allow outlawed debt pyramidsSEC exempts partnerships from Sarbanes OxleyNYSE facilitates excessive GP compensationFERC allows asset stripping at public expense

www.mcdep.com 40

What is Contrary Opinion in Energy?

Oil price likely be to higher than in the futures market, possibly by a lot in a surprise inflationary environmentNatural gas premium to oil likely to be higher than in the futures market as environmental advantages become more valuable as the politics sort outUnlevered present value of cash flow the most useful tool of energy valuationThe stocks that pay the least amount of fees to managers and financiers may be the among the best opportunitiesThe SEC, the NYSE, the Federal Energy Regulatory Administration, and the debt raters do not appear to protect thepublic interest in pipeline partnerships

www.mcdep.com 41

Wrapup

Invest in Energy for real return, inflation protection, deflation resistance, tax efficiencyOil is cheap, natural gas is cleanOwn stocks on basis of unlevered holdings of energy resources and businessesBuy Marathon, Anadarko, Canadian Oil Sands Trust and other energy producersSell Kinder Morgan and other pipeline partnerships

www.mcdep.com 42

Disclaimer and Disclosure

Independent energy investment analysis by Kurt Wulff doing business as McDep Associates is posted at www.mcdep.com. Mr. Wulff is not paid by covered companies. Neither he nor his spouse act contrary to a buy or sell rating. Analyses are prepared from sources and data believed to be reliable, but no representation is made as to their accuracy or completeness.