energy technology landscape: one indian …. ajit sapre reliance technology group 10th october, 2012...

TRANSCRIPT

Dr. Ajit Sapre

Reliance Technology Group

10th October, 2012

Energy Technology Landscape: One Indian Perspective

2

Outline

1. Strategic Drivers & Challenges

2. Climate Outlook

3. Resource Outlook

4. Role of Natural Gas

5. Role of Biotechnology

6. Inclusive Innovation – Gandhian Engineering

7. Academia Industry Interaction

1 2 3 4 5 6 7

Copyright © 2012 Reliance: All rights reserved.

3

Global

Green

Strategic

drivers

Growth

Emerging chemical leaders

from ME and Asia

Increasingly global supply

chain in fuels/ petrochemicals

Favoring Asia and ME

Commoditization of

specialties

Designer materials

Alternate feed-stocks

Carbon risk

Advancing “green wave”

Long-term Strategic Drivers & Challenges

Global “Green” Global Growth

“Green” Growth ?

Sustainability &/ or

Energy Security

Challenges

In the uncertain world innovation key to meet future global challenges

1 2 3 4 5 6 7

Copyright © 2012 Reliance: All rights reserved.

4

Climate Is Changing

Need collective action to mitigate potential disastrous consequences

Globally, June 2012 was:

36th consecutive warmest June

Mean temperature is on the rise, decade

over decade

Longer and hotter summers; more intense

heat waves

Higher temperatures lead to lower crop

fertility

More instances of weather deviations from

mean of the decade

In 1951-61 extreme weather happened

1/8% of time, now it happens 8% of time

Source: Bell Weather, The Economist, Aug 11, 2012; Hansen et al. PNAS

1 2 3 4 5 6 7

Copyright © 2012 Reliance: All rights reserved.

5 1 2 3 4 5 6 7

Replace with Arctic

Arctic Melting has accelerated

Global warming effect – More melting in summers would shrink the size over time Copyright © 2012 Reliance: All rights reserved.

6 1 2 3 4 5 6 7

Replace with Arctic

Arctic Melting has accelerated

Global warming effect – More melting in summers would shrink the size over time

Himalayan Glaciers are Retreating at 0.6% Area Reduction Annually

India at the risk of losing its major rivers,

source of drinking water and irrigation for more than one billion people

Copyright © 2012 Reliance: All rights reserved.

7

Global Action on Climate Mitigation – Moving Slowly

Advanced countries’ emissions increased in recent years,

both absolute and per capita, failing to meet Kyoto

protocol targets

Advanced countries have not done enough

“Durban Platform” agreement in Dec 2011 – Legally

binding for all countries – Terms to be agreed by 2015, to

come into effect by 2020

Goal is to ensure less than 2°C temperature rise

Specifics on the targets and aid money to developing

countries

Shale gas boom in the US – Is it a blue bridge to green

future or death of nuclear & renewables?

Need urgency in action by the world political leaders

“Okay – it’s agreed; we announce

– ‘to do nothing is not an option!’

then we wait and see how things

pan out. . . ” www.private-eye.co.uk

1 2 3 4 5 6 7

Copyright © 2012 Reliance: All rights reserved.

8

GHG Emissions Rose Dramatically since

1850 with Accelerating Industrial Revolution

However, since 1850, India contributed only 2.4% to global cumulative emissions,

and 4% since 1990

Region /

Country

Population

(million

GDP

(billion

2000 US $)

CO2

Emissions

(MTCO2)

Per-Capita

CO2

Emission

(tonnes)

World 7041 39493 28962 4.38

China 1347 2623 6071 4.58

India 1210 771 1146 1.18

Japan 128 5205 1236 9.68

USA 314 11468 5769 19.10

Germany 82 2065 798 9.71

1 2 3 4 5 6 7

Copyright © 2012 Reliance: All rights reserved.

9

Consumers in the West also Responsible for Emissions increase in the East

Today, emissions in a country accounted

through production and transportation of

goods there

Carbon leakage – Emissions in producing

countries to supply goods for consuming

countries

Consumption based CO2 accounting may

be more equitable?

Asia, particularly China, is a factory to the world

1 2 3 4 5 6 7

Copyright © 2012 Reliance: All rights reserved.

10

Equity Principle: Common but Differentiated Responsibilities

Emissions in Advanced Countries affect

the climate in Developing Countries

After 1850, ~70% CO2 emissions came

from US, EU, Russia, Japan and Canada,

with US leading the pack with 30%

Finite safe capacity of the atmosphere to

absorb greenhouse gases is a common

resource that belongs to all human

beings but was ‘expropriated’ in large

part by the Advanced Counties

Developing Countries provide a fertile ground for implementing novel climate

mitigation technologies, and innovative infrastructure development opportunities,

e.g., distributed power, bio-fuels, etc.

Developing countries cannot be expected to take on a disproportionate burden

Pic source: www.itsgettinghotinhere.org, A youth climate movement

1 2 3 4 5 6 7

Copyright © 2012 Reliance: All rights reserved.

11

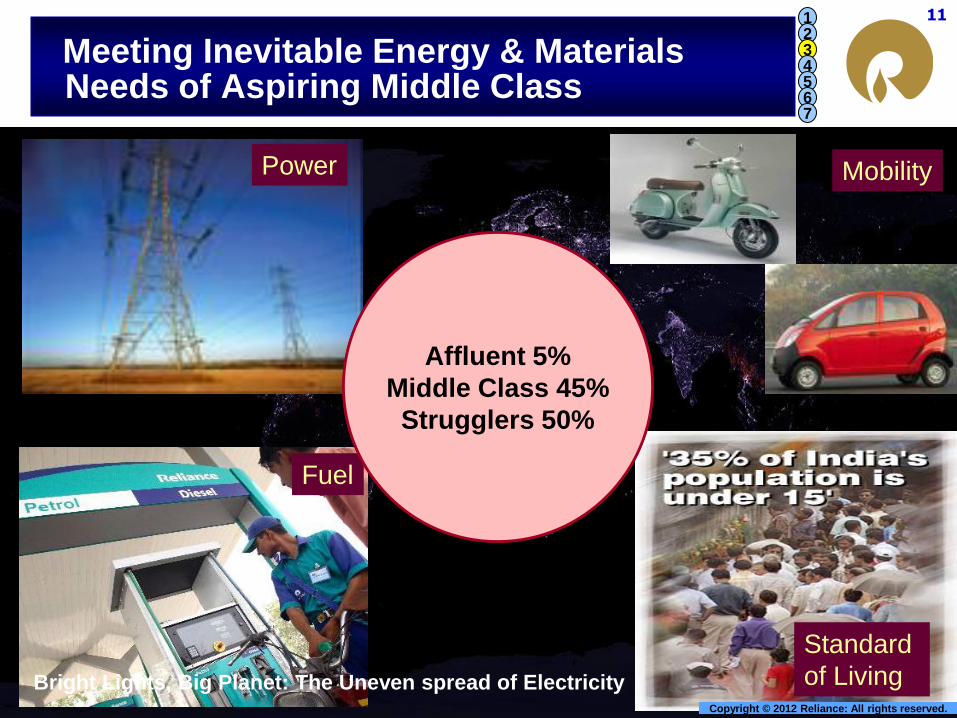

Meeting Inevitable Energy & Materials Needs of Aspiring Middle Class

Sustainability has to

account for well being

Of “Aspiring Middle

Class”

Power Mobility

Fuel

Standard

of Living

Sustainability has to

account for well being

of “Aspiring Middle Class”

Bright Lights, Big Planet: The Uneven spread of Electricity

Affluent 5%

Middle Class 45%

Strugglers 50%

1 2 3 4 5 6 7

Copyright © 2012 Reliance: All rights reserved.

12

The Global Energy Challenge

3,000 10,000 15,000 25,000

En

erg

y d

em

an

d

Industrialization

and personal

mobility take off

Services dominate

growth and basic

households energy

needs are met

Urbanization

Economic growth

requires little

additional energy

GDP/Capita in constant PPP terms

Demand for energy is growing rapidly as countries like India enter the most

energy-intensive phase of economic development

India

China

OECD (17% world population)

1 2 3 4 5 6 7

Non-OECD (83% world population)

Copyright © 2012 Reliance: All rights reserved.

13

The Global Energy Challenge

3,000 10,000 15,000 25,000

En

erg

y d

em

an

d

Urbanization

GDP/Capita in constant PPP terms

Demand for energy is growing rapidly as countries like India enter the most

energy-intensive phase of economic development

India

China

OECD (17% world population)

Leapfrogging

Efficient

Technology

Development

& Deployment

- - Sustainable

Path

More, Secure and Responsible energy technology for the growing world

Traditional

1 2 3 4 5 6 7

Non-OECD (83% world population)

Unsustainable

Copyright © 2012 Reliance: All rights reserved.

14

Indian Energy Demand & Supply

Energy efficient clean coal conversion technologies needed

Annual Energy Demand to increase from 590

Mtoe in 2009 to about 1,299 Mtoe by 2030

Today India imports ~70% crude oil and ~30%

natural gas (>$ 80 billion revenue outgo)

Today India has

0.6 % of World’s Gas reserves

0.4 % of Worlds Oil reserves

7% of World’s Coal reserves

Coal has a major role to meet India’s energy

needs

Coal demand will grow at a rate of ~8%/ yr

Indigenous production + imports

Carbon Capture & Sequestration critical

technology with growth of coal burning

Current

Source- Integrated Energy Policy- Planning Commission, Govt. of India

India is 5th largest energy consumer in the world 2030

India scenario (MMTPA) 2010 2015

Coal consumption 656 878

Coal imports 73 240

Petcoke capacity 7 16

1 2 3 4 5 6 7

Copyright © 2012 Reliance: All rights reserved.

15

Shale Gas Rapidly Replacing Coal in US

Shale gas emits 50% less carbon

dioxide than coal

If large scale projects in major growth

economies e.g. India and China, shift

to shale gas, carbon emission trends

could be reversed

In US, shale gas went from 1% of gas

production in 2001 to 37% in 2011

China plans shale gas output rise from

6.5 billion cubic meters in 2015 to 100

billion cubic meters in 2020

Cheap shale gas has taken a big bite

out of coal very quickly

Build a successful worldwide cooperation on shale gas technologies to help

near-term reduction in CO2

US Electricity Fuel mix

1 2 3 4 5 6 7

Copyright © 2012 Reliance: All rights reserved.

16

Shale Gas in India

Demand is outpacing supply, India has been a net

importer of natural gas since 2004

In 2010, 1.4 tcf produced and 0.5 tcf imported, with

1.5 tcf of unmet demand

Technically recoverable shale gas resources in

India at 63 tcf, compared with 1,275 tcf in China,

and 1,250 tcf in US and Canada

– ONGC & Schlumberger have started exploration

US-India MOU “Shale Gas Work Plan” to help India move in the right direction – Part

of Joint Clean Energy R&D center in India

India faces large gap in water supply and projected demand, 50% shortfall by 2030, at

~1,500 bcm demand with current supply of 740 bcm

Water-less technologies are needed, e.g., propane fracturing instead of hydraulic

fracturing

Advanced fracking technology needed to exploit shale gas resources in India

1 2 3 4 5 6 7

Copyright © 2012 Reliance: All rights reserved.

17

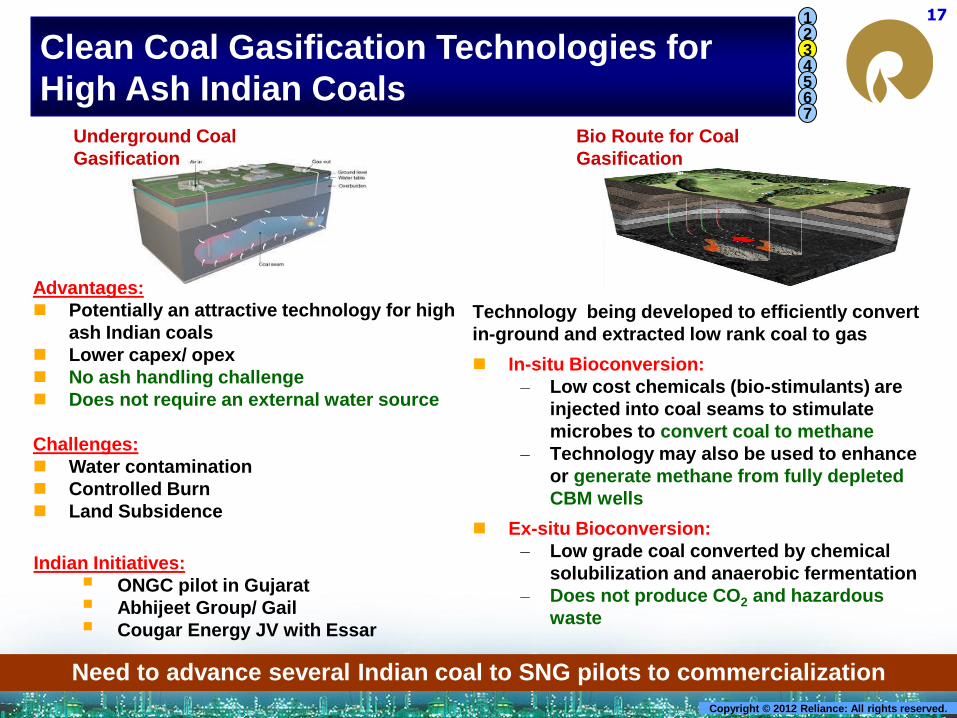

Clean Coal Gasification Technologies for

High Ash Indian Coals

Need to advance several Indian coal to SNG pilots to commercialization

Indian Initiatives:

ONGC pilot in Gujarat

Abhijeet Group/ Gail

Cougar Energy JV with Essar

Technology being developed to efficiently convert

in-ground and extracted low rank coal to gas

In-situ Bioconversion:

– Low cost chemicals (bio-stimulants) are

injected into coal seams to stimulate

microbes to convert coal to methane

– Technology may also be used to enhance

or generate methane from fully depleted

CBM wells

Ex-situ Bioconversion:

– Low grade coal converted by chemical

solubilization and anaerobic fermentation

– Does not produce CO2 and hazardous

waste

Underground Coal

Gasification

Bio Route for Coal

Gasification

1 2 3 4 5 6 7

Advantages:

Potentially an attractive technology for high

ash Indian coals

Lower capex/ opex

No ash handling challenge

Does not require an external water source

Challenges:

Water contamination

Controlled Burn

Land Subsidence

Copyright © 2012 Reliance: All rights reserved.

18

Reliance Petcoke Gasification Project – Deeper Integration of Refinery with Petrochemicals

Largest Pet-coke Gasification Project in the World – Future Ready for CO2 Mitigation

Largest refinery in the world with 1.4 MM bbl/day capacity, produces 6.4 MMT/yr petcoke

Petcoke gasification with 12 gasifiers – Kick off in May 2012, start-up by May 2015

Ultra clean refinery on path to become a bottomless refinery

CPP = cogen power plant

PSA = pressure swing adsorption Conoco-Philips gasifier

1 2 3 4 5 6 7

Copyright © 2012 Reliance: All rights reserved.

19

Sustainability and Reliance

"We have embraced sustainability as our core business strategy. We believe

sustainability is the very foundation of lasting success. We will use sustainability

principles to drive process innovation, new product development, improving

manufacturing efficiencies and reducing material and energy consumption. This

commitment is backed by active initiatives on the ground.“

Mukesh D. Ambani

CMD Reliance Industries

RIL’s Sustainability Objectives:

• Energy Security • Energy Efficiency • Renewable Energy • Socially Responsible Operations • Poverty Eradication

RIL's sustainability reporting quality has been rated as “Good" (highest rank) by

International Finance Corporation (World Bank Group)

1 2 3 4 5 6 7

Copyright © 2012 Reliance: All rights reserved.

20

Change in Energy Resources with Time

Will the world go back to biomass era to meet sustainability goals?

Will Biomass increase in the energy mix?

Will coal usage go up?

Post Fukushima what is the future of nuclear energy?

Will NG remain bridge to renewable energy?

20

10

1 2 3 4 5 6 7

Copyright © 2012 Reliance: All rights reserved.

21

Nuclear Energy Potential Future

Thorium – More abundant and safer than Uranium

Thorium waste has shorter half-life

Environmental friendly extraction with less CO2

emissions when compared to Uranium

India plans to start constructing a 300 MW Thorium

reactor in 2016-17

India has 25% of world’s Thorium reserves, and plans

to meet 30% of its energy demand with thorium-based

reactors by 2050

Need to develop safer, modular, scalable nuclear technology options

Need commercialization of latest generation nuclear reactors that addresses major concerns

(safety, uranium utilization, economics, proliferation, waste). Some examples:

Light water reactors – DEER by Radix Power & Energy, mPower by B&W, Russia’s KLT-40S

Fast neutron reactors – G4M by Gen4 Energy, STAR series at Argonne National Lab

Graphite-moderated high temperature reactors – China’s HTR-10, South Africa’s PBMR

Pressurized heavy water reactors – India’s PHWRs, Chashma in Pakistan

Travelling Wave Reactor using spent Uranium, buried deep in the ground – Terra Power

1 2 3 4 5 6 7

Copyright © 2012 Reliance: All rights reserved.

22

Future of Liquid Fossil Hydrocarbons?

Energy security will likely drive sustainability agenda

Food Heat Light

Clothes House

1 2 3 4 5 6 7

Copyright © 2012 Reliance: All rights reserved.

23

World Energy Mix – One forecast

World markets in fuels/ petrochemicals are interconnected

• Developing economies drive energy

consumption growth accounting for

65% of world consumption

• Fuel substitution happening in

Developed countries while all fuels

expanding in Developing countries

• Largest fuel contribution comes from

natural gas, which is around 31%

• Globally energy intensity is expected to

reduce and converge

• Convergence happening due to connected

world and rapid diffusion of technology

BP Energy Outlook 2012

1 2 3 4 5 6 7

Copyright © 2012 Reliance: All rights reserved.

24

Shale gas – Game changing US Energy/ Petrochemicals Outlook

NG price decoupled from oil in US

• US natural gas prices are under- $3/mmBTU

• Indian LNG marginal cost is as high as $15/mmBTU

• Boost to Petrochemicals due to associated ethane in shale gas

• LNG exports from US likely in the future?

Huge shale gas finds and production has decoupled gas price from oil in US

1 2 3 4 5 6 7

Copyright © 2012 Reliance: All rights reserved.

25

Use of NG in Transportation Sector?

Direct NG usage could have immediate impact on the transportation sector

Cost & Efficiency ?

Battery Technology/ Vehicle cost /

Recharging Infrastructure?

Natural Gas Gas

Infrastructure

• NG vehicles (CNG, LNG) likely to penetrate in heavy duty and fleet applications

• Minor modifications can convert gasoline and diesel engines into NG vehicles

• EV’s remain a technological and infrastructure hurdle

1 2 3 4 5 6 7

India has two million

CNG vehicles &

sector is growing fast

Copyright © 2012 Reliance: All rights reserved.

26

Penetration of Gas in Transport and Hybrids – Reduced Refining Capacity

0

20

40

60

80

100

120

140

160

CNG Diesel Gasoline

Passenger car sales by type Transport fuel demand by energy

type

CNG – Cleanest for vehicles, Lowest

GHG • Significant growth potential for gas in liquid fuels dominated

transport sector

• CNG - cleanest fossil fuel + with low price (especially in US)

• Electric and hybrid vehicles will also have significant share in

new vehicles sold by 2030

• Impact on the demand for refinery liquids will lead to capacity

rationalization and cuts in crude runs

Natural gas could be the next major transportation fuel – CNG/LNG/Electricity

BP Energy Outlook 2012

Transport

Emissions

1 2 3 4 5 6 7

Copyright © 2012 Reliance: All rights reserved.

27

Distributed Generation & Distributed Consumption for Electricity

4

Today’s Grid Electricity …

Power park

Hydrogen Storage

Industrial DG

Tomorrow’s Likely Choices …

Combined Heat and Power

Fuel Cell

e -

e -

Wind Farms

Rooftop Photo-voltaics

Remote Loads

Load as a resource

SMES

Smart Substation

Fuel Cell

Could we economically develop distributed production and consumption infrastructure for liquid fuels -- bio refineries?

Smart grid technology could accelerate distributed generation/consumption

Energy losses 68% for electricity vs. 8%

for natural gas to consumers

Village level mini-grids in India based

on gasifying agricultural waste

1 2 3 4 5 6 7

Copyright © 2012 Reliance: All rights reserved.

28

Growing Importance of Bio-based approach in Three main pillars of Indian Economy

Does bio-refinery concept provide a leap frogging technology opportunity ?

Source : India Brand Equity Foundation

Today’s cooking stove

only 10% energy

efficient

1 2 3 4 5 6 7

Copyright © 2012 Reliance: All rights reserved.

29

0102030405060708090

1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

Wheat $/MWh(t)

Oil $/MWh(t)

Bio-fuels or Renewable Electricity?

1 Ha land – 10 ton wheat/yr –

40 MWh/ha. yr energy

1 Ha land- 100 tons/yr energy crops

400 MWh/ha.yr energy

1Ha land – One 2 MW Wind Mill

Even with only 25% on time

– 4000 MWh/yr

Wind Mill is 10-100 times more

productive

Need on-purpose energy crops orders of magnitude more productive

Today, we have

reached Wheat & Oil

Energy Equilibrium

on Pricing

Oil Calorific value – 12MWht

Wheat Calorific value – 4MWht

US Oil & wheat prices $/MWht

1 2 3 4 5 6 7

Copyright © 2012 Reliance: All rights reserved.

30

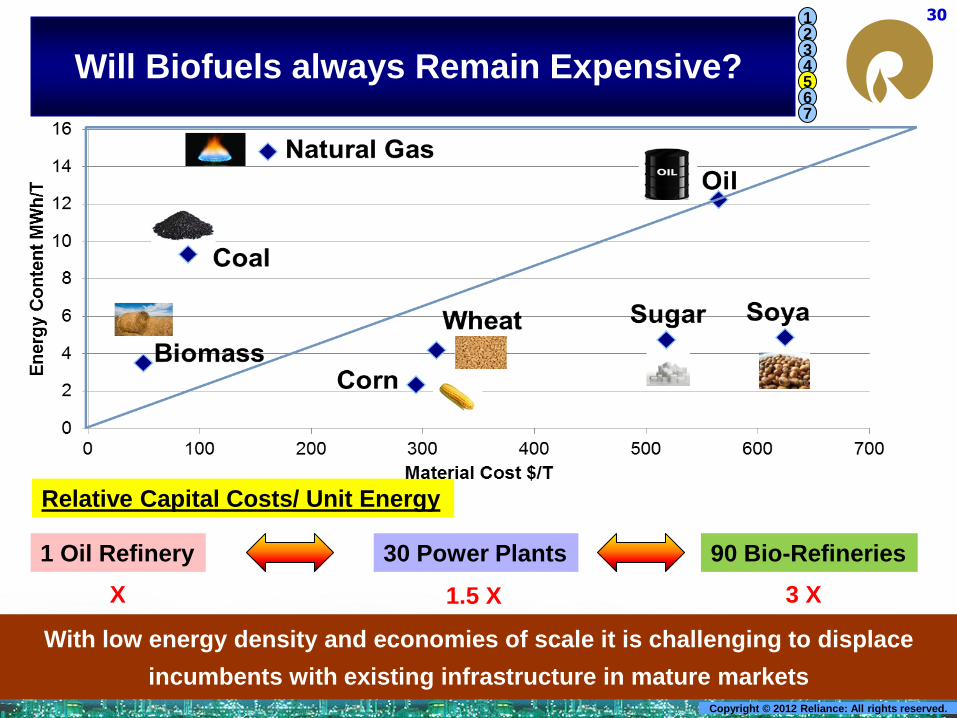

Will Biofuels always Remain Expensive?

With low energy density and economies of scale it is challenging to displace

incumbents with existing infrastructure in mature markets

1 Oil Refinery 90 Bio-Refineries 30 Power Plants

Relative Capital Costs/ Unit Energy

X 3 X 1.5 X

1 2 3 4 5 6 7

Copyright © 2012 Reliance: All rights reserved.

31

18

48

102

127

202

635

10,000

140,000

Transitioning to Low Areal Productivity Resources ?

Pumpjack

Algae farm

Jatropha

Corn

Do we need a distributed production/ consumption model for transportation fuel?

Require:

Large area to support the current

demand level

Overhaul of energy distribution

infrastructure to suit the fragmented

energy generation

1 2 3 4 5 6 7

Copyright © 2012 Reliance: All rights reserved.

32

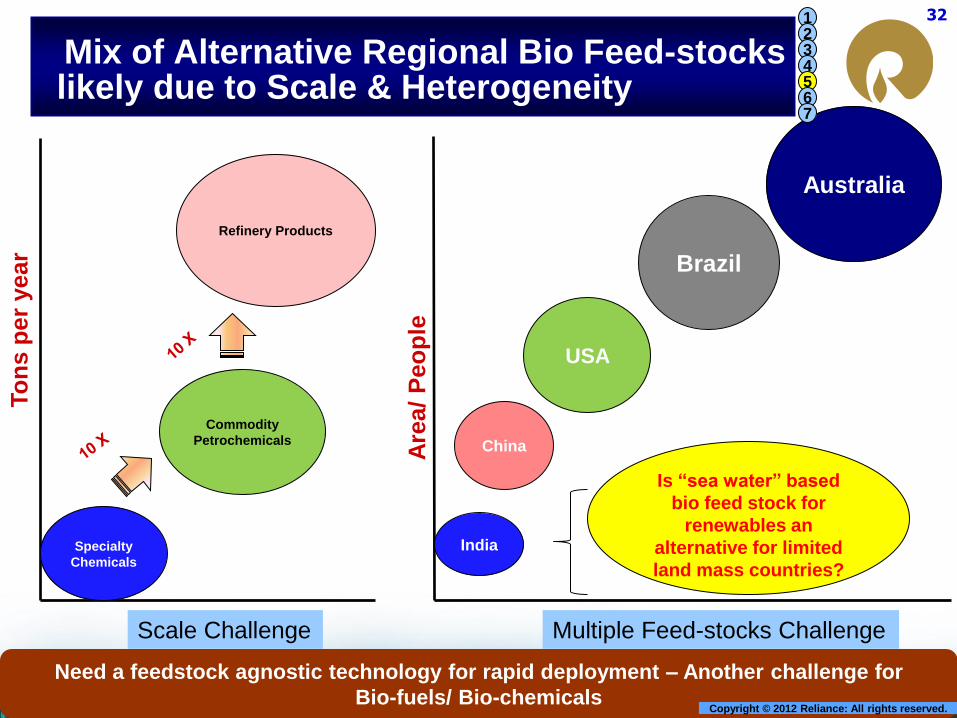

Mix of Alternative Regional Bio Feed-stocks likely due to Scale & Heterogeneity

Need a feedstock agnostic technology for rapid deployment – Another challenge for

Bio-fuels/ Bio-chemicals

To

ns p

er

year

Specialty

Chemicals

Commodity

Petrochemicals

Refinery Products

Scale Challenge

India

China

USA

Brazil

Australia

Are

a/

Peo

ple

Is “sea water” based

bio feed stock for

renewables an

alternative for limited

land mass countries?

Multiple Feed-stocks Challenge

1 2 3 4 5 6 7

Copyright © 2012 Reliance: All rights reserved.

33

Algae & Bio-technology for Energy, Petrochemicals & Wellness Products

Algae fuel can be grown

on marginal land with

non-potable, saline and

even waste water

Every gallon of algal oil produced consumes 12-15 kg of CO2

CO2

~600 kg Algal oil

1 barrel

Plant mass

on Earth

Photosynthesis

on Earth Aquatic plants Terrestrial plants

610

12

Sugarcane Switch

grass Algae

58

Corn

Growth

efficiency

MT/acre/yr

Sun Light + CO2 +Sea Water Bio- Oil, Bio-diesel, Ethanol, Nutraceuticals

Genetic modifications can improve yield, selectivity, tolerance to external factors

Algae are most efficient convertor of sunlight

Biomass Harvesting or Product Secretion ?

Open Pond Or Closed Photo- Bioreactor ?

1 2 3 4 5 6 7

Copyright © 2012 Reliance: All rights reserved.

34

Working through Biology Hierarchy

Genomics/systems biology, Environment

DNA manipulation,

mutation, synthetic biology,

pathway engineering, gene

expression

Kilo Biology

Nano

Biology

Production

Scale-up of biological systems to large scale industrial applications remain a challenge

Circadian rhythm

manipulation?

Is photosynthesis the

ultimate rate limiter for

metabolic pathway

manipulation

(PSI, PSII, etc.) ?

Photosynthesis

Metabolic Pathway

Engineering

1 2 3 4 5 6 7

Copyright © 2012 Reliance: All rights reserved.

35

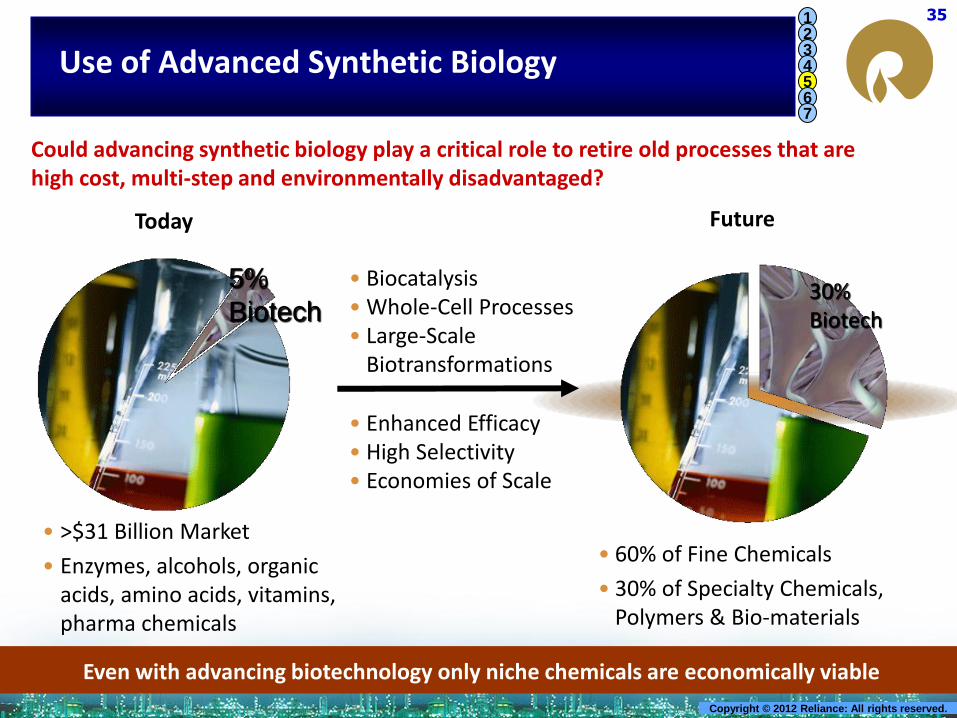

Use of Advanced Synthetic Biology

Even with advancing biotechnology only niche chemicals are economically viable

Could advancing synthetic biology play a critical role to retire old processes that are high cost, multi-step and environmentally disadvantaged?

Today

• >$31 Billion Market

• Enzymes, alcohols, organic acids, amino acids, vitamins, pharma chemicals

• Biocatalysis • Whole-Cell Processes • Large-Scale

Biotransformations

• Enhanced Efficacy • High Selectivity • Economies of Scale

Future

• 60% of Fine Chemicals

• 30% of Specialty Chemicals, Polymers & Bio-materials

30% Biotech

5%

Biotech

Today

1 2 3 4 5 6 7

Copyright © 2012 Reliance: All rights reserved.

36

Future of Bio based Commodity Chemicals – Ethylene to PE

Will cost of production of bio petrochemicals ever match fossil route?

14 40

12

10 30

8

6 20

4

210

0 0

20 40 60 80 100 120 140 160 180

Crude Price ($/bbl)

Su

gar P

rice (c

en

ts/lb

) C

orn

Pri

ce (

$/B

u)

Crude Preferred

Corn or Sugar Preferred

Cellulosic sugars

today

• North America becomes net exporter of energy

• Long-term Crude oil prices could be soft

• Developing countries growth

continues to stress supply

OR

1 2 3 4 5 6 7

Renewables are far too expensive to compete with fossil fuels if their price

is based solely on the cost of energy production

Copyright © 2012 Reliance: All rights reserved.

37

37

Bottles

Filling

Processing

Cleaning

Pillows

Fibers

Flakes

Collection

Recycling: Green Polyester in the Indian context

Business to fulfill societal obligation along with earning adequate returns for shareholders

– Waste bottles collected by unskilled

uneducated manpower - reduces

land fill & provides earning

opportunity for downtrodden

– Processed to produce fibers

– Fibers used to make pillows

– Business earning above cost of

capital – Waste to wealth

Improve quality of life for folks at the bottom of the pyramid by giving them work

opportunity

Bottle to Bottle Recycle of Polyester to same quality is also a reality

Average rate of recycling (in%) excluding re-use

30

47.353

70

0

20

40

60

80

US Germany Japan India

1 2 3 4 5 6 7

Copyright © 2012 Reliance: All rights reserved.

38

The Ethical Question !

40% of US corn is directed to run cars

European commission admits that the

targeted 10% of transportation biofuels

by 2020 would raise cereal prices by 3 –

6%

With every 1% increase in food prices, 16

million people go hungry

By 2021, 14% of world’s maize and other coarse grains, 16% of vegetable oil, and

34% of sugarcane will go to the fuel tank, only partly coming from increase in

production

Radical overhaul needed in policy and food production to ensure food supply for

the world’s poor

Need pragmatic and flexible policies to ensure a holistic perspective

Must the poor go hungry just so the rich can drive? --- The Guardian, Aug 13, 2012

1 2 3 4 5 6 7

Copyright © 2012 Reliance: All rights reserved.

39

Fundamental Belief that Sustainability can be achieved by poverty

eradication and meeting future aspirations of under privileged

It also means that not only to have innovation and passion but also compassion

Gandhian Engineering

“The earth has enough for Everybody’s needs, but not enough for Anybody’s greed”

“Poverty is the worst form of violence”

“More from Less for More and More”

1 2 3 4 5 6 7

Source: C K Prahalad and R A Mashelkar

Copyright © 2012 Reliance: All rights reserved.

40

Gandhian Engineering: Inclusive Innovation

Examples of Disruptive Inclusive

Innovations: – Tata-Nano : Affordable cars for 2000 $ !!! Order of magnitude cheaper with no

compromise of features

– Reliance Cellphones : Phone call for the price of postcard

(i.e. 0.005$/min), Order of magnitude cheaper with advanced features

Need boundary-less global open innovation framework

High Performance at Ultra low cost: Make products affordable to the poor without compromising quality so that even rich will desire these products

Involve the “Bottom of the Pyramid” for sustainability of Self, Society, Country

and the World Gandhian Engineering is as much needed by the rich as by the poor because

ultimately it affects the entire mankind as we run out of non-renewable resources

1 2 3 4 5 6 7

Copyright © 2012 Reliance: All rights reserved.

41

Biogas – An Indian Initiative for Distributed Energy

1897 – First ever anaerobic digester in

Mumbai, India, utilizing human waste to

generate gas for lighting needs

1937 – First successful manure to biogas

plant by S.V. Desai from the Indian

Agricultural Research Institute

Today, close to 5 Million biogas plants

installed in India

100 hotels in Bangalore to set up biofuel

units, to cooperate in implementation of

plastics ban and garbage segregation at

source

SEEPZ-SEZ, Mumbai with zero-waste

policy installed a biogas plant; 5 MT wet-

waste per day

Rural Innovations spreading to the cities

1 2 3 4 5 6 7

Copyright © 2012 Reliance: All rights reserved.

42

Solar Water Purifier

Solar Lantern

Solar Street Light Solar Water pump Solar Air conditioner

Bringing cheer to millions of rural Indians

Solar Energy Revolution for the Masses: 20 GW Solar Power by 2022

Solar Mobile Charger

1 2 3 4 5 6 7

Copyright © 2012 Reliance: All rights reserved.

43

Mix of Traditional & Modern Technology

Gandhian Engineering: 4 min pedaling = 4 hours of light !

The Leg

Power

75 watt

Generator

Most Modern &

Efficient Lighting

Devices – LED !

Most Modern

Energy Storage

Device – Ultra-

Capacitors !

Ray of hope – Gandhian Engineering

1 2 3 4 5 6 7

Copyright © 2012 Reliance: All rights reserved.

44

Energy Technology Deployment

Source: Kramer and Haigh, Nature, 2009

Deployment rates in energy sector is measured in decades

1 2 3 4 5 6 7

Physical limits to energy technology deployment rate – long time to reach materiality

Governments need to design policies to accelerate deployment – R&D and Pilots

Promote technology families and let market forces choose winners

Demand side action to increase efficiency and curtail consumption

Copyright © 2012 Reliance: All rights reserved.

45

Technology Deployment and Development

Slow

Slow

Fast

Fast

Technology Development Speed

Tech

no

log

y D

ep

loym

en

t S

peed

IT &

Communications

Technologies

Energy

Technologies

Characteristics of Energy Sector:

- Slow development/ deployment

- Irreversible nature of investment

- Very high capital intensity

Would biotechnology materially change the energy paradigm?

Biotechnology?

1 2 3 4 5 6 7

More, Secure and Responsible Energy Technology for the Growing World

Copyright © 2012 Reliance: All rights reserved.

46

Structure of Scientific Enterprise Changed in Past 30 Yrs

Industry and University Used to Work Hand in Glove

People/

Resources

Development,

Manufacturing,

Distribution/Sales

Laws, Regulation Money

University Government Industry

Skilled People

Knowledge

Solutions

Products

Skilled People

Chemical science and industry have been closely

intertwined throughout its history

Startups

Venture Capital

Private Equity

Industry and Academia have grown apart since the fall of the Berlin wall

and passing of Bayh-Dole Act

1 2 3 4 5 6 7

Copyright © 2012 Reliance: All rights reserved.

47

47

Is VC/PE Model Working for Cleantech ?

Investors are extra-cautious with long lead high capital technology deployment

Debts are hard to come by

VC/PE lacks the appetite for

scale-up and patience for returns

What is the right investment model?

More governmental support for

long term development with

appropriate IP management

Greater public private partnerships

with patient strategic capital

investments

VC/PE investments in biofuels

Overall VC performance (Source: Kauffman Report)

-40% -35%

-28% -28% -25%

-21% -19%

-2%

11% 2012 YTD Performance

IT Cleantech

1 2 3 4 5 6 7

Copyright © 2012 Reliance: All rights reserved.

48

Derive Maximum Value from all Knowledge

Need to build on collective connected ingenuity in today’s boundary-less world

Economies of

‘Scale’

Economies of

‘Scope’

Economies of

‘Learning’ Benefits of

being

BIGGER

Benefits of

being

BROADER

Benefits of

doing things

SMARTER Boundary-less integration of knowledge

- Universities

- National labs

- Public companies

- Private companies

Knowledge paradigm to energy sector:

Could it achieve leap frogging efficient

Development & Deployment?

1 2 3 4 5 6 7

Source: Alexander Van de Putte

Copyright © 2012 Reliance: All rights reserved.

49

Mind set Change: From Relay Race to Tango

Closer Pubic Private Partnerships Across

International Boundaries Is Required

1 2 3 4 5 6 7

Copyright © 2012 Reliance: All rights reserved.

50

Mind set Change: From Relay Race to Tango

Organizing scientific research on the scale of big operatic and theatrical production is still something new in science and engineering

Closer Pubic Private Partnerships Across

International Boundaries Is Required

1 2 3 4 5 6 7

Copyright © 2012 Reliance: All rights reserved.

51

Process Innovation

Product Innovation

Catalyst Innovation

Raw material

Flexibility

New Creative

Business Models

Public Private

Partnerships

CAPEX

Efficiency OPEX

Efficiency

Fossil Renewable

Labor

Talent

Indianization

Unique RIL

Capital

Project

Execution

Inclusive Innovation = Creativity X Execution

Innovations to meet needs

of Aspiring Middle Class

Collective Mandate:

Science for Solution,

Technology for Transformation, &

Innovation for Impact

1 2 3 4 5 6 7

I would prize every invention of science made for the benefit of all – Mahatma Gandhi

Copyright © 2012 Reliance: All rights reserved.

THANK YOU

Growth is Life

Innovation Led Growth

Copyright © 2012 Reliance: All rights reserved.