eng presentacion santander conference.ppt [modo...

TRANSCRIPT

������������������������������������������������

�������������

���������� ��

US$12.2 bn

US$1.4 bn

Revenues evolution by country 2001 – 2010

CAGR

+27 %

46%

30%

14%

Brazil

And a new cycle ofgrowth has began

73%

3Q 2011

8%21%

29%

41%

9%1%1%

�����������������������������������������������

2007

2006

2005

2004

2003

2002

2000

1993

1988

1982

1976

2008

2009

Source: Cencosud

2010

Opened the first

supermarket

IPO in the

Santiago Stock

Exchange

3Q 2011

������

������

� ��� ���������

����

� �����������

2010 Revenues: US$12.2 billion

Selling Area: 2.9 million m2

Stores: 773

Customers: more than 100 million

����������������������������������������� �����!������

Note: Figures include Bretas acquisition in October 2010

�����

� �����������

� ��� ���������

� ��������� ������

� �������� �������

� ������� �������

���������

� �����������

� ��� ���������

� �������� �������

� ������� �������

� �����������

� ������� �������

� �������� �������

� ������� �������

Business units First nine month period 20111

Revenues (US$11,380 mm)

Geographies First nine month period 20112

�"��������#��������������������������������������������

Source: CencosudNotes:1 Other businesses, which account for (0.2%) and (13%), are not included in revenues nor EBITDA, respectively2 Colombia, which accounts for (1%), is not included in EBITDA

EBITDA (US$1,039mm)

2010 Population (mm) Population 2010-2015E CAGR (%)

CCD countries1

PeruChile BrazilArgentina Colombia

�����������$���"�������������������#�������������

Source: U.S. Census Bureau and local national statistics institutes for each country1 Aggregate for Cencosud countries: Argentina, Brazil, Chile, Colombia and Peru2 Weighed average by total 2010 population3 Based on latest statistics available

2010 Population by age (mm)1

52% below 30

Unemployment levels (%)3

CCD countries1,2

2010 GDP (US$bn)1 GDP 2010-2015E CAGR (%)

CCD countries2

PeruChile BrazilArgentina Colombia

Investment � � � �

�������������������������������������

Source: International Monetary Fund and World Bank (World Development Indicators) 1 In current prices2 Aggregate for Cencosud countries: Argentina, Brazil, Chile, Colombia and Peru

2010 Total reserves / GDP (%)

CCD countries2

2010 Gross Debt/GDP (%)

CCD countries2

Investment grade � � � �

�����

������

������

������

������

������

������

������

������

��������

����

� 6.1% weight in Chilean IPSA index

� Largest retail component of the index and 6th largest component overall

� Average daily traded volume: US$14.8mm (last 6 months)

� Ranked third worldwide by Boston Consulting Group as retailer to create most value to shareholders

� Rated as BUY by 5 out of 7 international equity research firms

310%

195%

Price evolution since IPO (CENCOSUD-SN)

�����#�����������������#���������������������

����

���������� ���� ����� ���������! � ��"����# ��������� �"��������

Source: Bloomberg and company filings, as of November 2, 2011Note: Market capitalization converted to USD at exchange rate of CLP/USD 521.461 As of September 30,20112 As of December 31, 2011

Public market overview Ownership structure2

���$��%% �&�

�'���'�%����

"��

�' %����

���� ���

(����

���

(��� &��

����$���

�

$'���

���

US$mm, unless where otherwise notedShare price, as of December 30, 2011 (CLP) 3,007Shares outstanding (mm) 2,264Market capitalization 13,057(+) Net debt1 3,123(+) Minority interest1 169(-) Equity investments1

-70Firm value 16,279

�����

Sales evolution (US$ bn)

�����

�����������������������������#���

�

Source: CencosudNote: 2005 – 2009 figures in Chilean GAAP while 2010 and 2011 figures in IFRS

� Addition of 58 supermarkets, 1 new home improvement, 4 department stores and 1new shopping center in Chile versus 3Q2010

� Consolidation of Bretas

� In all the countries and formats Cencosud obtained positive same stores sales figures(double-digit SSS growth in Argentina and Peru)

Sales breakdown by business – 3Q 2011 Sales breakdown by country – 3Q 2011

%��������������������������&�'�����#���

��

Source: CencosudNote: 2005 – 2009 figures in Chilean GAAP while 3Q 2010 and 3Q 2011 figures in IFRS

������

��������

������

��������

���� ��������� �����

�����

�����

Mg 7.9%Mg. 7.2%

()*+,!�������#�#��������-./,���0

EBITDA evolution (US$ bn)

��Source: CencosudNote: 2005 – 2009 figures in Chilean GAAP while 2010 and 2011 figures in IFRS.

� The Company obtained an EBITDA higher versus 3Q10 due to better performance in 4 businessunits.

� Cencosud’s calculation of EBITDA includes a non cash effect that came from currenciesfluctuation (income from foreign exchange variations), that in 3Q11 amounted to CLP 20,596million.

� The Company’s adjusted EBITDA in 3Q11 increased 30% and the EBITDA margin was 8.3%,and increase of 48 bps compared to the previous year adjusted EBITDA.

��� ���

��������������� ������ ������� )��!�

%���������������������� )�*#��� )�*"��� ���"�

1���������*���� � *��#� �*� �� ����"�

1����������� )��*#��� )� *#�"� "����

*��������� )��*�#�� )��*��!� )����

*���������2�����)��$ )��� )�� � )� ���

()*+,!��������3���-� 2���0

Cencosud’s calculation of EBITDAincludes a non cash effect thatcame from currencies fluctuation(income from foreign exchangevariations)

•in 3Q11 was CLP 20,596 MM

•In 3Q10 was CLP 498 MM*���������2�����)��$ )��� )�� � )� ���

%#����� )��*���� ) �*�*

,��������� )� *� �� )��*��!� �����

������ ������� ������ �����

()*+,!������� !��� !�#� )��"�$

������� ������ ������� ������� ��

������� ���������� �� �� ��� �� �

•In 3Q10 was CLP 498 MM

EBITDA breakdown by business¹ – 3Q 2011 EBITDA breakdown by country² – 3Q 2011

*�������()*+,!����)��4�������1���������/�#���

��

Source: Cencosud¹ Other businesses which account for (17%) are not included. ² Colombia EBITDA (1%) is not included.

� More than 70% of EBITDA came from retail businesses

� Margin improvement was driven by supermarkets and home improvement divisions

� In supermarkets was achieved by better higher gross margins mainly in Chile andArgentina mostly in the Jumbo banners.

+�� ������� ��

68 stores 145 stores#1

North East Region (34%)Minas Gerais (25%) #1

#2

/������$��5�����������///����6���������

Source market share: Cencosud and AC Nielsen as of September 2011. In Chile and Peru figures are for march 2011 ��

184 stores261 stores#2

#2

* Dia Stores not include

*658 stores

EBITDA breakdown by country, YTD 3Q 2011

Sales evolution (US$ bn) EBITDA evolution (US$ mm)

CAGR

����

����

CAGR

����

����

SSS evolution by country 3Q 2011

Mg 7.0% Mg 6.9%

/������$��5�3��������������������������!�������

EBITDA breakdown by country, YTD 3Q 2011

�"

Source: CencosudNote: 2005 – 2009 figures in Chilean GAAP while 2010 and 2011 figures in IFRS.

SSS evolution by country 3Q 2011

� Prezunic is the 3rd largest supermarket operator of Rio de Janeiro and the

!�7������������2�4����5��������3��������)��4��

�!

� Prezunic is the 3rd largest supermarket operator of Rio de Janeiro and the6th in Brazil

� estimated revenues of USD 1.2 billion for 2011

� 31 stores strategically distributed in the metropolitan region of Rio de Janeirowith a selling area of 81,000 square meters and a distribution center of54,000 square meters

� 64,000 active cards (through a joint venture with Itaú Bank)

� The value of the transaction amounts to USD 497 million, payable within 5years. This value shall be adjusted by debt and working capital, estimated ata total amount of USD 108 million), being therefore net pay of USD390million.

All Prezunic Stores has the same layout:� 2,500 m2 selling area*� 230 employees� 26 checkouts

!�7������������2�4����5��������3��������)��4��

EBITDA evolution (US$ mm)Sales evolution (US$ mm)

CAGR

����

����

CAGR

����

����

SSS evolution by country 3Q 2011

Mg 6.1% Mg 7.2%

8���*����#���5�����������������3������������

�

Source: CencosudNote: 2005 – 2009 figures in Chilean GAAP while 2010 and 2011 figures in IFRS.(1) 2005 – 2010 Growth rate

SSS evolution by country 3Q 2011

• In Chile Easy closed one store inConcepcion (CLP 1 bn revenues in3Q10) and our competitor openeda store in the same month

• The performance in the north ofChile has to be improved

EBITDA evolution (US$ mm)Sales evolution (US$ mm)

���

������

����

�����CAGR

CAGR

Mg 4.9% Mg 4.0%

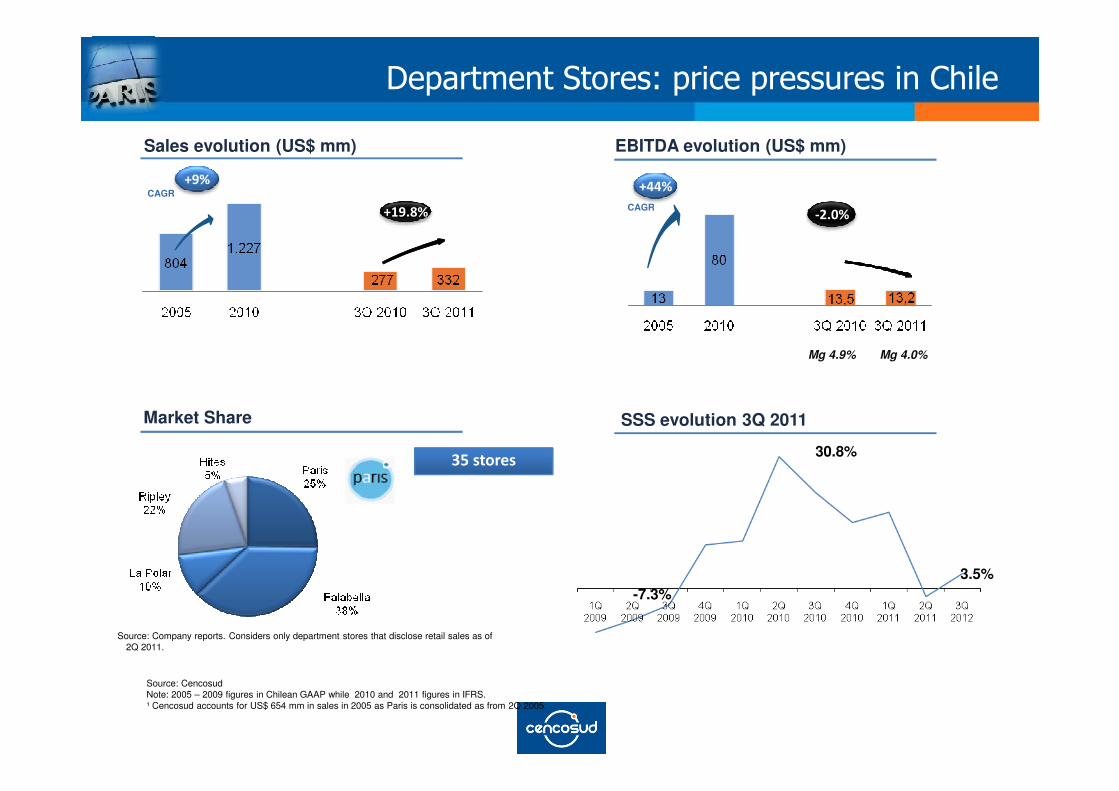

,��������/����5���������������������

Market Share

Source: Company reports. Considers only department stores that disclose retail sales as of 2Q 2011.

��

Source: CencosudNote: 2005 – 2009 figures in Chilean GAAP while 2010 and 2011 figures in IFRS.¹ Cencosud accounts for US$ 654 mm in sales in 2005 as Paris is consolidated as from 2Q 2005.

���������

SSS evolution 3Q 2011

3.5%

30.8%

-7.3%

EBITDA evolution (US$ mm)(1)Sales evolution (US$ mm)

CAGR

����������CAGR

���

����

Mg 68% Mg 73%

/�������������5�����������"���"�����������3�����

Geographic presence and occupancy rates

���

39%45%

55%

Source: CencosudNote: 2005 – 2009 figures in Chilean GAAP while 2010 and 2011 figures in IFRS.(1): Figures only include third party sales..

#214 Shopping Centers

582,241 m2

99% occupancy rate

#29 Shopping Centers

487,927 m2

97% occupancy rate

2 Shopping Centers65,763 m2

96% occupancy rate

�������������������������������

Gross loan portfolio evolution by country (US$ mm) Loan loss allowance as % of all loans

1���������/�#��5���������������������9���"��:2

Credit card usage in Cencosud by business 3Q 2011

��

Source: CencosudNote: 2007 – 2009 figures in Chilean GAAP while 2010 and 2011 figures in IFRS.¹ Since July 2010 ��!"��!�#�

����$ $

Geographic presence and active cards

Cencosud¹0.3 MM

Cencosud2.1 MM

Cencosud0.8 MM

JV with Bradesco0.9 MM

( ���� �%�, &'% &'$

Total debt evolution (US$ bn) Net debt evolution (US$ bn)

Capex (US$ mm) excl. acquisitions

�������

,3��#���������������������������7������������)����

��

Source: CencosudNote: 2005 – 2009 figures in Chilean GAAP while 2010 and 2011 figures in IFRS.

Net debt / EBITDA

- 25%- 14%

Financial debt / Equity

Total debt / EBITDA

EBITDA / Interest expenses

*����#������������������������

��

Source: CencosudNote: 2005 – 2009 figures in Chilean GAAP while 2010-2011 figures in IFRS. Multiples calculated in local currency.

+ 84%

Financial debt / EquityEBITDA / Interest expenses

- 17%

,3�!�����4����� /�����

Amortizaciones al Cierre Dic 2008

558

351385

594

138

7 7 18 25

119

26 27 57 67 68 69 70 70 52

221

0

100

200

300

400

500

600

700

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

Duration 4.7 Y

Debt Amortization December 2008

Source: Cencosud

Figures in USD MM��

Amortizaciones Hoy

240167

251

365 336

62 98

230

41 39

819

80 81 99 117 117 99

268

48 17115

0100200

300400500600

700800

900

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

Duration 7.4 Y

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

Debt Amortization Sep 2011

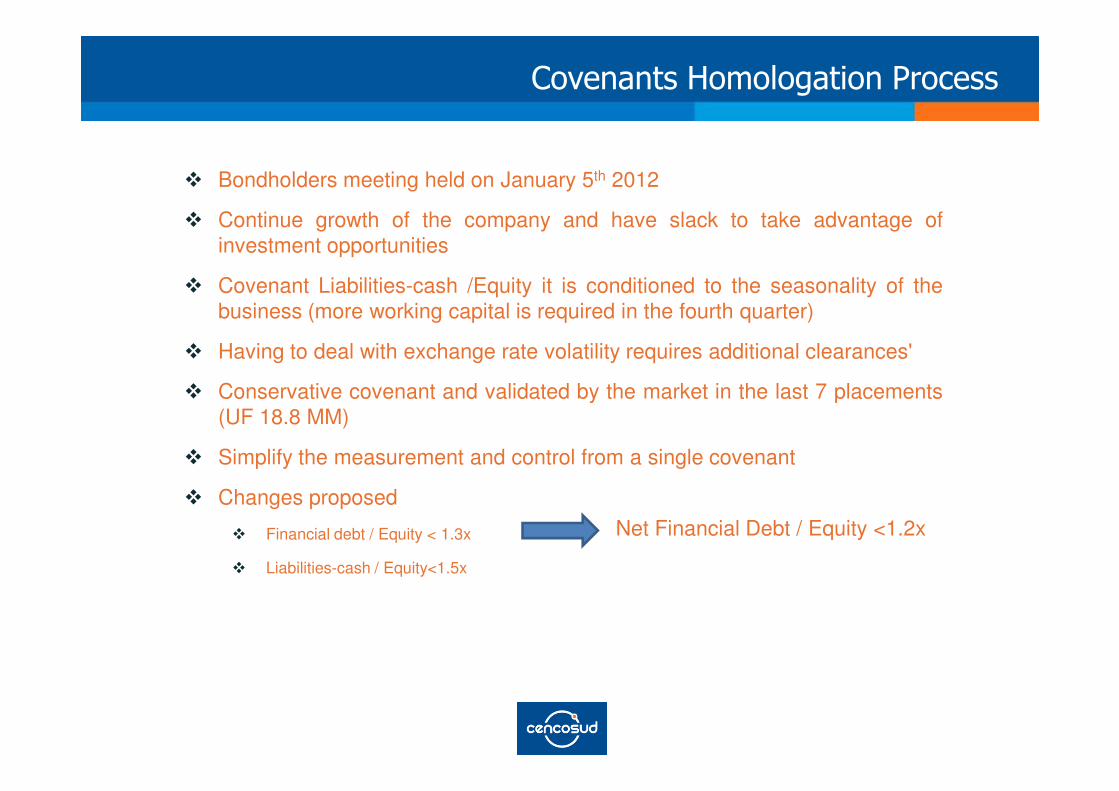

� Bondholders meeting held on January 5th 2012

� Continue growth of the company and have slack to take advantage ofinvestment opportunities

� Covenant Liabilities-cash /Equity it is conditioned to the seasonality of thebusiness (more working capital is required in the fourth quarter)

� Having to deal with exchange rate volatility requires additional clearances'

� Conservative covenant and validated by the market in the last 7 placements

��#������8������������2�����

� Conservative covenant and validated by the market in the last 7 placements(UF 18.8 MM)

� Simplify the measurement and control from a single covenant

� Changes proposed

� Financial debt / Equity < 1.3x

� Liabilities-cash / Equity<1.5x

Net Financial Debt / Equity <1.2x

!��"��� ������#

$%�� ��#

�"��&�#�"��&�#