engineering economics - ch 59 student - ecoccs.comecoccs.com/engineering economics - ch...

TRANSCRIPT

2/22/2017

1

Engineering Economics

2/22/2017

FE REVIEW COURSE – SPRING 2017

Paige Harris

2

Engineering Economics Knowledge

• 4 – 6 problems• Discounted cash flow

▫ Equivalence, PW, equivalent annual worth, FW, rate of return• Cost

▫ Incremental, average, sunk, estimating• Analyses

▫ Breakeven, benefit-cost, life cycle• Uncertainty

▫ Expected value and risk• Sections in FE Reference Handbook

▫ Engineering Economics

3

Engineering Economics

Year‐End & Other

Conventions

Cash Flow

Discount Factors

Single Payment

Equivalence

Uniform Series Equivalence

Uniform Gradient

Equivalence

NonannualCompounding

Depreciation Book Value

Capitalized Cost

Inflation

Break‐Even Analysis

Benefit‐Cost Analysis

2/22/2017

2

4

Year-End & Other Conventions

• Year-end convention: Assume that all receipts and disbursements (cash flows) take place at the end of the year in which they occur▫ Exceptions:

– Initial project cost (purchase cost)

– Trade-in allowance– Other cash flows that are

associated with the inception of the project at t = 0

5

Cash Flow

• Cash flows = the sums of money recorded as receipts or disbursements in a project’s financial records\

• Cash flow diagrams▫ Can be drawn to help visualize and

simplify problems that have diverse receipts and disbursements

▫ Horizontal (time) axis is marked off in equal increments, one per period

▫ Receipts ▫ Disbursements ▫ 2 or more transfers in same period

are placed end to end or combined▫ Sunk costs = expenses incurred

before t = 0

6

Cash Flow Continued

• Uniform series cash flow▫ Series of equal transactions

starting at t = 1 and ending at t = n

▫ Symbol A (annual amount) given to the magnitude of each individual cash flow

• Gradient series cash flow▫ Starts with a cash flow

(symbol G) at t = 2 and increases by G each year until t = n, at which time the final cash flow is (n – 1)G.– Gradient at t = 1 is 0

2/22/2017

3

7

Discount Factors

• The procedure for determining the equivalent amount is known as discounting

• Discount factors – symbolic and formula form

P. 131

8

Discount Factors

• Values of cash flow (discounting) factors are in tabulation form in Handbook▫ Pages 133-137

9

Single Payment EquivalenceSingle Payment Future Worth

• (1 + i)n

▫ Single payment compound amount factor• Common convention to substitute the standard functional

notation of (F / P, i%, n)• "Find F, given P, using an interest rate of i% over n years”

2/22/2017

4

10

Single Payment EquivalenceSingle Payment Future Worth Example

12

Single Payment EquivalenceSingle Payment Present Worth

• (1 + i)-n

▫ Single payment present worth factor

13

Single Payment EquivalenceSingle Payment Present Worth Example

2/22/2017

5

15

Uniform Series EquivalenceUniform Series Future Worth

• A = annual amount = cash flow that repeats at the end of each year for n years without change in amount

• Uniform series compound factor convert from an annual amount to future amount

16

Uniform Series EquivalenceUniform Series Future Worth Example

18

Uniform Series EquivalenceUniform Series Annual Value of a Sinking Fund

• Sinking fund = a fund or account into which annual deposits of Aare made in order to accumulate F at t = n in the future

• Sinking fund factor = (A/F)

2/22/2017

6

19

Uniform Series EquivalenceUniform Series Annual Value of a Sinking Fund Example

21

Uniform Series EquivalenceUniform Series Present Worth

• Annuity = a series of equal payments, A, made over a period of time

22

Uniform Series EquivalenceUniform Series Present Worth Example

2/22/2017

7

24

Uniform Series EquivalenceUniform Series Annual Value Using the Capital Recovery Factor

• Capital recovery factor = used when comparing alternatives with different lifespans

• Can convert the present value of each alternative into its equivalent annual value, using the assumption that each alternative will be renewed repeatedly up to the duration of the longest-lived alternative

25

Uniform Gradient EquivalenceUniform Gradient Present Worth

• Used to find present worth, P, of a cash flow that is increasing by a uniform amount, G.

26

Uniform Gradient EquivalenceUniform Gradient Future Worth

• Used to find future worth, F, of a cash flow that is increasing by a uniform amount, G.

2/22/2017

8

27

Uniform Gradient EquivalenceUniform Gradient Uniform Series Factor

• Used to find the equivalent annual worth, A, of a cash flow that is increasing by a uniform amount, G.

28

Uniform Gradient EquivalenceUniform Gradient Uniform Series Factor Example

30

Non-Annual CompoundingEffective Annual Interest Rate

• If there are m compounding periods during the year (2 for semiannual compounding, 4 for quarterly compounding, 12 for monthly compounding, etc.), the effective interest rate per period, i, is r/ m

• Effective annual interest rate, ie, can be calculated from the effective interest rate per period

P. 131

2/22/2017

9

31

Non-Annual CompoundingEffective Annual Interest Rate Example

33

DepreciationStraight Line Method

• Depreciation is the same each year

• Depreciation basis is divided uniformly among all of the years in the depreciation periods

• With the straight line method, depreciation is the same each year▫ Depreciation basis (C- Sn) is

divided uniformly among all of the n years in the depreciation period.

P. 132

34

DepreciationStraight Line Method Example

2/22/2017

10

36

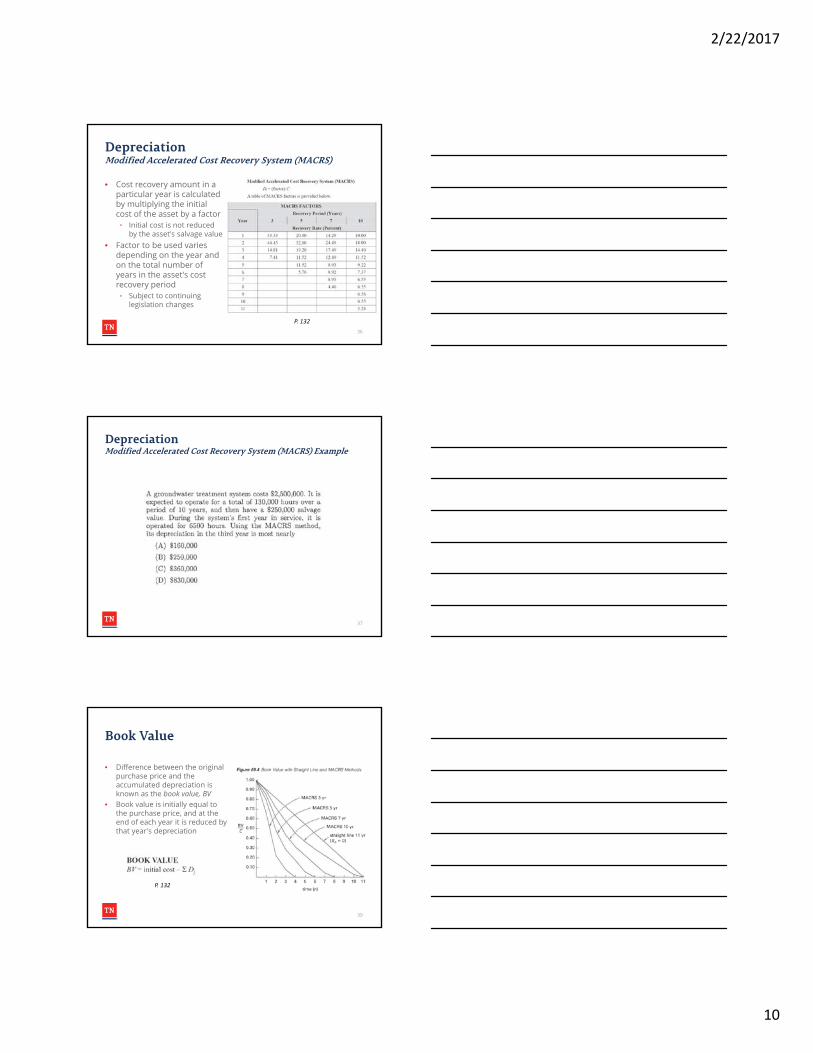

DepreciationModified Accelerated Cost Recovery System (MACRS)

• Cost recovery amount in a particular year is calculated by multiplying the initial cost of the asset by a factor▫ Initial cost is not reduced

by the asset's salvage value• Factor to be used varies

depending on the year and on the total number of years in the asset's cost recovery period▫ Subject to continuing

legislation changes

P. 132

37

DepreciationModified Accelerated Cost Recovery System (MACRS) Example

39

Book Value

• Difference between the original purchase price and the accumulated depreciation is known as the book value, BV

• Book value is initially equal to the purchase price, and at the end of each year it is reduced by that year's depreciation

P. 132

2/22/2017

11

40

Book Value Example

42

Capitalized Cost

• Present worth of a project with an infinite life is known as the capitalized cost

• Capitalized cost is the amount of money at t= 0 needed to perpetually support the project on the earned interest only

• Capitalized cost is a positive number when expenses exceed income

• Equation can be used when the annual costs are equal in every year

P. 132

43

Capitalized Cost Example

2/22/2017

12

45

Inflation

• f is a constant inflation rate per year

• Inflation-adjusted interest rate, d, can be used to compute present worth

P. 132

46

Inflation Example

48

Break-Even Analysis

• Method of determining when the value of one alternative becomes equal to the value of another

P. 131

2/22/2017

13

49

Benefit-Cost Analysis

• Used in municipal project evaluations where benefits and costs accrue to different segments of the community

• Present worth of all benefits, B, is divided by the present worth of all costs, C

• If the benefit-cost ratio, B / C, is greater than or equal to 1, the project is acceptable▫ Equivalent uniform annual costs

can be used in place of present worths

P. 132

50

Benefit-Cost Analysis Example

THANK YOU