entering a new league; buy - tupras.com.tr · interest cover 3.13x 1.74x 6.15x 8.04x 9.81x * for...

TRANSCRIPT

>> Employed by a non-US affiliate of MLPF&S and is not registered/qualified as a research analyst under the FINRA rules. Refer to "Other Important Disclosures" for information on certain BofA Merrill Lynch entities that take responsibility for this report in particular jurisdictions. BofA Merrill Lynch does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. Refer to important disclosures on page 46 to 48. Analyst Certification on Page 44. Price Objective Basis/Risk on page 44. 11495045

Tupras

Reinstatement of Coverage

BUY

Entering a new league; Buy

Equity | Turkey | Oil Refining & Marketing 19 March 2015

Anton Fedotov >> +7 495 662 6079 Research Analyst Merrill Lynch (Russia) [email protected] Karen Kostanian, CFA >> +7 495 662 6074 Research Analyst Merrill Lynch (Russia) [email protected] Denis Derushkin >> +7 495 662 6202 Research Analyst Merrill Lynch (Russia) [email protected] Jake Greenberg +44 20 7996 4815 Specialist Sales MLI (UK) [email protected]

Stock Data

Price TRY53.10 Price Objective TRY71.00 Date Established 19-Mar-2015 Investment Opinion C-1-9 Volatility Risk HIGH 52-Week Range TRY41.75-TRY57.50 Mrkt Val / Shares Out (mn) TRY13,297 / 250.4 Average Daily Volume 1,086,721 BofAML Ticker / Exchange TUPRF / IST Bloomberg / Reuters TUPRS TI / TUPRS.IS ROE (2015E) 21.2% Net Dbt to Eqty (Dec-2014A) 62.1% Est. 5-Yr EPS / DPS Growth 7.6% / NA Free Float 49.0%

Reinstating at Buy with TRY71 PO, 33% upside potential

We reinstate coverage of Tüpraş with a Buy rating and TRY71 PO, suggesting 33% upside potential. Tüpraş is the only pure refiner in our coverage cluster and we see it as a direct beneficiary of the weak oil price. The stock’s performance should be driven by high earnings growth, FCF improvement and attractive prospective dividend yield from 2015E.

Entering a new league via RUP launch Tüpraş is launching its flagship residuum upgrade project (RUP) in 2Q15, marking a new chapter in the company’s history. The RUP should allow complexity of refining to match that of most European peers, and raise Tüpraş’s yield of high-value added light oil product to an impressive 84%, underpinning further earnings growth.

Supportive macro environment The drop in crude prices has positively impacted refiners via higher margins and lower energy costs. Tüpraş’s net margin should exceed US$5/bbl by 2016E from US$3.2/bbl in 2014, while lower energy costs will add over c.US$100mn of savings.

Monopoly with flexible access to feedstock Tüpraş has the advantage of being the only refiner in Turkey’s high-growth oil product market. It also enjoys the benefits of diversified crude oil supply as it sources the feedstock from around 10 different countries. As RUP operations ramp up, Tüpraş can potentially save up to cUS$100mn per year by diversifying away from costly crude from Kazakhstan and Russia to heavier and cheaper grades.

Valuation undemanding; catalysts – RUP and div/FCF yield Tüpraş is trading on 7.4x P/E and 5.5x EV/EBITDA in 2016E, at a 30% discount to average EEMEA refiners P/E. The stock should be driven by the RUP launch in the near term, while our longer-term thesis is based on an expected 12-15% dividend and FCF yields. Estimates (Dec)

(TRY) 2013A 2014A 2015E 2016E 2017E EPS (Adjusted) 4.78 5.83 5.80 7.23 8.31 EPS Change (YoY) -18.2% 21.9% -0.5% 24.8% 14.8% Dividend / Share 1.58 0 3.48 6.51 7.48

Valuation (Dec) 2013A 2014A 2015E 2016E 2017E P/E 11.1x 9.11x 9.16x 7.34x 6.39x Dividend Yield 2.98% 0% 6.55% 12.3% 14.1% EV / EBITDA* 15.7x 22.2x 6.50x 5.48x 5.32x Free Cash Flow Yield* 2.21% 1.32% 8.09% 12.2% 15.4%

* For full definitions of iQmethod SM measures, see page 45.

Un

auth

ori

zed

red

istr

ibu

tio

n o

f th

is r

epo

rt is

pro

hib

ited

.T

his

rep

ort

is in

ten

ded

fo

r o

sman

.mem

iso

glu

@b

aml.c

om

.

Tupras 19 March 2015

2

iQprofile SM

Tupras Key Income Statement Data (Dec) 2013A 2014A 2015E 2016E 2017E (TRY Millions)

Sales 41,078 39,723 26,626 33,004 42,915 EBITDA Adjusted 1,094 773 2,639 3,130 3,228 Depreciation & Amortization (240) (258) (431) (445) (457) EBIT Adjusted 854 515 2,207 2,686 2,771 Net Interest & Other Income (841) (331) (379) (404) (151) Tax Expense / Benefit 1,186 1,286 (366) (456) (524) Net Income (Adjusted) 1,197 1,459 1,452 1,812 2,080

Average Fully Diluted Shares Outstanding 250 250 250 250 250 Key Cash Flow Statement Data

Net Income (Reported) 1,197 1,459 1,452 1,812 2,080 Depreciation & Amortization 240 258 431 445 457 Change in Working Capital 1,525 1,603 (141) (416) (348) Deferred Taxation Charge (1,192) (1,292) 0 0 0 Other CFO 779 404 (116) 286 361 Cash Flow from Operations 2,549 2,433 1,625 2,126 2,551 Capital Expenditure (2,255) (2,258) (550) (500) (500) (Acquisition) / Disposal of Investments 0 0 0 0 0 Other CFI 95.9 70.3 0 0 0 Cash Flow from Investing (2,159) (2,187) (550) (500) (500) Share Issue / (Repurchase) NA NA NA NA NA Cost of Dividends Paid (964) (396) 0 (871) (1,630) Increase (decrease) debt 2,278 1,233 (48.5) (545) (201) Other CFF (1,385) (961) (217) (172) (119) Cash Flow from Financing (71.2) (124) (266) (1,588) (1,951) Total Cash Flow (CFO + CFI + CFF) 319 121 810 37.8 100

FX and other changes to cash 82.4 114 (352) 0 0 Change in Cash 402 235 457 37.8 100 Change in Net Debt 1,876 998 (506) (582) (302)

Net Debt 2,859 3,857 3,351 2,768 2,467 Key Balance Sheet Data Property, Plant & Equipment 8,326 10,668 10,791 10,856 10,908 Goodwill 189 189 189 189 189 Other Intangibles 39.4 60.6 51.0 41.4 32.4 Other Non-Current Assets 2,820 4,024 4,080 4,144 4,230 Trade Receivables 1,957 170 114 141 183 Cash & Equivalents 3,663 3,898 4,356 4,394 4,494 Other Current Assets 4,145 2,923 1,846 2,282 3,019 Total Assets 21,139 21,933 21,427 22,048 23,056 Long-Term Debt 5,447 6,978 6,176 6,263 4,452 Other Non-Current Liabilities 157 181 181 181 181 Short-Term Debt 1,075 777 1,530 899 2,509

Other Current Liabilities 9,322 7,784 5,964 6,275 7,118 Total Liabilities 16,001 15,720 13,852 13,618 14,260 Total Equity 5,139 6,213 7,575 8,430 8,796

Total Equity & Liabilities 21,139 21,933 21,427 22,048 23,056 Business Performance* Return On Capital Employed 8.97% 4.52% 12.7% 14.6% 14.8%

Return On Equity 24.1% 25.9% 21.2% 22.8% 24.4% Operating Margin 2.08% 1.30% 8.29% 8.14% 6.46% Free Cash Flow (MM) 294 175 1,075 1,626 2,051 Quality of Earnings* Cash Realization Ratio 2.13x 1.67x 1.12x 1.17x 1.23x

Asset Replacement Ratio 9.38x 8.75x 1.27x 1.12x 1.09x Tax Rate NM NM 20.0% 20.0% 20.0% Net Debt/Equity 55.6% 62.1% 44.2% 32.8% 28.0% Interest Cover 3.13x 1.74x 6.15x 8.04x 9.81x

* For full definitions of iQmethod SM measures, see page 45.

Company Description Tupras is Turkey's only oil refiner. The refining

operations are conducted out of four sites around the country with a total capacity of 28.1mn tons per annum. Nelson Index Complexity of 7.3 should rise from the current 7.3 to 9.9 post the full launch of Residuum Upgrade Project in Izmit Refinery in 2Q 2015. The company also has a 40% stake in OPET, the third largest petroleum retailer in Turkey with approximately 1,300 fuel stations.

Investment Thesis Tupras is likely to benefit from its dominant position

in the Turkish refining sector assuming that Socar's Star refinery project will be operational by 2019YE. Moreover, earnings growth with the Residuum Upgrade Project coming into operation in 2015 is one of the major investment highlights for Tupras.

Stock Data Price to Book Value 1.8x

3

Tupras 19 March 2015

Contents Investment summary 4

Reinstating at Buy; 33% upside potential 6

RUP as the main growth driver 11

Energy cost savings 14

Crude oil mix to drive margins 17

Efficiency improvement drives growth 20

Turkish market in growth phase 21

Monopoly in an attractive market 25

Strong financials 27

Turkey: the macro view 29

Commodity view 31

Refining outlook in Europe 34

Risks to the investment case 37

Company background 38

Tupras 19 March 2015

4

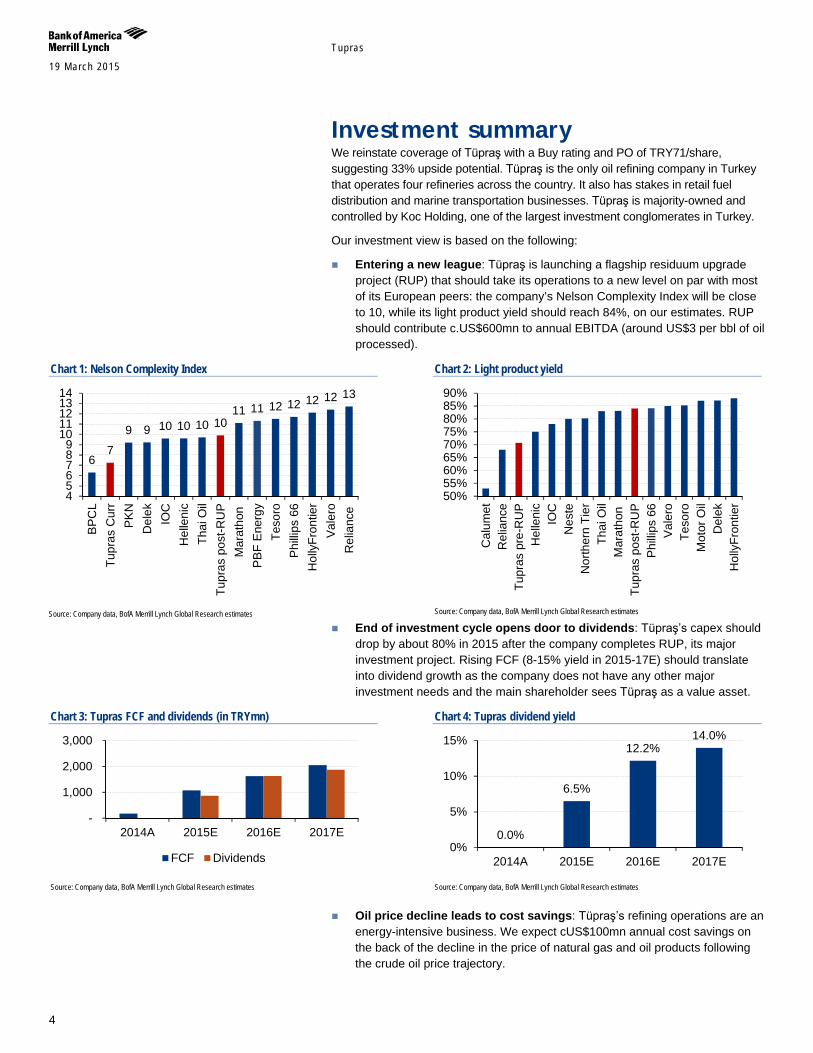

Investment summary We reinstate coverage of Tüpraş with a Buy rating and PO of TRY71/share, suggesting 33% upside potential. Tüpraş is the only oil refining company in Turkey that operates four refineries across the country. It also has stakes in retail fuel distribution and marine transportation businesses. Tüpraş is majority-owned and controlled by Koc Holding, one of the largest investment conglomerates in Turkey.

Our investment view is based on the following:

Entering a new league: Tüpraş is launching a flagship residuum upgrade project (RUP) that should take its operations to a new level on par with most of its European peers: the company’s Nelson Complexity Index will be close to 10, while its light product yield should reach 84%, on our estimates. RUP should contribute c.US$600mn to annual EBITDA (around US$3 per bbl of oil processed).

Chart 1: Nelson Complexity Index

Source: Company data, BofA Merrill Lynch Global Research estimates

Chart 2: Light product yield

Source: Company data, BofA Merrill Lynch Global Research estimates

End of investment cycle opens door to dividends: Tüpraş’s capex should drop by about 80% in 2015 after the company completes RUP, its major investment project. Rising FCF (8-15% yield in 2015-17E) should translate into dividend growth as the company does not have any other major investment needs and the main shareholder sees Tüpraş as a value asset.

Chart 3: Tupras FCF and dividends (in TRYmn)

Source: Company data, BofA Merrill Lynch Global Research estimates

Chart 4: Tupras dividend yield

Source: Company data, BofA Merrill Lynch Global Research estimates

Oil price decline leads to cost savings: Tüpraş’s refining operations are an energy-intensive business. We expect cUS$100mn annual cost savings on the back of the decline in the price of natural gas and oil products following the crude oil price trajectory.

6 7

9 9 10 10 10 10 11 11 12 12 12 12 13

456789

1011121314

BP

CL

Tupr

as C

urr

PK

ND

elek

IOC

Hel

leni

cTh

ai O

ilTu

pras

pos

t-RU

PM

arat

hon

PB

F E

nerg

yTe

soro

Phi

llips

66

Hol

lyFr

ontie

rV

aler

oR

elia

nce

50%55%60%65%70%75%80%85%90%

Cal

umet

Rel

ianc

eTu

pras

pre

-RU

PH

elle

nic

IOC

Nes

teN

orth

ern

Tier

Thai

Oil

Mar

atho

nTu

pras

pos

t-RU

PP

hilli

ps 6

6V

aler

oTe

soro

Mot

or O

ilD

elek

Hol

lyFr

ontie

r

-

1,000

2,000

3,000

2014A 2015E 2016E 2017E

FCF Dividends

0.0%

6.5%

12.2% 14.0%

0%

5%

10%

15%

2014A 2015E 2016E 2017E

Tupras 19 March 2015

5

Flexible access to crude oil supply: Tüpraş’s access to a diversified supply of crude oil feedstock stems from its advantageous geographical position. Post the RUP launch, the company should be able to process heavier and cheaper crude oil, which may potentially lead to an additional cost savings of up to US$100mn per annum.

Monopoly in a growing market: Turkey is a high-growth market for oil products with jet fuel and diesel demand up 11.2% and 4.2% in 2014, respectively. We forecast a significant middle-distillates deficit to persist over the coming years, which should support Tüpraş as the monopoly oil product producer in the country.

Improving financials to drive up shares: The launch of RUP, combined with higher refinery utilisation and cost savings, underpins Tüpraş’s impressive 22% EBITDA CAGR in 2015-18E, gradual deleveraging to 1.1x net debt/EBITDA in 2017E and rising dividend and FCF yields.

Chart 5: EBITDA (CCS) and Net debt (TRYmn)

Source: Company data, BofA Merrill Lynch Global Research estimates

Chart 6: Net debt/EBITDA

Source: Company data, BofA Merrill Lynch Global Research estimates

Rerating likely on the back of catalysts: Tüpraş is trading on 7.4x P/E and 5.5x EV/EBITDA in 2016E, including the full impact of RUP. The discount to the average 10x 2016E P/E of EEMEA peers is a high 29%. We believe the stock should be driven by the launch of RUP in the near term, while high EBITDA growth and improving FCF and dividends should pave the way for further rerating.

Chart 7: Tupras P/E progression

Source: BofA Merrill Lynch Global Research estimates

Chart 8: Tupras EV/EBITDA progression

Source: BofA Merrill Lynch Global Research estimates

-

2,000

4,000

6,000

2014A 2015E 2016E 2017E

EBITDA (CCS) Net debt

3.6

1.5 1.1 1.0

-

1.0

2.0

3.0

4.0

2014A 2015E 2016E 2017E

10.0x

7.1x 6.8x 6.3x 6.0x 5.8x

4

6

8

10

12

2015E 2016E 2017E 2018E 2019E 2020E

7.0x

5.7x 5.4x 5.2x 5.0x 4.8x

4

5

6

7

8

2015E 2016E 2017E 2018E 2019E 2020E

Tupras 19 March 2015

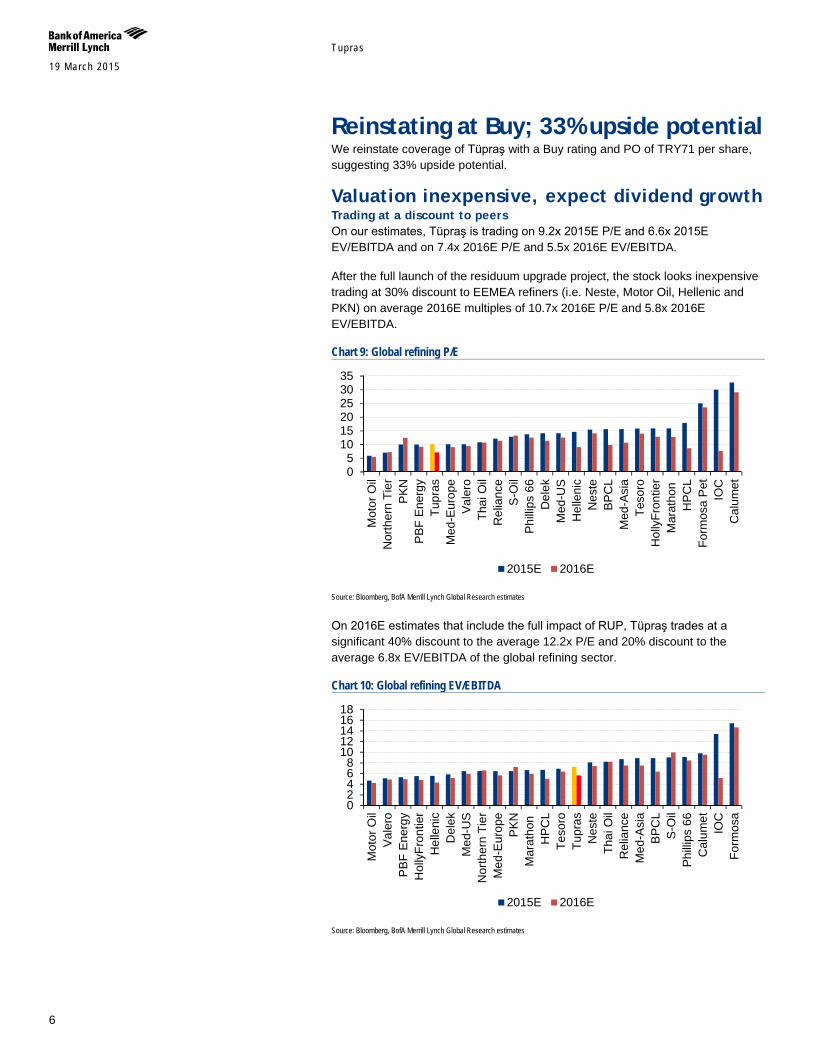

6

Reinstating at Buy; 33% upside potential We reinstate coverage of Tüpraş with a Buy rating and PO of TRY71 per share, suggesting 33% upside potential.

Valuation inexpensive, expect dividend growth Trading at a discount to peers On our estimates, Tüpraş is trading on 9.2x 2015E P/E and 6.6x 2015E EV/EBITDA and on 7.4x 2016E P/E and 5.5x 2016E EV/EBITDA.

After the full launch of the residuum upgrade project, the stock looks inexpensive trading at 30% discount to EEMEA refiners (i.e. Neste, Motor Oil, Hellenic and PKN) on average 2016E multiples of 10.7x 2016E P/E and 5.8x 2016E EV/EBITDA.

Chart 9: Global refining P/E

Source: Bloomberg, BofA Merrill Lynch Global Research estimates

On 2016E estimates that include the full impact of RUP, Tüpraş trades at a significant 40% discount to the average 12.2x P/E and 20% discount to the average 6.8x EV/EBITDA of the global refining sector.

Chart 10: Global refining EV/EBITDA

Source: Bloomberg, BofA Merrill Lynch Global Research estimates

05

101520253035

Mot

or O

ilN

orth

ern

Tier

PK

NP

BF

Ene

rgy

Tupr

asM

ed-E

urop

eV

aler

oTh

ai O

ilR

elia

nce

S-O

ilP

hilli

ps 6

6D

elek

Med

-US

Hel

leni

cN

este

BP

CL

Med

-Asi

aTe

soro

Hol

lyFr

ontie

rM

arat

hon

HP

CL

Form

osa

Pet

IOC

Cal

umet

2015E 2016E

02468

1012141618

Mot

or O

ilV

aler

oP

BF

Ene

rgy

Hol

lyFr

ontie

rH

elle

nic

Del

ekM

ed-U

SN

orth

ern

Tier

Med

-Eur

ope

PK

NM

arat

hon

HP

CL

Teso

roTu

pras

Nes

teTh

ai O

ilR

elia

nce

Med

-Asi

aB

PC

LS

-Oil

Phi

llips

66

Cal

umet

IOC

Form

osa

2015E 2016E

Tupras 19 March 2015

7

Turning into a dividend story Since its privatisation in 2006, Tüpraş has paid out its entire distributable profits as dividends in order to help its parent company Enerji Yatirimlari A.S. (EYAS), controlled by Koc Holding, repay its US$1.8bn acquisition loan. This dividend policy has been sustained despite the negative FCF since 2011.

The current remaining outstanding debt of EYAS is US$230mn payable in 2015. We see the current shareholder structure with Koc Holding as the controlling shareholder as positive for further dividend growth.

Tüpraş decided not to distribute dividends for 2014 due to a net loss posted in the statutory accounts on the back of a series of one-off losses and a negative inventory impact due to the massive decline in the oil price in 2H14.

We expect Tüpraş to resume paying dividends next year as earnings should grow on the back of the launch of the RUP expected in early 2Q15. We forecast DPS of TRY3.5 for 2015, TRY6.5 for 2016 and TRY7.5 for 2017. Tüpraş’s expected dividends would yield an attractive 6.5% for 2015 (payable in early 2Q16) and 12.2% for 2016 (payable in early 2Q17).

Chart 11: Tüpraş DPS (in TRY)

Source: Company data, BofA Merrill Lynch Global Research estimates

Chart 12: Tüpraş dividend yield

Source: Company data, BofA Merrill Lynch Global Research estimates

Tüpraş’s expected dividend yield would be the highest among the EEMEA refiners, which offer, on average, 4.4% for 2015E and 5.6% for 2016E. It would also be significantly higher than the average yields of the global refining peer group – 4.6% for 2015E and 4.6% for 2016E.

Chart 13: Global refiners dividend yield

Source: Bloomberg, BofA Merrill Lynch Global Research estimates

2.6 4.2

2.3 2.5 3.0 3.9 3.9

1.6 -

3.5

6.5 7.5

-

2.0

4.0

6.0

8.0

9%

14% 15%

8% 7% 9% 7%

4% 0%

7%

12% 14%

0%

5%

10%

15%

20%

0%2%4%6%8%

10%12%14%

Rel

ianc

eIO

CTe

soro

Mar

atho

nS

-Oil

Med

-Asi

aH

PC

LB

PC

LV

aler

oP

hilli

ps 6

6Fo

rmos

aP

KN

Nes

teD

elek

Med

-US

PB

F E

nerg

yTh

ai O

ilM

ed-E

EM

EA

Hel

leni

cTu

pras

Mot

or O

ilH

olly

Fron

tier

Cal

umet

Nor

ther

n Ti

er

2015E 2016E

Tupras 19 March 2015

8

FCF yield becoming solid Our dividend estimates are supported by robust expected FCF generation from 2015E. Dividends should be matched fully by strong FCF yielding 8% in 2015E, 12.1% in 2016E and 15.3% in 2017E.

Chart 14: Tüpraş FCF and dividends in TRYmn

Source: Company data, BofA Merrill Lynch Global Research estimates

Chart 15: FCF yield

Source: Company data, BofA Merrill Lynch Global Research estimates

PO TRY71 implies attractive 33% upside potential Our PO is based on the average of a DCF and comparable multiple valuation approach.

Table 1: Valuation summary US$m Weight US$m US$/share DCF 7,629 50% 3,815 15.23 Multiple 6,697 50% 3,349 13.37 12m target mcap estimate 7,163 28.6 Number of shares (m units) 250.4 250.4 12m PO (US$/share) 28.6 12m forward (US$/TRY) 2.50 12m PO (TRY/share) 71.00 Latest close (TRY/share) 53.50 Upside potential to PO (%) 32.7% Source: BofA Merrill Lynch Global Research estimates

Our DCF valuation results in a US$7.6bn equity value for Tüpraş. We use a 10.7% WACC for our DCF valuation based on 11.9% cost of equity, 5.2% after-tax cost of debt and 0% terminal growth.

Table 3: WACC calculation RFR 6.0% ERP 5.5% Beta 1.05 CoE 11.8% CoD 6.5% CoD after tax 5.2% Net Debt / Capitalisation 21% Equity / Capitalisation 80% WACC 10.7% Terminal growth rate 0.0% Source: BofA Merrill Lynch Global Research estimates

Our DCF-derived target equity value of US$7.6bn implies a TRY76.1/share price objective.

-

1,000

2,000

3,000

2014A 2015E 2016E 2017E

FCF Dividends

1.3%

8.0%

12.1% 15.3%

0%

5%

10%

15%

20%

2014A 2015E 2016E 2017E

Table 2: Beta calculation Unlevered beta 0.88 Net debt (2015YE) 1,678 Mcap 6,870 Tax 0.20 Geared beta 1.05 Source: BofA Merrill Lynch Global Research estimates

Tupras 19 March 2015

9

Table 4: Summary of DCF (US$mn) 2015E EV estimate 9,009 Less: Net debt (2015YE) 1,678 Less: minorities 28 Plus: subsidiaries 326 Target mcap (2015YE) 7,629 Number of shares (mn) 250.4 Valuation (US$/share) 30.5 Valuation (TRY/share) 76.1 Latest close (TRY/share) 53.5 Total return (%) 42% Source: BofA Merrill Lynch Global Research estimates

Table 5: DCF PO Sensitivity to WACC & Terminal Growth rate WACC

Termianl

Growth rate

71.1 10.00% 10.7% 11% 12.00% 13% 0% 77.3 71.1 69.1 62.2 56.4 1% 84.3 76.9 74.6 66.6 60.0 2% 92.9 84.0 81.2 71.9 64.3 3% 104.1 93.0 89.6 78.4 69.4

Source: BofA Merrill Lynch Global Research estimates

Our comparable multiple valuation is based on the average of 8x 2016E EV/EBITDA and 10x 2016E P/E target multiples Our target multiples are close to Tüpraş’s five-year historical average one-year forward multiples. Our 2016YE equity value estimates are then discounted using our 11.8% cost of equity. Our comparable multiple approach provides us with a US$6.7bn target equity value or TRY66.6 per share.

Table 6: Comparable multiple valuation (US$bn) Target multiple 8.0 Target multiple 10.0 16E EBITDA 1,234 15E Net income 754 16YE EV estimate 9,869 16YE Net Debt 1,378 16YE Minorities 32 16YE Subsidiaries 339 16YE equity value estimate 8,798 16YE equity value estimate 7,541 12m target equity value 7,212 12m target equity value 6,182 Weight 50% Weight 50% 2016E 12-m target equity value 6,697 # shares (mn) 250.4 Valuation (US$/share) 26.7 Valuation (TRY/share) 66.9 Latest close (TRY/share) 53.5 Total return (%) 25% Source: BofA Merrill Lynch Global Research estimates

Tupras 19 March 2015

10

Chart 16: Tupras P/E progression

Source: BofA Merrill Lynch Global Research estimates

Chart 17: Tupras EV/EBITDA progression

Source: BofA Merrill Lynch Global Research estimates

Chart 18: Tüpraş historical 1-year forward P/E

Source: Bloomberg, BofA Merrill Lynch Global Research estimates

Chart 19: Tüpraş historical 1-year forward EV/EBITDA

Source: Bloomberg, BofA Merrill Lynch Global Research estimates

10.0x

7.1x 6.8x 6.3x 6.0x 5.8x

4

6

8

10

12

2015E 2016E 2017E 2018E 2019E 2020E

7.0x

5.7x 5.4x 5.2x 5.0x 4.8x

4

5

6

7

8

2015E 2016E 2017E 2018E 2019E 2020E

6

7

8

9

10

11

12

13

Aug

-10

Dec

-10

Apr

-11

Aug

-11

Dec

-11

Apr

-12

Aug

-12

Dec

-12

Apr

-13

Aug

-13

Dec

-13

Apr

-14

Aug

-14

Dec

-14

456789

101112

Aug

-10

Dec

-10

Apr

-11

Aug

-11

Dec

-11

Apr

-12

Aug

-12

Dec

-12

Apr

-13

Aug

-13

Dec

-13

Apr

-14

Aug

-14

Dec

-14

Tupras 19 March 2015

11

RUP as the main growth driver RUP explained Since 2011, Tüpraş has focused on implementing a residuum upgrading project, a US$3bn investment to improve its competitiveness and profitability. The project consists of upgrading the Izmit refinery by improving its complexity to 14.5 from 7.8 currently. There will be no capacity additions, but the company will produce a higher share of white products: 4.5mn tons of raw materials will be transformed into 4.3mn tons of output. Of this, 3.5mn tons will be white products, comprising 2.88MMt of diesel, 0.52MMt of gasoline and 0.69MMt of LPG.

Chart 20: RUP feedstock and output

Source: Company data, BofA Merrill Lynch Global Research estimates

Management expects Tüpraş’s total refining capacity utilisation to increase to reach 95% post completion, compared with 74.9% in 2014 as the company will be able to process heavy product (i.e. atmospheric dip) in RUP units.

As of the end of January 2015, the company had spent a total of US$3bn on procurement and construction and the project was 99.8% complete. While the construction of the project was finished in December 2014, a test study of the units is currently under way and the full launch is planned in 2Q15.

RUP leads to a significant improvement in product slate… As a result of the RUP launch, we expect Tüpraş’s light product yield to rise from the current 71% to 84% in 2016. The product slate will be much more geared towards diesel (+81%), while fuel oil production should drop by 85%, on our estimates.

(3,036)

(1,214) (246)

69 86 522 690

2,883

(4,000)(3,000)(2,000)(1,000)

01,0002,0003,0004,000

Chart 21: Tupras capacity utilisation

Source: Company data, BofA Merrill Lynch Global Research estimates

77.9%

82.3% 78.7%

74.9%

82.6%

94.9%

70%

75%

80%

85%

90%

95%

100%

Tupras 19 March 2015

12

Chart 22: Tüpraş product slate in 2014

Source: Company data, BofA Merrill Lynch Global Research estimates

Chart 23: Tüpraş product slate in 2016

Source: BofA Merrill Lynch Global Research estimates

Post the launch of RUP, Tüpraş will be on par with most of its global peers in terms of complexity of refining operations.

Chart 24: Nelson Complexity Index

Source: Company data, BofA Merrill Lynch Global Research estimates

Chart 25: Light product yield

Source: Company data, BofA Merrill Lynch Global Research estimates

… and in margins Tüpraş recently guided that the positive impact from the RUP launch should add about US$650mn to annualised EBITDA. This translates into US$3.3/bbl in 2016, assuming a throughput increase to 26.7MMt to reach 95% capacity utilisation.

On our estimates, RUP should contribute US$419mn or US$2.5/bbl to 2015E EBITDA (assuming RUP launch from April 2015 and 82% total refining capacity utilisation) and US$599mn or US$3.1/bbl to EBITDA in 2016 and onwards (assuming ongoing 95% total refining capacity utilisation).

RUP profitability should be driven mainly by the diesel-fuel oil spread as the company will effectively replace fuel oil production with an increase in middle distillates. The spread has varied within a US$200-400/t range for the past two years with a decline recently on the back of the drop in the price of crude oil and related products.

4% 1%

22%

18% 27%

18%

1% 10% 1%

LPG Naphtha Gasolines

Jet fuel Diesel Fuel Oil

Lube oil Asphalt Coke/sulphur

4% 1%

24%

19% 38%

2% 1% 10% 4%

LPG Naphtha Gasolines

Jet fuel Diesel Fuel Oil

Lube oil Asphalt Coke/sulphur

6 7

9 9 10 10 10 10 11 11 12 12 12 12 13

456789

1011121314

BP

CL

Tupr

as C

urr

PK

ND

elek

IOC

Hel

leni

cTh

ai O

ilTu

pras

pos

t-RU

PM

arat

hon

PB

F E

nerg

yTe

soro

Phi

llips

66

Hol

lyFr

ontie

rV

aler

oR

elia

nce

50%55%60%65%70%75%80%85%90%

Cal

umet

Rel

ianc

eTu

pras

pre

-RU

PH

elle

nic

IOC

Nes

teN

orth

ern

Tier

Thai

Oil

Mar

atho

nTu

pras

pos

t-RU

PP

hilli

ps 6

6V

aler

oTe

soro

Mot

or O

ilD

elek

Hol

lyFr

ontie

r

Tupras 19 March 2015

13

Our calculations of the RUP impact are based on a US$250/t spread. On our estimates, each US$10/t move in the spread leads to a 7% change in the EBITDA of the RUP.

Chart 26: Diesel-fuel oil spread (US$/t)

Source: Bloomberg, BofA Merrill Lynch Global Research estimates

On our estimates, Tüpraş’s net refining margins should exceed US$5/bbl starting from 2016, which is a sizeable increase from the US$3.2/bbl posted in FY2014.

Chart 27: Tüpraş net refining margin (US$mn)

Source: Company data, BofA Merrill Lynch Global Research estimates

The margin increase will be a result not only of the RUP launch, but also significant cost savings on the back of lower energy costs, which we discuss in the following section.

200250300350400

3.3

2.5

3.2

5.0 5.3 5.4 5.4 5.5 5.6

2.0

3.0

4.0

5.0

6.0

FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20

Tupras 19 March 2015

14

Energy cost savings Tüpraş spent close to US$363mn or 63% of its clean CCS EBITDA on energy in 2014. As the energy price has almost halved since last year, we see further related cost savings as an important driver of Tüpraş’s profitability. We expect energy costs to go down due to the following reasons.

A 5-17% gas price decline in US$ in 2015E and 2016E In our base case, we expect the gas price for Tüpraş to go down by 5% in TRY from TRY798/mcm in 2014 to TRY758/mcm in 2015, or by 17% in US$ from US$364/mcm to US$303/mcm, respectively. A further 5% decline in both TRY and US$ in 2016 is also likely, in our view, if our oil price forecast materialises.

The cut in the gas price in Turkey should be driven by:

1. A low import gas price

2. 10.25% discount from Gazprom to Botas recently announced

3. Parliament elections in June 2015

Chart 28: Gas price (US$/mcm)

Source: BofA Merrill Lynch Global Research estimates

Chart 29: Botas’ gas price to Tupras (TRY/mcm)

Source: Botas data, BofA Merrill Lynch Global Research estimates

Russian gas accounts for c.60% of total gas consumed in Turkey, while the remaining import volumes are split between Iran (18%), Azerbaijan (7%) and others.

Chart 30: Turkey gas balance

Source: Oxford Institute for Energy Studies

Gazprom’s export gas prices are linked to a basket of oil products with a 6-9 month time lag. Oil product prices usually follow the crude oil price with a short time lag. This implies that Gazprom’s export price to Turkey will start reflecting January’s weakness in the crude oil price only in 3Q15.

435 421

285 237

410 364

303 288

100200300400500

2013 2014 2015 2016

Turkey input gas price Botas' gas price to Tupras

778 798

758

720

700720740760780800820

2013 2014 2015 2016

58%

18%

7%

17%

Russia Iran Azerbaijan Other

Tupras 19 March 2015

15

Moreover, Gazprom and the Turkish state company Botas recently started negotiations on a gas price discount as part of the agreement on the construction of the Turk Stream gas pipeline. The discount is planned at 10.25% and may be applied retroactively since the beginning of the year so that the gas price for Botas in the first quarter will fall to around US$332/mcm. We would expect Gazprom’s price to drop further, reaching a trough of US$165/mcm in 4Q15 on the back oil price decline.

Chart 31: Gazprom’s gas price to Turkey (US$/mcm)

Source: Company data, BofA Merrill Lynch Global Research estimates

Chart 32: Brent crude oil price (US$/bbl)

Source: BofA Merrill Lynch Global Research estimates

We see long-term positive trends for Turkish gas consumers including Tüpraş. Gazprom recently scrapped its plans to export gas to Europe via the South Stream pipeline and now plans to build the Turk Stream pipeline to Turkey instead. The construction of TANAP pipeline project was officially launched recently that will direct natural gas from Azerbaijan’s Shah Deniz field via Turkey to Europe. All this should help turn Turkey into a regional gas transportation hub, which would have a positive effect on the gas price for local consumers in the long term. Gazprom’s 10.25% discount to Botas would be the first step in that direction.

Liquids cost to drop by 48% in 2015 We expect the liquid energy cost (mainly fuel oil) to decline 48% in 2015 on the back of the global oil price drop. We forecast the average Brent oil price to go down by 52.6% to US$52/bbl in 2015 from US$98.9/bbl in 2014, driving down oil product prices accordingly.

Chart 33: Tupras liquids consumption (kt)

Source: BofA Merrill Lynch Global Research estimates

Chart 34: Liquids cost for Tupras (US$/t)

Source: BofA Merrill Lynch Global Research estimates

Total energy cost savings to exceed US$100mn per annum On our estimates, in 2014, Tüpraş consumed 0.75MMtoe of energy, composed of 0.15MMtoe of natural gas feedstock and 0.6MMtoe of other energy feedstock, mainly fuel oil.

150200250300350400450

2010 2011 2012 2013 2014 2015 201640

60

80

100

120

2010 2011 2012 2013 2014 2015 2016

500550600650700750800

2014 2015 2016200

300

400

500

600

2014 2015 2016

Tupras 19 March 2015

16

We expect gas consumption to increase by c.250ktoe/year once RUP becomes fully operational. Other energy costs (i.e. fuel oil) should rise in line with the higher refining capacity utilisation, planned to reach 95% post full RUP launch from the current 75%.

On our estimates, weighted average energy costs should go down by 43% from US$470/toe in 2014 to US$268mn in 2015 and by 40% to US$283/toe in 2016 driven by: 1) a lower crude oil price, 2) lower natural gas prices, and 3) TRY devaluation (Botas’s gas price for Tüpraş is denominated in TRY).

This should lead the energy cost to decline from US$2.4/bbl of crude oil processed in 2014 to US$1.7/bbl in 2015 and (-28% vs. 2014) and US$1.8/bbl in 2016 (-25% vs. 2016). In absolute figures, Tüpraş should achieve US$113mn and US$109mn in energy cost savings in 2015E and 2016E, respectively, corresponding to about 11% and 9% of its EBITDA.

Table 7: Tüpraş energy consumption, cost and savings 2014 2015E 2016E Total energy feedstock (ktoe) 750 996 1,156 - gas 150 335 396 - liquids (i.e. fuel oil) 600 662 760 Energy prices (US$/toe) - weighted average 470 268 283 - gas 328 273 259 - liquids (i.e. fuel oil) 505 265 296 Total energy cost (US$mn) 364 288 352 - gas 61 113 127 - liquids (i.e. fuel oil) 303 176 225 Energy cost in US$/bbl of throughput 2.4 1.7 1.8 % YoY -28% -24% Energy savings vs. 2014 (US$mn) 113 109 Energy savings vs. 2014 (TRYmn) 282 273 Source: Company data, BofA Merrill Lynch Global Research estimates

Tupras 19 March 2015

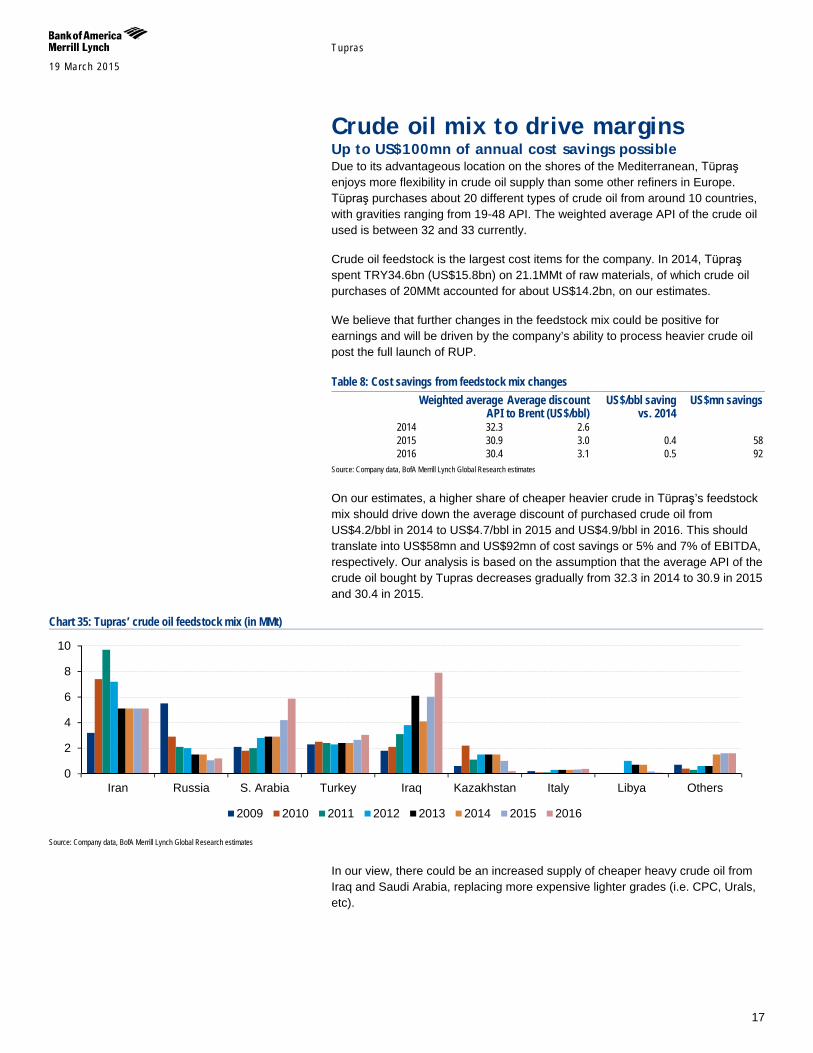

17

Crude oil mix to drive margins Up to US$100mn of annual cost savings possible Due to its advantageous location on the shores of the Mediterranean, Tüpraş enjoys more flexibility in crude oil supply than some other refiners in Europe. Tüpraş purchases about 20 different types of crude oil from around 10 countries, with gravities ranging from 19-48 API. The weighted average API of the crude oil used is between 32 and 33 currently.

Crude oil feedstock is the largest cost items for the company. In 2014, Tüpraş spent TRY34.6bn (US$15.8bn) on 21.1MMt of raw materials, of which crude oil purchases of 20MMt accounted for about US$14.2bn, on our estimates.

We believe that further changes in the feedstock mix could be positive for earnings and will be driven by the company’s ability to process heavier crude oil post the full launch of RUP.

Table 8: Cost savings from feedstock mix changes

Weighted average

API Average discount to Brent (US$/bbl)

US$/bbl saving vs. 2014

US$mn savings

2014 32.3 2.6 2015 30.9 3.0 0.4 58 2016 30.4 3.1 0.5 92

Source: Company data, BofA Merrill Lynch Global Research estimates

On our estimates, a higher share of cheaper heavier crude in Tüpraş’s feedstock mix should drive down the average discount of purchased crude oil from US$4.2/bbl in 2014 to US$4.7/bbl in 2015 and US$4.9/bbl in 2016. This should translate into US$58mn and US$92mn of cost savings or 5% and 7% of EBITDA, respectively. Our analysis is based on the assumption that the average API of the crude oil bought by Tupras decreases gradually from 32.3 in 2014 to 30.9 in 2015 and 30.4 in 2015.

Chart 35: Tupras’ crude oil feedstock mix (in MMt)

Source: Company data, BofA Merrill Lynch Global Research estimates

In our view, there could be an increased supply of cheaper heavy crude oil from Iraq and Saudi Arabia, replacing more expensive lighter grades (i.e. CPC, Urals, etc).

0

2

4

6

8

10

Iran Russia S. Arabia Turkey Iraq Kazakhstan Italy Libya Others

2009 2010 2011 2012 2013 2014 2015 2016

Tupras 19 March 2015

18

Chart 36: Tüpraş’s crude oil feedstock mix per country in 2014

Source: BofA Merrill Lynch Global Research estimates

Chart 37: Tüpraş’s crude oil feedstock mix per country in 2016

Source: BofA Merrill Lynch Global Research estimates

Higher oil intake from Iraq possible Since 2012, in most cases, Tüpraş has offset declining Iran crude oil imports with higher shipments from Iraq. In 2013, it imported 6.1mn tons of crude oil from Iraq, up from 1.8mn tons in 2009. However, on our estimates, Tüpraş’s purchase of Iraqi crude oil might have declined by about 2MMt to 4.1MMt in 2014 (undisclosed by Tupras) on the back of geopolitical instability in Iraq owing to the advance of Islamic State on its territory.

In the meantime, Iraq is still expected to make the largest contribution to OPEC capacity over the coming decade. Its 90 billion barrels of oil resources offer production longevity, making the country a key long-term supplier to the global oil market. Production has grown from 2.4 million b/d when the Technical Service Contracts came into force in 2010, to 3.3 million b/d in 2014. The majority of the production increase has come from the southern fields, but Kurdistan is becoming an important contributor.

According to WoodMackenzie’s estimates, Iraqi hydrocarbon liquids production could rise to around 4.5 mb/d in 2020, while Kurdistan's contribution is expected to increase from its current 8% to around 16%, with 725,000 b/d production forecast for 2020.

Chart 38: Iraq’s hydrocarbon liquids production (kboepd)

Source: WoodMackenzie

Chart 39: Tupras’ crude oil purchases from Iraq (hist. and forecast)

Source: Company data, BofA Merrill Lynch Global Research estimates

Due to the advance of Islamic State into Iraq output from the northern federal Iraqi fields is almost completely shut-in now. However, production from the

25%

7%

14%

12%

20%

7%

1%

Iran

Russia S. Arabia Turkey

Iraq Kazakhstan Italy

23%

5%

19%

12%

27%

2% 1%

Iran

Russia S. Arabia Turkey

Iraq Kazakhstan Italy

1,700

2,700

3,700

4,700

5,700

1.8 2.1 3.1

3.8

6.1

4.1

6.0

7.9

1

3

5

7

9

2009 2010 2011 2012 2013 2014 2015 2016

Tupras 19 March 2015

19

southern fields and Kurdistan remains unaffected, although the militants’ presence has increased security risks for oil operators in Iraq.

Higher purchases from Iraq would be value-accretive for Tüpraş, as these may be priced at a significant discount of around US$4-5/bbl to the Brent oil price. We believe Tüpraş will aim to grow purchases from Iraq to cover rising refining needs post the RUP launch, should the geopolitical situation allow. We would expect about a 2MMt of annual increase in oil purchases from Iraq in 2015 and 2016 by Tüpraş.

Iran remains potential catalyst Tüpraş used to buy 7-10MMt of Iranian crude oil per year before the latest sanctions against the Iranian energy sector came into effect in 2012. Tüpraş’s purchase of Iranian crude oil has dropped to around 5MMt/year since then and is now set on an annual basis for the company.

Chart 40: Tupras’ crude oil purchases from Iran (hist. and forecast)

Source: Company data, BofA Merrill Lynch Global Research estimates

Should Iran’s negotiations with the West over its nuclear programme end in a comprehensive agreement, it would have long-term positive implications for the export of Iranian crude to Turkey. 30 June 2015 is the key deadline for negotiations to watch at the moment. See EEMEA Economic Weekly: Iran negotiations – crunch time published on 13 March 2015 for more details on the Iran negotiations and potential outcomes.

We currently model Tüpraş making purchases of 5.1MMt of Iranian crude oil per year based on recent historical volumes. Assuming Iranian crude oil is priced at around a US$5/bbl discount to Brent, a 1MMt incremental supply of crude from Iran could result in about a US$15mn gain for Tüpraş. Our calculation is based on the assumption that Tüpraş’s crude oil purchase discount to Brent drops to around US$3.1/bbl in 2016, as highlighted above.

3.2

7.4

9.7

7.2

5.1 5.1 5.1

2

4

6

8

10

2009 2010 2011 2012 2013 2014 2015

Table 9: Impact of higher crude from Iran Additional

volume (MMt) Total volume

(MMt) US$mn gain 0 5.1 0 1 6.1 15 2 7.1 30 3 8.1 44 4 9.1 59 5 10.1 74

Source: BofA Merrill Lynch Global Research estimates

Tupras 19 March 2015

20

Efficiency improvement drives growth Apart from the flagship RUP, Tüpraş has undertaken other projects to streamline efficiency:

Izmir refinery: Investment in efficiency improvement projects at the Izmir refinery resulted in savings of more than US$30mn/annum. The installation of a new gas turbine with 25MW electricity generation capacity yielded annual energy savings of 132,383 gcal and annual monetary savings of US$9.7mn. Through modifications of operational parameters, diesel productivity was increased, which yielded US$11.3mn in annual savings. By improving operational parameters at crude oil units, semi-finished products were transformed into kerosene instead of naphtha. As a result, productivity increased 2%, and annual savings of US$12mn were achieved.

Kirikkale refinery: Investment to improve crude oil energy efficiency at Kirikkale will result in annual monetary savings of more than US$50mn

Chart 41: Investing in Efficiency projects (US$ mn)

Source: Company, Merrill Lynch Research

18

146

79 81

42

32 62

105 106

31 0

20406080

100120140160180200

2007 2008 2009 2010 2011 2012 2013

OMP EVP

Tupras 19 March 2015

21

Turkish market in growth phase Turkish oil product market in growth stage Relatively healthy economic growth in Turkey in recent years (i.e. GDP growth of 3.8% in 2013 and 2.7% in 2014) underpinned strong trends in petroleum product consumption in 2014:

jet fuel rose by 11.2% YoY

diesel consumption was up 4.2%

gasoline demand rose by 3.2%.

In the meantime, the country’s use of non-standard and informal petroleum products has dropped as a result of various measures being implemented.

Going forward, our macro research team expects 3.2% GDP growth in 2015 and 4% in 2016 in Turkey which, on our estimates, should translate into steady 2% per annum growth in total oil product demand, among the strongest rates in Europe. By 2020, Turkish consumption of petroleum products should reach 40Mt, on our estimates.

Most of this increase reflects incremental demand for gas/diesel oil, with the bulk of this representing road diesel, while a projected expansion in ethylene capacity should provide a substantial boost to naphtha sales. We expect the sales of most other oil products to increase during the forecast period.

Chart 43: Turkey oil product market growth (kt)

Source: BofA Merrill Lynch Global Research estimates

Gasoline consumption decline reversed Gasoline demand in Turkey has been in decline since the late 1990s because of the improved efficiency of gasoline engines as well as one of the highest retail fuel prices in Europe. As Turkey seeks accession to the EU, it is likely that it will increasingly adopt EU policy standards and initiatives. Thus, in line with wider EU policy, we expect the government to start pushing for a reduction in carbon

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

LPG Naphtha Gasolines

Jet fuel Total diesel Total fuel oil

Lube oil Asphalt Others

Chart 42: Turkey oil product demand growth

Source: BofA Merrill Lynch Global Research estimates

-2%0%2%4%6%8%

10%12%

Gasolines Jet fuel

Total diesel

Tupras 19 March 2015

22

emissions from transport. Therefore, growth in the car stock should be skewed towards new diesel and LPG cars, while the number of gasoline cars remains relatively static. We conservatively expect gasoline consumption to increase at only a 1-1.3% 2014-20E CAGR.

Local diesel market in deficit Turkey has large deficit in diesel, with domestic production covering only one-third of total demand in 2014.

Chart 44: Domestic production of diesel vs. imports in Turkey (MMt)

Source: Company data, WoodMackenzie, BofA Merrill Lynch Global Research estimates

Tüpraş’s full-scale launch of RUP should contribute about 2.9MMt/annum of diesel to domestic output and cover about 12% of demand in 2015E and 16% in 2016E. After the launch of RUP, Turkey will still have to import diesel to cover close to 50% of local demand.

Diesel demand driven by auto & GDP Diesel demand growth (c.5.2% pa from 2010-13) was driven largely by the road transport sector. Car penetration in Turkey of 165 cars per 1,000 people is still well below the European average of 500. Increasing purchasing power combined with a strong dieselisation trend in the car fleet has contributed to rising diesel consumption.

Chart 45: Turkey GDP YoY (%) vs. car sales (% yoy)

Source: Bloomberg, BofA Merrill Lynch Global Research

Chart 46: Total vehicle numbers in Turkey (mn)

Source: Company data, BofA Merrill Lynch Global Research estimates

While the recent strong dieselisation trend in the car fleet has contributed to rising diesel consumption, it is commercial transport which is estimated to account for around two thirds of diesel demand.

The other major sector of gas/diesel oil demand is Turkey's large agricultural sector. Agricultural fuel demand has grown steadily over the past decade and

5.6 5.3 8.1 9.6

11.1 12.1 9.9 8.7

0

5

10

15

20

2013 2014 2015 2016

Diesel production Diesel imports

-15%

0%

15%

30%

45%

60%

75%

-3

0

3

6

9

12

15

2009

2010

2011

2012

2013

GDP YoY (%) Car sales LTM (% yoy)

4.6 5.4 6.1 6.8 7.1 7.5 8.1 8.6 9.3 4.1 4.8

6.1 7 7.2 7.6 8 8.4 8.7

0

5

10

15

20

2002 2004 2006 2008 2009 2010 2011 2012 2013

Cars Other

Tupras 19 March 2015

23

continued increases in agricultural production are expected to result in this volume continuing to rise over the remainder of the forecast period.

Also, the increase in diesel consumption can be attributed to the implementation of the Special Consumption Tax (SCT) reimbursement in base oils to address problems such as the consumption of off-spec Number 10 diesel. These measures have been very effective in preventing this type of misconduct in the market.

We would expect growth momentum to be maintained until 2020 and forecast above a 2% 2015-20E CAGR of diesel demand in Turkey.

Chart 47: Turkey consumer confidence vs. car sales

Source: Bloomberg, BofA Merrill Lynch Global Research

Chart 48: Diesel consumption & GDP growth rate in Turkey

Source:, BofA Merrill Lynch Global Research

Rise in air traffic to boost jet fuel growth Jet fuel demand has grown strongly from 2011 at an average annual rate of 12% during this period. Growth in domestic air travel and the development of budget airlines (mainly inter-city flights) were among the key drivers. International travel has seen growth in this period as well, with a rise tourist numbers. Istanbul has become a hub for Turkish airlines and big investments in infrastructure will continue to bolster jet fuel consumption growth (above a 4% 2015-20E CAGR).

Chart 49: No of air passengers in Turkey (mn); 14% CAGR in past five years

Source: Company data, BofA Merrill Lynch Global Research estimates

Eurocontrol forecasts 7% CAGR growth for flight movements for Turkey (leading in Europe) thorough 2019. Turkish airports authority (DHMI) expects 9% CAGR growth in passenger numbers through 2023 (350mn pax in 2023 vs. 166mn achieved in 2014).

400,000

500,000

600,000

700,000

800,000

900,000

1,000,000

4045505560657075808590

2008

2009

2010

2011

2012

2013

2014

Turkey Consumer Confidence Car Sales LTM

-6%

-4%

-2%

0%

2%

4%

6%

8%

-6-4-202468

10

2009 2010 2011 2012 2013 9M-14

GDP Growth (LHS) Diesel Demand Growth (RHS)

35.8 41.2 50.6 58.3 64.5 76.1 43.6 44.3

52.2 59.4

65.4 73.4

0

25

50

75

100

125

150

2008 2009 2010 2011 2012 2013

Domestic International

Tupras 19 March 2015

24

Chart 50: # of air flights in Europe CAGR in 2012-2019E

Source: Eurocontrol Statistical Reference Area

Turkey as 2nd biggest auto-LPG market worldwide LPG demand grew rapidly to reach 1.3 Mt by the start of the last decade and, although the government has scaled back the subsidies since then, consumption continued its progress and overtook gasoline in 2010. The increase in gasoline price in recent years boosted conversions form gasoline to LPG, and the number of vehicles equipped to run on LPG is now estimated at 3 million. As a result, Turkey is the second largest auto-LPG market in the world amounting to 2.7 Mt in 2013.

Chart 51: Turkey’s car park by vehicle type

Source: WoodMackenzie

Fuel oil demand under pressure Fuel oil demand has been in terminal decline throughout the last decade as demand in the power and industrial sector has diminished, due to the steady displacement of fuel oil by natural gas in these sectors. Inland demand is expected to continue to fall in the period to 2025 although this is more than offset by rising marine bunker fuel demand, so that demand increases to 1.8 Mt by 2025. Overall, this represents an annual increase of 1.0% between now and the end of the forecast period.

012345678

Turk

eyG

eorg

iaA

zerb

haija

nA

rmen

iaM

oldo

via

Bul

garia

Rom

ania

Ukr

aine

Bel

arus

Mal

taH

unga

ryC

ypru

sS

lova

kia

Icel

and

Cro

atia

Bos

nia-

Her

z.Li

thua

nia

Pol

and

Ser

bia

& M

ont.

FYR

OM

Alb

ania

Slo

veni

aE

ston

iaM

oroc

coC

zech

Rep

.La

tivia

Gre

ece

San

ta M

aria

Aus

tria

Irela

ndS

wed

enB

elgi

umD

enm

ark

Ger

man

yIta

lyN

ethe

rland UK

Lisb

onFr

ance

Sw

itzer

land

Finl

and

Nor

way

Spa

inC

anar

y Is

l.

0

5000

10000

15000

20000

Conventional Hybrids AEV/PHEV Other LPG Diesel Gasoline

Tupras 19 March 2015

25

Monopoly in an attractive market Tüpraş is by far the leading player in the Turkish wholesale market for oil products across all the segments of the value chain:

Tüpraş controls all Turkey’s 28.1MMt refining capacity. In terms of geographical location, its refineries are deployed adjacent to consumption areas and are best suited to meet the country’s needs, which adds to the competitive strengths of the company.

It owns 59% of the total petroleum products storage capacity in Turkey, comprising 1.7 million tons of crude oil, 1.3 million tons of white product and 0.9 million tons of black product.

Tüpraş maintains a leading c.50% market share in wholesale of oil products in Turkey, which is mainly covered by own production, but also via imports (mainly diesel). The RUP should allow Tüpraş to raise its market share to 60% in 2016, on our estimates.

Chart 52: Tüpraş’s market share in 2014

Source: Company data, BofA Merrill Lynch Global Research estimates

Chart 53: Tüpraş’s market share in 2015E

Source: Company data, BofA Merrill Lynch Global Research estimates

Chart 54: Tüpraş’s market share in 2016E

Source: Company data, BofA Merrill Lynch Global Research estimates

Higher net refining margin than Med peers In line with its peers, Tüpraş’s refining margins compressed from 2011 to 1H14 driven by higher capacity utilisation across the industry, lower price differentials between crude grades and higher energy costs due to an increase in natural gas prices in Turkey. However, even in tough times, the company generates higher margins than its peers on average, mainly thanks to a Turkey inland price premium and a better crude oil sourcing mix. In 2014, Tüpraş’s net refining margin was US$3.2/bbl, US$1.2 above the Mediterranean net complex benchmark. The RUP project should add up to US$3/bbl to Tüpraş’s margin on our estimates.

8% 10% 18% 21%

39% 80%

94% 95% 98%

48.3%

0% 50% 100% 150%

NaphthaOthers

Lube oilLPG

DieselFuel oilJet fuel

GasolinesAsphalt

Total

10% 20% 24%

45% 53%

79% 93% 96% 98%

56%

0% 50% 100% 150%

NaphthaLube oil

LPGOthersDiesel

Fuel oilJet fuel

GasolinesAsphalt

Total

11% 19% 27%

54% 56% 60%

95% 96% 98%

60%

0% 50% 100% 150%

NaphthaLube oil

LPGFuel oilOthersFiesel

Jet fuelGasolines

AsphaltTotal

Tupras 19 March 2015

26

Chart 55: Net refining margins: Tüpraş vs. Med complex (US$/bbl)

Source: Company data, BofA Merrill Lynch Global Research estimates

Competition to challenge Tüpraş only from 2019 The state oil company of Azerbaijan, SOCAR, is building a new refinery in Turkey through the Star consortium (81.5% owned by SOCAR, 18.5% owned by TURCAS Rafineri Yatirimlari A.S), which could end Tüpraş’s domestic monopoly when completed in 2018. Located on the Aegean coast, the refinery will have 10MMt capacity (vs. 28.1MMt for Tüpraş), according to the current plan. The new refinery will feed its sister petrochemical company, Petkim, 1.7mn tons of naphta. In addition, Star will produce 0.5mn tons of jet fuel and 6mn tons of ULSD diesel.

Additional refining capacity coming on stream post 2018 should have only a limited impact on Tüpraş and the local market, given the considerable deficit of diesel. On our estimates, Turkey will still have to import close to 4MMt of diesel post the launch of Star in 2018.

Chart 56: Turkey diesel balance post the launch of Star refinery

Source: Company data, BofA Merrill Lynch Global Research estimates

5.3

3.3

2.5 3.2

4.6 5.1

1.2

4.2

1.7 2.0

2.8 2.4

0.0

1.0

2.0

3.0

4.0

5.0

6.0

FY11 FY12 FY13 FY14 FY15 FY16

Tupras net refining margin Med net refining margin

6.0 11.1 12.1 9.9 8.7 9.1 9.4

3.8

5.6 5.3 8.1 9.6 9.6 9.6 9.6

0

5

10

15

20

2013 2014 2015 2016 2017 2018 2019

Star production Imports Tupras production

Tupras 19 March 2015

27

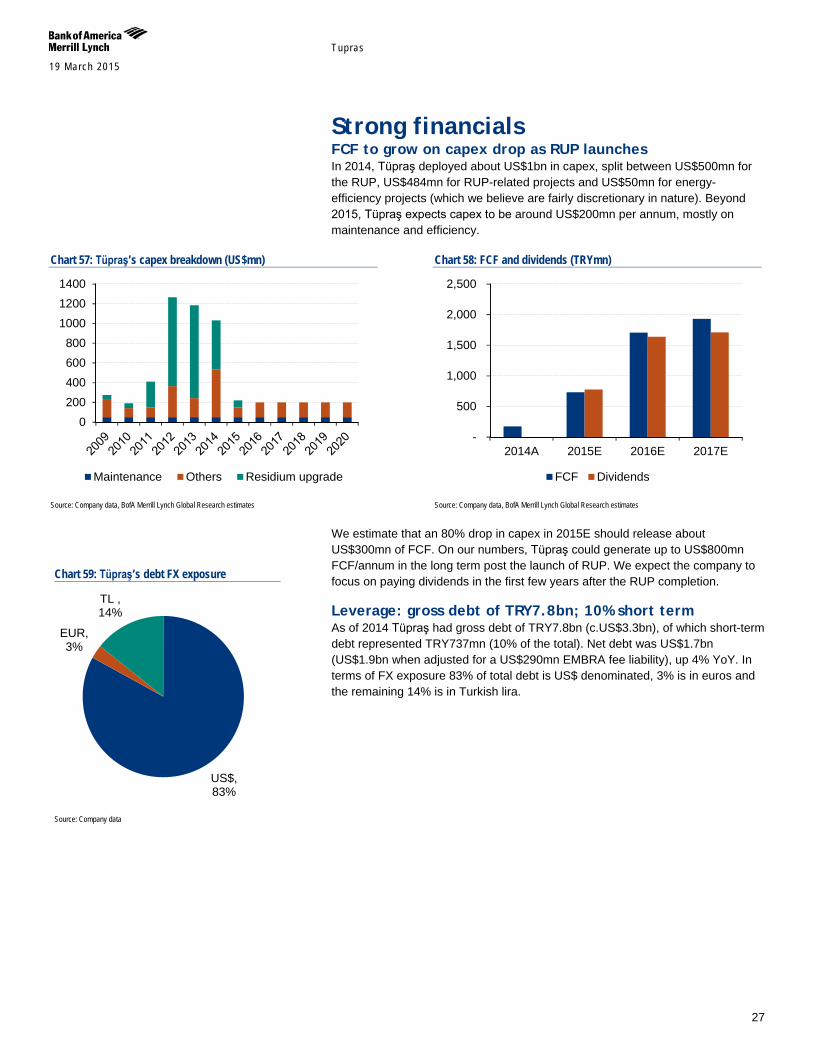

Strong financials FCF to grow on capex drop as RUP launches In 2014, Tüpraş deployed about US$1bn in capex, split between US$500mn for the RUP, US$484mn for RUP-related projects and US$50mn for energy-efficiency projects (which we believe are fairly discretionary in nature). Beyond 2015, Tüpraş expects capex to be around US$200mn per annum, mostly on maintenance and efficiency.

Chart 57: Tüpraş’s capex breakdown (US$mn)

Source: Company data, BofA Merrill Lynch Global Research estimates

Chart 58: FCF and dividends (TRYmn)

Source: Company data, BofA Merrill Lynch Global Research estimates

We estimate that an 80% drop in capex in 2015E should release about US$300mn of FCF. On our numbers, Tüpraş could generate up to US$800mn FCF/annum in the long term post the launch of RUP. We expect the company to focus on paying dividends in the first few years after the RUP completion.

Leverage: gross debt of TRY7.8bn; 10% short term As of 2014 Tüpraş had gross debt of TRY7.8bn (c.US$3.3bn), of which short-term debt represented TRY737mn (10% of the total). Net debt was US$1.7bn (US$1.9bn when adjusted for a US$290mn EMBRA fee liability), up 4% YoY. In terms of FX exposure 83% of total debt is US$ denominated, 3% is in euros and the remaining 14% is in Turkish lira.

0200400600800

100012001400

Maintenance Others Residium upgrade

-

500

1,000

1,500

2,000

2,500

2014A 2015E 2016E 2017E

FCF Dividends

Chart 59: Tüpraş’s debt FX exposure

Source: Company data

US$, 83%

EUR, 3%

TL , 14%

Tupras 19 March 2015

28

Chart 60: Tüpraş Debt Maturity profile (TRY mn)

Source: Company, BofA Merrill Lynch Global Research

We expect Tüpraş’s net debt/EBITDA to go down from 5.9x in 2014 to 1.1x in 2017E on the back of high earnings growth and gradual deleveraging post the RUP launch.

Chart 61: Net debt/EBITDA

Source: Company, BofA Merrill Lynch Global Research

Impact of FX on Tüpraş: positive in the long term Besides export revenues, which are US$-denominated, Tüpraş generates around 81% of its revenue domestically. These revenues are in Turkish lira but also US$-linked. The company may also incur gains and losses from inventory due to FX. That said, excluding raw materials, capex and finance costs, most of Tüpraş’s operating costs are in Turkish lira.

On the debt side, Tüpraş is exposed to FX risk as 83% of gross debt is US$-denominated, 3% is in euros and the remaining 14% is in Turkish lira. Weaker lira implies an FX loss owing to the US$-denominated debt revaluation.

All in all, on our estimates, a 10% weakening in TRY has 17% positive impact on Tupras EBITDA and mostly negligible below 2% negative impact of on the net income in 2015. In longer term, the company wins from weaker TRY once FX losses stemming from the debt revaluation are left behind and the products are priced based on a stronger USD.

737

1,489

840

2,343

477

1,827

-

500

1,000

1,500

2,000

2,500

2015 2016 2017 2018 2019 2020+

5.9

1.8 1.2 1.1

-

2.0

4.0

6.0

8.0

2014A 2015E 2016E 2017E

Tupras 19 March 2015

29

Turkey: the macro view Trimming GDP growth forecasts In its recent report Trimming GDP growth forecast, our macroeconomics research team highlighted that Turkey has largely missed a great opportunity to ride a strong cyclical tailwind and to address its macro vulnerabilities smoothly at a time when the Fed’s normalisation of rates is looming. As a result, first domestic politics hit the TRY and Turkish assets, and then soured EM risk sentiment on the back of increased concerns of an earlier-than-expected Fed hike took its toll.

Further volatility in both domestic politics and global financial markets in 2Q15 is likely to take its toll on economic activity and macro indicators. The risks are to the downside on GDP growth and the CAD, and to the upside on inflation in 2015 due to TRY weakness. Leading indicators suggest that both private consumption and investments have been slow to recover in 1Q15. Our 2015E GDP growth forecast was cut by 0.5ppt to 3.2%.

June elections key to the outlook Turkey is expected to hold parliamentary elections on 7 June. The elections have become the crossroads for the outlook for Turkish assets. President Erdogan has suggested that June elections could represent a break from the past in terms of both moving to a presidential system and introducing a new economic framework. The row between President Erdogan and the Central Bank of Turkey (CBT) on monetary policy caused the markets to question the CBT’s independence going forward. One concern is ‘interference’ with the CBT’s policy, which could lead to more aggressive rate cuts than desired and result in the TRY weakening.

Chart 62: Real GDP growth to bounce back, but recovery delayed

Source: Haver, BofA Merrill Lynch Global Research

Chart 63: Domestic demand is likely to strengthen

Source: Haver, BofA Merrill Lynch Global Research

-6

-4

-2

0

2

4

6

8

10

12

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

e

2015

F

2016

F

Real GDP growth (%yoy)

-5-3-113579

111315

03 04 05 06 07 08 09 10 11 12 13 1Q14 14F 15FPrivate cons. Public cons. GFCFInventories Net exports GDP growth

%

Tupras 19 March 2015

30

Chart 64: External demand pulling down Turkish IP growth

Source: Haver, BofA Merrill Lynch Global Research

Chart 65: Weaker TRY is likely to dent domestic confidence

Source: Haver, BofA Merrill Lynch Global Research

A ‘Robin Hood’ recovery Lower oil prices act as a significant tax cut for a large number of consumers, funded by a few oil exporters. This income redistribution from rich, saving countries to poor, non-saving peers should be positive for growth as the latter have a higher marginal propensity to consume. This is also the case for the EEMEA region and Turkey is comfortably at the receiving end of this transfer.

In a global backdrop with lower oil prices and global yields, Turkey stands out in EEMEA for four main reasons, in our view: 1) its economy is relatively more closed and depends more on domestic demand, with exports to GDP at 25%; 2) the average age of the population is a young 29.3 and this demographic has a higher tendency to spend; 3) it is one of the main energy importers, with energy imports to GDP at 7%; and 4) its growth model depends heavily on lower interest rates

Side effects of low oil price The side effect of lower oil prices on Turkey’s growth would be a rise in oil product exports because some 80% head to Europe and MENA. In addition, lower crude prices have a positive impact on inflation as fuel prices in TRY have come down by roughly 15% from July highs to end-2014 and by another 5% in January.

-30

-10

10

30

30

40

50

60

Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15

PMI_TUTurkish IP growth (rhs, % yoy)

60

70

80

90

100

110

120

55

60

65

70

75

80

85

Jan-

07

Jan-

08

Jan-

09

Jan-

10

Jan-

11

Jan-

12

Jan-

13

Jan-

14

Jan-

15

Consumer Confidence IndexReal Sector Confidence Index (sa)

Exhibit 1: Gross National Savings (% of GDP)

Source: Haver, Bank of America Global Research

Tupras 19 March 2015

31

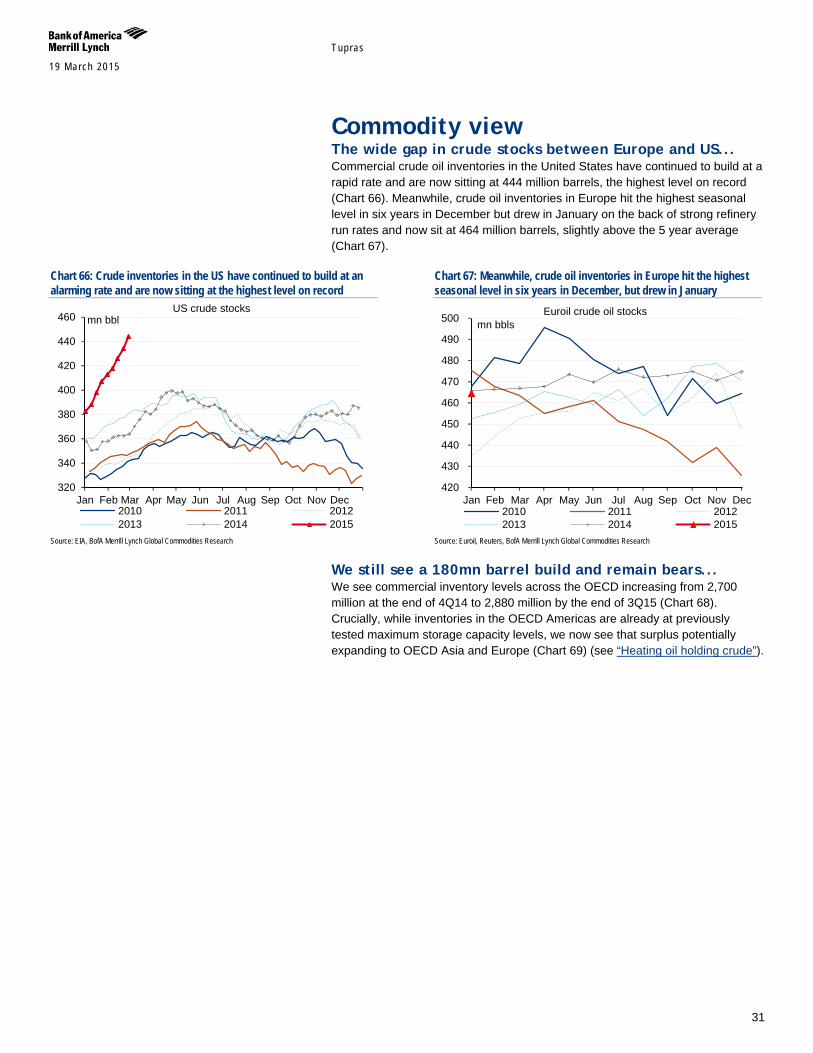

Commodity view The wide gap in crude stocks between Europe and US... Commercial crude oil inventories in the United States have continued to build at a rapid rate and are now sitting at 444 million barrels, the highest level on record (Chart 66). Meanwhile, crude oil inventories in Europe hit the highest seasonal level in six years in December but drew in January on the back of strong refinery run rates and now sit at 464 million barrels, slightly above the 5 year average (Chart 67).

Chart 66: Crude inventories in the US have continued to build at an alarming rate and are now sitting at the highest level on record

Source: EIA, BofA Merrill Lynch Global Commodities Research

Chart 67: Meanwhile, crude oil inventories in Europe hit the highest seasonal level in six years in December, but drew in January

Source: Euroil, Reuters, BofA Merrill Lynch Global Commodities Research

We still see a 180mn barrel build and remain bears... We see commercial inventory levels across the OECD increasing from 2,700 million at the end of 4Q14 to 2,880 million by the end of 3Q15 (Chart 68). Crucially, while inventories in the OECD Americas are already at previously tested maximum storage capacity levels, we now see that surplus potentially expanding to OECD Asia and Europe (Chart 69) (see “Heating oil holding crude”).

320

340

360

380

400

420

440

460

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

mn bbl US crude stocks

2010 2011 20122013 2014 2015

420

430

440

450

460

470

480

490

500

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec2010 2011 20122013 2014 2015

Euroil crude oil stocks mn bbls

Tupras 19 March 2015

32

Chart 68: We see commercial stock levels in the OECD increasing from 2.70 bn at the end of 4Q14 to 2.88 bn by the end of 3Q15

Source: IEA, BofA Merrill Lynch Global Commodities Research

Chart 69: We now see the crude oil surplus potentially expanding to OECD Asia and Europe

Source: IEA, BofA Merrill Lynch Global Commodities Research

...but we mark our targets up given current price levels Since we still expect global oil supply to run above demand for at least six more months, we believe that downward pressure on petroleum prices will likely continue. Yet, the Brent market has been somewhat tighter than we projected on the back of unexpected disruptions. Meanwhile WTI weakness has become extremely pronounced even against domestic grades like Light Louisiana Sweet (Chart 70) that are only a pipeline move away. On the back of these reasons, we shift our WTI end of 1Q and 2Q target to $45 and $41, respectively, and move our Brent end of 1Q and 2Q target to $55 and $48 (Chart 71). So we remain bearish, but in a different shade of gray.

Chart 70: WTI weakness has become extremely pronounced even against domestic grades like Light Louisiana Sweet

Source: Bloomberg, BofA Merrill Lynch Global Commodities Research

Chart 71: We shift our WTI end of 1Q and 2Q target to $45 and $41 respectively, and our Brent end of 1Q and 2Q target to $55 and $48

Source: Bloomberg, BofA Merrill Lynch Global Commodities Research

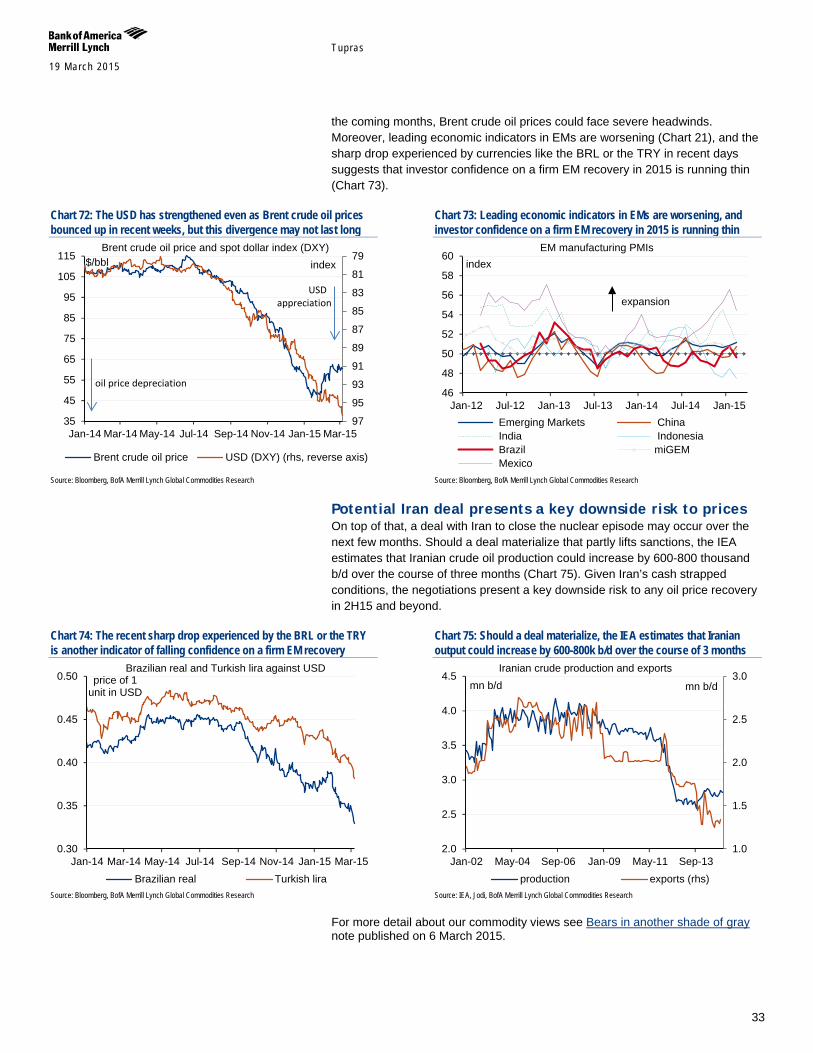

The strong USD, high stocks, and weak EMs cap oil prices Very high inventory levels are perhaps the main reason to remain cautious on the global crude oil price outlook over the next few months. While the microeconomics of the oil industry are poor, the global macro framework is not helping. To begin with, the USD has continued to strengthen even as Brent crude oil prices bounced up in recent weeks (Chart 72). Should the USD rally further in

2,500

2,600

2,700

2,800

2,900

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

mn bbl

OECD total oil stocks (crude, ngl, products, feedstock)

2009 2010 2011 20122013 2014 2015

440450460470480490500510520530540

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

mn bbl OECD Europe & Asia crude oil stocks

2009 2010 20112012 2013 2014

(7)

(6)

(5)

(4)

(3)

(2)

(1)

-

Oct-14 Feb-15 Jun-15 Oct-15 Feb-16 Jun-16

$/bbl

WTI-LLS

WTI-LLS (03-Mar-15) WTI-LLS (31-Dec-14)WTI-LLS (28-Nov-14) WTI-LLS (29-Oct-14)WTI-LLS (29-Sep-14)

30

40

50

60

70

80

90

100

110

120

Sep-12 Mar-13 Sep-13 Mar-14 Sep-14 Mar-15 Sep-15

$/bbl

Brent & WTI crude oil: forecast versus forward

WTI Brent

forward

BofAML EoQ fcast

Tupras 19 March 2015

33

the coming months, Brent crude oil prices could face severe headwinds. Moreover, leading economic indicators in EMs are worsening (Chart 21), and the sharp drop experienced by currencies like the BRL or the TRY in recent days suggests that investor confidence on a firm EM recovery in 2015 is running thin (Chart 73).

Chart 72: The USD has strengthened even as Brent crude oil prices bounced up in recent weeks, but this divergence may not last long

Source: Bloomberg, BofA Merrill Lynch Global Commodities Research

Chart 73: Leading economic indicators in EMs are worsening, and investor confidence on a firm EM recovery in 2015 is running thin

Source: Bloomberg, BofA Merrill Lynch Global Commodities Research

Potential Iran deal presents a key downside risk to prices On top of that, a deal with Iran to close the nuclear episode may occur over the next few months. Should a deal materialize that partly lifts sanctions, the IEA estimates that Iranian crude oil production could increase by 600-800 thousand b/d over the course of three months (Chart 75). Given Iran’s cash strapped conditions, the negotiations present a key downside risk to any oil price recovery in 2H15 and beyond.

Chart 74: The recent sharp drop experienced by the BRL or the TRY is another indicator of falling confidence on a firm EM recovery

Source: Bloomberg, BofA Merrill Lynch Global Commodities Research

Chart 75: Should a deal materialize, the IEA estimates that Iranian output could increase by 600-800k b/d over the course of 3 months

Source: IEA, Jodi, BofA Merrill Lynch Global Commodities Research

For more detail about our commodity views see Bears in another shade of gray note published on 6 March 2015.

79

81

83

85

87

89

91

93

95

9735

45

55

65

75

85

95

105

115

Jan-14 Mar-14 May-14 Jul-14 Sep-14 Nov-14 Jan-15 Mar-15

index $/bbl Brent crude oil price and spot dollar index (DXY)

Brent crude oil price USD (DXY) (rhs, reverse axis)

USD appreciation

oil price depreciation 46

48

50

52

54

56

58

60

Jan-12 Jul-12 Jan-13 Jul-13 Jan-14 Jul-14 Jan-15

index EM manufacturing PMIs

Emerging Markets China India Indonesia Brazil miGEM Mexico

expansion

0.30

0.35

0.40

0.45

0.50

Jan-14 Mar-14 May-14 Jul-14 Sep-14 Nov-14 Jan-15 Mar-15

price of 1 unit in USD

Brazilian real and Turkish lira against USD

Brazilian real Turkish lira

1.0

1.5

2.0

2.5

3.0

2.0

2.5

3.0

3.5

4.0

4.5

Jan-02 May-04 Sep-06 Jan-09 May-11 Sep-13

mn b/d Iranian crude production and exports

production exports (rhs)

mn b/d

Tupras 19 March 2015

34

Refining outlook in Europe Lower crude price boosts margins for some, at least for now Global crude oil prices have been in freefall in recent months, and we still see limited support for the market in the near term. The bulging surplus in crude oil is giving a mild boost to refiners via plunging feedstock costs.

In Europe, crude processing has seen a strong recovery since June when it averaged below 9.5 million b/d, the lowest refinery run rate since 1985, and utilisation rates are now above seasonal averages.

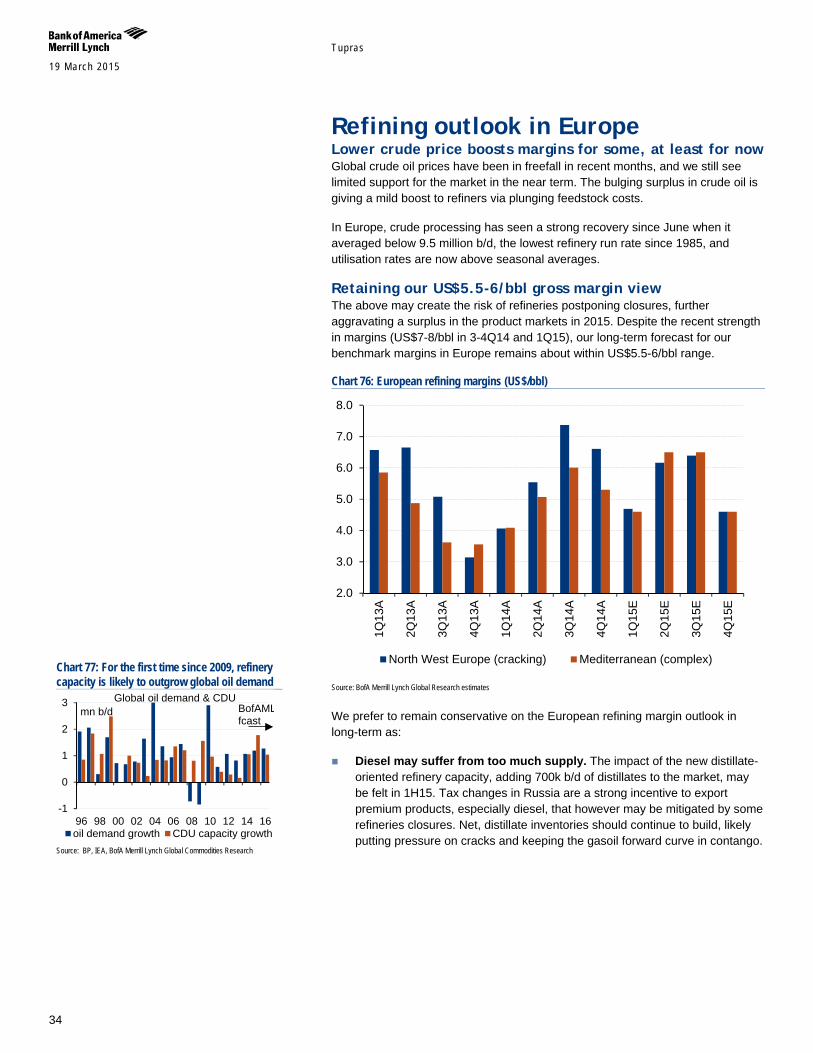

Retaining our US$5.5-6/bbl gross margin view The above may create the risk of refineries postponing closures, further aggravating a surplus in the product markets in 2015. Despite the recent strength in margins (US$7-8/bbl in 3-4Q14 and 1Q15), our long-term forecast for our benchmark margins in Europe remains about within US$5.5-6/bbl range.

Chart 76: European refining margins (US$/bbl)

Source: BofA Merrill Lynch Global Research estimates

We prefer to remain conservative on the European refining margin outlook in long-term as:

Diesel may suffer from too much supply. The impact of the new distillate-oriented refinery capacity, adding 700k b/d of distillates to the market, may be felt in 1H15. Tax changes in Russia are a strong incentive to export premium products, especially diesel, that however may be mitigated by some refineries closures. Net, distillate inventories should continue to build, likely putting pressure on cracks and keeping the gasoil forward curve in contango.

2.0

3.0

4.0

5.0

6.0

7.0

8.0

1Q13

A

2Q13

A

3Q13

A

4Q13

A

1Q14

A

2Q14

A

3Q14

A

4Q14

A

1Q15

E

2Q15

E

3Q15

E

4Q15

E

North West Europe (cracking) Mediterranean (complex)Chart 77: For the first time since 2009, refinery capacity is likely to outgrow global oil demand

Source: BP, IEA, BofA Merrill Lynch Global Commodities Research

-1

0

1

2

3

96 98 00 02 04 06 08 10 12 14 16

mn b/d Global oil demand & CDU

oil demand growth CDU capacity growth

BofAML fcast

Tupras 19 March 2015

35

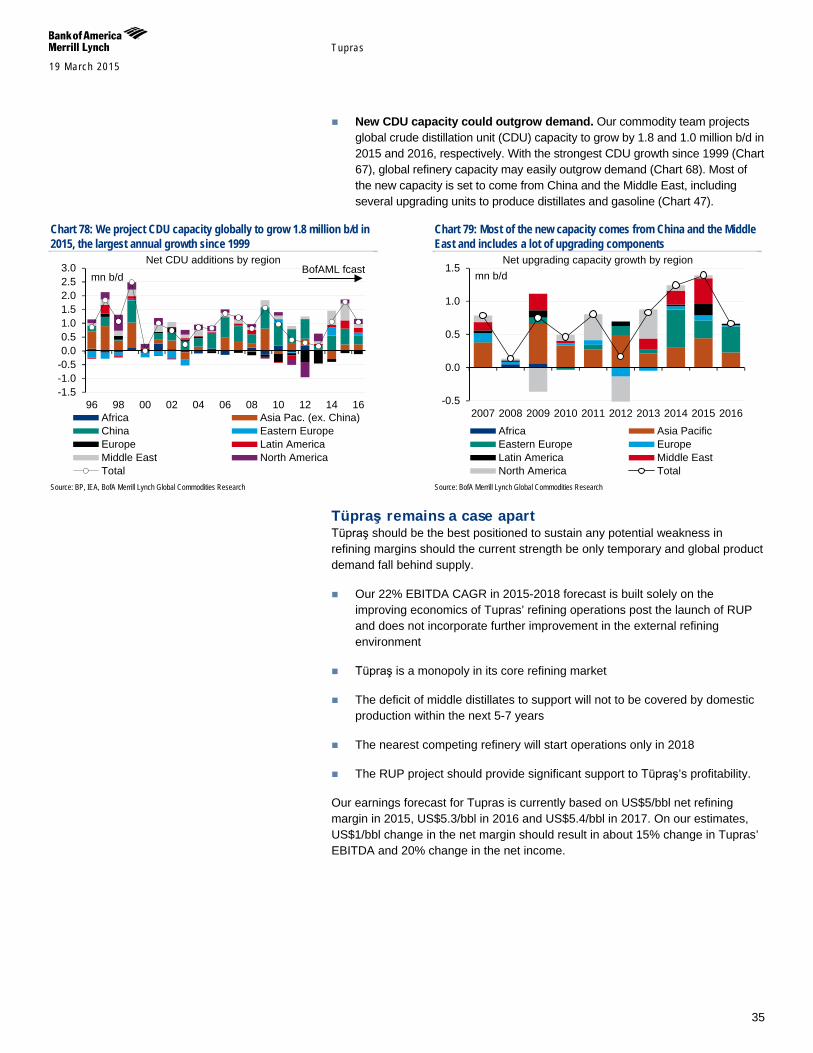

New CDU capacity could outgrow demand. Our commodity team projects global crude distillation unit (CDU) capacity to grow by 1.8 and 1.0 million b/d in 2015 and 2016, respectively. With the strongest CDU growth since 1999 (Chart 67), global refinery capacity may easily outgrow demand (Chart 68). Most of the new capacity is set to come from China and the Middle East, including several upgrading units to produce distillates and gasoline (Chart 47).

Chart 78: We project CDU capacity globally to grow 1.8 million b/d in 2015, the largest annual growth since 1999

Source: BP, IEA, BofA Merrill Lynch Global Commodities Research

Chart 79: Most of the new capacity comes from China and the Middle East and includes a lot of upgrading components

Source: BofA Merrill Lynch Global Commodities Research

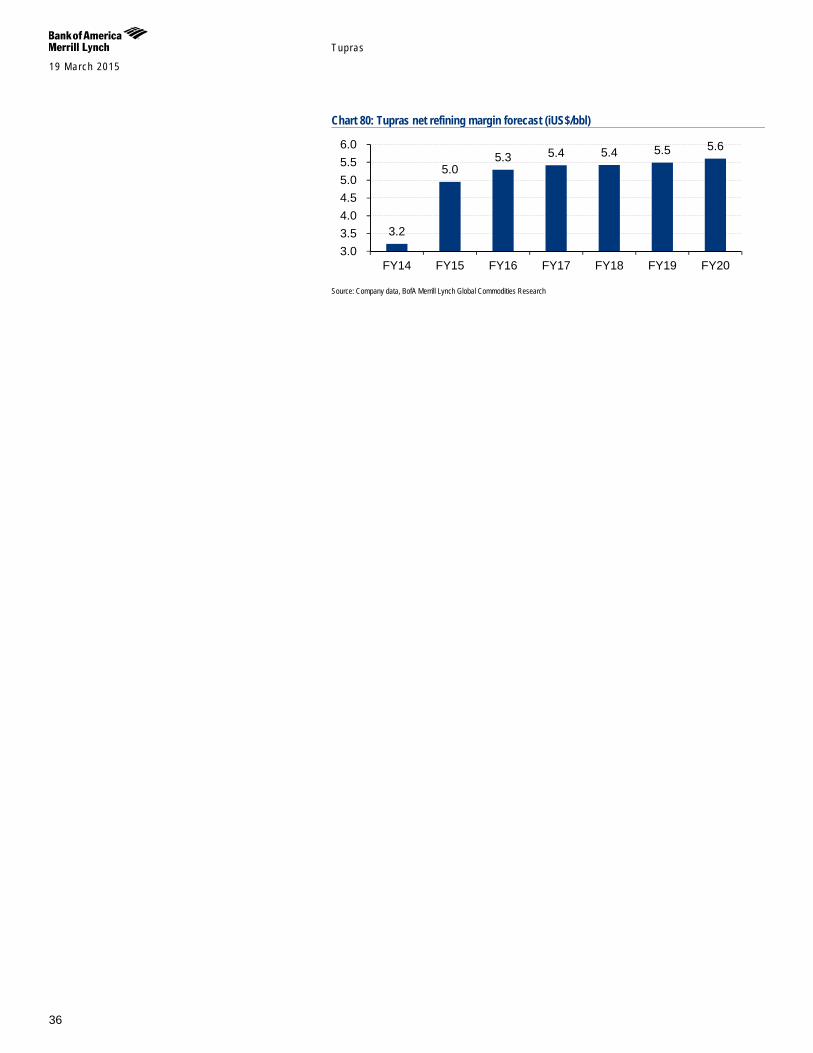

Tüpraş remains a case apart Tüpraş should be the best positioned to sustain any potential weakness in refining margins should the current strength be only temporary and global product demand fall behind supply.

Our 22% EBITDA CAGR in 2015-2018 forecast is built solely on the improving economics of Tupras’ refining operations post the launch of RUP and does not incorporate further improvement in the external refining environment

Tüpraş is a monopoly in its core refining market

The deficit of middle distillates to support will not to be covered by domestic production within the next 5-7 years

The nearest competing refinery will start operations only in 2018

The RUP project should provide significant support to Tüpraş’s profitability.

Our earnings forecast for Tupras is currently based on US$5/bbl net refining margin in 2015, US$5.3/bbl in 2016 and US$5.4/bbl in 2017. On our estimates, US$1/bbl change in the net margin should result in about 15% change in Tupras’ EBITDA and 20% change in the net income.

-1.5-1.0-0.50.00.51.01.52.02.53.0

96 98 00 02 04 06 08 10 12 14 16

mn b/d Net CDU additions by region

Africa Asia Pac. (ex. China)China Eastern EuropeEurope Latin AmericaMiddle East North AmericaTotal

BofAML fcast

-0.5

0.0

0.5

1.0

1.5

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

mn b/d Net upgrading capacity growth by region

Africa Asia PacificEastern Europe EuropeLatin America Middle EastNorth America Total

Tupras 19 March 2015

36

Chart 80: Tupras net refining margin forecast (iUS$/bbl)

Source: Company data, BofA Merrill Lynch Global Commodities Research

3.2

5.0 5.3 5.4 5.4 5.5 5.6

3.03.54.04.55.05.56.0

FY14 FY15 FY16 FY17 FY18 FY19 FY20

Tupras 19 March 2015

37

Risks to the investment case Our investment thesis may be prone to the following risks:

Changes in the refining outlook: Tüpraş is a pure play on refining margins and may be negatively affected should global supply of oil products outgrow demand. However, it is better positioned to withstand any macro shocks than its refining peers in EEMEA due to: (1) its dominant position in the Turkey market; and (2) flexible access to crude oil and ability to diversify its supply sources. In the meantime, our model is built based on our rather conservative long-term US$5.75/bbl in-house benchmark gross Med margin.

Risks to dividends: Tupras’ expected resumption and increase in dividends may come under question, if 1) Koc Holding acquires other assets in the oil & gas (i.e. upstream) via Tupras, 2) new upgrade projects in other refineries are launched (i.e. Kirikkale, Izmir).

Regulatory risk: 11% devaluation of TRY vs. USD year-to-date poses the risk of the regulators trying to put caps on the oil product prices in Turkey to curb down the inflation. In our view, such a risk is more relevant for the retail business rather than wholesale, as wholesale oil product prices in Turkey are linked to the CIF Mediterranean price quotes.