enterprise pillar e3 – enterprise strategy docs/2010 syllabus docs/e3/e3...enterprise strategy 3...

TRANSCRIPT

DO NOT OPEN THIS QUESTION PAPER UNTIL YOU ARE TOLD TO DO SO

© The Chartered Institute of Management Accountants 2014

E3 –

Ent

erpr

ise

Stra

tegy

Enterprise Pillar

E3 – Enterprise Strategy 18 November 2014 - Tuesday Morning Session

Instructions to candidates

You are allowed three hours to answer this question paper.

You are allowed 20 minutes reading time before the examination begins during which you should read the question paper and, if you wish, highlight and/or make notes on the question paper. However, you will not be allowed, under any circumstances, to open the answer book and start writing or use your calculator during this reading time.

You are strongly advised to carefully read ALL the question requirements before attempting the question concerned (that is all parts and/or sub-questions).

ALL answers must be written in the answer book. Answers written on the question paper will not be submitted for marking.

You should show all workings as marks are available for the method you use.

The pre-seen case study material is included in this question paper on pages 2 to 6. The unseen case study material, specific to this examination, is provided on pages 8 to 10.

Answer the compulsory questions in Section A on page 11. This page is detachable for ease of reference.

Answer TWO of the three questions in Section B on pages 14 to 19.

Maths tables and formulae are provided on pages 21 and 22.

The list of verbs as published in the syllabus is given for reference on page 23.

Write your candidate number, the paper number and examination subject title in the spaces provided on the front of the answer book. Also write your contact ID and name in the space provided in the right hand margin and seal to close.

Tick the appropriate boxes on the front of the answer book to indicate the questions you have answered.

TURN OVER

12

64

93

November 2014 2 Enterprise Strategy

Pre-seen case study Introduction Y was formed in 1900. It manufactures and sells top quality confectionery. For many years, Y has been recognised as a successful company and has become a household name particularly throughout Europe. Its fame is built on the very high quality confectionery products it sells through its own high street stores (some of which it owns and some which it leases). Y has just over 3,500 employees. All of Y’s products are manufactured in its factory in the European country in which it is based (which is in the eurozone). The products are distributed through a multi-channel network comprising of Y’s own stores and ‘online’ business, franchises and retail partners. In addition, Y has now started to supply confectionery to large retail stores and supermarkets on a contract basis. These stores sell Y’s products and also ‘own brand label’ confectionery that Y manufactures for them. Y’s product range includes a wide variety of milk, white, plain and diabetic chocolate products. Previously Y’s main sales had been chocolate products but now the company has expanded into producing other forms of confectionery which do not contain chocolate in any form, for example cakes and other sweets (candies). Y’s customers continue to have strong regard for the quality of its products. Although Y exports its products throughout the world, its largest market is within Europe. Y’s customers vary from individuals to corporate clients which purchase Y’s products to present to their own clients as corporate gifts. Although individual customers buy from Y’s stores, franchises or online, corporate clients purchase goods directly from Y on a contract basis. Business structure Y has a simple business structure. It has a head office (which includes its corporate treasury function) and two divisions: Direct Customer Sales (DCS), and Manufacturing and Commercial (MC). The activities of each division are as follows: DCS DCS has the following sales outlets:

• Y’s own stores • Franchises • Online sales

MC MC undertakes all purchasing of ingredients and manufacturing of Y’s products. It then supplies these products internally to:

• DCS for its sales through its own outlets externally to:

• Corporate clients • External retail stores and supermarkets which sell Y’s products under Y’s own label and

also under the stores’ own labels. Both divisions are investment centres but have limited capital investment authority, for expenditure up to EUR 10,000 per item. Major capital investments, above EUR 10,000 per item, have to be authorised by head office. DCS does not allow any of its outlets to make any capital investment at all without its prior approval. Each of DCS’s sales outlets is regarded as a profit centre, including online sales which is a single profit centre in its own right. Brand development is carried out by both of the divisions. Any brand development costs, such as promotion, above EUR 10,000 must be approved at head office.

Enterprise Strategy 3 November 2014

The decline of high street sales has led Y to reduce the number of its stores and expand other sales outlets. This has resulted in some staff being re-trained and re-deployed. Y currently has just over 300 of its own stores and fewer than 200 franchises. It also has developed its own website. This has been very popular and has enabled its international business to grow. In addition, as internet shopping has become more popular, Y has been able to develop its online sales business and has introduced ‘click and collect’ services using its stores and franchise businesses as the collection points. Mission, Aim and Objectives Y’s mission statement, agreed by the Board of Directors last year is: “To delight customers by providing luxurious products which strengthen the brand.” Y’s overall aim is to increase shareholder value by improving profit margins through increased sales and reduced costs. Despite the difficult economic conditions in Europe, the chocolate market has continued to grow in the last five years. Y’s customers engage particularly with chocolate products in response to austere economic conditions seeing them as an affordable alternative to higher priced gifts. Y is now placing greater emphasis on trying to ‘de-seasonalise’ its sales by not being reliant on the seasonal peak sales periods. Y is encouraging customers to buy its products throughout the year through all of its sales channels. This demands a strong focus on developing brand awareness. Y intends to achieve the continued development and growth of its business by meeting two strategic objectives which are to:

1. Engage with the widest range of customers through the development of Y’s markets and products through a wide variety of sales channels. The focus of this is on the delivery of products the customer demands, where they are required and when they are wanted.

2. Enhance the customer experience through strong and effective customer relationship management. The focus of this is on clear and consistent branding and marketing to encourage customer retention and loyalty all the year round.

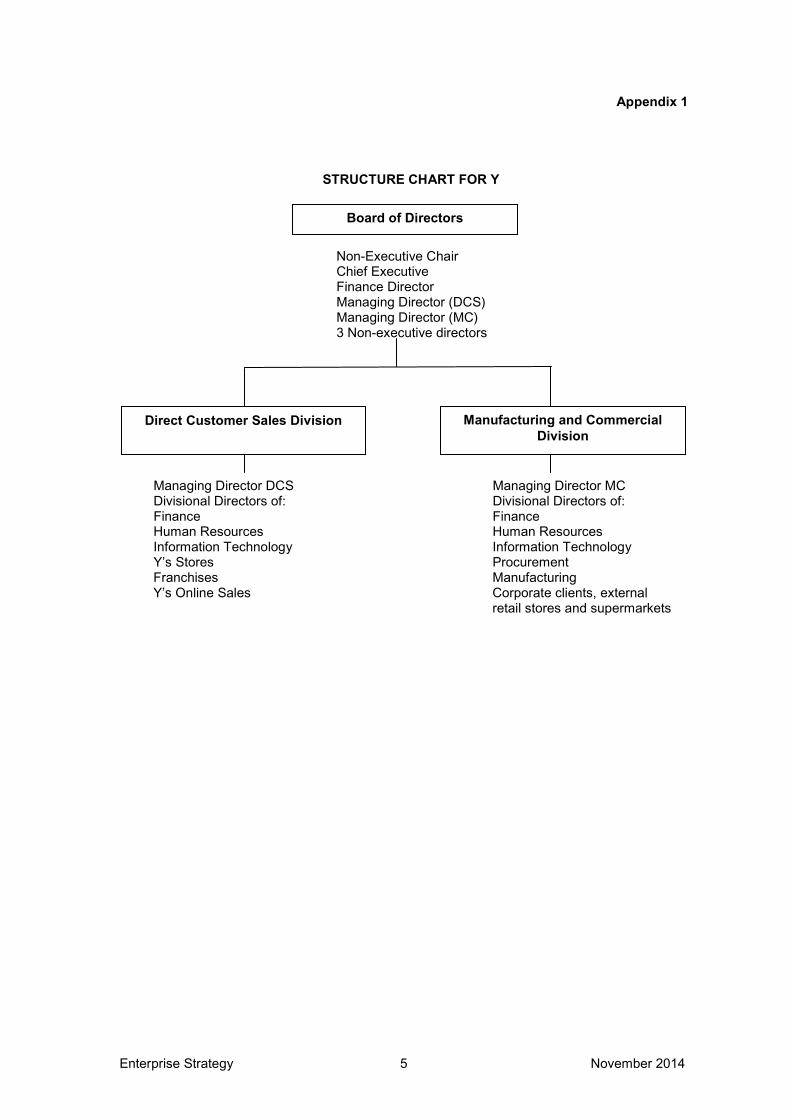

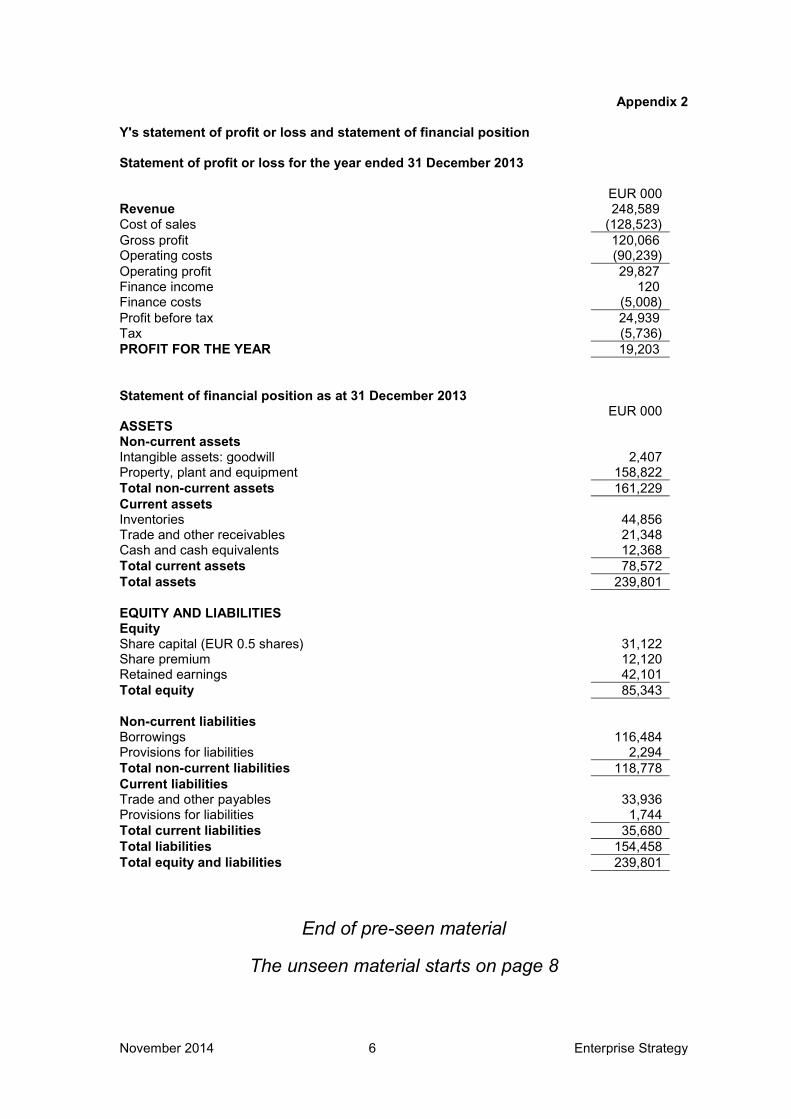

Y’s Board and Divisional Management The Board comprises a non-executive Chairman, a newly appointed Chief Executive, the Managing Directors of the two divisions, the Finance Director and three non-executive directors. The company applies good corporate governance principles and practice and the Board has a committee structure which includes an Audit Committee. The divisional structures reflect their different activities. The Managing Director of each division has a team comprising three divisional directors covering the functions of Finance, Human Resources and Information Technology. In addition, the DCS division has three divisional directors, one each responsible for Y’s stores, franchises and online sales. In addition to the divisional directors for Finance, Human Resources and IT, the MC division has three divisional directors, one responsible for procurement, one for manufacturing and one for commercial clients, retail stores and supermarkets. The structure for Y’s Board and its divisions is presented at Appendix 1. Financial overview Extracts from the statement of profit or loss for the year ended 31 December 2013 and statement of financial position as at 31 December 2013 are shown in Appendix 2. They show that in the last financial year, Y achieved an operating profit margin of 12% and profit after tax of 7.7%. Despite its best efforts in heavily re-investing in the business, Y’s bottom-line profit has stagnated. The Board is concerned that the expected actual profit for the year ended 31 December 2014, when compared with the forecast, is not looking as promising as was first thought. The Board is also mindful that some of Y’s borrowings are due for re-payment in 2015.

November 2014 4 Enterprise Strategy

In response to these concerns, the Board of Directors has determined the following financial objectives for Y:

• That it should operate on a sound financial basis in order to increase profit and shareholder value.

• That it should pay a regular and consistent dividend each year. Environmental and Corporate Social Responsibility Y aims to carry out its business with as little damage to the environment as possible and to operate in a fair manner with regard to all its stakeholders. It is keen to ensure that each of its suppliers adheres to high ethical and environmental standards with regard to sources of materials and treatment of employees. Y imports cocoa from Africa and Indonesia. Y has initiated schemes to encourage sustainable farming of cocoa and farmers are being trained in effective agricultural methods. The introduction of an industry approved certification programme has enabled farmers to achieve higher levels of income from increased production and to access additional training directed at improving their production yields. All raw materials sourced from Africa and Indonesia are priced in US Dollars (USD). All of Y’s products contain only the ingredients listed on the packaging. The packaging also shows nutritional content and gives advice on recommended volumes of consumption. Y tries to ensure that the packaging used for its products is recyclable and kept as minimal as possible to balance concerns over material usage with commercial marketing requirements. Environmentally friendly lighting has been introduced in Y’s factory which has reduced consumption of electricity and emission of carbon dioxide. Y has introduced annual independent health and safety audits in its factory and retail outlets. All factory staff have undertaken food safety and health and safety in the workplace training at the required industry standard level. Workplace benefits, such as life and medical insurance, staff discounts and membership of local gymnasia, as well as competitive salaries and wages are offered to all of Y’s employees. Strategic developments In order to achieve its overall mission, aim and objectives, Y intends to expand its online channel to increase its sales to corporate clients and external retail stores and supermarkets. These sales yield a higher margin than that achieved through sales in Y’s own high street stores. The Board also intends to further rationalise the number of its high street stores.

Enterprise Strategy 5 November 2014

Appendix 1

STRUCTURE CHART FOR Y

Non-Executive Chair Chief Executive Finance Director Managing Director (DCS) Managing Director (MC) 3 Non-executive directors

Managing Director DCS Managing Director MC Divisional Directors of: Divisional Directors of: Finance Finance Human Resources Human Resources Information Technology Information Technology Y’s Stores Procurement Franchises Manufacturing

Y’s Online Sales Corporate clients, external retail stores and supermarkets

Board of Directors

Direct Customer Sales Division Manufacturing and Commercial Division

November 2014 6 Enterprise Strategy

Appendix 2

Y's statement of profit or loss and statement of financial position Statement of profit or loss for the year ended 31 December 2013

EUR 000 Revenue 248,589 Cost of sales (128,523) Gross profit 120,066 Operating costs (90,239) Operating profit 29,827 Finance income 120 Finance costs (5,008) Profit before tax 24,939 Tax (5,736) PROFIT FOR THE YEAR 19,203 Statement of financial position as at 31 December 2013 EUR 000 ASSETS Non-current assets Intangible assets: goodwill 2,407 Property, plant and equipment 158,822 Total non-current assets 161,229 Current assets Inventories 44,856 Trade and other receivables 21,348 Cash and cash equivalents 12,368 Total current assets 78,572 Total assets 239,801 EQUITY AND LIABILITIES Equity Share capital (EUR 0.5 shares) 31,122 Share premium 12,120 Retained earnings 42,101 Total equity 85,343 Non-current liabilities Borrowings 116,484 Provisions for liabilities 2,294 Total non-current liabilities 118,778 Current liabilities Trade and other payables 33,936 Provisions for liabilities 1,744 Total current liabilities 35,680 Total liabilities 154,458 Total equity and liabilities 239,801

End of pre-seen material

The unseen material starts on page 8

Enterprise Strategy 7 November 2014

This page is blank

November 2014 8 Enterprise Strategy

SECTION A – 50 MARKS [You are advised to spend no longer than 90 minutes on this question]

ANSWER THIS QUESTION

Question One Unseen case material

Y intends to continue to develop through the delivery of the two strategic objectives (pre-seen page 3) to ensure the continued growth of the business. The two strategic objectives are:

• Strategic objective 1 (SO1): To engage with the widest range of customers through the development of Y's markets and products through a wide variety of sales channels. The focus of this is on the delivery of products the customer demands, where they are required and when they are wanted.

• Strategic objective 2 (SO2): To enhance the customer experience through strong and effective customer relationship management. The focus of this is on clear and consistent branding and marketing to encourage customer retention and loyalty all the year round.

Y’s sales development strategies Y currently operates its own retail stores and a number of franchise outlets on the high streets of towns and cities throughout Europe. Due to the continued challenges to the European economy, Y’s sales on the high street have been reducing annually for the last 5 years. Despite this, Y believes that its retail stores are a vital sales channel. Therefore, Y has decided that investment in its retail stores and employees must be made to improve the customer experience and the brand image. This will be achieved through engaging better with customers in the retail stores and providing a wide range of high quality products. Y is proposing to close 30 to 40 of its own retail stores during the course of the 2015 financial year and focusing upon ensuring that the remaining stores are in the best locations to attract customers. In the last two years, Y has seen a growth in the sales of its own label products to supermarkets. It is predicted that sales of Y’s own label products in supermarkets will have grown by 10% by the end of 2014, as a result of Y increasing its distribution network to a wider range of supermarket chains and through supplying a greater variety of its year-round products. Y anticipates further growth in its sales to supermarkets and intends to continue to invest in improving its expertise in managing its supermarket customer accounts. Y operates a website, through which it sells a wide range of products. This has proved to be a very successful sales channel since its launch in 2012. Y is keen to develop its e-business sales channel and is considering using the website to sell an even wider product range including gift hampers. Y considers that its website will play an important role in the development of its international sales to individual customers. Y’s international sales are anticipated to grow strongly in the next 2 years. Y aims to invest in a structured country-by-country approach and learn from its experience as it progresses. Over the past year, Y has been encouraged by the number of sales achieved in international markets, particularly from international supermarket sales. In the last year, Y has started to manufacture luxury hand-made products for other external retail stores, some of which sell these products under their 'own brand' labels. This is an opportunity for Y to create innovative products but the Board realises that this is likely to require investment in staff training and facilities. Y is planning to open 6 ‘Y Cafes’ in city centre locations within its home country within the first 3 months of 2015 with plans for further expansion later in the year. These will sell a range of Y’s products as well as offering food and refreshments and other gift items.

Enterprise Strategy 9 November 2014

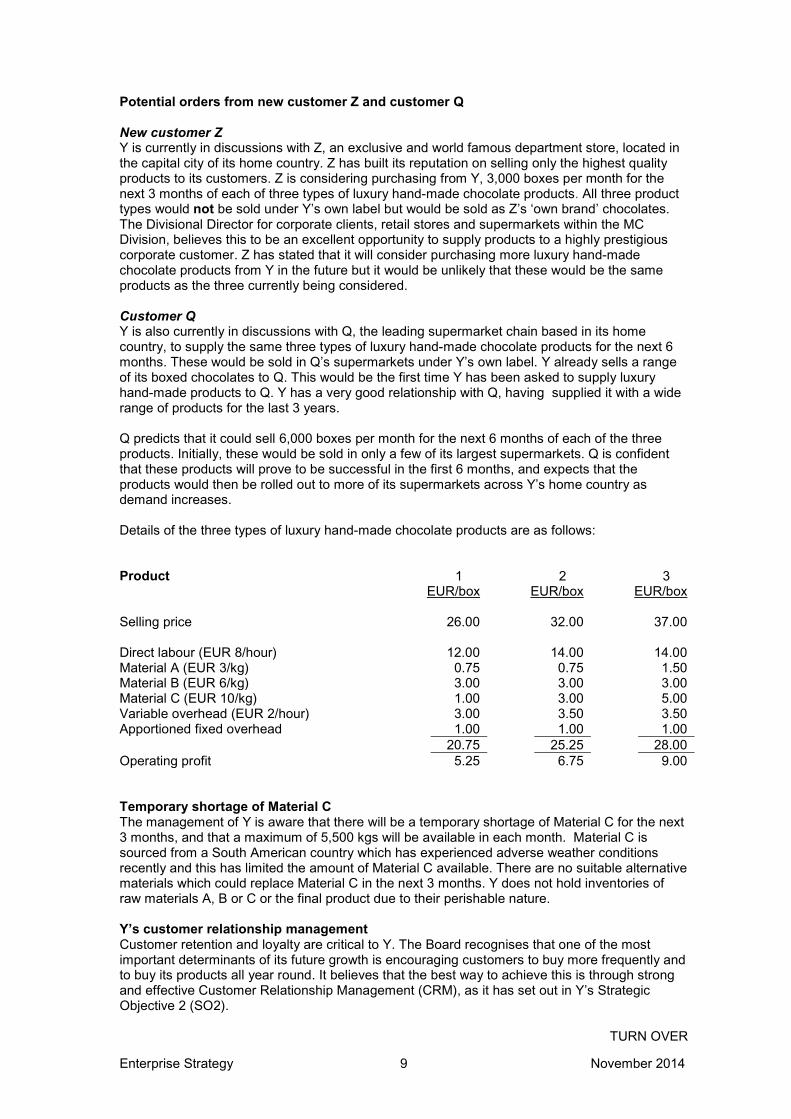

Potential orders from new customer Z and customer Q New customer Z Y is currently in discussions with Z, an exclusive and world famous department store, located in the capital city of its home country. Z has built its reputation on selling only the highest quality products to its customers. Z is considering purchasing from Y, 3,000 boxes per month for the next 3 months of each of three types of luxury hand-made chocolate products. All three product types would not be sold under Y’s own label but would be sold as Z’s ‘own brand’ chocolates. The Divisional Director for corporate clients, retail stores and supermarkets within the MC Division, believes this to be an excellent opportunity to supply products to a highly prestigious corporate customer. Z has stated that it will consider purchasing more luxury hand-made chocolate products from Y in the future but it would be unlikely that these would be the same products as the three currently being considered. Customer Q Y is also currently in discussions with Q, the leading supermarket chain based in its home country, to supply the same three types of luxury hand-made chocolate products for the next 6 months. These would be sold in Q’s supermarkets under Y’s own label. Y already sells a range of its boxed chocolates to Q. This would be the first time Y has been asked to supply luxury hand-made products to Q. Y has a very good relationship with Q, having supplied it with a wide range of products for the last 3 years. Q predicts that it could sell 6,000 boxes per month for the next 6 months of each of the three products. Initially, these would be sold in only a few of its largest supermarkets. Q is confident that these products will prove to be successful in the first 6 months, and expects that the products would then be rolled out to more of its supermarkets across Y’s home country as demand increases. Details of the three types of luxury hand-made chocolate products are as follows: Product 1 2 3 EUR/box EUR/box

EUR/box

Selling price 26.00 32.00 37.00 Direct labour (EUR 8/hour) 12.00 14.00 14.00 Material A (EUR 3/kg) 0.75 0.75 1.50 Material B (EUR 6/kg) 3.00 3.00 3.00 Material C (EUR 10/kg) 1.00 3.00 5.00 Variable overhead (EUR 2/hour) 3.00 3.50 3.50 Apportioned fixed overhead 1.00 1.00 1.00 20.75 25.25 28.00 Operating profit 5.25 6.75 9.00 Temporary shortage of Material C The management of Y is aware that there will be a temporary shortage of Material C for the next 3 months, and that a maximum of 5,500 kgs will be available in each month. Material C is sourced from a South American country which has experienced adverse weather conditions recently and this has limited the amount of Material C available. There are no suitable alternative materials which could replace Material C in the next 3 months. Y does not hold inventories of raw materials A, B or C or the final product due to their perishable nature. Y’s customer relationship management Customer retention and loyalty are critical to Y. The Board recognises that one of the most important determinants of its future growth is encouraging customers to buy more frequently and to buy its products all year round. It believes that the best way to achieve this is through strong and effective Customer Relationship Management (CRM), as it has set out in Y’s Strategic Objective 2 (SO2).

TURN OVER

November 2014 10 Enterprise Strategy

Y considers that a key factor in building and managing strong customer relationships will be the continued development and use of Y’s website. Y strongly believes that e-business will be a key feature of strengthening and building strong customer relationships, ensuring customer retention and strengthening its reputation as a year-round confectionery retailer.

End of unseen material

The requirement for Question One is on the opposite page

Enterprise Strategy 11 November 2014

(Total for Section A = 50 marks)

End of Section A Section B starts on page 14

TURN OVER

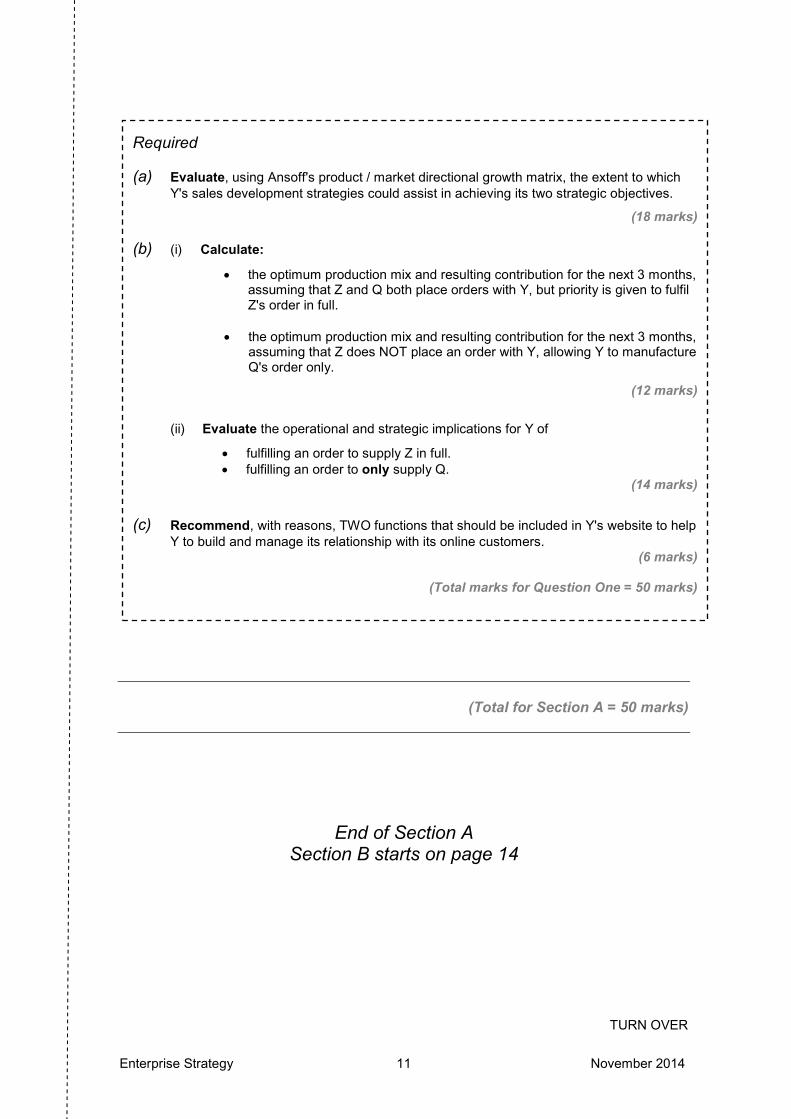

Required (a) Evaluate, using Ansoff's product / market directional growth matrix, the extent to which

Y's sales development strategies could assist in achieving its two strategic objectives.

(18 marks)

(b) (i) Calculate:

• the optimum production mix and resulting contribution for the next 3 months, assuming that Z and Q both place orders with Y, but priority is given to fulfil Z's order in full.

• the optimum production mix and resulting contribution for the next 3 months, assuming that Z does NOT place an order with Y, allowing Y to manufacture Q's order only.

(12 marks)

(ii) Evaluate the operational and strategic implications for Y of

• fulfilling an order to supply Z in full. • fulfilling an order to only supply Q.

(14 marks)

(c) Recommend, with reasons, TWO functions that should be included in Y's website to help Y to build and manage its relationship with its online customers.

(6 marks)

(Total marks for Question One = 50 marks)

November 2014 12 Enterprise Strategy

This page is blank

Enterprise Strategy 13 November 2014

This page is blank

TURN OVER

November 2014 14 Enterprise Strategy

SECTION B – 50 MARKS [You are advised to spend no longer than 45 minutes on each question in this section]

ANSWER TWO OF THE THREE QUESTIONS – 25 MARKS EACH

Question Two P is an IT consultancy business based in Country M’s capital city. P specialises in consultancy activities relating principally to database management and IT security. Since its formation in 2004, P has grown organically and has built a strong reputation within its two areas of specialisation. Competition is strong in the IT consultancy industry and P faces competition from a number of local and international IT consultancy businesses operating throughout Country M. P employs highly qualified and skilled IT staff, whose time is charged out to clients on an hourly basis. P’s clients expect high quality service delivery and many also require P to be available to respond 24 hours a day, 7 days a week. P has been highly innovative in the last few years, with a number of its IT staff building upon their areas of expertise and knowledge to develop new opportunities in P’s IT consultancy portfolio. These new consultancy activities are in the areas of big data and cyber security. P’s five senior partners hold monthly meetings in which they discuss performance. At these meetings, the five senior partners mainly focus upon comparing actual performance versus budgeted performance for the revenues and profit generated by P. The partners also review the latest market share and client feedback information, based upon client surveys carried out each month. P’s IT staff are paid an annual salary and individual bonuses are also paid, based upon a team manager's assessment of each individual’s performance and achievement of targets throughout the year. It is rare that bonuses are not paid and most IT staff are not consulted directly by their team manager regarding their targets. The five senior partners receive a fixed salary and a bonus based upon the overall annual business profits. At a recent monthly meeting, the five senior partners discussed performance targets for P for 2015. One of the founding partners, who had recently returned from a conference attended by a range of consultancy businesses, expressed concern that P’s existing performance information is not focussed on the key activities of P’s business. He believes that as a service business, P must focus upon a wider range of dimensions beyond just market share and financial performance.

.

The requirement for Question Two is on the opposite page

Enterprise Strategy 15 November 2014

Section B continues on page 16

TURN OVER

Required (a) Explain FOUR characteristics of a service business, using P to illustrate your

answer. (8 marks)

(b) Evaluate the current process used by the five senior partners when reviewing P's performance and the current process used to set targets.

You should use Fitzgerald and Moon's 'Building Block Model' to assist in structuring your answer.

(11 marks)

(c) Recommend, with reasons, TWO suitable performance measures which could be used to assist P in measuring those areas of its business in which it must succeed, in order to remain competitive.

(6 marks)

(Total for Question Two = 25 marks)

November 2014 16 Enterprise Strategy

Question Three M is a retailer of children’s games and toys, with stores located in many cities throughout the world. The games and toys which M sells are sourced from hundreds of suppliers from around the world. M works closely with its supply chain to ensure that all of its suppliers of games and toys understand and adhere to M’s high ethical standards. All of M’s suppliers are monitored regularly to verify their compliance in areas such as fair and proper treatment of employees. These include fair wage payments and adherence to local working hours laws, health and safety training and non-discrimination activities. M also has strict policies that suppliers are prohibited from offering bribes, gifts, or favours to gain a competitive advantage with M. M is currently in discussions with B, a family run business in Eastern Europe to supply a range of traditional wooden toys including rocking horses and dolls' houses. This order would provide B with guaranteed work over the next two years for its current 100 factory employees. B has a reputation for high quality products and has made toys for a number of other retailers throughout Europe. It is owned and run by Mr Fox, the son of the original founder of the business. Mr Fox has worked for B for 35 years. He has a very strong belief in the family traditions of the business and although B has a senior management team, Mr Fox makes most of the key business decisions himself, with limited consultation with the senior managers. Most of B’s current senior management team have worked at B for fewer than five years. In the recent economic recession, over 50 employees were made redundant by B. The remaining 100 factory employees have not received a pay rise for the last three years and most are paid at the national minimum wage rate. A large proportion of B’s employees have worked for B for many years and are highly skilled. Over 70% of B’s factory employees are over the age of 50. B’s employees sometimes work overtime for no additional payment and most fear that if they don’t do unpaid overtime they would lose their jobs. Investment in staff training, in particular in health and safety procedures, has reduced dramatically in the last three years and few staff have any formal qualifications. Unemployment levels in the country within which B is located are currently very high. Mr Fox frequently reminds staff, in the monthly news bulletin posted on notice boards throughout the factory, that they are lucky to work for such a prestigious and long-standing family-run business. M’s supplier inspection team undertakes a factory visit prior to placing an order with any new supplier. Prior to a planned visit to B, Mr Fox called all of B’s employees to a meeting in which he informed them that if M were to place an order with B, then this will save the business from closure. B’s employees were instructed not to discuss with M’s inspection team the overtime they regularly worked and many of B’s employees felt threatened that they would lose their jobs if they did so. During the visit by M’s supplier inspection team to B’s factory a few days later, Mr Fox offered to pay for trips to expensive and exclusive restaurants and attractions for M’s inspection team, whilst they were visiting the country. M’s inspectors were highly impressed by the quality of the output produced by B and by the loyalty and commitment demonstrated by B’s staff. However, they had a number of serious concerns with B’s company culture and its ability to comply with M’s ethical standards. Before any decision is made about selecting B and placing an initial order, M’s inspection team must consider a range of ways in which it could help B to meet M’s ethical standards.

The requirement for Question Three is on the opposite page

Enterprise Strategy 17 November 2014

Section B continues on page 18

TURN OVER

Required (a) Discuss how the recent actions of Mr Fox would compromise M's requirement that

its suppliers act in accordance with M's high ethical standards. (6 marks)

(b) Evaluate each of the relevant aspects of B's current cultural web and advise on the

ways in which it would need to change to enable B to meet the high ethical standards M sets for its suppliers.

(10 marks)

(c) Recommend, with reasons, THREE ways in which M could assist Mr Fox to improve his and B's ethical standards.

(9 marks)

(Total for Question Three = 25 marks)

November 2014 18 Enterprise Strategy

Question Four C is an organisation which owns and operates a world famous tourist attraction of historic interest located in Country A. The tourist attraction is an ancient castle set within landscaped gardens and a large area of parkland. The grounds contain a large adventure playground for children, three cafes and a large shop in which visitors can buy a range of gifts. There is also a large function room, where business conferences and weddings are regularly held. In the summer of 2015, C intends to open a number of holiday lodges located within the grounds. C has over 10,000 season ticket holders, who are customers that buy an annual pass which allows them to enter the attraction on as many occasions as they wish throughout the year. Most season ticket holders are local people who enjoy the peace and tranquillity of the location. Most season tickets are purchased by retired people or by parents with young children. C holds large pop music concerts once or twice per year which often attract thousands of young people. It also regularly runs a variety of children’s events throughout the holiday and festive periods. C’s current website was set up 5 years ago. The website is informational, outlining all of C’s facilities, opening times, contact details and C’s forthcoming events. There are currently no online booking or contact facilities for customers on the website. Customers who wish to buy tickets for events and concerts or book conferences must do so by telephone or through personal visits to C. C recently appointed a marketing manager, J, who has worked in the travel and tourism industry for 20 years. J was surprised to find that C does not undertake any analysis of its customer segments and that its advertising and marketing efforts are largely focused on very traditional methods. These include advertisements in regional and national newspapers, in magazines and on radio and through marketing leaflets and brochures. J wishes to undertake an immediate review of C’s marketing strategy. He believes that through a better understanding of its customer segments it could target its customers more effectively. J also believes that C should use the Internet more effectively to engage with its customer segments, using an e-business approach.

The requirement for Question Four is on the opposite page

Enterprise Strategy 19 November 2014

End of Question Paper Maths Tables and Formulae are on Pages 21 and 22

Required (a) Advise C of the importance of understanding its customer segments. Your answer

should include advice to C on the most appropriate ways in which C could segment its customers.

(9 marks)

(b) Discuss the benefits for C of employing an e-business approach to engage with its customer segments.

(10 marks)

(c) Recommend, with reasons, TWO different types of Web 2.0 technologies which could be used by C to engage with its customers more effectively.

(6 marks)

(Total for Question Four = 25 marks)

November 2014 20 Enterprise Strategy

This page is blank

Enterprise Strategy 21 November 2014

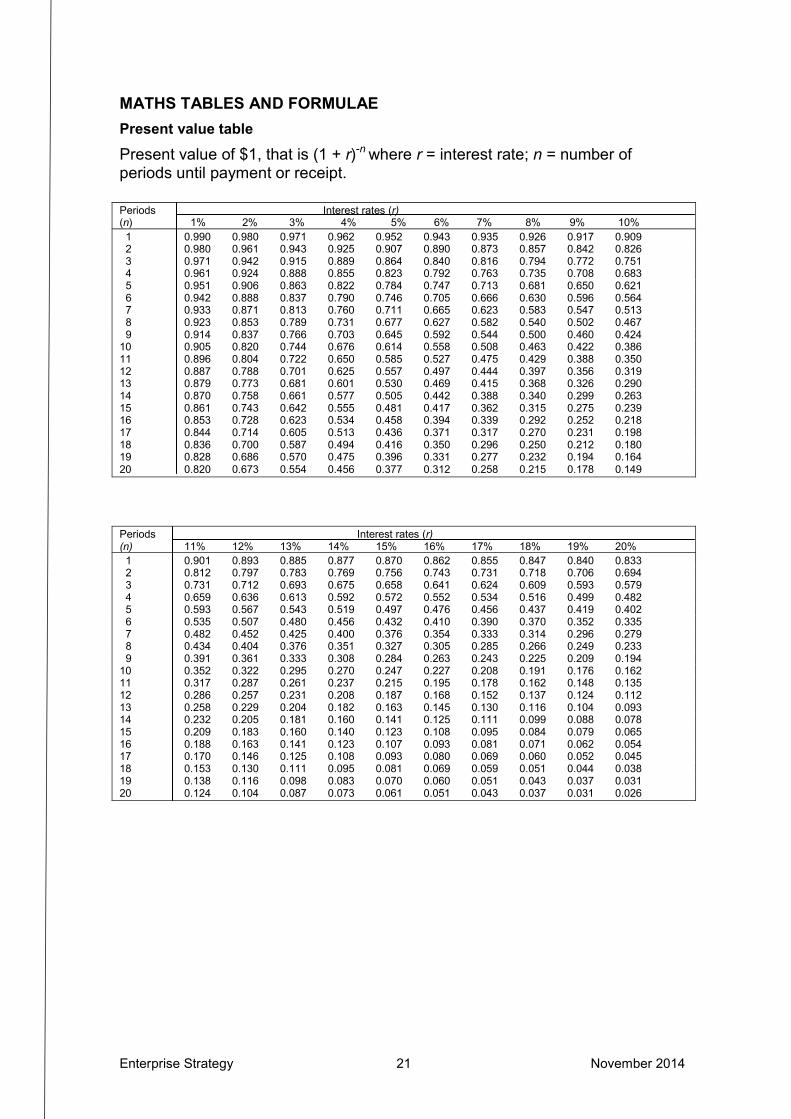

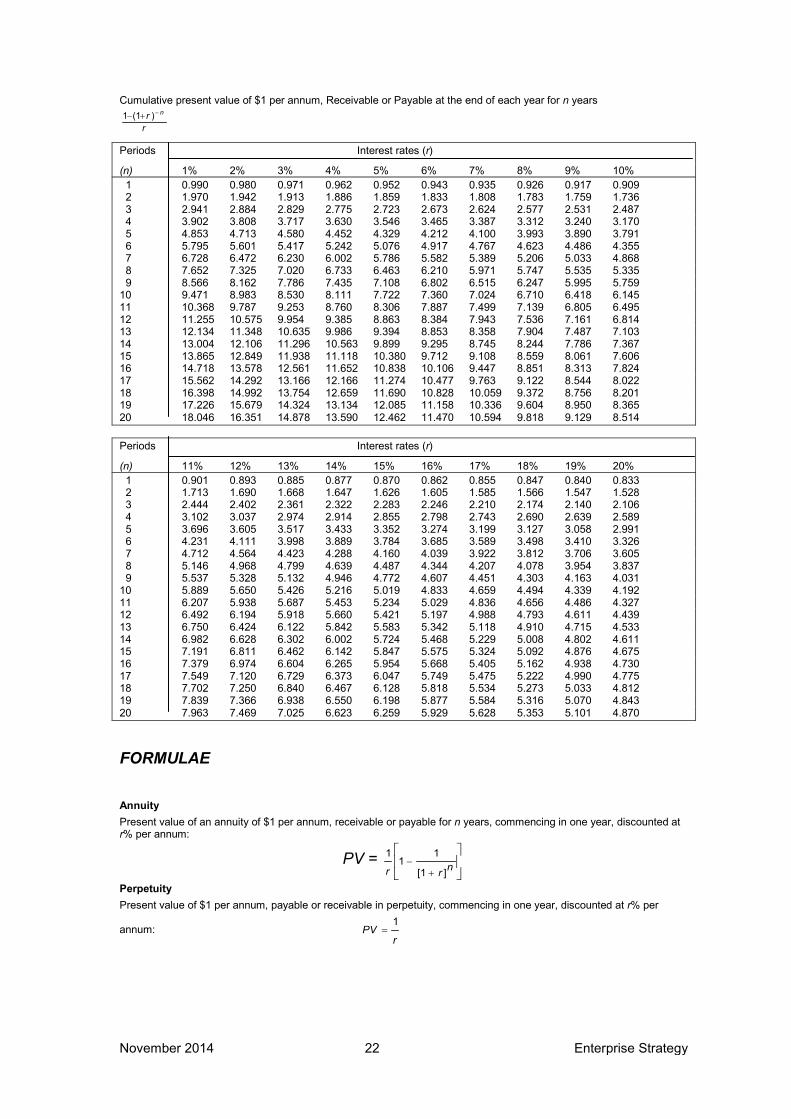

MATHS TABLES AND FORMULAE Present value table

Present value of $1, that is (1 + r)-n where r = interest rate; n = number of periods until payment or receipt.

Periods Interest rates (r) (n) 1% 2% 3% 4% 5% 6% 7% 8% 9% 10% 1 0.990 0.980 0.971 0.962 0.952 0.943 0.935 0.926 0.917 0.909 2 0.980 0.961 0.943 0.925 0.907 0.890 0.873 0.857 0.842 0.826 3 0.971 0.942 0.915 0.889 0.864 0.840 0.816 0.794 0.772 0.751 4 0.961 0.924 0.888 0.855 0.823 0.792 0.763 0.735 0.708 0.683 5 0.951 0.906 0.863 0.822 0.784 0.747 0.713 0.681 0.650 0.621 6 0.942 0.888 0.837 0.790 0.746 0.705 0.666 0.630 0.596 0.564 7 0.933 0.871 0.813 0.760 0.711 0.665 0.623 0.583 0.547 0.513 8 0.923 0.853 0.789 0.731 0.677 0.627 0.582 0.540 0.502 0.467 9 0.914 0.837 0.766 0.703 0.645 0.592 0.544 0.500 0.460 0.424 10 0.905 0.820 0.744 0.676 0.614 0.558 0.508 0.463 0.422 0.386 11 0.896 0.804 0.722 0.650 0.585 0.527 0.475 0.429 0.388 0.350 12 0.887 0.788 0.701 0.625 0.557 0.497 0.444 0.397 0.356 0.319 13 0.879 0.773 0.681 0.601 0.530 0.469 0.415 0.368 0.326 0.290 14 0.870 0.758 0.661 0.577 0.505 0.442 0.388 0.340 0.299 0.263 15 0.861 0.743 0.642 0.555 0.481 0.417 0.362 0.315 0.275 0.239 16 0.853 0.728 0.623 0.534 0.458 0.394 0.339 0.292 0.252 0.218 17 0.844 0.714 0.605 0.513 0.436 0.371 0.317 0.270 0.231 0.198 18 0.836 0.700 0.587 0.494 0.416 0.350 0.296 0.250 0.212 0.180 19 0.828 0.686 0.570 0.475 0.396 0.331 0.277 0.232 0.194 0.164 20 0.820 0.673 0.554 0.456 0.377 0.312 0.258 0.215 0.178 0.149

Periods Interest rates (r) (n) 11% 12% 13% 14% 15% 16% 17% 18% 19% 20% 1 0.901 0.893 0.885 0.877 0.870 0.862 0.855 0.847 0.840 0.833 2 0.812 0.797 0.783 0.769 0.756 0.743 0.731 0.718 0.706 0.694 3 0.731 0.712 0.693 0.675 0.658 0.641 0.624 0.609 0.593 0.579 4 0.659 0.636 0.613 0.592 0.572 0.552 0.534 0.516 0.499 0.482 5 0.593 0.567 0.543 0.519 0.497 0.476 0.456 0.437 0.419 0.402 6 0.535 0.507 0.480 0.456 0.432 0.410 0.390 0.370 0.352 0.335 7 0.482 0.452 0.425 0.400 0.376 0.354 0.333 0.314 0.296 0.279 8 0.434 0.404 0.376 0.351 0.327 0.305 0.285 0.266 0.249 0.233 9 0.391 0.361 0.333 0.308 0.284 0.263 0.243 0.225 0.209 0.194 10 0.352 0.322 0.295 0.270 0.247 0.227 0.208 0.191 0.176 0.162 11 0.317 0.287 0.261 0.237 0.215 0.195 0.178 0.162 0.148 0.135 12 0.286 0.257 0.231 0.208 0.187 0.168 0.152 0.137 0.124 0.112 13 0.258 0.229 0.204 0.182 0.163 0.145 0.130 0.116 0.104 0.093 14 0.232 0.205 0.181 0.160 0.141 0.125 0.111 0.099 0.088 0.078 15 0.209 0.183 0.160 0.140 0.123 0.108 0.095 0.084 0.079 0.065 16 0.188 0.163 0.141 0.123 0.107 0.093 0.081 0.071 0.062 0.054 17 0.170 0.146 0.125 0.108 0.093 0.080 0.069 0.060 0.052 0.045 18 0.153 0.130 0.111 0.095 0.081 0.069 0.059 0.051 0.044 0.038 19 0.138 0.116 0.098 0.083 0.070 0.060 0.051 0.043 0.037 0.031 20 0.124 0.104 0.087 0.073 0.061 0.051 0.043 0.037 0.031 0.026

November 2014 22 Enterprise Strategy

Cumulative present value of $1 per annum, Receivable or Payable at the end of each year for n years

rr n−+− )(11

Periods Interest rates (r) (n) 1% 2% 3% 4% 5% 6% 7% 8% 9% 10% 1 0.990 0.980 0.971 0.962 0.952 0.943 0.935 0.926 0.917 0.909 2 1.970 1.942 1.913 1.886 1.859 1.833 1.808 1.783 1.759 1.736 3 2.941 2.884 2.829 2.775 2.723 2.673 2.624 2.577 2.531 2.487 4 3.902 3.808 3.717 3.630 3.546 3.465 3.387 3.312 3.240 3.170 5 4.853 4.713 4.580 4.452 4.329 4.212 4.100 3.993 3.890 3.791 6 5.795 5.601 5.417 5.242 5.076 4.917 4.767 4.623 4.486 4.355 7 6.728 6.472 6.230 6.002 5.786 5.582 5.389 5.206 5.033 4.868 8 7.652 7.325 7.020 6.733 6.463 6.210 5.971 5.747 5.535 5.335 9 8.566 8.162 7.786 7.435 7.108 6.802 6.515 6.247 5.995 5.759 10 9.471 8.983 8.530 8.111 7.722 7.360 7.024 6.710 6.418 6.145 11 10.368 9.787 9.253 8.760 8.306 7.887 7.499 7.139 6.805 6.495 12 11.255 10.575 9.954 9.385 8.863 8.384 7.943 7.536 7.161 6.814 13 12.134 11.348 10.635 9.986 9.394 8.853 8.358 7.904 7.487 7.103 14 13.004 12.106 11.296 10.563 9.899 9.295 8.745 8.244 7.786 7.367 15 13.865 12.849 11.938 11.118 10.380 9.712 9.108 8.559 8.061 7.606 16 14.718 13.578 12.561 11.652 10.838 10.106 9.447 8.851 8.313 7.824 17 15.562 14.292 13.166 12.166 11.274 10.477 9.763 9.122 8.544 8.022 18 16.398 14.992 13.754 12.659 11.690 10.828 10.059 9.372 8.756 8.201 19 17.226 15.679 14.324 13.134 12.085 11.158 10.336 9.604 8.950 8.365 20 18.046 16.351 14.878 13.590 12.462 11.470 10.594 9.818 9.129 8.514 Periods Interest rates (r) (n) 11% 12% 13% 14% 15% 16% 17% 18% 19% 20% 1 0.901 0.893 0.885 0.877 0.870 0.862 0.855 0.847 0.840 0.833 2 1.713 1.690 1.668 1.647 1.626 1.605 1.585 1.566 1.547 1.528 3 2.444 2.402 2.361 2.322 2.283 2.246 2.210 2.174 2.140 2.106 4 3.102 3.037 2.974 2.914 2.855 2.798 2.743 2.690 2.639 2.589 5 3.696 3.605 3.517 3.433 3.352 3.274 3.199 3.127 3.058 2.991 6 4.231 4.111 3.998 3.889 3.784 3.685 3.589 3.498 3.410 3.326 7 4.712 4.564 4.423 4.288 4.160 4.039 3.922 3.812 3.706 3.605 8 5.146 4.968 4.799 4.639 4.487 4.344 4.207 4.078 3.954 3.837 9 5.537 5.328 5.132 4.946 4.772 4.607 4.451 4.303 4.163 4.031 10 5.889 5.650 5.426 5.216 5.019 4.833 4.659 4.494 4.339 4.192 11 6.207 5.938 5.687 5.453 5.234 5.029 4.836 4.656 4.486 4.327 12 6.492 6.194 5.918 5.660 5.421 5.197 4.988 4.793 4.611 4.439 13 6.750 6.424 6.122 5.842 5.583 5.342 5.118 4.910 4.715 4.533 14 6.982 6.628 6.302 6.002 5.724 5.468 5.229 5.008 4.802 4.611 15 7.191 6.811 6.462 6.142 5.847 5.575 5.324 5.092 4.876 4.675 16 7.379 6.974 6.604 6.265 5.954 5.668 5.405 5.162 4.938 4.730 17 7.549 7.120 6.729 6.373 6.047 5.749 5.475 5.222 4.990 4.775 18 7.702 7.250 6.840 6.467 6.128 5.818 5.534 5.273 5.033 4.812 19 7.839 7.366 6.938 6.550 6.198 5.877 5.584 5.316 5.070 4.843 20 7.963 7.469 7.025 6.623 6.259 5.929 5.628 5.353 5.101 4.870

FORMULAE

Annuity Present value of an annuity of $1 per annum, receivable or payable for n years, commencing in one year, discounted at r% per annum:

PV =

+− nrr ][1

11

1

Perpetuity Present value of $1 per annum, payable or receivable in perpetuity, commencing in one year, discounted at r% per

annum: r

PV1

=

Enterprise Strategy 23 November 2014

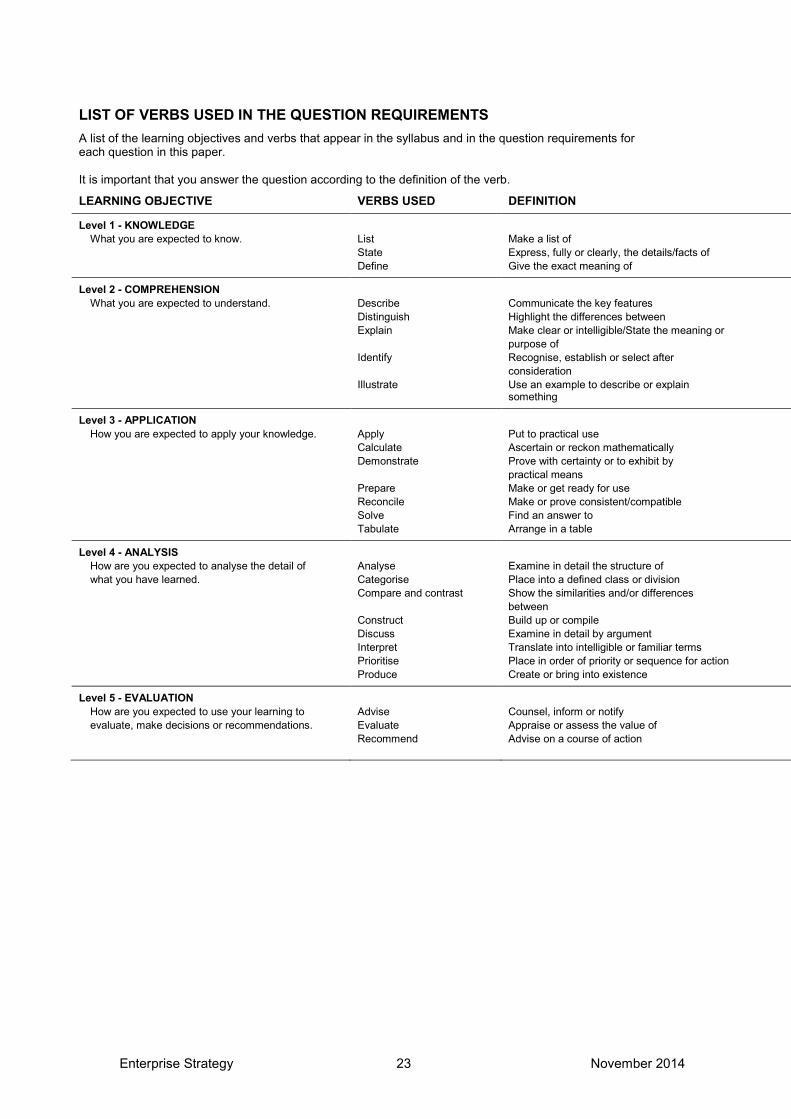

LIST OF VERBS USED IN THE QUESTION REQUIREMENTS A list of the learning objectives and verbs that appear in the syllabus and in the question requirements for each question in this paper. It is important that you answer the question according to the definition of the verb.

LEARNING OBJECTIVE VERBS USED DEFINITION

Level 1 - KNOWLEDGE

What you are expected to know. List Make a list of State Express, fully or clearly, the details/facts of Define Give the exact meaning of

Level 2 - COMPREHENSION What you are expected to understand. Describe Communicate the key features

Distinguish Highlight the differences between Explain Make clear or intelligible/State the meaning or

purpose of Identify Recognise, establish or select after

consideration Illustrate Use an example to describe or explain

something

Level 3 - APPLICATION How you are expected to apply your knowledge. Apply

Calculate Put to practical use Ascertain or reckon mathematically

Demonstrate Prove with certainty or to exhibit by practical means

Prepare Make or get ready for use Reconcile Make or prove consistent/compatible Solve Find an answer to Tabulate Arrange in a table

Level 4 - ANALYSIS How are you expected to analyse the detail of what you have learned.

Analyse Categorise

Examine in detail the structure of Place into a defined class or division

Compare and contrast Show the similarities and/or differences between

Construct Build up or compile Discuss Examine in detail by argument Interpret

Prioritise Translate into intelligible or familiar terms Place in order of priority or sequence for action

Produce Create or bring into existence

Level 5 - EVALUATION How are you expected to use your learning to evaluate, make decisions or recommendations.

Advise Evaluate Recommend

Counsel, inform or notify Appraise or assess the value of Advise on a course of action

November 2014 24 Enterprise Strategy

Enterprise Pillar

Strategic Level Paper

E3 – Enterprise Strategy

November 2014

Tuesday Morning Session