entrepreneurship and venture investment in china york chen 陈友忠 id techventures ltd....

Post on 18-Dec-2015

266 views

TRANSCRIPT

Entrepreneurship and Venture Investment in China

York Chen 陈友忠iD TechVentures Ltd. 智基创投

Jan., 15, 2008, Ann ArborGlobal Private Equity and Emerging Markets

Univ. of Michigan

Entrepreneurship and Venture Investment in China

• China VC Market Overview, 2007 • China at the Center of Global VC Market • The Hot Market and On Going Soft-landing • From High Tech to High Growth • From USD Offshore to RMB Onshore Investment • Deal Structure in China

• Venture Opportunities in China

VC Investment Annual Amount

Source: China VC Annual Report, Jan-Nov Data, by Zero2IPO

VC Investment Industry Breakdown

Source: China VC Annual Report, Jan-Nov Data, by Zero2IPO

VC Investment Geographical Distribution

Source: China VC Annual Report, Jan-Nov Data, by Zero2IPO

VC Investment: RMB vs. USD

Source: China VC Annual Report, Jan-Nov Data, by Zero2IPO

VC Investment Stage Distribution

*Average amt. is based on deals with disclosed value.

Source: China VC Annual Report, Jan-Nov Data, by Zero2IPO

VC Investment Stage Distribution(in Deal Number)

Source: China VC Annual Report, Jan-Nov Data, by Zero2IPO

VC Investment Stage Distribution(in Amount Invested)

Source: China VC Annual Report, Jan-Nov Data, by Zero2IPO

VC Deals Exit

Source: China VC Annual Report, Jan-Nov Data, by Zero2IPO

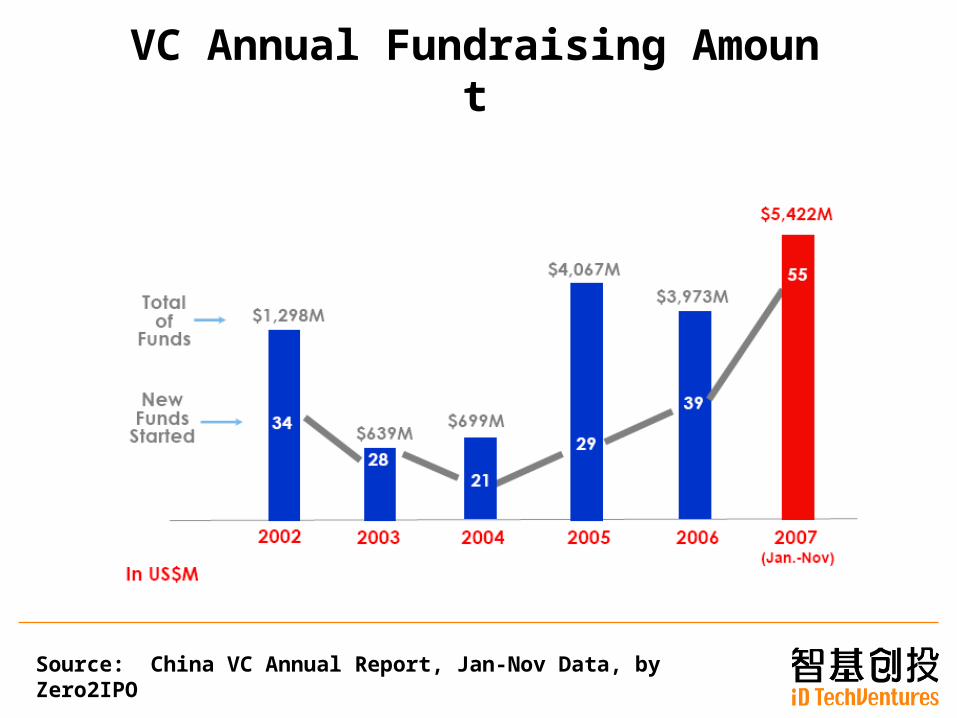

VC Annual Fundraising Amount

Source: China VC Annual Report, Jan-Nov Data, by Zero2IPO

China at the Center of Global VC Market

China at the Center of Global VC Market• China, for the first time, surged to the second spot in the global VC

market. Top four in terms of 2006 investment amount (Dr. Martin Haemmig):– USA: US$25.75 B (VentureOne data)– China: US$1.78 B (Zero2IPO data)– UK: US$1.73 B (VentureOne data)– Israel: US$1.62 B (Israel VC Association data)

• But, considering VC activity’s significance to its economy, China’s VC industry is still at an infant stage. Top four countries’ VC amount to its GDP (Dr. Mannie Liu):– Israel: about 0.5% – Europe: about 0.3 to 0.4% – USA: about 0.2%– China: about 0.067%

Foreign VC Funding Flow in China

AngelFFF

LP

GP

Start-upLP Fund

FoF

Foreign Funding

Suppliers

Foreign VCs with

Operation in China

Chinese Start-ups

With Offshore

Entities

VC: Much Internationalized Ind.At the moment, foreign VCs lead the way supplying more than 70% of VC funding in China.

• Fund raising completely from foreign LP and FoFs• Fund managed by foreign GP companies with liaison office

s in China• Fund outflow to offshore holding entities owned by Chinese

entrepreneurs• Divestment through overseas IPO and M&A• Chinese portfolio are funded by offshore money. So, VC a

ctivity is less affected by China economic cycle and macro policy.

• Among all industries, VC’s manpower comes with the highest educational and professional level, mostly foreign trained.

Note: point 5 & 6 are views of Mr. Zhao Min( 赵民 ), Chairman, Adfaith Management Consultant ( 正略钧策 ), July 12, 2006

16

Foreign VC: Go Alone or Go Thru Local Teams?

• VC is a localized operation in terms of local talents, local supporting infrastructure, local decision making, and should even local fund raising.

• Out of the driving distance and crossing the Pacific is just too tough for American counterparts. “Tourist VC” won’t work. Sand Hill Road VCs will either enhance their own local operation or park their interests with a local team.

• Two examples of shifting to partnership: – KPCB gave up own effort, to work through an

enhanced TDF team joined by SAIF’s Joe. Raised a China Fund, 360M, in April ‘07.

– Mayfield stopped its own effort in China by parking all interests in China with GSR Fund II.

17

Local VC: To Partner or Not to Partner?

• Home grown VCs, many of them grown out of hi-tech/financial groups or government entities, are emerging as key players.

• China GP teams are pondering should they outsource fund raising challenges to Sand Hill Road peers by giving up some economic interests and operational independence?

• A question to follow: will there be independently owned and managed China-rooted VCs in the long run?

China Rooted VC Brands

• CDH 鼎辉• CDH VC 鼎辉创投• SAIF 赛富• Legend 联想• New Margin 联创• Infotech 英富泰克• DT 德同创投• SBCVC 软银中国• iDT VC 智基创投

18

“Great Leap” of Mega Funding

• Ballooning of VC fund raising in China. US$4B VC fund raised each year for both ’06 and ’05. Added US$5.4B for ‘07.

• Quite a few mega VC/PE funds raised in 1H ‘07, in less than two or even only 1.5 years from previous vintage ’05 funds.

• Mega funds raised in 1H ‘07:

– TDF II (120M) to “KPCB China Fund” 360M

– Sequoia China Capital I (200M) to total 750M (Sequoia China Capital II 250M and Sequoia China Growth I 500M)

– SAIF II (643M) to SAIF III 1.1B

– CDH PE II (310M) To CDH PE III 1.6B

– IDG Accel I (290M) to IDG Accel II 550M

19

A China Miracle: Chasing for Better Return Drives Funding to China

• Sand Hill Road peers took one or two decades to reach mega funding size. For example, KPCB, founded in ‘72, had its Fund IX reached 550M in ‘99, then Fund XII of 600M in ’06.

• It’s a “China Miracle” for local VC/PE to reach mega size in just a few years. And, all these funding are endorsed and invested by reputable and leading Western LPs and FoFs. Take SAIF III. It gathered one of the most impressive LPs including endowment funds of Harvard, Princeton, Cornell and Dartmouth, CalPERS and NY State pension funds, Dupont, Common Fund, Horsley Bridge, .. (*)

• The VC/PE funds in China have really seen good financial returns in past few years. And, these foreign investors are confident about the future opportunity going forward in China.

*: Source: Andy Yan Interviewed by Zero2IPO eWeekly, May, 2007

Another China Miracle:The Booming Local Stock Market

• The foundation of “China Miracle” with huge foreign funding is the long sustaining high growth of local economy, which is the same ground for current booming stock market and high P/E in China.

• It looks scary for Shanghai Composite jumped from 1000 in 05 to 5100 in 07, with average PE stays at 50X. But, for 10 years up to 03, it stayed at 1500 level, and even dropped down to 1000 in 05. No appreciation for more than 10 years while the local economy comes with impressive double digit growth. So, with a longer time horizon, the hot market might just reflect “under value” adjustment.

• Accumulated fortune and personal saving (up to USD2.3 trillion) channeled into limited investment vehicle, such as real estates and stock market.

The Hot Market and On Going Soft-landing

China VC up to Mid-’06: Active and being Over-heating

• After ten years subdued and “Check In, No Check Out” VC environment, China VC starts to kick off a virtuous circle from 2004. Successful and active divestment brought high return to VC investors. And, in return facilitated successful fund raising for more active venture activities in China.

• With improving and potentially high returns in China, many mainstream VCs, LP funds and hightech MNCs are flocking into China.

• Keywords of China VCs changed in 04 to 06: – “It’s here, and it’s for real”.– THEN: Why China, and why now? NOW: How?– “Cautiously Optimistic”

• The market is characterized by strong supply of GP teams, LP funds and VC People

More VC Players Joining the Market

• One of the most significant development of China VC since ’04 has been the market getting world’s attention, and the flocking-in of Sand Hill Road VCs.

• More veteran VC players from Taiwan, Singapore, Israel, Korea, Japan and Europe are also setting operations in China.

• The hot environment and proven divestment track-record also invites many China focused first-time GP teams, LP funds as well as FoFs.

• Foreign VCs into China is not only seeking local direct investment opportunity, but also out of the need to support their venture activities in their home countries. Many deal flows based in the Valley will likely have China presence. In some cases, even doing the due diligence for a foreign deal might need to visit China.

Five Routes Sand Hills Rd VCs Take to Enter China

• Model A (Setting up own China fund)– Sequoia China; KPCB China

• Model B (Joint or Franchising Fund)– IDG Accel China Fund; DFJ DragonFund China

• Model C (Global GP becomes a China LP)– As a LP to a China fund to have a platform to develop China

opportunity. • Model D (Liaison offices with local professionals)

– DCM, NEA, Bessemer, Atlas, Redpoint, BlueRun, GAP, Granite, Highland, ….

• Model E (Sideline observers, ad-hoc investors)– Continue to explore the China strategy, or not yet buy-in the China

story

From original presentation “The Way We Were, China VC in 2005”Shanghai, Dec., 14th, 2005, CVCF

Global GP Becomes a China LP

• Len Baker pioneered and defined the unique model. His Sutter Hill invested 8M each into Chengwei’s fund I and II in ‘99 and ‘04 respectively, and 5M into TDF in ‘05.

• The closeness and strategic relationship between the two parties, and economic terms for US parties, are varied.

• Qiming, without an Ignition name, is more than “Ignition China”. Two VC veterans from the Seattle relocated to Shanghai bridging the HQ and China “branch” under a much solid and substantial mechanism.

• DCM – Legend Capital

• 3i - CDH

• Sierra – Gobi

• Light Speed – DT Capital

• Sutter Hill – Chengwei, (TDF)

• Greylock; NEA – N. Light

• Worldview - Infotech

• Mayfield - GSR

• Ignition - Qiming

Much Funding Chasing Quality Deals

• Considering the fact that rather big portion of funding is focusing on local value add service segments (internet, web2.0, MVAS, broadband, ….), the issue of fund’s over-supply is sector specific.

• And, many funds, especially first-time funds raised in 2005, have the pressure to “pour” out investment quickly. Investment pace is quicken than what it should be.

• While funding supply multiplied, quality deal flows not increased at the same pace. Supply-demand mechanism at work. Valuation jacks up. Start-ups get much bigger funding than originally planned.

• Illustrating cases: Blog China (Bokee) and BlogCN.

LP Funds’ Larger Allocation for Asia- Case Study on Horsley Bridge International Funds

Fund Year Territory Coverage

HB Int’l I 1998 Europe/Israel

HB Int’l II

(Actual allocation: 15%, 4 Asia funds)

2000 Europe/Israel

Asia (<25%)

HB Int’l III(Actual allocation: 30%, including 5 China funds)

2004 Europe/Israel

Asia (No Limit)

Source: Mr. Gary Bridge presentation on Zero2IPO Conference

Palo Alto, April 25, 2006

More Professionals Jumping On

Though with a short history in China, VC’s virtuous circle is in the forming. Successful VC-backed entrepreneurs are turning around and becoming:

• Serial entrepreneurs

• GP venture capitalists

• LP investors

• Angel investors

Entrepreneur Turns VC• GSR James Ding (Asiainfo)• Sequoia Neil Shen (Ctrip)• DCM Hurst Lin (Sina)• BlueRidge Justin Tang (eLong)• Northern Feng Deng; Yan Ke Li

ght (Netscreen)• CyberNaut Zhu Ming (WebEx)• CBC Capital Edward Tian (CNC)• TPG Sing Wang (Tom)• Matrix Bo Shao (EachNet)

Reshuffling of VC Professionals• Like in other industries, old playe

rs are supplying talents to new comers. New GPs, by head-hunting, to jump-start operation in the rather competitive environment.

• VC is a people business. Deal flows usually go with the people into new funds.

• VC job opportunity opening up, and a war of retaining and recruiting good people. HR cost lifts up.

• For newly build-up VC teams, the “break-in” of team members will be a challenge to go through.

• Sequoia China:– Zhang Fan (DFJ)– Zhou Qui (Legend)– Steven Ji (Walden)

• CDH Ventures:– Wang Gongquan (IDG)– Wang Shu (IDG)– Huang Yan (Intel)– Vivian Chen (Walden)

• Granite: – Foo Jixun (DFJ)– Jenny Lee (Jafco)

• Qiming:– Duane Kuang (Intel)– Ed Zhou (Cisco)

• KPCB:– Joe Zhou (SAIF)– Tina, David, Forrest (TDF)

Events in ‘06 Led to Softened and Reserved VC Environment

• VCs’ investment during the over-heating period are coming to a “Reality Check”. A time to review and to see if anything need to be adjusted.

• Government regulatory measures on cross-border transaction are putting negative implications on overseas VC investment in China.

• MVAS, provides substantial revenue source to China internet companies, experiences depressed environment due to MII and operators’ discipline measures since June ‘06. And, government agencies’ crackdown on TV Shopping, music, game and UGC video.

• The momentum for “China Concept” IPO has not been carried on from 05 to 06. Latest stock performance of those listed Chinese companies are also not encouraging.

More Cautious Investment Pace

After mid-’06, China VCs proactively do self adjustment in areas of:– Take more reserved and cautious steps

toward new investment. Slow down investment pace.

– Not to chase around deals. Tender term sheets carefully.

– Deals’ valuation coming down. Investment terms shifting to be more favorable to VCs.

– Avoid Web2.0. Cautious on MVAS, and other deals without sensible revenue projection.

Diversifying Investment Focus• Pure Web2.0 projects were difficulty to get VC attention and funding. • MVAS will take time to recover. Maybe need to wait till 3G launch for

a new start.• VCs are still keen and willing to bet on future killer app for internet and

broadband applications. IPTV opportunity is still a few years away.• Many VCs start to pay attention to non-Internet, or even non-TMT, sec

tors. On top of IT hardware opportunities (IC design, Semicon, key component, module, …), VCs interests have extending to:– Medical devices and health care services,– Retailing, franchising and branding for consumer services and goo

ds– Alternative energy and green tech– Manufacturing, logistics, Mining, …. – Outsourcing services

“Soft-landing” for a Healthy Adjustment

• On the macro, as long as China economy continues to open up and with healthy growth, VC activities here will continue to be active and promising. We continue to see foreign VCs and LPs interests toward China keeping high.

• In 2000, we experienced a VC “Hard-landing”, reflecting passively to the dotcom corruption. Painfully taking huge casualties, and it took 3 years to recover.

• Since mid-’06, we are taking the counter-measure actions into our own hands by proactively do the self-adjustment before the situation running out of control. The on-going soft-landing since mid 06 illustrates maturity of China VC industry.

From High Tech to High Growth

TMT Investment (%) Decreases

Healthcare2.5%Other

Hi-tech9.4%

Traditional13.0%

Services13.3%

Unknown1.4%

IT60.3%

2005 VC Investment: USD1.06B 2007 VC Investment: USD3.18B

Source: Zero2IPO Annual China VC Data

High Growth: New Cluster for VC Inv.

• Observation of China stock markets:– China stock markets in Shanghai and Shenzhen are

mainly servicing government owned entities. Most of 1500 listed companies are of government conglomerates.

– Stock market re-engineering has being on for only two years. Less than 200 listed are of private SME.

– As a result, quite some good and long operating traditional companies are still kept private. These companies are usually being listed in the West.

• Projecting China economy’s healthy growth into the future, these high growth companies are growing to become a promising cluster, and good target for VC/PE investment.

37

Diversifying of VC/PE Operation

Stage

Deal Generation

IPO

Location

Entrepreneurs

Deal Structure

Sector

Early/Expansion

Own Screening

Red Chips

Coastal East

Returnees

Offshore USD

High Tech (TMT)

From

Late/Pre-IPO

Thru Partnership

A & H Shares

West & Inland

Locals

Onshore RMB

High Growth

Expand to

From High Tech to High Growth• Crowded, overheating and competitive TMT sectors putti

ng constraints on return potential.• And, not like in the mature economies, high return

opportunity in China might not necessarily be powered by high tech. Still quite lots of traditional sectors not being well served. And each sector, no matter how narrowly defined, present high growth and high margin potential, and as a result high return opportunity for investment.

• Zero2IPO data also shows that TMT sectors dropped from some 70% for past several years to below 50% in 2007.

• Successful IPOs since 06 of New Oriental, Home-Inns, Belle Shoes, Weiqian Lamen, …. Illustrate the high growth sector opportunities.

Consumer Power in China(a flavor of high growth investment in China)

• With fast growing GDP and urbanization, the middle-class is expanding quickly as a powerful consumer group. Products and services addressing their consumer needs gradually become an important target of VC/PE investment.

• Cases in point:– Food: Mengniu, Shuanghui, Huiyuan, Youge– Restaurants: Weiqian, Chamate, Zhenggongfu, Xiaofeiyang, Littl

e Swan, …– Education: New Oriental, ChinaEDU, 100e, …– Medical services: CiJi, AiKang, Jiamei, ….– Hotels: Home-Inns, Mandarin Court, 168/268, ….

40

From USD Offshore to RMB Onshore Investment

China’s Foreign VC Operation- Funding & Divest. Stay Offshore ( 二头在外 )

Fund Raising & Set up Fund

Deal Flow Screen

& Investment

Portfolio Management

Divestment &Financial Returnto LPs

The Changing Tides• The shifting tides are mainly due to the legal and regulat

ory changes happening in past three years. Through SAFE circulars #75 and #106, MOC #10 and other administrative measures, Chinese government tried to discourage local deals to be restructuring into offshore holding for USD funding and overseas listing.

• As a result, offshore restructuring becomes much time consuming and challenge, if not impossible.

• At the same time, the local VC/PE environment is greatly improved. The local IPO, legal framework and LP funding sources are getting better.

• It might take years for RMB onshore investment to become the mainstream of VC/PE activities in China. But, an emerging trend needs to be watched closely.

Domestic, 160M, 15%

Foreign, 740M, 70%

Sino-foreign JV

175M, 16.5%

RMB Inv Significance Only be Seen from 08 Onward

By Number of Deals By Amount Invested (US$M)

2005 VC Investment: USD1.06B 2007 VC Investment: USD3.18B

Source: Zero2IPO Annual China VC Data

LPLP

USDUSDFundFund

LPLP

RMBRMBFundFund

Project Project

123

ProjectProject ProjectProject ProjectProject

Onshore Offshore

Foreign LPs & Funds in China Projects(Current Status)

(Offshore Holding)

3a

Route 1: invest into China projects’ offshore holding entities, mostly in CaymanRoute 2: Direct cross border investment and turn a China entity into a JVRoute 3a & 3: to sponsor and initiate a local registered RMB fund.

Direct Investment into Chinese Co Using Existing Offshore LP Fund

Offshore

Onshore

Local ShareholdersLocal Shareholders

Local Co., Ltd.Local Co., Ltd.

LP FundLP Fund

SPVSPV

Foreign Invested Co. Ltd.Foreign Invested Co. Ltd.

Local ShareholdersLocal Shareholders

LP FundLP Fund

SPVSPV

A Share ListedA Share Listed

Local ShareholdersLocal Shareholders PublicPublic

(Route 2)

Source : Mr. D.C. Lee, SBI Crosby, Jan., 17th, 2007, Shenzhen

46

Onshore Offshore

GPGP

Fund Mgmt

Fund Mgmt

USD Fund

LP

LP 2

LP 3

LP 1

A Foreign Fund Sponsors a RMB Fund

RMB Fund

(Route 3a)

47

Overseas LPs’ Role• Conventional LP practice (long term, not interfering GP

operation, management fee/carried arrangement) prevailing in the West is not yet popular in China. Local LP funding supply is still at shortage.

• At the moment, government owned/affiliated funds could be a good source for RMB funding. Many government agencies (ministries, banks, provinces, municipalities, hi-tech parks...) set up matching funds ( 引导基金 ) to support RMB fund formation.

• With the improving of legal, forex and tax issues, overseas LPs and FoFs, in the mid-long terms, will continue to play a key role in supplying funding into China’s VC/PE industry.

Get Government LP Funding?- A Debatable Issue• Pro:

- To enlarge the fund size for economies of scale. And, bigger fund size to be eligible for registering as “non-institution” entity (minimum USD10M)

- Government endorsement for fund set-up as well as better tax terms, SAFE approval, project’s R&D subsidy, IPO opportunity, deal flow sourcing, …

- Avoid perception of a foreign fund without local root.

• Con:- Local LP likes to involve in fund management. Put negative i

mpact to a GP’s independence and decision making process.- The fund and its GP will need to register in a particular city, a

nd with constraints on investment’s location, sectors, … - Not easy to bring more than one government LP to invest into

a fund.

Government Funding as LP• Model I (LP & GP)

On top of LP funding, government entities will also be shareholder to GP, which turns to be a JV. Involved formally and directly in VC management and decision making.

• Model II (Involve in Decision Making)Government entities won’t join GP set up and operation. But, will join Investment Committee and usually have a veto right

• Model III (More as a Conventional LP)Not involved in decision making and not put limitation on where to invest. But, will ask the GP and the fund to be registered in the local.

USDFund

RMBJV

Fund

123

RMBLocalFund

4LPLP LPLP

USDUSDFundFund

RMBRMBJVJV

FundFund

RMBRMBLocalLocalFundFund

ProjectProject ProjectProject ProjectProject ProjectProject

Onshore Offshore

Foreign LPs & Funds in China Projects(Future Scenario)

(Offshore holding)

3a

3b

Route 3b: foreign LP’s direct investment into local RMB fundsRoute 4: local LP’s investment into foreign funds or FoFs

Deal Structure in China

Distinct Foreign and Local Operation• Distinction of USD offshore holding investment and

RMB local entity investment is a particular phenomena in China.

• Foreign VCs: use offshore USD fund to invest into China deals’ offshore holding entities with all equity activities happening outside of Chinese jurisdiction. Local VCs: use RMB to invest into deals’ PRC entities and seek local divestment.

• Distinct Foreign and Local VC Groups- Foreign VC contributed more than 70% of funding. - For many years, the encouraging trend of profitable

exits is only applicable to foreign VCs. Local VCs’ profitable divestment is only happening since 07.

Offshore Holding a Preferred Structure(up to 07, and changing)

Offshore holding arrangement is a preferred structure for Chinese entrepreneurs and VCs as it provides a feasible and practical route for funding, divestment and all equity events. Its advantage and attraction to Chinese entrepreneurs and VC communities:- Go away from laws and regulations in China. Many

of them are not friendly to venture activities, including lack of preferred shares, stock options limitation, double tax, …

- Bypassing capital account control on foreign exchange

- More flexible and usually profitable divestment options by overseas IPO, M&A or trade sales.

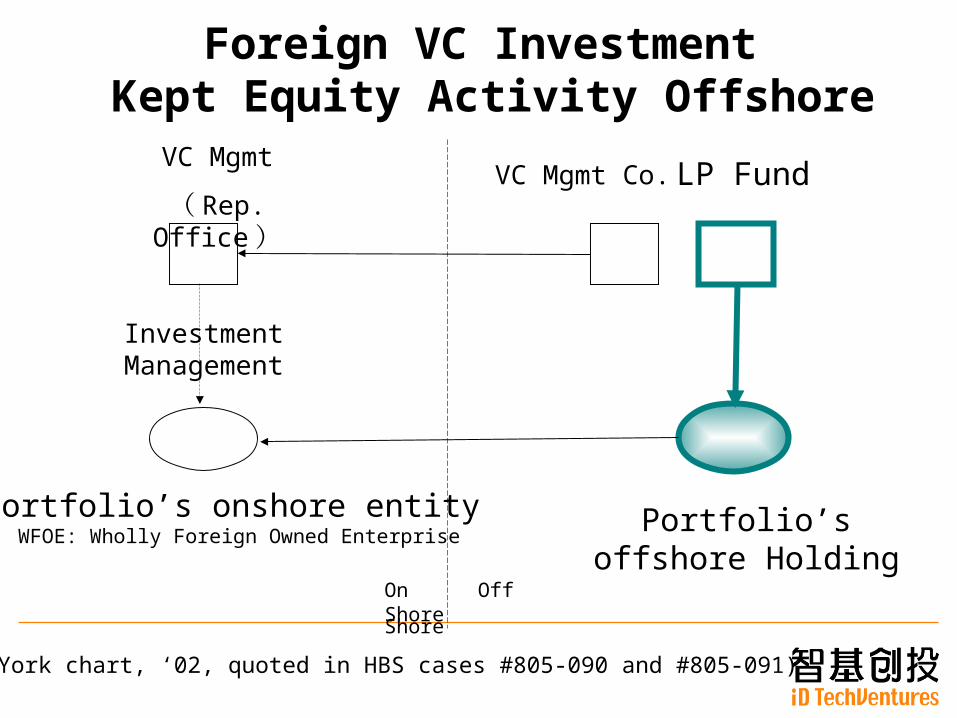

Foreign VC Investment Kept Equity Activity Offshore

Investment Managemen

t

VC Mgmt

( Rep. Office )

Portfolio’s onshore entity Portfolio’s offshore Holding

VC Mgmt Co.

On OffShore Shore

WFOE: Wholly Foreign Owned Enterprise

LP Fund

(York chart, ‘02, quoted in HBS cases #805-090 and #805-091)

Special PRC Vehicle for Projects Off-limit to Foreign Co.

Offshore Holding

WFOE

VC Mgmt Co.

(Rep. Office)VC Mgmt Co. LP Fund

InvestmentManagement

A SPV Co.

Invest

On Off

Shore Shore(Licensing & revenue

booking vehicle)

(York chart, ’02, quoted in HBS cases #805-090 and #805-091)

Restructuring into Offshore Holdings• Offshore restructuring involves the following steps:

- The Chinese founders set up an offshore holding company in Cayman Island or BVI with the shareholding structure and management control mirroring those of their local company in China.

- With kind of swap scheme, transferring the equity they hold in the Chinese local company to the offshore holding. This will typically convert the local company into a WFOE (Wholly Foreign Owned Enterprise).

• The offshore holding company will then be the vehicle seeking VC investment, future funding as well as for listing or be merged. All equity events happening offshore. Companies’ funding and IPO proceeds will be kept offshore, and remit into China as and when operation required. Chinese founders’ assets, rights and proceeds stays offshore.

RMB Funding as an Optional Source• The current offshore entities set up, getting USD investm

ent and looking for offshore market listing is getting tougher and might not be a viable option in for longer term.

• Eventually, the VC/PE industry in China will do local RMB fund raising, local RMB investment into local entities, and have the portfolio divested thru local IPO or M&A. So, to complete the four major activities of a VC cycle (funding, investing, value add to portfolio, and divestment) all onshore.

• VC investors as well as entrepreneurs should take note to watch the emerging mega shift closely, and explore RMB fund initiative seriously. 2007 was the year kicking off a long transition toward the mega shift.

Venture Opportunities in China

- The “Three Represents”

Conceptualized and first presented in Zero2IPO China VC Conference Dec. 16, 2004; Beijing

(Part I)

China: World Market & World Factory

Product & services to serve the domestic market

• Huge & growing domestic market

• WTO and opening up• Stable inv/buz environment• Engine for global economy

growth• An integral part of MNC’s

globalization

Manufacture, R&D, … to serve the world

• Abundant engineers, skillful & diligent labor

• Local talents fostered by MNC

• Management fr abroad & HK/TW

• Private sector is catching up• MNCs’ Asian HQs and R&D

center• Fr “Made in China” to “Create

in China”

Emulating the Business Model Across the Pacific

• China is a huge market. Any business model, even focusing on a very niche market, it could be successful.

• Even just emulating a well proven and successful business model from the States is feasible.

• US companies will need to focus on huge and challenging local market first. Even for going abroad, it will go to Europe and Japan first. A golden time window for China start up to “copy” and grow.

• The market leader in a particular segment may go public; the 2nd and 3rd could be potential M&A targets for MNC in the same sector who want to jump starts or complement its China development. (refer to next slide)

Potential Exits for China start-ups

Lead players may go IPO

• Ctrip 、 eLong• 51Job• Shanda 、 NetEase 、 The9

World Perfect, Jinshan, ..• Dangdang (on IPO route)• Baidu 、 Huicong• Linktone 、 Tom Online

KongZhong 、 HurrayTencents

Others may be acquired

ChinaHR (40% by Monster)17173 、 Digital Red

Joyo (by Amazon)3721 (by Yahoo)MemeStar, Power Genius,Treasure Base, Goodfeel,Crillion…(several scores)

Huge local market represents the opportunities in consumer products

and services• China has a huge local market. A segment leader could make a

powerful player no matter how narrow the vertical market is defined. • The statistics we are familiar with, such as 550M mobile users, 137M

Internet users, 91M broadband users and 5.5M college graduates every year…., could transfer into huge business opportunity.

• Consumer market is much promising than enterprise market.• Consumer products have big sales opportunity, while consumer

services have maximum capital efficiency.• Opportunity for entrepreneurs and investors :

- Local value add services (MVAS, broadband, internet, Web2.0,…)

- Media, advertising, digital contents, …- Other products and services concerning daily life, health and

amusement

World factory status represents the opportunities in ‘import substitution’

• China has been the world factory, a powerhouse to churn out products sold all over the world. However, quite some key components are imported or supplied by foreign players. So, ‘import substitution’ provides opportunities for local entrepreneurs.

• It’s not necessary about leading technology. KSF are on mature technology, large volume, with longer term demand and higher price elasticity.

• Core competences: global standard product design (technology), local manufacturing (cost) and good local customer relationship (service)

• Opportunities for entrepreneurs and investors:

1. IC design

2. Key components design and manufacturing

Abundant cost effective resources represents the opportunities in outsourcing services

• With China’s abundant engineer, cheap labor, cost effective operation, and stable business environment, it could provide outsourcing services to global market.

• Start ups should leverage China-based advantages to provide value-added services to enhance competence and competitiveness.

• Core competence: international standard operation, overseas marketing activities (order taking) and the scaling up/down ability

• Opportunities for entrepreneurs and investors:- Hardware OEM/ODM services- SW outsourcing, BPO and Call Center service- IC design and outsourcing service- Digital content creation, …

Venture Deals with Chinese Characteristics

- China Deals’ “Three Represents”

Conceptualized and first presented in China VC Half-Year Conference, Zero2IPOBeijing, Jul. 8th, 2002

(Part II)

Know-how and Know-who

• China projects requires both Know-how and know-who.• “Returnees” (Sea Turtle 海归 /龟 ) refers to managers and

entrepreneurs coming back from abroad. My new definition :- ‘Ocean Turtle’ ( 大洋龟 ) : Conventional definition of returnees, with

oversea education and MNC exposure. But being remote from home country for long.

- ‘Strait Turtle’ ( 海峡龟 ) : Professionals from Taiwan, HK & Singapore. With MNC experience, global views and familiar with China Market

- ‘River Turtle’ ( 江河龟 ) : Local management of MNC operation in China. Familiar with both international operation and local market

“If Ebay is the shark in the Pacific, Alibaba could be the crocodile in the Yangtze River.”

– Jack Ma, Alibaba

Represents Those with Practical Technology Application

• Advanced technologies helps to build up entry barriers & develop the business successfully. But, in China, it’s “Technology Application, NOT Technology Creation”.

• Leading edge technology and critical innovation breakthrough are of global competition. It will be tough and impractical to find locally developed technology, which could stand for global competition. However, service, integration and localized technology application are of local competition.

• A practical approach: To see how to apply those well proven advanced global technology and business model into China’s local market.

• Good role models of “From SI to Products” (by Asiainfo, Huawei, …. ), TMT Model (Trading-Manufacturing-Technology, by Legend/Lenovo) and OEM-OBM Model (Acer).

Represents Those Servicing the Mega Local Market

• China has a huge local market to be served. A start-up could be highly successful even by only servicing the local market.

• “Import Substitution” business has also big potential. Take IC design. It will be much feasible for local start ups to target at ICs with huge quantity, stable demand, price sensitive and trailing edge tech. Those will be highly demanded by the “World’s Factory” by replacing imported components.

• Channel and logistics has high value as China market is vast, diversified and segmented.

• Need close cooperation and complementary strength of returnees and locally grown-up talents; Emphasize on both marketing (know-who) & technology (know-how).

Represents Those with Highest Execution Power

• Implementation counts, NOT Presentation. Entrepreneurs need to focus fully on operation on the ground.

• Key stumbling points: Time to Product, Time to Market, Time to Revenue, & Time to Profit

• “Alumni” founding team for founding members being worked for several years together as a team in MNCs is a big plus. Founding members will need times to “break-in” and be seasoned in order to exercise team power.

• Exit is the cardinal principle. Only those could be successfully

exited are good projects.

China: a Risky Market for Foreigners China is a tough market for foreign players. Business initiative needs “ 摸着石头过河” (a Chinese proverb: holding the rock to cross the river). Familiarize with local regulations, market admittance system and industry practice to avoid operational and legal risks. 摸着石头过河

危机会

Thank You !

www.idtvc.com

VC Blog http://yorkchen.fastart.cn雁行中国 http://blog.sina.com.cn/yanxing