environmental and social reporting after incidents web viewenvironmental and social reporting after...

TRANSCRIPT

Environmental and Social Reporting After IncidentsThe effect of the Deepwater Horizon oil spill

Andrew Maarschalkerweerd01-03-2012

Student nr: 315863amSupervisor: Dr. K.E.H. MaasErasmus University RotterdamErasmus School of EconomicsMaster Thesis Accounting, Auditing and Control

Acknowledgements

This Master thesis is the conclusion of the Master degree Accounting, Auditing and Control at Erasmus University Rotterdam. By means of this acknowledgements page I would like to thank those who assisted me either personally or academically.

I would like to thank both supervisors that assisted me in the writing process: From the Erasmus School of Economics, Dr. Karen Maas; From PwC, Maarten Hoornweg RA. Both supervisors gave me good feedback and ideas that I could use in my master thesis. I also would like to thank PwC Rotterdam for offering me a place to write my thesis and a chance to get an insight into what they do.

I also would like to thank Dr. C.D. Knoops, who supervised me in the first part of the writing process during the Seminar Advanced Financial Accounting. I also would like to thank my fellow students for giving feedback on my paper during this seminar.

I would like to thank my family and friends for supporting me during my studies.

A special thanks to Professor Colbert, one of my lecturers during my exchange at Trinity College Dublin, who inspired me to continue my studies in the field of accountancy.

Rotterdam, 01-03-2012Andrew Maarschalkerweerd

1

Executive Summary

In the last couple of decades there has been a large increase in the voluntary disclosure of environmental information by companies. In this thesis I specifically look at these disclosures surrounding incidents and how companies change their disclosures. The main question that is posed in this thesis is “What are the reasons for voluntary disclosure and how do companies respond to certain incidents?”. This main question is then split up into sub-questions and these are discussed in several chapters.

Firstly the theoretical fundament of this thesis is set out. Several frameworks used for voluntary disclosure are discussed. These help companies to disclose information in a structured manner. This helps several stakeholders by making the information more comparable. Also theories are discussed that can explain voluntary disclosures by companies, of which legitimacy theory and media agenda setting theory are the most important for the study conducted later.

Legitimacy theory predicts that companies, when they are threatened to breach their ‘social contract’ with society, will disclose more information. Patten (1992) takes this theory even further and tests whether companies in the same industry as a threatened company, will increase their disclosures. This is specifically done for companies in the oil sector after the Exxon Valdez oil spill relating to their environmental disclosures. He finds that companies, although unrelated in a business sense with Exxon, increase their disclosures. Also companies that are larger (measured in log revenues) show a larger increase in their scores than smaller companies. Companies that are partly responsible for the slow clean-up response also showed a larger increase in their scores.Media agenda setting theory predicts that media convey the concerns of the public but also influence the public opinion on certain topics, especially if they are far away from the public. Therefore managers are also influenced by topics that are discussed in the media.

I replicate Patten’s study by examining the disclosures of companies in the oil sector after the BP oil spill in the Gulf of Mexico, to see whether the relation still holds. I quantify the disclosures by means of an environmental disclosure index model as developed in Aerts and Cormier (2009) for the years 2009 and 2010 (before and after the incident). Firstly, I test the hypothesis that the disclosures significantly increase and secondly, whether there is a difference when companies are larger and whether there is a difference for US companies opposed to non-US companies.I find that companies still disclose significantly more after an incident, even if they are not responsible for the incident (the only relation being that they operate in the same environmental sensitive industry). When this information is split-up into economic (reactive, related to litigation) disclosures and social (soft claims) I find that both are significant.I cannot find any evidence that larger companies also show a larger increase in the scores of both years, as Patten found in his study. This might be explained by how companies deal with environmental disclosures today compared with the end of the 1980’s or beginning of the 1990’s.I cannot find any evidence that US companies increase their disclosure to a larger extent than non-US companies. A reason for this could be that all companies are large listed companies in the US and that their historic location has become irrelevant.

2

3

Table of Contents

Acknowledgements.................................................................................................................................1Executive Summary................................................................................................................................2Table of Contents....................................................................................................................................31. Introduction........................................................................................................................................5

1.1 Topic introduction..........................................................................................................................51.2 Topic and research question...........................................................................................................51.3 Structure..........................................................................................................................................6

2. Theories and methods behind this research.....................................................................................82.1 Introduction....................................................................................................................................82.2 Social and environmental disclosures.............................................................................................82.3 The Global Reporting Initiative....................................................................................................11

2.3.1 Reporting principles for defining content..............................................................................122.3.2 Reporting principles for defining quality..............................................................................122.3.3 Reporting guidance for boundary setting..............................................................................122.3.4 Standard disclosure................................................................................................................132.3.5 Oil & gas sector supplement..................................................................................................142.3.6 The future..............................................................................................................................14

2.4 Other standards.............................................................................................................................14

2.4.1 AccountAbility framework....................................................................................................142.4.2 ISO 14001..............................................................................................................................152.4.3 ISO 26000..............................................................................................................................15

2.5 Theories........................................................................................................................................15

2.5.1 Political economy theories.....................................................................................................152.5.2 Media agenda setting theory..................................................................................................172.5.3 Voluntary disclosure theory...................................................................................................17

2.6 Models..........................................................................................................................................18

2.6.1 Measuring the quality of voluntary disclosures.....................................................................182.6.2 Limitations.............................................................................................................................18

2.7 Research in relation to the theories...............................................................................................192.8 Conclusion....................................................................................................................................19

3. Literature review..............................................................................................................................213.1 Introduction..................................................................................................................................213.2 General literature..........................................................................................................................21

3.2.1 Capital market reactions........................................................................................................213.2.2 Characteristics of firms and countries...................................................................................223.2.3 Mandatory reporting..............................................................................................................233.2.4 Different disclosures..............................................................................................................23

3.3 Specific incidents..........................................................................................................................243.4 Environmental disclosure index models.......................................................................................27

3.4.1 Financial disclosures..............................................................................................................273.4.2 Environmental disclosures.....................................................................................................273.4.3 Additional factors: litigation and monetary and non-monetary information.........................30

4

3.4.4 Model for this study...............................................................................................................30

3.5 Conclusion....................................................................................................................................31

4. The BP oil spill..................................................................................................................................324.1 Introduction..................................................................................................................................324.2 An overview.................................................................................................................................324.3 Responsibility...............................................................................................................................344.4 Conclusion....................................................................................................................................34

5. Hypotheses development and research design...............................................................................365.1 Introduction..................................................................................................................................365.2 Hypotheses....................................................................................................................................365.3 Research and sample.....................................................................................................................375.4 Methodology.................................................................................................................................385.5 Conclusion....................................................................................................................................38

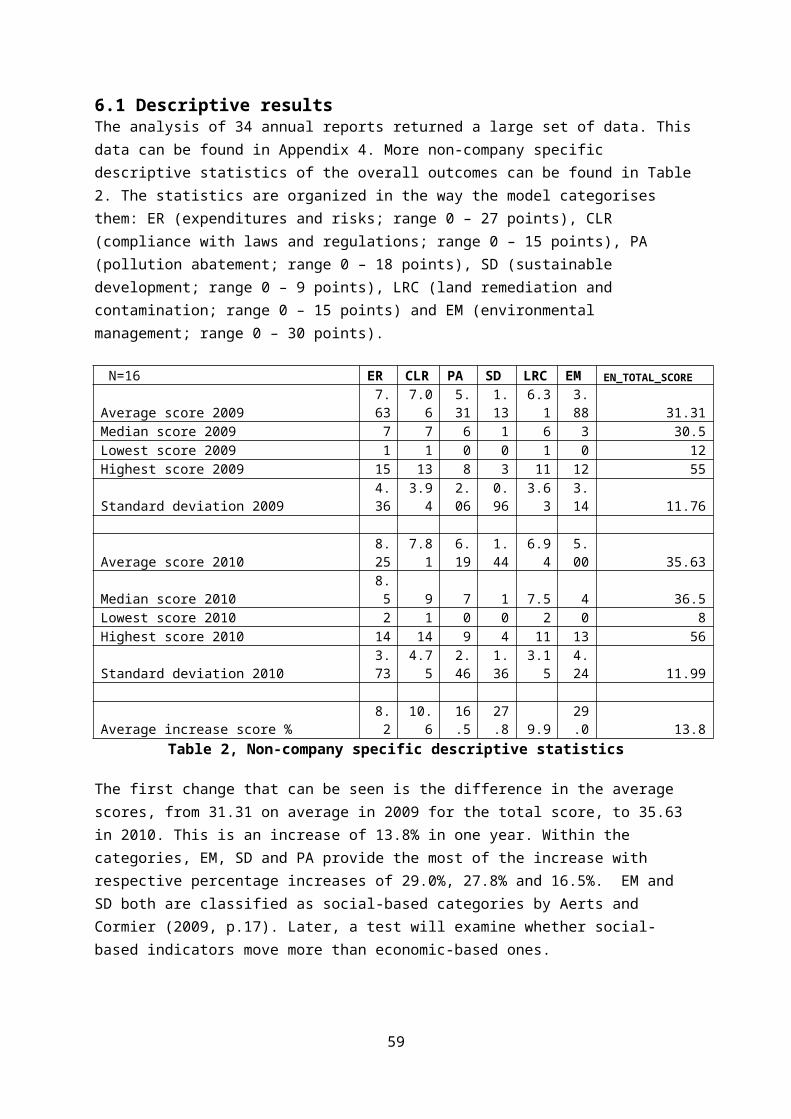

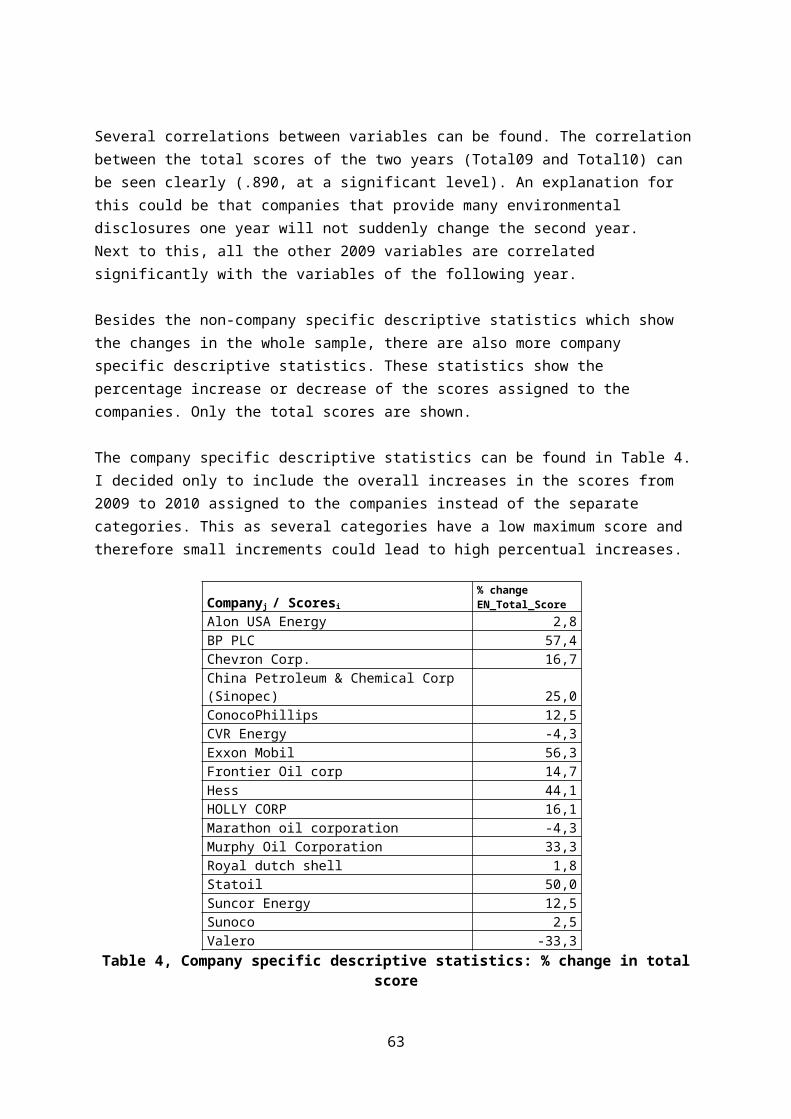

6. Results and analysis..........................................................................................................................396.1 Descriptive results........................................................................................................................396.2 Statistical results...........................................................................................................................43

7. Conclusion.........................................................................................................................................497.1 Summary and findings..................................................................................................................497.2 Limitations and suggestions for future research...........................................................................517.3 Generalisability.............................................................................................................................52

8. Bibliography......................................................................................................................................53Appendix 1.............................................................................................................................................56Appendix 2.............................................................................................................................................60Appendix 3.............................................................................................................................................61Appendix 4.............................................................................................................................................62Appendix 5.............................................................................................................................................63

5

1. Introduction

1.1 Topic introductionCompanies have been present for a very long time. A main facet is reporting on the company performance. Companies engage in this reporting to inform parties that have provided them the resources or chance to come to a certain performance. The focus of this reporting process used to be relatively limited: Most of the attention of the reporting process was on showing how well the company performed financially, while other (non-financial) factors were often omitted, although these factors are often very important to those affected. In the last decades a change has occurred in this reporting process. A change that has affected how companies and other entities report their performance to the people affected (also known as stakeholders). More and more, the focus of the reporting process has shifted away from only financial reporting to a broader form of reporting. This form of reporting would generally include how the company interacts with society as whole and other stakeholders instead of only internal stakeholders such as employees, lenders and shareholders. Issues such as the environment and the usage of labour in developing countries are topics that increasingly can be found in disclosures of companies.

The main article of reference within this thesis will be Patten (1992). Patten discusses the change in disclosures after an incident in the oil sector. It was found that companies increased their disclosures significantly after the Exxon Valdez oil spill. This did not only hold for Exxon, but for companies throughout the industry.Approximately twenty years later we will try to assess whether this relation still holds in a world where additional disclosure is becoming common. This will be done by replicating Patten’s study but with an updated model and a new incident: The BP oil spill in the Gulf of Mexico in 2010.

1.2 Topic and research questionThis thesis will look into the disclosures by companies and their place with respect to a broader set of stakeholders. Several theories that can explain why companies voluntarily disclose information are discussed. Companies are more and more making additional disclosures, although scholars still dispute why a company would do so. Next to that, I will investigate the current literature on how companies deal with their disclosures around incidents that might affect them. This thesis will be structured into several chapters and in these chapters, each (sub)-question will be answered. The main question is: What are the reasons for voluntary disclosure and how do companies respond to certain incidents?The sub questions to be answered in the separate sections are:

- What are the theories behind voluntary disclosure?- What does the literature say on voluntary disclosure and more specific in response to

incidents?- What went wrong at the time of the BP oil spill?- How is this research on environmental disclosure at the time of the BP oil spill

conducted?- Are there any changes in the environmental disclosures of oil companies since the BP oil

spill?

6

This thesis gives a clear insight to anyone who wants to investigate voluntary disclosure practice. Next to that, the field of accountancy can see it as an addition to the increasing literature on voluntary disclosure around incidents. In general voluntary disclosure has increased; therefore it might be relevant to see whether incidents still influence a company’s reporting behaviour.

1.3 StructureThe structure of this thesis is as follows: in the second chapter, theories and methods of assessing the voluntary disclosure process will be discussed.First a general assessment will be made of voluntary social and environmental disclosure. When did it start? This is further explained by means of a four step framework.Also the Global Reporting Initiative will be discussed. The GRI is one of the first real frameworks that gives guidance to entities on how to report on their non-financial performance. In this section the guidelines of the framework will be discussed. Next to the GRI, other frameworks are also reviewed

The first theories that will be discussed are: legitimacy theory, stakeholder theory and institutional theory: Every theory explains a different way in which companies respond to the stakeholders around them. These three theories are embedded into the so called ‘Political economy theory’ (Gray, Owen and Adams, 1996) that states that politics, economics and society cannot be seen separate from each other but have to be seen as overlapping concepts that will influence each other when one of the three factors is changed. Therefore they should not be seen as competing but as complementary explanations. Next to these theories (that all relate to the Political economy theory), the media agenda setting theory will also be discussed briefly. This theory credits the media for bringing up many issues that are subsequently taken over by companies as important issues.

In the last part the attention shifts to how one can examine environmental disclosures. This subject is still at this moment open to debate since most of the social and environmental disclosures are all qualitative instead of quantitative. This brings an extra difficulty to the research of the subject, as some text cannot be compared with others. Over the last thirty to forty years, academics came up with measures to solve this problem and by that, have made voluntary disclosures more comparable to each other: Some methods just count the number of pages or sentences in which a company discloses their policies, while others are more sophisticated.

In the third chapter of this thesis, the current literature in the field of voluntary disclosures is discussed. Why do companies disclose voluntarily? Do they benefit from this and are there contradicting explanations for this behaviour?

The first part provides a general overview of the literature that relates to voluntary disclosures, environmental reporting and CSR (Corporate Social Responsibility) reporting. This is done by means of several sub-chapters.

Next to the general literature in the field of voluntary disclosure, an overview is presented of a more specific field. The literature on voluntary disclosure around the occurrence of incidents is looked at. One of the first scholars to study this field was Patten (1992). He examined the effect that the Exxon Valdez oil disaster had on the voluntary disclosure that the oil sector provided. He did not take Exxon into account but still he found a significant increase in the disclosure of companies in the oil sector after the incident happened. An explanation is sought for why this happens and why companies have

7

to do this. Even companies that are unrelated in a business sense to Exxon, were found to increase their disclosure. This was a major finding as a narrow economic view predicts that every company is responsible for its own mistakes and that others will not have to alter their behaviour.It is found that many previous studies used models that were derived from one of the first environmental disclosure index models from Wiseman (1982).

In the fourth chapter an overview is presented on the Deepwater Horizon oil spill in the Gulf of Mexico. Next to this, a separate paragraph looks at who could be held responsible for the oil spill.

In the fifth section of this thesis the research that will be conducted is introduced. The hypotheses are presented on the change in voluntary disclosure after incidents. The research design and methods will be presented.

In the sixth chapter the results and analysis are presented. Firstly, the descriptive statistics from the sample are given and discussed. After this, the results and outcomes of this study are presented and discussed.

In the seventh chapter this thesis is concluded. This is done by giving an overview of the chapters, the outcomes of the study and listing the limitations of the study. Some suggestions for future research will be given and the contribution of this study will be discussed.

8

2. Theories and methods behind this research

2.1 IntroductionIn this section of this thesis, the underlying theories of social and environmental described. Over the last decades some theories have been defined, and they have in common that they try to explain why companies provide voluntary disclosures on these topics.

In the second paragraph, social and environmental reporting is reviewed. The history of the process will be discussed and then this is examined by the why-who-for what-how framework set out by Deegan and Unerman (2006, pp.309-365). In the third paragraph the Global Reporting Initiative will be discussed. This is a way of reporting for companies: Not only on financial aspects, but also on environmental and social aspects.In the fourth paragraph a brief overview is given of other frameworks used in environmental reporting. In the fifth section, the theories that relate to voluntary disclosures are discussed. The theories described are: legitimacy theory, stakeholder theory, institutional theory and media agenda setting theory. The methods that are used when studying disclosures will also be discussed. Several options exist, varying from subjective to semi-objective.

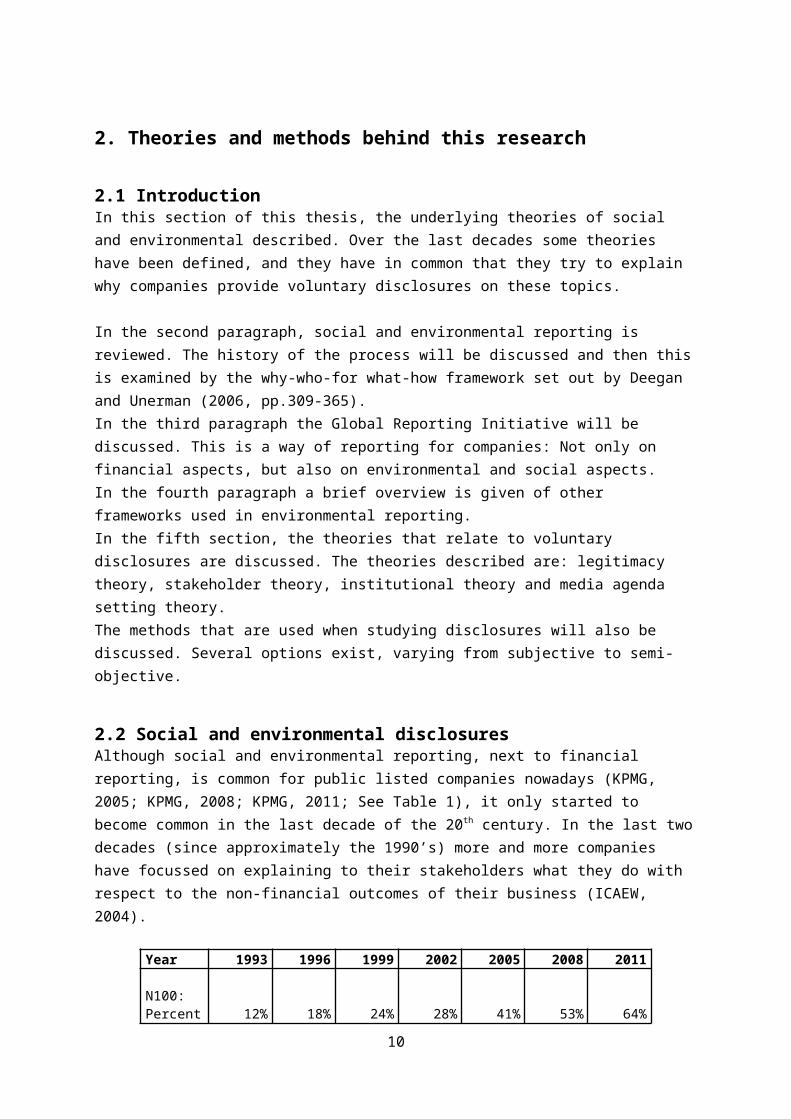

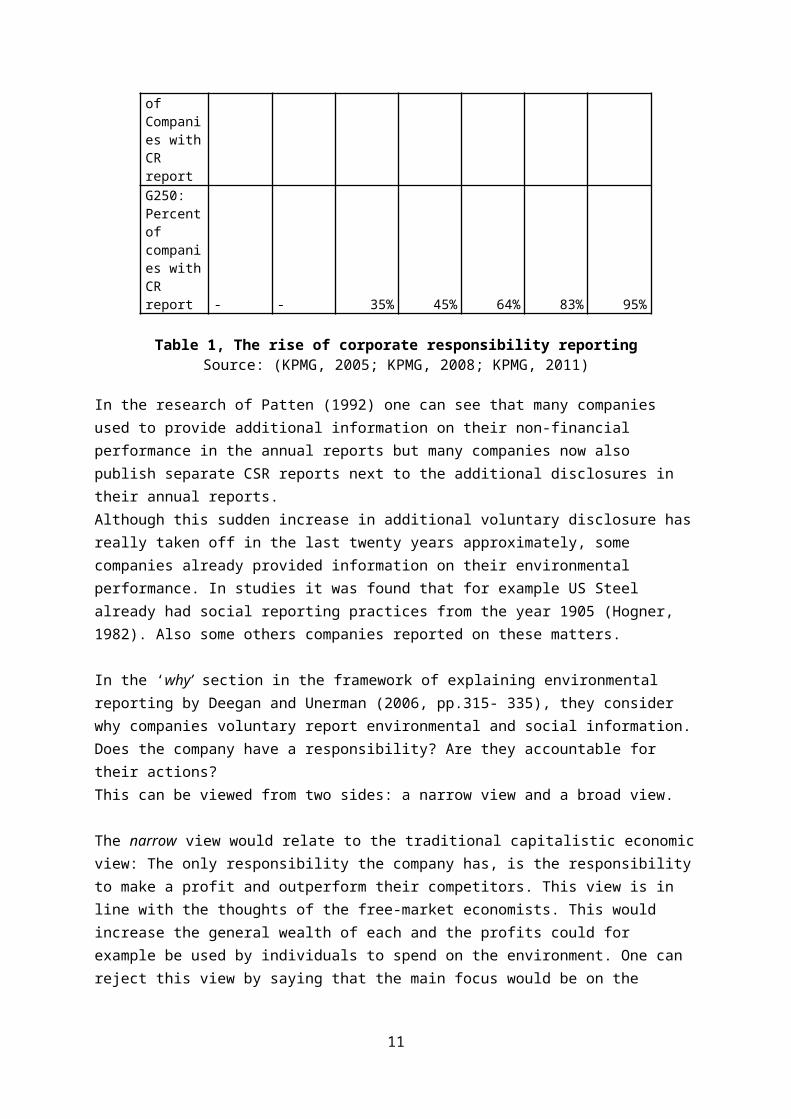

2.2 Social and environmental disclosuresAlthough social and environmental reporting, next to financial reporting, is common for public listed companies nowadays (KPMG, 2005; KPMG, 2008; KPMG, 2011; See Table 1), it only started to become common in the last decade of the 20th century. In the last two decades (since approximately the 1990’s) more and more companies have focussed on explaining to their stakeholders what they do with respect to the non-financial outcomes of their business (ICAEW, 2004).

Year 1993 1996 1999 2002 2005 2008 2011

N100: Percent of Companies with CR report 12% 18% 24% 28% 41% 53% 64%

G250: Percent of companies with CR report - - 35% 45% 64% 83% 95%

Table 1, The rise of corporate responsibility reportingSource: (KPMG, 2005; KPMG, 2008; KPMG, 2011)

In the research of Patten (1992) one can see that many companies used to provide additional information on their non-financial performance in the annual reports but many companies now also publish separate CSR reports next to the additional disclosures in their annual reports. Although this sudden increase in additional voluntary disclosure has really taken off in the last twenty years approximately, some companies already provided information on their environmental

9

performance. In studies it was found that for example US Steel already had social reporting practices from the year 1905 (Hogner, 1982). Also some others companies reported on these matters.

In the ‘why’ section in the framework of explaining environmental reporting by Deegan and Unerman (2006, pp.315- 335), they consider why companies voluntary report environmental and social information. Does the company have a responsibility? Are they accountable for their actions?This can be viewed from two sides: a narrow view and a broad view.

The narrow view would relate to the traditional capitalistic economic view: The only responsibility the company has, is the responsibility to make a profit and outperform their competitors. This view is in line with the thoughts of the free-market economists. This would increase the general wealth of each and the profits could for example be used by individuals to spend on the environment. One can reject this view by saying that the main focus would be on the owners of the company instead of the society and stakeholders as a whole.The second view is the broad view. This view does not focus on the financial side only but also considers social and environmental issues. If these are systematically ignored, it might result in the company being excluded in some parts of society. This might increase the costs of capital for the companies and subsequently result in lower return on investment. Companies that endorse the broad view report and communicate on the three factors (environmental, social and financial disclosures) by for example employing techniques such as ‘triple bottom line’ and the ‘global reporting initiative’. These will be examined later.

In the ‘who’ section of the framework by Deegan and Unerman (2006, pp.335-340), the company questions itself as to who it has to report their additional information.This section is to a great degree related to the ‘Stakeholder theory’ and the two different sides of this theory. Should the managers only provide information to the owners or the providers of capital (debt-providers and shareholders) as considered in the managerial view or should it be a more all-inclusive disclosure process as considered in the ethical view? This can differ from company to company, as different entities have different direct stakeholders. A large oil company will for example have to report more to the general public on their environmental policies than a small trading company. In Figure 1, one can see how many stakeholders a company might have. This does not stop at the providers of capital and direct business relations.

Figure 1, Stakeholders and the organisationSource: Deegan and Unerman (2006, p.369)

10

Many companies will actually identify their main stakeholders. Owen, Shaw and Cooper (2005), tried to find out which stakeholder is in general considered to be the most important. In Figure 2 the results of the study can be seen (Owen, Shaw and Cooper 2005, p.39). One can see that there is still a difference in the importance of stakeholders. The study was conducted by issuing a survey to 40 managers in the United Kingdom. They had to rate the stakeholders based on a ‘Likert-scale’ from 1 (not very important) to 5 (very important).

Figure 2, Importance of stakeholders as Seen by managers in the UKSource: Owen, Shaw and Cooper (2005, p.39)

In the ’for what’ stage, Deegan and Unerman (2006, pp.340-352), the company has now acknowledged that there is a demand for the social and environmental disclosures. In this stage it is then necessary to find out what this demand consists of: For what kind of information is there this demand? When identifying what the needs of the users are, another problem arises: The problem of different kind of stakeholders. Some stakeholders are close to the company (think of employees, suppliers, creditors and providers of capital), while some stakeholders are not that close to the company (e.g. the public, and even here one can differ between the public of developed nations and undeveloped nations). There are five problems when wanting to ascertain what the different demands are from the different stakeholders (Deegan and Unerman 2006, p.346).

1. There are many different kinds of stakeholders. Figure 1 illustrates the different types of stakeholders. Each such group has different individuals that make up the group and all these individuals might have different requirements of information.

2. The problem of being related (close) to the company or not that close to the company. Stakeholders that are close to the company can express their views in a more direct manner than stakeholders that are not that close to the company.

3. Some stakeholders might feel reluctant to discuss their concerns with the company. While in developed nations there might be many rules and regulations that govern the employee-employer relationship, in less developed nations these laws might be not that explicit. This can result in a fearful stakeholder: The stakeholder might not give his true opinion (e.g. the fear of losing one’s occupation)

4. Some companies, although they try, lack attention for some stakeholders their needs. Therefore their problems remain unobserved.

5. The company cannot always engage with their stakeholders (e.g. the unborn and other living animals and plants). Although these groups might be affected by the current operations of the firm, they cannot be consulted for their views.

11

When the company finally obtains all the concerns and wishes from the various types of stakeholders another problem arises: Some stakeholders might have different or even opposing views on certain issues.

In the ‘how’ sections of the framework two main methods are discussed: the ‘Triple Bottom Line’ (TBL) and the ‘Global Reporting Initiative’ (GRI). These came into place as there were no rules and regulations in the area of social and environmental reporting. The two try to make the reporting initiatives undertaken by the companies more comparable. By making the disclosures more comparable, transparency increases and a better assessment can be made of the efforts made by the different companies.

The TBL has tried to shift predominantly financial (bottom line) focus to a more inclusive focus. The triple referring to: financial, environmental and social. The downside of this method is that it seems to indicate that it is a numerical measurement. This is not the case: One can maximize the financial factor, but the two other factors cannot be measured as a single number. This is then very difficult to capture the efforts put into the environmental and social factors. Compared to the GRI, this is not a method that can be put into practice by means of a framework.

Next to the TBL method a company can also use the GRI method. This method is specifically developed to increase the comparability of social and environmental reporting. In total the GRI method has 79 indicators. In the next paragraph an elaboration is given.

2.3 The Global Reporting InitiativeThe GRI is the first real framework that entities can use if they wish to report on their sustainability practices. As the organisation behind the GRI wants to include as many organisations as possible they specifically highlight that the framework is based on fundament of consensus-seeking and including as many stakeholders as possible.The whole project started in 1997/1998, where the idea of creating a disclosure framework was first conceived. After this the first real GRI framework was released in 2000 (G1). Subsequently the second version of the framework was released in 2002 (G2) and the current version was released in 2006 (G3). The organisation constantly changes their framework and does not simply continue using one framework without taking the changing environment into account.

The GRI consists of three main parts that cannot always be used together. The parts are: the guidelines, the protocols and the sector supplements. The guidelines are the main part of the GRI. Within the guidelines there is a difference between the definitions (this can be seen as a framework) and the standardized disclosures as propagated by the GRI (these can be seen as the indicators). Even before these two parts are explained, the GRI is discussed and the GRI reporting framework is defined as being “intended to serve as a generally accepted framework for reporting on an organization’s economic, environmental and social performance”. It then goes on by stating that “it is designed for use by organizations of any size, sector or location” (Global Reporting Initiative, 2006). This emphasizes that every entity can use sustainability reporting and due to that, stakeholders can compare companies to each other. Next to this purpose, two other main purposes are stated in the overview: benchmarking and demonstrating.

12

The guidelines start by defining what the report its content, quality and boundaries should be. This is done by means of certain principles, which will be discussed here. This way of building up the framework is comparable to the way the conceptual framework builds up to IFRS.

2.3.1 Reporting principles for defining contentThe upcoming principles define what should be included in the content of a report (Global Reporting Initiative 2006, pp.7-13).

1. Materiality. Just as materiality in other accounting frameworks, it means that only items should be reported to the stakeholders that report on significant effects and that would change the opinion of users when these items are not reported.

2. Stakeholder inclusiveness. The company acknowledges that it does not have just one type of stakeholders and by doing this makes their reports multi-purpose. They do this by identifying their stakeholders and how they fulfil the information needs of them.

3. Sustainability context. The company should make clear that each report does not only succeed the previous report with new individual numbers. The reporting process should be a continuing effort exerted by the company to improve the environment and social issues in a more broad sense.

4. Completeness. The report should reflect every aspect of the company’s significant environmental, social and economical outcomes.

2.3.2 Reporting principles for defining qualityThe upcoming principles, when used, will ensure quality of the report given out by the company (Global Reporting Initiative 2006, pp.13-17).

1. Balance. All parts of the company’s performance should be reflected. Indifferent of whether this is good or bad news. Otherwise the report will function as a sort of advertisement.

2. Comparability. The same principle as the principle that is used in the conceptual framework as presented by the IASB: Users of these reports should be able to compare information with previous periods and other companies.

3. Accuracy. Information provided, indifferent to whether it is qualitative or quantitative information should be accurate. Qualitative information should be clear, detailed and balanced. Quantitative information should be correctly measured and presented.

4. Timeliness. Information provided should be on a regular scale and by this it informs users of the information.

5. Clarity. Information should be clear to users that study the report diligently.6. Reliability. Information that is provided by the company should be reliable. This will ensure

that users can trust the information that they use.

2.3.3 Reporting guidance for boundary settingNext to defining and stipulating by means of principles what should be included in environmental and social reports, the guidelines also explain what should not be included. This is the so called boundary of the report. The guidelines (Global Reporting Initiative, 2006, p.17) stipulate: “The Sustainability Report Boundary should include the entities over which the reporting organization exercises control or significant influence both in and through its relationships with various entities upstream (e.g. supply chain) and downstream (e.g. distribution and customers)”. In this definition an important part relies on the terms ‘control’ and ‘significant influence’. The definition of control: “the power to govern the financial and operating policies of an enterprise so as to obtain benefits from its activities” (Global Reporting Initiative, 2006, p.17) and significant

13

influence: “the power to participate in the financial and operating policy decisions of the entity but not the power to control those policies” (Global Reporting Initiative, 2006, p.17).This can be seen in Figure 3 (Global Reporting Initiative, 2006, p.18).

Figure 3, Boundary of sustainability reportingSource: (Global Reporting Initiative, 2006, p.18)

2.3.4 Standard disclosureNext to the theoretical principles that underlie the GRI, there is also a chapter in the guidelines that elaborates on the more practical side of using environmental and social reports.In part two of the guidelines information is given on strategy and profile, management approach and performance indicators. In the first section, strategy and profile, an overall profile of the company is presented to the user. This enables the user to get an impression of the company. It will give the reader an overview of the company from above, so that together with the indicators, a full picture of the company is conveyed.The management approach is more related to the specific indicators. It gives the user information on how the management interacts with the business that is related to the specific indicators. Therefore this part is given before a company discusses the indicators.The last section of the standard disclosure is the indicators: the practical points companies will have to report on when they use the global reporting initiative. There are two main types of indicators: core indicators and additional indicators. The core indicators are mandatory to use when adopting GRI reporting, while additional indicators can be used by some companies but are often not material for all companies. When core indicators do not align with the underlying principles given by the guidelines, these are also not applicable for the company.

14

Subsequently, the reporting indicators are split up in several categories: economic, environmental and social. Social is then again split up into four categories: Labour, human rights, society and product responsibility.

2.3.5 Oil & gas sector supplementNext to the ‘normal’ GRI, the GRI organisation has been increasingly focussing on sectors. They bring this into practice by developing and issuing sector supplements. These sector supplements try to act upon issues that apply for that specific sector. This, as sectors such as oil & gas and mining and metals affect their environment to a larger extent than a simple trading industry.

Currently the sector supplement for the oil & gas industry is under construction. Issues that are taken into account in the sector supplement are: emissions, water, bio fuels, health impact assessment, safety processes and renewable energy. Next to these factors many others are accounted for.

The final version of the document is expected to be published at the end of 2011. The project is developed by an international working group. The working group consists of both companies (e.g. BP and Shell) and other organisations in the oil sector1.

2.3.6 The futureAs more companies report on their non-financial performance, the general trend of it being a side-report also decreases. One of the developments is so called integrated reporting. Integrated reporting is currently being developed by the International Integrated Reporting Committee (IIRC). On their own website they say that “The IIRC has been created to respond to the need for a concise, clear, comprehensive and comparable integrated reporting framework structured around the organization’s strategic objectives, its governance and business model and integrating both material financial and non-financial information” (International Integrated Reporting Committee, 2011).

This form of reporting propagates the usage of one report instead of multiple reports. KPMG (2010, p. 3) says “It seems time for a transformation in corporate reporting: from a focus on financial information to a concept where all types of relevant information for assessing and evaluating a company’s quality, performance, value and impact are reported in a comprehensive way”.

As integrated reporting would increase the way companies report on their overall performance, the Global Reporting Initiative backs their efforts (KPMG 2010, p.2).

2.4 Other standards

2.4.1 AccountAbility frameworkA framework that assists companies to report in a sustainable way is the AccountAbility Framework. As many other frameworks, the AccountAbility framework is set up by multiple stakeholders: This as different stakeholders, have different views on sustainability. Currently the AccountAbility AA1000 series are used. These consist of: AccountAbility principle standard, Assurance standard and the Stakeholder engagement standard (AccountAbility, 2011).

The first one can be used by companies that want to comply with the AccountAbility framework. It defines three principles that need to be adhered. These principles are: inclusivity, materiality and responsiveness (AccountAbility 2008a pp.9-16). The webpage of AccountAbility says: “The

1 The list of companies and organizations that are a member of the international Working Group can be found at: http://www.globalreporting.org/ReportingFramework/SectorSupplements/OilAndGas/ [Accessed: 29 June 2011]

15

principles have been used by leading companies since 2008 and are compatible with other sets of principles in the marketplace, such as the UN Global Compact, GRI and ISO 26000” (AccountAbility, 2011).

The Assurance standard was created for a different group of stakeholders. This standard was made for assurance providers, such as auditing firms. With the standard they can see whether companies adhere to the AccountAbility Framework (AccountAbility, 2008b).

The last standard was created for again another group of stakeholders. This time the rest of the stakeholders in the process were taken into account. This as this makes the organisation perform better and it gives a contribution to the licence to operate (AccountAbility, 2008c). The standard goes on describing how to increase the quality of stakeholder engagement.

2.4.2 ISO 14001The International Organization for Standardization (ISO) has their own standard on environmental management within organisations. This standard is ISO 14001. It can be compared to the GRI as it both has requirements (ISO 14001) and guidelines (ISO 14004) published as separate standards.

One of the main features of ISO 14001 is that it does not specify any level of performance that a company has to reach. Instead, it is a “framework for a holistic, strategic approach to the organization's environmental policy, plans and actions” (ISO, 2011a). A reason for this flexibility is that it is difficult to generate one standard for many different companies, this as companies differ in many aspects.

Other standards within ISO 14001 elaborate on specific items such as: 14031 that gives guidance to companies on how to evaluate their environmental performance, 14063 that gives guidance on how to communicate the environmental performance and 14064 on how to account for greenhouse gas.

2.4.3 ISO 26000Next to ISO standard 14001, the ISO also published a specific standard on social responsibility as a management system that can be used by companies. This standard is not a certification standard such as 14001, but can be used voluntarily by companies that wish to do so. As with many frameworks, it is made to be used by many different stakeholders: both private as public companies.

ISO 26000 provides guidance on: concepts, background and trends, principles and practices, core subjects and issue of social responsibility, integrating and implementing social responsible behaviour, identifying and engaging with stakeholders and communicating commitment (ISO, 2011b).

2.5 Theories

2.5.1 Political economy theories

2.5.1.1 Legitimacy theoryThe first theory that can be considered to have an influence on the CSR and additional disclosure process is the legitimacy theory. It is defined by Deegan and Unerman (2006, p.271) as the assertion “that organisations continually seek to ensure that they are perceived as operating within the bounds and norms of their respective societies, that is, they attempt to ensure that their activities are perceived by outside parties as being ‘legitimate’”.

16

This process is not a static one but changes and companies will have to adjust to the current values held by different societies at different times. The expectations that society has, are considered to be included in a ‘social contract’ that the company has with society. This social contract is an amalgamation of implicit and explicit (e.g. rules, regulations and laws) expectations of society with respect to the conduct of the business. The company will have to ensure that they stay aligned with this contract. If not, it might lose its legitimacy to operate in society and by that the chance to make future profits.

The company in question will have to express their intentions with respect to the environment and social issues. This is usually done by expressing this in the annual accounts or specific CSR reports. This information is then available to the public.

2.5.1.2 Stakeholder theoryIf compared to the legitimacy theory, stakeholder theory considers the different stakeholders as more independent actors. Subsequently, with each of these actors, the company will have a separate ‘social contract’.Within stakeholder theory, there are two branches: Each type considering a different relation between the company and the stakeholders. The first branch is the ethical/moral (normative) type of stakeholder theory. The second branch is the managerial (positive) version of stakeholder theory. Of course there are different relations between the different types of stakeholders and the company. Shareholders will have more interaction with the board (shareholder meetings) of the company than the general public or environmental groups.

The ethical/moral (normative) view of the stakeholder theory is defined by Deegan and Unerman (2006, p.286) as “all stakeholders have the right to be treated fairly by an organization, and that issues of stakeholder power are not directly relevant”. This view relates to the stakeholders having some fundamental rights in their lives and these cannot be compromised by entities that are seeking profit.

The managerial (positive view of stakeholder theory actually differs from the normative view in the power relation. This view is defined by Gray, Owen and Adams (1996, p.45) as: “The stakeholders are identified by the organisation of concern, by reference to the extent to which the organisation believes the interplay with each groups needs to be managed in order to further the interests of the organisation”, where, when the power of the stakeholder increases, also the level of attention of the company to the needs of these stakeholder increases. Usually the providers of capital are considered as vital to the company, while secondary stakeholders are considered to be less important (see Figure 2).

2.5.1.3 Institutional theoryInstitutional theory is the third theory and overlaps (as all three do) the other two theories. Just as the other theories, it tries to explain the way companies report their social and environmental disclosures. Dillard, Rigsby and Goodman (2004, p.507) define it as: “concerns the development of the taken for granted assumptions beliefs and values underlying organizational characteristics... [with the accounting based studies] suggesting the importance of social culture and environment on the practice of accounting; the use of accounting practices as rationalizations in order to maintain appearances of legitimacy”.In other words companies will try to adjust their way of reporting to what is expected of them to remain a profitable company and remain legitimate.

17

Also in this theory there are some sub branches: One can distinguish between isomorphism and decoupling. Isomorphism can be seen as the change that the adaption of the institutional practice brings along (here: social and environmental reporting). This again can be divided into three sub categories as done by DiMaggio and Powell (1983):

1. Coercive isomorphism. Organisations are influenced and will change their policies with respect to their non-financial performance due to the influence of stakeholders. When the stakeholders want to see changes, the company will align themselves, as they are dependent on these stakeholders.

2. Mimetic isomorphism. As the word ‘mimetic’ suggests, a company will try to mime other companies (in their industry) with respect to the social and environment disclosures.

3. Normative isomorphism. As the word ‘normative’ suggests, this category is influence by norms and how one should act. Managers can be influenced by their personal background but also by groups and organisations they belong to. This creates a social force that influences managers and the disclosure of the company they work for.

Next to isomorphism there is a second branch of institutional theory: decoupling. This is the actual usage of social and environmental reporting, while the company does not align with these stated processes.

2.5.2 Media agenda setting theoryAs predicted by legitimacy theory, companies will have to be legitimate to operate. This legitimacy is often derived from the current views from stakeholders. In turn, one can ask how the companies – managers – can derive these expectations. Concerns are often communicated by the media. By means of this same media, managers will inform themselves and try to react to certain issues that might cause a threat to the legitimacy of the company.

One can then ask how the opinions of the public are formed. Ader (1995, p.300) found that there is a link between the level of media reporting and the public opinion. In this sense, the media sets the agenda of what is seen as important. Ader (1995) finds that the effect of the media agenda setting theory is higher when the event that is reported is relatively unknown to the media consumer, and therefore needs the media to get information on the topic.

Capriotti (2009) says that a company needs the media as part of being corporate visible. The more a company is seen in the media, the more prominent the company becomes. Companies then can be associated by consumers economically and socially (Capriotti 2009, p.228). The economic role relates to the role the company has as a producer and the creation of profits. The social role relates to “respect of human rights, care for the environment, and make an economic and social contribution to the community” (Capriotti 2009, p.228).

2.5.3 Voluntary disclosure theoryClarkson et al. (2008) contrast the previous theories with the voluntary disclosure theory. This economic-based theory predicts that companies that have good environmental performances tend to disclose more environmental information than companies that do not. This theory lies in line with the Principal-Agent theory. Better performing companies disclose more information to signal they are performing better. The information asymmetry between the company and the stakeholders decreases. This additional disclosure is something only good performing companies can do. Companies that have worse performances cannot just copy this behaviour, so they

18

report less or even nothing. Due to this investors can distinguish between good environmental performers and bad ones.

2.6 Models

2.6.1 Measuring the quality of voluntary disclosuresAn important issue is measuring the social and environmental disclosures made by companies. The main objective of analyzing disclosures is identifying the quality of the information provided. This can be done is several ways as identified by Beattie et al. (2004). Here one can distinguish between the so named ‘subjective ratings’ and the ‘semi-objective’ ratings. The semi-objective rating again consists of two subcategories: ‘disclosure index studies’ and ‘textual analyses’.Subjective ratings look at several ratings that are given to companies based on their voluntary disclosure. These ratings are often provided by users of financial statements (e.g. financial analysts that would normally analyse the statements on a daily basis). Although they are acquainted with the statements, this is still quite subjective, as two individuals could rank the same disclosure completely differently.In the past there was a well-known American subjective rating that was assigned to companies on a yearly basis. This was given out by the Association of Investment Management and Research (AIMR), however they stopped with this rating system in 1997. Next to this better-known rating, there are many other assessments published.

Another method of rating the quality of disclosures is the disclosure index studies within the semi-objective ratings. This model looks at the quantity of disclosures that are given within disclosures provided by the company and this is seen as the indicator of the quality of disclosure.These models are usually based on some specified questions and subsequently a score is given when the text complies with certain conditions. These conditions together and the points assigned form the total score. Several models can be made, based on different facts:

1. Binary (0 or 1, present or non-present) or an ordinal measure (e.g. 0 for not disclosed, 1 for qualitative disclosure and 2 for quantitative disclosure). This was used by Botosan (1997).

2. Weighted or unweighted model. More weight can be given to certain terms when they are considered to be more important than items that are deemed to be unimportant. This is usually done by surveying users of specific information.

3. Grouping of items into hierarchical categories.

The last method is the textual method, also within the semi-objective rating. This method will in general look at the readability, the thematic content and linguistic side of the disclosures. I will not further elaborate on these topics as these will not be used in this thesis.

2.6.2 LimitationsAs both the subjective, as the semi-objective method, classify texts based on either the text or the context, these ratings are not really ‘hard figures’. For the semi-objective disclosure index models, the quality of the text is measured by the quantity of the text. This is a major limitation because companies could increase the quantity of their disclosures, to appear better in several index studies.For subjective models, the limitations are even larger as individuals perceive different elements as having a different importance to the text. This decreases the comparability of the outcome.

19

2.7 Research in relation to the theoriesIn this chapter several theories have been discussed. The research that will be done in this thesis derives its fundament from these theories.In chapter 6 hypotheses are tested that relate to increase of environmental reporting in relation to incidents. The hypotheses are based implicitly on the theories that are discussed in this chapter. Therefore a link is established between the theories discussed and the hypotheses tested later in this thesis. Two theories are especially used: legitimacy theory and media agenda setting theory.

In specific legitimacy theory can be seen as a fundament: This as this theory explains why companies would report after an incident to a general set of stakeholders. Legitimacy theory says there is a dynamic ‘social contract’ between the company and society. As this is a dynamic and not a static contract it changes all the time. Therefore other expectations arise after a negative incident, such as the Deepwater Horizon oil spill. To regain the perception of being a legitimate company within society companies might alter their way of reporting. In this thesis the Deepwater Horizon oil spill is investigated and the effects it had on voluntary disclosure of the companies within the 2911 SIC code (Standard Industrial Classification). It can be expected that companies will increase their environmental disclosures to signal that they are a legitimate company within the industry.

The second theory that influences the hypotheses is the media agenda setting theory: As can be seen in chapters 4 and 5, the media reported relatively a lot on the deepwater horizon oil spill. This could have influenced the opinion of the general public and indirectly could have set the agenda for the companies. Media agenda setting theory is in line with legitimacy theory and therefore could have influenced the ‘social contract’ of the company with the general public. This in turn could indirectly influence the reporting from the companies towards the stakeholders.

Both hypotheses then investigate whether the incident influenced the reporting after the oil spill towards the general stakeholders.

2.8 ConclusionIn this chapter, theories, methods and frameworks are considered that are used in research currently conducted on voluntary disclosure of environmental and social information. In the first section, a general introduction to social and environmental reporting was given. It was found that the first forms already started at the beginning of the 20th century although it was not that common. It only started to grow quickly in the 1990’s. Currently one could not imagine a business community without any social and environmental reporting.

After this general introduction, the social and environmental reporting framework by Deegan and Unerman (2006) was discussed. They examined it by using the why-who-for what-how framework. In the ‘why’ section, two views were investigated: One can have a narrow (short-term, self-interested) view or a broad (longer-term, more considering) view. In the ‘who’ section it was found that, in line with the managerial side of stakeholder theory, some differences still exist between the importance of different stakeholders as considered by managers, with the shareholders being considered most important and the suppliers least. In the ‘for what’ part, it was found that when the company wants to identify the needs of stakeholders there are some difficulties. Five general difficulties are considered. In the last section, the ‘how’ part, two methods are discussed that can be used to report to several stakeholders: The TBL and GRI methods. The first still has some practical difficulties and the second is being used more and more.

20

It was found that the GRI consists of a framework and a set of indicators that can be used in communication to stakeholders. The indicators are more concrete and practical. Also a specific sector supplement is under construction that will improve the factors on which companies within the oil & gas sector can report.

Next to the GRI, a limited overview was given on other frameworks. The AccountAbility framework and two ISO standards were examined.

The first of the three political economy theories is the legitimacy theory. Companies have an explicit and implicit ‘social contract’ with society and when this contract is breached their legitimacy to operate might fall away.The second theory is the stakeholder theory. This theory has two branches. The first branch, the ethical/moral (normative) theory states that all stakeholders should be treated in an equal manner. The second theory is the managerial (positive) branch and predicts that more influential stakeholders would be heard more than less influential stakeholders. The third theory, the institutional theory, considers that companies are forced to disclose environmental and societal information. Also in this theory two branches exist: Isomorphism, which considers forces that actually changes the company, while the second branch, decoupling, says that companies might be forced to disclose information but in reality they would not change any policies.

Next to this, two other theories are investigated: The media agenda setting theory and the voluntary disclosure theory. The first theory explains that some concerns that are conveyed by the public to companies are actually instigated by media coverage. The second, voluntary disclosure theory, contrasts with the previous theories by saying that companies that perform better environmentally, will disclose more.

In the last section of this chapter, different methods were considered that can be used for the measurement of the quality of voluntary disclosures. In the paper of Beattie et al. (2004), two general methods are considered: the subjective method which is based on subjective ratings given by a certain group of stakeholders. The second method is the semi-objective method. This method can be divided into the disclosure index model and the textual method. After this, the limitations of the semi-objective and subjective methods were discussed.

21

3. Literature review

3.1 Introduction In this chapter, the most important literature in the field of social and environmental reporting is presented. I investigate why additional information is so often voluntary disclosed and what several studies find on voluntary social and environmental information. The studies have been selected on subject relevance.

In the second paragraph a broader and more general literature overview relating to social and environmental disclosure is given. In the third paragraph, a more specific part of the literature will be discussed. In this section, articles that explore voluntary social and environmental disclosures/reporting after certain incidents will be discussed. In the fourth paragraph multiple studies are listed that use models to classify disclosures. First, one of the first disclosure index model studies will be discussed. Secondly, several studies are listed that use environmental disclosure index models. From these models, a model is derived that will be used in the empirical part of this thesis.In Appendix 1 an overview of the discussed papers is given.

3.2 General literature

3.2.1 Capital market reactionsAnderson and Frankle (1980) make a link between the voluntary disclosure of social information and the effects on the capital market. They define social reporting as “the communication and reporting of information concerning a firm’s community involvement, human resources, environmental impact and products/service contributions”. The authors looked at the voluntary social disclosures of Fortune 500 firms that were listed at the New York Stock exchange in 1972. Subsequently they divided the companies into two groups: one group with voluntary social disclosures and one without these disclosures. As theoretical basis they used the capital asset pricing model (CAPM). Everything else being equal, one could expect that the return on investment should be the same between the two groups.

An interesting point of the research is that the authors define two different (competing) hypotheses next to the 0 hypothesis. The first expects that firms that do not engage in voluntary social reporting have a higher return on investment. This as the extra costs that are made by these firms would not be profitable. The second expects that the firms that do engage in voluntary social reporting have a higher return on investment. This can be explained as shareholders are willing to pay a premium for companies that operate ethically.

The results of the study show that all firms that voluntary disclose information have in general a higher return on investment compared to firms that do not disclose voluntary information. For portfolios that had a Beta of 0.8 and 1.2 this was significant on a 5% level. For the portfolio Beta=1.0, this was higher but not significant.A general conclusion can be drawn that the market favours companies that disclose social information to companies that do not.

22

A more recent study is from Botosan (1997). She investigated the relation between the disclosures made by companies and the cost of capital. This was done by investigating the annual reports and the disclosures made in them. In her research, the first hypothesis investigated whether there was a negative association between the disclosures of a company and the cost of capital. The second hypothesis examined whether this association is stronger for smaller companies than for larger companies. This, as smaller companies have less disclosures and the annual report plays a bigger role in their reporting process.

The sample consisted of 122 manufacturing firms. One industry was chosen by Botosan while different industries show different characteristics and this could influence the outcome of the study. A disclosure index model is created to assess the level of voluntary disclosure. 0 points were awarded for no disclosure, 1 point for qualitative disclosure and 2 points for quantitative disclosure as “precise information is more useful and may enhance management’s reporting reputation and credibility”, (Botosan 1997, p.334).

She found that companies with a lower analyst-following could significantly decrease their cost of capital as they would report more. Especially when they reported on forecast information and important non-financial statistics.

3.2.2 Characteristics of firms and countriesKolk et al. (2001) examined the largest 250 firms from the Fortune 500. The authors looked at their environmental reporting and how this differs with some firm specific characteristics. These characteristics are ‘sector’ and ‘nationality’.

In the first section they looked at additional disclosures in reports in general. They showed that, based on the reporting year 1999, there are some differences in reporting between sectors. They divided the reports into: Environmental reports, environmental information (less than the first category), no environmental information and non-response. Although 30% of the global 250 consists of financial firms, only 14.9% had environmental reports. 44.6% of the financial firms fell into the category: no environmental information. In general around 67% had some kind of environmental information.They first look at the link between nationality and additional disclosures. They find that in a country such as the Netherlands, where some environmental reporting is required there is a higher level than when this choice is voluntary. Also the UK and Germany score high in this index. The UK can be explained by the pressure exerted by the investment community, while in Germany the governments support the European Eco-Management and Audit Scheme (EMAS).

Then the authors shifted their attention to the different kinds of sectors. The trend is that sectors that clearly have an influence on society and the environment are more likely to issue some kind of environmental report. This can be seen in the pharmaceutical and chemical sectors. Here a score of 100% environmental reporting is reached. This is in line with legitimacy theory, which can explain the level of reporting. This contrasts with, for example, the insurance sector where still many companies do not report on their environmental behaviour. The authors expect that due to more standards (e.g. GRI) a second wave of environmental reporting will start.

Although by this time there is more and more emphasis on corporate environmental disclosure, there are still companies not adhering to this demand. Solomon and Lewis (2002) investigate this paradox. They attempt to identify why companies would or would not disclose additional information and what the incentives or disincentives are.

23

They start by identifying four sectors that can explain incentives in additional disclosures. These are: market, political, social and accountability incentives. When looking at market incentives, the best known is the incentive to reduce the cost of capital. Entities that operate in an ethical manner might have less difficulties attracting capital than companies that do not. Subsequently they discuss the other incentives. Disincentives mentioned in the paper are the lack of demand for environmental reporting and then cost of additional disclosures outweigh the benefits.To further examine this, the authors distributed a survey under 625 persons. Further there were 3 subgroups formed: users (normative users and interested groups) and providers. With the normative group being a group with strong views although probably a lack of use (e.g. academics, government officials) and examples of users of the interested group are financial analysts, media and banks.The survey wanted to examine whether the respondents were incentivized in any kind. With a usable response rate of 43% this survey can be considered as very reliable.

The main outcomes are that all three groups believe that corporate environmental reporting is important, with the main incentive being ‘accountability’. Both user groups expressed the opinion that companies sometimes use voluntary reporting to improve their corporate image. On the basis of this outcome the writers give some policy recommendations. One option could be making additional reporting mandatory. This would result in not getting a competitive advantage and in more comparability. A second is making all parties more aware of the demand and views from other parties on their actions undertaken. This might align the user groups more.

3.2.3 Mandatory reportingWhen then looking at an example of mandatory environmental reporting, as opposed to voluntary, the focus can be shifted to the paper of Larrinaga et al. (2002). They investigated the Spanish situation. In Spain a special standard is active that requires companies to mandatory disclose environmental information about the company. In the paper the authors show that ‘simply’ making environmental reporting mandatory, does not solve all problems. The new Spanish standard requires all companies to disclose information on their environmental performance. These disclosures have to be made in the annual accounts, in a prescribed manner and in a conventional accounting way. In the research 70 firms were examined. Of these 70 firms, only 23% complied with the disclosure process in 1999 (after introduction of the mandatory reporting process). The authors also included a content analysis based on the law that prescribed what to include in the annual accounts. Based on this they had a score: from 0 (non-reporting) to 7 (maximum reporting). The average was 0.5 (1.8 for reporting companies) in the year after the introduction, 1999. Even when companies were disclosing information, the authors found that the companies tended to report one side of their story: the side that enhanced the positive image of the company.

The authors conclude by making a clear distinction between two types of reforms in the environmental reporting sector. Reforms can be administrative or institutional. Administrative reforms are reforms that only change the rules and regulations. This happened in Spain by making environmental reporting mandatory in 1998. An institutional reform is created when entities actually change their behaviour and really want to comply with a change.

3.2.4 Different disclosuresCho and Patten (2007) think that mistakes are made continuously in environmental disclosure research. Not all environmental issues that are disclosed by management are disclosed to legitimize the organisation. Therefore the authors distinguish between litigation and non-litigation reporting. The authors argue that litigation related disclosures are mandatory and cannot be adjusted. Therefore one

24

has to examine non-litigation related disclosures. Secondly they distinguish between monetary (high valuated) disclosures and non-monetary (lower valuated) disclosures.The authors develop a classification that uses eight items. Next to an overall score that is assigned to a company, non-monetary and monetary items are also accounted for separately. Next to that they examined the 10-K reports. It was found by the authors that, all in line with legitimacy theory, within the non environmental sensitive industry, the lesser performing companies employed less monetary disclosures than more successful companies.

Clarkson et al. (2008) test two theories behind voluntary disclosures that are made by companies. Firstly they discuss the economic based theories: companies with good environmental performance will voluntary disclose a lot of information and this will be as objective as possible (to contrast with non good environmental performers). Secondly the socio-political theories: companies with a bad environmental performance will voluntary disclose a lot of information, this to legitimize themselves.

The authors used 191 firms that disclosed information in 2003 from firms that operate in the five most polluting sectors. They improved the previous models by not looking at mandatory disclosures (the same as Cho and Patten did) and they performed their content analysis based on the GRI. They find that there is a positive relationship between environmental reporting and voluntary disclosure and not a negative one. This contrasts with Cho and Patten (2007). Although they find this contrast, they also find that many companies that had negative media attention would increase their voluntary disclosure. This is then often done by making so called ‘soft claims’ (Clarkson et al. 2008, p.21). This is in line with the media agenda setting theory.

3.3 Specific incidentsThe first paper that is discussed is the paper of Patten (1992). This paper has been one of the first to examine the environmental disclosures after a certain incident. The incident that was taken into account was the ‘Exxon Valdez’ oil spill, where a ship of Exxon crashed into a reef off the coast of Alaska on the 24th of March 1989. This accident resulted in an oil spill of 11 million gallons of oil (41.5 million litres). Exxon, as expected by legitimacy theory, disclosed in the reporting year a total of 6 pages on the environment (3.5 on the oil spill and 2.5 on other environmental issues). In 1988, the oil company only reported 0.6 pages on their environmental policies.Patten, on the other hand, did not want to investigate the disclosures made by Exxon, but wanted to examine the disclosures made by the other oil companies. There was a chance that the legitimacy of the other oil companies was also at risk. Patten brought up two main arguments for this:

1. Seven oil companies (including Exxon) had a joint- venture (Alyeska) that was responsible for any oil spill. This service would have to respond within 5 hours, but in total in took 12 hours for the first response. Therefore they were partly responsible for the significance of the oil spill.

2. As with many accidents within a sector, the general public’s attitude towards a sector will change. Even when the company did not have any (business) link with the particular incident.

Patten therefore examined the annual reports of 21 of 23 publicly traded oil companies and looked at the environmental disclosures in 1989 compared to 1988. Patten took disclosures into account that fitted into a seven factor model and then just counted the page numbers as an absolute figure.

After the counting of the page numbers, Patten developed two tests. The first one simply checked the mean and standard deviation of the disclosures in the two years. Here a significant increase in disclosures was found in 1989 (mean: 1.9, σ: 1.469) compared to 1988 (0.61, σ: 0.784) at the 0.01

25

level: Also when the finding was split up into two parts: financial and non-financial disclosures, both were significant.

Secondly Patten developed a linear regression, which investigated whether the difference in disclosures of an individual company were related to a) the size, b) part-ownership/non-ownership of Alyeska2. Also here the results turned out to be both significant at the 0.05 level. This means that companies that were partly responsible for not responding had a significant higher level of disclosure compared to companies that were not in the cooperation. Secondly, companies that were larger also had reported significantly more than small companies.

The outcome from this test backs the legitimacy theory in that companies will have to legitimize them when operating in a sector that is sensitive: Also when they were not related to the incident themselves.

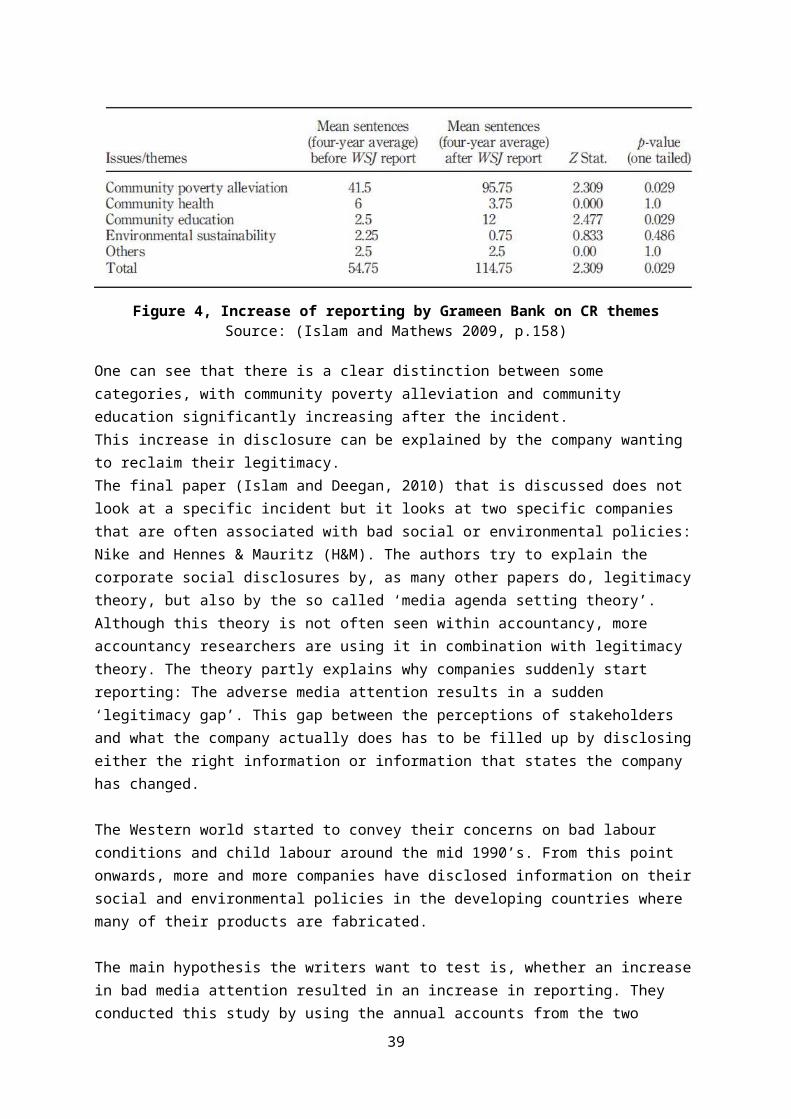

Next to environmental incidents as seen in the paper by Patten, there are also ‘soft’ incidents that can question a company’s legitimacy. This happened to ‘Grameen Bank’ (GB), a Microfinance Institute (MFI). The bank issues small loans to individuals in less developed countries. With this money they can start their own business and then they will repay the MFI. GB operates and reports in Bangladesh, but it has no obligation of making annual reports available. Therefore the disclosures made by GB are self regulated.In 2001, the Wall Street Journal (WSJ) was very critical about GB and the manner in which they reported. The main criticism was on certain policies of the bank of converting overdue loans in to so called ‘flexible’ loans.