environmental disclosure committee newsletter - american bar

TRANSCRIPT

1Environmental Disclosure Committee, December 2012

December 2012Vol. 10, No. 1

Environmental DisclosureCommittee Newsletter

MEMBERSHIP VICE CHAIR NOTEPeter J. Gioello Jr.

As your new vice chair for Membership, I wanted totake this opportunity to introduce myself and to leteveryone know that they should feel free to reach outto me with any comments or suggestions having to doin any way with the Environmental DisclosureCommittee.

At this time, we have 259 committee members locatedin 36 states and Puerto Rico. Our membership listincludes several students, attorneys in private law firms,government attorneys, public interest attorneys and in-house counsel at companies in various sectors,including but not limited to the insurance, finance, oiland gas, energy, food, retail, and environmentalengineering sectors. We hope that we are able toattract new members in the upcoming year—please doyour part and tell friends and colleagues about ourcommittee.

At the recent Section meeting in Austin, committeemembers connected with one another and discussedpotential programming for the upcoming year. Outsideof the section events, we are hoping that members areable to connect with one another throughout the year aswell. For example, attorneys in a particular industry orgeographic region may wish to come together andorganize some sort of event or draft a timely article. Asin past years, we are welcome to ideas and

suggestions—just send them through me or to anotherone of the committee leaders.

We will be sure to keep everyone posted aboutupcoming events. In the meantime, please let me knowif you would like to become more involved or if youhave any programming suggestions or ideas for newsarticles in the next year. Have a safe and happyholiday season!

Peter Gioello is an associate at Cahill Gordon &Reindel LLP in the Environmental Practice Groupfocusing principally on environmental risks inconnection with corporate transactions. He is vicechair of Membership for the EnvironmentalDisclosure Committee for the ABA Section ofEnvironment, Energy, and Resources and is amember of the Environmental Law Committee forthe New York City Bar Association.

Join the Environmental DisclosureCommittee online!

Committee Web site:http://apps.americanbar.org/dch/committee.cfm?com=NR351700

Committee List Serve Address:[email protected]

Section LinkedIn Group:http://www.linkedin.com/groups?home=&gid=1018127

Connect to the Section on Facebook:http://www.facebook.com/ABAEnvLaw

Follow us on Twitter:http://twitter.com/ABAEnvLaw

2 Environmental Disclosure Committee, December 2012

Environmental DisclosureCommittee NewsletterVol. 10, No. 1, December 2012David A. Roth, Editor

In this issue:

Membership Vice Chair NotePeter J. Gioello Jr. ................................. 1

Defensible Cost EstimatingFundamentals in the Context ofEnvironmental DisclosureMichael Berman and Paul Brookner . 3

Water-Related Risks and OpportunitiesUpdateE. Lynn Grayson ..................................... 9

How Incorporation of IFRS into U.S.Financial Reporting Standards MayAffect the Reporting of EnvironmentalLiabilitiesBrian Henthorn and Lisa Walsh ......... 11

Uncovering the Mystery of Materiality inToday’s MarketJerome Lavigne-Delville, J.D., andJean Rogers, Ph.D. .............................. 18

Copyright © 2012. American Bar Association.All rights reserved. No part of this publicationmay be reproduced, stored in a retrievalsystem, or transmitted in any form or by anymeans, electronic, mechanical,photocopying, recording, or otherwise,without the prior written permission of thepublisher. Send requests to Manager,Copyrights and Licensing, at the ABA, e-mail:[email protected].

Any opinions expressed are those of thecontributors and shall not be construed torepresent the policies of the American BarAssociation or the Section of Environment,Energy, and Resources.

January 25-27, 2013ABA SEER Winter Council MeetingLa Concha ResortSan Juan, PR

February 6-12, 2013ABA Midyear MeetingDallas, TX

February 26, 2013Key Environmental Issues in US EPARegion 4Atlanta, GA

March 21-23, 201342nd Spring ConferenceGrand America HotelSalt Lake City, UT

April 11-12, 2013ABA Petroleum Marketing Attorneys’MeetingWashington, DC

April 18, 2013ABA Public Lands and Resources LawSymposiumMissoula, MT

April 19-21, 2013ABA SEER Spring Council MeetingGreenough, MT

June 5-7, 201331st Annual Water Law ConferenceLas Vegas, NV

CALENDAR OF SECTION EVENTS

AMERICAN BAR ASSOCIATION

SECTION OF ENVIRONMENT,ENERGY, AND RESOURCES

For full details, please visit www.ambar.org/EnvironCalendar

3Environmental Disclosure Committee, December 2012

DEFENSIBLE COST ESTIMATINGFUNDAMENTALS IN THE CONTEXT OFENVIRONMENTAL DISCLOSUREMichael Berman and Paul Brookner

Reporting entities in the United States, along with theirlegal and financial counsel, are generally wellacquainted with the requirements associated with thedisclosure, quantification, and reporting ofenvironmental liabilities. Traditionally some reportingentities may have assumed that environmental liabilitieswere not material to their overall financial bottom lines.However, over the past decade of the post–Sarbanes-Oxley era, a focus on the quantification of contingentenvironmental liabilities has become more prominent.That is, the need to specifically quantify the magnitudeof costs associated with an environmental liability hasbeen required or requested more and more frequently.

This task of quantification has always beencomplicated by the inherent uncertainty in estimating anunknown (such as, what might have happenedunderground decades ago), often based on limited dataand information, as well as the highly site-specificaspects of many environmental liabilities. For example,a similar historic industrial practice in one location mayhave resulted in minimal impact—but in anotherlocation may have resulted in significant environmentalliabilities. The task of appropriately valuingenvironmental liabilities is made more complex in theface of changing financial accounting regulations (suchas those focused on contingent asset retirementobligations and disclosure of liabilities associated withgreenhouse gases); prudent business practices in thecontext of increasing corporate cash flow concerns andbankruptcies; pressure from shareholders to providecorporate transparency, and ongoing litigation risks.

It is our observation that systems and approaches usedto comply with the environmental liability valuation (or“ELV”) aspect of financial reporting requirements varywidely from entity to entity, as appropriate for therespective nature of their environmental liabilityportfolios. However, we have observed somefundamental principles and similarities, as well as someemerging trends, in how many entities are quantifyingtheir environmental liabilities. This article provides an

overview of these core approaches and trends in thecontext of our experience supporting clients in broadaspects of ELV and financial reporting.

ELV in the Framework of Disclosure

In general terms, ELV can be defined as an estimateused for a specific purpose to quantify the cost toaddress an environmental condition. This basicdefinition is broadly applicable. However, each ELVanalysis needs to be done in the context of how theterms “specific purpose,” “quantify,” and“environmental condition” are applied by the prevailingrequirements and various stakeholders in the estimatethat is being conducted. As such, an ELV analysis ofthe same “environmental condition” could result in avery different value, when applied under differentcircumstances.

The example of a large leaking underground storagetank can be considered. It may be known that anunderground tank has been leaking (perhaps throughleak detection monitoring or inventory lossdocumentation). But, at least initially, the magnitude ofthe environmental impact is generally not known and,as a result, there is a broad range of costs that may beincurred to ultimately address the issue. Anenvironmental expert may be asked to value thisliability and the result of such an analysis may bedifferent, depending on the purpose of the analysis. Forexample:

· A short-term budgeting analysis may onlyfocus on the costs that are expected in animmediate future time frame (e.g., the currentor next financial period).

· An analysis in support of a feasibility study fora Superfund site will typically seek to providean estimate consistent with the U.S.Environmental Protection Agency (EPA)costing guidance (e.g., using a specifieddiscount rate and within an uncertainty range of+50/-30 percent).

· An analysis to support an insurance claimmay focus on costs that are recoverable underthe available coverage (e.g., considering onlycosts associated with an occurrence during acoverage period).

4 Environmental Disclosure Committee, December 2012

· An analysis in support of a merger,divestiture, or acquisition or a legaldispute over environmental liability may seekto determine a risk-weighted expected value ofthe liability—or, alternately, may not focus onthe value of this liability at all if it is below acertain cost threshold.

· An ELV analysis in support of financialdisclosure decision making in the FederalAccounting Standards Board (FASB) and theU.S. Securities and Exchange Commission(SEC) framework will necessarily focus oncosts that are required under the relevantstandards and regulations (e.g., costsassociated with a contingent loss will focus onthe costs that are “probable and reasonablyestimable”).

While the specific requirements associated with thedisclosure and reporting of environmental liabilities arebeyond the scope of this article, environmentalliabilities generally fall into one of the followingcategories:

· Contingent Loss—Addressed underAccounting Standard Codification (ASC) 450(Contingencies) (Former FAS 5);

· Asset Retirement Obligation (ARO)—Addressed under ASC 410 (Asset Retirementand Environmental Obligations); or

· Contingent ARO—Addressed under bothASC 410 and ASC 450.

Common ELV Guidance

Within the framework of various financial reportingstandards, environmental professionals most typicallylook to certain guidance documents to provide adefensible foundation for environmental cost estimates.While there is no “right way” to complete anenvironmental liability evaluation, a host of guidancedocuments is available, several of which are listed atthe end of this article. These guidance documentsinclude those published by EPA, the U.S. Departmentof Defense, U.S. Department of Energy, and othernongovernmental industry groups, such as theAssociation for the Advancement of Cost Estimation(AACE).

Another relevant guidance document worth mentioningis the ASTM’s E2173-07 (2011) Standard Guide forDisclosure of Environmental Liabilities. ASTMprovides this guidance as an overview for the strategyand decision-making framework required to determinewhich environmental liabilities require disclosure anddescribes the reporting requirements that are relevantto such disclosure. This document does not addresshow estimates of environmental liability can or shouldbe made.

One of the more frequently referenced guidancedocuments generally used by environmental experts isthe ASTM E2137-06 (2011) , Standard Guide forEstimating Monetary Costs and Liabilities forEnvironmental Matters. First published in 2001, thisstandard was revised in 2006 and reauthorized in2011. While ASTM E2137 does not provide a“cookbook” approach to ELV, it does provide a solidframework and fundamental basis for completinganalyses in a variety of contexts—including in supportof environmental liability disclosure and reporting.

ASTM E2137 describes a suite of fundamentalcomponents that should be considered in developingany environmental cost estimate. These componentscan be summarized as follows:

· understanding the information to be used· understanding costs and liabilities to be

included/excluded· determining the appropriate estimation

approach· understanding and quantifying the appropriate

uncertainty· considering contingencies· considering net present value (NPV)· considering allocation, offsets, and recoveries

All of these steps are vital to conducting and being ableto defend any environmental cost estimate. Several ofthe key aspects are discussed below.

Choice of Estimation Approach—StatisticalBasis

At its heart, the decision of how to approach a costestimate is grounded in statistics. Since there is inherent

5Environmental Disclosure Committee, December 2012

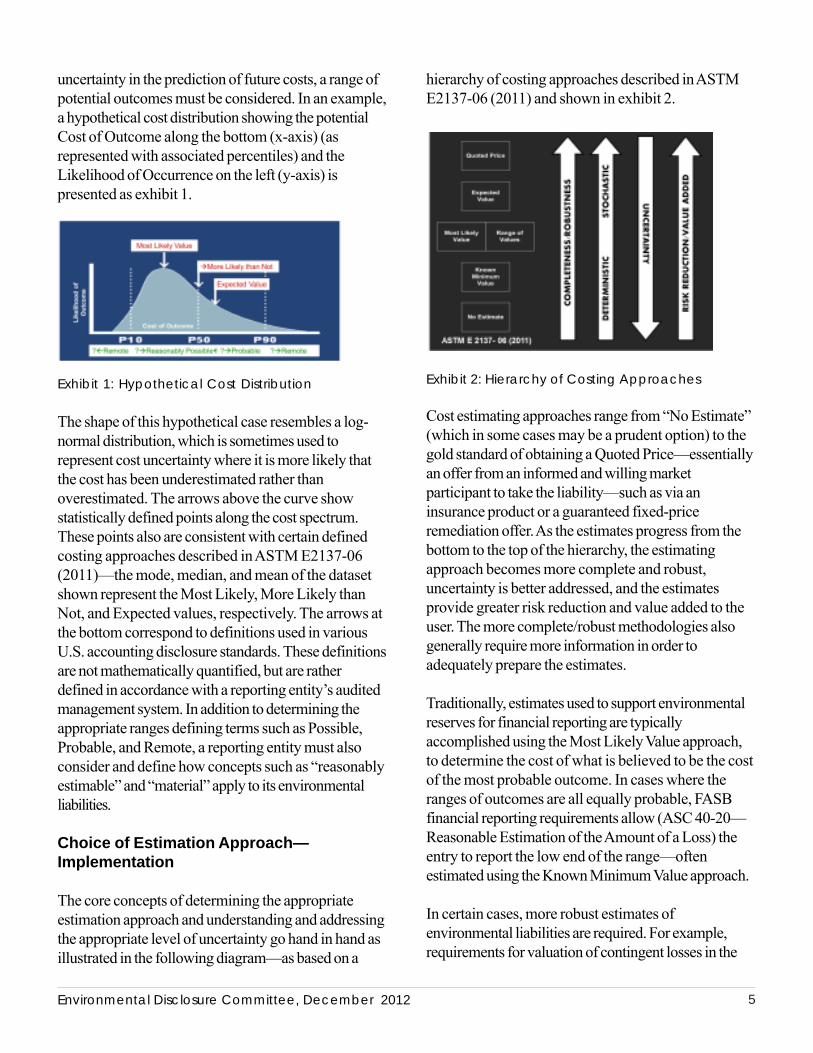

uncertainty in the prediction of future costs, a range ofpotential outcomes must be considered. In an example,a hypothetical cost distribution showing the potentialCost of Outcome along the bottom (x-axis) (asrepresented with associated percentiles) and theLikelihood of Occurrence on the left (y-axis) ispresented as exhibit 1.

Exhibit 1: Hypothetical Cost Distribution

The shape of this hypothetical case resembles a log-normal distribution, which is sometimes used torepresent cost uncertainty where it is more likely thatthe cost has been underestimated rather thanoverestimated. The arrows above the curve showstatistically defined points along the cost spectrum.These points also are consistent with certain definedcosting approaches described in ASTM E2137-06(2011)—the mode, median, and mean of the datasetshown represent the Most Likely, More Likely thanNot, and Expected values, respectively. The arrows atthe bottom correspond to definitions used in variousU.S. accounting disclosure standards. These definitionsare not mathematically quantified, but are ratherdefined in accordance with a reporting entity’s auditedmanagement system. In addition to determining theappropriate ranges defining terms such as Possible,Probable, and Remote, a reporting entity must alsoconsider and define how concepts such as “reasonablyestimable” and “material” apply to its environmentalliabilities.

Choice of Estimation Approach—Implementation

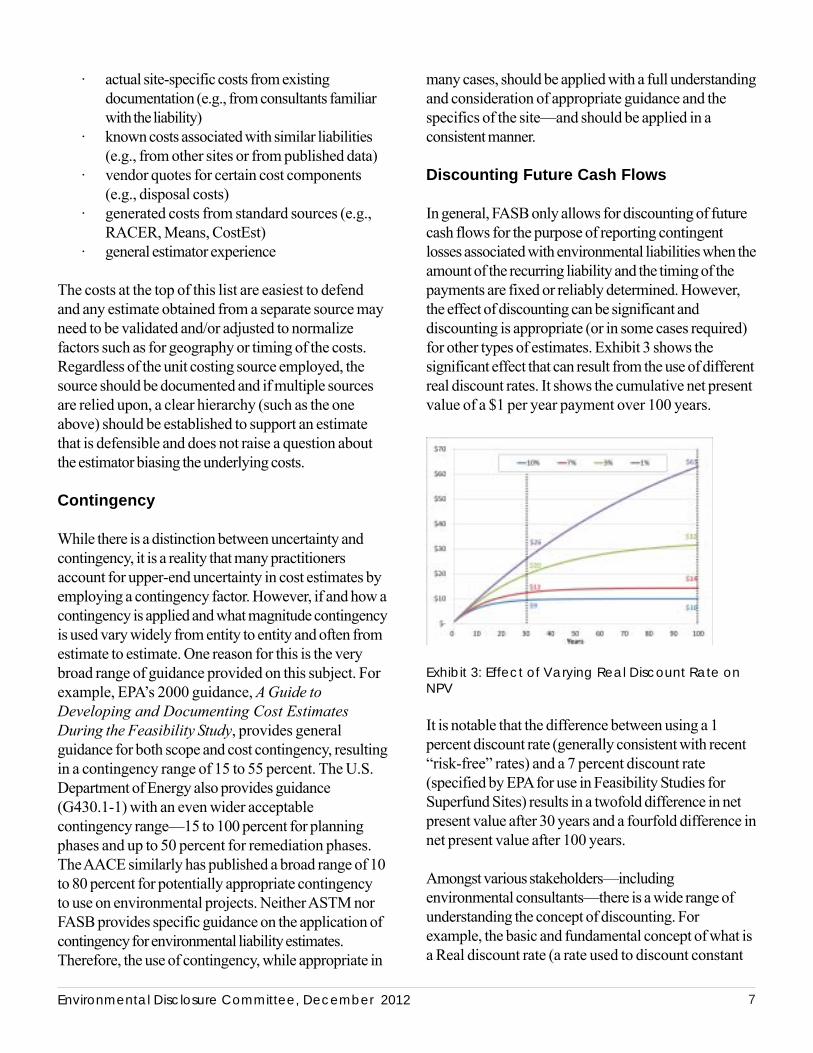

The core concepts of determining the appropriateestimation approach and understanding and addressingthe appropriate level of uncertainty go hand in hand asillustrated in the following diagram—as based on a

hierarchy of costing approaches described in ASTME2137-06 (2011) and shown in exhibit 2.

Exhibit 2: Hierarchy of Costing Approaches

Cost estimating approaches range from “No Estimate”(which in some cases may be a prudent option) to thegold standard of obtaining a Quoted Price—essentiallyan offer from an informed and willing marketparticipant to take the liability—such as via aninsurance product or a guaranteed fixed-priceremediation offer. As the estimates progress from thebottom to the top of the hierarchy, the estimatingapproach becomes more complete and robust,uncertainty is better addressed, and the estimatesprovide greater risk reduction and value added to theuser. The more complete/robust methodologies alsogenerally require more information in order toadequately prepare the estimates.

Traditionally, estimates used to support environmentalreserves for financial reporting are typicallyaccomplished using the Most Likely Value approach,to determine the cost of what is believed to be the costof the most probable outcome. In cases where theranges of outcomes are all equally probable, FASBfinancial reporting requirements allow (ASC 40-20—Reasonable Estimation of the Amount of a Loss) theentry to report the low end of the range—oftenestimated using the Known Minimum Value approach.

In certain cases, more robust estimates ofenvironmental liabilities are required. For example,requirements for valuation of contingent losses in the

6 Environmental Disclosure Committee, December 2012

context of business combinations (ASC 805) requirethe estimation of such costs at their Fair Value(potentially represented via a Quoted Price orExpected Value). The disclosure of “PollutionRemediation Obligations” by state and municipalgovernment entities (Government Accounting StandardBoard Financial Accounting Foundation 49) requiresthe reporting of the Expected Value of such liabilities.In addition, parallel requirements that apply to thequantification of environmental liabilities in the contextof International Financial Accounting Standards (IFAS)also require a more robust quantification ofenvironmental liabilities using either an Expected Valueapproach or a mid-point of a Range of Values(International Accounting Standard 37—Provisions,Contingent Liabilities and Contingent Assets).

Inherently, the most complex estimating approachesrequire greater knowledge and experience from theestimator, and more sophisticated tools for completion.For example, a single point estimate, such as a KnownMinimum Value, can be prepared with a simplespreadsheet or from an existing consultant estimate.More complex multi-point estimates, such as ExpectedValues, necessitate more complex tools such asspreadsheet models that incorporate stochasticsimulation methods, such as Monte Carlo analysis viaspecialized software tools (e.g., Palisade’s @Risk orOracle’s Crystal Ball).

All of these estimation techniques can draw unit costsfrom a variety of sources ranging from institutional/consultant expert knowledge to published sources likeunit cost books (e.g., those published by R.S. Means)or unit costs compiled and made available bygovernment agencies. There are also a number ofsoftware packages available that are intendedspecifically for environmental cost estimating, such asRACER (AECOM) and CostPro (EPA).

Items Included/Excluded

An estimate must consider and define what costs andliabilities are to be included and excluded. For thepurpose of a cost estimate in support of financialreporting, different categories of costs/liabilities areoften created for reporting under different reporting

requirements. For example, liabilities associated withremediation obligations from legacy or Superfundliabilities are typically handled as contingent losses(ASC 450), whereas closure or decommissioningrequirements, either expected from the start or arisingunexpectedly, are typically addressed as AROs(contingent or otherwise). As discussed above, thesedifferent categories of costs may require estimation andreporting in different ways. The inclusion of costs in aninappropriate category can have ramifications in theacceptability of the reported costs by auditors, as wellas have cascading effects on other businessconsiderations such as insurance coverage andpotential recoverability of costs under theComprehensive Environmental Response,Compensation, and Liability Act.

Uncertainty

Any estimate that attempts to predict the future hasinherent uncertainty, and variables like scientificinterpretation, evolution of technology, regulatoryenforcement, and public opinion only broaden therange of possible cost outcomes. Therefore, anyestimation approach must be developed andimplemented with an understanding of the acceptablelevel of uncertainty. In the case of ELV in support offinancial reporting, uncertainty is acknowledged andallowed within the regulatory framework. However,reporting entities are required to disclose instanceswhere uncertainty may represent contingent losses thatmay be material. Some reporting entities address thisby developing more robust estimates, such asExpected Values, which—by definition—incorporatethe likelihood and magnitude of a range of possibleoutcomes and costs. Other reporting entities provide asecond, reasonable worst-case cost (essentially anupper end of a Range of Cost approach) for certainsignificant liabilities.

Source of Unit Costs

Any consultant or expert preparing a defensible costestimate will need unit costs or cost components tobuild ELV. In general, the available categories of costsare as follows:

7Environmental Disclosure Committee, December 2012

· actual site-specific costs from existingdocumentation (e.g., from consultants familiarwith the liability)

· known costs associated with similar liabilities(e.g., from other sites or from published data)

· vendor quotes for certain cost components(e.g., disposal costs)

· generated costs from standard sources (e.g.,RACER, Means, CostEst)

· general estimator experience

The costs at the top of this list are easiest to defendand any estimate obtained from a separate source mayneed to be validated and/or adjusted to normalizefactors such as for geography or timing of the costs.Regardless of the unit costing source employed, thesource should be documented and if multiple sourcesare relied upon, a clear hierarchy (such as the oneabove) should be established to support an estimatethat is defensible and does not raise a question aboutthe estimator biasing the underlying costs.

Contingency

While there is a distinction between uncertainty andcontingency, it is a reality that many practitionersaccount for upper-end uncertainty in cost estimates byemploying a contingency factor. However, if and how acontingency is applied and what magnitude contingencyis used vary widely from entity to entity and often fromestimate to estimate. One reason for this is the verybroad range of guidance provided on this subject. Forexample, EPA’s 2000 guidance, A Guide toDeveloping and Documenting Cost EstimatesDuring the Feasibility Study, provides generalguidance for both scope and cost contingency, resultingin a contingency range of 15 to 55 percent. The U.S.Department of Energy also provides guidance(G430.1-1) with an even wider acceptablecontingency range—15 to 100 percent for planningphases and up to 50 percent for remediation phases.The AACE similarly has published a broad range of 10to 80 percent for potentially appropriate contingencyto use on environmental projects. Neither ASTM norFASB provides specific guidance on the application ofcontingency for environmental liability estimates.Therefore, the use of contingency, while appropriate in

many cases, should be applied with a full understandingand consideration of appropriate guidance and thespecifics of the site—and should be applied in aconsistent manner.

Discounting Future Cash Flows

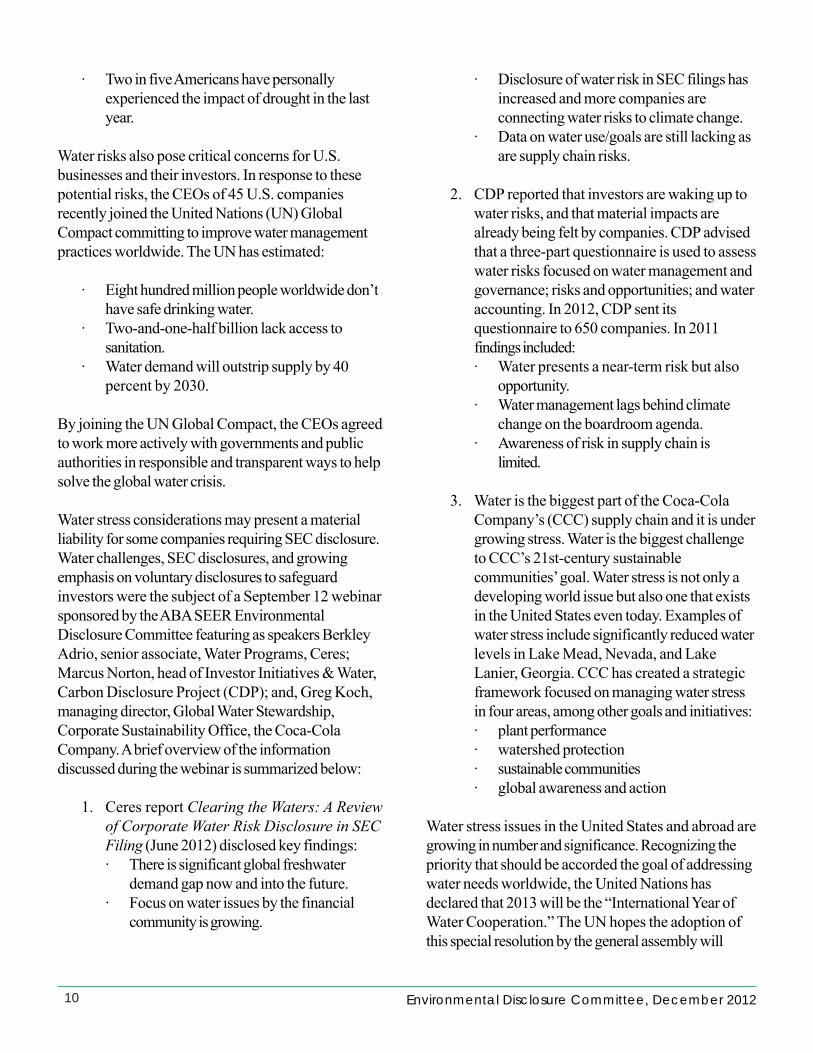

In general, FASB only allows for discounting of futurecash flows for the purpose of reporting contingentlosses associated with environmental liabilities when theamount of the recurring liability and the timing of thepayments are fixed or reliably determined. However,the effect of discounting can be significant anddiscounting is appropriate (or in some cases required)for other types of estimates. Exhibit 3 shows thesignificant effect that can result from the use of differentreal discount rates. It shows the cumulative net presentvalue of a $1 per year payment over 100 years.

Exhibit 3: Effect of Varying Real Discount Rate onNPV

It is notable that the difference between using a 1percent discount rate (generally consistent with recent“risk-free” rates) and a 7 percent discount rate(specified by EPA for use in Feasibility Studies forSuperfund Sites) results in a twofold difference in netpresent value after 30 years and a fourfold difference innet present value after 100 years.

Amongst various stakeholders—includingenvironmental consultants—there is a wide range ofunderstanding the concept of discounting. Forexample, the basic and fundamental concept of what isa Real discount rate (a rate used to discount constant

8 Environmental Disclosure Committee, December 2012

dollar cash flows) versus a Nominal discount rate (arate used to discount inflated future cash flows) is notwidely understood.

For these reasons, it is important that discounting andan appropriate discount rate be considered andapplied carefully. It is notable that, in accordance withEPA guidance, the use of a 7 percent discount rate iswidely used today. However, this convention wasestablished to allow for the comparison of differentestimates and it has not been updated to reflect thechanges in actual economic reality.

Future Trends

In the years since Sarbanes-Oxley in 2002, there havebeen incremental changes to the manner in whichentities must report their environmental liabilities. FASBInterpretation Notice No. 47 in 2005 solidifiedrequirements associated with accounting for conditionalAROs. In 2007, the revised FASB Statement No.141clarified reporting requirements associated with“business combinations,” including that losscontingencies must be reported at their fair value whenpossible. FASB progressed to two Exposure Drafts onits project to consider expanding loss contingencydisclosure and reporting requirements under ASC 450.However, in 2012, FASB voted to end this projectand not accept changes considered in the ExposureDrafts.

The framework for financial reporting in the UnitedStates appears to have stabilized for the time being.However, some reporting entities are moving to morerobust approaches for valuing their environmentalliabilities. As discussed earlier, reasons for this moverange from business combinations to internationalaccounting standard drivers to more macro-leveldrivers for better measurement and corporatetransparency. As a result, we have observed thefollowing trends and changes in the way thatenvironmental consultants are asked to supportfinancial reporting processes:

· more robust estimate approaches, such asExpected Value estimates that reflect multiplecost outcomes

· estimates being accomplished by environmentalexperts or consultants with input from reportingentities, legal, accounting, and riskmanagement personnel

· estimates that consider assets and liabilitiestogether and that include a broader range ofliabilities, such those associated with carbonemissions and other life-cycle costconsiderations

· the general application of more advancedfinancial analytical tools, such as tail riskanalysis, real options valuation, synthetic fairvalue, and customized discounting strategies, toassess environmental liability

Reporting entities should continue to be attentive to thecurrent state of the practice in environmental liabilitycost estimation. In some cases, more thorough analysismay be required to comply with applicable standards.In all cases, more thorough analysis can yield moreaccurate and defensible estimates and potentially justifylower environmental reserve accruals.

Useful References

The following references provide additional informationrelevant to ELV and may be helpful in consideringapproaches and methodologies to estimateenvironmental liabilities in the context of financialreporting requirements:

· AACE. Total Cost ManagementFramework. Accessible at http://www.aacei.org/resources/tcm.

· American Institute of Certified PublicAccountants, Inc. 1996. ACC Section 10,680,Statement of Position 96-1 EnvironmentalRemediation Liabilities, October 10.

· ASTM International. 2011. E2173-07 (2011),Standard Guide for Disclosure ofEnvironmental Liabilities. Available forpurchase from ASTM at http://www.astm.org/Standards/E2173.htm.

· ASTM International. 2011. E2137-06 (2011),Standard Guide for Estimating MonetaryCosts and Liabilities for EnvironmentalMatters. Available for purchase from ASTMat http://www.astm.org/Standards/E2137.htm.

9Environmental Disclosure Committee, December 2012

· FASB. Accounting Standards Codification.Available at https://asc.fasb.org (loginrequired).

· Government Accounting Standards Board.2006. Summary of Statement No. 49:Accounting and Financial Reporting forPollution Remediation Obligations (Issued11/06). Available at http://www.gasb.org/st/summary/gstsm49.html.

· International Accounting Standards Board.2012. Technical Summary on InternationalAccounting Standard 37 Provisions,Contingent Liabilities and ContingentAssets. http://www.ifrs.org/IFRSs/Documents/English%20IAS%20and%20IFRS%20PDFs%202012/IAS%2037.pdf.

· USEPA. 2000. A Guide to Developing andDocumenting Cost Estimates During theFeasibility Study. EPA 540-R-00-002,OSWER 9355.0-75. July. Available at http://www.epa.gov/superfund/policy/remedy/sfremedy/rifs/costest.htm.

· U.S. Department of Defense. 2006.Environmental Liabilities Best Practices Guide.May. Available at http://www.acq.osd.mil/pepolicy/pdfs/Environmental%20Liabilities%20Best%20Practices%20Guide_Final.pdf.

· U.S. Department of Energy. Guidance 430.1Series. Relevant chapters available at https://www.directives.doe.gov/directives/current-directives/directives-current-400-series.

Michael Berman and Paul Brookner are seniorpractitioners with Geosyntec Consultants. Theyprovide expert support to legal, industry, andgovernment clients on projects involving theevaluation, quantification, and mitigation ofenvironmental remediation liabilities. They can bereached at [email protected] [email protected], respectively.

WATER-RELATED RISKS AND OPPORTUNITIESUPDATEE. Lynn GraysonJenner & Block

In late November 2012, major U.S. newspaperscarried headlines about a possible halt of barge trafficon the Mississippi River resulting from a significantdrop in water levels caused by this year’s droughtconditions. Barges already are required to carry lighterloads due to historic river lows between St. Louis,Missouri, and Cairo, Illinois. Governors of states alongthe Mississippi River, members of Congress, and rivershipping trade groups have asked President Obama tointervene in managing water flows from tributarywaterways to avoid “disastrous economicconsequences . . .” for barge operators and those whoship on the Mississippi River.

News about water-related problems is on the rise asare growing concerns about how to manage waterneeds now and in the future. Many believe that waterscarcity may be emerging as the most significantconsequence of climate change. In August 2012, anORC International report for the Civil Society Institute,Drought, Water and Energy—A National Survey ofAttitudes, provided some interesting insights into howAmericans viewed water concerns:

· Americans are worried about drought andwant to see clean drinking water get a highernational priority.

· Two-thirds of Americans now think climatechange is “real” or “appears to be happening.”

· Four out of five Americans are concernedabout increased drought, wildfires, andextreme weather events.

· Nearly two-thirds of Americans are veryconcerned about possible shortages of safedrinking water.

· Four out of five Americans believe theavailability of ample clean water should be atop national priority for the United States.

10 Environmental Disclosure Committee, December 2012

· Two in five Americans have personallyexperienced the impact of drought in the lastyear.

Water risks also pose critical concerns for U.S.businesses and their investors. In response to thesepotential risks, the CEOs of 45 U.S. companiesrecently joined the United Nations (UN) GlobalCompact committing to improve water managementpractices worldwide. The UN has estimated:

· Eight hundred million people worldwide don’thave safe drinking water.

· Two-and-one-half billion lack access tosanitation.

· Water demand will outstrip supply by 40percent by 2030.

By joining the UN Global Compact, the CEOs agreedto work more actively with governments and publicauthorities in responsible and transparent ways to helpsolve the global water crisis.

Water stress considerations may present a materialliability for some companies requiring SEC disclosure.Water challenges, SEC disclosures, and growingemphasis on voluntary disclosures to safeguardinvestors were the subject of a September 12 webinarsponsored by the ABA SEER EnvironmentalDisclosure Committee featuring as speakers BerkleyAdrio, senior associate, Water Programs, Ceres;Marcus Norton, head of Investor Initiatives & Water,Carbon Disclosure Project (CDP); and, Greg Koch,managing director, Global Water Stewardship,Corporate Sustainability Office, the Coca-ColaCompany. A brief overview of the informationdiscussed during the webinar is summarized below:

1. Ceres report Clearing the Waters: A Reviewof Corporate Water Risk Disclosure in SECFiling (June 2012) disclosed key findings:· There is significant global freshwater

demand gap now and into the future.· Focus on water issues by the financial

community is growing.

· Disclosure of water risk in SEC filings hasincreased and more companies areconnecting water risks to climate change.

· Data on water use/goals are still lacking asare supply chain risks.

2. CDP reported that investors are waking up towater risks, and that material impacts arealready being felt by companies. CDP advisedthat a three-part questionnaire is used to assesswater risks focused on water management andgovernance; risks and opportunities; and wateraccounting. In 2012, CDP sent itsquestionnaire to 650 companies. In 2011findings included:· Water presents a near-term risk but also

opportunity.· Water management lags behind climate

change on the boardroom agenda.· Awareness of risk in supply chain is

limited.

3. Water is the biggest part of the Coca-ColaCompany’s (CCC) supply chain and it is undergrowing stress. Water is the biggest challengeto CCC’s 21st-century sustainablecommunities’ goal. Water stress is not only adeveloping world issue but also one that existsin the United States even today. Examples ofwater stress include significantly reduced waterlevels in Lake Mead, Nevada, and LakeLanier, Georgia. CCC has created a strategicframework focused on managing water stressin four areas, among other goals and initiatives:· plant performance· watershed protection· sustainable communities· global awareness and action

Water stress issues in the United States and abroad aregrowing in number and significance. Recognizing thepriority that should be accorded the goal of addressingwater needs worldwide, the United Nations hasdeclared that 2013 will be the “International Year ofWater Cooperation.” The UN hopes the adoption ofthis special resolution by the general assembly will

11Environmental Disclosure Committee, December 2012

serve as a platform to increase people’s awareness ofwater-related problems and promote action on waysto solve them. More information about the InternationalYear of Water Cooperation and the work of UN-Water is available at http://www.unwater.org/.

Increased scrutiny on water stress concerns shouldencourage companies to assess current and futurewater demands. In doing so, companies will betterunderstand the materiality of water and related risks totheir business. Investors and the organizations thatrepresent them want to know more and more aboutthe impact of water risks on company operations andoverall financial performance. Whether necessitated bythe Securities and Exchange Commission or voluntary,companies can expect more inquiries from investorsand shareholders about water stress concerns andmore demands for reporting and disclosure.

E. Lynn Grayson is a partner at Jenner & Block inChicago and cochair of the firm’s Environmentaland Workplace Health and Safety Practice Group.She is a member of the Environmental DisclosureCommittee and moderated the ABA’s September12 webinar on water risks.

HOW INCORPORATION OF IFRS INTO USFINANCIAL REPORTING STANDARDS MAYAFFECT THE REPORTING OF ENVIRONMENTALLIABILITIESBrian Henthorn and Lisa Walsh

Summary

In 2000, the United States Securities and ExchangeCommission (SEC) began exploring possibleconvergence of domestic and international accountingstandards (International Financial Reporting Standards,or IFRS). Its goal was to create a single set of high-quality global accounting standards. In July 2012, afteryears of study, the SEC issued a final staff report whichdiscussed some of the implications of incorporatingIFRS into the U.S. financial reporting system; however,the staff report did not provide SEC endorsement ofan incorporation plan, or a timetable for if and whensuch an endorsement or decision would be reached.

Much has been written about the history and currentstatus of these incorporation efforts, as well as whatthe future may hold; however, these articles have notfocused explicitly on the effect of IFRS incorporation,if and when it occurs, on the financial reporting ofenvironmental liabilities. This article provides a verybrief overview of the status of IFRS incorporationefforts, and then focuses on how an SEC decision toendorse or reject incorporation could affect thereporting of environmental liabilities. This article alsoexamines independent efforts to update the U.S. andinternational accounting standards governingenvironmental liabilities, and implications for U.S.companies.

Our findings suggest that no significant changes in therequirements governing reporting of environmentalliabilities will occur in the United States for at leastseveral years, whether IFRS incorporation is endorsedor not, due to the delays in incorporation andcompletion of independent projects to update domesticstandards and IFRS. Ultimately, however, we believethe SEC will either reject or endorse incorporationwith the following potential consequences:

12 Environmental Disclosure Committee, December 2012

· If the SEC ultimately rejectsincorporation—the reporting of environmentalliabilities in the US would remain unchanged inthe short term; however, domestic efforts toimprove disclosure of environmental liabilitiesin U.S. financial statements may affect howthese liabilities are disclosed in the long term.

· If the SEC decides to endorseincorporation—IFRS will likely become thegoverning standard for the reporting ofenvironmental liabilities in the United States.Incorporation could result in significant changesto how companies report their environmentalliabilities. The SEC has indicated that achievingincorporation may take several years,particularly in areas such as reportingenvironmental liabilities where there aresubstantive differences between U.S. andinternational reporting standards. Additionally,an independent project being undertaken in theUnited Kingdom to update the IFRS onenvironmental liabilities should also bemonitored, as any changes to the IFRS couldaffect US companies should incorporationoccur.

A Brief History of IFRS Incorporation Efforts

For the last 12 years, the SEC has been exploringpossible convergence of domestic and internationalaccounting standards in order to create a single set ofhigh-quality global accounting standards. See SEC,February 24, 2010, Commission Statement in Supportof Convergence and Global Accounting Standards, p.4 (SEC 2010 Statement). Efforts began in earnest in2002 as the domestic (Financial Accounting StandardsBoard or FASB) and international (InternationalAccounting Standards Board or IASB) accountingboards signed a memorandum of understanding (MoU)to collaborate on the development of commonreporting standards. See SEC, July 13, 2012, WorkPlan for the Consideration of Incorporating IFRS intothe Financial Reporting System for U.S. Issuers, FinalStaff Report, p. 10 (SEC 2012 Report).

While the two accounting boards continued theirefforts to develop common standards in specific areas

through the MoU and other joint projects, inNovember 2008 the SEC issued a proposed roadmapto the broader incorporation of international financialreporting standards (IFRS) into U.S. reportingstandards (Roadmap). Specifically, this Roadmapsought to examine the implications of replacing ormerging the domestic financial reporting standards(Generally Accepted Accounting Principles, or GAAP)with IFRS. The Roadmap also provided support forIFRS, stating that “…the IFRS has the potential tobest provide the common platform on whichcompanies can report and investors can comparefinancial information.” See SEC, Nov. 14, 2008,Roadmap for the Potential Use of Financial StatementsPrepared in Accordance with IFRS by U.S. Issuers,pp. 9-11 (SEC 2008 Roadmap).

Momentum toward incorporation of IFRS into USreporting standards began to build in 2010 when theSEC issued a work plan to examine issues raised bycommenters to the 2008 Roadmap (Work Plan). TheWork Plan also was designed to identify IFRSincorporation issues that would be researched by theSEC, and pave the way for the SEC to decidewhether, when, and how to incorporate IFRS. Thisdecision was anticipated in 2011. If the SEC decidedin 2011 to transition U.S. GAAP toward IFRS, thefirst year under a new accounting system wasprojected to be 2015 or 2016, allowing for a four tofive year transition period for U.S. companies to adjustto the new standards. See SEC 2010 Statement, p. 2.See Also SEC, February 2010, Work Plan for theConsideration of Incorporating IFRS into the FinancialReporting System for U.S. Issuers, pp. 1-3 (SEC2010 Work Plan).

However, the SEC did not make its decision in 2011.Rather, in July 2012 the SEC staff issued a final reporton the issues identified in the 2010 Work Plan; thisreport further summarized the staff’s findings on theimplications of incorporating IFRS in the United States,but did not express any policy recommendation by theSEC staff as to whether IFRS should be incorporatedinto U.S .financial reporting requirements. See SEC2012 Report, Introductory Note. Just as importantly,the final report did not specify next steps toward a

13Environmental Disclosure Committee, December 2012

decision, and did not indicate when such a decisioncould be reached.

Whereas in 2011 it appeared that the incorporation ofIFRS into U.S. financial reporting was forthcoming, thelack of a SEC endorsement as of November 2012raises questions about if and when IFRS will come tothe United States. This article examines the implicationsfor U.S. companies depending on the SEC’s decisionon incorporation, specifically with regard to thefinancial reporting of environmental liabilities.

If the SEC Endorses Incorporation of IFRS

Although the SEC has not yet endorsed a specificcourse of action regarding incorporation, if the SECultimately endorses the incorporation of IFRS, this willhave varying implications for U.S. companies. Whilethe exact method of incorporation is still uncertain atthis time (endorsement, convergence, and“condorsement” are all approaches the SEC hasexamined), the end result is that U.S. companies willneed to be prepared to adopt international accountingstandards for their financial reporting. See SEC, May26, 2011, Exploring a Possible Method ofIncorporation, pp. 5-7. Condorsement is a hybridapproach that shares characteristics of both theendorsement approach (incorporating individual IFRSsinto domestic standards directly) and the convergenceapproach (maintaining domestic standards butconverging those standards to more closely align withIRFS). The condorsement approach would allow theUnited States to remain the standard setter fordomestic standards, and also provide a transitionperiod for individual standards to be converged, suchthat eventually compliance in GAAP would alsorepresent compliance with IFRS.

For many areas where U.S. GAAP and IFRS arealready similar, or where joint projects under the MoUhave converged the standards, this transition will berelatively straightforward. Contingent andenvironmental liabilities, however, have fundamentaldifferences between U.S. GAAP and IFRS. See SEC2012 Report, pp. 14-15.

Key Differences Between IFRS and USGAAP Governing the Reporting ofEnvironmental Liabilities

The first major difference between IFRS and U.S.GAAP treatment of environmental liabilities for financialreporting purposes is the threshold under which aliability is recognized. Both standards (FASBAccounting Standards Codification–Topic 450(Contingencies), or ASC 450 and InternationalAccounting Standard 37–Provisions, ContingentLiabilities and Contingent Assets, or IAS 37) use theterm “probable”; however each standard defines thatterm differently. Under U.S. GAAP, probable isdefined as when an “event or events are likely tooccur.” See ASC 450-20-20. Interpretations of what“likely” means may vary; however the AmericanInstitute of Certified Public Accountants (AICPA)states that it is “typically interpreted to mean about80%.” See AICPA Website, IFRS for SMEs–U.S.GAAP Comparison Wiki, http://wiki.ifrs.com/Provisions-and-Contingencies (AICPA Website).IFRS, on the other hand, defines probable as “morelikely than not,” which would mean any likelihoodabove 50 percent. See IAS 37, p. A1016. See AlsoSEC, Nov. 16, 2011, A Comparison of U.S. GAAPand IFRS, p. 30.

Another major difference between IFRS and USGAAP is in the measurement of a liability within arange. U.S. GAAP requires the measurement to be anentity’s best estimate, or if no amount within a range isbetter than any other estimate, the minimum of thatrange. See ASC 450-20-30-1. IFRS requires that theestimate should be “the amount that an entity wouldrationally pay to settle or transfer the obligation …”Uncertainties in the estimate should be measured byusing an expected value or mid-point of the range,depending on the specific circumstances. See IAS 37,p. A1018.

Finally, one other major difference is in themeasurement of a liability with regard to timing. U.S.GAAP requires that the measurement should be the

14 Environmental Disclosure Committee, December 2012

cost of performing the remediation “when it is expectedto be performed” (i.e., undiscounted). See AICPAWebsite. IFRS requires that liabilities be discounted tocalculate a net present value. See IAS 37, p. A1020.

Impact of Key Differences

The above—and other differences—can result in largechanges in environmental accruals if a company musttransition from U.S. GAAP to IFRS. Specifically, withregard to recognition of a loss, U.S. GAAP uses ahigher threshold (approx. 80 percent) than IFRS(greater than 50 percent); the impact is that liabilitieswill be recognized earlier under IFRS than under U.S.GAAP. See SEC 2012 Report, p. 15.

Additionally, with regard to the measurement of a loss,the amount recognized under IFRS is likely to behigher than that under U.S. GAAP, especially whenuncertainty is involved. This is because U.S. GAAPallows one to accrue the minimum of a range if noestimate within the range is better than another; IFRSrequires that “all possible” outcomes be considered incalculating an expected value or mid-point of therange. See IAS 37, p. A1018. Thus, by definition,estimates prepared under IFRS would consider high-cost, low-probability outcomes as well as the minimumcost outcome. Moreover, whereas U.S. GAAPrequires the development of one estimate (theminimum), under IFRS in order to calculate anexpected value or mid-point, a range of estimates mustbe prepared.

In an interview with Accounting Today in September2012, FASB ChairLeslie Seidman discussed some ofthe hurdles that had arisen which made universaladoption of IFRS problematic and unlikely, one ofwhich was the differences in the accounting ofenvironmental liabilities:

So, it means there has to be some sort of atransition plan for those cases where we havegaps in IFRS, if you will, and then the othercases where there might be concerns about theconsistency of application of IFRS in aparticular area, or cases where we think thatthere are problems with applying an existing

IFRS standard in the US environment; such as,for example, the accounting for contingencies,where we’ve heard widespread concern aboutusing an expected value type approach in theUS environment.

See Accounting Today TV, Sept. 6, 2012, Interviewwith FASB Chair Leslie Seidman on Convergence withIFRS.

Increases in the measurement of environmentalliabilities under IFRS may be offset to some extent bythe requirement to discount the liabilities to account forthe time value of money.

Whether or not the reduction from calculating a presentvalue offsets the increase from using the expected valuemethodology depends on the specific circumstancessurrounding the uncertainty of the response action andthe associated cash flows of the liability beingmeasured.

Other Potential Changes to the IFRSGoverning the Reporting of EnvironmentalLiabilities

In addition to the global IFRS incorporation efforts, theIASB has been in the process of updating the IFRSgoverning environmental liabilities (IAS 37: Provisions,Contingent Liabilities, and Contingent Assets) since2005. Should this update be completed prior toincorporation of IFRS in the United States, anychanges to IFRS proposed in the update wouldbecome applicable to U.S. companies afterincorporation is completed.

Updating IAS 37 began in June 2005, when the IASBissued its first exposure draft. Two of the primary goalsof the IAS 37 update were to address inconsistencieswith other IFRSs, and to improve the measurement ofliabilities. See IASB, January 2010, Exposure DraftSnapshot: IAS 37 Replacement, p. 2. With regard tothe inconsistencies with other standards, IASBproposed to remove the probable (more likely thannot) threshold from IAS 37, as it was not used in otherstandards, and it was deemed to be unnecessary if anexpected value approach to measurement was used.

15Environmental Disclosure Committee, December 2012

With regard to the measurement of liabilities, the boardproposed to specify that an expected value orexpected cash flow approach should be always usedto measure an environmental liability. See IASB, June2005, Exposure Draft of Proposed Amendments toIAS 37 Provisions, Contingent Liabilities andContingent Assets and IAS 19 Employee Benefits, pp.15-16. See also IASB, September 2010, Staff Paper:Liabilities–IFRS to replace IAS 37, p. 10 (2010 IASBStaff Paper).

Commenters to the first exposure draft issued in 2005voiced concerns about the changes to the measurementof liabilities, and as a result, the draft was revised inJanuary 2010 with additional guidance specifyingprecisely what entities should measure, and how theyshould achieve that aim. Specifically, the revisionsnoted that the expected value calculation should bebased on contractor prices, and include a riskpremium. See IASB, January 2010, Exposure Draft:Measurement of Liabilities in IAS 37, p. 5. See Also2010 IASB Staff Paper, p. 4.

Further comments were received in 2010, some ofwhich included opposition to some of the proposedchanges, specifically with regard to the use of expectedvalue, measurement of contractor prices, and judgmentabout whether a liability exists. As a result, inNovember 2010 IASB proposed to reverse itschanges on the recognition threshold, and keep theprobable (more likely than not) threshold. See IASBStaff Paper, pp. 10–14. See also IASB, November2010, Staff Paper: Liabilities–IFRS to Replace IAS37, Recognition Criteria–Threshold for “LiabilityExists” Criterion, p. 6. IASB did not addresscommenters’ concerns regarding expected value orthe use of contractor prices.

Before any revisions could be made to IASB’sexposure draft, the update project was paused andstaff was transferred to work on higher priorityprojects. See IASB and FASB, Nov. 29, 2010,Progress Report on Commitment to Convergence ofAccounting Standards and a Single Set of High QualityGlobal Accounting Standards, p. 2. The IFRS websitefor the project indicates that it has been on hold since

January 2011 pending ongoing deliberations about theIASB future work plan. See IFRS Website, Jan. 26,2011, Liabilities–Amendments to IAS 37 (Paused),http://www.ifrs.org/Current-Projects/IASB-Projects/Liabilities/Pages/Liabilities.aspx.

Timing of IFRS Incorporation for U.S.Companies

In its February 2010 Work Plan, the SEC estimatedthat a transition to incorporate IFRS in the US wouldtake approximately four to five years. See SEC 2010Work Plan, pp. 1–3. As of November 2012, nodecision had been reached by the SEC. It appearsunlikely that any decision will be reached until 2013 atthe earliest. Furthermore, the four to five year transitionperiod may be an underestimate for certain standards.The July 2012 final report by SEC staff noted that forstandards with fundamental differences between U.S.GAAP and IFRS (such as environmental liabilities) itmay be difficult to resolve those differences even withinfive to seven years. See SEC 2012 Report, p. 14. Thistime frame does not account for the independent effortto update IAS 37. While this effort is currently paused,should efforts resume this may also prolong the timeperiod necessary to converge the standards governingthe reporting of environmental liabilities.

If the SEC decides to endorse incorporation ofIFRS in 2013, the effects of incorporation areunlikely to be felt by U.S. companies for severalyears. A prudent long-term strategy for companiesis to closely monitor any decisions from the SECthat may affect the timing of incorporation, as wellas monitor any potential changes to IAS 37.

If the SEC Rejects Incorporation of IFRS

Companies which currently have or may have in thefuture an international presence should continue tomonitor developments in IFRS. If the SEC decides toreject incorporation of IFRS into U.S. GAAPstandards, U.S. companies will not have to considerthe implications of IFRS on their domestic reporting ofenvironmental liabilities. However, for companies thathave international operations, there may still berequirements to file separate financial statements

16 Environmental Disclosure Committee, December 2012

domestically under U.S. GAAP, and internationallyunder IFRS.

Changes to the U.S. GAAP StandardGoverning the Reporting of EnvironmentalLiabilities

Even for those companies which solely operate in theUS, a decision to reject incorporation of IFRS doesnot mean that no changes will be made to domesticaccounting standards. Separate from the global IFRSincorporation efforts, since 2008 the FASB has been inthe process of updating the U.S. GAAP standardgoverning reporting of environmental liabilities. As of2008, this was the Statement of Financial AccountingStandards No. 5 (FAS 5): Accounting forContingencies; however, FAS 5 was subsequentlycodified in 2009 as FASB Accounting Standards(ASC) Topic 450 (Contingencies).

In 2008, FASB issued an exposure draft on theDisclosure of Certain Loss Contingencies, intended toamend the existing FAS 5. The amendment wouldexpand the disclosures of certain loss contingenciesincluding environmental liabilities. Specific changesanticipated in the exposure draft included requiringmore quantitative and qualitative information aboutdisclosures, tracking changes in disclosures over time,and requiring disclosures for liabilities whose likelihoodwas believed to be remote if they would be expectedto result in a material loss. See FASB, June 5, 2008,Exposure Draft–Disclosure of Certain LossContingencies, pp. v-vi.

Based on opposition expressed in comments to theexposure draft, largely from the legal profession, theexposure draft was withdrawn. In July 2010, a newexposure draft was issued, with some changes from the2008 version to address the commenters’ concerns.One of the objectives of the exposure draft was tomake the disclosures under U.S. GAAP similar tothose required by IAS 37 under IFRS. See FASB,August 2010, FASB In Focus–Proposed AccountingStandards Update: Disclosures of Certain LossContingencies, p. 1. See Also FASB, July 20, 2010,Exposure Draft–Contingencies (Topic 450), p. 3(2010 FASB Exposure Draft).

If the exposure draft had been finalized as re-issued,the guidance would have become effective inDecember 2010. See 2010 FASB Exposure Draft, p.46. However, commenters continued to expressopposition to the revised draft. In particular,commenter opposition focused on the possibility thatenhanced disclosures could be prejudicial to thereporting entity. Furthermore, some commentersbelieved that disclosures could be improved byenforcing compliance with the existing standards, ratherthan changing the existing standards. See FASB, July9, 2012, Board Meeting Handout: Disclosure ofCertain Loss Contingencies, p. 1 (2012 FASBHandout). As a result, the exposure draft was notfinalized in December 2010.

In July 2012, a FASB board meeting was held todiscuss the project objectives and determine nextsteps. The board noted that feedback received on boththe 2008 and 2010 exposure drafts wasoverwhelmingly negative. See 2012 FASB Handout, p.1. As a result, FASB voted to discontinue the project.See FASB, July 12, 2012, Minutes of the July 9, 2012Board Meeting: Disclosure of Certain LossContingencies, p. 2. According toFASB Chair LeslieSeidman:

Based on feedback received from a wide rangeof constituents on two exposure drafts over aperiod of four years, the board concluded thatexisting loss contingency disclosurerequirements are adequate. As a result of theincreased scrutiny of loss contingencydisclosures in recent years, the board concludedthat improvements to financial reporting aremore likely to be achieved through robustcompliance than through additional standardsetting.

Changes to the U.S. GAAP Standard onDisclosures

While the project to update disclosure requirements forenvironmental liabilities was terminated, anotherseparate project continued whose purpose is to updatedisclosures across financial statements as a whole (notsolely limited to environmental liabilities). Specifically,in July 2012, FASB issued a discussion paper on

17Environmental Disclosure Committee, December 2012

improving the effectiveness of disclosures in notes tofinancial statements. This discussion paper included anumber of proposals to improve disclosures, many ofwhich were previously discussed in the rejectedexposure draft for environmental liabilities. See FASB,July 12, 2012, Discussion Paper–DisclosureFramework, p. 1 (2012 FASB Discussion Paper).

For example, the discussion paper noted that FASBshould consider requiring companies to track changesin disclosures over time, and detail the reason for thesechanges. The discussion paper also noted that indetermining whether to disclose a liability, a looseapproximation of the probability-weighted value shouldbe used to assess materiality. Furthermore, liabilitieswhose likelihood is believed to be remote but is of highmagnitude would require disclosure. See 2012 FASBDiscussion Paper, pp. 23, 48.

Due to the early stage of this general disclosure project(comments on the discussion paper are due in mid-November 2012), it is too soon to tell whether theproposed revisions to disclosures will be retained ormodified in future drafts, and if and when thoserevisions would go into effect. At a minimum, it isunlikely that there will be any changes to disclosurerequirements for at least a year. Given the large numberof comments expressed on the proposed (andultimately rejected) update to FAS 5 and ASC 450,which contained many of the same changes as thedisclosure discussion paper, it should not be surprisingif there are substantive concerns expressed to thebroader discussion paper on disclosures as well. As aresult, it could take several years to finalize an updateto disclosure requirements and satisfy commenters’concerns.

Conclusion

Unlike last year, when an SEC decision to endorseIFRS incorporation appeared imminent, and whenupdates to domestic and international accounting ofenvironmental liabilities were proceeding alongseparate but parallel tracks, it now appears unlikelythat there will be any changes required as to how U.S.companies report environmental liabilities within thenext several years. While updates to domestic andinternational standards on environmental liabilities have

been paused or ceased, this does not preclude therestarting of these projects in the future, or in the caseof domestic standards, the issuance of reviseddisclosure standards for financial statements in general.Furthermore, unlike the IFRS incorporation effortswhere it is expected that companies will have multipleyears to transition to IFRS, updates to domesticstandards could be implemented relatively quicklyfollowing standard finalization.

Many reasons remain for companies to continue tomonitor developments in the United States and abroadand to evaluate the implications of incorporating certainindividual IFRSs into U.S. reporting, including thereporting of environmental liabilities. Specifically, ascompanies grow globally, they may be subject toIFRS. Also, companies with non-U.S. subsidiaries,stakeholders and vendors must remain aware ofchanges to domestic and international standards.Understanding the evolution of these standards willhelp companies minimize the impact of reporting underdifferent accounting standards across the globe. Finally,it is critical to involve securities counsel in the reviewand proper implementation of these evolving standards.

While more uncertain than it was a year ago, someincorporation of IFRS into U.S. financial reporting stillappears likely. Companies that proactively considerand analyze the impacts of incorporation (specificallyfor areas with major differences in the standards, suchas reporting environmental liabilities) will be betterpositioned to adopt new standards with minimumdisruption should incorporation occur.

Brian Henthorn is a senior consultant at GnarusAdvisors LLC ([email protected]). LisaWalsh is a director at Gnarus Advisors LLC([email protected]). Mr. Henthorn and Ms.Walsh provide expertise in the valuation ofenvironmental liabilities in multiple contexts,including financial reporting, restructuring/bankruptcy, risk transfer, and strategicmanagement.

The opinions express are those of the authors and donot necessarily reflect the views of the firm or itsclients. This article is for general informationpurposes and is not intended to be and should notbe taken as legal advice.

18 Environmental Disclosure Committee, December 2012

UNCOVERING THE MYSTERY OF MATERIALITYIN TODAY’S MARKETJerome Lavigne-Delville, J.D., andJean Rogers, Ph.D.

On October 4, 2012, the Sustainability AccountingStandards Board (SASB) was officially launched inSan Francisco, with the goal of developing and publiclydistributing comprehensive, industry-specificsustainability accounting standards for companies,investors, and the public. To understand thesignificance of this mission requires a closer look at theevolution of corporate disclosure in the United States,the challenges that have necessitated this new set ofstandards, and the multi-stakeholder benefits ofmandating sustainability disclosure. A recent whitepaper entitled On Materiality and Sustainability:The Value of Disclosure in the Capital Markets,released by the Initiative for Responsible Investment atHarvard University, offers a clear and compellingargument for incorporating material, non-financialissues in corporate reporting, as well as methods toidentify and monitor these issues.

The paper further elaborates on a 2010 white paperentitled From Transparency to Performance:Industry-Based Sustainability Reporting on KeyIssues, also published by the Initiative for ResponsibleInvestments, which presented a framework for howindustry-based Key Performance Indicators (KPIs)could be developed. In proposing a mandated systemof KPIs, authors Steve Lydenberg, Jean Rogers, andDavid Wood sought to create guidance that wasrelevant to the core operations of a business. Citing theneed for standard, mandated KPIs, the authors wrote:“As an increasing number of governments and stockexchanges encourage or require sustainabilityreporting, corporations and financial markets in theUnited States run the risk of diminishing theircompetitiveness in sustainability. This data could becrucial in aligning business practices with those of asustainable economy and in providing a means forbenchmarking the performance of large corporationsas they interact with society and the environment.”

History of Corporate Disclosure

As a result of the Securities Exchange Act of 1934,Congress created the Securities and ExchangeCommission (SEC), a new federal agency chargedwith market oversight. Congress empowered thisagency to both require corporate disclosure for the firsttime, and oversee that disclosure. The need for bothwas evident in the wake of the 1929 stock marketcrash and the Great Depression, which shook publictrust and investors’ confidence in the financial market.By mandating this disclosure, Congress aimed toassure fair and honest markets, reliable prices, andunencumbered interstate commerce. The exactinformation required for corporate disclosure,however, was (and has been) left to interpretation, forthe most part. The courts and the SEC have “generallydefined information sufficiently ‘material’ to requirereporting as information that would be useful to‘reasonable’ investors considering a ‘total mix’ ofinformation in their decision making,” according toMateriality and Sustainability.

At the time, many, including the SEC, interpreted thismandate to include reporting on corporate financials,and did not consider sustainability data, or ESG(environmental, social, and governance) as part ofrequired reporting. For many years, reports on thefinancial conditions of publicly traded corporationswere indeed sufficient to assure trust in the companiesand the financial markets on which their stocks weretraded.

In 1973, the SEC created the Financial AccountingStandards Board (FASB), an accounting oversightbody to ensure that financial reporting was trustworthy,on the recommendation of the Wheat Committeethrough its 1972 “Report of the Study onEstablishment of Accounting Principles.” Francis M.Wheat, an attorney and former commissioner of theSecurities and Exchange Commission, chaired theseven-member study group.

By requiring the transparent disclosure of materialissues to investors, the U.S. financial accounting systemplays a fundamental role in making our markets themost efficient, liquid, and resilient in the world.However, the construct for standardized financial

19Environmental Disclosure Committee, December 2012

reporting to investors was developed in a time when acompany’s ability to create value was constrainedlargely by the ability to access financial capital.

The Growing Demand for SustainabilityData

Today’s market faces new and different challengesfrom that of 1934, when the SEC was created, or even1973, when FASB was formed. Since then, companieshave been operating in a much more globalenvironment, facing a new set of risks andopportunities, and significant resource constraintsbeyond access to capital. This is accompanied by asignificant rise of intangible value as part of companies’total market value, from 18 percent in 1975 to 80percent today, highlighting both the limitation of thecurrent accounting system and the emergence of new,less tangible value drivers, including environmental,social, and governance factors.

Building on the foundations laid by the SEC and FASBa new, standardized language is needed to articulatethe material, non-financial risks and opportunitiesfacing companies today. These non-financial risks andopportunities that affect corporations’ ability to createlong-term value are characterized as “sustainability”issues. Sustainability issues vary by industry becausethey are closely aligned with business models, the waycompanies compete, their use of resources, and theirimpact on society.

Some argue there is legal standing to mandatesustainability disclosure. A number of legal scholarshave recently pointed out that the SEC has the abilityunder the current law to require the disclosure of non-financial data—including sustainability or ESG—as itdeems necessary.

Materiality and Sustainability adds:

[Legal scholars] have also argued that the SEC hasan obligation to require sustainability disclosure if asubstantial portion of the investment communityconsiders this information material (a substantialnumber of institutional investors now assert ESGdata is important to their investment process); if

corporations are disclosing only “half-truths”(several thousand corporations worldwide nowpublish sustainability reports, but in widely differingdepths and formats); and if asymmetries in theavailability of corporate data exist (a widening gapexists between institutional investors who haveaccess to ESG data and retail investors who donot).

Because current regulatory and legal frameworks aresufficiently broad, and material information is alreadyrequired to be disclosed by the SEC, there is anopportunity—and a growing necessity—to standardizeindustry-specific sustainability key performanceindicators, which SASB aims to develop. With betterclarity on the materiality of ESG issues, and astandardized format for disclosure underpinned byverifiable data, the information becomes decision-useful for investors and the public. A decision-usefulformat, i.e., one that enables peer-to-peer comparisonand benchmarking, is critical to meet the currentdemand for disclosure from market participants whounderstand the risks, as well as the opportunities,posed by today’s ESG challenges. Relentless attentionto the materiality of the issues as well as a standardizedform of disclosure will create a de facto mandatoryreporting environment in the United States without theneed for any additional regulation. As companies beginto report performance on material ESG issues facingtheir industry, negative attention from marketbeneficiaries will shift from those disclosing materialinformation to those omitting material information,further fueling the demand.

Materiality and Sustainability states the broaderimplications of sustainability disclosure: “Put simply,disclosure of material sustainability data is necessary toassess corporations’ ability to disrupt —eitherpositively or negatively—the economic, environmental,and social systems within which they operate underconditions of substantial complexity and uncertainty.The greater the potential for corporate practices toimpact these systems, the longer the term of thesepotential impacts, and the greater the uncertaintiesinvolved, the greater the need for disclosure.”Since the 1980s, investors, stock exchanges,regulators, and corporations have shown growing

20 Environmental Disclosure Committee, December 2012

interest in such reporting. Among the indications of thisgrowing demand, as cited by Materiality andSustainability, are:

· the Principles for Responsible development,whose institutional investors as of 2012numbered over 1000 and represented assetsunder management of some $30 trillion

· the listing requirements by various stockexchanges around the world, including those inSouth Africa, China, Brazil, and India, fordisclosure of sustainability data as acomponent of good governance

· the requirement of regulators, including those inFrance, Denmark, Sweden, China, Malaysia,and Indonesia, that corporations report onsustainability issues or explain why they do notdo so

· the Securities and Exchange Commission’s2001 ruling that asset owners have a fiduciaryduty to vote on shareholder resolutionsappearing on corporate proxy statements,hundreds of which address environmental,social, and governance issues each year

· a 2009 Robeco and Booz & Co. studyestimated socially responsible assets undermanagement as of 2007 at $5 trillionworldwide and projected growth to $26.5trillion, or 15 percent to 20 percent of totalassets by 2015

Multi-stakeholder Benefits of DisclosureThe benefits of sustainability data are manifold, thoughat the core, they are very aligned with the original goalsof the SEC and FASB: to ensure public and investors’trust, as well as enable a robust sustainable market. Atthe macro level, such data can help reduce financialrisks and increase investment opportunities, whilemitigating distrust and excessive speculation, and“averting, moderating, or shortening nationalemergencies caused by financial crises or corporatemisdeeds,” according to Materiality andSustainability.

At the micro level, each stakeholder stands to benefitfrom the integration of sustainability data in corporatereporting—from investors, corporations, and

governments, to our capital markets and the generalpublic. While the systematic disclosure of materialsustainability KPIs will come at some cost tocorporations, it will lead to a substantial return oninvestment. As outlined in the white paper, thesebenefits include increased competitiveness of U.S.financial markets and corporations; reduced overallcosts and liabilities for corporations; increasedprovision of products and services with broad societalbenefits; and reduced governmental oversight andregulatory burdens, among many others.

In addition, it is SASB’s belief that the existence ofcomprehensive, industry-specific sustainabilityaccounting standards will provide investors andcompanies with decision-useful, comparableinformation on material issues with the potential toaffect short- and long-term value creation.

The Role of SASBThe Sustainability Accounting Standards Board wasfounded to fill a current void in corporate reporting byquantifying the value of corporate non-financialinformation. SASB will develop and publicly distributecomprehensive, industry-specific sustainabilityaccounting standards for the benefit of companies,investors, and the public.

As its first initiative, SASB is producing a MaterialityMap that weights the priority of sustainability issues byindustry across 10 sectors, which is useful for assetallocation strategies and understanding exposure tocertain kinds of environmental, social, and governancerisk. SASB will also identify issues deemed mostmaterial in each of 89 industries through an evidence-based approach, and will develop corresponding keyperformance indicators suitable for disclosure in theForm 10-K, thereby facilitating comparable corporatereporting. Bloomberg LP, an early supporter of SASB,will also collaborate in developing the evidence-basedMateriality Map by enabling robust searching of tens ofthousands of source documents to substantiate themateriality of ESG issues and create unique industryprofiles.

For the various reasons stated in this article, andbeyond, there is a growing need for sustainability data

21Environmental Disclosure Committee, December 2012

disclosure to insure the public and investors’ trust—both of which are the lifeblood for a healthy market.The growing demand for this data has posed severalchallenges, the most problematic of which is a resultingmyriad of data reporting styles, and the proliferation ofimmaterial information. The increased interest indisclosure beyond financial data has led to numerousmethods of sustainability reporting that vary greatlybetween corporations and industries in the UnitedStates. While the need for such disclosure is crucial intoday’s market, inconsistency in reporting has raisedmore challenges than solutions. Much of the disparity isdue to different interpretations of what is sufficiently“material” to report, as required by the SEC.

SASB aims to simplify and streamline the process byestablishing an understanding of material sustainabilityissues facing industries and creating sustainabilityaccounting standards suitable for disclosure in standardfilings. The creation of the SEC and FASB has beeninstrumental to attaining the level of financial reportingnecessary to maintain well-functioning capital markets.SASB will continue that evolution by standardizingdisclosure of sustainability information, which isincreasingly material but not currently available in adecision-useful format. A complete view of risks andopportunities will reestablish the trust that fuelscorporations and the financial markets, and our capitalmarkets will be better able to meet the needs ofinvestors and society.

Jerome Lavigne-Delville is director of StandardsDevelopment for SASB. Prior to joining theorganization, he was programme officer at theUnited Nations Global Compact, responsible forsustainability performance, disclosure, andfinancial markets. He has had a long career incorporate sustainability, blending nearly 15 years ofexperience in corporate law, investment banking,and social responsibility.

Jean Rogers is executive director and founder ofSASB. She is a former Loeb Fellow at HarvardUniversity who has authored multiple publicationsand won several awards. Dr. Rogers holds a Ph.D.in environmental engineering from the IllinoisInstitute of Technology, an M.E. in environmentalengineering and a B.E. in civil engineering, bothfrom Manhattan College.

CALL FOR NOMINATIONS

Environment, Energy, and ResourcesDedication to Diversity and Justice AwardThis award will recognize people, entities, ororganizations that have made significantaccomplishments or demonstrated recog-nized leadership in the areas of environmentaljustice and/or a commitment to gender,racial, and ethnic diversity in the environ-ment, energy, and natural resources legalarea. Accomplishments in promoting accessto environment/energy/resources rule of lawand to justice can also be recognized via thisaward.

2013 ABA Award for DistinguishedAchievement in Environmental Law andPolicyThis award recognizes individuals ororganizations who have distinguishedthemselves in environmental law and policy,contributing significant leadership inimproving the substance, process orunderstanding of environmental protectionand sustainable development.

Environment, Energy, and ResourcesGovernment Attorney of the Year AwardThis award will recognize exceptionalachievement by federal, state, tribal, or localgovernment attorneys who have worked orare working in the field of environment,energy, or natural resources law and areesteemed by their peers and viewed ashaving consistently achieved distinction in anexemplary way. The Award will be forsustained career achievement, not simplyindividual projects or recent ccomplishments.Nominees are likely to be currently serving, orrecently retired, career attorneys for federal,state, tribal, or local governmental entities.

Nomination deadlines: May 13, 2013.

These Awards will be presented at the ABAAnnual Meeting in San Francisco in August2013.

For further details about these awards,please visit the Section Web site at

www.ambar.org/EnvironAwards

22 Environmental Disclosure Committee, December 2012