epic research special report of 20 jan 2016

TRANSCRIPT

DAILY REPORT

20th

JAN. 2016

YOUR MINTVISORY Call us at +91-731-6642300

Global markets at a glance Asian share markets slipped early Wednesday as a relent-less slide in oil prices wiped out an attempted rally on Wall Street and dealt a fresh blow to risk appetite. Equity mar-kets reacted by reversing some of Tuesday's rare gains, and MSCI's broadest index of Asia-Pacific shares outside Ja-pan .MIAPJ0000PUS dropped 0.3 percent. Japan's Nikkei fell 0.7 percent, while Australian stocks lost 0.4 percent. Chinese markets had led the bounce on Tuesday with the CSI300 index up 3.0 percent and the Shanghai Composite Index rising 3.2 percent. That rally was puzzling to many given the economic news from China was hardly bright, and the International Monetary Fund cut its global growth forecasts for the third time in less than a year. US stocks closed mixed Tuesday, stabilizing after a sharply lower start to the year despite pressure from a fresh de-cline in oil prices. The S&P 500 held above key technical level, its August low of 1,867. US stocks closed mixed Tues-day, stabilizing after a sharply lower start to the year de-spite pressure from a fresh decline in oil prices. The S&P 500 held above key technical level, its August low of 1,867. The Dow Jones industrial average closed about 28 points higher, holding little of its opening gains of more than 180 points but more than recovering from a roughly 88-point dip in afternoon trade. UnitedHealth and McDonald's con-tributed the most to gains, while Exxon Mobil and Chevron were the greatest weights on the index. The Dow trans-ports gave up opening gains to close about half a percent lower. Previous day Roundup Bulls took a charge over Dalal Street on Tuesday as global rally post China GDP data and short covering helped equity benchmarks snap four-day loss. Banking stocks along with index heavyweights like Reliance Industries and L&T drove market higher. The broader markets outperformed bench-marks. The Sensex rallied 291.47 points or 1.21 percent to 24479.84, and the Nifty surged 84.10 points or 1.14 per-cent to 7435.10 after hitting an intraday high of 7462.75. Index stats The Market was very volatile in last session. The sartorial indices performed as follow; Consumer Durables [up 82.83pts], Capital Goods [up 345.92Pts], PSU [up 25.54pts], FMCG [up 23.51Pts], Realty [up 19.63pts], Power [up 22.54pts], Auto [up 189.93Pts], Healthcare [up 228.23Pts], IT [up 13.17pts], Metals [up 4.89Pts], TECK [up 27.91pts], Oil& Gas [up 88.34pts].

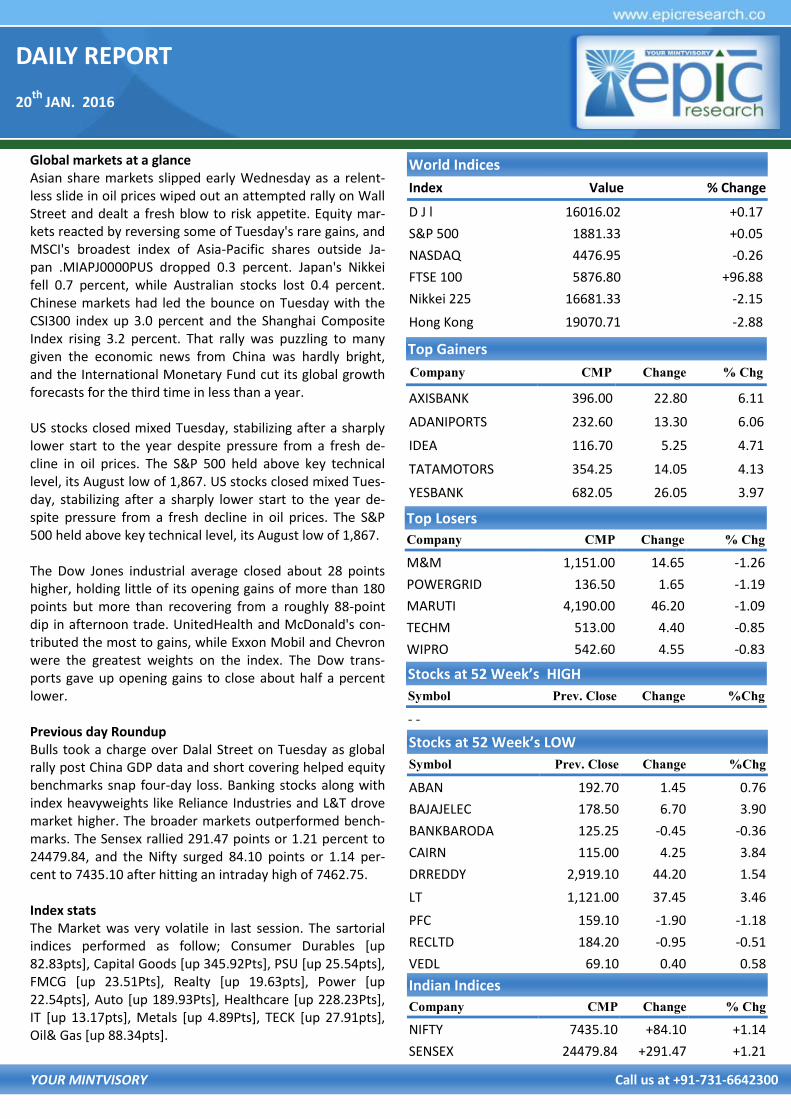

World Indices

Index Value % Change

D J l 16016.02 +0.17

S&P 500 1881.33 +0.05

NASDAQ 4476.95 -0.26

FTSE 100 5876.80 +96.88

Nikkei 225 16681.33 -2.15

Hong Kong 19070.71 -2.88

Top Gainers

Company CMP Change % Chg

AXISBANK 396.00 22.80 6.11

ADANIPORTS 232.60 13.30 6.06

IDEA 116.70 5.25 4.71

TATAMOTORS 354.25 14.05 4.13

YESBANK 682.05 26.05 3.97

Top Losers

Company CMP Change % Chg

M&M 1,151.00 14.65 -1.26

POWERGRID 136.50 1.65 -1.19

MARUTI 4,190.00 46.20 -1.09

TECHM 513.00 4.40 -0.85

WIPRO 542.60 4.55 -0.83

Stocks at 52 Week’s HIGH

Symbol Prev. Close Change %Chg

- -

Indian Indices

Company CMP Change % Chg

NIFTY 7435.10 +84.10 +1.14

SENSEX 24479.84 +291.47 +1.21

Stocks at 52 Week’s LOW

Symbol Prev. Close Change %Chg

ABAN 192.70 1.45 0.76

BAJAJELEC 178.50 6.70 3.90

BANKBARODA 125.25 -0.45 -0.36

CAIRN 115.00 4.25 3.84

DRREDDY 2,919.10 44.20 1.54

LT 1,121.00 37.45 3.46

PFC 159.10 -1.90 -1.18

RECLTD 184.20 -0.95 -0.51

VEDL 69.10 0.40 0.58

DAILY REPORT

20th

JAN. 2016

YOUR MINTVISORY Call us at +91-731-6642300

STOCK RECOMMENDATION [CASH] 3. LINCOLN

After giving sharp correction LINCOLN finished with bullish reversal sign on daily chart it create bullish candle since it is too volatile for that it will be good for buy above 182 for target of 185 190 200 with stop loss of 179 MACRO NEWS Results today: Axis Bank , DHFL , UltraTech Cement ,

Edelweiss Financial Services , GATI, Indiabulls Housing Finance, JSW Energy, KPIT Technologies, NIIT, Nucleus Software, Reliance Infrastructure, Sasken Communica-tion, South Indian Bank, Tata Elxsi, Tata Sponge Iron, Triveni Engineering

Power companies - Government to consider new power tariff policy today.

RBI to inject liquidity of Rs 10,000 cr via OMOs on Wednesday

China steel output falls 2.3% in 2015, first drop in over 30 yrs

Vintage car rally organisers move Supreme Court over NGT ban on diesel

Maruti Suzuki's Baleno pips Hyundai's Elite i20 at No. 1 spot, sells 10,572 units in December

VAT effect: Petrol price in Delhi up by 96 paise a litre, diesel by 53 paise

India's plastic packaging industry to touch $73 billion by fiscal 2020

A strict FDA, competition may slow pharma growth; ex-port may halve to 8 per cent by 2020

IMF cuts FY16 world GDP target to 3.4%, maintains India outlook

Seek USD 1 billion from Indian government in damages for attaching shareholding in Cairn India

RBI says IDFC Bank authorised to be a receiving office for sovereign gold bond 2016

Neyveli Lignite to enter steel industry Indian Bank board approves raising Rs 1,100 crore via

basel-III compliant Tier-II bonds

STOCK RECOMMENDATIONS [FUTURE] 1. BANKBARODA [FUTURE]

BANKBARODA FUTURE still facing selling pressure despite we seen bounce back in banking share where many of finished more then 3% gain but BANKBARODA end with 0.56% loss while on daily chart it create pennant pattern so below 124 we can see vertical fall for that it will be good to sell below 124 for target of 122 118 with stop loss of 125.80. 2. ICICI BANK [FUTURE]

Last session rally lead by private banks in which ICICI Bank given reversal sign on EOD chart but on hourly chart it create cup & handle pattern whose breakout will come above 231 & pattern target will be 240 since in last session it got de-mand around 227 so we advise to buy it above 231 for target of 235– 240 with stop loss of 226.90

DAILY REPORT

20th

JAN. 2016

YOUR MINTVISORY Call us at +91-731-6642300

FUTURE & OPTION

MOST ACTIVE CALL OPTION

Symbol Op-

tion

Type

Strike

Price

LTP Traded

Volume

(Contracts)

Open

Interest

NIFTY CE 7,500 45.50 4,49,452 50,37,600

NIFTY CE 7,400 94.65 2,48,649 28,98,675

BANKNIFTY CE 15,500 151.00 86,231 5,21,700

ABIRLANUVO CE 2,050 15.85 7,472 82,000

RELIANCE CE 1,100 8.60 6,641 26,00,500

SBIN CE 200 1.00 4,310 59,90,000

INFY CE 1,160 10.50 3,943 14,07,500

HCLTECH CE 840 15.00 3,285 2,60,400

MOST ACTIVE PUT OPTION

Symbol Op-

tion

Type

Strike

Price

LTP Traded

Volume

(Contracts)

Open

Interest

NIFTY PE 7,400 57.80 3,44,986 57,59,850

NIFTY PE 7,300 30.95 3,05,219 71,02,275

BANKNIFTY PE 15,000 132.10 77,780 7,68,720

ABIRLANUVO PE 2,050 0.05 4,746 3,88,000

RELIANCE PE 1,000 8.70 4,267 11,69,000

INFY PE 1,100 5.15 3,339 18,56,000

RELIANCE PE 980 5.00 2,269 3,87,500

AXISBANK PE 380 6.25 1,937 7,18,000

FII DERIVATIVES STATISTICS

BUY OPEN INTEREST AT THE END OF THE DAY SELL

No. of

Contracts Amount in

Crores No. of

Contracts Amount in

Crores No. of

Contracts Amount in

Crores NET AMOUNT

INDEX FUTURES 43828 2316.31 36549 1925.50 309777 16541.47 390.81

INDEX OPTIONS 617173 33306.25 600485 32512.46 1504074 82227.77 793.79

STOCK FUTURES 103022 4637.61 95615 4394.54 1104396 49647.34 243.06

STOCK OPTIONS 70562 3338.03 73873 3503.96 94675 4350.28 -165.93

TOTAL 1261.73

STOCKS IN NEWS HCL Tech Q2 profit rises 11% to Rs 1920 cr; $ revenue

meets forecast Reliance Q3 profit beats estimates, up 10%; GRM at 7-

year high Maruti falls; Morgan Stanley says S-Cross price cut may

hit profit RPower Q3 profit rises 38%, generation up over 3-fold ITC's Yippee nears Rs 1,000-crore mark, gains from

Maggi controversy Godrej & Boyce acquires 51% stake in home and acces-

sories brand India Circus CoalIndia to spend Rs 200cr on initial technical upgrade NIFTY FUTURE

Nifty in last trading session took some upward run thus covering some loss but the correction in the index is not yet over and Nifty also has a strong resistance around 7600. Nifty overall is in bearish zone and it may come down to 7250, so we advise you to sell it from around 7500 for the targets of 7400 and 7300 with 7650

INDICES R2 R1 PIVOT S1 S2

BANK NIFTY 7,519.00 7,477.00 7,420.00 7,378.00 7,321.00

NIFTY 15,484.00 15,376.00 15,231.00 15,123.00 14,978.00

DAILY REPORT

20th

JAN. 2016

YOUR MINTVISORY Call us at +91-731-6642300

RECOMMENDATIONS

GOLD

TRADING STRATEGY:

BUY GOLD ABOVE 26200 TARGET 26280 26370 SL 26100

SELL GOLD BELOW 26000 TARGET 25920 25820 SL 26100

SILVER

TRADING STRATEGY:

BUY SILVER ABOVE 34500 TARGET 34700 35000 SL 34200

SELL SILVER BELOW 34200 TARGET 34000 33700 SL 34500

COMMODITY ROUNDUP US crude wallowed at its lowest since 2003 after the world's energy watchdog warned the market could "drown in over-supply". US crude futures CLc1 shed another 49 cents to a new trough at USD 27.97 in early trade, while Brent crude LCOc1 was quoted at USD 28.76 a barrel. Taking positive cues from global market and pick up in do-mestic demand, lead prices were up by 0.73% to Rs 109.80 per kg in futures trade. At MCX lead for delivery this month edged up by 80 paise, or 0.73% to Rs 109.80 per kg in a business turnover of 458 lots. Similarly, the metal for deliv-ery in far-month February rose by 70 paise, or 0.64% to Rs 110.20 per kg in four lots. The rise in lead futures is due to pick up in demand from battery-makers in the spot market and a firm global trend. MCX Copper showed gains in the last evening and was showing bargain hunting after the news of Chinese GDP growth was discounted. The prices already factored in the debacle of Chinese growth and this was the reason that the gains was noted after the data set showed depletion in Chi-nese GDP. Also assisting the markets of Copper was the re-vival of equity bourses across globe. Indian Copper was trading at Rs 301.15 per kg, up 1.53%. The prices tested a high of Rs 302.85 per kg and a low of Rs 297.85 per kg. How-ever coming days are expected to be rough for Copper and peers. China's refined copper consumption in November hit 810,000 mt, edging up 10,000 mt month on month, on higher domestic output of automobiles, cable and trans-formers, state-run metals consultancy Beijing Antaike said Monday. China's November net refined copper imports were 270,000 mt, up 10,000 mt month on month, the re-port said. The country's refined copper supply in November was 920,000 mt, also up 10,000 mt months on month, it said. Zinc prices recovered 0.89% to Rs 102 per kg in futures trad-ing today as speculators created fresh positions, taking posi-tive cues from the overseas markets. Besides, increased de-mand from consuming industries in the spot market sup-ported the uptrend. At the Multi Commodity Exchange, zinc for delivery in the current month was trading higher by 90 paise, or 0.89%, to Rs 102 per kg in a business turnover of 712 lots. The metal for delivery in February rose by 90 paise to trade at Rs 102.80 per kg in 14 lots. Marketmen attrib-uted the rise in zinc futures to fresh bets created by partici-pants on the back of a firm global trend after data showed China's economy expanding at 6.9% last year, close to the target set by the country's leadership.

DAILY REPORT

20th

JAN. 2016

YOUR MINTVISORY Call us at +91-731-6642300

NCDEX

NCDEX INDICES

Index Value % Change

CASTOR SEED 3408 -1.47

CHANA 4825 +0.06

CORIANDER 6180 -3.56

COTTON SEED 2030 -2.36

GUAR SEED 3074 -3.15

JEERA 13350 -1.07

MUSTARDSEED 4490 -0.60

SOY BEAN 3750 +1.35

SUGAR M GRADE 3235 -0.52

TURMERIC 8704 -5.98

RECOMMENDATIONS

DHANIYA

BUY CORIANDER APR ABOVE 6940 TARGET 6985 7135 SL

BELOW 6875

SELL CORIANDER APR BELOW 6500 TARGET 6455 6305 SL

ABOVE 6565

GUARGUM

BUY GUARGUM FEB ABOVE 5970 TARGET 6020 6090 SL

BELOW 5910

SELL GUARGUM FEB BELOW 5790 TARGET 5740 5670 SL

ABOVE 5850

Amid pick up in demand at domestic spot market and re-stricted supplies from producing regions, mentha oil-prices were up by 0.25% to Rs 888.30 per kg in futures mar-ket today. At MCX mentha oil for delivery in February edged up by Rs 2.20, or 0.25% to Rs 888.30 per kg in a business turnover of 22 lots. On similar lines, the oil for delivery in January traded higher by Re 1, or 0.11% to Rs 876.30 per kg in 59 lots. Fresh positions built up by speculators after pick up in demand from consuming industries in the spot market against restricted supplies from Chandausi in Uttar Pradesh led to the rise in mentha oil prices at futures trade. Crude palm oil prices were down by 0.26% to Rs 426 per 10 kg in futures trading today as speculators booked profits at prevailing levels amid sluggish demand in the spot market. Besides, adequate stocks position due to higher supplies from major producing regions fuelled the downtrend. At MCX crude palm oil for delivery in January fell by Rs 1.10, or 0.26% to Rs 426 per 10 kg with a business turnover of 29 lots. Similarly, the oil for delivery in February weakened by Re 1, or 0.23% to Rs 430.80 per 10 kg in 40 lots. Besides profit-booking by traders, fall in demand in the spot market mainly influenced crude palm oil prices at futures trade. Chana prices fell further by 0.73% to Rs 4,343 per quintal in futures trading as participants engaged in reducing their positions, tracking a weak trend at spot market on low de-mand. Furthermore, adequate stocks in the physical market on pick up in supplies from producing regions fuelled the downtrend. At the NCDEX chana for delivery in far-month April drifted by Rs 32, or 0.73% to Rs 4,343 per quintal with an OI of 3,960 lots. CHANA for delivery in January traded lower by Rs 27, or 0.63% to Rs 4,291 per quintal in 26,850 lots. The fall in chana futures to slackened demand against sufficient stocks on higher supplies from producing regions.

DAILY REPORT

20th

JAN. 2016

YOUR MINTVISORY Call us at +91-731-6642300

RBI Reference Rate

Currency Rate Currency Rate

Rupee- $ 67.5630 Yen-100 57.3700

Euro 73.5018 GBP 96.4192

CURRENCY

USD/INR

BUY USD/INR JAN ABOVE 67.75 TARGET 67.88 68.03 SL BE-

LOW 67.55

SELL USD/INR JAN BELOW 67.68 TARGET 67.55 67.4 SL

ABOVE 67.88

EUR/INR

BUY EUR/INR JAN ABOVE 73.73 TARGET 73.88 74.08 SL BE-

LOW 73.53

SELL EUR/INR JAN BELOW 73.44 TARGET 73.29 73.09 SL

ABOVE 73.64

CURRENCY MARKET UPDATES: One loser was sterling which carved out a seven-year low after Bank of England Governor Mark Carney said he had no "set timetable" for raising interest rates. The pound sank as deep as USD 1.4127, before steadying around USD 1.4164. The US dollar edged higher against a basket of cur-rencies on Tuesday, after data showed that a slowdown in China's fourth-quarter growth matched expectations and as the International Monetary Fund cut its global growth forecast. The dollar index, which measures the greenback's strength against a trade-weighted basket of six major cur-rencies, was at 99.37. The European unit slipped 0.17% to trade at 1.0875. The ZEW Centre for Economic Research said that its index of German economic sentiment declined by 5.9 points to 10.2 this month from December's reading of 16.1. Annual rate of inflation in the euro area came in at 0.2% in December, in line with forecasts. On a month-over-month basis con-sumer prices were flat. USD/JPY gained 0.54% to 117.97, off overnight lows of 117.22 and Friday's four-and-a-half month trough of 116.50. As against the pound, the dollar was lower with GBP/USD up 0.49% to 1.4314, off Friday's five-year lows of 1.4247. Sterling strengthened after the U.K. Office for National Sta-tistics said the consumer price index rose 0.1% in Decem-ber from a month earlier, matching forecasts. The annual rate of inflation rose 0.2%, ahead of forecasts of 0.1% and the highest since January 2015. The pound failed to rise versus the Indian Rupee on Mon-day despite the release of data in the morning showing a widening of the Indian trade deficit to 11.66bn in Decem-ber from 9.78bn in November. The widening of the trade gap was explained as resulting from a decline in commod-ity prices, a general fall in demand due to the global slow-down and a rise in gold imports due to increased demand because of the onset of the Indian marriage season. In the financial year from April to December, cumulative exports had also shown to have fallen

DAILY REPORT

20th

JAN. 2016

YOUR MINTVISORY Call us at +91-731-6642300

Date Commodity/ Currency

Pairs Contract Strategy Entry Level Target Stop Loss Remark

19/01/16 NCDEX DHANIYA APR. BUY 6860 6905-7055 6795 BOOKED PROFIT

19/01/16 NCDEX DHANIYA APR. SELL 6750 6705-6555 6815 BOOKED FULL PROFIT

19/01/16 NCDEX GUARGUM FEB. BUY 6100 6150-6220 6040 NOT EXECUTED

19/01/16 NCDEX GUARGUM FEB. SELL 5910 5860-5790 5970 BOOKED FULL PROFIT

19/01/16 MCX GOLD FEB. BUY 26200 26280-26370 26100 NOT EXECUTED

19/01/16 MCX GOLD FEB. SELL 26000 25920-25820 26100 BOOKED PROFIT

19/01/16 MCX SILVER MAR. BUY 34200 34400-34700 33900 BOOKED FULL PROFIT

19/01/16 MCX SILVER MAR. SELL 33900 33700-33400 34200 NOT EXECUTED

Date Scrip

CASH/

FUTURE/

OPTION

Strategy Entry Level Target Stop Loss Remark

19/01/16 NIFTY FUTURE SELL 7420 7360-7260 7550 CALL OPEN

19/01/16 LT FUTURE SELL 1075 1065-1050 1090 SL TRIGGERED

19/01/16 RELCAP FUTURE SELL 339 335-330 343 NOT EXECUTED

19/01/16 INDUSIND BANK CASH SELL 894 884 908 NO PROFIT N LOSS

15/01/16 LUPIN FUTURE BUY 1725 1750-1780 1693 SL TRIGGERED

DAILY REPORT

20th

JAN. 2016

YOUR MINTVISORY Call us at +91-731-6642300

NEXT WEEK'S U.S. ECONOMIC REPORTS

ECONOMIC CALENDAR

The information and views in this report, our website & all the service we provide are believed to be reliable, but we do not accept any

responsibility (or liability) for errors of fact or opinion. Users have the right to choose the product/s that suits them the most. Sincere ef-

forts have been made to present the right investment perspective. The information contained herein is based on analysis and up on sources

that we consider reliable. This material is for personal information and based upon it & takes no responsibility. The information given

herein should be treated as only factor, while making investment decision. The report does not provide individually tailor-made invest-

ment advice. Epic research recommends that investors independently evaluate particular investments and strategies, and encourages in-

vestors to seek the advice of a financial adviser. Epic research shall not be responsible for any transaction conducted based on the infor-

mation given in this report, which is in violation of rules and regulations of NSE and BSE. The share price projections shown are not nec-

essarily indicative of future price performance. The information herein, together with all estimates and forecasts, can change without no-

tice. Analyst or any person related to epic research might be holding positions in the stocks recommended. It is understood that anyone

who is browsing through the site has done so at his free will and does not read any views expressed as a recommendation for which either

the site or its owners or anyone can be held responsible for . Any surfing and reading of the information is the acceptance of this dis-

claimer. All Rights Reserved. Investment in equity & bullion market has its own risks. We, however, do not vouch for the accuracy or the

completeness thereof. We are not responsible for any loss incurred whatsoever for any financial profits or loss which may arise from the

recommendations above epic research does not purport to be an invitation or an offer to buy or sell any financial instrument. Our Clients

(Paid or Unpaid), any third party or anyone else have no rights to forward or share our calls or SMS or Report or Any Information Pro-

vided by us to/with anyone which is received directly or indirectly by them. If found so then Serious Legal Actions can be taken.

Disclaimer

TIME REPORT PERIOD ACTUAL CONSENSUS

FORECAST PREVIOUS

MONDAY, JAN. 18

NONE SCHEDULED

MARTIN LUTHER KING JR. HOLIDAY

TUESDAY, JAN. 19

10 AM HOME BUILDERS' INDEX JAN. 61 61

WEDNESDAY, JAN. 20

8:30 AM CONSUMER PRICE INDEX DEC. -0.1% 0.0%

8:30 AM CORE CPI DEC. 0.1% 0.2%

8:30 AM HOUSING STARTS DEC. 1.190 MLN 1.173 MLN

THURSDAY, JAN. 21

8:30 AM WEEKLY JOBLESS CLAIMS JAN. 16 N/A 284,000

8:30 AM PHILLY FED JAN -4.0 -10.2

FRIDAY, JAN. 22

9;45 AM MARKIT PMI FLASH JAN. -- 51.2

10 AM EXISTING HOME SALES DEC. 5.15 MLN 4.76 MLN

10 AM LEADING ECONOMIC INDICATORS DEC. -- 0.4%