equity snapshot - danareksadmia.danareksaonline.com/upload/morning pack 20170119.pdf · the ipo is...

TRANSCRIPT

Equity SNAPSHOT Thursday, January 19, 2017

Danareksa Sekuritas – Equity SNAPSHOT

FROM EQUITY RESEARCH

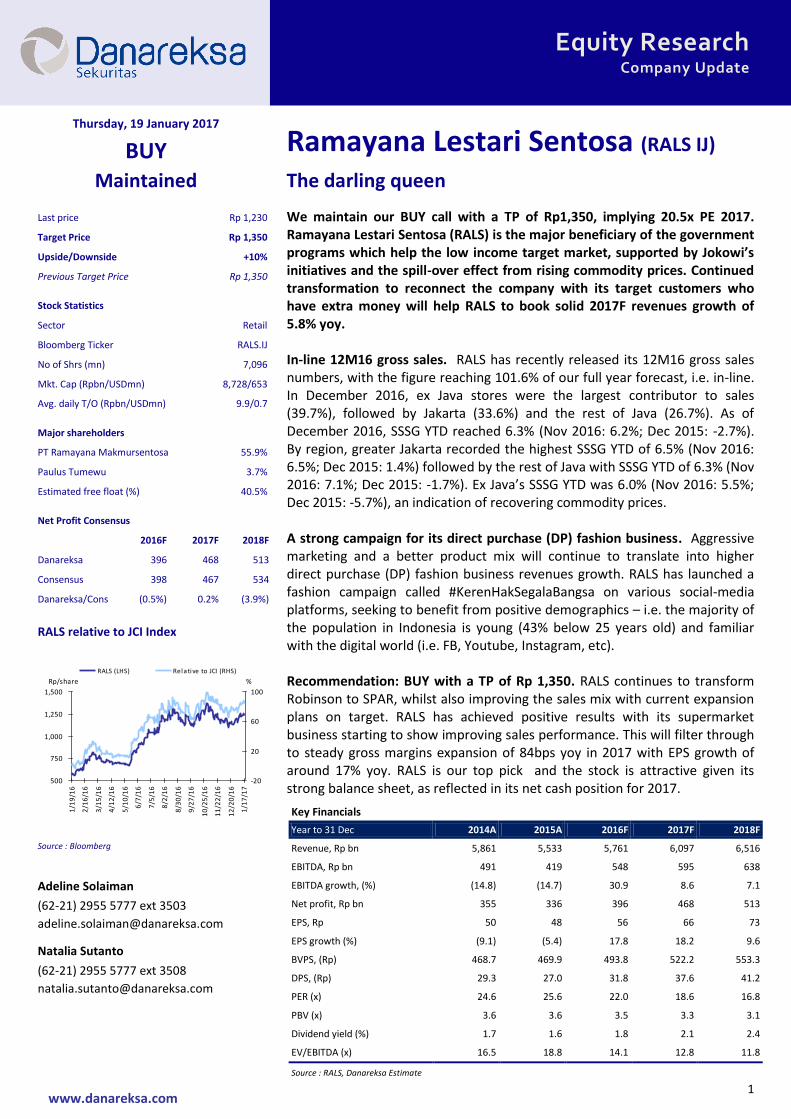

Ramayana Lestari Sentosa: The darling queen (RALS IJ. Rp 1,230. BUY. TP Rp1,350) We maintain our BUY call with a TP of Rp1,350, implying 20.5x PE 2017. Ramayana Lestari Sentosa (RALS) is the major beneficiary of the government programs which help the low income target market, supported by Jokowi’s initiatives and the spill-over effect from rising commodity prices. Continued transformation to reconnect the company with its target customers who have extra money will help RALS to book solid 2017F revenues growth of 5.8% yoy.

To see the full version of this report, please click here

MARKET NEWS

Sector Banking: FSA to Issue a New Regulation concerning bank

recovery plans Banking: Middle-level banks target higher fee based income

Retail: Going digital Corporate

Adhi Karya: revises up the IPO proceeds target for Adhi

Persada Gedung Agung Podomoro prepares Rp6tn for capex

Graha Layar Prima: Expansion by cooperating with Trans Retail Hanson International: three Malaysian companies pull out of JV

Kalbe Farma: To commence its new biosimilar factory in mid-

2018 Mitra Adiperkasa: Targets Rp700bn of capex in 2017

Sido Muncul: Targets Rp 2.7tn of revenues Siloam: Acquires two hospitals

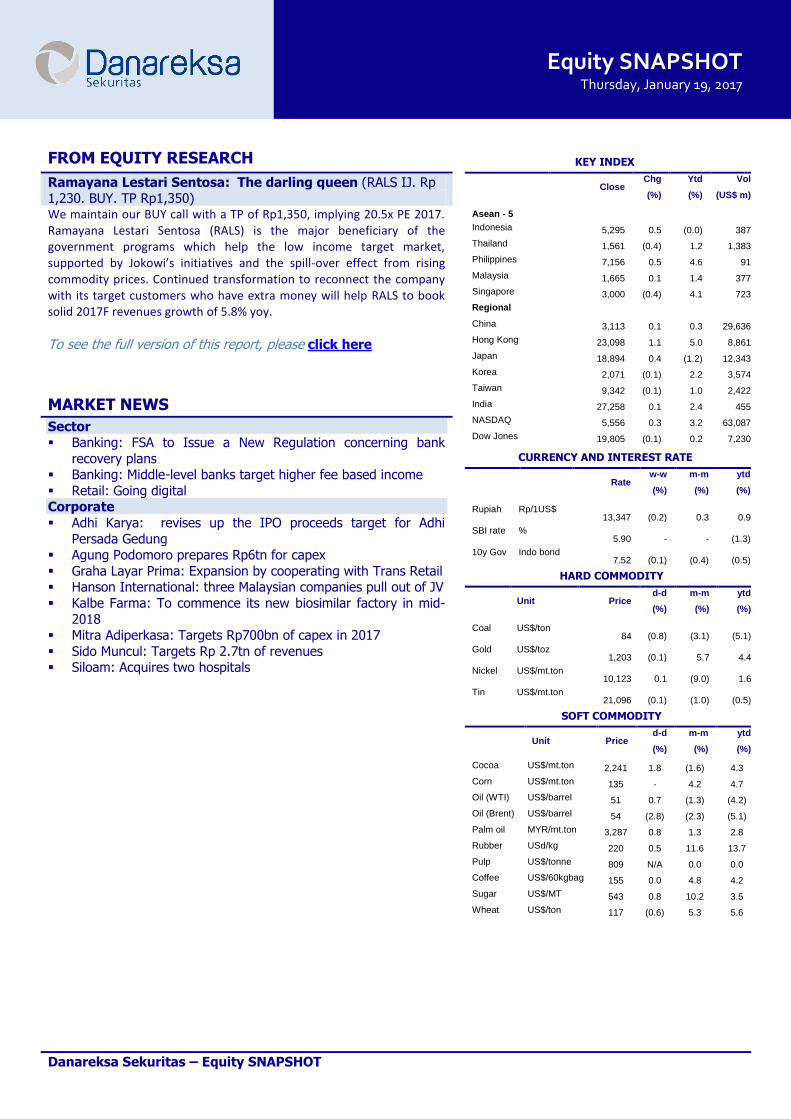

KEY INDEX

Close

Chg Ytd Vol

(%) (%) (US$ m)

Asean - 5

Indonesia 5,295 0.5 (0.0) 387

Thailand 1,561 (0.4) 1.2 1,383

Philippines 7,156 0.5 4.6 91

Malaysia 1,665 0.1 1.4 377

Singapore 3,000 (0.4) 4.1 723

Regional

China 3,113 0.1 0.3 29,636

Hong Kong 23,098 1.1 5.0 8,861

Japan 18,894 0.4 (1.2) 12,343

Korea 2,071 (0.1) 2.2 3,574

Taiwan 9,342 (0.1) 1.0 2,422

India 27,258 0.1 2.4 455

NASDAQ 5,556 0.3 3.2 63,087

Dow Jones 19,805 (0.1) 0.2 7,230

CURRENCY AND INTEREST RATE

Rate

w-w m-m ytd

(%) (%) (%)

Rupiah Rp/1US$ 13,347

(0.2)

0.3

0.9

SBI rate % 5.90

-

-

(1.3)

10y Gov Indo bond 7.52

(0.1)

(0.4)

(0.5)

HARD COMMODITY

Unit Price

d-d m-m ytd

(%) (%) (%)

Coal US$/ton 84

(0.8)

(3.1)

(5.1)

Gold US$/toz 1,203

(0.1)

5.7

4.4

Nickel US$/mt.ton 10,123

0.1

(9.0)

1.6

Tin US$/mt.ton 21,096

(0.1)

(1.0)

(0.5)

SOFT COMMODITY

Unit Price

d-d m-m ytd

(%) (%) (%)

Cocoa US$/mt.ton 2,241 1.8 (1.6) 4.3

Corn US$/mt.ton 135 - 4.2 4.7

Oil (WTI) US$/barrel 51 0.7 (1.3) (4.2)

Oil (Brent) US$/barrel 54 (2.8) (2.3) (5.1)

Palm oil MYR/mt.ton 3,287 0.8 1.3 2.8

Rubber USd/kg 220 0.5 11.6 13.7

Pulp US$/tonne 809 N/A 0.0 0.0

Coffee US$/60kgbag 155 0.0 4.8 4.2

Sugar US$/MT 543 0.8 10.2 3.5

Wheat US$/ton 117 (0.6) 5.3 5.6

Source: Bloomberg

1

Equity Research Company Update

www.danareksa.com

Thursday, 19 January 2017

Ramayana Lestari Sentosa (RALS IJ) BUY

Maintained The darling queen

We maintain our BUY call with a TP of Rp1,350, implying 20.5x PE 2017. Ramayana Lestari Sentosa (RALS) is the major beneficiary of the government programs which help the low income target market, supported by Jokowi’s initiatives and the spill-over effect from rising commodity prices. Continued transformation to reconnect the company with its target customers who have extra money will help RALS to book solid 2017F revenues growth of 5.8% yoy. In-line 12M16 gross sales. RALS has recently released its 12M16 gross sales numbers, with the figure reaching 101.6% of our full year forecast, i.e. in-line. In December 2016, ex Java stores were the largest contributor to sales (39.7%), followed by Jakarta (33.6%) and the rest of Java (26.7%). As of December 2016, SSSG YTD reached 6.3% (Nov 2016: 6.2%; Dec 2015: -2.7%). By region, greater Jakarta recorded the highest SSSG YTD of 6.5% (Nov 2016: 6.5%; Dec 2015: 1.4%) followed by the rest of Java with SSSG YTD of 6.3% (Nov 2016: 7.1%; Dec 2015: -1.7%). Ex Java’s SSSG YTD was 6.0% (Nov 2016: 5.5%; Dec 2015: -5.7%), an indication of recovering commodity prices. A strong campaign for its direct purchase (DP) fashion business. Aggressive marketing and a better product mix will continue to translate into higher direct purchase (DP) fashion business revenues growth. RALS has launched a fashion campaign called #KerenHakSegalaBangsa on various social-media platforms, seeking to benefit from positive demographics – i.e. the majority of the population in Indonesia is young (43% below 25 years old) and familiar with the digital world (i.e. FB, Youtube, Instagram, etc). Recommendation: BUY with a TP of Rp 1,350. RALS continues to transform Robinson to SPAR, whilst also improving the sales mix with current expansion plans on target. RALS has achieved positive results with its supermarket business starting to show improving sales performance. This will filter through to steady gross margins expansion of 84bps yoy in 2017 with EPS growth of around 17% yoy. RALS is our top pick and the stock is attractive given its strong balance sheet, as reflected in its net cash position for 2017.

Last price Rp 1,230

Target Price Rp 1,350

Upside/Downside +10%

Previous Target Price Rp 1,350

Stock Statistics

Sector Retail

Bloomberg Ticker RALS.IJ

No of Shrs (mn) 7,096

Mkt. Cap (Rpbn/USDmn) 8,728/653

Avg. daily T/O (Rpbn/USDmn) 9.9/0.7

Major shareholders

PT Ramayana Makmursentosa 55.9%

Paulus Tumewu 3.7%

Estimated free float (%) 40.5%

Net Profit Consensus

2016F 2017F 2018F

Danareksa 396 468 513

Consensus 398 467 534

Danareksa/Cons (0.5%) 0.2% (3.9%)

RALS relative to JCI Index

Source : Bloomberg

Adeline Solaiman

(62-21) 2955 5777 ext 3503

[email protected] Natalia Sutanto

(62-21) 2955 5777 ext 3508

500

750

1,000

1,250

1,500

1/1

9/1

6

2/1

6/1

6

3/1

5/1

6

4/1

2/1

6

5/1

0/1

6

6/7

/16

7/5

/16

8/2

/16

8/3

0/1

6

9/2

7/1

6

10

/25

/16

11

/22

/16

12

/20

/16

1/1

7/1

7

-20

20

60

100

RALS (LHS) Relative to JCI (RHS)

%Rp/share

Key Financials

Year to 31 Dec 2014A 2015A 2016F 2017F 2018F

Revenue, Rp bn 5,861 5,533 5,761 6,097 6,516

EBITDA, Rp bn 491 419 548 595 638

EBITDA growth, (%) (14.8) (14.7) 30.9 8.6 7.1

Net profit, Rp bn 355 336 396 468 513

EPS, Rp 50 48 56 66 73

EPS growth (%) (9.1) (5.4) 17.8 18.2 9.6

BVPS, (Rp) 468.7 469.9 493.8 522.2 553.3

DPS, (Rp) 29.3 27.0 31.8 37.6 41.2

PER (x) 24.6 25.6 22.0 18.6 16.8

PBV (x) 3.6 3.6 3.5 3.3 3.1

Dividend yield (%) 1.7 1.6 1.8 2.1 2.4

EV/EBITDA (x) 16.5 18.8 14.1 12.8 11.8

Source : RALS, Danareksa Estimate

Equity SNAPSHOT Thursday, January 19, 2017

Danareksa Sekuritas – Equity SNAPSHOT

SECTOR Banking: FSA to Issue a New Regulation concerning bank recovery plans

The Financial Services Authority (OJK) will implement a new regulation concerning bank recovery plans for domestic

systematically important banks (DSIB). The new regulation will cover bank plans for financial difficulties, liquidity and capital. There will be 12 large banks required to make recovery plans. (Kontan)

Banking: Middle-level banks target higher fee based income

BBTN targets a 35% increase in fee based income in 2017. BABP and MAYA, meanwhile, target 30% and 50%

growth in fee based income. In addition, BBTN also targets banc assurance, trading treasury and fee based business this year. (Kontan)

Retail: Going digital

The Indonesian Retail Association (Aprindo) is encouraging retailers to go digital and participate in the era of e-commerce. Aprindo believes that technology will be the future of the retail industry. (Kontan)

CORPORATE Adhi Karya: revises up the IPO proceeds target for Adhi Persada Gedung

Adhi Karya (ADHI) has revised up the IPO proceeds target for its subsidiary, Adhi Persada Gedung, to around Rp3.0tr from the initial target of Rp1.5tr to Rp2.5tr. ADHI is still waiting for information from its advisor regarding

the IPO. The IPO is scheduled for 2H17 with a 30% - 40% stake to be offered to the public. In addition, ADHI also

plans to issue preferred stock for Adhi Persada Gedung worth Rp2.0tr to several strategic investors, with a 3-year option to buy back the stock. The proceeds from the preferred stock will be used for bridging financing of LRT

project. Adhi Persada Gedung was established in 2014 and booked Rp1.02tr of assets as of September 2016. The company engages in building construction. (Bisnis Indonesia)

Agung Podomoro prepares Rp6tn for capex

Agung Podomoro (APLN) has prepared Rp5-6tn for capex, 25-50% higher than 2016’s capex allocation of Rp4tn.

The management stated that the capex will be used to develop new and existing projects. The source of financing will be from internal cash, bank loans, and/or bond issuances. In addition, the company is also exploring land block

sales of 216.28ha in Karawang. The transaction is expected to be completed by 1Q17. Regarding the REIT, the company is looking at whether to sell two hotels, Pullman Central Park and Sifotel Bali Nusa Dua with fair value of

the total assets of Rp3.2tn. The company further added that the capex would not be used for developing its

reclamation project, Pluit City. At the moment, the company is fulfilling all the requirements set by the government. In 2017, APLN seeks to make Rp3.5tn of marketing sales, up by 30% compared to realization in 2016 of Rp2.7tn.

(Bisnis Indonesia)

Graha Layar Prima: Expansion by cooperating with Trans Retail Graha Layar Prima (BLTZ) will cooperate with Trans Retail to open new cinemas in various cities in Indonesia. BLTZ

plans to open 15-20 new cinemas in 2017, with 6 of them to cooperate with Trans. However, the company has not disclosed the needed investment for the expansion, which will be funded by internal cash. (Kontan)

Hanson International: three Malaysian companies pull out of JV

Three Malaysian companies, Sime Darby Bhd, I&P Group Sdn, Bhd, and SP Setia Sdn. Bhd said that they have

terminated their joint venture company with Hanson International (MYRX) that was initially intended to develop Maja. According to MYRX, the company will enter into another joint operation agreement with the Ciputra Group to

develop the area. (Bisnis Indonesia)

MARKET NEWS

Equity SNAPSHOT Thursday, January 19, 2017

Danareksa Sekuritas – Equity SNAPSHOT

Kalbe Farma: To commence its new biosimilar factory in mid-2018

Kalbe Farma (KLBF) plans to commence the operation of its new biosimilar factory (total investment: USD35mn) in

mid-2018, which will produce erythropoietin (EPO) for diseases related to kidneys and cancer. At present, the company is in the process of attaining product certification. This new factory will have a total capacity of 10mn units

of EPO to tap the domestic market and for exports. Currently, KLBF imports EPO products from China totaling 1mn units/year, partially to meet demand from the national health program. However, the management of KLBF expects

higher demand for EPO over the next 5-10 years, following the increasing number of participants in the national

health program. (Bisnis Indonesia)

Mitra Adiperkasa: Targets Rp700bn of capex in 2017 Mitra Adiperkasa (MAPI) expects to spend around Rp700bn on capex in 2017. Going forward, MAPI will aggressively

open F&B outlets (Starbucks brand). At this stage, e-commerce only contributes around 1% of the company’s total revenues. (Kontan)

Comment: The company’s capex estimate is in-line with our expectation. We advise investors to HOLD the stock. Our TP is Rp5,000. (Adeline) Sido Muncul: Targets Rp 2.7tn of revenues

Sido Muncul (SIDO) targets Rp 2.7tn of revenues in 2017, +15% yoy compared to last year’s expectation of Rp

2.44tn. To reach this target, SIDO plans to improve the distribution of some dormant products such as Susu Jahe and Kopi Jahe. (Kontan)

Siloam: Acquires two hospitals Siloam International Hospital (SILO) has acquired two hospitals in Bekasi and Mataram. SILO acquired 100% of the

shares of Sentosa Hospital, located in Bekasi, worth Rp 26.5 bn and 100% of the shares of Graha Ultima Medika (GUM) Hospital, located in Mataram, worth Rp 155bn. These investments will contribute directly to SILO’s 2017

gross operating income. Both hospitals are expected to serve patients of the National Health Program. (Investor Daily)

Danareksa Sekuritas – Equity SNAPSHOT

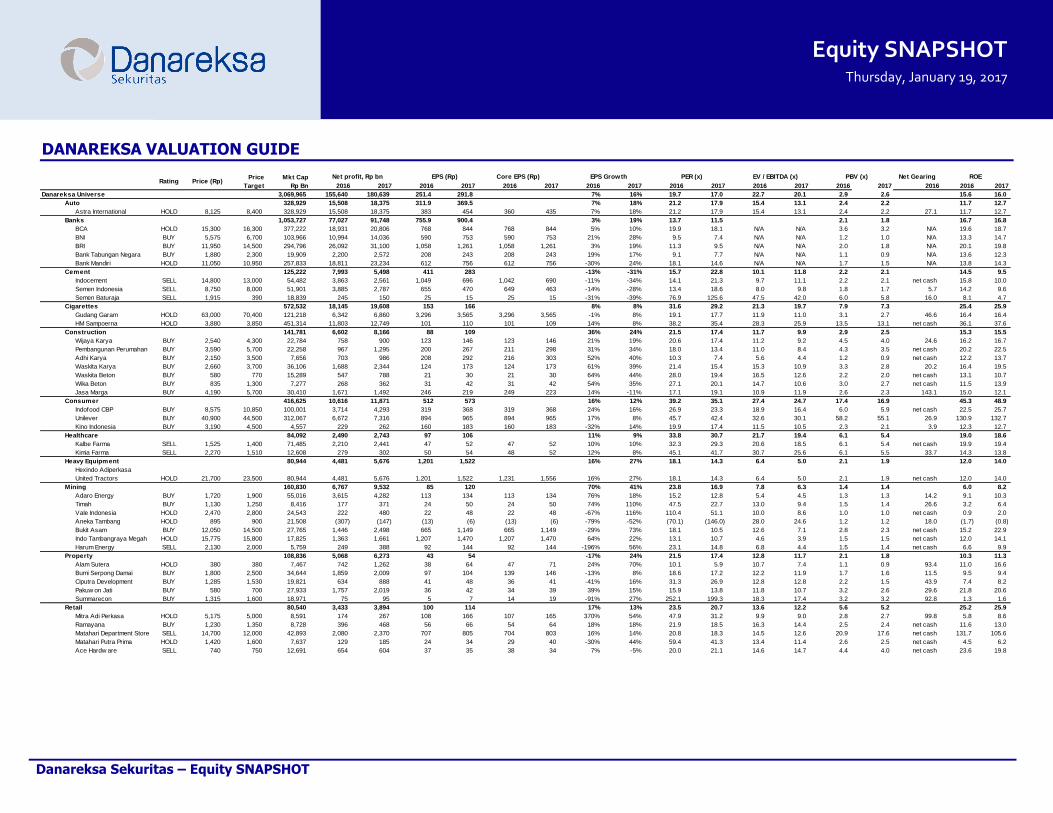

Price Mkt Cap

Target Rp Bn 2016 2017 2016 2017 2016 2017 2016 2017 2016 2017 2016 2017 2016 2017 2016 2016 2017

Danareksa Universe 3,069,965 155,640 180,639 251.4 291.8 7% 16% 19.7 17.0 22.7 20.1 2.9 2.6 15.6 16.0

Auto 328,929 15,508 18,375 311.9 369.5 7% 18% 21.2 17.9 15.4 13.1 2.4 2.2 11.7 12.7

Astra International HOLD 8,125 8,400 328,929 15,508 18,375 383 454 360 435 7% 18% 21.2 17.9 15.4 13.1 2.4 2.2 27.1 11.7 12.7

Banks 1,053,727 77,027 91,748 755.9 900.4 3% 19% 13.7 11.5 2.1 1.8 16.7 16.8

BCA HOLD 15,300 16,300 377,222 18,931 20,806 768 844 768 844 5% 10% 19.9 18.1 N/A N/A 3.6 3.2 N/A 19.6 18.7

BNI BUY 5,575 6,700 103,966 10,994 14,036 590 753 590 753 21% 28% 9.5 7.4 N/A N/A 1.2 1.0 N/A 13.3 14.7

BRI BUY 11,950 14,500 294,796 26,092 31,100 1,058 1,261 1,058 1,261 3% 19% 11.3 9.5 N/A N/A 2.0 1.8 N/A 20.1 19.8

Bank Tabungan Negara BUY 1,880 2,300 19,909 2,200 2,572 208 243 208 243 19% 17% 9.1 7.7 N/A N/A 1.1 0.9 N/A 13.6 12.3

Bank Mandiri HOLD 11,050 10,950 257,833 18,811 23,234 612 756 612 756 -30% 24% 18.1 14.6 N/A N/A 1.7 1.5 N/A 13.8 14.3

Cement 125,222 7,993 5,498 411 283 -13% -31% 15.7 22.8 10.1 11.8 2.2 2.1 14.5 9.5

Indocement SELL 14,800 13,000 54,482 3,863 2,561 1,049 696 1,042 690 -11% -34% 14.1 21.3 9.7 11.1 2.2 2.1 net cash 15.8 10.0

Semen Indonesia SELL 8,750 8,000 51,901 3,885 2,787 655 470 649 463 -14% -28% 13.4 18.6 8.0 9.8 1.8 1.7 5.7 14.2 9.6

Semen Baturaja SELL 1,915 390 18,839 245 150 25 15 25 15 -31% -39% 76.9 125.6 47.5 42.0 6.0 5.8 16.0 8.1 4.7

Cigarettes 572,532 18,145 19,608 153 166 8% 8% 31.6 29.2 21.3 19.7 7.9 7.3 25.4 25.9

Gudang Garam HOLD 63,000 70,400 121,218 6,342 6,860 3,296 3,565 3,296 3,565 -1% 8% 19.1 17.7 11.9 11.0 3.1 2.7 46.6 16.4 16.4

HM Sampoerna HOLD 3,880 3,850 451,314 11,803 12,749 101 110 101 109 14% 8% 38.2 35.4 28.3 25.9 13.5 13.1 net cash 36.1 37.6

Construction 141,781 6,602 8,166 88 109 36% 24% 21.5 17.4 11.7 9.9 2.9 2.5 15.3 15.5

Wijaya Karya BUY 2,540 4,300 22,784 758 900 123 146 123 146 21% 19% 20.6 17.4 11.2 9.2 4.5 4.0 24.6 16.2 16.7

Pembangunan Perumahan BUY 3,590 5,700 22,258 967 1,295 200 267 211 298 31% 34% 18.0 13.4 11.0 8.4 4.3 3.5 net cash 20.2 22.5

Adhi Karya BUY 2,150 3,500 7,656 703 986 208 292 216 303 52% 40% 10.3 7.4 5.6 4.4 1.2 0.9 net cash 12.2 13.7

Waskita Karya BUY 2,660 3,700 36,106 1,688 2,344 124 173 124 173 61% 39% 21.4 15.4 15.3 10.9 3.3 2.8 20.2 16.4 19.5

Waskita Beton BUY 580 770 15,289 547 788 21 30 21 30 64% 44% 28.0 19.4 16.5 12.6 2.2 2.0 net cash 13.1 10.7

Wika Beton BUY 835 1,300 7,277 268 362 31 42 31 42 54% 35% 27.1 20.1 14.7 10.6 3.0 2.7 net cash 11.5 13.9

Jasa Marga BUY 4,190 5,700 30,410 1,671 1,492 246 219 249 223 14% -11% 17.1 19.1 10.9 11.9 2.6 2.3 143.1 15.0 12.1

Consumer 416,625 10,616 11,871 512 573 16% 12% 39.2 35.1 27.4 24.7 17.4 16.9 45.3 48.9

Indofood CBP BUY 8,575 10,850 100,001 3,714 4,293 319 368 319 368 24% 16% 26.9 23.3 18.9 16.4 6.0 5.9 net cash 22.5 25.7

Unilever BUY 40,900 44,500 312,067 6,672 7,316 894 965 894 965 17% 8% 45.7 42.4 32.6 30.1 58.2 55.1 26.9 130.9 132.7

Kino Indonesia BUY 3,190 4,500 4,557 229 262 160 183 160 183 -32% 14% 19.9 17.4 11.5 10.5 2.3 2.1 3.9 12.3 12.7

Healthcare 84,092 2,490 2,743 97 106 11% 9% 33.8 30.7 21.7 19.4 6.1 5.4 19.0 18.6

Kalbe Farma SELL 1,525 1,400 71,485 2,210 2,441 47 52 47 52 10% 10% 32.3 29.3 20.6 18.5 6.1 5.4 net cash 19.9 19.4

Kimia Farma SELL 2,270 1,510 12,608 279 302 50 54 48 52 12% 8% 45.1 41.7 30.7 25.6 6.1 5.5 33.7 14.3 13.8

Heavy Equipment 80,944 4,481 5,676 1,201 1,522 16% 27% 18.1 14.3 6.4 5.0 2.1 1.9 12.0 14.0

Hexindo Adiperkasa

United Tractors HOLD 21,700 23,500 80,944 4,481 5,676 1,201 1,522 1,231 1,556 16% 27% 18.1 14.3 6.4 5.0 2.1 1.9 net cash 12.0 14.0

Mining 160,830 6,767 9,532 85 120 70% 41% 23.8 16.9 7.8 6.3 1.4 1.4 6.0 8.2

Adaro Energy BUY 1,720 1,900 55,016 3,615 4,282 113 134 113 134 76% 18% 15.2 12.8 5.4 4.5 1.3 1.3 14.2 9.1 10.3

Timah BUY 1,130 1,250 8,416 177 371 24 50 24 50 74% 110% 47.5 22.7 13.0 9.4 1.5 1.4 26.6 3.2 6.4

Vale Indonesia HOLD 2,470 2,800 24,543 222 480 22 48 22 48 -67% 116% 110.4 51.1 10.0 8.6 1.0 1.0 net cash 0.9 2.0

Aneka Tambang HOLD 895 900 21,508 (307) (147) (13) (6) (13) (6) -79% -52% (70.1) (146.0) 28.0 24.6 1.2 1.2 18.0 (1.7) (0.8)

Bukit Asam BUY 12,050 14,500 27,765 1,446 2,498 665 1,149 665 1,149 -29% 73% 18.1 10.5 12.6 7.1 2.8 2.3 net cash 15.2 22.9

Indo Tambangraya Megah HOLD 15,775 15,800 17,825 1,363 1,661 1,207 1,470 1,207 1,470 64% 22% 13.1 10.7 4.6 3.9 1.5 1.5 net cash 12.0 14.1

Harum Energy SELL 2,130 2,000 5,759 249 388 92 144 92 144 -196% 56% 23.1 14.8 6.8 4.4 1.5 1.4 net cash 6.6 9.9

Property 108,836 5,068 6,273 43 54 -17% 24% 21.5 17.4 12.8 11.7 2.1 1.8 10.3 11.3

Alam Sutera HOLD 380 380 7,467 742 1,262 38 64 47 71 24% 70% 10.1 5.9 10.7 7.4 1.1 0.9 93.4 11.0 16.6

Bumi Serpong Damai BUY 1,800 2,500 34,644 1,859 2,009 97 104 139 146 -13% 8% 18.6 17.2 12.2 11.9 1.7 1.6 11.5 9.5 9.4

Ciputra Development BUY 1,285 1,530 19,821 634 888 41 48 36 41 -41% 16% 31.3 26.9 12.8 12.8 2.2 1.5 43.9 7.4 8.2

Pakuw on Jati BUY 580 700 27,933 1,757 2,019 36 42 34 39 39% 15% 15.9 13.8 11.8 10.7 3.2 2.6 29.6 21.8 20.6

Summarecon BUY 1,315 1,600 18,971 75 95 5 7 14 19 -91% 27% 252.1 199.3 18.3 17.4 3.2 3.2 92.8 1.3 1.6

Retail 80,540 3,433 3,894 100 114 17% 13% 23.5 20.7 13.6 12.2 5.6 5.2 25.2 25.9

Mitra Adi Perkasa HOLD 5,175 5,000 8,591 174 267 108 166 107 165 370% 54% 47.9 31.2 9.9 9.0 2.8 2.7 99.8 5.8 8.6

Ramayana BUY 1,230 1,350 8,728 396 468 56 66 54 64 18% 18% 21.9 18.5 16.3 14.4 2.5 2.4 net cash 11.6 13.0

Matahari Department Store SELL 14,700 12,000 42,893 2,080 2,370 707 805 704 803 16% 14% 20.8 18.3 14.5 12.6 20.9 17.6 net cash 131.7 105.6

Matahari Putra Prima HOLD 1,420 1,600 7,637 129 185 24 34 29 40 -30% 44% 59.4 41.3 13.4 11.4 2.6 2.5 net cash 4.5 6.2

Ace Hardw are SELL 740 750 12,691 654 604 37 35 38 34 7% -5% 20.0 21.1 14.6 14.7 4.4 4.0 net cash 23.6 19.8

Core EPS (Rp)Rating Price (Rp)

Net profit, Rp bn EPS (Rp) Net Gearing ROE EPS Growth PER (x) EV / EBITDA (x) PBV (x)

DANAREKSA VALUATION GUIDE

Equity SNAPSHOT Thursday, January 19, 2017

Equity SNAPSHOT Thursday, January 19, 2017

Danareksa Sekuritas – Equity SNAPSHOT

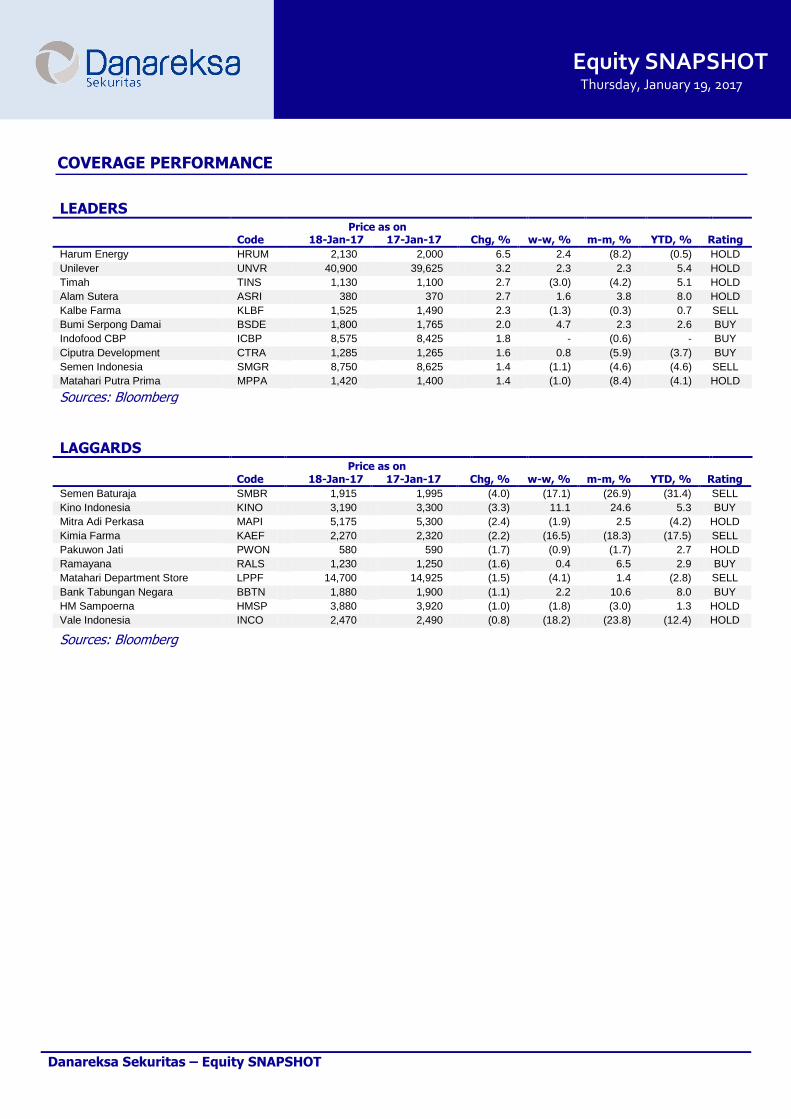

LEADERS Price as on Code 18-Jan-17 17-Jan-17 Chg, % w-w, % m-m, % YTD, % Rating

Harum Energy HRUM 2,130 2,000 6.5 2.4 (8.2) (0.5) HOLD

Unilever UNVR 40,900 39,625 3.2 2.3 2.3 5.4 HOLD

Timah TINS 1,130 1,100 2.7 (3.0) (4.2) 5.1 HOLD

Alam Sutera ASRI 380 370 2.7 1.6 3.8 8.0 HOLD

Kalbe Farma KLBF 1,525 1,490 2.3 (1.3) (0.3) 0.7 SELL

Bumi Serpong Damai BSDE 1,800 1,765 2.0 4.7 2.3 2.6 BUY

Indofood CBP ICBP 8,575 8,425 1.8 - (0.6) - BUY

Ciputra Development CTRA 1,285 1,265 1.6 0.8 (5.9) (3.7) BUY

Semen Indonesia SMGR 8,750 8,625 1.4 (1.1) (4.6) (4.6) SELL

Matahari Putra Prima MPPA 1,420 1,400 1.4 (1.0) (8.4) (4.1) HOLD

Sources: Bloomberg

LAGGARDS Price as on Code 18-Jan-17 17-Jan-17 Chg, % w-w, % m-m, % YTD, % Rating

Semen Baturaja SMBR 1,915 1,995 (4.0) (17.1) (26.9) (31.4) SELL

Kino Indonesia KINO 3,190 3,300 (3.3) 11.1 24.6 5.3 BUY

Mitra Adi Perkasa MAPI 5,175 5,300 (2.4) (1.9) 2.5 (4.2) HOLD

Kimia Farma KAEF 2,270 2,320 (2.2) (16.5) (18.3) (17.5) SELL

Pakuwon Jati PWON 580 590 (1.7) (0.9) (1.7) 2.7 HOLD

Ramayana RALS 1,230 1,250 (1.6) 0.4 6.5 2.9 BUY

Matahari Department Store LPPF 14,700 14,925 (1.5) (4.1) 1.4 (2.8) SELL

Bank Tabungan Negara BBTN 1,880 1,900 (1.1) 2.2 10.6 8.0 BUY

HM Sampoerna HMSP 3,880 3,920 (1.0) (1.8) (3.0) 1.3 HOLD

Vale Indonesia INCO 2,470 2,490 (0.8) (18.2) (23.8) (12.4) HOLD

Sources: Bloomberg

COVERAGE PERFORMANCE

Equity SNAPSHOT Thursday, January 19, 2017

Danareksa Sekuritas – Equity SNAPSHOT

PREVIOUS REPORTS

Gudang Garam (GGRM IJ): A defensive play Snapshot20170118

Waskita Beton Precast: Hoping for another good year Snapshot20170117 Cement: Still under pressure Snapshot20170116

Metal Mining Sector : Global supply risks have boosted metal mining prices, Cement: Not encouraging sales in

December 2016 (Underweight) Snapshot20170113 UNVR: Safe haven, Ace Hardware Indonesia: In-line 12M16 sales Snapshot20170112

PTPP: Higher capital for higher growth, RALS: In-line 12M16 gross sales Snapshot20170111 BBNI: Accelerating performance, ASRI: beats our marketing sales target Snapshot20170110

Equity SNAPSHOT Thursday, January 19, 2017

Danareksa Sekuritas – Equity SNAPSHOT

PT Danareksa Sekuritas

Jl. Medan Merdeka Selatan No. 14 Jakarta 10110 Indonesia Tel (62 21) 29 555 888 Fax (62 21) 350 1709

Equity Research Team

Sales team

Disclaimer

The information contained in this report has been taken from sources which we deem reliable. However, none of P.T. Danareksa Sekuritas and/or its affiliated companies and/or their respective employees and/or agents makes any representation or warranty (express or implied) or accepts any responsibility or liability as to, or

in relation to, the accuracy or completeness of the information and opinions contained in this report or as to any information contained in this report or any other such information or opinions remaining unchanged after the issue thereof.

We expressly disclaim any responsibility or liability (express or implied) of P.T. Danareksa Sekuritas, its affiliated companies and their respective employees and agents whatsoever and howsoever arising (including, without limitation for any claims, proceedings, action , suits, losses, expenses, damages or costs) which may be brought against or suffered by any person as a results of acting in reliance upon the whole or any part of the contents of this report and neither P.T. Danareksa Sekuritas, its

affiliated companies or their respective employees or agents accepts liability for any errors, omissions or misstatements, negligent or otherwise, in the report and any liability in respect of the report or any inaccuracy therein or omission there from which might otherwise arise is hereby expresses disclaimed.

The information contained in this report is not be taken as any recommendation made by P.T. Danareksa Sekuritas or any other person to enter into any agreement with regard to any investment mentioned in this document. This report is prepared for general circulation. It does not have regards to the specific person who may

receive this report. In considering any investments you should make your own independent assessment and seek your own professional financial and legal advice.

[email protected] (62-21) 29555 888 ext. 3128

Novrita E. Putrianti [email protected] (62-21) 29555 888 ext. 3132

Ehrliech Suhartono

[email protected] (62-21) 29555 888 ext.3513 Construction

Maria Renata

[email protected] (62-21) 29555 888 ext. 3145

Yunita L. Nababan

[email protected] (62-21) 29555 888 ext.3512 Technical Analyst

Lucky Bayu Purnomo

[email protected] (62-21) 2955 888 ext. 3511 Consumer

Puti Adani

[email protected] (62-21) 29555 888 ext. 3125

Laksmita Armandani

[email protected] (62-21) 29555 888 ext.3504 Cement, Property

Antonia Febe Hartono

[email protected] (62-21) 29555 888 ext. 3109

Muhammad Hardiansyah

[email protected] (62-21) 29555 888 ext. 3121

Tuty Sutopo

[email protected] (62-21) 29555 888 ext. 3137

Upik Yuzarni

[email protected] (62-21) 29555 888 ext. 3139

Kevin Giarto

[email protected] (62-21) 2955 888 ext. 3530 Auto, Coal, Heavy Equip., Metal, Cement

Stefanus Darmagiri

[email protected] (62-21) 29555 888 ext.3508 Consumer, Tobacco, Property

Natalia Sutanto [email protected] (62-21) 29555 888 ext.3500 Head of Research, Strategy, Banking

Agus Pramono, CFA

[email protected] (62-21) 2955 888 ext. 3503 Retail

Adeline Solaiman

[email protected] (62-21) 2955 888 ext. 3506 Research Associate

Melati Laksmindra Isnandari