essays on financial econometrics and derivatives pricing · the unifying themes of this...

TRANSCRIPT

2012-11

Mateusz P. DziubinskiPhD Thesis

Department of economics anD businessaarHus uniVersitY • DenmarK

essays on financial econometricsand Derivatives pricing

Essays on Financial Econometrics and Derivatives Pricing

By Mateusz P. Dziubinski

A dissertation submitted to

Business and Social Sciences, Aarhus University,

in partial fulfilment of the requirements of

the PhD degree in

Economics and Management

Contents

Preface v

Summary vii

Chapter 1. Option Valuation with the Simplied ComponentGARCH Model 1

Chapter 2. Conditionally-Uniform Feasible Grid SearchAlgorithm 25

Chapter 3. Commodity Derivatives Pricing with InventoryEects 57

iii

Preface

This PhD dissertation was written in the period from February 2008to February 2012 during my studies at the Department of Economicsand Business at Aarhus University. I am grateful to the departmentand to the Center for Research in Econometric Analysis of Time Series(CREATES), funded by the Danish National Research Foundation, forgenerous nancial support in connection with courses and conferences.I am further grateful to CREATES for providing excellent researchfacilities.

A number of people have contributed to the making of this thesis.I would like to express my sincere gratitude to my main advisor TimoTeräsvirta for providing guidance and numerous insightful commentsand suggestions throughout my PhD studies. I am grateful for havinghad the opportunity to work with my co-author Christian Bach on oneof the chapters. I hope we can continue our collaboration in the yearsto come.

At Aarhus University I would like to thank the faculty and fel-low students. I would also like to thank CREATES, Department ofEconomics and Business, Department of Mathematics, and ComputerScience Department for providing outstanding courses, seminars, con-ferences, and support. Special thanks also to Steen Thorbjørnsen forshowing me that stochastic processes can be easy and Svend Erik Gra-versen for revealing the mysteries of stochastic calculus to me and evenspending his free time doing so.

At the Department of Economics and Business I would like tothank my fellow PhD students for providing me with a welcoming,friendly environment and opportunities to discuss economics, nanceand (un)related topics. Christian deserves my gratitude for sharing anoce with me and providing me with endless opportunities for conver-sation, debate and learning relevant to our common interests. Finally,I would like to thank Anders for accompanying me on our individualyet common journey in the probability theory wonderland.

Last but not least, I would like to thank my family for their con-tinuing love and support.

Mateusz "Matt" P. Dziubinski, Aarhus, February 2012.

v

vi PREFACE

The predefense was held on March 21, 2012. I would like to thankthe members of the assessment committee, Peter Christoersen, OlafPosch (chair), and Lars Stentoft for their comments and suggestionsfor improvements. Most of those have been incorporated into the dis-sertation.

Mateusz "Matt" P. Dziubinski, Aarhus, July 2012.

Summary

The unifying themes of this dissertation are nancial econometricsand derivatives pricing. An underlying topic is the price behavior of anancial asset, be it a stock market index or a commodity derivative,with an additional focus on the factors aecting this behavior, like thevolatility and inventory levels. Practical implementation issues arisingin applying the models, together with an empirical motivation for thewhy are emphasized over a purely theoretical model treatment anddevelopment or the sole focus on the how.

The thesis contains three independent chapters, of which the rsttwo can be viewed as contributions to nancial econometrics, whereasthe third chapter has to do with derivatives pricing. In the rst chapter,entitled "Option Valuation with the Simplied Component GARCHModel", I introduce the Simplied Component GARCH (SCGARCH)option pricing model, show and discuss sucient conditions for non-negativity of the conditional variance, apply the model to both low-frequency and high-frequency nancial data, and consider the optionvaluation, comparing the model performance with similar models fromthe literature. Two volatility components in my model allow me tosatisfactorily model time structure of volatility.

The SCGARCH model builds on Engle and Lee (1999), Heston andNandi (2000), and Christoersen et al. (2008) (hereafter referred to asCJOW) models. Engle and Lee (1999) introduced the volatility com-ponent model in the GARCH context, while Heston and Nandi (2000)introduced a model with a closed-form solution for the European calloption-pricing formulas. The CJOW model is a generalization of theHeston and Nandi model allowing for a time-varying long-run com-ponent. The SCGARCH model is a simplied variant of the CJOWmodel, in which the non-negativity of the conditional variance is en-sured.

In the second chapter, entitled "Conditionally-Uniform FeasibleGrid Search Algorithm", I present and evaluate a numerical optimiza-tion method (together with an algorithm for choosing the startingvalues) pertinent to the constrained optimization problem where thevariables have to satisfy a sequentially dependent set of constraints.In practice, these arise (for instance) in the estimation of the modelswith inequality constraints, in particular GARCH models such as theEngle and Lee (1999) GARCH model and the Simplied Component

vii

viii Summary

GARCH (SCGARCH) model. The numerical optimization method, theConditionally-Uniform Feasible Grid Search (CUFGS), is essentially aparticular kind of a random grid search coupled with a constrainedfeasible Sequential Quadratic Programming (SQP) algorithm.

One of the reasons for developing it are the problems encounteredwhen using non-specialized gradient-based algorithms due to con-strained feasible space requirement and scaling. For example, in rela-tion to the Broyden-Fletcher-Goldfarb-Shanno (BFGS) algorithm, pop-ular among econometricians, Nocedal and Wright (2006) write:

(1) BFGS updating is generally less eective for constrained prob-

lems than in the unconstrained case because of the requirement

of maintaining a positive denite approximation to an under-

lying matrix that often does not have this property.(2) SQP methods are most ecient if the number of active con-

straints is nearly as large as the number of variables, that is,

if the number of free variables is relatively small. They re-

quire few evaluations of the functions, in comparison with aug-

mented Lagrangian methods, and can be more robust on badly

scaled problems.

I also provide the objective function and analytical gradient com-putation algorithms for the SCGARCH model, which are useful for thepractical implementation purposes.1

In the third chapter, "Commodity Derivatives Pricing with In-ventory Eects" (written jointly with Christian Bach), we introducetractable models for commodity derivatives pricing with inventory andvolatility eects, introduce a new, maturity-wise calibration methodcompatible with these models and apply it to modeling the commodityderivatives associated with the crude oil market.

The role of inventories in explaining price and volatility of com-modities has been studied in several papers. Brennan (1958) and Telser(1958) are early studies on the eect of the level of inventory on agricul-tural commodities, but the inventory eect has also been documentedfor metals (Ng and Pirrong (1994)) and oil and natural gas markets(Geman and Ohana (2009)). Instead of relying on a proxy for inven-tory data, we use weekly data on oil inventories. Geman and Nguyen(2005) construct a database of soybean inventory over a 10-year periodand show that volatility can be written as an exact inverse functionof inventory. In this chapter we do not nd such a clear relationship,

1To implement MLE in practice it is useful to have the analytical gradient.There are at least two reasons for that. First, in case of GARCH models estimationusing gradient-based optimization the analytical gradient is more accurate than itsnumerical approximation, see (Zivot, 2009, Section 5.1) and Brooks et al. (2001).Second, it may also be applied for computing the outer-product gradient (OPG)estimate of the information matrix.

Summary ix

although we see strong signs of the relationship between inventory andvolatility being negative.

We contribute to the existing literature in several respects. First,whereas the previous literature uses futures data for investigating therelationship between inventory and volatility, we use the informationavailable in options traded on futures. Second, performance assessmentin the previous literature has primarily evolved around explaining mo-ments of data or forecasting prices of futures. Instead, we asses theperformance of our model by considering both its ability of explain-ing prices in-sample and out-of-sample assessing both the pricing-performance and the hedging-performance of the models. Third, wemodel the futures surface rather than the spot price process, and limitthe number of parameters to calibrate (using the observed inventoryprocess instead of a latent one). We introduce a new, maturity-wise cal-ibration method compatible with this modeling methodology. Fourth,we use actual data on inventories rather than a proxy. Fifth, our modelis very exible and allows for analyzing several dierent types of rela-tionships between inventory and volatility.

Bibliography

Brennan, M. J. (1958). The supply of storage. The American Economic

Review 48 (1), 5072.Brooks, C., S. P. Burke, and G. Persand (2001). Benchmarks andthe accuracy of GARCH model estimation. International Journal ofForecasting 17 (1), 45 56.

Christoersen, P., K. Jacobs, C. Ornthanalai, and Y. Wang (2008).Option valuation with long-run and short-run volatility components.Journal of Financial Economics 90 (3), 272297.

Engle, R. F. and G. G. J. Lee (1999). A permanent and transi-tory component model of stock return volatility. In R. F. Engleand H. White (Eds.), Cointegration, Causality, and Forecasting: A

Festschrift in Honuor of Clive W.J. Granger, pp. 475497. OxfordUniversity Press.

Geman, H. and V. Nguyen (2005). Soybean inventory and forwardcurve dynamics. Management Science 51 (7), 10761091.

Geman, H. and S. Ohana (2009). Forward curves, scarcity and pricevolatility in oil and natural gas markets. Energy Economics 31 (4),576585.

Heston, S. and S. Nandi (2000). A closed-form GARCH option valua-tion model. Review of Financial Studies 13 (3), 585625.

Ng, V. K. and S. C. Pirrong (1994). Fundamentals and volatility:Storage, spreads, and the dynamics of metals prices. The Journal ofBusiness 67 (2), 20330.

Nocedal, J. and S. Wright (2006). Numerical optimization (second ed.).Springer: Springer.

Telser, L. G. (1958). Futures trading and the storage of cotton andwheat. Journal of Political Economy 66 (3), 233255.

Zivot, E. (2009). Practical issues in the analysis of univariate GARCHmodels. In T. G. Andersen, R. A. Davis, J.-P. Kreiÿ, and T. Mikosch(Eds.), Handbook of Financial Time Series, pp. 113155. Springer.

xi

CHAPTER 1

Option Valuation with the Simplied Component

GARCH Model

1

OPTION VALUATION WITH THE SIMPLIFIEDCOMPONENT GARCH MODEL

MATT P. DZIUBINSKI

Abstract. We introduce the Simplied Component GARCH (SC-GARCH) option pricing model, show and discuss sucient condi-tions for non-negativity of the conditional variance, apply it tolow-frequency and high-frequency nancial data, and consider theoption valuation, comparing the model performance with simi-lar models from the literature. Two volatility components in ourmodel, short-term and long-term, allow us to model time-structureof volatility.

JEL Classication. G12, C32.

1. Introduction

In this paper we introduce a discrete-time volatility model in whichthe conditional variance of the underlying asset follows a particularGARCH process. Our model can be used for option pricing, while twovolatility components allow us to model time structure thereof.

The model builds on Engle and Lee (1999), Heston and Nandi (2000)and Christoersen et al. (2008) (hereafter referred to as CJOW) mod-els. The model by Engle and Lee (1999) introduced the volatility com-ponent model in the GARCH context, while Heston and Nandi (2000)introduced a model with a closed-form solution for the European calloption-pricing formulas. The CJOW model is a generalization of theHeston and Nandi model allowing for a time-varying long-run com-ponent. Our model is a simplied specication of the CJOW model,which solves the problem of ensuring the non-negativity of the condi-tional variance.

Date: August 7, 2012.2000 Mathematics Subject Classication. Primary 37M10, 62M10, 91B84; Sec-

ondary 62P05.Key words and phrases. Stochastic volatility, volatility components, GARCH,

option pricing.We wish to thank Timo Teräsvirta for a discussion regarding non-negativity con-

ditions. We acknowledge nancial support by the Center for Research in Economet-ric Analysis of Time Series, CREATES, funded by the Danish National ResearchFoundation. All errors, omissions and mistakes are author's own responsibility.

2

OPTION VALUATION WITH THE SCGARCH MODEL 3

The paper proceeds as follows. In Section 2 we provide basic deni-tions and notation. We introduce the model in Section 3 (in which wealso discuss the non-negativity conditions), and discuss the estimationthereof in Section 4. In Section 5 we present the estimation results.Section 6 is devoted to option pricing, and, nally, Section 7 containsour conclusions.

2. Basic Definitions and Notation

We assume as given a probability space (Ω,F , P ) and a ltration F =(Ft)t∈T, where, depending on the context, we shall assume T = Z+ orT = Z ∩ [0, T ], T > 0 or T = Z ∩ [−1, T ], T ≥ 0. We refer to P as thephysical probability measure and we call (Ω,F ,F, P ) a ltered physicalprobability space. We shall also use probability measure Q on (Ω,F)and refer to it as the risk-neutral probability measure.

A stochastic process X on (Ω,F , P ) is a collection of R-valued randomvariables (Xt)t∈T, and we denote it by X = (Xt)t∈T.

The process X is said to be adapted if Xt ∈ Ft ∀t ∈ T (that is, it is Ftmeasurable for each t ∈ T).

The process X is said to be predictable if Xt ∈ Ft−1 ∀t ∈ T, and wedenote this by X ∈ P .The process X is said to be (F, P )-white noise with mean µX and

variance σ2X , writtenX

P∼ WN(µX , σ2X) if and only if, under probability

measure P , X has mean µX ∈ R and covariance function γ(s, t) =σ2Xδ|t−s|, where δh := 10(h) is the Kronecker delta and σ2

X ∈ R++.

The process X is said to be (F, P )-Gaussian white noise with mean

µX and variance σ2X , written X

P∼ GWN(µX , σ2X) if and only if X

P∼WN(µX , σ

2X) and Xt

P∼ N (µX , σ2X) ∀t ∈ T.

First-order partial dierential operator with respect to x is denoted ∂x.

For further details regarding stochastic processes and time series werefer the reader to Protter (2005) and Brockwell and Davis (1991).

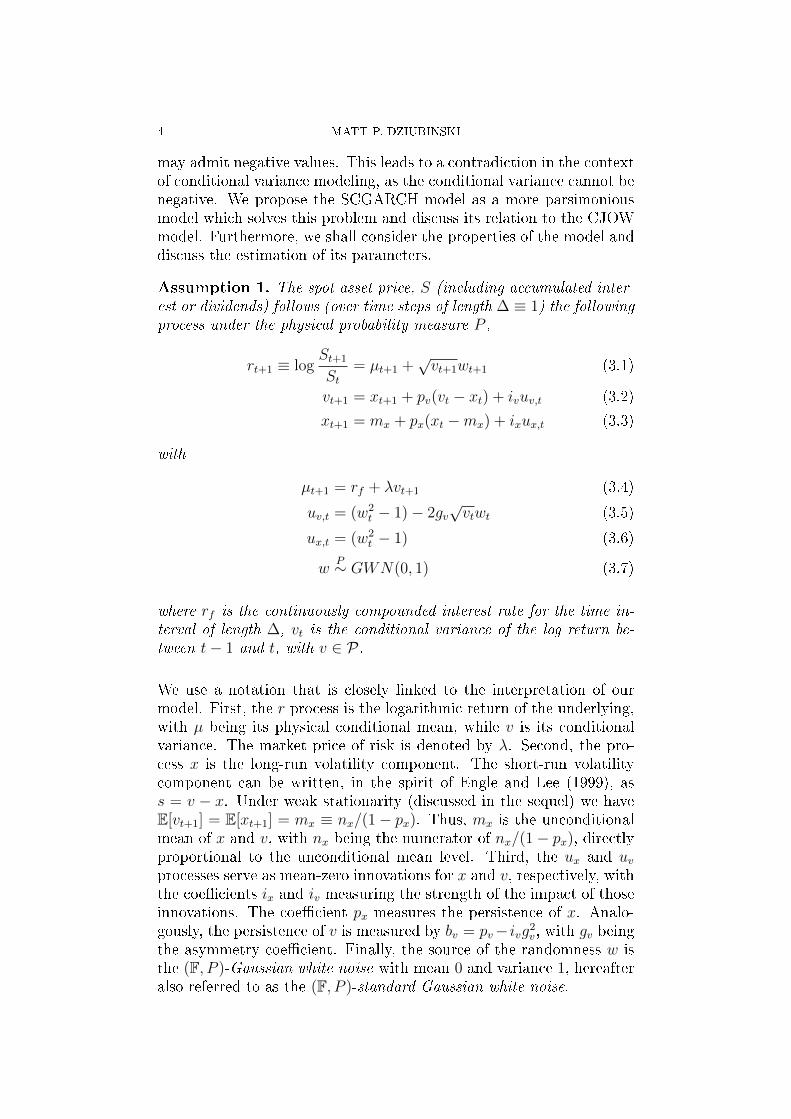

3. The Model

We begin by presenting the SCGARCH and the CJOW models. Theadvantages of the CJOW model are the existence of a (quasi-)closed-form solution for the option pricing formulas, improved ability to modelthe smirk and the path of spot volatility and, distinctively, the ability tomodel the volatility term structure for details, see Christoersen et al.(2008). A problem with this model is that the volatility components

4 MATT P. DZIUBINSKI

may admit negative values. This leads to a contradiction in the contextof conditional variance modeling, as the conditional variance cannot benegative. We propose the SCGARCH model as a more parsimoniousmodel which solves this problem and discuss its relation to the CJOWmodel. Furthermore, we shall consider the properties of the model anddiscuss the estimation of its parameters.

Assumption 1. The spot asset price, S (including accumulated inter-est or dividends) follows (over time steps of length ∆ ≡ 1) the followingprocess under the physical probability measure P ,

rt+1 ≡ logSt+1

St= µt+1 +

√vt+1wt+1 (3.1)

vt+1 = xt+1 + pv(vt − xt) + ivuv,t (3.2)

xt+1 = mx + px(xt −mx) + ixux,t (3.3)

with

µt+1 = rf + λvt+1 (3.4)

uv,t = (w2t − 1)− 2gv

√vtwt (3.5)

ux,t = (w2t − 1) (3.6)

wP∼ GWN(0, 1) (3.7)

where rf is the continuously compounded interest rate for the time in-terval of length ∆, vt is the conditional variance of the log return be-tween t− 1 and t, with v ∈ P.

We use a notation that is closely linked to the interpretation of ourmodel. First, the r process is the logarithmic return of the underlying,with µ being its physical conditional mean, while v is its conditionalvariance. The market price of risk is denoted by λ. Second, the pro-cess x is the long-run volatility component. The short-run volatilitycomponent can be written, in the spirit of Engle and Lee (1999), ass = v − x. Under weak stationarity (discussed in the sequel) we haveE[vt+1] = E[xt+1] = mx ≡ nx/(1− px). Thus, mx is the unconditionalmean of x and v, with nx being the numerator of nx/(1− px), directlyproportional to the unconditional mean level. Third, the ux and uvprocesses serve as mean-zero innovations for x and v, respectively, withthe coecients ix and iv measuring the strength of the impact of thoseinnovations. The coecient px measures the persistence of x. Analo-gously, the persistence of v is measured by bv = pv− ivg2

v , with gv beingthe asymmetry coecient. Finally, the source of the randomness w isthe (F, P )-Gaussian white noise with mean 0 and variance 1, hereafteralso referred to as the (F, P )-standard Gaussian white noise.

OPTION VALUATION WITH THE SCGARCH MODEL 5

3.1. Non-Negativity of the Conditional Variance. First, we shalllook at the CJOW model and consider the issues regarding the non-negativity of the conditional variance arising in its application.

3.1.1. CJOWModel. First, recall that Christoersen et al. (2008) modelcan be rewritten in our notation, replacing (3.6) with

ux,t = (w2t − 1)− 2gx

√vtwt (3.8)

and keeping the remaining equations intact.

The problem with this specication is that there is no guarantee onnon-negativity of v and since v is the conditional variance process, wearrive at a possible contradiction. In order to examine the seriousnessof the problem, we perform a simulation study and analyze the behaviorof the model.

3.1.2. CJOWModel Simulation Study. We perform a simulation studyto examine the behavior of this model performing a grid search withrespect to px searching from 0.0 to 1.0 with a step size of 0.001. Wedo this both for the original CJOW model and a deterministic versionthereof (i.e. the one where the driving noise process is assumed tobe identically equal to zero instead of a standard GWN), xing all theother parameter values to those in Table 1 in Christoersen et al. (2008)(for convenience, we reproduce it in Table 1) in addition setting rfto 1.000× 10−1. We choose this particular parameter value, since it isthe one used by Christoersen et al. (2008) to dierentiate between theComponent and the Persistent Component (px = 1) models. Further-more, the reason we consider the unit interval as the parameter rangeis that for px < 0 non-negativity issues arise immediately (as we shallshow later on), while px > 1 leads to non-stationarity (in particular,the explosiveness of x and, consequently, v). For purposes of this study,T = Z ∩ [0, T ], T = 1, 000.

We divide the set of px coecient values into invalid and valid values,where the invalid ones are those that lead to negative values of v. Wend that the low parameter values are invalid, while the higher onesare valid the boundary being at approximately 0.9. This means forall px < 0.9 in our simulation study there exists a t(px) ∈ T such

that vt(px) < 0. Note, that in practice this leads to v1/2t(px) returning

6 MATT P. DZIUBINSKI

T = 1,000 Simulationrf 1.000× 10−1

λ 2.092× 10+0

nx 8.208× 10−7

iv 1.580× 10−6

ix 2.480× 10−6

pv 6.437× 10−1

px 9.896× 10−1

gv 4.151× 10+2

gx 6.324× 10+1

Table 1. The coecient values used for the CJOWmodel simulation study.

NaN1 for the IEEE 7542 conforming architecture. Since commonlyapplied optimization routines will reject arguments leading to NaNs(or terminate with an error, leading to restarting the optimization withdierent starting values), this potentially explains the estimate of px =0.9896 obtained by Christoersen et al. (2008), which is very close to1. Hence, due to this numerical property of the model, one cannotnecessarily infer high persistence to hold in this case. This is becausethe high estimate might well be a numerical artifact, as opposed tobeing an empirical property of the data described by the model.

In addition, as we change the sample size T , the boundary value in-creases as the sample size increases. A possible interpretation of thisnding is that as the model runs for a longer time (i.e., as we have moredraws in the generated sample) the chance of drawing at least one neg-ative value increases. However, this is not solely due to Gaussianity ofw, because we obtain similar result for the deterministic version of themodel (i.e. even for a biased forecast) in fact, the boundary is higherfor the deterministic case than the stochastic one.

3.1.3. CJOW Model Discussion. We shall now proceed as follows:assuming the CJOW model, we rewrite (3.2) and (3.3), substituting(3.5) and (3.8), respectively:

vt+1 = xt+1 + pv(vt − xt) + iv((w2

t − 1)− 2gv√vtwt

)(3.9)

xt+1 = nx + pxxt + ix((w2

t − 1)− 2gx√vtwt

)(3.10)

1The term NaN stands for Not a Number. Here it results from applying thesquare root function to argument outside its domain, due to attempt to take thesquare root of a negative number.

2IEEE Standard 754 is a oating-point arithmetic standard, the most commonoating-point representation of real numbers today on computers for further ref-erence, see IEEE Task P754 (2008).

OPTION VALUATION WITH THE SCGARCH MODEL 7

where

nx = mx(1− px). (3.11)

Rearranging terms, we obtain

xt+1 = nx + pxxt − 2ixgx√vtwt + ix

((w2

t − 1))

(3.12)

= nx − ix + pxxt + ix(wt − gx√vt)

2 − ixg2xvt. (3.13)

Now, assume px > 0 and v > 0. Consider two cases with respect to ix.If we assume ix < 0, we have, in (3.13), that −ixg2

xvt > 0 and −ix > 0 this, however, results in ix(wt − gx

√vt)

2 < 0. On the other hand,if we assume 0 < ix (and we may also want ix < nx < nx, so thatnx − ix > 0), then −ixg2

xvt < 0. Hence, we conclude that P (∃t ∈ T :xt < 0) > 0. However, since x is the long-run volatility component, itshould remain non-negative over time.

Furthermore, even if we assume x = 03, we obtain

vt+1 = pvvt + iv((w2

t − 1)− 2gv√vtwt

)(3.14)

= pvvt + iv(w2t − 2gv

√vtwt + g2

vvt − g2vvt − 1

)(3.15)

= −iv + pvvt + iv((wt − gv

√vt)

2 − g2vvt)

(3.16)

= −iv + bvvt + iv (wt − gv√vt)

2(3.17)

where

bv = pv − ivg2v . (3.18)

Now, for all iv 6= 0, P (∃t ∈ T : vt < 0) > 0. In fact, we can obtain

the result for an arbitrary t ∈ T, using (3.17) and the fact that wP∼

GWN(0, 1):

P (vt+1 < 0|vt > 0) (3.19)

= P (−iv + bvvt + iv (wt − gv√vt)

2< 0|vt > 0) (3.20)

= P ((wt − gv√vt)

2< (iv − bvvt)/iv|vt > 0) (3.21)

= P (−(iv − bvvt)/iv < wt − gv√vt < (iv − bvvt)/iv|vt > 0) (3.22)

= P (−(iv − bvvt)iv

+ gv√vt < wt <

(iv − bvvt)iv

+ gv√vt | vt > 0) > 0,

(3.23)

as long as the interval(−(iv − bvvt)/iv + gv

√vt, (iv − bvvt)/iv + gv

√vt)

is non-empty.

An analogous result can be obtained for the x process. However, inorder to show the possibility of the negative conditional variance, theexistence result is sucient.

3Note that this is the weakest assumption possible to ensure non-negativity ofx, i.e., x ≥ 0 weaker than assuming x > 0.

8 MATT P. DZIUBINSKI

We conclude that assuming a non-zero skewness parameter gx leads toa model that can result in negative values for the volatility components.

Note, that this is an inherent problem of the CJOW model per se in particular, this is not merely a peripheral problem limited to agiven particular numerical treatment of the model (as in, for instance,particular discretization schemes applied to the Heston model). Thisalso implies that the numerical optimization problem arising in theestimation of the CJOWmodel will, in general, be an ill-posed problem,due to inherent numerical instability associated with the presence ofthe NaN results on the IEEE 754 conforming architecture.

3.1.4. Heston-Nandi GARCH(2,2) model. Christoersen et al. (2004,Section 4.2) provide the mapping between CJOW and Heston-NandiGARCH(2,2). We can write the conditional variance in the componentmodel as a Heston-Nandi GARCH(2,2) process.

rt+1 = rf + λht+1 +√ht+1zt+1 (3.24)

ht+1 = w + b1ht + b2ht−1 + a1(zt − c1

√ht)

2 + a2(zt−1 − c2

√ht−1)2

(3.25)

zP∼ GWN(0, 1) (3.26)

where

a1 = iv + ix (3.27)

a2 = −(pxiv + pvix) (3.28)

b1 = (px + pv)−(ivgv + ixgx)

2

a1

(3.29)

b2 =−(pxivgv + pvixgx)

2

a2

− pxpv (3.30)

c1 =gviv + gxix

a1

(3.31)

c2 = −pxgviv + pvgxixa2

(3.32)

w = (nx − ix)(1− pv)− iv(1− px) (3.33)

Note that we can easily ensure non-negativity of the conditional vari-ance in the HN-GARCH(2,2) model (HN) imposing (sucient) condi-tions given by the following inequality constraints:

w > 0, b1 > 0, b2 > 0, a1 > 0, a2 > 0 (3.34)

As such, the original, unrestricted HN model does not suer from thelack of simple non-negativity conditions. In contrast, nonlinear param-eter restrictions (3.27)(3.33) are precisely what makes it quite dicult

OPTION VALUATION WITH THE SCGARCH MODEL 9

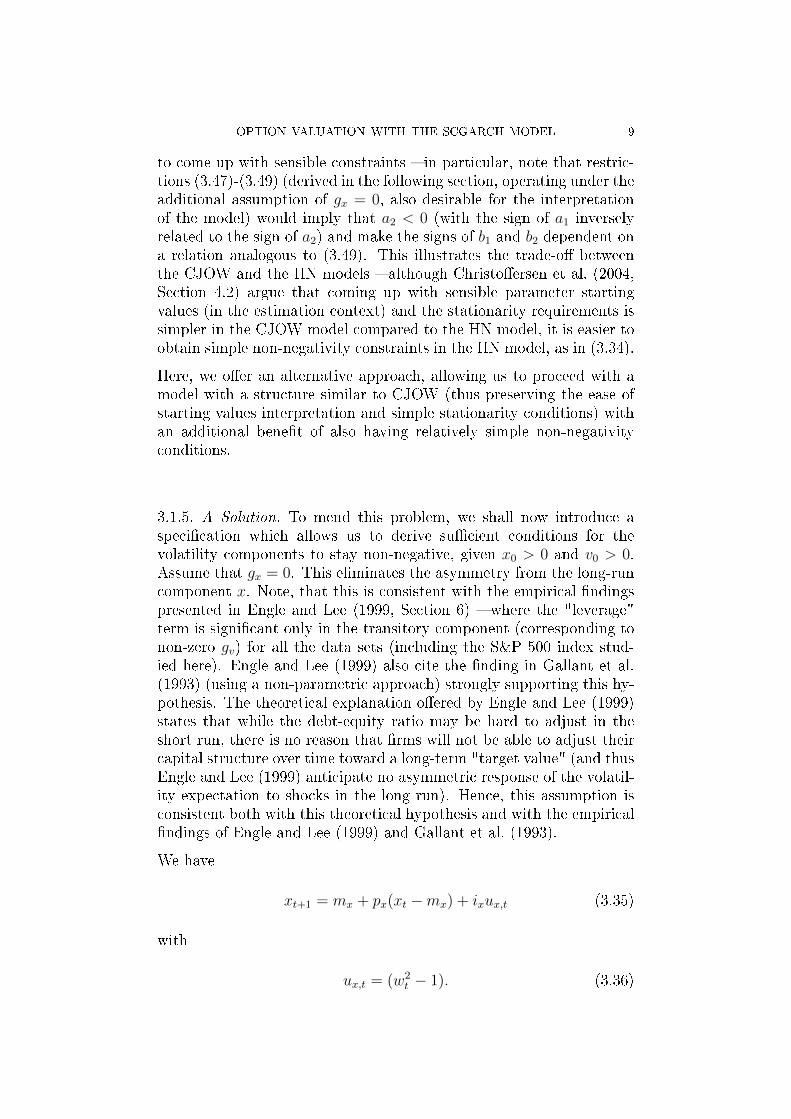

to come up with sensible constraints in particular, note that restric-tions (3.47)-(3.49) (derived in the following section, operating under theadditional assumption of gx = 0, also desirable for the interpretationof the model) would imply that a2 < 0 (with the sign of a1 inverselyrelated to the sign of a2) and make the signs of b1 and b2 dependent ona relation analogous to (3.49). This illustrates the trade-o betweenthe CJOW and the HN models although Christoersen et al. (2004,Section 4.2) argue that coming up with sensible parameter startingvalues (in the estimation context) and the stationarity requirements issimpler in the CJOW model compared to the HN model, it is easier toobtain simple non-negativity constraints in the HN model, as in (3.34).

Here, we oer an alternative approach, allowing us to proceed with amodel with a structure similar to CJOW (thus preserving the ease ofstarting values interpretation and simple stationarity conditions) withan additional benet of also having relatively simple non-negativityconditions.

3.1.5. A Solution. To mend this problem, we shall now introduce aspecication which allows us to derive sucient conditions for thevolatility components to stay non-negative, given x0 > 0 and v0 > 0.Assume that gx = 0. This eliminates the asymmetry from the long-runcomponent x. Note, that this is consistent with the empirical ndingspresented in Engle and Lee (1999, Section 6) where the "leverage"term is signicant only in the transitory component (corresponding tonon-zero gv) for all the data sets (including the S&P 500 index stud-ied here). Engle and Lee (1999) also cite the nding in Gallant et al.(1993) (using a non-parametric approach) strongly supporting this hy-pothesis. The theoretical explanation oered by Engle and Lee (1999)states that while the debt-equity ratio may be hard to adjust in theshort run, there is no reason that rms will not be able to adjust theircapital structure over time toward a long-term "target value" (and thusEngle and Lee (1999) anticipate no asymmetric response of the volatil-ity expectation to shocks in the long run). Hence, this assumption isconsistent both with this theoretical hypothesis and with the empiricalndings of Engle and Lee (1999) and Gallant et al. (1993).

We have

xt+1 = mx + px(xt −mx) + ixux,t (3.35)

with

ux,t = (w2t − 1). (3.36)

10 MATT P. DZIUBINSKI

Rearranging (3.35) and substituting (3.36) we obtain

xt+1 = mx(1− px) + pxxt + ix(w2t − 1) (3.37)

= nx − ix + pxxt + ixw2t (3.38)

where

nx = mx(1− px). (3.39)

Note, that (3.38) follows the GMACH(1, 1) model by Yang and Bewley(1995)4. Now, in order to obtain non-negative values of x, we neednx > ix > 0 and px > 0. Furthermore, under weak stationarity (forwhich we also need |px| < 1) we have

E[xt+1] = mx ≡nx

1− px. (3.40)

This motivates our previous notation mx for the unconditional meanof x.

Inserting (3.38) and (3.5) into (3.2) yields:

vt+1 = xt+1 + pv(vt − xt) + ivuv,t (3.41)

= nx − ix + pxxt + ixw2t

+ pv(vt − xt) + ivuv,t (3.42)

= nx − ix + pxxt + ixw2t

+ pv(vt − xt) + iv((w2

t − 1)− 2gv√vtwt

). (3.43)

Rearranging terms and using pv = bv + ivg2v we have

vt+1 = nx − ix + pxxt + ixw2t

+ (bv + ivg2v)(vt − xt) + iv

(w2t − 1− 2gv

√vtwt

)(3.44)

= (nx − ix − iv) + (px − bv − ivg2v)xt + ixw

2t

+ bvvt + iv(w2t − 2gv

√vtwt + ivg

2v

)(3.45)

= (nx − ix − iv) + (px − pv)xt + bvvt

+ ixw2t + iv (wt − gv

√vt)

2(3.46)

Now, assuming bv > 0, iv > 0 and ix > 0, we have a sucient conditionfor non-negativity of v, which is (nx − ix − iv) + (px − pv)x > 0. Sincewe have already established conditions for non-negativity of x, we needto ensure that in addition to them, (nx − ix − iv) > 0, (px − pv) > 0and bv > 0. Thus, the joint sucient conditions for non-negativity of

4This is similar to assuming c = 0 in the model by Heston and Nandi (2000) ina way that we also obtain GMACH(1, 1) dynamics.

OPTION VALUATION WITH THE SCGARCH MODEL 11

the volatility components v and x are as follows:

px ≤ 1, bv > 0, iv > 0, ix > 0 (3.47)

nx > ix + iv (3.48)

px > pv > ivg2v > 0 (3.49)

Restrictions in (3.47) are analogous to those in Engle and Lee (1999).Note, that similarly to Engle and Lee (1999) we also assume that theweak stationarity restriction px < 1 holds. The economic interpre-tation of (3.48) is that the mean long-term volatility level has to besuciently high relative to the strength of the innovation impact (re-call from (3.40) that nx is the numerator of the unconditional mean,i.e. mx ≡ nx/(1− px)). The interpretation of (3.49), which can also bestated as px > bv > 0, is that the persistence of the long-run componenthas to be higher than the one of the short-run component and that theimpact of the innovation(s) to the short-run component cannot be asstrong as to outweigh the persistence.

Hereafter we shall denote our parameter vector by

θ := (rf , λ, nx, iv, ix, pv, px, gv)T

and the restricted parameter space

Θ := θ ⊆ Θ : (3.47)− (3.49),

where Θ ⊆ Rp, p = 8.

4. Maximum Likelihood Estimation

We shall now derive a Maximum Likelihood Estimator (MLE)5 for ourmodel. For notational convenience we assume that the sample includesan observation for t = 0. Hereafter we shall assume that non-negativityconditions (3.47)(3.49) hold.

First, note that by the assumptions (3.1)(3.7) we have that wP∼

GWN(0, 1) and v ∈ P . Using this and (3.1) yields rt|Ft−1P∼ N (µt, vt).

Hence, the conditional probability density function (PDF) of rt|Ft−1 is

f(rt|Ft−1) =1√2πvt

exp

(−(rt − µt)2

2vt

). (4.1)

5The kind of MLE we derive is called the conditional MLE in Hayashi (2000) see pp. 547549.

12 MATT P. DZIUBINSKI

Using (3.1) again and simplifying we obtain

f(rt|Ft−1) =1√2πvt

exp

(−(√vtwt)

2

2vt

)(4.2)

=1√2πvt

exp

(−vtw

2t

2vt

)(4.3)

=1√2πvt

exp

(−w

2t

2

). (4.4)

Now, we can formulate our MLE in terms of an M-estimator. If thePDFs are parametrized by a parameter vector θ then the M-estimatorusing the log-likelihood of the sample over t = 0, 1, ..., N can be writtenas:

θ = arg maxθ∈Θ

Qn(θ) (4.5)

Qn(θ) =1

N

N∑

t=0

`t(θ) (4.6)

`t(θ) = log f(rt|Ft−1; θ) (4.7)

= −1

2log(2π)− 1

2log(vt)−

1

2w2t . (4.8)

Note, that using proportional and monotonic transformations, we canstate our problem for the purposes of minimization as follows:

θ = arg minθ∈Θ

Qn(θ) (4.9)

Qn(θ) =N∑

t=0

lt(θ) (4.10)

lt(θ) = log(vt) + w2t . (4.11)

For the numerical details, including objective function computationalgorithm and analytical gradient formulas, we refer the reader to Dz-iubinski (2010).

5. Estimation Results

Due to the results in Dziubinski (2010) we choose Conditionally-UniformFeasible Grid Search (CUFGS) with Feasible Sequential Quadratic Pro-gramming (FSQP) to estimate the models. FSQP allows us to solve theconstrained optimization problem (4.9), while coupling it with CUFGSenables us to widen the search space thus increasing the chance ofconvergence.

OPTION VALUATION WITH THE SCGARCH MODEL 13

We use the S&P 500 index data to calculate the (log) returns. Wet our model to both daily (source: Yahoo Finance, period 1/3/19507/22/2009) and high-frequency (5-minute) data (source: Price-Data.comS&P 500, period 4/21/198212/6/2007 from Price-Data.com). For thepurposes of research reproducibility, we use the same starting valuesas the ones in the column Estimation Starting Values in Table 1 inDziubinski (2010).6

We have considered three methods of obtaining the standard errors the OPG method, the numerical Hessian, and the sandwich estimator.Since there are numerical issues present when inverting the numericalHessian (even if it is obtained using analytical rst derivatives), wechoose to report the OPG standard errors. 7

Note that looking at the estimates for two data sets sampled at dierentfrequencies is a way to empirically investigate temporal aggregationproperties of our model. See Zivot (2009, Section 3.4) for a discussionof temporal aggregation in a context of GARCH models.

The estimates obtained using the FSQP-AL CUFGS optimization algo-rithm8 appear in Table 2. The problems with the large standard errors(causing insignicance) were practically not encountered in case of theFSQP optimization (where we used sandwich estimation and only usedOPG or Hessian errors in case of numerical problems; the only problemwas with a NaN gv standard error in low-frequency data). This conrmsour belief that the choice of the optimization method matters a greatdeal. Unsurprisingly, as in the similar models in the term-structurecomponents GARCH literature, there are still some issues with esti-mating λ and gv. The persistence seems to be slightly lower in case ofthe low-frequency data (coecients pv and px) note, however, thatequality of pv and px means that CUFGS yielded px to be optimal atthe lower corner solution. Furthermore, pv constitutes the lower boundfor px generated by CUFGS.

The results for the FSQP-NL CUFGS optimization algorithm in Table3 are mostly similar to those discussed above. It can be seen (looking

6Note, that as Zivot (2009) reports, a poor choice of starting values can lead toan ill-behaved log-likelihood and cause convergence problems, which is why we usethe starting values that satisfy the non-negativity conditions.

7As an alternative, one could also use analytical Hessian. In fact, Fiorentiniet al. (1996) and Hafner and Herwartz (2008) report, in the context of GARCHestimation, that the analytical Hessian signicantly outperforms the approximation.However, in our model, this comes at a cost of calculating 82 = 64 derivatives (or,

ensuring that the estimates θ remain in Θ and using Qn ∈ C2(Θ) with symmetry

due to Young's Theorem, 8(8+1)2 = 36 derivatives). Also, bootstrapping the errors

is a possibility.8For a discussion of the FSQP-AL and the FSQP-NL CUFGS optimization al-

gorithms see Dziubinski (2010).

14 MATT P. DZIUBINSKI

at the estimates and associated standard errors) that gv seems to beestimated more accurately in this case.

Daily Data 5-minute DataT 14, 984 523, 068rf 5.604× 10−4 (1.048× 10−4) 2.685× 10−10 (1.548× 10−6)

λ −7.024× 10−1 (1.392× 10+0) −4.392× 10+0 (1.475× 10+0)nx 4.744× 10−6 (5.998× 10−7) 1.047× 10−7 (8.741× 10−9)

iv 2.320× 10−6 (4.376× 10−7) 2.742× 10−8 (1.785× 10−9)

ix 2.396× 10−6 (9.433× 10−7) 7.714× 10−8 (6.401× 10−9)pv 9.375× 10−1 (3.896× 10−3) 9.157× 10−1 (6.563× 10−3)px 9.375× 10−1 (7.828× 10−3) 9.157× 10−1 (6.652× 10−3)gv 2.183× 10+2 (NaN) 1.595× 10+1 (1.247× 10+2)

Qn(θ) −1.29423× 10+5 −6.7172× 10+6

Table 2. The estimates (standard errors in parenthe-ses) obtained for the S&P 500 data using FSQP-ALCUFGS optimization algorithm.

Daily Data 5-minute DataT 14, 984 523, 068rf 7.028× 10−4 (1.174× 10−4) 2.906× 10−29 (1.540× 10−6)

λ −4.007× 10−1 (1.488× 10+0) −3.913× 10+0 (1.465× 10+0)nx 4.040× 10−6 (8.989× 10−7) 1.049× 10−7 (2.714× 10−10)

iv 3.474× 10−6 (1.910× 10−8) 2.018× 10−10 (8.008× 10−5)

ix 5.336× 10−7 (1.097× 10−7) 1.047× 10−7 (8.008× 10−5)pv 9.460× 10−1 (4.777× 10−3) 9.155× 10−1 (1.350× 10−1)px 9.460× 10−1 (4.312× 10−2) 9.155× 10−1 (1.784× 10−4)gv 1.022× 10+2 (4.339× 10+0) 5.031× 10+2 (9.509× 10+1)

Qn(θ) −1.29362× 10+5 −6.71722× 10+6

Table 3. The estimates (standard errors in parenthe-ses) obtained for the S&P 500 data using FSQP-NLCUFGS optimization algorithm.

6. Option Pricing

We shall consider option pricing under our model. In general, there areseveral approaches to look at:

OPTION VALUATION WITH THE SCGARCH MODEL 15

(1) CJOW risk-neutralization using the conditional moment gen-erating function (MGF), based on Christoersen et al. (2008)

(2) Monte-Carlo, Empirical Martingale Simulation (EMS), basedon Duan and Simonato (1998)

(3) Monte-Carlo, Empirical Martingale Correction (EMC), basedon Chorro et al. (2010)

(4) alternative risk-neutralization method,(5) dierent model specication and derivation of the pertinent

non-negativity conditions:(a) change the source of randomness w so that it follows a

distribution with positive support,(b) change the v and x specication, e.g. formulate the equa-

tions in log terms in the spirit of an EGARCH model.

The pricing formulas using the analytical methods might be harder toderive (and would often be infeasible in the case of exotic options).The disadvantage of the Monte-Carlo-based pricing methods might beslower performance and, besides, they might need further adjustmentto ensure the martingale property, see Duan and Simonato (1998) andChorro et al. (2010).

6.1. CJOW-MGF Approach. As our model is a simplication of theChristoersen et al. (2008) model we may, in principle, consider usingthe option-pricing formulas presented there. In practice, however, adiculty arises in attempts to apply them. In order to perform theoption valuation one needs to derive the moment generating function(MGF) for the component GARCH process (provided in Appendix Aof Christoersen et al. (2008)), specify the dynamics under the risk-neutral measure Q (provided in Appendix B of Christoersen et al.(2008)) and proceed with the option-valuation formula (given in section4.4 of Christoersen et al. (2008)). The problem arises in the secondstep, the risk-neutralization.

Following Christoersen et al. (2008) we need EQ[exp(rt+1)] = exp(rf ),which requires that

rt+1 ≡ logSt+1

St= µQt+1 +

√vt+1w

Qt+1 (6.1)

with

µQt+1 = rf −1

2vt+1. (6.2)

This in turn implies that

wQt+1 = wt+1 + (λ+1

2)√vt+1. (6.3)

16 MATT P. DZIUBINSKI

We also want to ensure the equality of the conditional variances underthe two measures:

VP [rt+1|Ft] = VQ[rt+1|Ft]. (6.4)

We therefore need to have equal variance innovations under the twomeasures that is

(wt − gi√vt)

2 = (wQt − gQi√vt)

2, i = v, x. (6.5)

This can be achieved by dening the risk-neutral parameters:

gQi = gi + λ+1

2, i = v, x. (6.6)

Now, the problem is that in our specication we have

gx = 0. (6.7)

Thus

gQx = λ+1

2. (6.8)

This means

gQx = 0 ⇐⇒ λ = −1

2. (6.9)

Hence, without restricting the market price of risk λ to a value whichis not particularly realistic, we cannot ensure that the Q-dynamic isgoing to remain such that we stay within our class of models (where wecan apply the sucient conditions for non-negativity of the conditionalvariance).

6.2. Empirical Martingale Simulation (EMS). EMS is a variance-reduction method ensuring the martingale property to be used withMonte Carlo pricing. The problem from our point of view is, how-ever, that the EMS relies on the formulation of the model under theQ measure that is, a prior risk-neutralization. However, our model(similarly to CJOW) is stated under the P measure, so analytical risk-neutralization would be required. But then, the one available method(CJOW, discussed above) is not applicable if we want to stay withinour class of models. This excludes the EMS from any further consid-erations.

6.3. Empirical Martingale Correction (EMC). The Empirical Mar-tingale Correction method is, in fact, inspired by the EMS, see Chorroet al. (2010). The fundamental dierence is that it is applicable tothe models stated under the P measure, such as ours. In this method,we make no assumption on the risk-neutralization (i.e. the shape ofthe pricing kernel, involving Radon-Nikodym derivative dQ

dP), and we

compute prices for options with time to maturity (T − t) by simulatingsampled paths of the stochastic model under the historical measure P.

OPTION VALUATION WITH THE SCGARCH MODEL 17

To rule out arbitrage opportunities, we directly impose risk neutralityconstraints. The ith sampled historical nal price for the underlying isdenoted by ST,i.

The Empirical Martingale Correction works such that the previouslysampled prices are replaced by:

ST,i =ST,i

1N

∑Ni=1 ST,i

Ster(T−t). (6.10)

The sampled average of ST,i is exactly equal to Ster(T−t), that is, the

risk neutral conditional expectation. With this approach, we only shiftthe historical distribution in a way that prevents arbitrage opportuni-ties by implicitly changing the drift of this distribution. Chorro et al.(2010) compare this approach with the ane Stochastic Discount Fac-tor (SDF) methodology in Cochrane (2002) and nd that the pricesobtained by these two methods are close to each other.

6.4. Option Pricing Results. Finally, we compare the option pricingresults in our model with those in the Black-Scholes-Merton modeland Heston-Nandi GARCH(1, 1) model (HN). In this section we usedaily data only. For comparison, we consider option pricing underthe SCGARCH model using the estimates obtained using FSQP-ALand FSQP-NL (applying CUFGS in both cases). We estimate the HNmodel using fOptions R package for details, see Wuertz (2007). Theestimation results are shown in Table 4.

N = 14,984 Daily Dataλ 3.451× 10+0

ω 1.139× 10−281

α 3.671× 10−6

β 9.005× 10−1

γ 1.196× 10+2

Log-Likelihood 88559.65Persistence 0.953Variance 7.806764× 10−5

Table 4. The estimates obtained for the S&P 500 dailydata: the HN model.

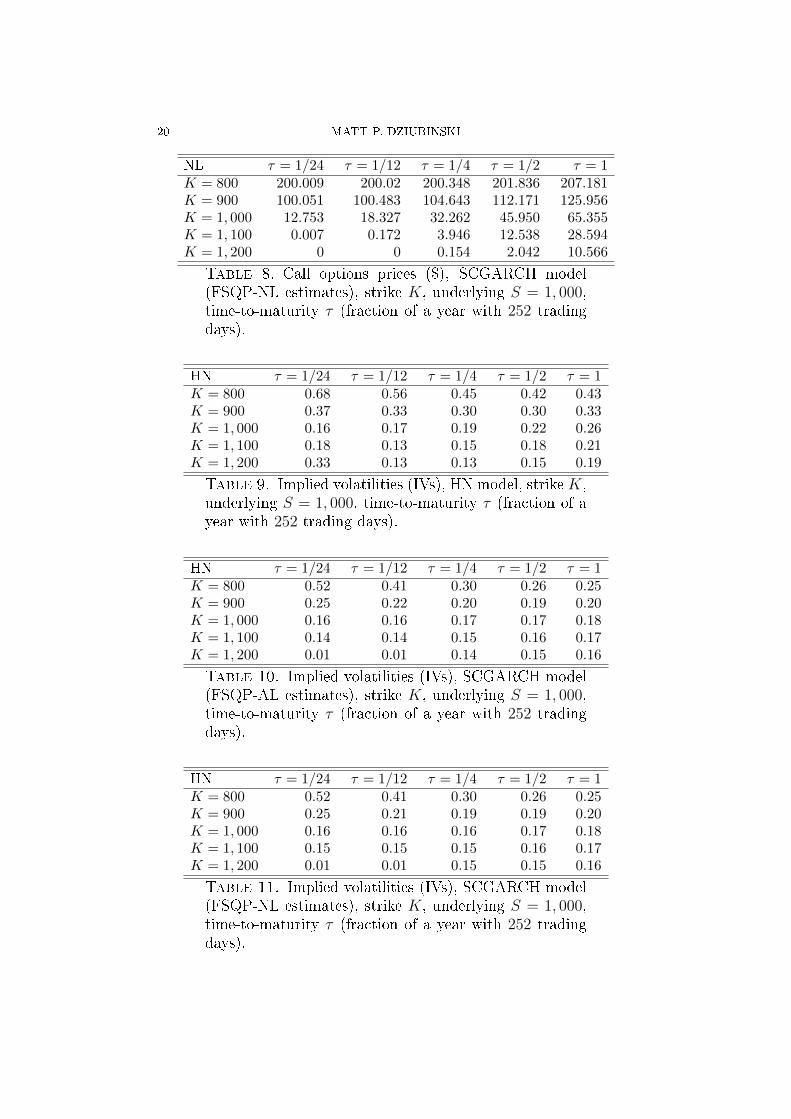

We present the pricing results across moneyness and maturity in Tables58, with implied volatilities (IVs) reported in Tables 911.

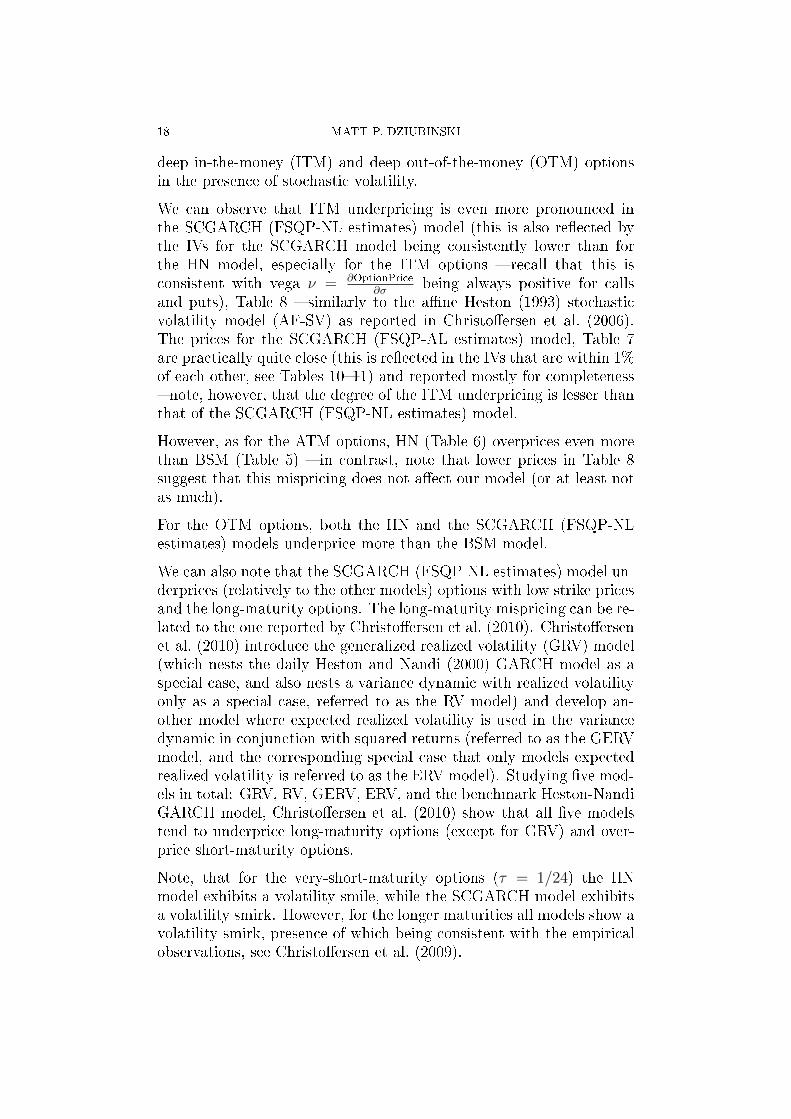

Note that Hull and White (1987) nd that the Black and Scholes (1973)model tends to overprice at-the-money (ATM) options and underprice

18 MATT P. DZIUBINSKI

deep in-the-money (ITM) and deep out-of-the-money (OTM) optionsin the presence of stochastic volatility.

We can observe that ITM underpricing is even more pronounced inthe SCGARCH (FSQP-NL estimates) model (this is also reected bythe IVs for the SCGARCH model being consistently lower than forthe HN model, especially for the ITM options recall that this isconsistent with vega ν = ∂OptionPrice

∂σbeing always positive for calls

and puts), Table 8 similarly to the ane Heston (1993) stochasticvolatility model (AF-SV) as reported in Christoersen et al. (2006).The prices for the SCGARCH (FSQP-AL estimates) model, Table 7are practically quite close (this is reected in the IVs that are within 1%of each other, see Tables 1011) and reported mostly for completeness note, however, that the degree of the ITM underpricing is lesser thanthat of the SCGARCH (FSQP-NL estimates) model.

However, as for the ATM options, HN (Table 6) overprices even morethan BSM (Table 5) in contrast, note that lower prices in Table 8suggest that this mispricing does not aect our model (or at least notas much).

For the OTM options, both the HN and the SCGARCH (FSQP-NLestimates) models underprice more than the BSM model.

We can also note that the SCGARCH (FSQP-NL estimates) model un-derprices (relatively to the other models) options with low strike pricesand the long-maturity options. The long-maturity mispricing can be re-lated to the one reported by Christoersen et al. (2010). Christoersenet al. (2010) introduce the generalized realized volatility (GRV) model(which nests the daily Heston and Nandi (2000) GARCH model as aspecial case, and also nests a variance dynamic with realized volatilityonly as a special case, referred to as the RV model) and develop an-other model where expected realized volatility is used in the variancedynamic in conjunction with squared returns (referred to as the GERVmodel, and the corresponding special case that only models expectedrealized volatility is referred to as the ERV model). Studying ve mod-els in total: GRV, RV, GERV, ERV, and the benchmark Heston-NandiGARCH model, Christoersen et al. (2010) show that all ve modelstend to underprice long-maturity options (except for GRV) and over-price short-maturity options.

Note, that for the very-short-maturity options (τ = 1/24) the HNmodel exhibits a volatility smile, while the SCGARCH model exhibitsa volatility smirk. However, for the longer maturities all models show avolatility smirk, presence of which being consistent with the empiricalobservations, see Christoersen et al. (2009).

OPTION VALUATION WITH THE SCGARCH MODEL 19

BSM τ = 1/24 τ = 1/12 τ = 1/4 τ = 1/2 τ = 1K = 800 202.266 204.526 213.506 226.904 253.488K = 900 102.550 105.127 116.270 133.473 165.920K = 1, 000 12.882 19.098 36.996 57.901 93.228K = 1, 100 0.005 0.199 4.848 16.757 43.962K = 1, 200 8× 10−10 6× 10−5 0.236 3.168 17.390

Table 5. Call options prices ($), BSM model, strike K,underlying S = 1, 000, time-to-maturity τ (fraction of ayear with 252 trading days).

HN τ = 1/24 τ = 1/12 τ = 1/4 τ = 1/2 τ = 1K = 800 202.209 204.527 213.628 227.459 254.714K = 900 102.495 105.334 117.605 135.623 168.677K = 1, 000 12.970 19.667 38.187 59.816 96.081K = 1, 100 0.069 0.078 3.711 15.900 44.827K = 1, 200 0.068 3× 10−6 0.052 2.041 16.403

Table 6. Call options prices ($), HN model, strike K,underlying S = 1, 000, time-to-maturity τ (fraction of ayear with 252 trading days).

AL τ = 1/24 τ = 1/12 τ = 1/4 τ = 1/2 τ = 1K = 800 200.009 200.023 200.448 202.11 207.738K = 900 100.073 100.613 105.064 112.791 126.780K = 1, 000 12.816 18.429 32.530 46.404 66.046K = 1, 100 0.004 0.127 3.768 12.513 28.883K = 1, 200 0 0 0.116 1.922 10.580

Table 7. Call options prices ($), SCGARCH model(FSQP-AL estimates), strike K, underlying S = 1, 000,time-to-maturity τ (fraction of a year with 252 tradingdays).

20 MATT P. DZIUBINSKI

NL τ = 1/24 τ = 1/12 τ = 1/4 τ = 1/2 τ = 1K = 800 200.009 200.02 200.348 201.836 207.181K = 900 100.051 100.483 104.643 112.171 125.956K = 1, 000 12.753 18.327 32.262 45.950 65.355K = 1, 100 0.007 0.172 3.946 12.538 28.594K = 1, 200 0 0 0.154 2.042 10.566

Table 8. Call options prices ($), SCGARCH model(FSQP-NL estimates), strike K, underlying S = 1, 000,time-to-maturity τ (fraction of a year with 252 tradingdays).

HN τ = 1/24 τ = 1/12 τ = 1/4 τ = 1/2 τ = 1K = 800 0.68 0.56 0.45 0.42 0.43K = 900 0.37 0.33 0.30 0.30 0.33K = 1, 000 0.16 0.17 0.19 0.22 0.26K = 1, 100 0.18 0.13 0.15 0.18 0.21K = 1, 200 0.33 0.13 0.13 0.15 0.19

Table 9. Implied volatilities (IVs), HN model, strikeK,underlying S = 1, 000, time-to-maturity τ (fraction of ayear with 252 trading days).

HN τ = 1/24 τ = 1/12 τ = 1/4 τ = 1/2 τ = 1K = 800 0.52 0.41 0.30 0.26 0.25K = 900 0.25 0.22 0.20 0.19 0.20K = 1, 000 0.16 0.16 0.17 0.17 0.18K = 1, 100 0.14 0.14 0.15 0.16 0.17K = 1, 200 0.01 0.01 0.14 0.15 0.16

Table 10. Implied volatilities (IVs), SCGARCH model(FSQP-AL estimates), strike K, underlying S = 1, 000,time-to-maturity τ (fraction of a year with 252 tradingdays).

HN τ = 1/24 τ = 1/12 τ = 1/4 τ = 1/2 τ = 1K = 800 0.52 0.41 0.30 0.26 0.25K = 900 0.25 0.21 0.19 0.19 0.20K = 1, 000 0.16 0.16 0.16 0.17 0.18K = 1, 100 0.15 0.15 0.15 0.16 0.17K = 1, 200 0.01 0.01 0.15 0.15 0.16

Table 11. Implied volatilities (IVs), SCGARCH model(FSQP-NL estimates), strike K, underlying S = 1, 000,time-to-maturity τ (fraction of a year with 252 tradingdays).

OPTION VALUATION WITH THE SCGARCH MODEL 21

One could add that another empirically interesting exercise would beto use the option prices in estimation, similarly to what Christoersenet al. (2008) suggested. Note, however, that in our model we do notuse analytical option pricing formulas, but instead apply a Monte-Carlomethod. On a single-core CPU (central processing unit) this methodis too slow to be used in this application. 9 A very promising ap-proach, however, would be to use parallelized many-core GPU (graph-ics processing unit) computation since MC is a so-called embarrass-ingly parallel problem, that would yield very signicant performanceimprovements. In particular, in an application of MC pricing involvingpath-dependent options, Joshi (2010) demonstrates that it is possibleto get accuracy of 2 × 10−4 in less than a ftieth of a second, con-cluding that GPU technology has rendered the Monte Carlo pricingof Asian options suciently fast that there is no longer any need foranalytic approximations. This approach would also make possible toinvestigate forecasting properties of the model.

7. Conclusions

This paper presents a discrete-time volatility model in which the un-derlying follows a process with conditional variance driven by the newSimplied Component GARCH process. It is a more parsimoniousmodel than the CJOW one and allows us to derive sucient conditionsfor non-negativity of the conditional variance.

Maximum likelihood estimation of the model is discussed.

We provide an empirical illustration, applying the model to the S&P500 index data. The results are consistent with our economic intuition.

We propose an option pricing method consistent with our model

9As a practical illustration, note the reported "0" prices for K = $1,200 optionsin Table 8. We believe these are numerical artifacts which result from the slowconvergence rate of the MC procedure while we have also obtained "0" prices evenfor K = $1,100 when using 1,000 MC iterations (which only took 4.3 s to compute),the results we report here have been obtained with 100,000 MC iterations, whichrequire over 120 min per table (each with 5 distinct strikes and 5 distinct maturities,giving 25 distinct options). Typically, S&P 500 data set containing 500 distinctoptions per day (with 100 distinct strikes ranging from $900 to $1,900 and 5 distinctmaturities of 15, 45, 75, 165, and 345 days) would require approximately 500

25 × 2 h= 40 h per 1 iteration of the optimization algorithm (since each iteration requiresoption pricing) for 1 day of data. With the average number of 750 iterations onewould expect total required execution time of approximately 30,000 h for 1 day ofdata. This underscores the fact that using single-core CPU is not enough for anempirically relevant estimation (with empirically relevant sample sizes) when usingthe MC pricing methods.

22 MATT P. DZIUBINSKI

The performance of the pricing method across moneyness and maturityis compared with that of the Heston-Nandi GARCH and Black-Scholes-Merton models. The results of the comparison suggest that our modelmight constitute a particularly interesting choice for the valuation ofthe ATM options.

Several of the future research directions and possible extensions tothis work are worth consideration regarding to the advanced grid-generation techniques and optimization algorithms and applications ofGPUs allowing for more advanced pricing and forecasting applications.We provide a number of approaches to achieve that in the respectivesections of this paper.

References

Brockwell, P. J. and R. A. Davis (1991): Time Series: Theoryand Methods, New York: Springer Verlag, 2nd ed.

Chorro, C., D. Guegan, and F. Ielpo (2010): Martingalizedhistorical approach for option pricing, Finance Research Letters, 7,2428.

Christoffersen, P., S. Heston, and K. Jacobs (2009): TheShape and Term Structure of the Index Option Smirk: Why Mul-tifactor Stochastic Volatility Models Work So Well, ManagementScience, 55, 19141932.

Christoffersen, P., K. Jacobs, B. Feunou, and N. Meddahi

(2010): The Economic Value of Realized Volatility, Working Paper.Christoffersen, P., K. Jacobs, and K. Mimouni (2006): AnEmpirical Comparison of Ane and Non-Ane Models for EquityIndex Options, Working Paper, McGill University.

Christoffersen, P., K. Jacobs, C. Ornthanalai, and

Y. Wang (2008): Option valuation with long-run and short-runvolatility components, Journal of Financial Economics, 90, 272297.

Christoffersen, P., K. Jacobs, and Y. Wang (2004): Op-tion Valuation with Long-run and Short-run Volatility Components,CIRANO Working Papers 2004s-56, CIRANO.

Cochrane, J. (2002): Asset Pricing, Princeton University Press.Duan, J.-C. and J.-G. Simonato (1998): Empirical MartingaleSimulation for Asset Prices, Management Science, 44, 12181233.

Dziubinski, M. P. (2010): Conditionally-Uniform Feasible GridSearch (CUFGS), CREATES Working Paper.

Engle, R. F. and G. G. J. Lee (1999): A Permanent and Transi-tory Component Model of Stock Return Volatility, in Cointegration,Causality, and Forecasting: A Festschrift in Honor of Clive W.J.Granger, University Press, 475497.

OPTION VALUATION WITH THE SCGARCH MODEL 23

Fiorentini, G., G. Calzolari, and L. Panattoni (1996): Ana-lytic Derivatives and the Computation of GARCH Estimates, Jour-nal of Applied Econometrics, 11, 399417.

Gallant, A. R., P. E. Rossi, and G. Tauchen (1993): NonlinearDynamic Structures, Econometrica, 871907.

Hafner, C. and H. Herwartz (2008): Analytical quasi maximumlikelihood inference in multivariate volatility models, Metrika, 67,219239.

Hayashi, F. (2000): Econometrics, Princeton University Press.Heston, S. and S. Nandi (2000): A closed-form GARCH optionvaluation model, Review of Financial Studies, 13, 585625.

Hull, J. C. and A. D. White (1987): The Pricing of Options onAssets with Stochastic Volatilities, Journal of Finance, 42, 281300.

IEEE Task P754 (2008): IEEE 754-2008, Standard for Floating-Point Arithmetic.

Joshi, M. (2010): Graphical Asian Options, Wilmott Journal, 2,97107.

Protter, P. E. (2005): Stochastic Integration and Dierential Equa-tions, Springer, 2nd ed.

Wuertz, D. (2007): fOptions: Financial Software Collection-fOptions. R package version 260.72, in Rmetrics.

Yang, M. and R. Bewley (1995): Moving average conditional het-eroskedastic processes, Economics Letters, 49, 367 372.

Zivot, E. (2009): Practical Issues in the Analysis of UnivariateGARCH Models, in Handbook of Financial Time Series, Springer,113155.

(Matt P. Dziubinski) CREATESSchool of Economics and Management

University of Aarhus

Building 1322, DK-8000 Aarhus C

Denmark

E-mail address, Matt P. Dziubinski: [email protected]

CHAPTER 2

Conditionally-Uniform Feasible Grid Search

Algorithm

25

CONDITIONALLY-UNIFORM FEASIBLE GRID

SEARCH ALGORITHM

MATT P. DZIUBINSKI

Abstract. We present and evaluate a numerical optimizationmethod (together with an algorithm for choosing the starting val-ues) pertinent to the constrained optimization problem where thevariables have to satisfy a sequentially dependent set of constraints.In practice, these arise (for instance) in the estimation of the mod-els with inequality constraints, in particular GARCH models suchas the Engle and Lee (1999) GARCH model and the SimpliedComponent GARCH (SCGARCH) model. We also provide algo-rithms for the objective function and analytical gradient compu-tation for SCGARCH. The method improves upon ad hoc modi-cations of unconstrained optimization algorithms (such as BFGSwith a penalized objective function) prevalent in practice and isfound to be more eective in nding the solution.

JEL Classication. C32, C51, C58, C61, C63, C88.

1. Introduction

In this paper we present a numerical optimization method applicable toconstrained optimization problems, where the variables have to satisfya sequentially dependent set (SDS) of constraints (i.e., the one involvingconstraints involving multiple variables, where a variable constrainedby a given relation is then involved in a subsequent constraint for an-other set of variables). The method, the Conditionally-Uniform Feasi-ble Grid Search (CUFGS), is essentially a particular kind of a randomgrid search coupled with a constrained feasible Sequential QuadraticProgramming (SQP) algorithm.

Date: August 7, 2012.2000 Mathematics Subject Classication. Primary 62F30, 65C60, 65Y20, 90C30,

90C55; Secondary 37M10, 62M10, 91B84.Key words and phrases. Constrained optimization, GARCH, infeasibility, infer-

ence under constraints, nonlinear programming, performance of numerical algo-rithms, SCGARCH, sequential quadratic programming.

We acknowledge nancial support by the Center for Research in Economet-ric Analysis of Time Series, CREATES, funded by the Danish National ResearchFoundation.

26

CONDITIONALLY-UNIFORM FEASIBLE GRID SEARCH ALGORITHM 27

We apply it to the estimation of the Engle and Lee (1999) GARCHmodel (hereafter referred to as EL) and the Simplied ComponentGARCH Model (SCGARCH) of Dziubinski (2011).

One of the reasons for developing it are the problems encounteredwhen using non-specialized (unconstrained) gradient-based optimiza-tion algorithms due to constrained feasible space requirement andscaling. For example, in relation to the Broyden-Fletcher-Goldfarb-Shanno (BFGS) algorithm, popular with econometricians, Nocedal andWright (2006) write:

(1) BFGS updating is generally less eective for constrained prob-lems than in the unconstrained case because of the requirementof maintaining a positive denite approximation to an underly-ing matrix that often does not have this property.

(2) SQP methods are most ecient if the number of active con-straints is nearly as large as the number of variables, that is,if the number of free variables is relatively small. They requirefew evaluations of the functions, in comparison with augmentedLagrangian methods, and can be more robust on badly scaledproblems.

Note that observation (2) in particular applies to the SCGARCHmodel,with 8 constraints and 8 variables.

As an unconstrained optimization algorithm, BFGS does not apply toconstrained optimization problems per se. However, it is often usedin conjunction with ad hoc modications (such as penalized objectivefunction), which are generally less eective. In addition, it is also nota good t for the badly scaled or highly constrained models (i.e., oneswhere the number of active constraints is nearly as large as the numberof variables) which is also often the case for the GARCH models withnon-negativity inequality constraints.

In contrast, our algorithm is specically designed for the SDS-constrainedoptimization problems. We illustrate its superior performance in twoapplications (estimation of two dierent GARCH models), both in aMonte Carlo study (with a known DGP, data-generating process) andon a real-world data (S&P 500 index returns). Another advantage ofthe CUFGS algorithm is that it be coupled with another algorithmother than FSQP (which extends it to the cases where the other op-timization method is known, but when one still faces the problem ofgenerating feasible starting values consistent with the constraints-SDS).In this study we focus on the CUFGS-FSQP coupling for empirical ap-plications.

28 MATT P. DZIUBINSKI

The paper proceeds as follows. In Section 2 we present the SCGARCHmodel and the Engle and Lee (1999) GARCH model. We discuss es-timation in Section 3. In Sections 4 and 5 we analyze the estimationalgorithms and show the results. Section 6 contains our conclusions.

In the Appendix, we also provide the objective function and analyticalgradient computation algorithms for SCGARCH, useful for the practi-cal implementation purposes.

2. The Models

For reference we present the SCGARH and the EL models; for detailssee Dziubinski (2011) and Engle and Lee (1999), respectively. Theobserved time-series (e.g., log return on the spot asset price), r follows(over time steps of length ∆ ≡ 1) the following process under the(physical) probability measure P ,

rt+1 ≡ logSt+1

St= µt+1 + εt+1 (2.1)

εt+1 =√vt+1wt+1 (2.2)

vt+1 = xt+1 + pv(vt − xt) + ivuv,t (2.3)

xt+1 = mx + px(xt −mx) + ixux,t (2.4)

with

µt+1 = rf + λvt+1 (2.5)

uv,t = (w2t − 1)− 2gv

√vtwt (2.6)

ux,t = (w2t − 1) (2.7)

wP∼ GWN(0, 1) (2.8)

where rf is the continuously compounded interest rate for the timeinterval of length ∆, vt is the conditional variance of the log returnbetween t − 1 and t, with v ∈ P . The process w is a Gaussian white

noise with mean 0 and variance 1, i.e., wtP∼ N (0, 1) ∀t ∈ T and w

P∼WN(0, 1) (under probability measure P , w has mean 0 and covariancefunction γ(s, t) = δ|t−s|, where δh := 10(h) is the Kronecker delta).

This model is a simplied specication of the Christoersen et al.(2008) model, solving the problem of ensuring non-negativity of theconditional variance. The sucient conditions for non-negativity ofvolatility components v and x are:

px ≤ 1, bv > 0, iv > 0, ix > 0 (2.9)

nx > ix + iv (2.10)

px > pv > ivg2v > 0 (2.11)

CONDITIONALLY-UNIFORM FEASIBLE GRID SEARCH ALGORITHM 29

We denote our parameter vector by

θSCGARCH := (rf , λ, nx, iv, ix, pv, px, gv)T

and the restricted parameter space by

ΘSCGARCH := θSCGARCH ⊆ ΘSCGARCH : (2.9)− (2.11),where ΘSCGARCH ⊆ RpSCGARCH , pSCGARCH = 8.

Now, we can obtain the Engle and Lee (1999) GARCH model fromthe SCGARCH model, replacing (2.5), (2.6), and (2.7) above with thefollowing:

µt+1 = rf (2.12)

uv,t = ε2t − xt (2.13)

ux,t = ε2t − vt (2.14)

The sucient conditions for non-negativity of volatility components vand x are:

0 > px ≤ 1, pv > 0, iv > 0, ix > 0, nx > 0 (2.15)

px > iv + pv > 0 (2.16)

pv > ix > 0 (2.17)

In this case, we denote our parameter vector by

θEL := (rf , nx, iv, ix, pv, px)T

and the restricted parameter space by

ΘEL := θEL ⊆ ΘEL : (2.15)− (2.17),where Θ ⊆ RpEL , pEL = 6.

Note that (2.15)-(2.17) involve two linear sequentially dependent con-straints, ix − pv < 0 and iv + pv − px < 0 in order to verify whetherpx satises its constraint one rst needs to know pv which must obeyits own constraint.

Constraints given by (2.9)-(2.11) involve three sequentially dependentconstraints (one non-linear and two linear, respectively): ivg

2v−pv < 0,

ix + iv − nx < 0, pv − px < 0 here, iv aects the rst two constraints(needed for pv and nx), while pv (from the rst constraint) is requiredto verify the subsequent constraint for px.

3. Maximum Likelihood Estimation

A statistical method used for estimating the models is the MaximumLikelihood Estimation (MLE), which involves maximizing an objectivefunction (called the (log)likelihood function) in order to obtain theestimates.

30 MATT P. DZIUBINSKI

Dziubinski (2011) shows that we can state our optimization problemas a constrained minimization problem:

θ = arg minθ∈Θ

QN(θ) (3.1)

QN(θ) =N∑

t=0

lt(θ) (3.2)

lt(θ) = log(vt) + w2t . (3.3)

where θ is a generic parameter specialized to θEL for the EL modeland to θSCGARCH for the SCGARCH model (with the rest of the entitiesspecialized analogously).

4. A Simulation Study of Estimation Method Choice

4.1. Overview. In this section we provide an overview of some of themethods to estimate the models under consideration.

We simulate each model using the coecient values given in Table 1(they are interesting in practice, since they have the same magnitude asthose in Table 1 of Dziubinski (2011)), omitting inapplicable parame-ters for the EL model, and estimate the parameters using the simulateddata and the following algorithms1:

(1) NM - Nelder-Mead(2) FR - Fletcher-Reeves(3) PR - Polak-Ribière(4) BFGS - Broyden-Fletcher-Goldfarb-Shanno(5) SA - Simulated Annealing(6) PG - Projected Gradient(7) SPG - Spectral Projected Gradient(8) FSQP - Feasible Sequential Quadratic Programming

The Nelder-Mead (also known as downhill simplex) algorithm is aderivative-free optimization method, FR and PR are nonlinear con-jugate gradient methods, BFGS is a quasi-Newton method. PG is anextension of the steepest descent method for unconstrained minimiza-tion, where a line search is performed over the direction of a projectedgradient. SPG is similar to PG, except accelerated convergence due tothe choice of the spectral step-length; see Birgin et al. (2000) for details.

1We use the implementations thereof provided by O2scl anobject-oriented library for numerical programming in C++ see:http://o2scl.sourceforge.net/. The exception is FSQP, which uses CF-SQP implementation see Lawrence et al. (1997).

CONDITIONALLY-UNIFORM FEASIBLE GRID SEARCH ALGORITHM 31

Simulation (DGP) Estimation Starting Valuesrf 1.000× 10−1 9.000× 10−2

λ 2.000× 10+0 1.800× 10+0

nx 8.000× 10−6 7.200× 10−6

iv 1.000× 10−6 9.000× 10−7

ix 2.000× 10−6 1.800× 10−6

pv 6.000× 10−1 5.400× 10−1

px 9.000× 10−1 8.100× 10−1

gv 4.000× 10+2 3.600× 10+2

Qn,SCGARCH −8.427097× 10+3 −6.228086× 10+3

Qn,EL −125, 348 −115, 476

Table 1. The coecient values used in the simulationstudy. Sample sizes NSCGARCH = 1,000 and NEL =15,000. Both in the simulation and in the estimationwe are omitting inapplicable parameters for the ELmodel.

SA is a probabilistic metaheuristic (convergence to an optimal solutionis not guaranteed) for the global derivative-free optimization. FSQPis a quadratic programming method applicable to the constrained op-timization problems. For the rst four algorithms, see Nocedal andWright (2006), for SA see Henderson et al. (2003) or Dreo et al. (2005),for PG see Kelley (1999) and for SPG see Birgin et al. (2000).

FSQP is based on Sequential Quadratic Programming (SQP), modiedso as to generate feasible iterates. Sequential quadratic programming(SQP) methods model the general constrained optimization problemby a quadratic programming subproblem at each iterate and denethe search direction to be the solution of this subproblem. It is im-portant to design the quadratic subproblem so that it yields a goodstep for the nonlinear optimization problem, see Nocedal and Wright(2006). A description of FSQP can be found in Lawrence et al. (1997).There are two FSQP algorithms: FSQP-AL and FSQP-NL. In theFSQP-AL (monotone line search), an Armijo type arc search (hencethe "A" in "FSQP-AL") is used with the property that the step of unitlength is eventually accepted, which is a requirement for superlinearconvergence. In the FSQP-NL algorithm the same eect is achievedby means of a nonmonotone search (hence the "N" in "FSQP-NL")along a straight line. In other words, in the FSQP-AL algorithm theobjective function decreases at each iteration, while in FSQP-NL wehave a decrease of the objective function within at most four iterations.For details, see Lawrence et al. (1997).

For reproducibility purposes, we use the default seed for the SimulatedAnnealing. To minimize the warm-up period we use the unconditional

32 MATT P. DZIUBINSKI

mean of v and x to initialize v0 and x0, that is, we set the startingvalues to mx derived from the starting values of nx and px.

Note, that McCullough and Renfro (1999) and Brooks et al. (2001)stress the importance of reporting the initial values provided to theGARCH estimation software. Without them, any conditional het-eroscedasticity model is only partially specied, because the elementson which the likelihood is conditioned are not specied if the initial val-ues are not given. McCullough and Renfro (1999) also report that theinitialization of the series, though often overlooked, can substantiallyaect the solution produced by the software.

4.2. Constraints. In practice we may actually need a constrainedminimization algorithm in order to ensure that the non-negativity con-ditions hold. Only the last three algorithms in our list are of this type(note, that PG and SPG only allow for hypercubic constraints, whileFSQP allows for nonlinear functional constraints).

A solution commonly used in practice, see for example in Rouah andVainberg (2007), is to implement a penalty, so that violating non-negativity conditions generates a large value of the objective function.For the methods requiring this modication, we adjust the algorithmsas follows:

Penalized-Objective-Function l(N, θ, w, v, x, r)Input: a parameter vector θ, starting values r0, v0, x0

Output: the objective function l ≡∑Nt=0 lt(θ)

1 if Positivity-Conditions(θ) 6= TRUE

2 then return Penalty

3 l ← Summand l0(θ, w, v, x, r)4 for t← 0 to (N − 1) do5 l← l + Summand lt+1(θ, w, v, x, r)6 return l

Penalized-Gradient ∇l(N, θ, w, v, x, r)Input: a parameter vector θ, starting values r0, v0, x0

Output: the gradient g ≡ ∇l(θ)1 if Positivity-Conditions(θ) 6= TRUE

2 then return Penalty

3 l ← Summand l0(θ, w, v, x, r)4 g ← Summand ∇l0(θ, w, v, x, r)5 for t← 0 to (N − 1) do6 l← l + Summand lt+1(θ, w, v, x, r)7 g ← g + Summand ∇lt+1(θ, w, v, x, r)8 return g

CONDITIONALLY-UNIFORM FEASIBLE GRID SEARCH ALGORITHM 33

The boolean expression Positivity-Conditions(θ) is TRUE ⇐⇒θ ∈ Θ, and FALSE otherwise. Analogously to Rouah and Vainberg(2007), Penalty is assumed constant and large enough to have the or-der of magnitude larger than the objective function evaluated at start-ing values.

4.3. Results with the known DGP optimization study for the

SCGARCH model. For the SCGARCH model the maximum num-ber of iterations is 1,000 in all of the cases2 The sample size N = 1, 000.

NM FR PRrf = 9.000× 10−2 = 9.000× 10−2 = 9.000× 10−2

λ 2.800× 10+0 = 1.800× 10+0 = 1.800× 10+0

nx = 7.200× 10−6 7.673× 10−6 7.671× 10−6

iv = 9.000× 10−7 4.946× 10−13 3.834× 10−14

ix = 1.800× 10−6 2.786× 10−6 2.748× 10−6

pv = 5.400× 10−1 = 5.400× 10−1 = 5.400× 10−1

px = 8.100× 10−1 = 8.100× 10−1 = 8.100× 10−1

gv = 3.600× 10+2 = 3.600× 10+2 = 3.600× 10+2

Time (s) 0.0× 10+0 1.3439× 10+2 1.34516× 10+2

Qn(θ) −6.244133× 10+3 −6.747140× 10+3 −6.741407× 10+3

Table 2. The estimated coecient values obtained inthe estimation study using NM, FR and PR. Penaltyset to 999, 999.999. Symbol = indicates that the valuesare equal to the initial values.

We use the starting values reported in the third column (denoted Esti-mation Starting Values) of Table 1. The results are reported in Tables2 and 3. We notice that almost every unconstrained optimization al-gorithm performs unsatisfactorily. This may be due to the dicultyensuring that the estimates remain in Θ. The Penalty encountered inthis case introduces non-smoothness of the objective function, whereasmany of the algorithms require smoothness for convergence. Similarly,Zivot (2009) reports that the GARCH log-likelihood function is not

2The reason for choosing this criterion as opposed to, say, maximum elapsedtime, is to ensure the reproducibility of the results, independent of the performanceof the computer hardware.

34 MATT P. DZIUBINSKI

SA PG SPGrf 9.008× 10−2 = 9.000× 10−2 9.003× 10−2

λ 1.800× 10+0 = 1.800× 10+0 = 1.800× 10+0

nx 3.917× 10−5 7.666× 10−6 5.381× 10−5

iv 1.079× 10−6 7.248× 10−233 4.167× 10−6

ix 3.702× 10−6 2.670× 10−6 2.960× 10−7

pv 5.398× 10−1 = 5.400× 10−1 = 5.400× 10−1

px 8.102× 10−1 = 8.100× 10−1 = 8.100× 10−1

gv 3.600× 10+2 = 3.600× 10+2 = 3.600× 10+2

Time (s) 1.72× 10−1 2.937× 100 2.75× 100

Qn(θ) −7.625983× 10+3 −6.729235× 10+3 −7.609727× 10+3

Table 3. The estimated coecient values obtained inthe estimation study using SA, PG and SPG. Penaltyset to 999, 999.999. Symbol = indicates that the valuesare equal to the initial values.

FSQP-AL FSQP-NLrf 9.908070× 10−2 1.084674× 10−1

λ 1.557766× 10+1 −9.986293× 10+1

nx 3.017787× 10−5 3.007165× 10−5

iv 3.068260× 10−7 1.509107× 10−7

ix 2.191491× 10−6 2.295927× 10−6

pv 2.525282× 10−1 1.805605× 10−1

px 6.252131× 10−1 6.280134× 10−1

gv 3.583449× 10+2 3.623615× 10+2

Time (s) 1.88× 10−1 7.66× 10−1

Qn(θ) −8.432699× 10+3 −8.435838× 10+3

Table 4. The estimated coecient values obtained inthe estimation study using FSQP.

always well behaved, which may cause diculties for standard opti-mization techniques, especially when one takes into account the needto ensure that the positive variance and stationarity constraints hold.

Simulated annealing, as a local search algorithm (metaheuristic) ca-pable of escaping local optima by allowing hill-climbing moves, faresbetter in our benchmark. As it is not gradient-based, smoothness isnot an important requirement.

One may also notice that in some cases the only arguments changingsignicantly are nx, iv and ix. This may result from the disproportion-ately high sensitivity of the objective function to those three arguments.In particular, compare the value of Qn for Estimation Starting Values

CONDITIONALLY-UNIFORM FEASIBLE GRID SEARCH ALGORITHM 35

in Table 1 to the one returned in case of the NM algorithm in Table 2 a change in one variable (λ) is enough to signicantly alter the valueof the objective function. We suspect similar behavior in case of nx, ivand ix for the FR, PR, PG, and SPG algorithms.

Below we present the summary of the estimation study results for therst seven algorithms:

(1) NM: only the value of λ has changed,(2) FR: the value of ix has improved compared to (1) (which proba-

bly led to an improvement in the objective function value), theiv has worsened, long computation time,

(3) PR: very similar to FR, other than iv is an order of magnitudefurther from the true value,

(4) BFGS: BFGS failed to produce results dierent from the start-ing values after 2.628280× 10+2 s,

(5) SA: better than all of the above,(6) PG: exhibits a problem with iv, other than that mediocre per-

formance (on par with NM, FR, PR),(7) SPG: nonmonotone line search combined with spectral choice

of step length lead to a signicant improvement compared toPG; iv does not suer problems as pronounced as in the caseof FR, PR or PG, nx is slightly better than in SA; still, theobjective function value is slightly worse than SA. A possiblereason: λ, pv, px, gv did not change at all.

Finally, we discuss the results in Table 4 for FSQP algorithm and con-sider two variants of it.

What is striking is that the objective function values have improvedsignicantly compared to those obtained by the previously discussedalgorithms.3 This suggests that FSQP might be the best choice for theestimation.

The estimate that is worth of attention is λ. Estimation of this param-eter appears dicult, possibly less so in the FSQP-AL case. However,the problem observed in all of the above algorithms, is that the es-timates quite often remain equal to their initial values. This case iscommon in the component GARCH models estimation issues werealso reported by Christoersen et al. (2008). Furthermore, it is worthnoting that in the optimization settings we have used a very large in-terval (-100, 100) for the allowed values of the λ estimate comparedto the true value. In practice, one would restrict it to an empirically

3In fact, they are slightly better than those corresponding to the DGP webelieve the reason is the nite sample of our simulation study and the eects ofconditioning on the initial values not dying o.

36 MATT P. DZIUBINSKI

reasonable (and realistic) range, depending on the beliefs and the ex-perience of the researcher. For example, limiting it to (1, 3), we obtainan estimate of 1.72 by FSQP-AL and 1 by FSQP-NL (note the cor-ner case). This seems to suggest that FSQP-AL deals better with thisproblem than FSQP-NL. We have also chosen to report the more neg-ative results so as to not create an impression of an unfair treatmentcompared to the other algorithms.

As for the other results, the ones for rf , nx, ix and gv are comparable;FSQP-AL fares slightly better than FSQP-NL for iv. Unfortunately,the estimates of pv and px are not that close to the DGP ones (FSQP-AL fares slightly better for pv). This might also be due to a smallsample N = 1, 000.

In order to nd out whether rescaling the parameters to the same mag-nitude would yield an improvement, we simulate the model with DGPparameters set to rf = 1.0e-001, λ = 5.0e-001, nx = 4.0e-001, iv =1.0e-001, ix = 2.0e-001, pv = 2.5e-001, px = 7.5e-001, gv = 1.0e+000.However, we experience similar diculties as in the original case. Fur-thermore, one may argue that ex ante the researcher cannot alwaysknow the appropriate scale without performing estimation in the rstplace.

4.4. Results with the known DGP optimization study for the

EL model. In this section we discuss the results for the Engle andLee (1999) GARCH model.

In the following, we present the summary of the estimation study re-sults for all the algorithms (here, FSQP denotes the FSQP-NL variant)using the articially generated data with known DGP: 4