essentials of treasury management essentials of

TRANSCRIPT

1

Essentials of Treasury Management Essentials of Treasury Management ––Chapter 8 Chapter 8

Payment SystemsPayment SystemsKaren A. Slaughter, CTPKaren A. Slaughter, CTP

Amegy Bank of TexasAmegy Bank of Texas

2

Tricks, Tips and Tools

• Read, Read, Read• Flashcards• Books on tape• Study groups• AFP online course• Rice Continuing Education• Your HTMA chapter• TMExam.com

35/170

3

Chapter 8 - Outline

• Overview of Payment Methods• Paper-Based Payments• Electronic Payments• Payment System Risk• Future of Payments

10 Questions on Exam

4

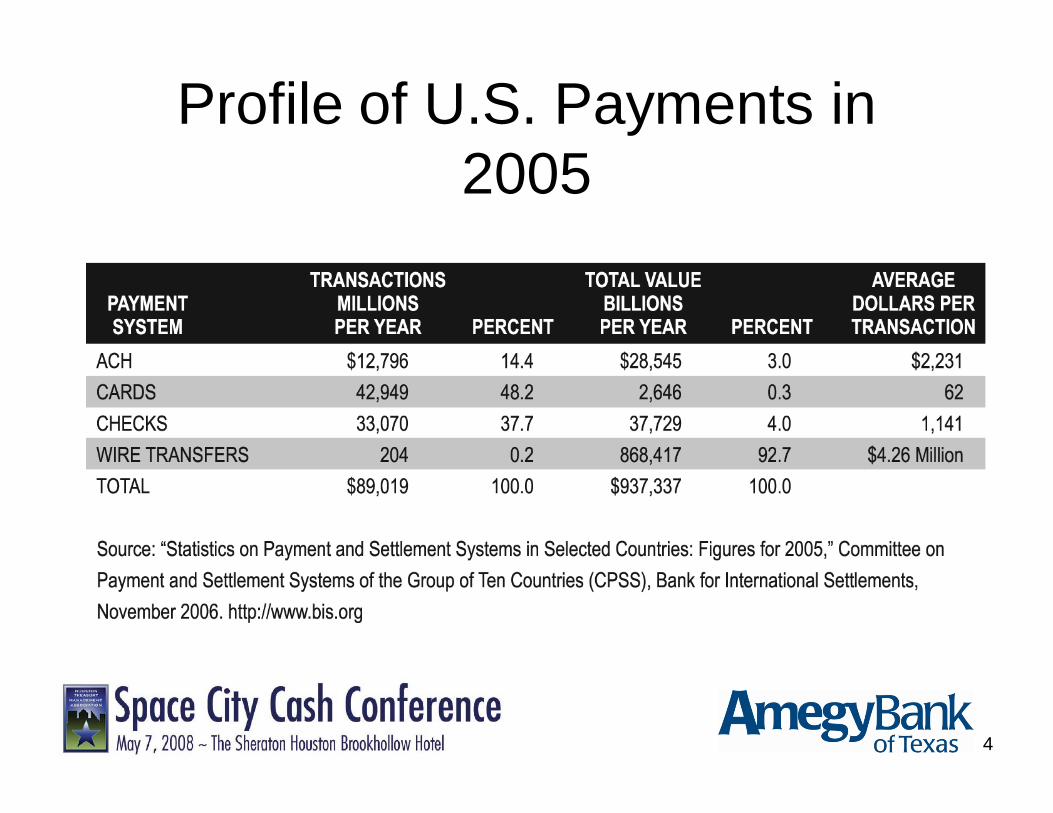

Profile of U.S. Payments in 2005

5

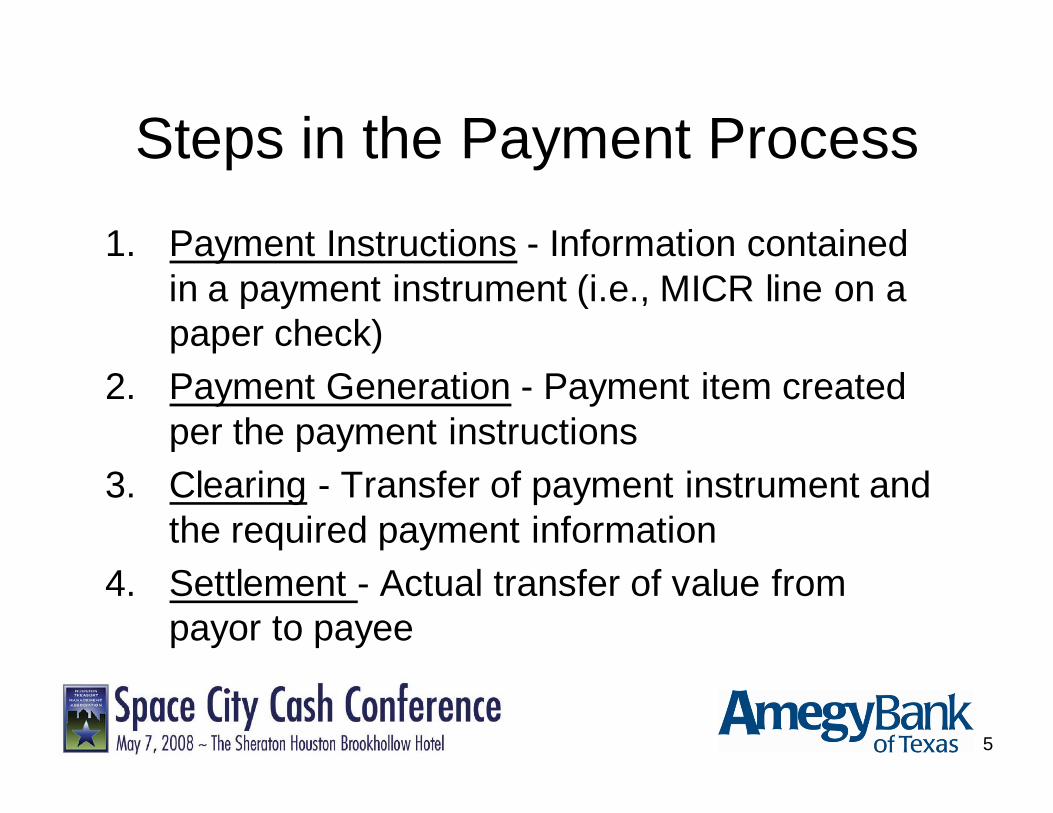

Steps in the Payment Process

1. Payment Instructions - Information contained in a payment instrument (i.e., MICR line on a paper check)

2. Payment Generation - Payment item created per the payment instructions

3. Clearing - Transfer of payment instrument and the required payment information

4. Settlement - Actual transfer of value from payor to payee

6

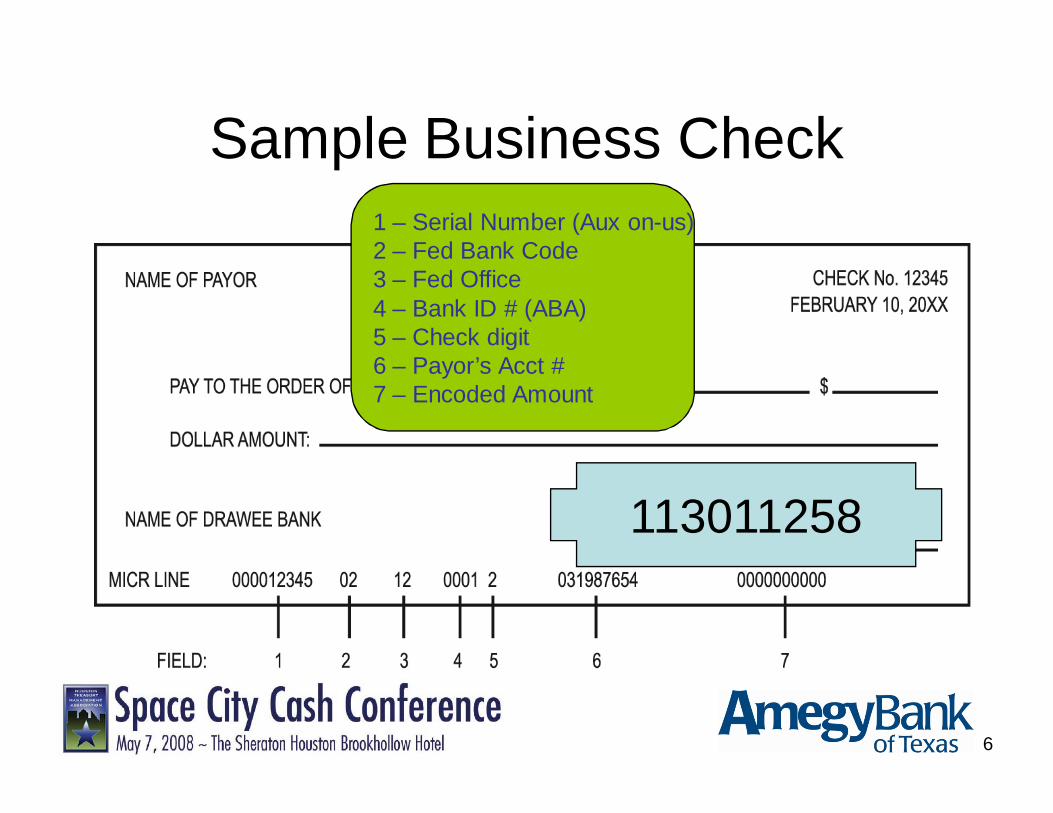

Sample Business Check1 – Serial Number (Aux on-us)2 – Fed Bank Code3 – Fed Office4 – Bank ID # (ABA)5 – Check digit6 – Payor’s Acct #7 – Encoded Amount

113011258

7

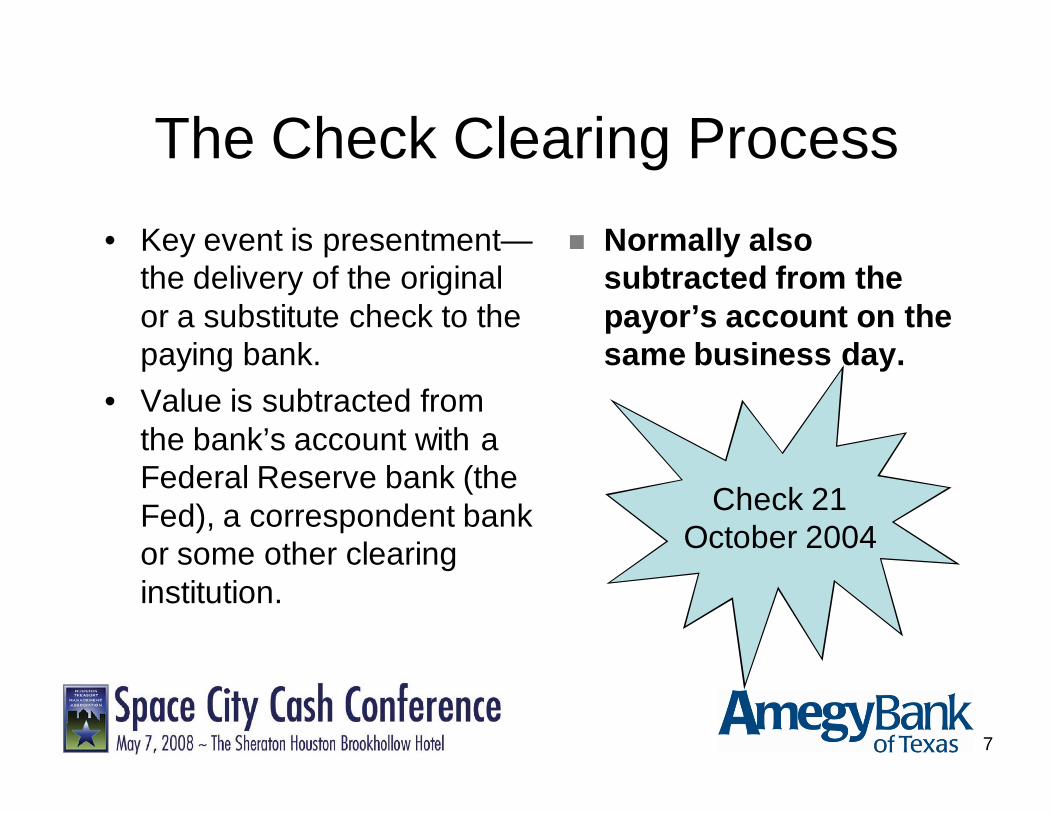

The Check Clearing Process• Key event is presentment—

the delivery of the original or a substitute check to the paying bank.

• Value is subtracted from the bank’s account with a Federal Reserve bank (the Fed), a correspondent bank or some other clearing institution.

Normally also subtracted from the payor’s account on the same business day.

Check 21October 2004

8

Federal Reserve Districts

9

Interbank Check Clearing

• Checks drawn on banks other than the bank of deposit

• Clearing channels– Clearing house

• Formal or informal– Federal Reserve Bank (Fed)– Correspondent bank– Direct send or direct exchange

10

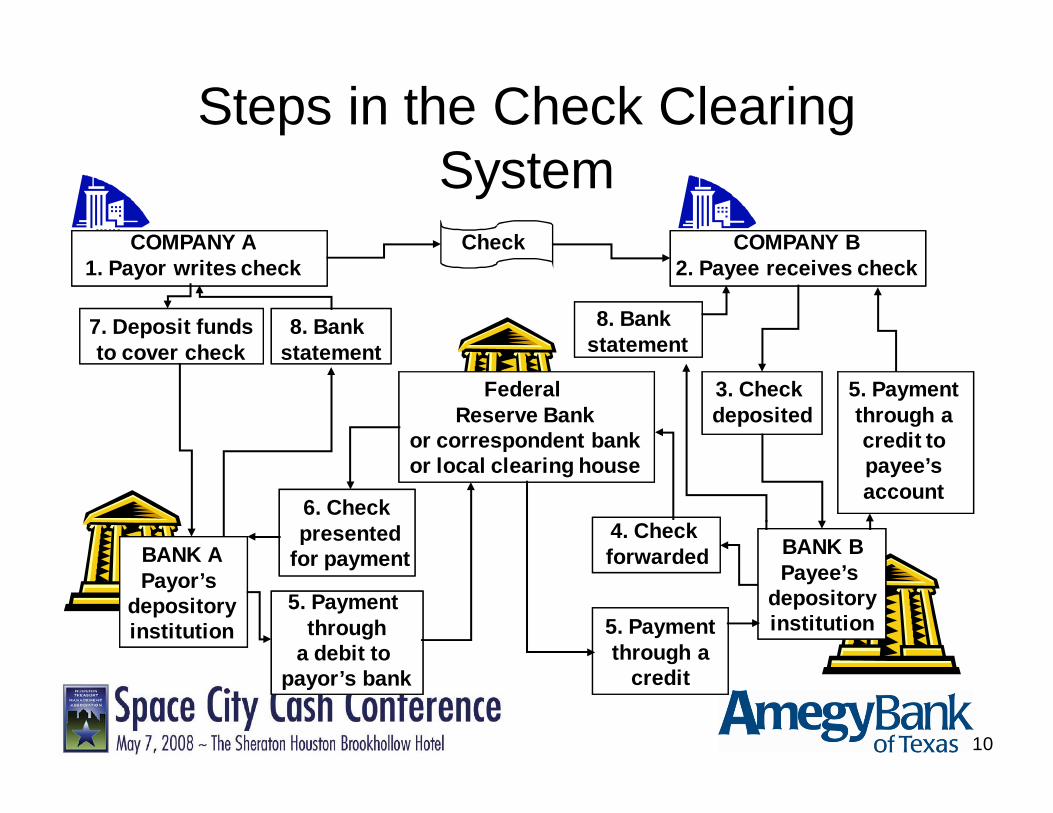

Steps in the Check Clearing System

COMPANY A1. Payor writes check

Federal Reserve Bank

or correspondent bankor local clearing house

Check COMPANY B2. Payee receives check

3. Check deposited

7. Deposit fundsto cover check

4. Check forwarded

6. Check presented

for paymentBANK APayor’s

depositoryinstitution

5. Payment through

a debit to payor’s bank

5. Paymentthrough a

credit

5. Paymentthrough acredit topayee’saccount

BANK BPayee’s

depositoryinstitution

8. Bank statement

8. Bank statement

11

Check Clearing TimelineP

rese

ntm

ent

Rev

iew

/ au

thor

ize

/ ret

urn

Red

epos

it /

Cha

rgeb

ack

Not

ify o

n ite

ms

> $2

,500

Mid

nigh

t ne

xt

busi

ness

day

4:00

pm

2nd

bank

ing

day

12

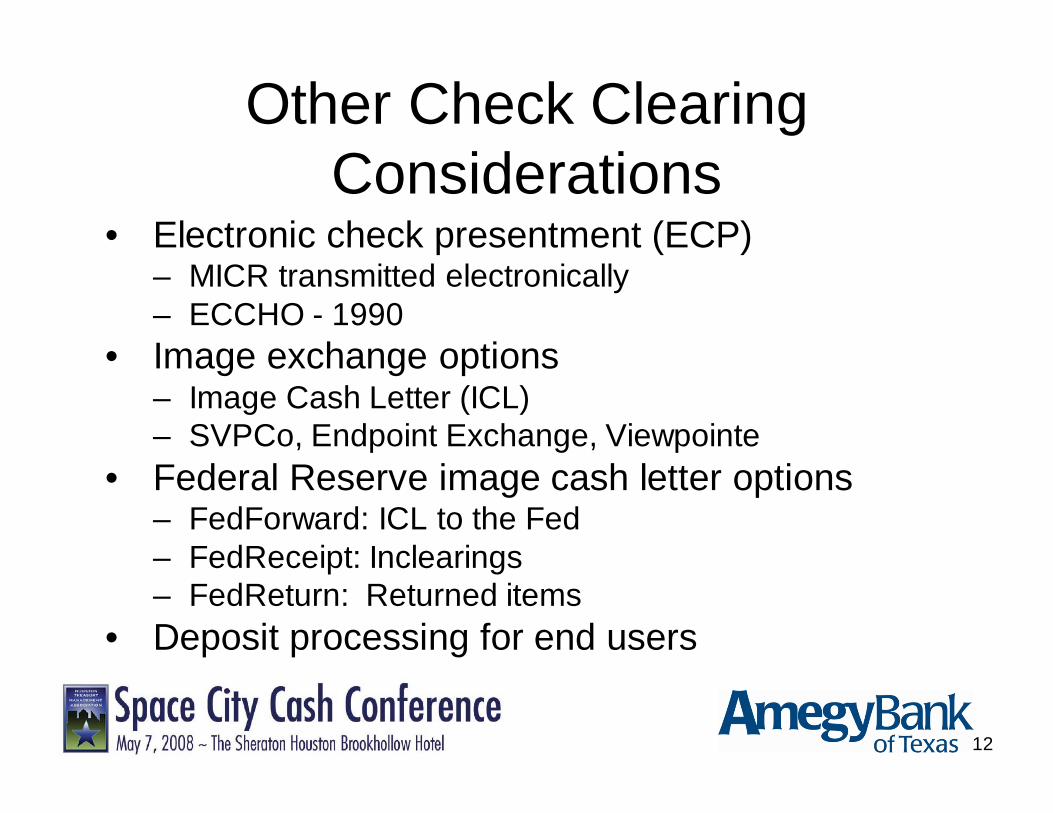

Other Check Clearing Considerations

• Electronic check presentment (ECP)– MICR transmitted electronically– ECCHO - 1990

• Image exchange options– Image Cash Letter (ICL)– SVPCo, Endpoint Exchange, Viewpointe

• Federal Reserve image cash letter options– FedForward: ICL to the Fed– FedReceipt: Inclearings– FedReturn: Returned items

• Deposit processing for end users

13

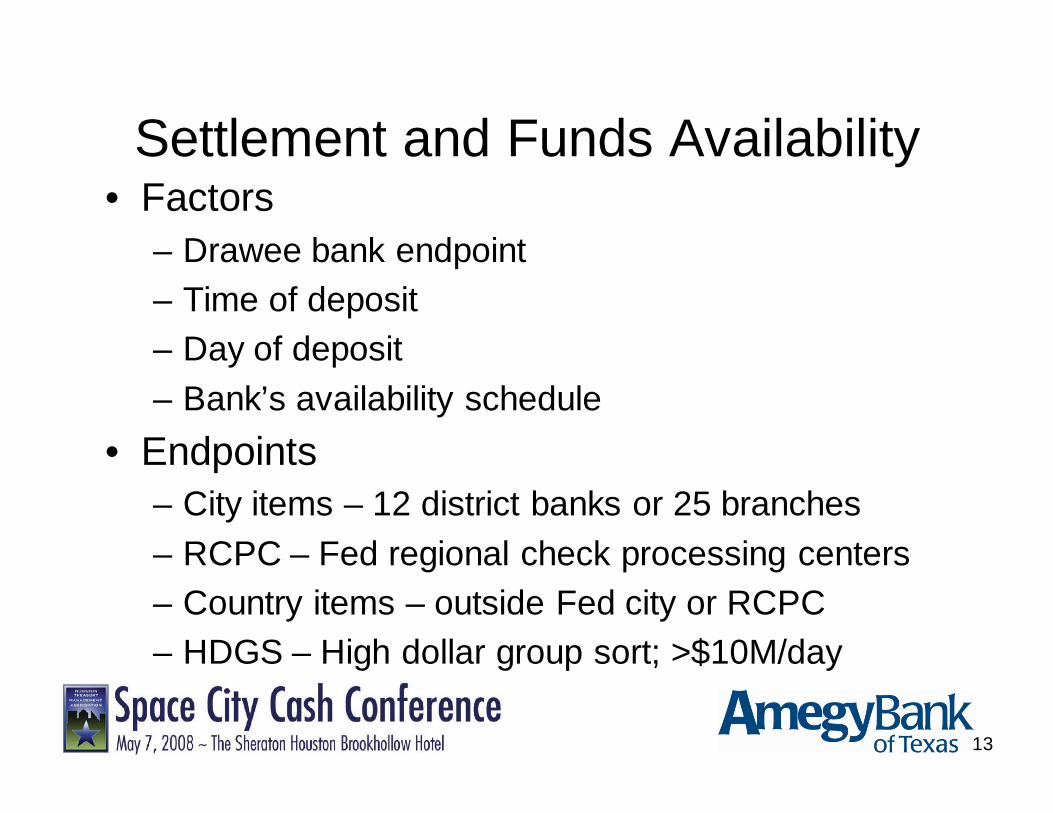

Settlement and Funds Availability• Factors

– Drawee bank endpoint– Time of deposit– Day of deposit– Bank’s availability schedule

• Endpoints– City items – 12 district banks or 25 branches– RCPC – Fed regional check processing centers– Country items – outside Fed city or RCPC– HDGS – High dollar group sort; >$10M/day

14

Settlement and Funds Availability• Deadlines and Deposit Timing

– Defines the start and end of a banking day– The time of day when a deposit must be received

to be posted to the depositor’s account– Established by individual banks

• Deposit Deadline– The time of day, based on an item’s drawee

endpoint, by which an item must be at the depository bank’s processing center ready for transit in order to qualify for the availability stated on that bank’s availability schedule

15

Settlement and Funds Availability• Availability Schedules

– Usually 0 – 2 days float– POD method– Part of pricing

• Related Funds Availability Terms – Balances and float:

• Ledger balances• Deposit float ($ and days)• Collected balances• Available balances

– Availability factors:• Pre-encoding• Reject items• As-of adjustments

16

Additional Paper Payment Instruments

• Payable through draft (PTD)• Remotely created check/ pre-authorized draft• Money order• Travelers checks• Sight and time drafts• Cashier’s check/certified check

17

Returned Items

• % of returns increasing• Check verification / check guarantee• Return reason

– NSF– Account closed, stop payment, fraud, etc.

• RCK• FedReturn

18

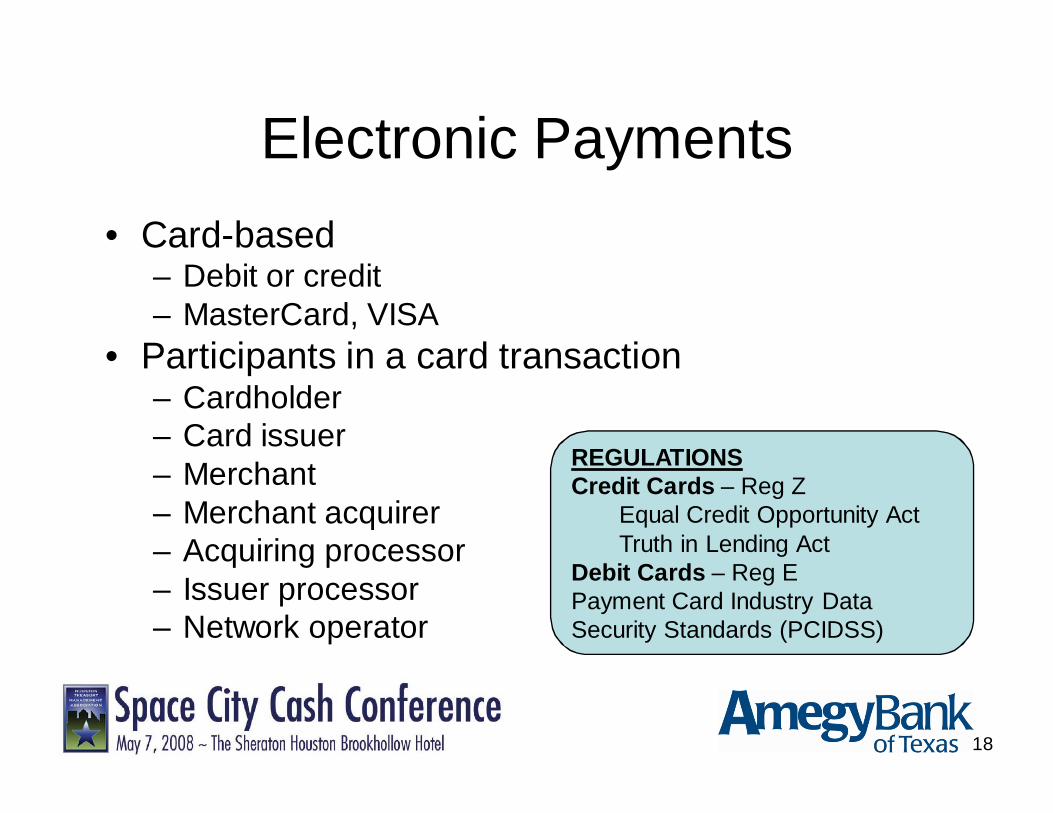

Electronic Payments• Card-based

– Debit or credit– MasterCard, VISA

• Participants in a card transaction– Cardholder– Card issuer– Merchant– Merchant acquirer– Acquiring processor – Issuer processor– Network operator

REGULATIONSCredit Cards – Reg Z

Equal Credit Opportunity ActTruth in Lending Act

Debit Cards – Reg EPayment Card Industry Data Security Standards (PCIDSS)

19

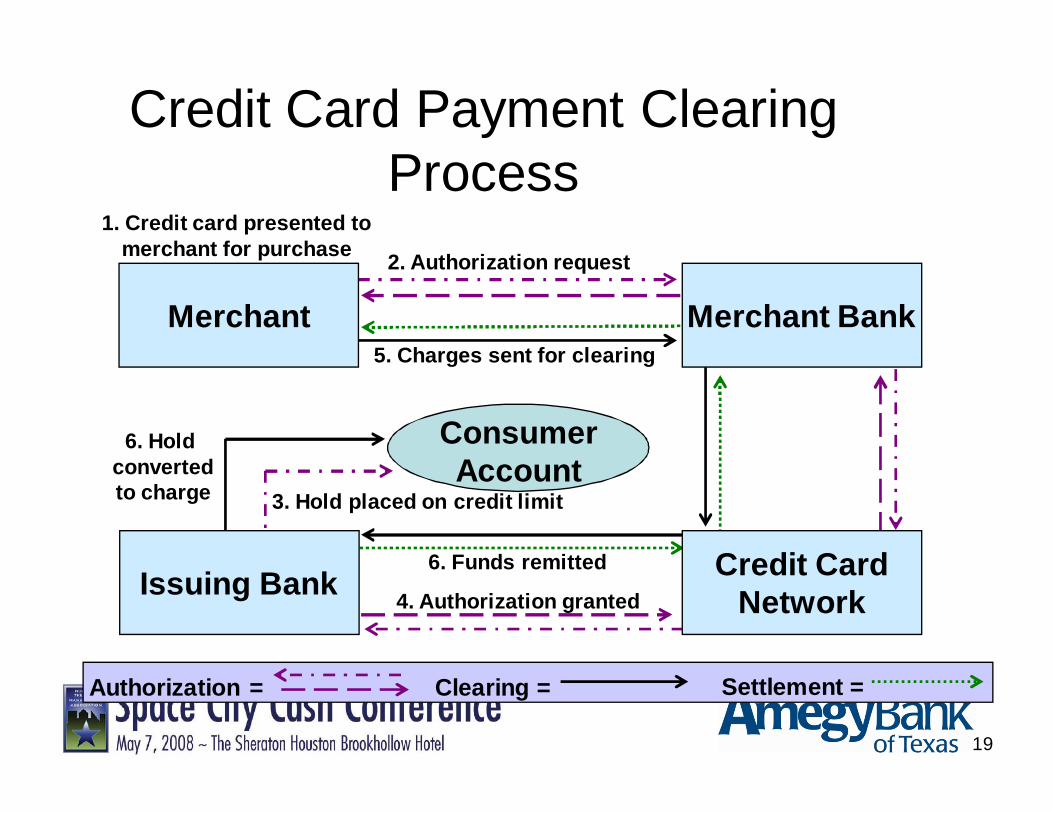

Credit Card Payment Clearing Process2. Authorization request

5. Charges sent for clearing

4. Authorization granted

Merchant Merchant Bank

Credit CardNetwork

ConsumerAccount

1. Credit card presented tomerchant for purchase

6. Hold convertedto charge

6. Funds remitted

3. Hold placed on credit limit

Authorization = Clearing = Settlement =

Issuing Bank

20

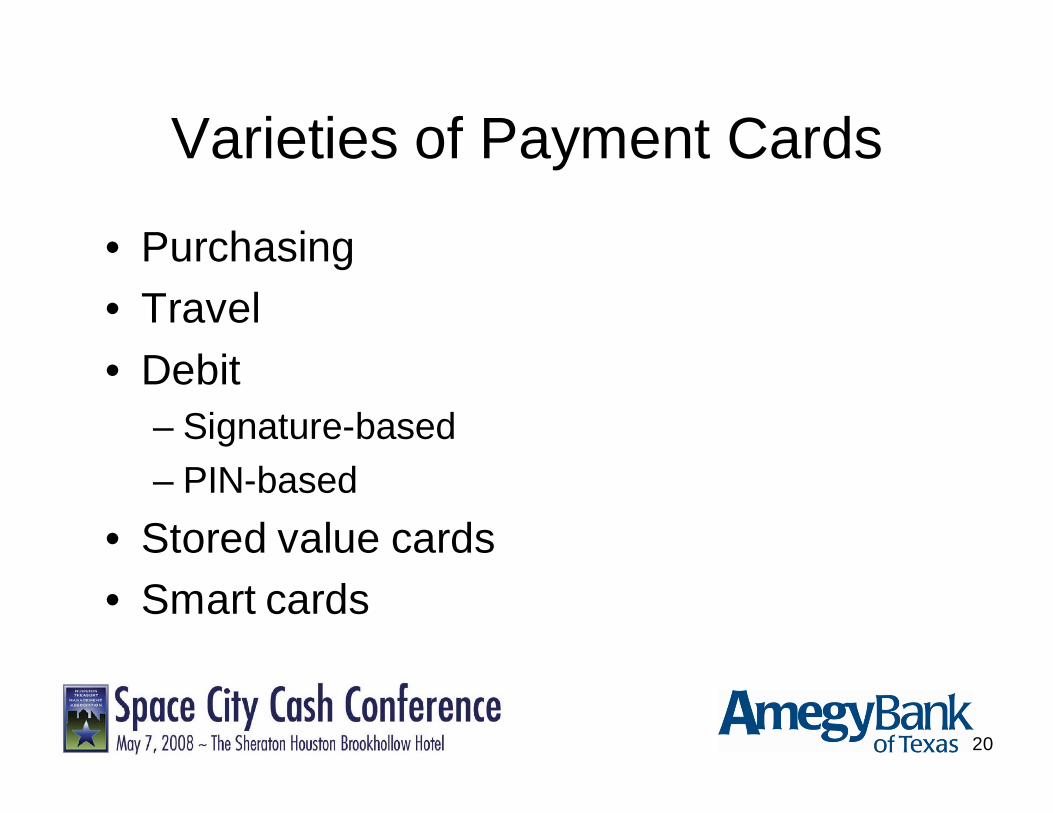

Varieties of Payment Cards

• Purchasing• Travel• Debit

– Signature-based– PIN-based

• Stored value cards• Smart cards

21

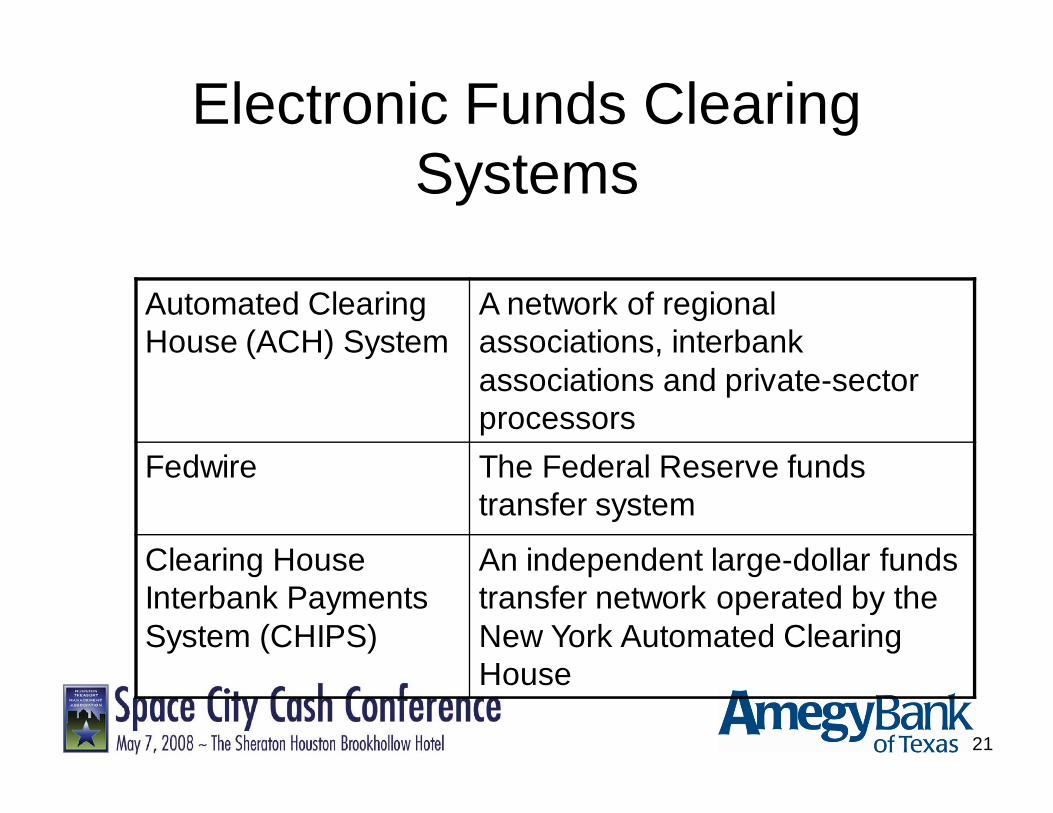

Electronic Funds Clearing Systems

Automated Clearing House (ACH) System

A network of regional associations, interbank associations and private-sector processors

Fedwire The Federal Reserve funds transfer system

Clearing House Interbank Payments System (CHIPS)

An independent large-dollar funds transfer network operated by the New York Automated Clearing House

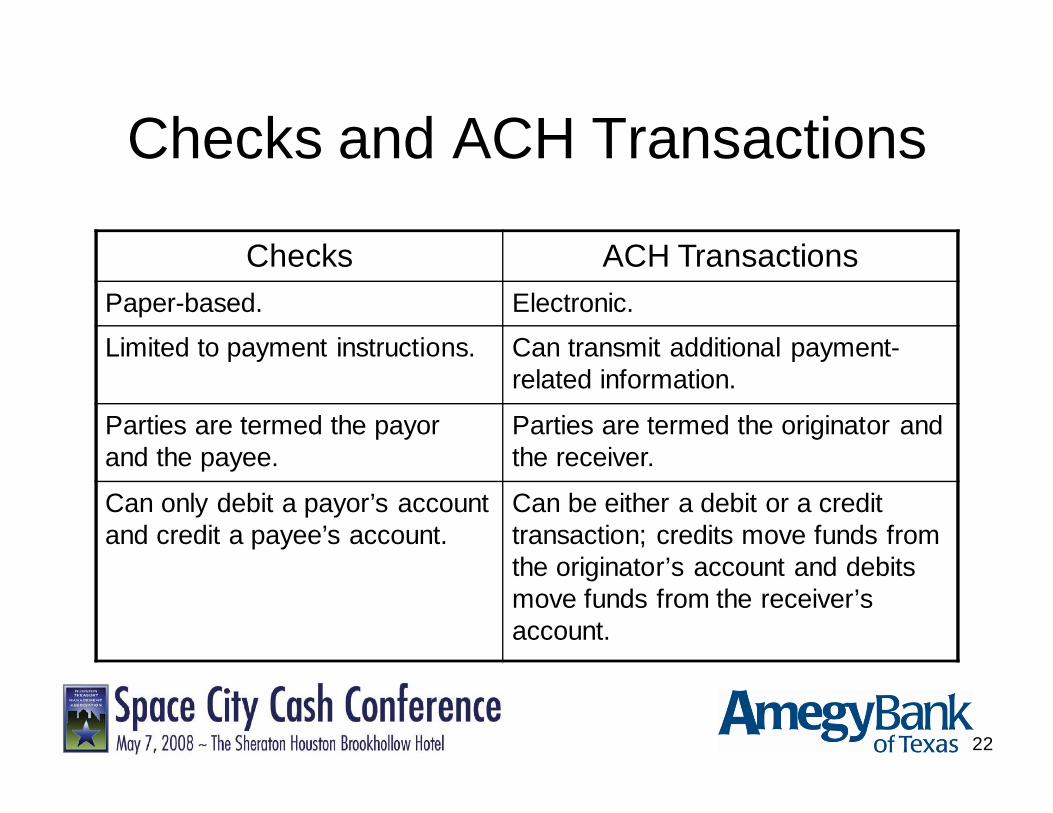

22

Checks ACH TransactionsPaper-based. Electronic.

Limited to payment instructions. Can transmit additional payment-related information.

Parties are termed the payor and the payee.

Parties are termed the originator and the receiver.

Can only debit a payor’s account and credit a payee’s account.

Can be either a debit or a credit transaction; credits move funds from the originator’s account and debits move funds from the receiver’s account.

Checks and ACH Transactions

23

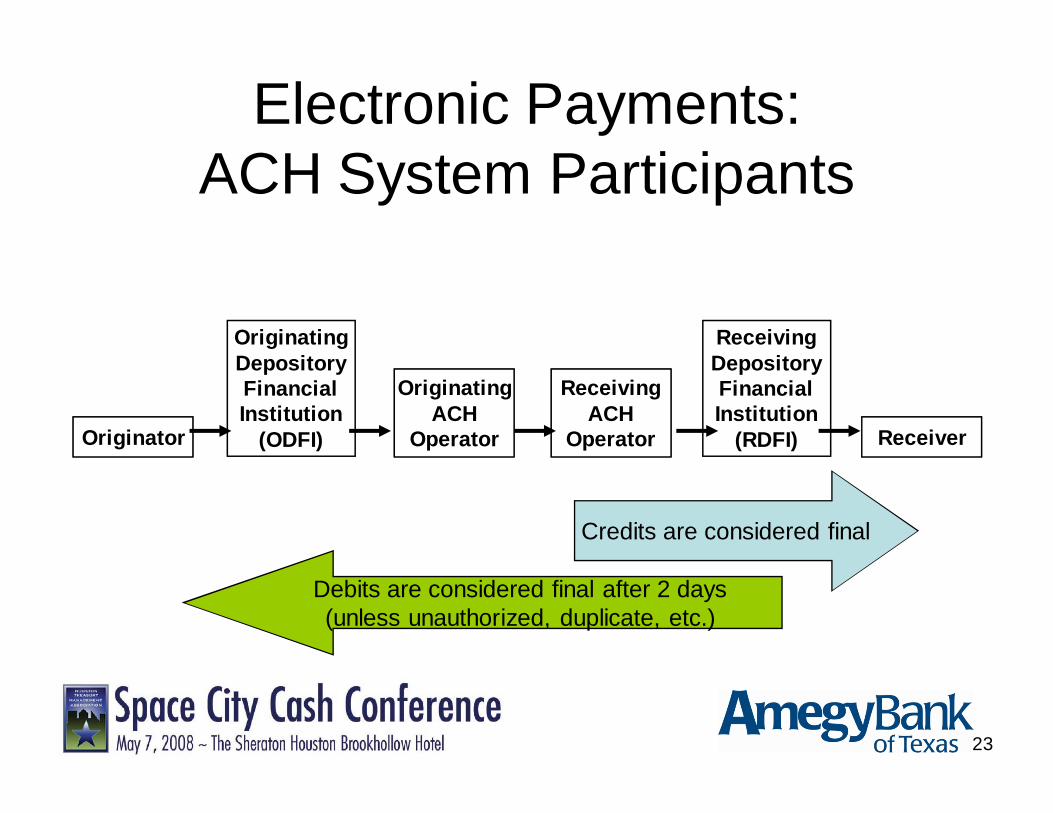

Electronic Payments: ACH System Participants

OriginatingACH

Operator

OriginatingDepositoryFinancialInstitution

(ODFI) Receiver

ReceivingDepositoryFinancialInstitution

(RDFI)

ReceivingACH

OperatorOriginator

Credits are considered final

Debits are considered final after 2 days (unless unauthorized, duplicate, etc.)

24

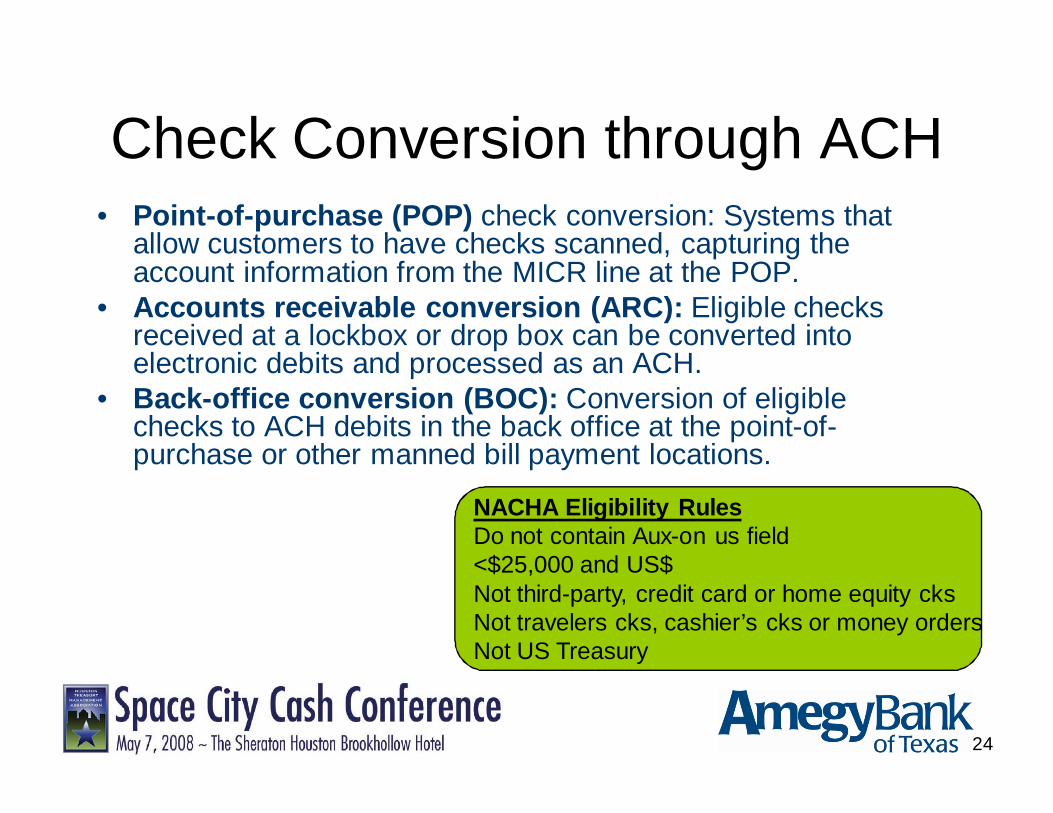

Check Conversion through ACH• Point-of-purchase (POP) check conversion: Systems that

allow customers to have checks scanned, capturing the account information from the MICR line at the POP.

• Accounts receivable conversion (ARC): Eligible checks received at a lockbox or drop box can be converted into electronic debits and processed as an ACH.

• Back-office conversion (BOC): Conversion of eligible checks to ACH debits in the back office at the point-of-purchase or other manned bill payment locations.

NACHA Eligibility RulesDo not contain Aux-on us field<$25,000 and US$Not third-party, credit card or home equity cksNot travelers cks, cashier’s cks or money ordersNot US Treasury

25

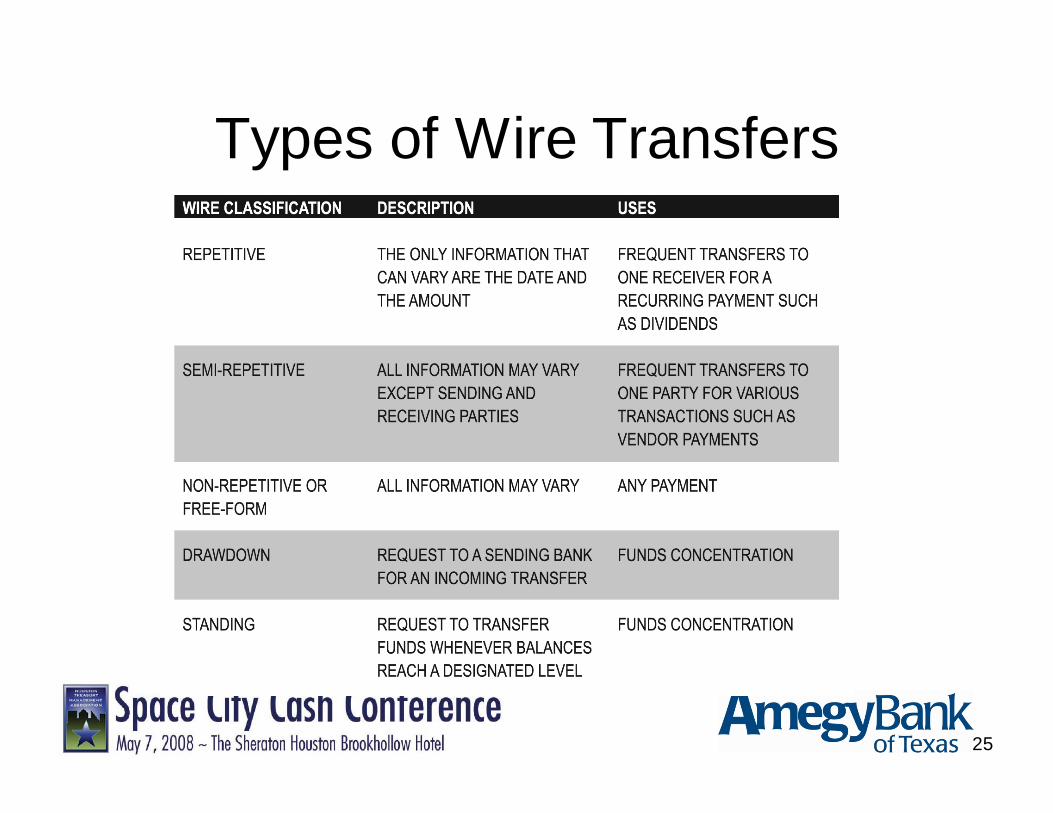

Types of Wire Transfers

26

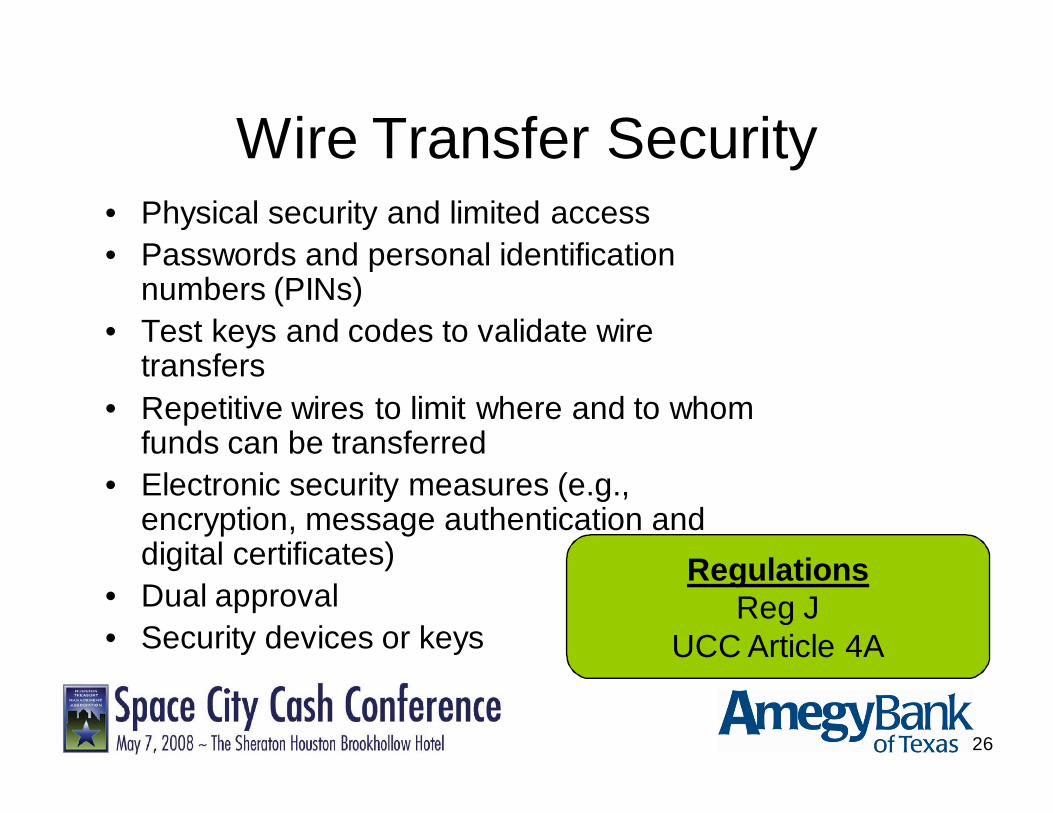

Wire Transfer Security• Physical security and limited access• Passwords and personal identification

numbers (PINs)• Test keys and codes to validate wire

transfers• Repetitive wires to limit where and to whom

funds can be transferred• Electronic security measures (e.g.,

encryption, message authentication and digital certificates)

• Dual approval • Security devices or keys

RegulationsReg J

UCC Article 4A

27

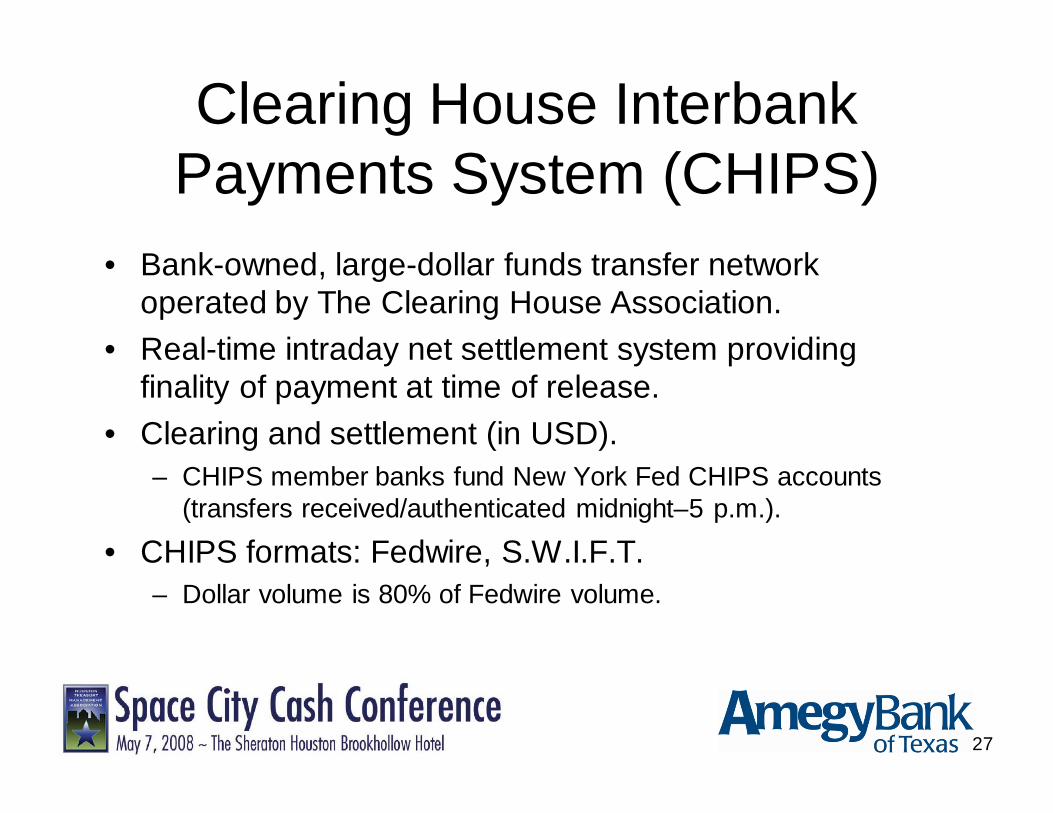

Clearing House Interbank Payments System (CHIPS)

• Bank-owned, large-dollar funds transfer network operated by The Clearing House Association.

• Real-time intraday net settlement system providing finality of payment at time of release.

• Clearing and settlement (in USD).– CHIPS member banks fund New York Fed CHIPS accounts

(transfers received/authenticated midnight–5 p.m.).

• CHIPS formats: Fedwire, S.W.I.F.T.– Dollar volume is 80% of Fedwire volume.

28

Society for Worldwide Interbank Financial Telecommunication

(S.W.I.F.T.)

• Not a funds transfer network; transmits information about financial transactions.

• Settlement occurs through Fedwire, CHIPS, correspondent accounts or other RTGS systems.

www.swift.com

29

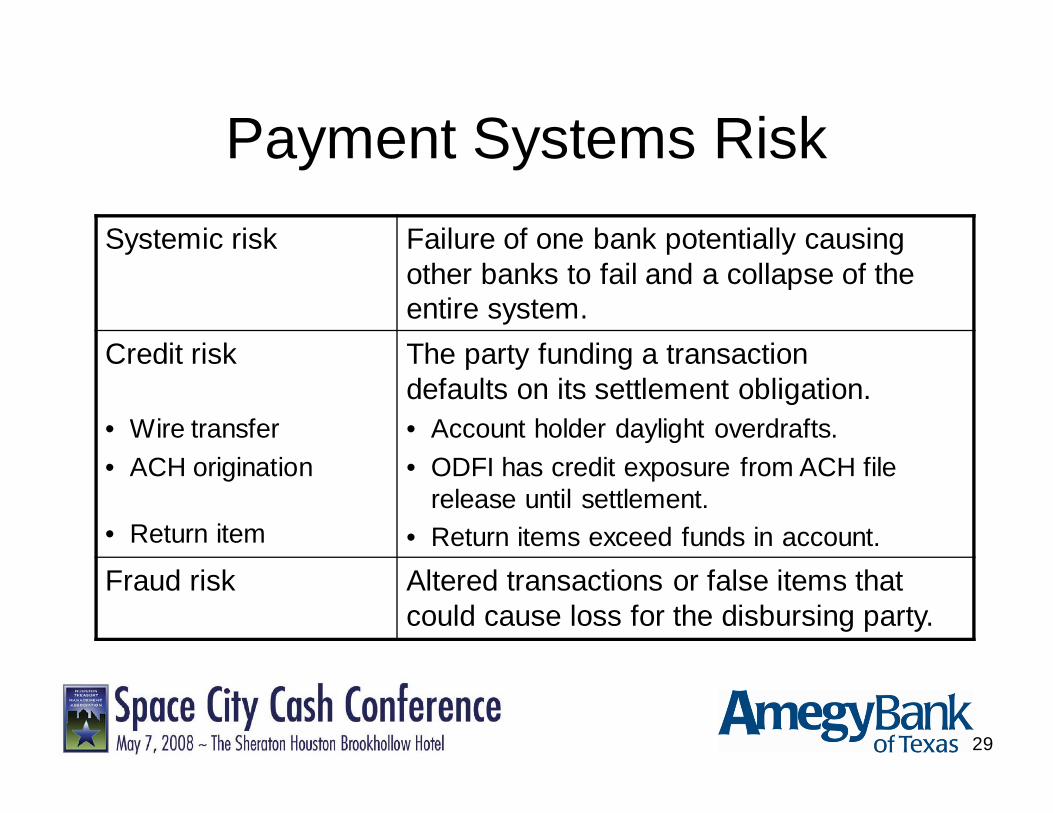

Payment Systems RiskSystemic risk Failure of one bank potentially causing

other banks to fail and a collapse of the entire system.

Credit risk

• Wire transfer• ACH origination

• Return item

The party funding a transactiondefaults on its settlement obligation.• Account holder daylight overdrafts.• ODFI has credit exposure from ACH file

release until settlement.• Return items exceed funds in account.

Fraud risk Altered transactions or false items that could cause loss for the disbursing party.