establishing foreign branches abroad by indian company

TRANSCRIPT

SETTING UP OF

BRANCH OFFICE

ABROADContributed byCS Sowrabh S Rao

CS Vineeth T

CS Nikita Agarwal

INTRODUCTION

Branch office:-

Section 2(14) of Companies Act, 2013 – anyestablishment decsribe as such by the company

Who can establish a branch abroad?

A person resident in India can establish a branch orliaison office outside India or he can establish a JV orWOS with a person resident outside India.

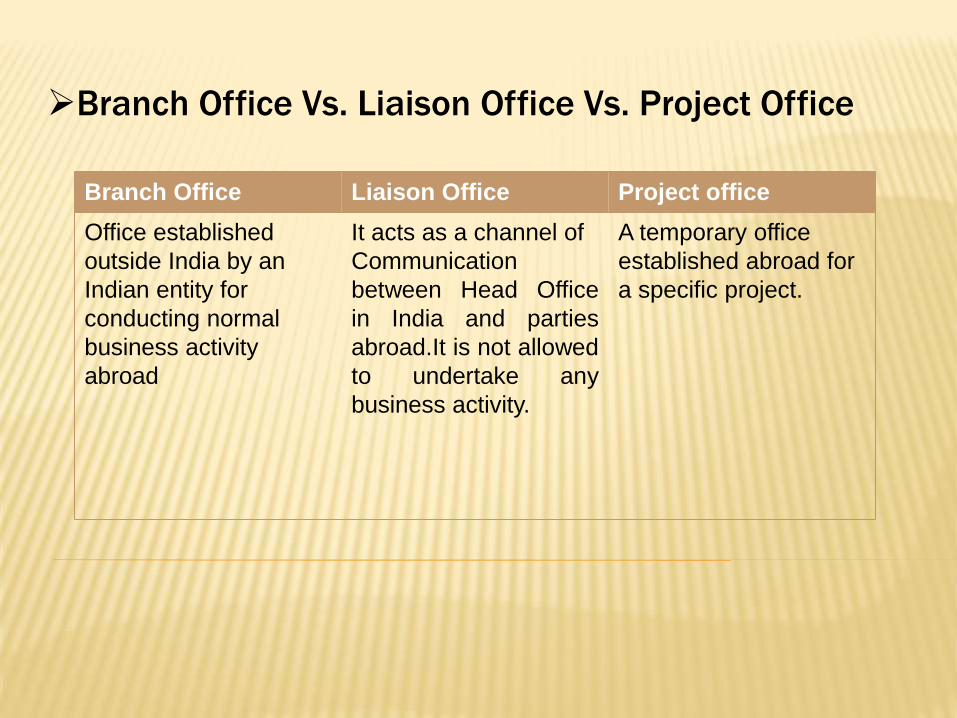

Branch Office Vs. Liaison Office Vs. Project Office

Branch Office Liaison Office Project office

Office established

outside India by an

Indian entity for

conducting normal

business activity

abroad

It acts as a channel of

Communication

between Head Office

in India and parties

abroad.It is not allowed

to undertake any

business activity.

A temporary office

established abroad for

a specific project.

Benefits of setting up of branch abroad

• Spreading up of Business

• Increasing Customer Base

• Easy accessibility of product

• Geographical Benefits

HOW TO ESTABLISH A BRANCH OFFICE ABROAD?

Residential Status:- Overseas Branch office

will be considered as resident of India

STEPS INVOLVED

• Approval of Board for establishment of

Branch

• Appointment of Authorised Representative

• Opening of Bank Account

• Filing of forms and applications, along with

supporting documents to RBI through AD

• Compliance with country specific

requirements

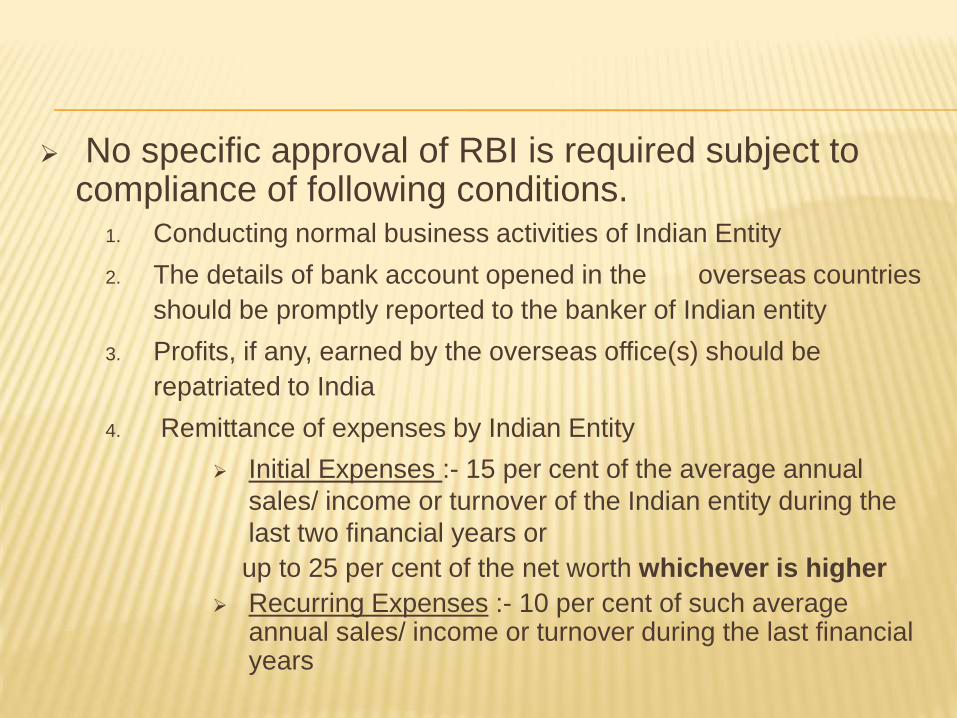

No specific approval of RBI is required subject to compliance of following conditions.

1. Conducting normal business activities of Indian Entity

2. The details of bank account opened in the overseas countries

should be promptly reported to the banker of Indian entity

3. Profits, if any, earned by the overseas office(s) should be

repatriated to India

4. Remittance of expenses by Indian Entity

Initial Expenses :- 15 per cent of the average annual

sales/ income or turnover of the Indian entity during the

last two financial years or

up to 25 per cent of the net worth whichever is higher

Recurring Expenses :- 10 per cent of such average annual sales/ income or turnover during the last financial years

Exemption for restriction on remittance of

expenses

• If remittances are made out of funds held in

EEFC account of Indian Entity

• Within 2 years of establishment of branch in

100% EOU or EPZ or STP/HTP

3. The details of bank account opened in the

overseas countries should be promptly

reported to the banker of Indian firm / company

4. Profits, if any, earned by the overseas

office(s) should be repatriated to India

Failure to satisfy the above condition

requires RBI approval through AD

Acquisition of Property for branch office

•Purchase of Office equipments and other assets for the normal business operations of the overseas branch office shall not be treated capital account transactions and hence No RBI permission.

•Acquisition of immovable property outside India by way of lease, not exceeding a period of five years by the overseas branch or office is permitted without obtaining the RBI’s permission.

Prohibition on activities of Branch Office:

• Shall not enter into contract or agreement in contravention of the Act or rules or regulations applicable to it.

• Shall not create any financial or contingent liabilities for head office in India.

• Shall not invest surplus fund abroad without prior approval of RBI but such surplus fund should be repatriated to India.

Documents to be submitted

• Form A2

• TT Application

• Form OBR- Along with the following documents

• Correspondence, if any, in original together with photocopies regarding the arrangement made in foreign Countries.

• Bank certificate together with copies for immediately preceding four calendar half years in support of export realization.

•Particulars of the turnover duly certified by the Statutory Auditors.

back

COUNTRY SPECIFIC REQUIREMENTS

1. New Zealand

- Reservation of name by the branch

- File application for registration within

10 working days along with the

required documents

- Post registration requirements

2. Portugal

- Appostalised Documents to Commercial

Registry

- Post Registration

- Balance sheet and Profit and loss

account of Company and Branch

Separately

- IT return in form “Modelo 22” within 5th

month of end of FY

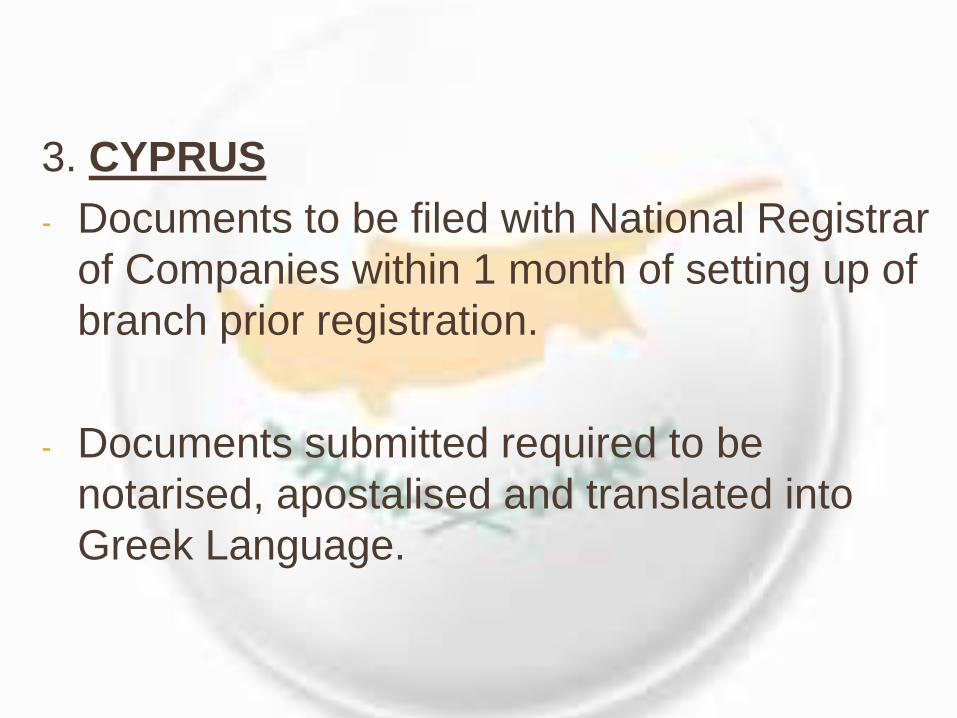

3. CYPRUS

- Documents to be filed with National Registrar

of Companies within 1 month of setting up of

branch prior registration.

- Documents submitted required to be

notarised, apostalised and translated into

Greek Language.

Thank You***