estate survey report - american bankers association€¦ · · 2016-04-221st annual aba...

TRANSCRIPT

1st Annual ABA Commercial Real Estate Survey Report

April 2016

aba.com 1-800-BANKERS

aba.com 1-800-BANKERS

Staff Contributors:

Bob Davis, Executive Vice President, American Bankers AssociationRod Alba, SVP, Sr. Regulatory Counsel, American Bankers AssociationAshley Gunn, Senior Banking Analyst, American Bankers Association

Data Processing and Analysis provided by:

Michael Mazur, Senior Manager, American Bankers Association

The American Bankers Association extends its appreciation to the bankers who contributed essential information to the 1st edition of the Commercial Real Estate Lending Survey. Their participation in this extensive study, despite already heavy reporting burdens, ensured the success of this research project.

2

Acknowledgements

aba.com 1-800-BANKERS

The 1ST Real Estate Lending Survey had the participation of 136 banks. The data was collected from February 4, 2016 to March 21, 2016, and in most cases reports calendar year or year-end results. In other cases, data reflect current activities and expectations at the time of data collection. Of the survey participants, 77 percent of respondents were commercial banks and 23 percent were savings institutions. About 61 percent of the participating institutions had assets of less than $1 billion. This survey serves as an important resource for members as it provides an unbiased yearly snapshot of industry activity and bankers’ responses to market, regulatory, and other developments. This year’s survey is notable in reflecting the increased impact of new regulations on the commercial real estate industry.

• Banks continue to be active in CRE lending as evidenced by construction and CRE concentration levels; 19% of respondents have over 100% construction concentration and 9% have over 300% CRE concentration

• 82 percent of banks anticipate increasing their capital concentrations claiming strategic planning as the main driver for the increase

• Market characteristics remained constant as approximately 50% reported that demand, liquidity, cap rates and underwriting standards are all in line with levels seen in 2014; demand and liquidity showed the greatest variance

• Multifamily, office and retail represent the most active lending classes, making up approximately 62% of a banks’ CRE lending portfolio on an average basis

• Exactly half the banks surveyed currently have outstanding loans classified as HVCRE, and approximately one-third of respondents increased pricing, after the rule went into effect, to reflect the additional capital cost from the HVCRE classification

• About 65% of banks expect some type of measurable reduction in credit availability as a result of the recently released “Statement on Prudent Risk Management for CRE Lending”

3

A Summary of Key Findings

aba.com 1-800-BANKERS

4% 1%

12%

10%

13%

21%

31%

4% 4% Up to $50 million

$51-$100 million

$101-$200 million

$201-300 million

$301-$500 million

$501 million-$1 billion

$1 billion-$10 billion

$10 billion-$20 billion

Over $20 billion

77%

23%

Savings Bank/Institution

Commercial Bank

85%

15%

Stock

Mutual/MHC

Participant Profile Breakdown

4

49%

32%

19%

OCC

FDIC

Federal Reserve

Bank Asset Size Bank Ownership Type

Bank Charter Type Primary Federal Regulator

aba.com 1-800-BANKERS

Bank’s Headquarters

8%

4%

4%

8%

7%

22%

3%

9%

23%

12%

Northwest (Alaska, Oregon, Washington)

Southwest (Arizona, California, Hawaii, New Mexico,Nevada)

Mountain (Colorado, Idaho, Montana, Utah, Wyoming)

Plains (Iowa, Kansas, Missouri, North Dakota,Nebraska, South Dakota)

South (Arkansas, Louisiana, Oklahoma, Texas)

Great Lakes (Illinois, Indiana, Michigan, Minnesota,Ohio, Wisconsin)

Lower Southeast (Alabama, Florida, Georgia,Mississippi, Puerto Rico)

Middle Southeast (Kentucky, North Carolina, SouthCarolina, Tennessee, West Virginia)

Mid-Atlantic (D.C., Delaware, Maryland, New Jersey,New York, Pennsylvania, Virginia)

New England (Connecticut, Massachusetts, Maine,New Hampshire, Rhode Island, Vermont)

5

aba.com 1-800-BANKERS

CRE Capital Concentrations

4%

35%

23%

19%

19%

0%

1 to 25%

26 to 50%

51 to 99%

100% and over

2%

34%

29%

26%

9%

0%

1 to 99%

100 to 199%

200 to 299%

300% and over

Construction, Land, Development, and Other Land

Multifamily, Nonfarm Residential Properties and Construction

6

aba.com 1-800-BANKERS

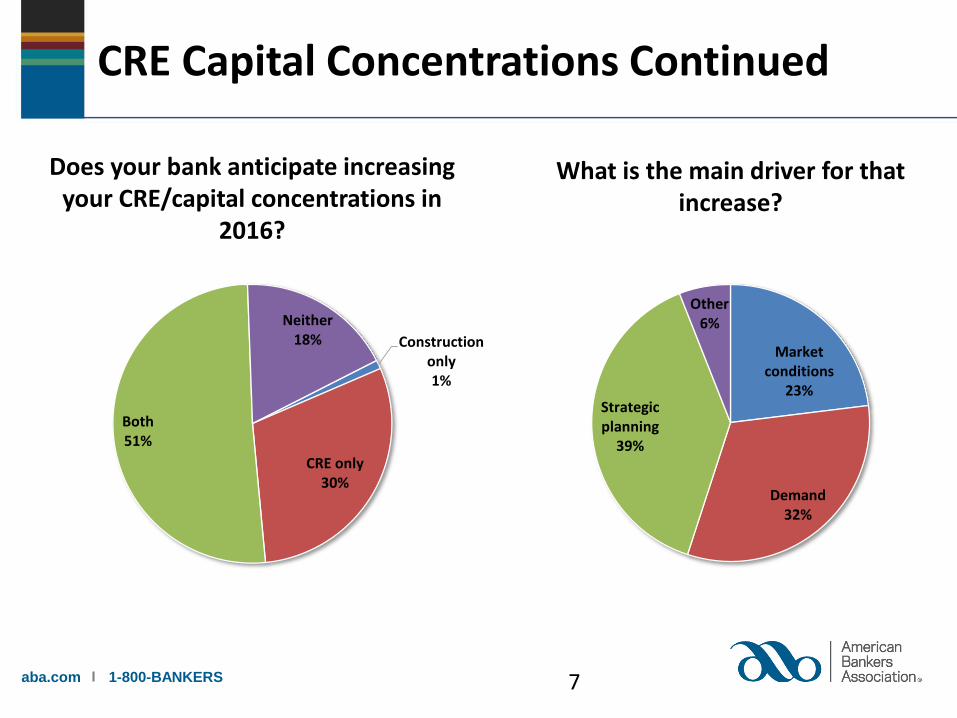

Does your bank anticipate increasing your CRE/capital concentrations in

2016?

Construction only1%

CRE only30%

Both51%

Neither18%

Market conditions

23%

Demand32%

Strategic planning

39%

Other6%

What is the main driver for that increase?

CRE Capital Concentrations Continued

7

aba.com 1-800-BANKERS

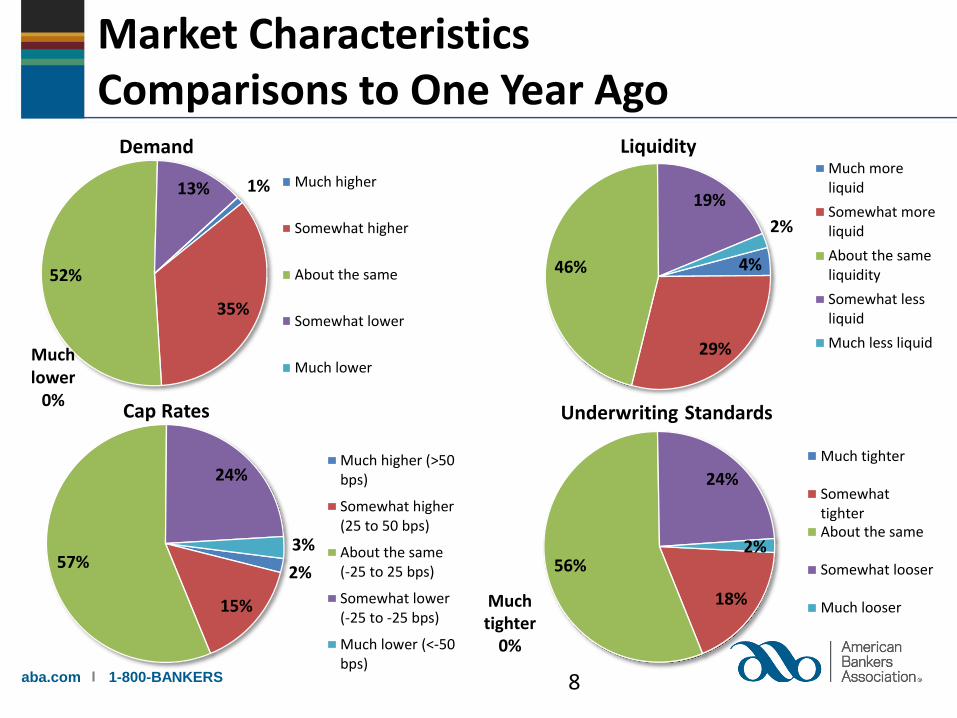

1%

35%

52%

13%

Much lower

0%

Much higher

Somewhat higher

About the same

Somewhat lower

Much lower

4%

29%

46%

19%

2%

Much moreliquid

Somewhat moreliquid

About the sameliquidity

Somewhat lessliquid

Much less liquid

2%

15%

57%

24%

3%

Much higher (>50bps)

Somewhat higher(25 to 50 bps)

About the same(-25 to 25 bps)

Somewhat lower(-25 to -25 bps)

Much lower (<-50bps)

18%

56%

24%

2%

Much tighter

SomewhattighterAbout the same

Somewhat looser

Much looser

Market CharacteristicsComparisons to One Year Ago

Demand

Cap Rates

Liquidity

Underwriting Standards

Much tighter

0%

8

aba.com 1-800-BANKERS

Biggest Challenges in CRE Lending

64

21

121

55

34

26

29

3

Regulatory burden and requirements

Lack of borrower demand

Competition from bank lenders

Competition from non-bank lenders

Fewer credit-worthy projects

Lack of qualified borrowers

Appraisal challenges

Other

Mark all that Apply

21

6

80

6

8

5

4

2

Single-Most Important Challenge

9

aba.com 1-800-BANKERS

CMBS market0%

Government agency0%

Insurance company

1%

Large banks13%

Regional banks49%

Community banks34%

Nonbank lenders1%

Credit unions1%

Other 0%

Biggest Competitor

10

aba.com 1-800-BANKERS

Average Breakdown of CRE Portfolio by Sector

Multifamily28%

Office18%

Industrial12%

Hospitality8%

Retail16%

Healthcare7%

Other 12%

Includes: • Storage• Land• Religious• Mixed Use • Residential

Construction

11

aba.com 1-800-BANKERS

Loan-to-Value Ratios for Originated CRE Loans

4%

6%

12%

25%

45%

8%1%

Loan-to-value ratio 40% or less

Loan-to-value between 40% and 50%

Loan-to-value between 50% and 60%

Loan-to-value between 60% and 70%

Loan-to-value between 70% and 80%

Loan-to-value between 80% and 90%

Loan-to-value greater than 90%

12

aba.com 1-800-BANKERS

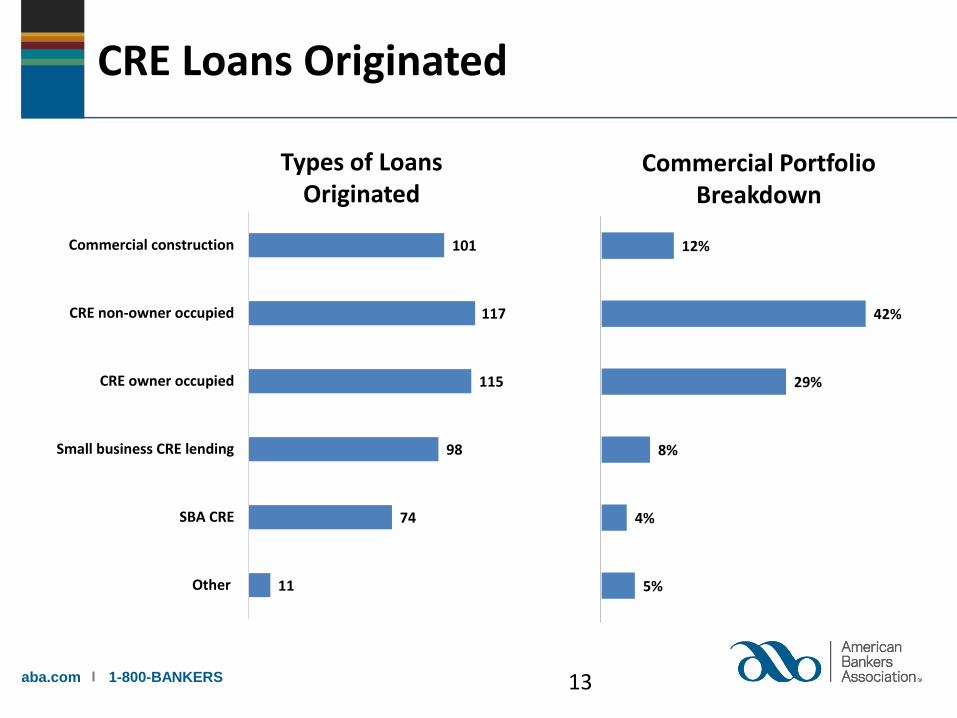

CRE Loans Originated

101

117

115

98

74

11

Commercial construction

CRE non-owner occupied

CRE owner occupied

Small business CRE lending

SBA CRE

Other

12%

42%

29%

8%

4%

5%

Types of Loans Originated

Commercial Portfolio Breakdown

13

aba.com 1-800-BANKERS

28%

16%37%

11%

9%

5 years

7 years

10 years

15 years

Other

2%

21%60%

17%

15 years

20 years

25 years

Other

Much higher

0%

21%

45%34%

Much lower

0%

Much higher

Somewhathigher

Unchanged

Somewhatlower

Much lower

46%

33%

6%

15%

15%

20%

25%

Other

Amortization Periods

Target Return on Equity Interest Rates as Compared to One Year Ago

Maximum Maturity

Underwriting Covenants

14

aba.com 1-800-BANKERS

Interest-Only Loans

Yes60%

No40%

Most banks reported interest-only loans make up 5 to 25 percent of the 2015 portfolio, with some reporting as high as 44, and even, 80 percent.

Does your bank originate interest-only loans?

15

aba.com 1-800-BANKERS

Selling Loans and Participations to Other Financial Institutions

Yes73%

No27%

Yes46%

No54%

Did Your Bank Sell Loan Participations?

Did Your Bank Sell CRE Loans?

16

aba.com 1-800-BANKERS

49

27

24

2

1

2

Banks of similar size

Smaller banks

Larger banks

Nonbanks

Credit unions

Other

Loans and Participations Sold to Other Financial Institutions

17

aba.com 1-800-BANKERS

High-Volatility Commercial Real Estate (HVCRE)

Yes50%

No50%

Most banks reported outstanding HVCRE classified loans make up less than 10% of the 2015 portfolio. However, a couple banks reported up to 33% of

their portfolio as HVCRE.

Does you bank currently have loans outstanding that are classified as HVCRE?

18

aba.com 1-800-BANKERS

Yes55%

No45%

HVCRE Continued

Yes71%

No29%

If HVCRE outstanding, were any loans originated after January 1, 2015 (when the rule went into

effect)?

Yes37%

No63%

If HVCRE outstanding, did your bank increase pricing to reflect

the additional capital cost of the HVCRE classification?

Has your bank quoted any CRE loan terms that were structured

to avoid the classification but were then lost to a competitor

who didn’t have the same requirements or were declined

by the borrower?

Most reported that proper rule interpretation and remaining competitive given the additional cost are the biggest challenges associated with the HVCRE classification.

19

aba.com 1-800-BANKERS

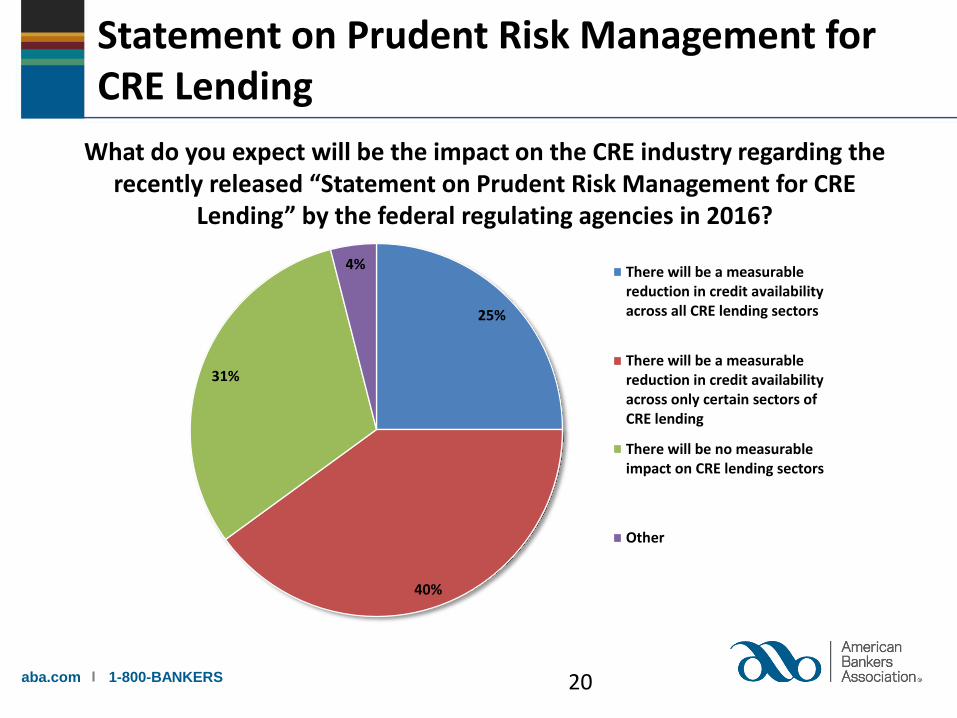

Statement on Prudent Risk Management for CRE Lending

25%

40%

31%

4% There will be a measurablereduction in credit availabilityacross all CRE lending sectors

There will be a measurablereduction in credit availabilityacross only certain sectors ofCRE lending

There will be no measurableimpact on CRE lending sectors

Other

What do you expect will be the impact on the CRE industry regarding the recently released “Statement on Prudent Risk Management for CRE

Lending” by the federal regulating agencies in 2016?

20

aba.com 1-800-BANKERS

Primary Concerns Regarding the Commercial Real Estate Market

Regulatory Burden

Low Cap Rates

Increasing Interest Rates

Competition

Economic Environment & Market Conditions

CRE Outlook for 2016

21