ethanol in brasil: a model to follow or to avoid? (latin america … · 2015-12-16 · weather...

TRANSCRIPT

Ethanol in Brasil: a model to follow or to avoid? (Latin America mini-series 3 of 4)Dario Gaeta

Understand the Ethanol economic

environment in Brazil: past, present and

future

Know how a Sugarcane mill works

Evaluate the recent milestones of the Ethanol

Program

Keep asking…

Objectives

Milestones of the Ethanol in Brazil

Basics about Sugarcane Ethanol

Comparison between Ethanol and Gasoline

Feasibility of the Ethanol as biofuel

Future of the Bio feedstock – end of Oil era?

Futurology

Q&A

AGENDA

Early 70’s ‐ launched the Ethanol Program by Military Government

Late 70’s –Ethanol car developed, production grew 6 fold

80’s ‐ second oil crisis, ethanol supply crisis

Late 90’s – blend increased to 22%

2003 – FFC launched

2005‐2007 – ethanol booming

2008 – 2014 – ethanol blowing

2016 – ethanol Phoenix program

Milestones for Sugarcane Ethanol in Brazil

Source: UNICA

SUGARCANE MILL and BASICSUNICA PRESENTATION

http://english.unica.com.br/virtual‐mill/video‐new/virtual‐mill.htm

• 5MM t of sugarcane p.y.

• 3.000 employees

• 24/7 – 260 days

• > 800 vehicles

• 40 MM USD maintenance cost every year

• 10.000 ha replant every year

• 300 MM l Ethanol

• 250 Th t Sugar

KEY NUMBERS – Sugarcane mill

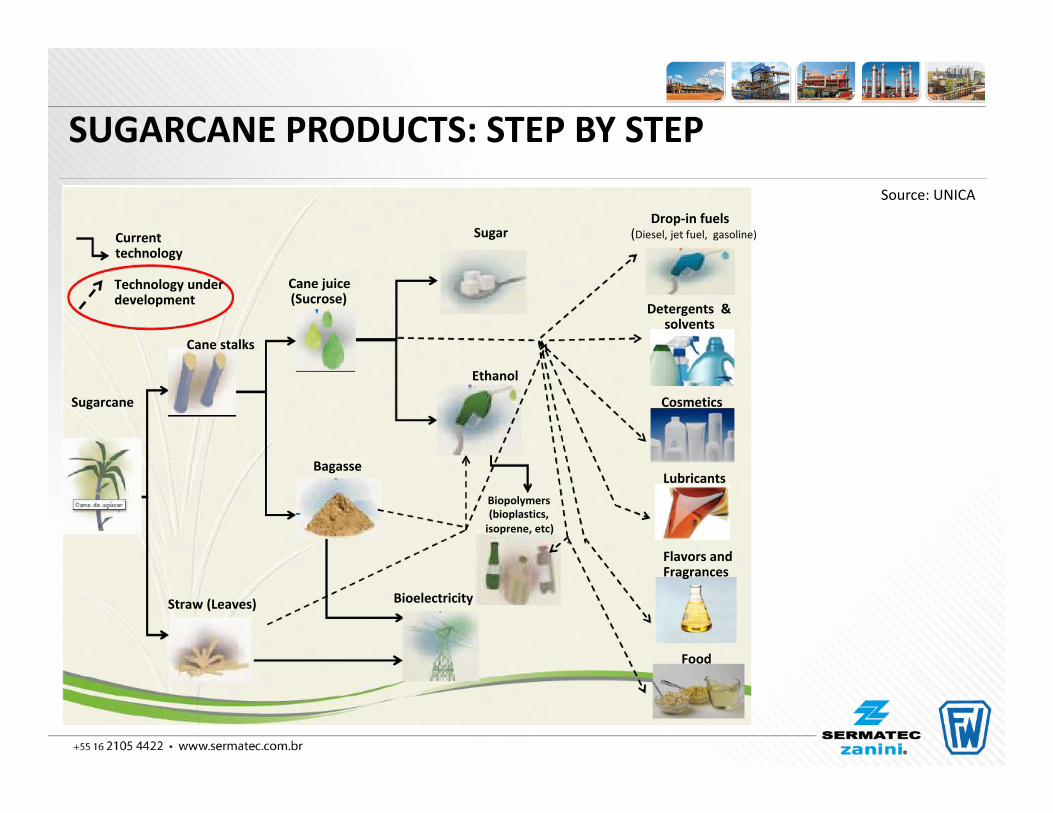

Cane juice(Sucrose)

Bagasse

Ethanol

Sugarcane

SugarCurrenttechnology

Technology underdevelopment

Cane stalks

Detergents &solvents

Cosmetics

Drop‐in fuels(Diesel, jet fuel, gasoline)

Straw (Leaves) Bioelectricity

Biopolymers(bioplastics,isoprene, etc)

Lubricants

Flavors andFragrances

Food

Source: UNICA

SUGARCANE PRODUCTS: STEP BY STEP

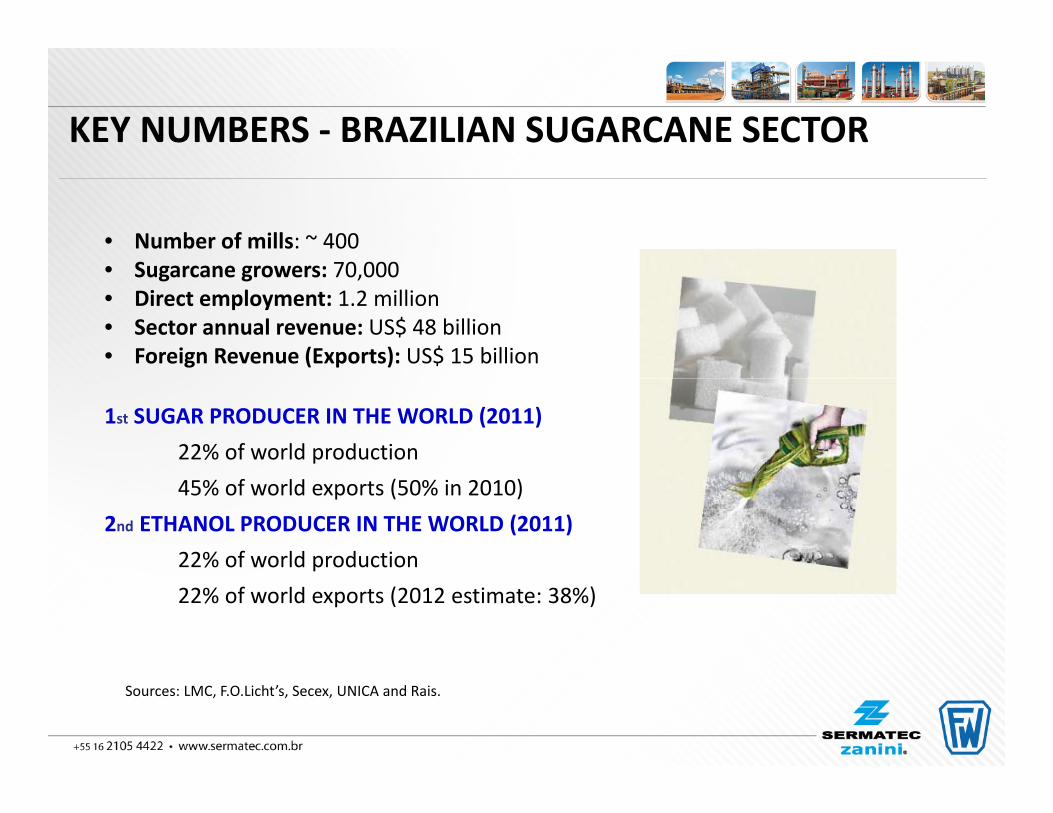

Sources: LMC, F.O.Licht’s, Secex, UNICA and Rais.

• Number of mills: ~ 400• Sugarcane growers: 70,000• Direct employment: 1.2 million• Sector annual revenue: US$ 48 billion• Foreign Revenue (Exports): US$ 15 billion

1st SUGAR PRODUCER IN THE WORLD (2011)22% of world production45% of world exports (50% in 2010)

2nd ETHANOL PRODUCER IN THE WORLD (2011)22% of world production22% of world exports (2012 estimate: 38%)

KEY NUMBERS ‐ BRAZILIAN SUGARCANE SECTOR

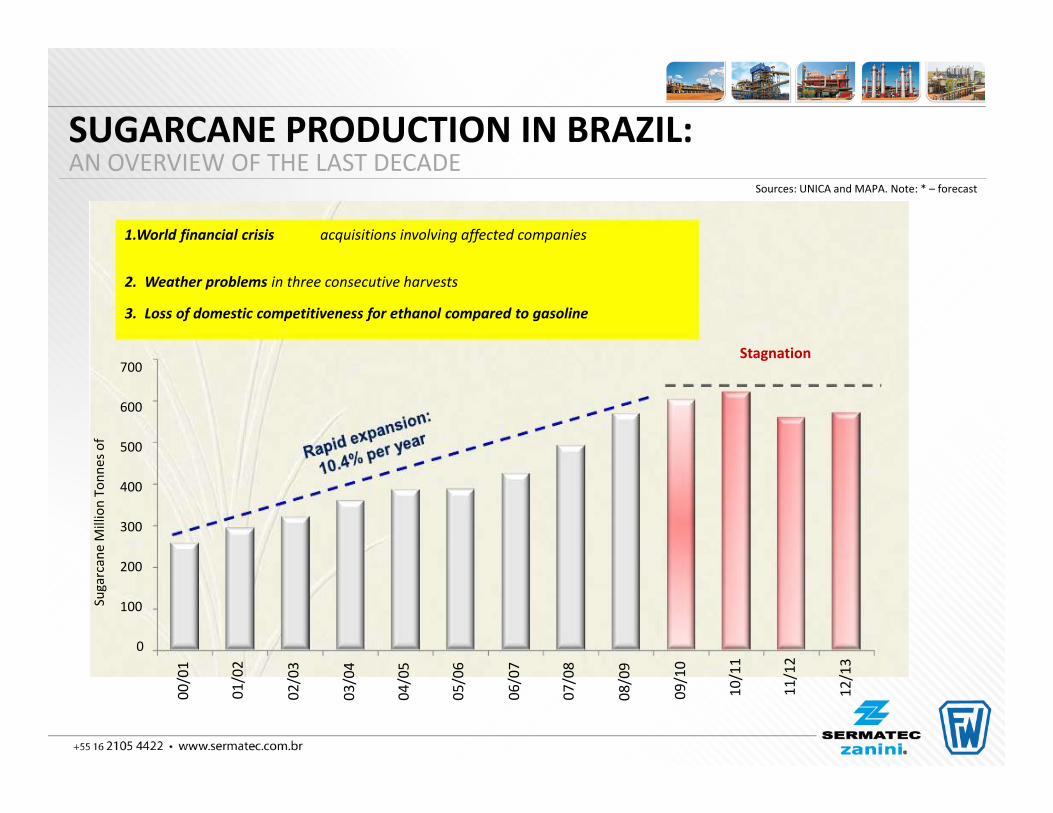

SugarcaneMillionTonn

esof

00/01

01/02

02/03

03/04

04/05

05/06

06/07

07/08

08/09

09/10

12/13

10/11

11/12

Stagnation

1.World financial crisis acquisitions involving affected companies

2. Weather problems in three consecutive harvests

3. Loss of domestic competitiveness for ethanol compared to gasoline

700

600

500

400

300

200

100

0

Sources: UNICA and MAPA. Note: * – forecast

SUGARCANE PRODUCTION IN BRAZIL:AN OVERVIEW OF THE LAST DECADE

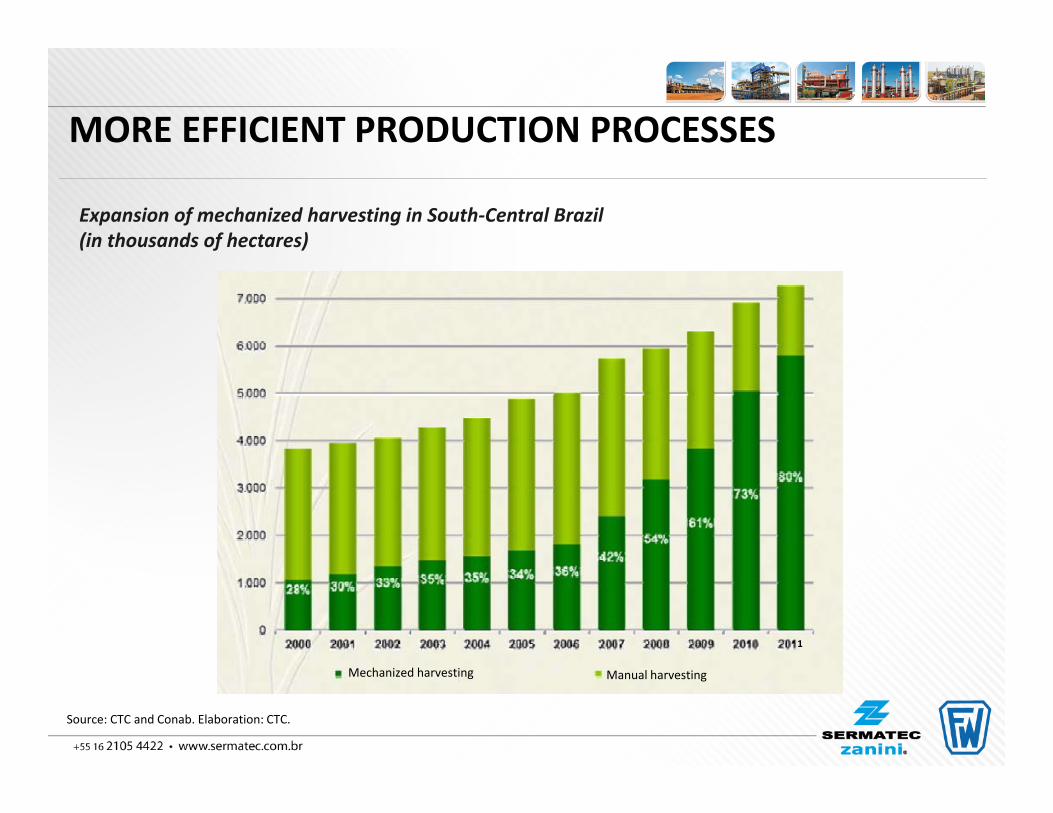

Expansion of mechanized harvesting in South‐Central Brazil(in thousands of hectares)

1

Mechanized harvesting Manual harvesting

Source: CTC and Conab. Elaboration: CTC.

MORE EFFICIENT PRODUCTION PROCESSES

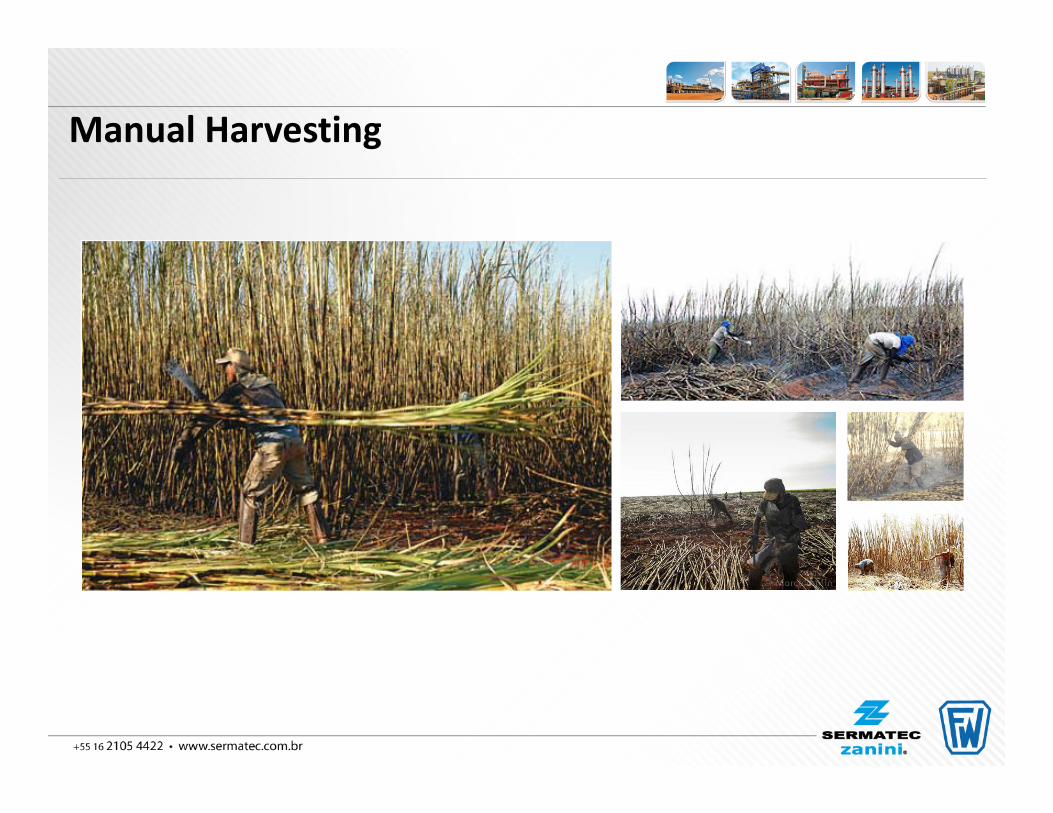

Manual Harvesting

Mechanized Harvesting

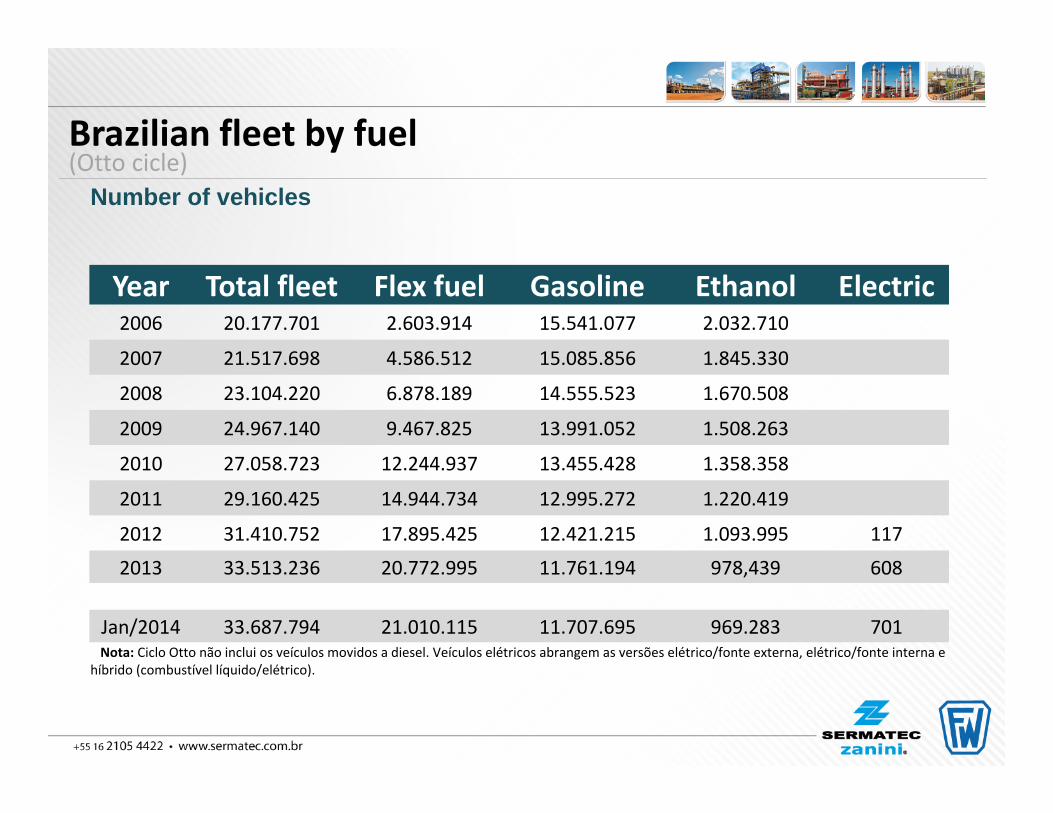

Brazilian fleet by fuel(Otto cicle)

Number of vehicles

Year Total fleet Flex fuel Gasoline Ethanol Electric2006 20.177.701 2.603.914 15.541.077 2.032.710

2007 21.517.698 4.586.512 15.085.856 1.845.330

2008 23.104.220 6.878.189 14.555.523 1.670.508

2009 24.967.140 9.467.825 13.991.052 1.508.263

2010 27.058.723 12.244.937 13.455.428 1.358.358

2011 29.160.425 14.944.734 12.995.272 1.220.419

2012 31.410.752 17.895.425 12.421.215 1.093.995 117

2013 33.513.236 20.772.995 11.761.194 978,439 608

Jan/2014 33.687.794 21.010.115 11.707.695 969.283 701Nota: Ciclo Otto não inclui os veículos movidos a diesel. Veículos elétricos abrangem as versões elétrico/fonte externa, elétrico/fonte interna e

híbrido (combustível líquido/elétrico).

motorcycles

(million)

Fleet

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

Millions

ofvehicles

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2018

2019

2020

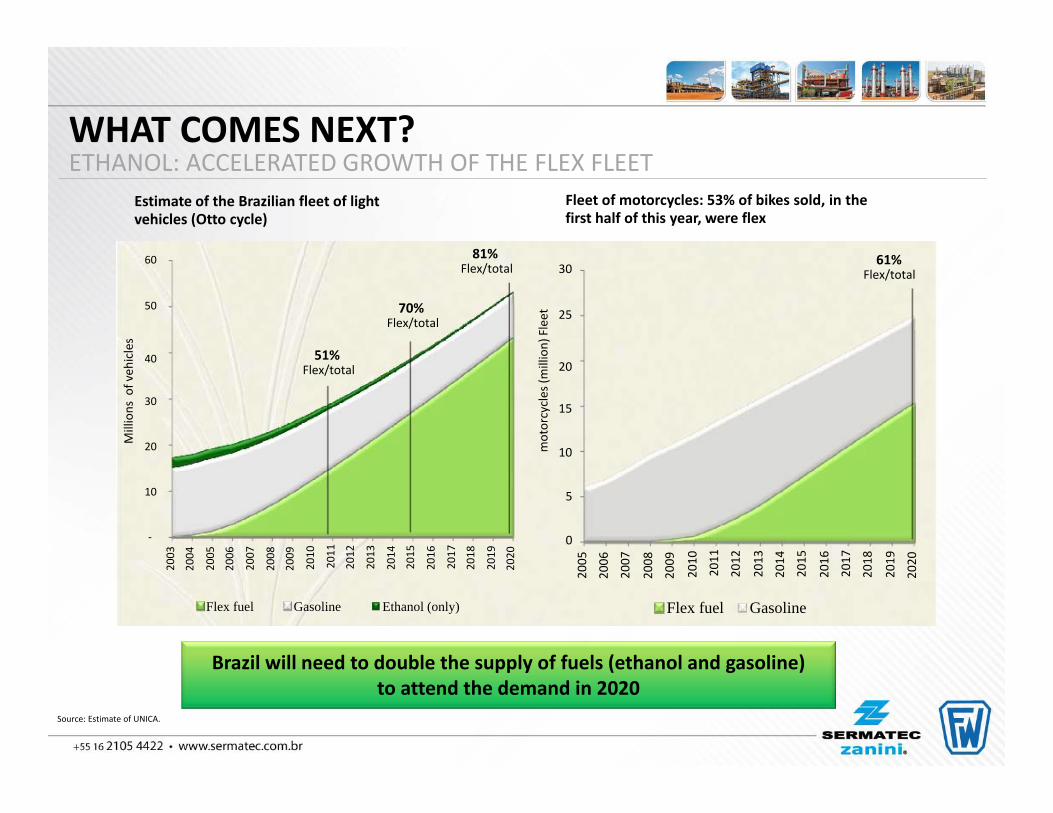

Estimate of the Brazilian fleet of lightvehicles (Otto cycle)

50

60

51%Flex/total

70%Flex/total

81%Flex/total

25

3061%

Flex/total

Fleet of motorcycles: 53% of bikes sold, in thefirst half of this year, were flex

40

30

20

10

‐

Flex fuel Gasoline Ethanol (only)

20

15

10

5

0

Flex fuel Gasoline

Source: Estimate of UNICA.

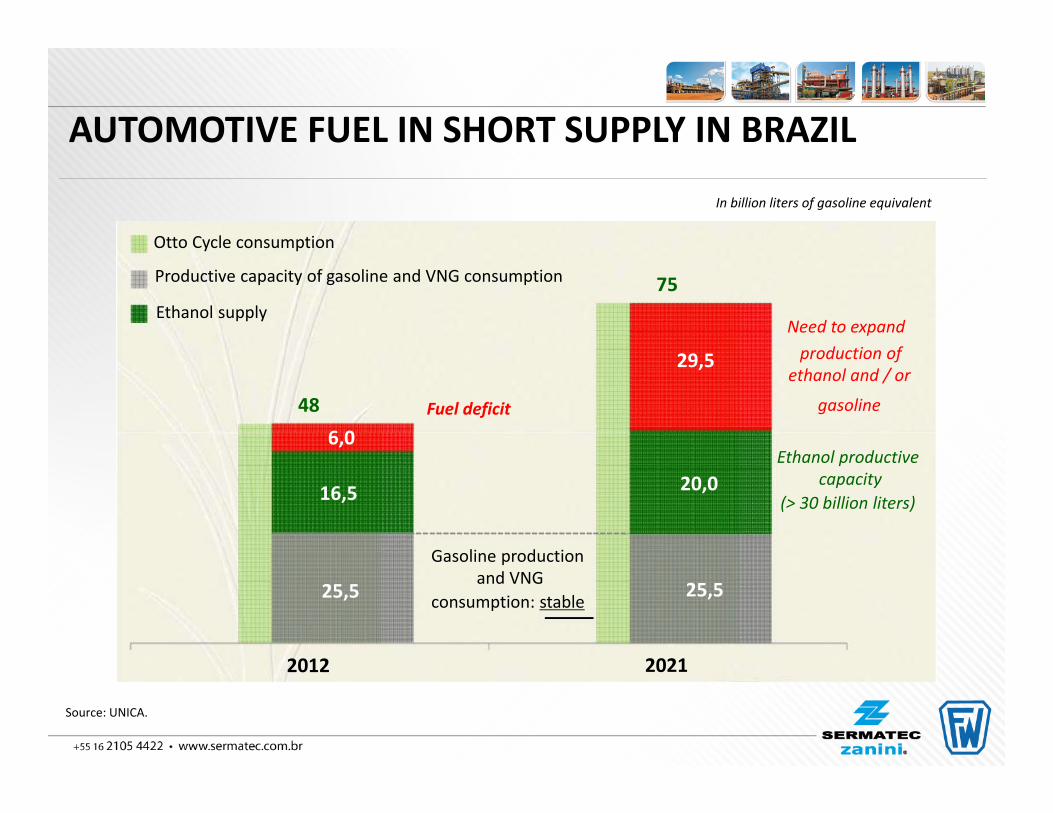

Brazil will need to double the supply of fuels (ethanol and gasoline)to attend the demand in 2020

WHAT COMES NEXT?ETHANOL: ACCELERATED GROWTH OF THE FLEX FLEET

48

75Ethanol supply

Productive capacity of gasoline and VNG consumption

29,5

Need to expandproduction of

ethanol and / or

gasoline

Otto Cycle consumption

Fuel deficit

6,0

16,5

25,5

2012

25,5

2021

20,0Ethanol productive

capacity(> 30 billion liters)

Gasoline productionand VNG

consumption: stable

Source: UNICA.

In billion liters of gasoline equivalent

AUTOMOTIVE FUEL IN SHORT SUPPLY IN BRAZIL

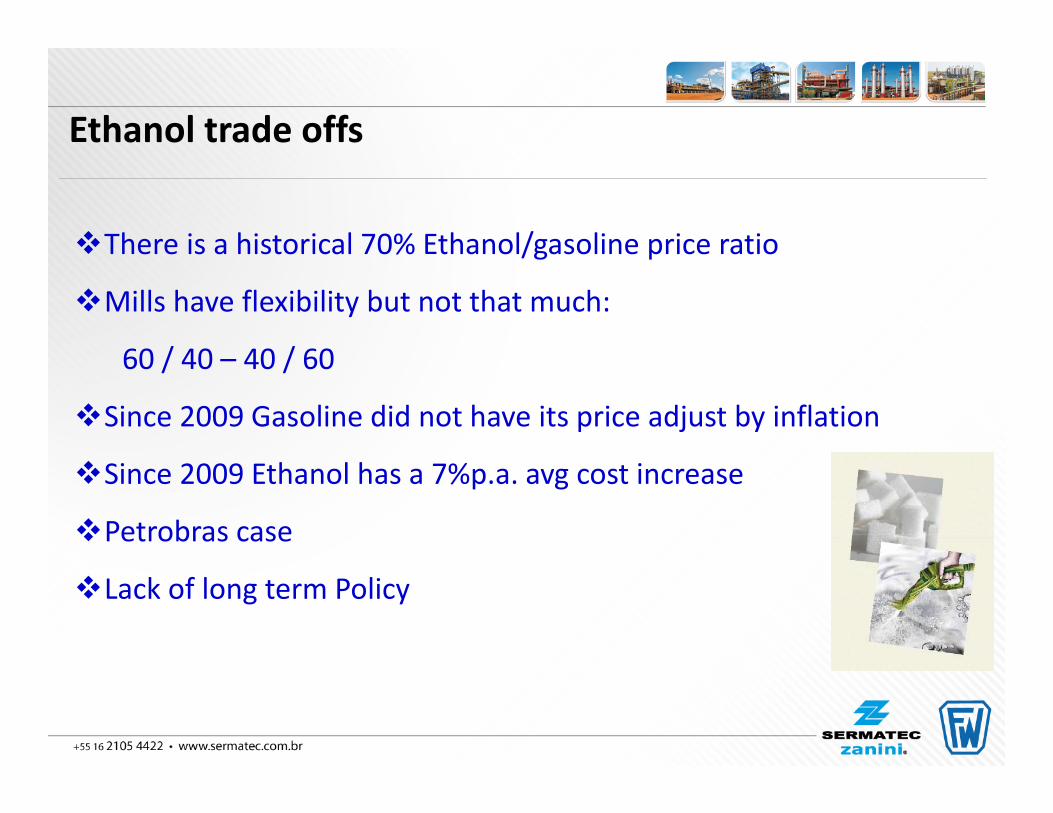

There is a historical 70% Ethanol/gasoline price ratio

Mills have flexibility but not that much:

60 / 40 – 40 / 60

Since 2009 Gasoline did not have its price adjust by inflation

Since 2009 Ethanol has a 7%p.a. avg cost increase

Petrobras case

Lack of long term Policy

Ethanol trade offs

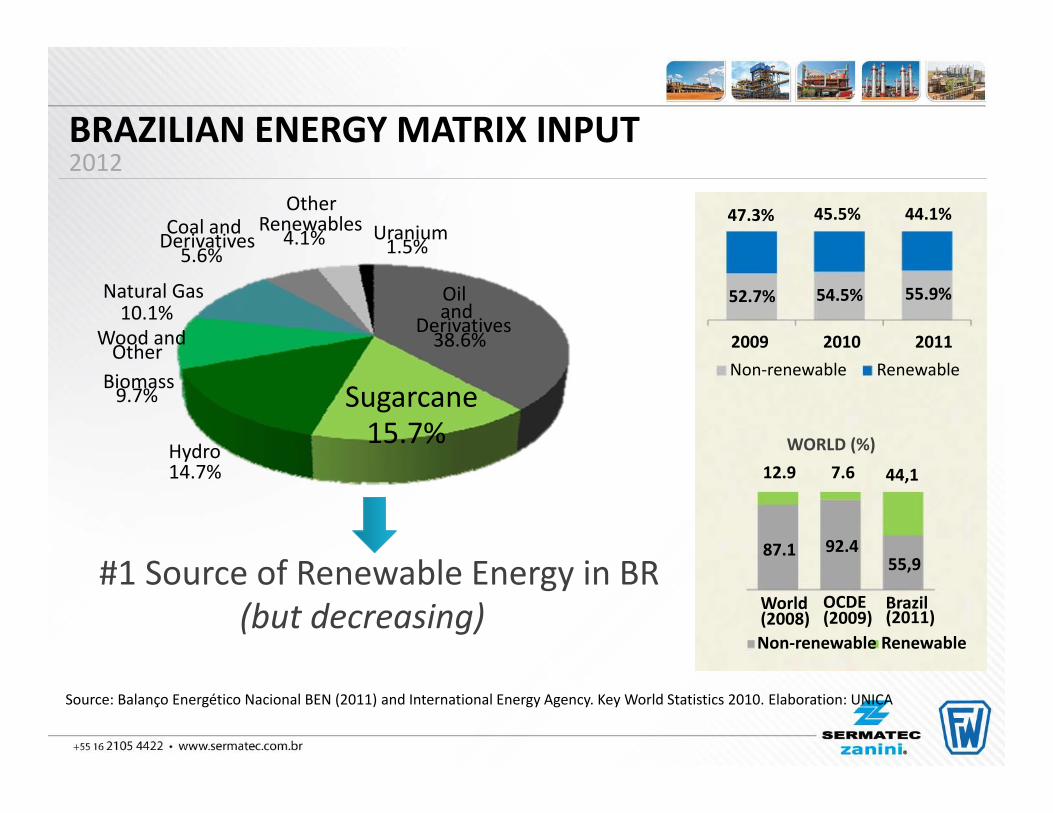

Source: Balanço Energético Nacional BEN (2011) and International Energy Agency. Key World Statistics 2010. Elaboration: UNICA

BRAZILIAN ENERGY MATRIX INPUT2012

52.7% 54.5% 55.9%

47.3% 45.5% 44.1%

2009 2010 2011Non‐renewable Renewable

WORLD (%)12.9 7.6 44,1

87.1

World(2008)

92.4

OCDE(2009)

55,9

Brazil(2011)

Non‐renewable Renewable

Oiland

Derivatives38.6%

Natural Gas10.1%

Wood andOther

Coal andDerivatives5.6%

OtherRenewables

4.1% Uranium1.5%

Sugarcane15.7%

Hydro14.7%

Biomass9.7%

#1 Source of Renewable Energy in BR(but decreasing)

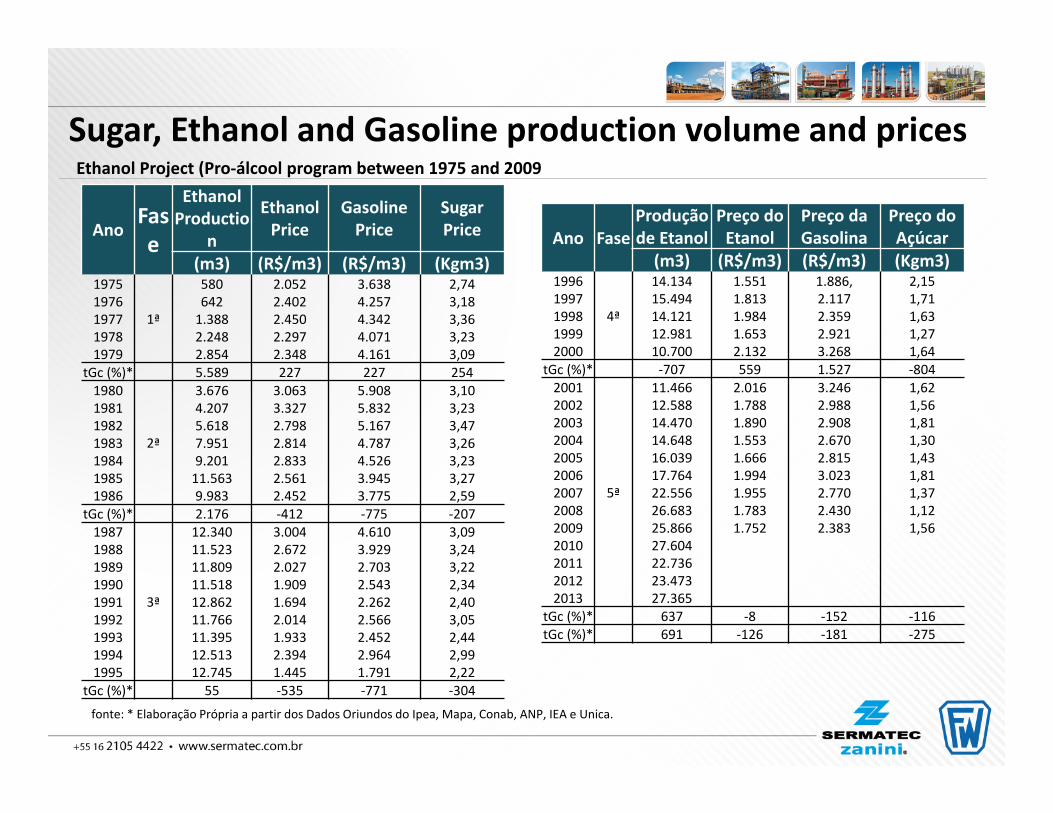

Sugar, Ethanol and Gasoline production volume and prices

AnoFase

EthanolProductio

n

EthanolPrice

GasolinePrice

Sugar Price

(m3) (R$/m3) (R$/m3) (Kgm3)19751976197719781979

1ª

5806421.3882.2482.854

2.0522.4022.4502.2972.348

3.6384.2574.3424.0714.161

2,743,183,363,233,09

tGc (%)* 5.589 227 227 2541980198119821983198419851986

2ª

3.6764.2075.6187.9519.20111.5639.983

3.0633.3272.7982.8142.8332.5612.452

5.9085.8325.1674.7874.5263.9453.775

3,103,233,473,263,233,272,59

tGc (%)* 2.176 ‐412 ‐775 ‐207198719881989199019911992199319941995

3ª

12.34011.52311.80911.51812.86211.76611.39512.51312.745

3.0042.6722.0271.9091.6942.0141.9332.3941.445

4.6103.9292.7032.5432.2622.5662.4522.9641.791

3,093,243,222,342,403,052,442,992,22

tGc (%)* 55 ‐535 ‐771 ‐304

Ethanol Project (Pro‐álcool program between 1975 and 2009

Ano FaseProdução de Etanol

Preço do Etanol

Preço da Gasolina

Preço do Açúcar

(m3) (R$/m3) (R$/m3) (Kgm3)19961997199819992000

4ª

14.13415.49414.12112.98110.700

1.5511.8131.9841.6532.132

1.886,2.1172.3592.9213.268

2,151,711,631,271,64

tGc (%)* ‐707 559 1.527 ‐8042001200220032004200520062007200820092010201120122013

5ª

11.46612.58814.47014.64816.03917.76422.55626.68325.86627.60422.73623.47327.365

2.0161.7881.8901.5531.6661.9941.9551.7831.752

3.2462.9882.9082.6702.8153.0232.7702.4302.383

1,621,561,811,301,431,811,371,121,56

tGc (%)* 637 ‐8 ‐152 ‐116tGc (%)* 691 ‐126 ‐181 ‐275

fonte: * Elaboração Própria a partir dos Dados Oriundos do Ipea, Mapa, Conab, ANP, IEA e Unica.

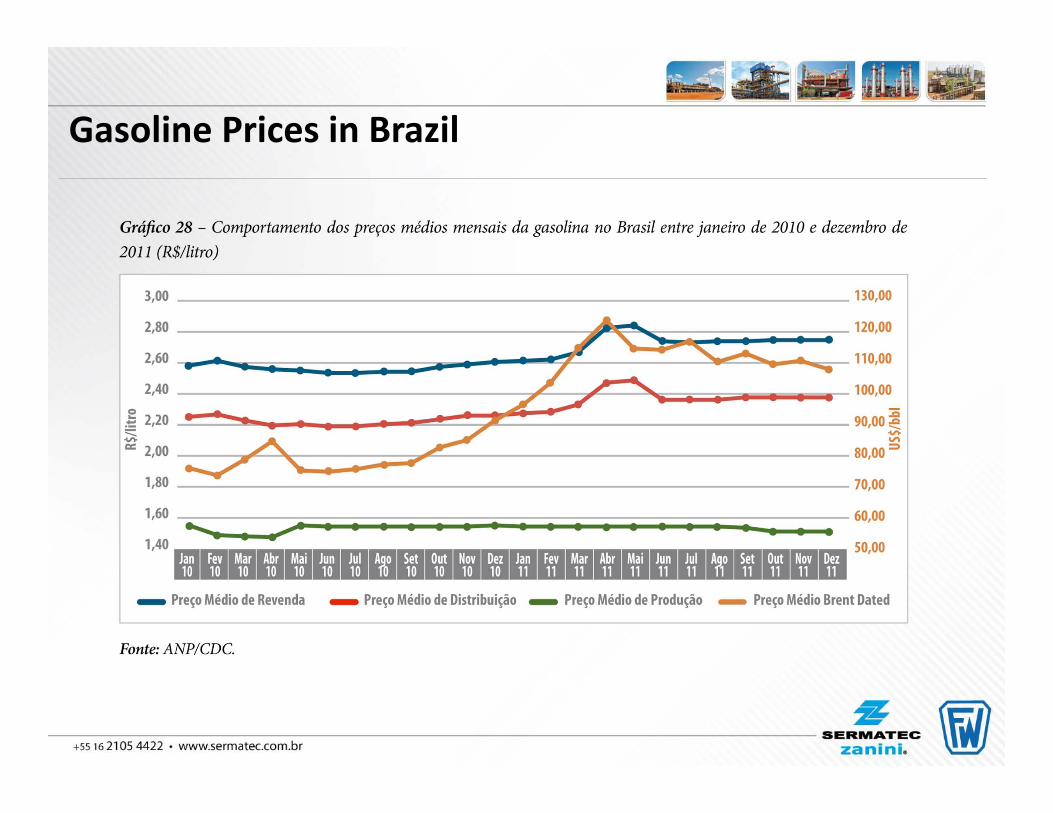

Gasoline Prices in Brazil

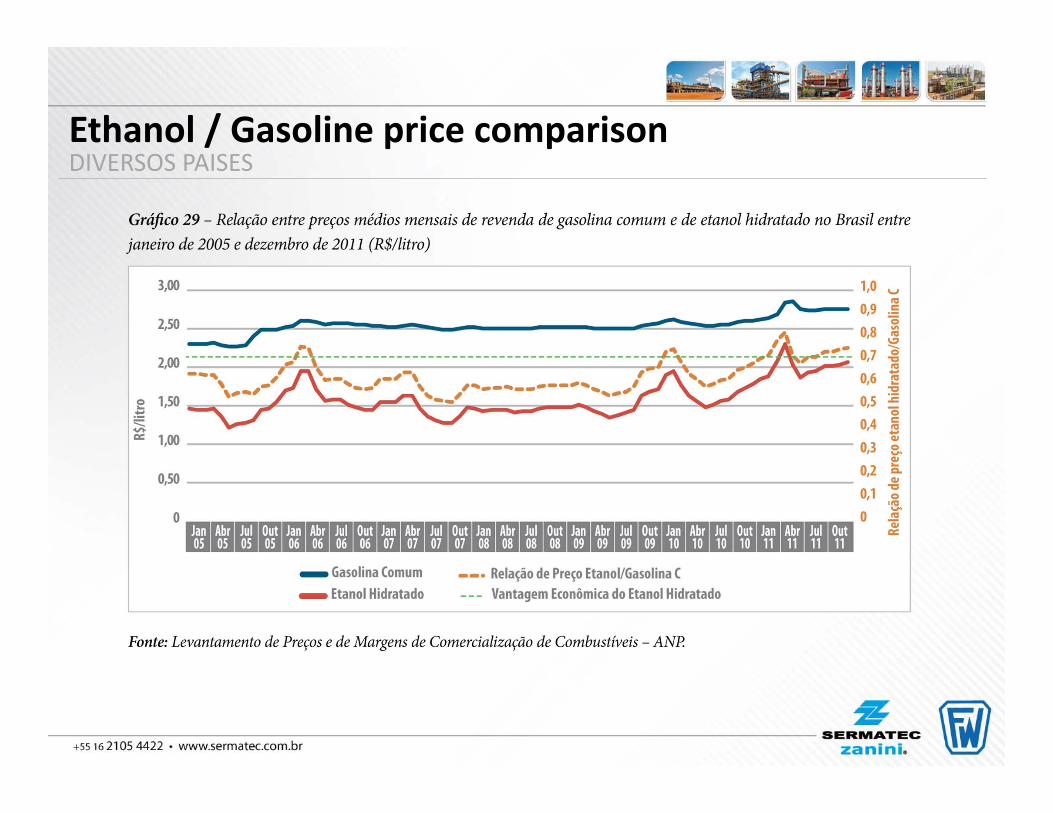

Ethanol / Gasoline price comparisonDIVERSOS PAISES

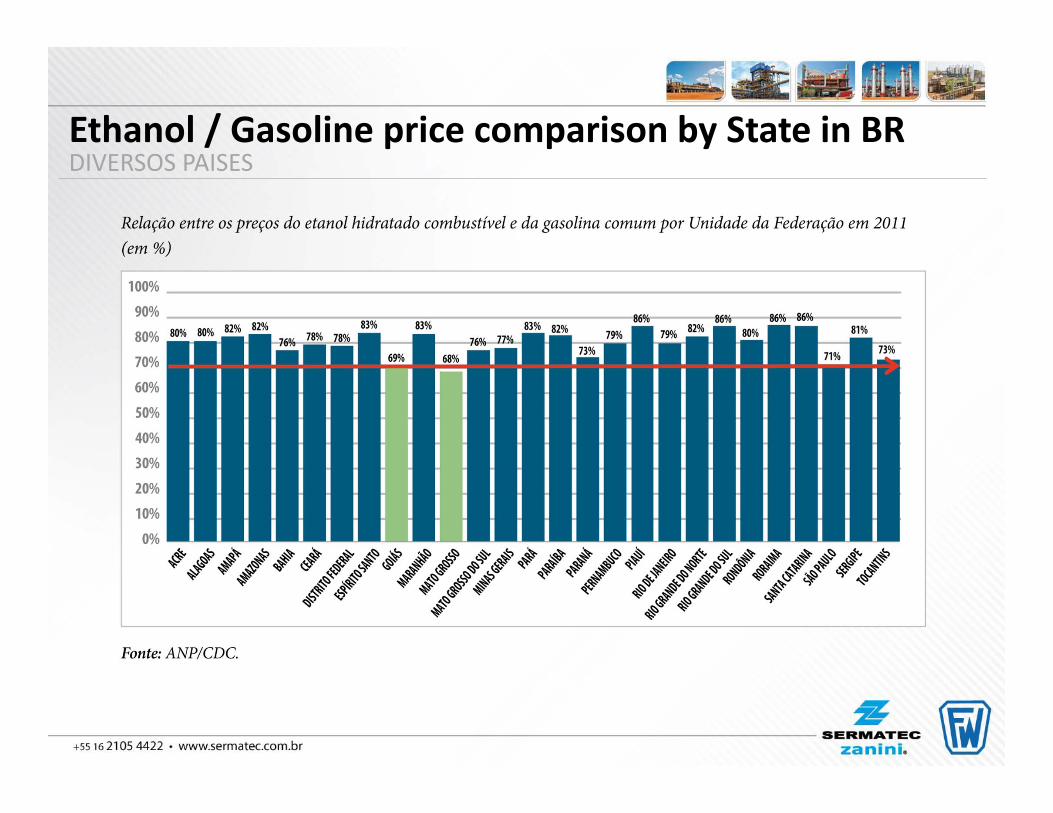

Ethanol / Gasoline price comparison by State in BRDIVERSOS PAISES

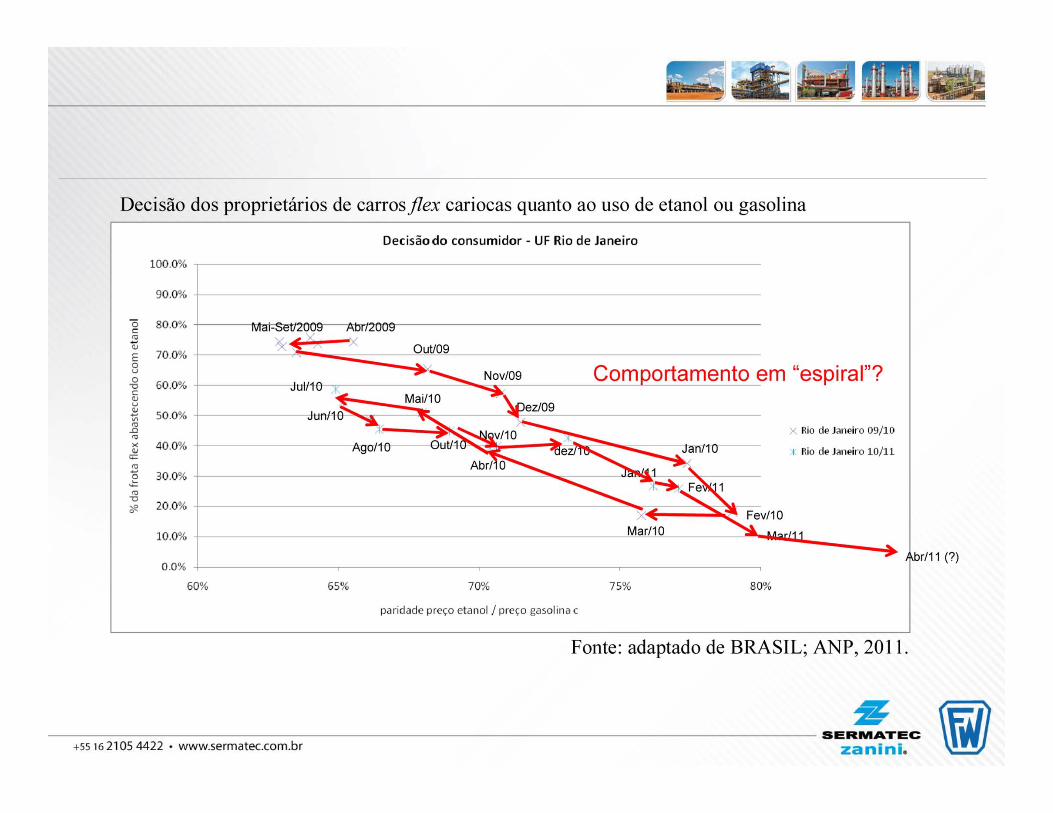

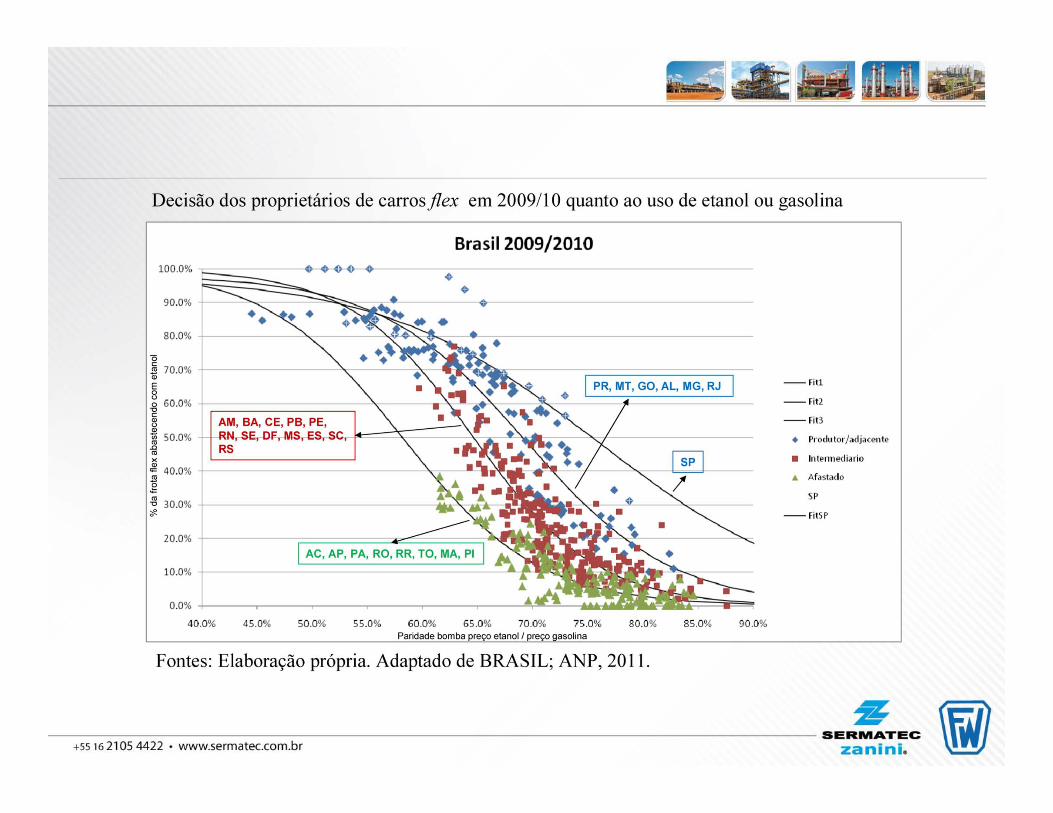

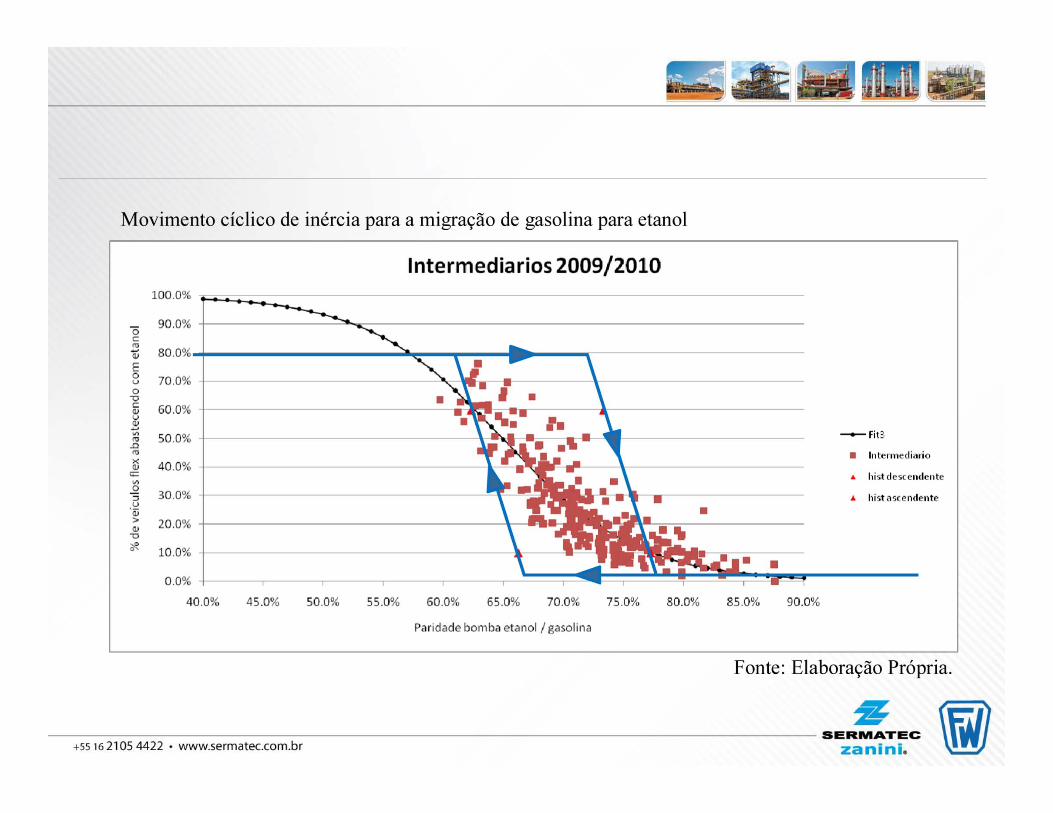

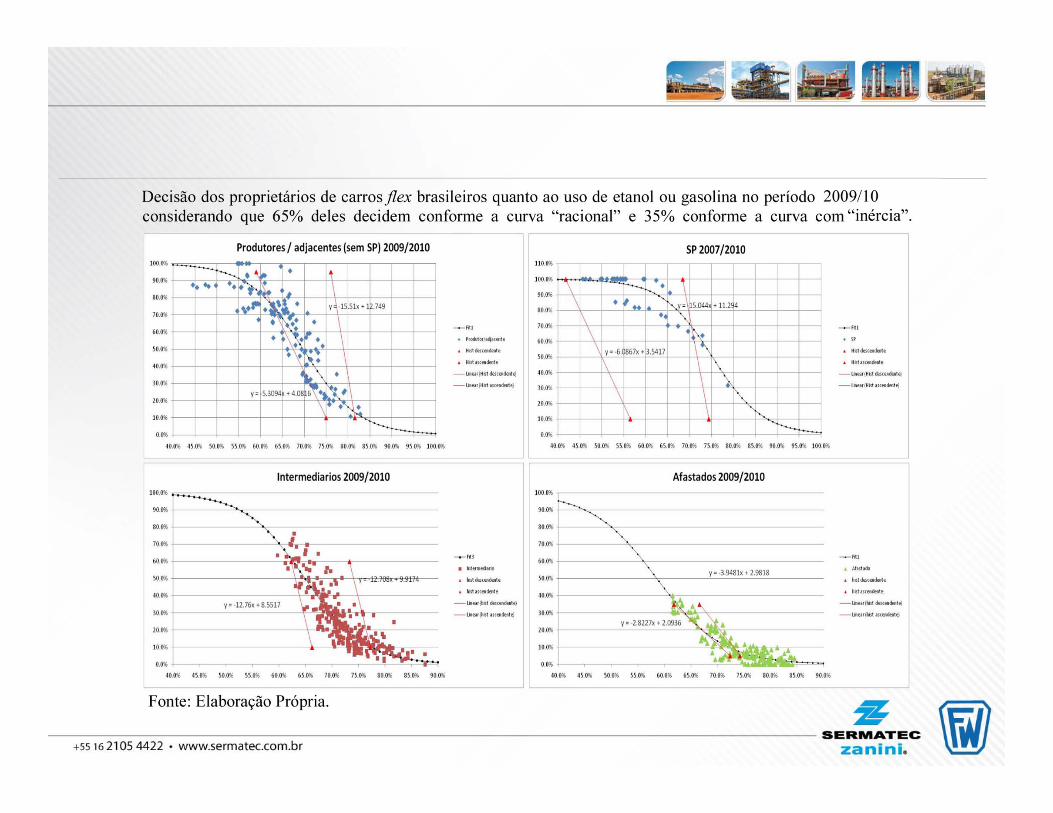

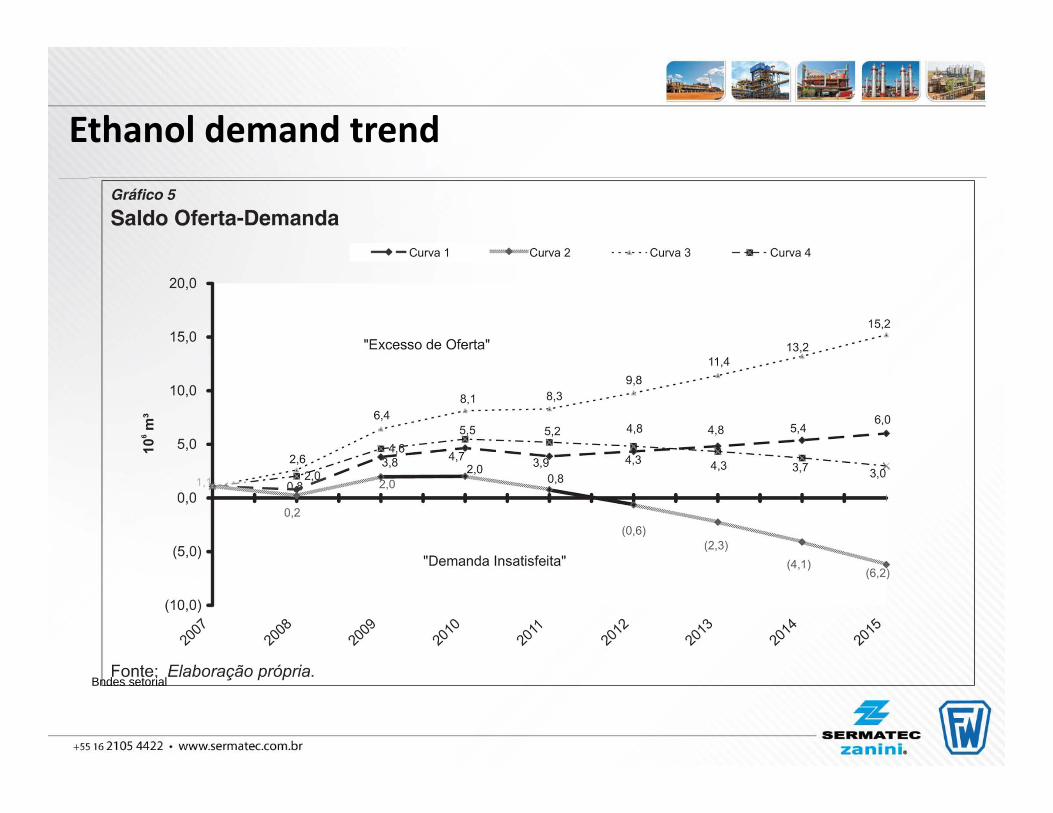

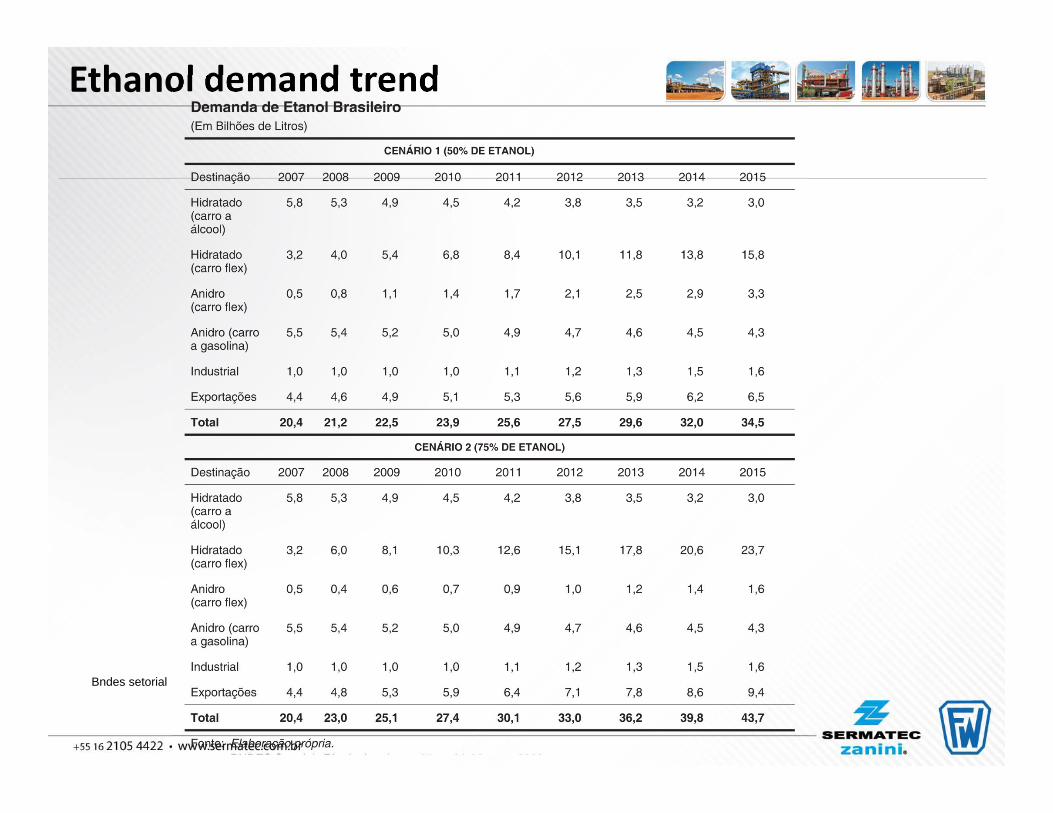

Ethanol demand trend

Bndes setorial

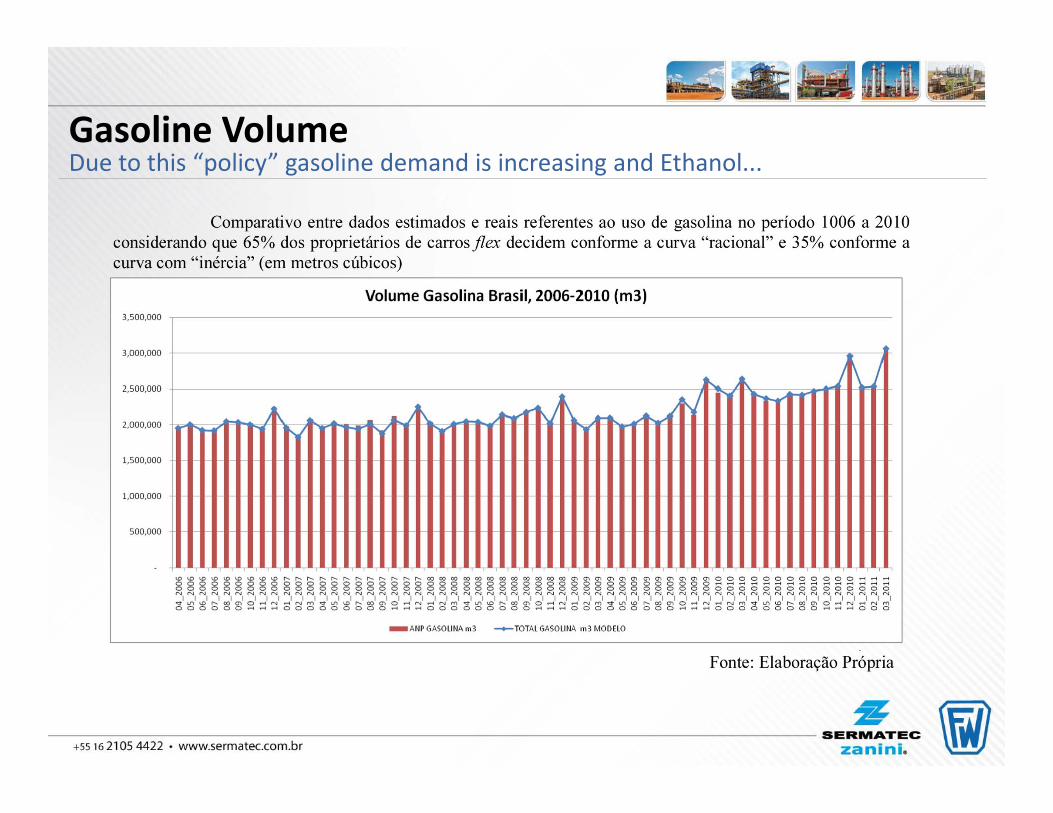

Gasoline VolumeDue to this “policy” gasoline demand is increasing and Ethanol...

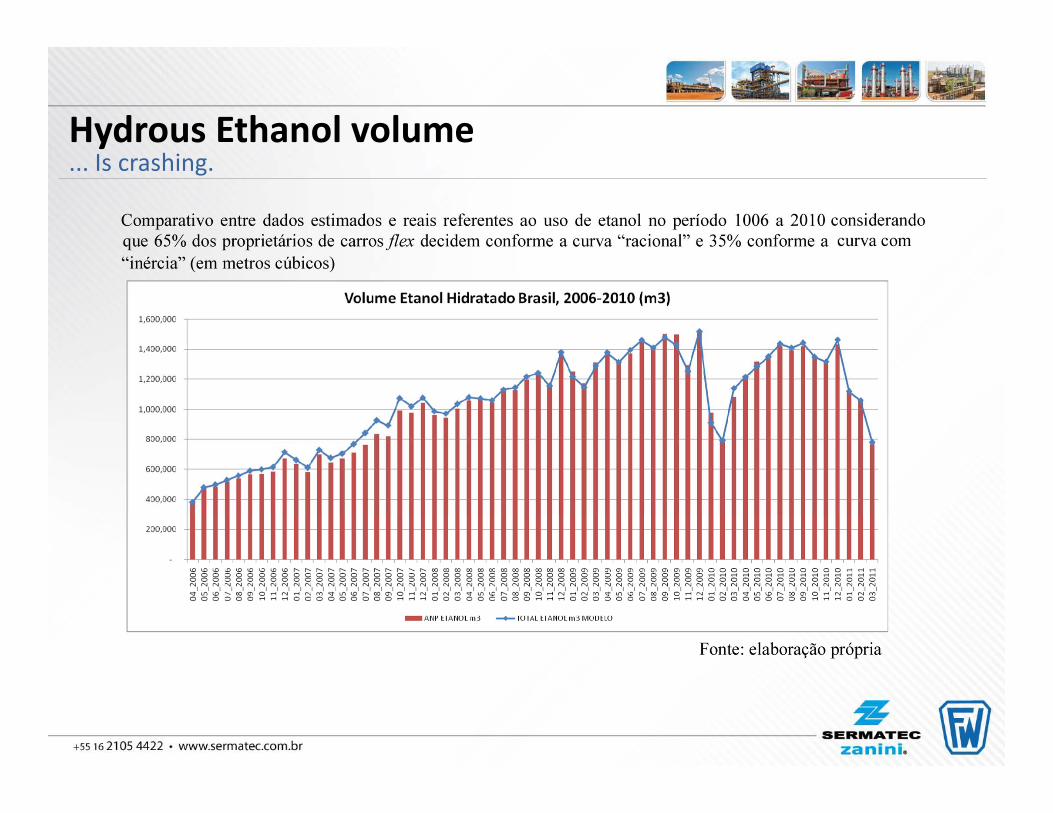

Hydrous Ethanol volume... Is crashing.

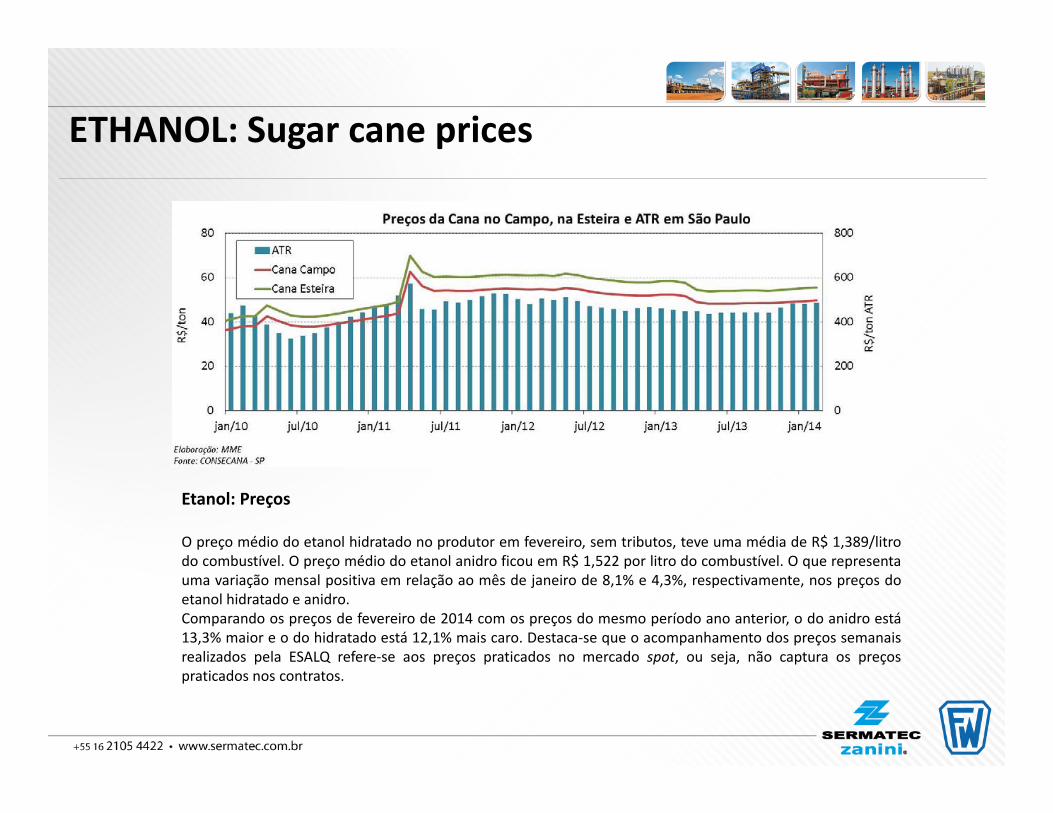

ETHANOL: Sugar cane prices

Etanol: Preços

O preço médio do etanol hidratado no produtor em fevereiro, sem tributos, teve uma média de R$ 1,389/litrodo combustível. O preço médio do etanol anidro ficou em R$ 1,522 por litro do combustível. O que representauma variação mensal positiva em relação ao mês de janeiro de 8,1% e 4,3%, respectivamente, nos preços doetanol hidratado e anidro.Comparando os preços de fevereiro de 2014 com os preços do mesmo período ano anterior, o do anidro está13,3% maior e o do hidratado está 12,1% mais caro. Destaca‐se que o acompanhamento dos preços semanaisrealizados pela ESALQ refere‐se aos preços praticados no mercado spot, ou seja, não captura os preçospraticados nos contratos.

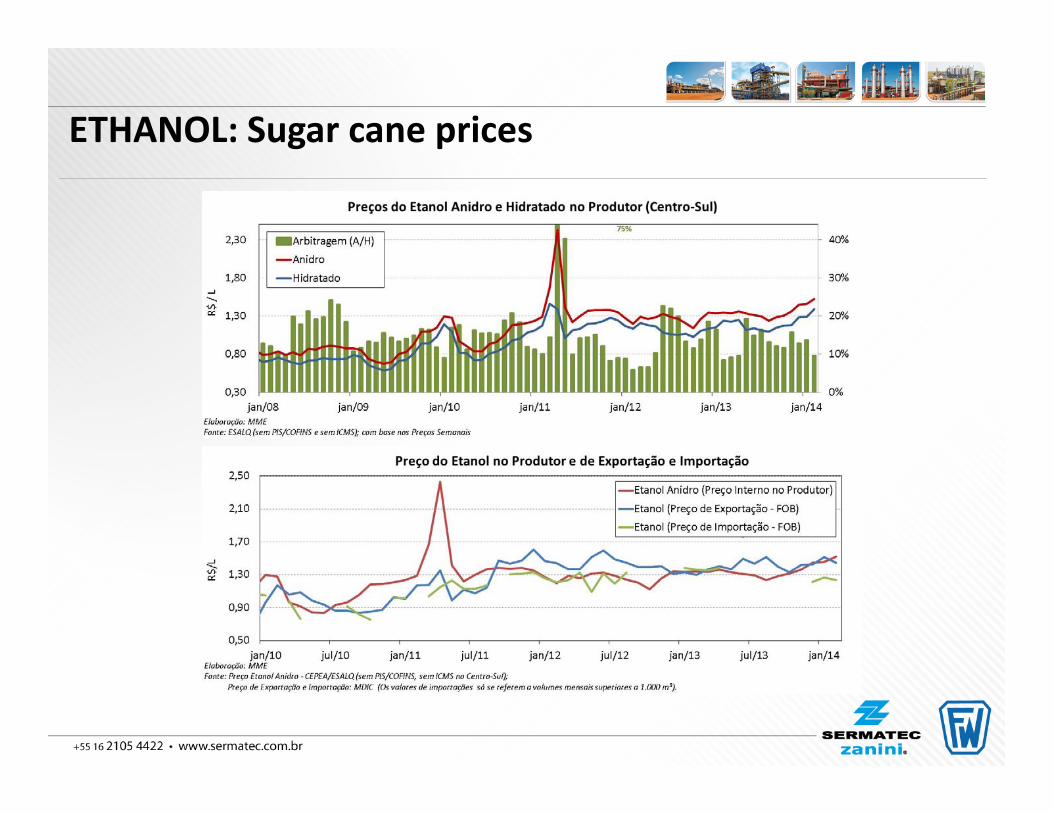

ETHANOL: Sugar cane prices

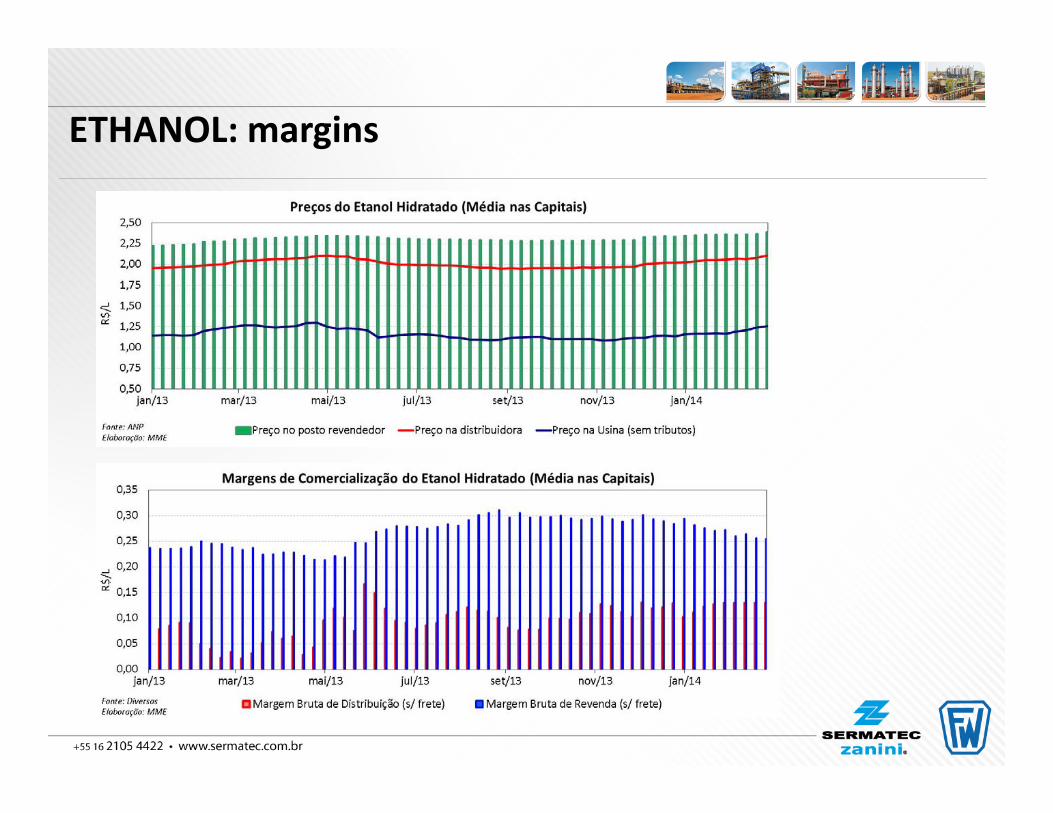

ETHANOL: margins

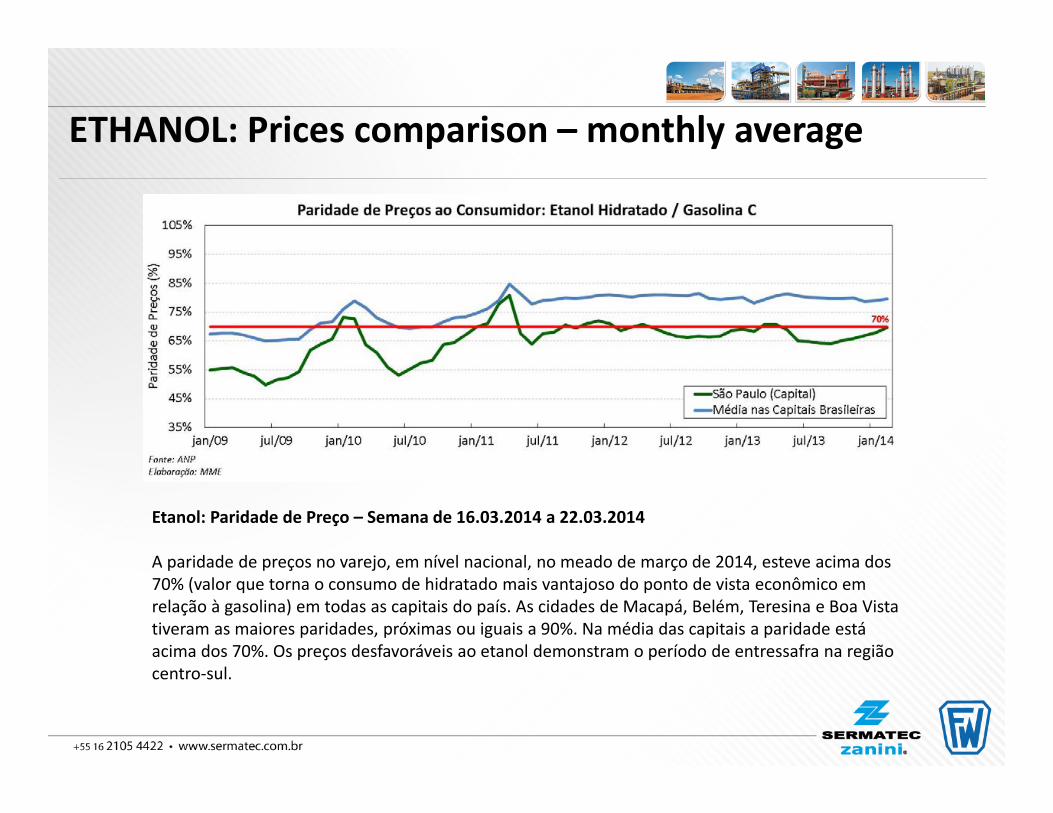

ETHANOL: Prices comparison – monthly average

Etanol: Paridade de Preço – Semana de 16.03.2014 a 22.03.2014

A paridade de preços no varejo, em nível nacional, no meado de março de 2014, esteve acima dos 70% (valor que torna o consumo de hidratado mais vantajoso do ponto de vista econômico em relação à gasolina) em todas as capitais do país. As cidades de Macapá, Belém, Teresina e Boa Vista tiveram as maiores paridades, próximas ou iguais a 90%. Na média das capitais a paridade está acima dos 70%. Os preços desfavoráveis ao etanol demonstram o período de entressafra na região centro‐sul.

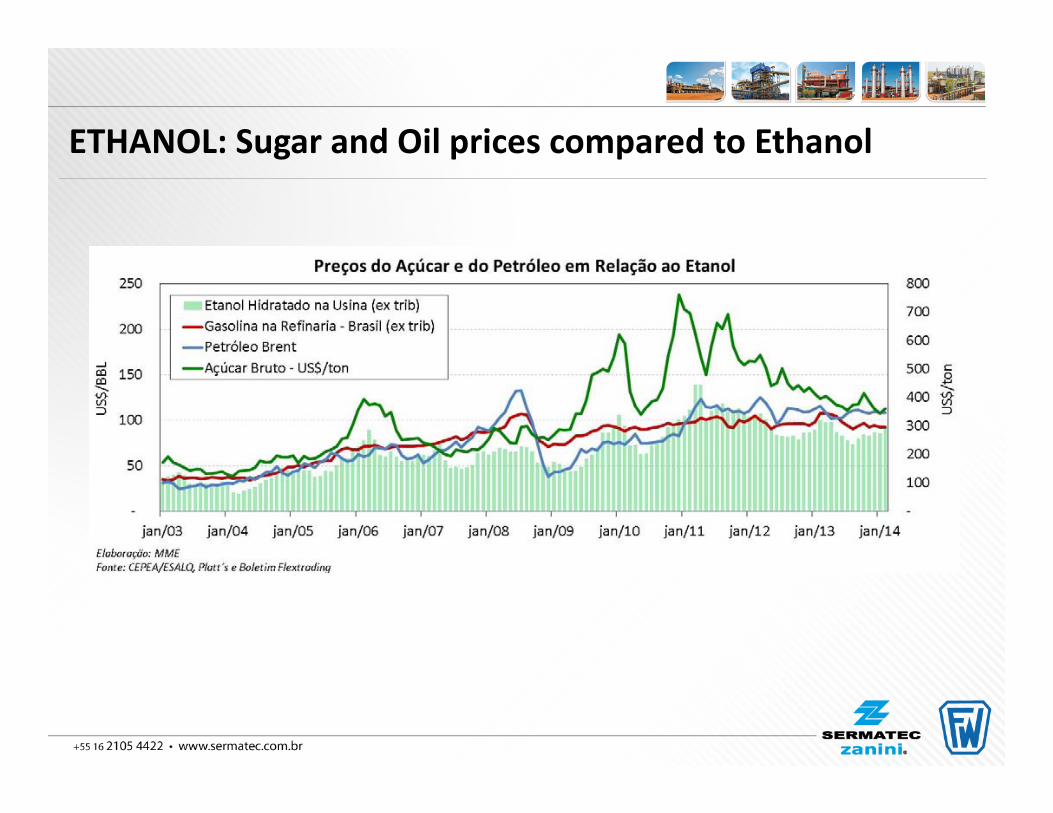

ETHANOL: Sugar and Oil prices compared to Ethanol

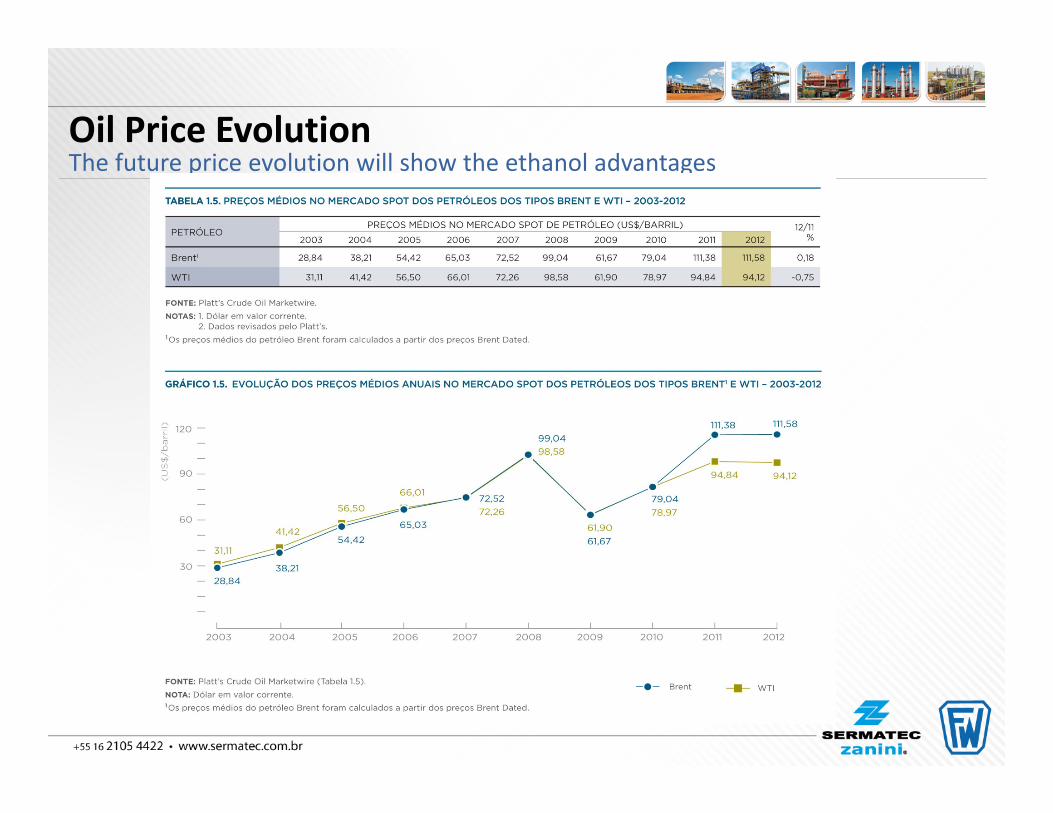

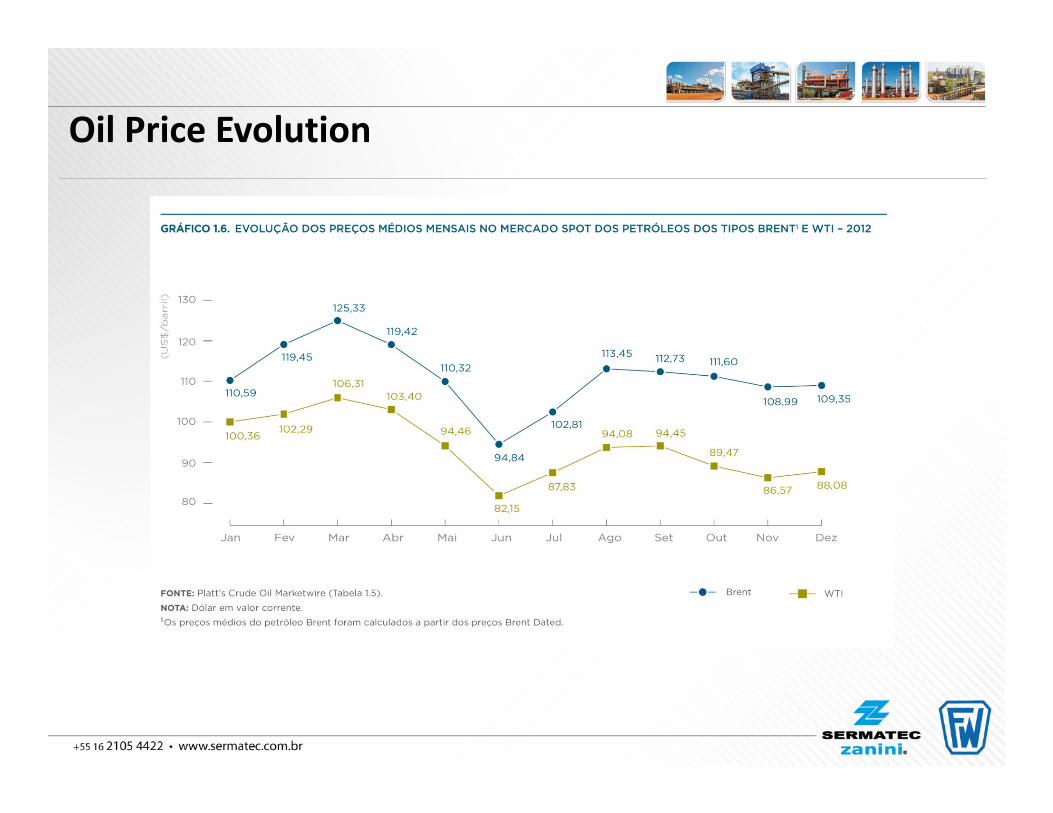

Oil Price EvolutionThe future price evolution will show the ethanol advantages

Oil Price Evolution

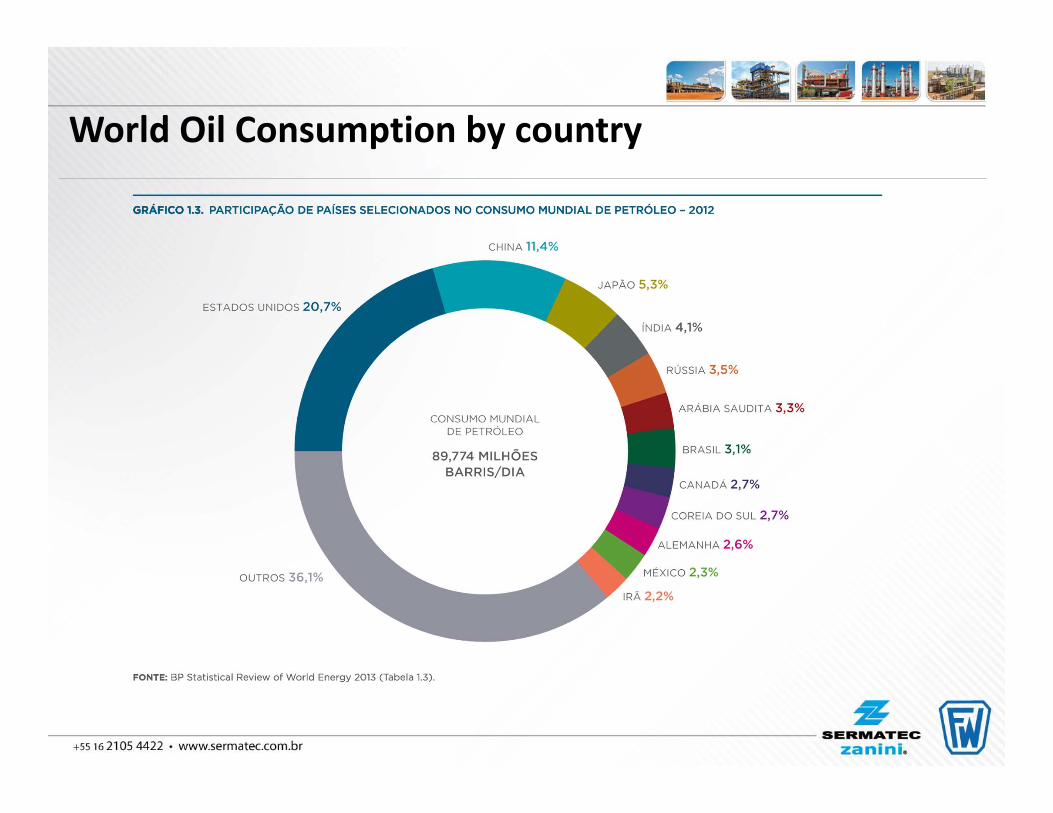

World Oil Consumption by country

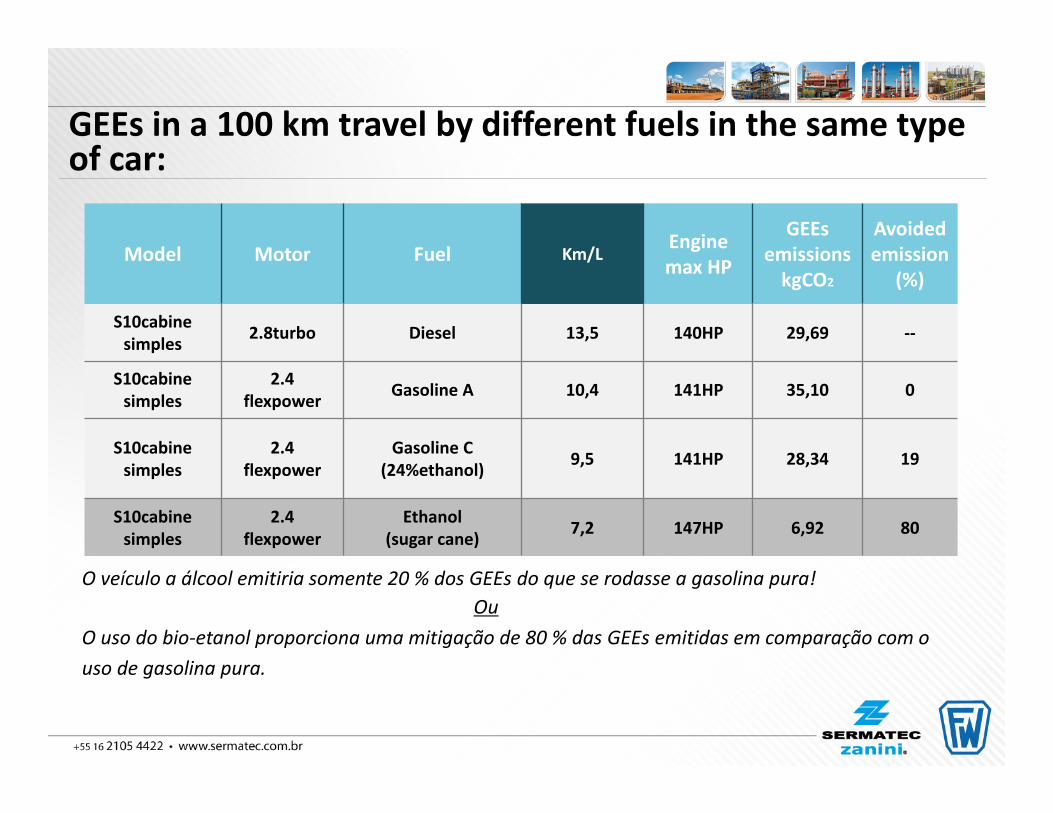

Model Motor Fuel Km/LEngine max HP

GEEsemissionskgCO2

Avoidedemission

(%)

S10cabinesimples 2.8turbo Diesel 13,5 140HP 29,69 ‐‐

S10cabinesimples

2.4flexpower Gasoline A 10,4 141HP 35,10 0

S10cabinesimples

2.4flexpower

Gasoline C(24%ethanol) 9,5 141HP 28,34 19

S10cabinesimples

2.4flexpower

Ethanol(sugar cane) 7,2 147HP 6,92 80

O veículo a álcool emitiria somente 20 % dos GEEs do que se rodasse a gasolina pura!Ou

O uso do bio‐etanol proporciona uma mitigação de 80 % das GEEs emitidas em comparação com ouso de gasolina pura.

GEEs in a 100 km travel by different fuels in the same type of car:

Ethanol will be an additive to gasoline worldwide

Biomass residue will have cost (waste also)

Algae may be the biggest source of CH

Nanotech will open new frontiers

Futurolgy

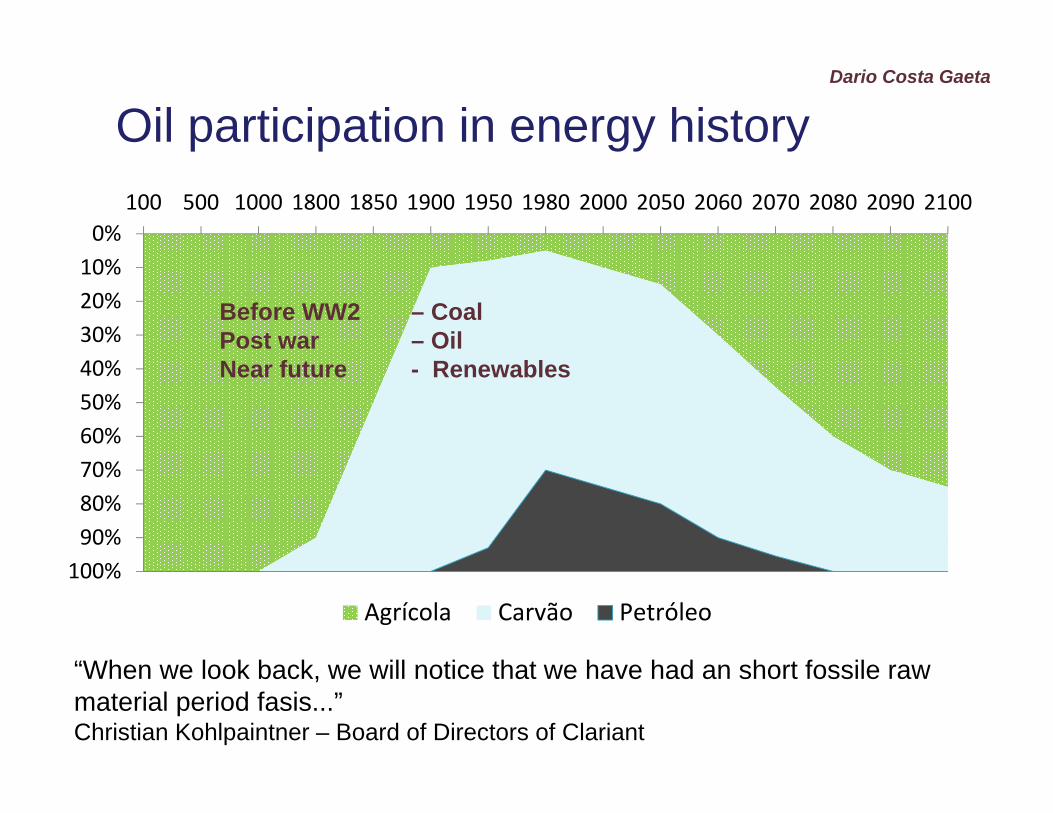

0%10%20%30%40%50%60%70%80%90%100%

100 500 1000 1800 1850 1900 1950 1980 2000 2050 2060 2070 2080 2090 2100

Agrícola Carvão Petróleo

Before WW2 – CoalPost war – OilNear future - Renewables

Dario Costa Gaeta

“When we look back, we will notice that we have had an short fossile rawmaterial period fasis...”Christian Kohlpaintner – Board of Directors of Clariant

Oil participation in energy history

Thank you!!!

Back up

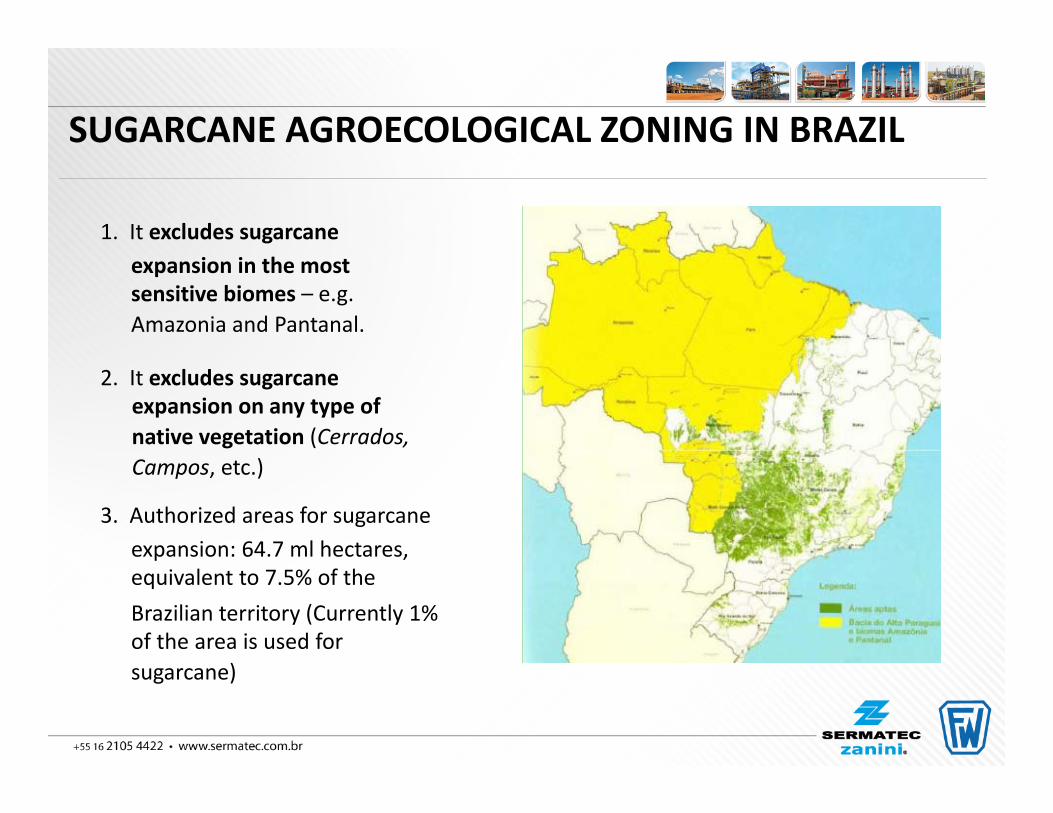

1. It excludes sugarcaneexpansion in the mostsensitive biomes – e.g.Amazonia and Pantanal.

2. It excludes sugarcaneexpansion on any type ofnative vegetation (Cerrados,Campos, etc.)

3. Authorized areas for sugarcaneexpansion: 64.7 ml hectares,equivalent to 7.5% of theBrazilian territory (Currently 1%of the area is used forsugarcane)

SUGARCANE AGROECOLOGICAL ZONING IN BRAZIL

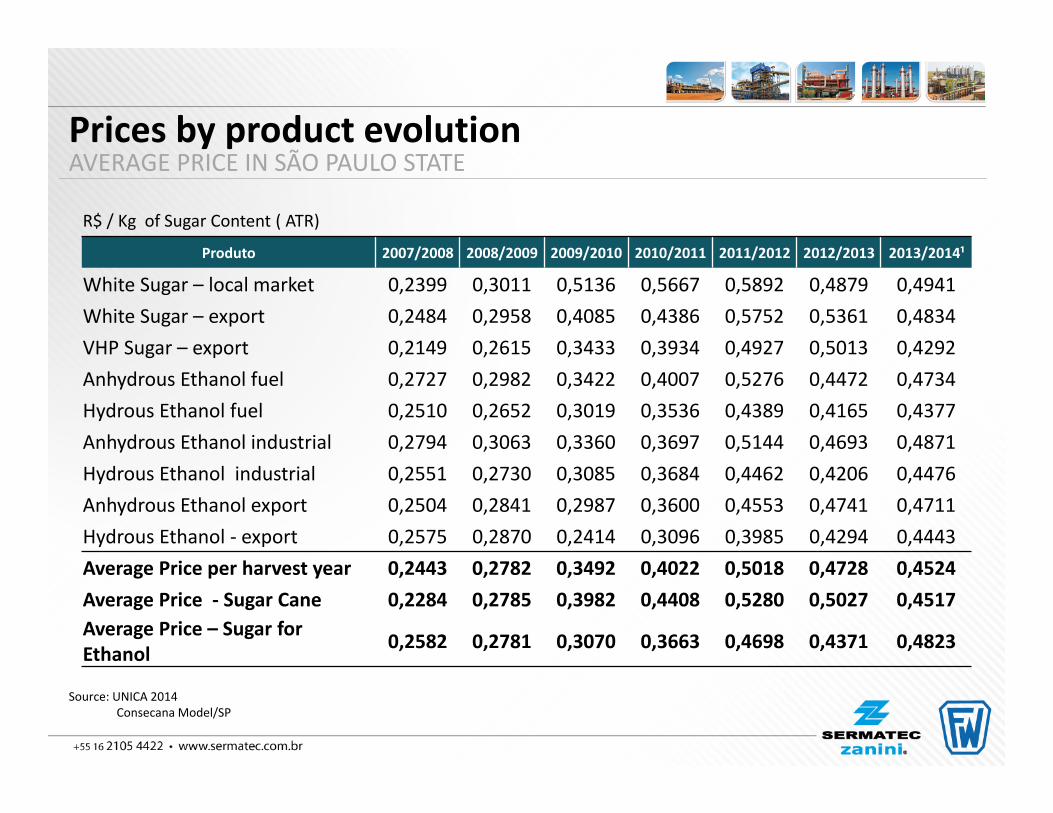

Prices by product evolutionAVERAGE PRICE IN SÃO PAULO STATE

Source: UNICA 2014Consecana Model/SP

R$ / Kg of Sugar Content ( ATR)

Produto 2007/2008 2008/2009 2009/2010 2010/2011 2011/2012 2012/2013 2013/2014¹

White Sugar – local market 0,2399 0,3011 0,5136 0,5667 0,5892 0,4879 0,4941White Sugar – export 0,2484 0,2958 0,4085 0,4386 0,5752 0,5361 0,4834VHP Sugar – export 0,2149 0,2615 0,3433 0,3934 0,4927 0,5013 0,4292Anhydrous Ethanol fuel 0,2727 0,2982 0,3422 0,4007 0,5276 0,4472 0,4734Hydrous Ethanol fuel 0,2510 0,2652 0,3019 0,3536 0,4389 0,4165 0,4377Anhydrous Ethanol industrial 0,2794 0,3063 0,3360 0,3697 0,5144 0,4693 0,4871Hydrous Ethanol industrial 0,2551 0,2730 0,3085 0,3684 0,4462 0,4206 0,4476Anhydrous Ethanol export 0,2504 0,2841 0,2987 0,3600 0,4553 0,4741 0,4711Hydrous Ethanol ‐ export 0,2575 0,2870 0,2414 0,3096 0,3985 0,4294 0,4443Average Price per harvest year 0,2443 0,2782 0,3492 0,4022 0,5018 0,4728 0,4524Average Price ‐ Sugar Cane 0,2284 0,2785 0,3982 0,4408 0,5280 0,5027 0,4517Average Price – Sugar for Ethanol 0,2582 0,2781 0,3070 0,3663 0,4698 0,4371 0,4823

Ethanol demand trend

Bndes setorial