eu regulations impacting investment management and · pdf fileeu regulations impacting...

TRANSCRIPT

EU Regulations

Impacting Investment

Management and

Funds

IMAS Lunchtime Talk Series

Diana Quinn

29th April 2015

© 2015 KPMG Services Pte. Ltd. (Registration No: 200003956G), a Singapore incorporated company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. Printed in Singapore.

1

Agenda

Investment Management Horizon Scanning

• Regulatory Themes

• The EU Regulatory Pipeline

2015/2016 Key EU regulations for Singapore firms

• MiFID II

• AIFMD

• EMIR

• UCITS

The SIFI debate

© 2015 KPMG Services Pte. Ltd. (Registration No: 200003956G), a Singapore incorporated company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. Printed in Singapore.

2

Horizon Scanning: The investment management canvas

KPMG performs continuous scanning and analysis of the global, regional and national regulatory

horizon, identifying drivers and themes, and potential impacts on firms, markets and clients.

Insurance

Funds Pension

Funds

Other

Institutions

HNW &

Charities

Distributors

Fund

Accounting

Fund Admin

Depositary

Payment

Systems

CustodySettlement

& Clearing

Dealing

Admin

Trading

Venues

Brokers

Data Vendors

Index

Providers

Listing

Authority

Financial

Reporting

Credit Ratings

Banks

Segregated Mandates

Issuers

Investment Funds

Capital Markets

Market Infrastructure

Investment & Fund

Management

Risk governance

Data and reporting

Conduct

Structural market change

Remuneration

Culture

Growing coherence & co-operation

The industry has entered in a new era of regulatory clarity, although its growing stature

in the global economy will drag it further under the regulatory spotlight. There are some key areas

where regulation and other pressures are forcing asset managers to make significant changes.

© 2015 KPMG Services Pte. Ltd. (Registration No: 200003956G), a Singapore incorporated company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. Printed in Singapore.

3

Theme Singapore EU

Remuneration/

Costs & Charges

Transparency

Risk Management

TCF / Conduct

AML / ABC

Market Abuse

Regulatory themes: Singapore & EU

Source

AIFMD MiFID II

AMLD

MAD II

AIFMD MiFID II CRD IV

MMF,

EuSEF,

EuVECA,

ELTIF

MiFID II /

MiFIR EMIR AIFMD

MiFID II UCITS V AIFMD CRD IV PRIIP KID /

UCITS KIID

MMF,

EuSEF,

EuVECA,

ELTIF

UCITS VI

UCITS VI

KYC & AML

Short selling

disclosure

ASEAN CIS

Conflicts of

Interest

Conflicts of

Interest

Conflicts of

Interest

RMF/ RBC2

Licensing &

Conduct of

Business

© 2015 KPMG Services Pte. Ltd. (Registration No: 200003956G), a Singapore incorporated company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. Printed in Singapore.

4

EU regulation pipeline

IM Firms/IM services Key points 2014 2015 2016<

CRD IV

• EU Basel 3 rules

• Bonus cap

• Leverage and liquidity

ratios

• Limited national

discretions

MiFID II / MiFIR

• Market structure

• Transparency

requirements

• Investor protection

• Third Countries

AMLD II • Additional requirements re

terrorist funding

Shareholder Rights

Directive

• Additional disclosures for

listed firms & AIFs, and for

IMs

Key: RTS/ITS – Regulatory/Implementing Technical Standard; DA – Delegated Act

Insurance clients &

distribution Key points 2014 2015 2016<

Solvency II • Risk based capital

• Governance

• Reporting

IMD II • Increased disclosure

• Ban on commission

IORPD II • Improved governance

• Increased transparency

• Cross border

Intended as high-level summary and not a comprehensive listing

FINREP reporting

begins (Sept)

COREP reporting

begins (Jan)

Leverage ratio

(2018)

Liquidity ratio

(2018)

Adopted (March) Draft RTS and Guidelines Implementation

(Mar/Apr 2017)

RTS CVA risk own

funds (Jun)

EBA benchmark

internal models

(Apr)

EBA guidelines on

governance/ suitability of

management (Dec)

RTS regulatory

capital (Dec)

RTS liquidity risk

(Jan)

Final technical

requirements

Implementation

(2016)

In trialogue

Final advice to EC on

Das (Dec)

Draft RTS / ITS (Dec)

Implementation

(Jan 2017)

Under negotiation

Implementation

(2016 -

unlikely)

Final DAs (June) Final RTS / ITS

(Dec)

Under negotiation

Implementation

(Dec 2016 -

unlikely)

Implementation

(2017)

Draft RTS / ITS

(Feb)

© 2015 KPMG Services Pte. Ltd. (Registration No: 200003956G), a Singapore incorporated company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. Printed in Singapore.

5

EU regulation pipeline cont.

Capital Markets &

infrastructure Key points 2014 2015 2016<

EMIR • Clearing

• Reporting

• Risk mitigation

MAD II / MAR • Tougher requirements

• Additional sanctions

Benchmarks

Regulation

• Technical standards and

interoperability

• Cap interchange fees

Central Securities

Depositories

• Timing and conduct of

securities settlement

FTT • 11 Euro-zone countries

• UK legal challenge

Non-Bank/CCP

Resolution • Treatment of client assets

Securitisations

New proposal under “CMU”

Prospectus

Directive Review New proposal under “CMU”

Covered Bonds

Regulation New proposal under “CMU”

Consultation Document

Consultation Document

Consultation Document

NOTE: in addition to new requirements directly applicable to IMs, MiFID II & MiFIR also herald significant changes to e.g. trading

venues, which the front and back offices of IMs will need to monitor and navigate

Clearing obligation in

force (Dec)

Under negotiation

Draft rules Implementation

(July 2016)

Implementation (July) Final requirements

Implementation

(2017)

Final Advice on DAs and

RTSs

Book-keeping

Implementation

(2023/25)

Proposal expected Q3

Negotiations

on-going

Implementation

(2016 - unlikely)

Proposal expected Q3

Proposal expected Q3

Implementation of

T+2 (Jan 2015)

Proposal expected Q3

Intended as high-level summary and not a comprehensive listing

© 2015 KPMG Services Pte. Ltd. (Registration No: 200003956G), a Singapore incorporated company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. Printed in Singapore.

6

EU regulation pipeline cont.

Funds & Fund

Managers Key points 2014 2015 2016<

AIFMD

• Investor protection

• Transparency

• Regulatory capital

UCITS V

• Depositaries

• Manager Remuneration

• Sanctions

“UCITS VI”

Likely topics:

• Eligible investment

strategies

• Performance fees

• MiFID II alignment

issues

PRIIP KID

• Key Information

Document

• Investor protection

EuSEFs/EuVECAs

ELTIFs

• Limited assets

• Restricted access

Money Market Funds

• Severe restrictions for

CNAVs

• Liquidity requirements

• Credit quality

Intended as high-level summary and not a comprehensive listing

ESMA report on functioning of EU AIF/AIFM passports and on application of passports to

non-EU AIF/AIFM (July)

Draft RTS / DA drafting In force from Q4 (optional regime)

Likely termination of national private placement regimes

(2018)

Trialogue to begin

Implementation (July 2013)

Final Advice to EC on DAs

Implementation (Mar 2016)

Implementation (Dec 2016)

Draft DA / RTS / ITS

In force from 2013 (optional regimes)

Final Advice to EC on DAs & draft ITS

Under construction

ESAs Consultation 2nd Consultation

Under CMU: encourage

take-up

MiFID II / MiFIR

© 2015 KPMG Services Pte. Ltd. (Registration No: 200003956G), a Singapore incorporated company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. Printed in Singapore.

8

Overview of MiFID II

MiFID II is the long awaited update to the existing MiFID framework aimed at improving

transparency and reducing risk in the financial markets. It is comprised of:

• MiFIR: A regulation addressing issues related to transparency and market infrastructure

• MiFID II: A directive addressing issues related to business conduct

MiFID II combined with EMIR completes the European response to the G20 commitment made in

Pittsburgh in 2009 to manage the risks associated with OTC derivatives trades

What is MiFID II?

MiFID II/

MiFIR

Transparency

Market Infrastructure, Trading and

Clearing

Governance

Transaction Reporting

Authorisation, Branches and

Passporting

Data Publication and Access

Investor Protection

Micro- structural

Issues

Commodity Derivatives

© 2015 KPMG Services Pte. Ltd. (Registration No: 200003956G), a Singapore incorporated company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. Printed in Singapore.

9

MiFID II: Key themes and business impact

Market structure and

transparency requirements

could lead to fragmentation of

liquidity and increased cost

Commodity markets – position

limits will apply but the

methodology has yet to be

worked out

The market structure changes

are likely to introduce greater

complexity for managers in terms

of data points and feeds

High Frequency Trading

definition proposed by ESMA

will have a much wider

impact than was originally

envisaged

Systems and processes will need

to be adjusted for both MiFID II

and MAD, including trade and

transaction reporting

Consolidated tape provisions

could deter some investment

banks from making quotes, driving

liquidity away from the market

Limitations on dark pools may

reduce ability to transact large

trades without suffering large

market impact costs

Reporting requirements are

Numerous – could cause

Duplication with each other and

With other Directives e.g. EMIR

Disclosure of cost requirements

means that vertically integrated

firms will need to make more of a

separation between costs

The intention of the Directive is

that the client facing firm

must aggregate the cost of

the product and provide a £/%

amount

Firms will need to identify and

disclose conflicts of interest in

sufficient detail to enable

the client to make an informed

decision

Revised best execution

provisions will require firms to

annually publish their top five

trading venues and repapering of

client agreements may be needed

Many Member States are already

intervening around products,

but the Directive will enhance the

focus on this

There is likely to be further debate

around the respective

responsibilities of the product

manufacturer and the distributor

Tightening of execution only

regime through narrower

definition of non complex

products

Ban on inducements will require

managers to consider their

processes and their

adherence to the requirements

Market structure Investor

protection

Transparency Disclosure

MiFID II

© 2015 KPMG Services Pte. Ltd. (Registration No: 200003956G), a Singapore incorporated company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. Printed in Singapore.

10

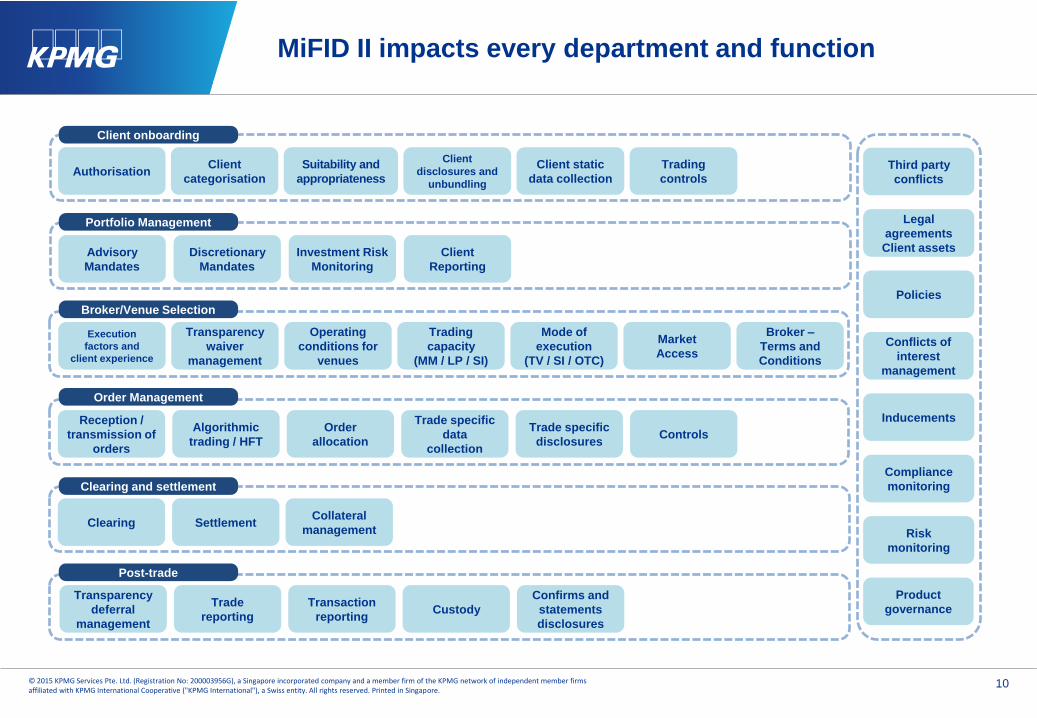

MiFID II impacts every department and function

Clearing Settlement Collateral

management

Transparency

deferral

management

Trade

reporting

Transaction

reporting Custody

Confirms and

statements

disclosures

Authorisation Client

categorisation

Suitability and

appropriateness

Client

disclosures and

unbundling

Client static

data collection

Trading

controls

Advisory

Mandates

Discretionary

Mandates

Investment Risk

Monitoring

Client

Reporting

Client onboarding

Broker/Venue Selection

Order Management

Clearing and settlement

Post-trade

Portfolio Management

Reception /

transmission of

orders

Algorithmic

trading / HFT

Trade specific

data

collection

Trade specific

disclosures

Order

allocation Controls

Third party

conflicts

Legal

agreements

Client assets

Risk

monitoring

Policies

Compliance

monitoring

Product

governance

Conflicts of

interest

management

Inducements

Execution

factors and

client experience

Transparency

waiver

management

Trading

capacity

(MM / LP / SI)

Mode of

execution

(TV / SI / OTC)

Operating

conditions for

venues

Market

Access

Broker –

Terms and

Conditions

© 2015 KPMG Services Pte. Ltd. (Registration No: 200003956G), a Singapore incorporated company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. Printed in Singapore.

11

MiFID II: Estimated timeline

Apr 2014

Plenary vote to

adopt MiFID II

12 Jun 2014 published

in OJ

1 Aug 2014

CP & DP close

19 Dec 2014

Advice on Delegated

Acts

Jun 2015

‘Final’ RTS

Dec 2015

‘Final’ ITS

Jun 2016

Transposition into national

law of member states

Jan 2017

Implementation

2014 2015 2016 2017 Q2 Q3 Q4 Q2 Q3 Q4 Q2 Q3 Q4 Q2

22 May 2014

ESMA publish DP & CP

Implementation timeline Estimated dates Parliamentary approval

3 Jul 2015

Draft Technical Standards

submitted by ESMA on various

matters

3 Jan 2016

ESMA guidelines on management

body, client knowledge and

competence, transaction reporting to

competent authorities

19 Feb 2014

Final texts published for

national consideration YOU

ARE

HERE

© 2015 KPMG Services Pte. Ltd. (Registration No: 200003956G), a Singapore incorporated company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. Printed in Singapore.

12

Challenges

Market Impact / Trading venues / Trading

• Identify all markets & platforms you trade on

• Existing counterparties services

• Governance & controls requirements

• Trade placement strategy

• Third country firms accessibility to retail clients

• Overlap with AIFMD and EMIR

• More onerous conditions for establishing branches

and subsidiaries in EU

• Outsourcing and delegation

Data Collection and Reporting

• Identify all products

• Data retention capabilities for 5 years

• Transaction reporting

• Static data and referential data

• Repapering of clients

• Best execution requirements

• Complex products for retail clients

• Distribution arrangements and new product manufacturing

Investor Protection Third Country Access & Passporting

Some key considerations

Commissions Non-monetary benefits

Independent advice Prohibited Generally

prohibited

Minor non-monetary benefits are permissible under

certain circumstances

Portfolio management Prohibited Generally

prohibited

Minor non-monetary benefits are permissible under certain

circumstances

Non-independent advice (and

other investment services)

Member States can impose

stricter requirements

Generally prohibited– only permissible if designed to enhance the quality of the

relevant service to the client

Eg UK, Netherlands, Belgium: Prohibited for retail clients

Generally prohibited– only permissible if designed to enhance the quality of the relevant service to the client

Eg UK: Review of hospitaltity & distributor training led to stricter guidance

on what is permissible

AIFMD

© 2015 KPMG Services Pte. Ltd. (Registration No: 200003956G), a Singapore incorporated company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. Printed in Singapore.

14

Overview of AIFMD

• AIFMD stands for Alternative Investment Fund Managers Directive

• European Commission proposed the AIFMD in April 2009 as a response to the financial

crisis and it entered into force in July 2011 with a two year transposition deadline

• Alternative Investment Fund Managers (AIFM) will have to apply for authorisation in

order to manage an Alternative Investment Fund (AIF), if the amount of assets under

management exceeds certain thresholds (€ 500 million unleveraged / € 100 million

leveraged)

• Authorised EU-AIFM managing/marketing EU-AIF will in return be provided with two

passports enabling them to offer their management services (Management Passport)

and market their AIF throughout the EU (Marketing Passport)

What is the AIFMD?

© 2015 KPMG Services Pte. Ltd. (Registration No: 200003956G), a Singapore incorporated company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. Printed in Singapore.

15

Overview of AIFMD cont.

• Any Undertaking for Collective Investment (UCI) other than UCITS which raises capital

from a number of investors with a view to investing it in accordance with a defined

investment policy for the benefit of those investors

• Legal person whose regular business is managing one or more AIFs

• An entity performing either portfolio management and/or risk management is

‘managing an AIF’ and must seek authorisation as AIFM

• In addition, an AIFM may also perform other functions such as administration, marketing

or activities related to the assets of AIF

• UCITS management companies can obtain an additional AIFM licence

• External AIFM = legal person appointed by or on behalf of the AIF

• Self-managed AIFM = where the corporate legal form allows it

What is an AIF?

Who is the AIFM?

Which types of AIFMs exist?

© 2015 KPMG Services Pte. Ltd. (Registration No: 200003956G), a Singapore incorporated company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. Printed in Singapore.

16

AIFMD

• Markets and instruments

• Illiquid assets, actual

riskprofile and risk

management tools

• Results of stress tests

• Leverage

• Systemic risk information

• Cash flow monitoring

• Monitoring role and custody

• Liability

• Externally managed:

EUR 125.000

when more than EUR 250 mln

AUM, 0,02% over this, capped

on EUR 10 mln

• Objective reasons

• No letterbox entity

• Co-operation agreement

• Monitoring role manager

• Functionally and

hierarchically separate

• Due diligence investments

• Limits on leverage

• Stress tests

• Includes senior staff incl.

senior management, portfolio

manager and functions with

an impact on risk profile

• Multi year framework, and

variable elements, at least

40% deferred over 3 to 5 yrs

• Policy: adjustment needed to

included further disclosure

on Preferential treatment

• Extension of scope

• Guarantees for independent

valuation

• Functionally independent

from portfolio management

Remuneration

Conflict

of interest

Risk and

Liquidity

management

Valuation

Depositary

Transparency

Capital

requirements

Delegation

AIFMD: Key themes and business impact

© 2015 KPMG Services Pte. Ltd. (Registration No: 200003956G), a Singapore incorporated company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. Printed in Singapore.

17

July

2011

Sept

2011

July

2013

Jan

2019

July

2014

July

2015

Oct

2015

Jul

2017

Nov

2011

2012

Transparency Reporting is

effective for ALL impacted

firms, including Non-EU Firms

Strategic analysis >> >> Implementation >>>>> Authorization and ongoing compliance

YOU

ARE

HERE

Publication in the

Official Journal

(1 July 2011)

Entry into Force

(21 July 2011)

ESMA technical advice on

Delegated Acts (Level II)

Deadline for

authorisation of

existing AIFMs

EU passport may be

made available for

non-EU AIFMs and

non-EU AIFs

Possible withdrawal

of national PPRs on

ESMA’s advice

Deadlines for

responses on ESMA

consultations

AIFMD draft law was

deposited in Luxembourg

Parliament

Passport

introduction

for EU AIFMs

managing

EU AIFs

ESMA opinion on the

passport regime for

non-EU funds and

managers

Deadline for

transposition

into EU

national laws

EU Commission

published Delegated

Regulation

(May 2013)

Q4

2013

Oct

2018

Review of the

Directive by the EU

Commission and

possible start of

AIFMD II

ESMA advice on the

functioning of the

passport and whether

to turn off NPPRs

AIFMD: Estimated timeline

© 2015 KPMG Services Pte. Ltd. (Registration No: 200003956G), a Singapore incorporated company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. Printed in Singapore.

18

Private Placement

(subject to additional AIFMD

requirements)

AIFMD - Marketing Passport

+ Private Placement

AIFMD - Marketing Passport

+ Private Placement ???

AIFMD - Management Passport

+ Delegation arrangements

Delegation arrangements

(subject to AIFMD requirements)

AIFMD - Management Passport

+ Delegation arrangements

Routes

Non-EU Managers

Marketing AIF in the EU Managing EU AIF

From 2015

From 2013

From 2018

Non-EU Managers: Routes to access the EU market

© 2015 KPMG Services Pte. Ltd. (Registration No: 200003956G), a Singapore incorporated company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. Printed in Singapore.

19

What is marketing ?

‘Marketing‘ in accordance with Article 4 of the AIFMD means:

• direct or indirect offering or placement

• at the initiative of the AIFM or on behalf of the AIFM

• of units or shares of an AIF it manages

• to (professional) investors domiciled or with a registered office in the Union

NOT covered:

• Passive marketing

• Marketing to retail investors

Non-EU Managers: Marketing definition

National Law

AIFMD

© 2015 KPMG Services Pte. Ltd. (Registration No: 200003956G), a Singapore incorporated company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. Printed in Singapore.

20

Non-EU Managers: Marketing Private Placement

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022...

Option 1:

AIFMD-Passport

Option 2:

Private Placement

© 2015 KPMG Services Pte. Ltd. (Registration No: 200003956G), a Singapore incorporated company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. Printed in Singapore.

21

Non-EU Managers: Marketing Private Placement cont.

Dual AIF marketing regime in the EU: Private Placement & AIFMD Passport

AIFMD Passport

Private

Placement

Regimes

AIF private placement allowed, but in some cases strict local requirements will apply (e.g. France and Germany). AIF private placement not yet possible (e.g. Croatia, Greece, Latvia and Poland). More clarification needed whether the private placement allowed (e.g. Spain).

EMIR

© 2015 KPMG Services Pte. Ltd. (Registration No: 200003956G), a Singapore incorporated company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. Printed in Singapore.

23

Overview of EMIR

• EMIR stands for European Markets Infrastructure Regulation

• European legislation aimed at increasing stability and enhancing transparency of the

OTC derivatives market.

What is the EMIR?

High levels of counterparty risk in

OTC derivatives market space.

Low transparency on OTC derivatives

trading and exposures.

Expansive volumes in OTC derivatives

market.

Asymmetric valuations of OTC

derivatives across counterparties.

Need for Structural reforms (based on

collateralisation) aimed at creating a

structured and responsible OTC derivatives

market.

Growing consensus among G20 countries

about the need for more transparency in the

financial system. (EMIR is just the start...)

Need to closely regulate the growing OTC

derivatives market due to its emerging

systemic importance.

Growing consensus among regulators and

stakeholders for fair and accurate valuation of

derivative positions across the industry.

Why EMIR?

© 2015 KPMG Services Pte. Ltd. (Registration No: 200003956G), a Singapore incorporated company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. Printed in Singapore.

24

EMIR: Key themes and business impacts

• Fund Managers;

• Asset Managers;

• Hedge Funds;

• Investment Banks;

• Brokers;

• Commodities Firms (Trading Arms);

• Clearers;

• Custodians;

• Corporates (NFCs – specific timelines coming).

Who does it affect

• Central clearing of all standardised OTC derivative contracts.

• Collateralisation of all OTC derivative contracts.

• Individual and omnibus segregation of client money.

• Enhanced risk mitigation techniques for non-centrally cleared

OTC derivatives including:

– Daily valuations. (Mark-to – market, mark-to-model)

– Timely Confirmation requirements.

– Dispute resolution

• Daily trade and position reporting of all derivative contracts to

trade repositories.

What does it mean?

© 2015 KPMG Services Pte. Ltd. (Registration No: 200003956G), a Singapore incorporated company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. Printed in Singapore.

25

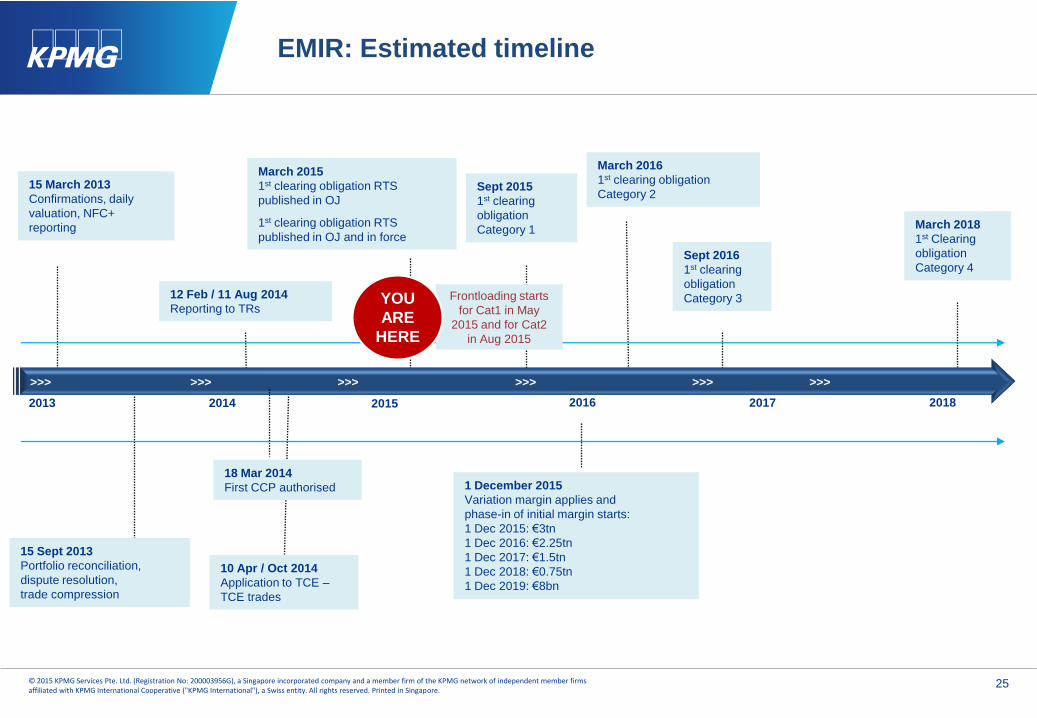

EMIR: Estimated timeline

2013 2015 2018

15 March 2013

Confirmations, daily

valuation, NFC+

reporting

1 December 2015

Variation margin applies and

phase-in of initial margin starts:

1 Dec 2015: €3tn

1 Dec 2016: €2.25tn

1 Dec 2017: €1.5tn

1 Dec 2018: €0.75tn

1 Dec 2019: €8bn

March 2016

1st clearing obligation

Category 2

2017

Sept 2016

1st clearing

obligation

Category 3 12 Feb / 11 Aug 2014

Reporting to TRs

March 2018

1st Clearing

obligation

Category 4

2014

15 Sept 2013

Portfolio reconciliation,

dispute resolution,

trade compression

>>> >>> >>> >>> >>> >>>

18 Mar 2014

First CCP authorised

2016

March 2015

1st clearing obligation RTS

published in OJ

1st clearing obligation RTS

published in OJ and in force

Sept 2015

1st clearing

obligation

Category 1

10 Apr / Oct 2014

Application to TCE –

TCE trades

Frontloading starts

for Cat1 in May

2015 and for Cat2

in Aug 2015

YOU

ARE

HERE

© 2015 KPMG Services Pte. Ltd. (Registration No: 200003956G), a Singapore incorporated company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. Printed in Singapore.

26

Central Clearing: SFA vs EMIR

Timing

Entity reqs

Scope

Collateral

Intra group

Extra

territoriality

Reporting

Non-financials

Singapore’s Securities and Futures Act (SFA) EU’s EMIR

SFA was amended in 2012 to implement OTC derivatives reforms in relation

to reporting and clearing of OTC derivatives transactions and the regulation of

OTC derivatives trade repositories and clearing facilities

A corporation seeking to operate a clearing facility in Singapore must be either

an “approved clearing house” or a “recognised clearing house” (RCH)

Derivative contracts encompass commodities, credit, equities, foreign exchange

and interest rates

Any money, letter of credit, banker’s draft, certified cheque, guarantee or other

similar instrument; any securities; any futures contract, derivatives contract or

other similar financial contract, arrangement or transaction; or any other asset of

value acceptable to an approved clearing house or a recognised clearing house

Intra-group transactions are exempt from the clearing mandate (but subject to

collateralisation requirements)

Overseas clearing facilities are required to comply with the SFA and seek

authorisation under the SFA regime as overseas RCHs if their acts are treated

as carried out in Singapore for the purposes of section 339 SFA

A party subject to the reporting mandate is required to report OTC derivatives

contract to an eligible Trade Repository (TR) within one business day of the

contract being entered into or amended if the contract relates to any product

that is required to be reported and the contract is booked / traded in Singapore

Hedging transactions by non-financial entities will be excluded from

derivative exposure when determining whether non-financial entities

have exceeded the threshold

EMIR came into force on 16 August 2012, although the

clearing requirements have not yet taken effect

Potential for duplicated entity requirements

Excludes listed derivatives but currently includes FX forwards

Wider definition to include Cash, Gov Securities, gold, high

quality corp bonds, equities

Excluded from clearing requirements and uncleared

potentially excluded from collateral requirements

Awaiting detail on extra territorial application

Extensive data set. Reporting by EOD following working day.

Confirmations EOD

Trades for commercial hedging exempt

UCITS

© 2015 KPMG Services Pte. Ltd. (Registration No: 200003956G), a Singapore incorporated company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. Printed in Singapore.

28

UCITS Regulation: constant evolution

The big question:

Will the UCITS depositary be able to be in the same group as the Management Company?

ESMA consultation seeking to align national

regulatory approaches

Interest rate hedged share classes will not be

allowed (they must be separate sub-funds)

Share Classes vs Sub-funds

A growing contents list:

• MiFID rules applied to ManCos (and AIFMs)

• Tightening of eligible investment strategies

• Costs disclosure & Performance Fees

“UCITS VI”

UCITS V – depositaries, manager

remuneration & sanctions

NBNI G-SIFIs

© 2015 KPMG Services Pte. Ltd. (Registration No: 200003956G), a Singapore incorporated company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. Printed in Singapore.

30

Non-Bank Non-Insurer Global Systemically Important

Financial Institutions

NBNI G-SIFIs: the longest acronym? Could include both IMs and individual Funds

IOSCO Consultation Paper, January 2014:

“….to identify NBNI financial entities whose distress or disorderly failure, because of their size, complexity and systemic interconnectedness, would cause

significant disruption to the global financial system and economic activity across jurisdictions”

“…an indicator-based measurement approach where multiple indicators are selected to reflect the different aspects of what generates negative externalities and

makes the distress or disorderly failure of a financial entity critical for the stability of the financial system”

Impact Factors The indicators used will be tailored to specific sector/entity

types

Size: The importance of a single entity for the stability of the

financial system generally increases with the scale of financial

activity that the entity undertakes.

Complexity: The systemic impact of a financial entity’s distress

or failure is expected to be positively related to its overall

complexity, i.e. its business, structural and operational

complexity. That is, in principle, the more complex a financial

entity, the more difficult, costly and time-consuming it will be to

resolve the failing institution.

Interconnectedness: Systemic risk can arise through direct and

indirect inter-linkages between entities within the financial

system so that individual failure or distress can have

repercussions throughout the financial system.

.

Substitutability: The systemic importance of a single financial

entity increases in cases where it is difficult for other entities in

the system to provide the same or similar services in a

particular business line or segment in the global market in the

event of a failure.

Global activities (cross-jurisdictional activities): The global

impact from a financial entity’s distress or failure should vary in

line with its share of cross-border assets and liabilities. The

greater the global reach of a financial entity, the more

widespread the spill-over effects from its failure.

© 2015 KPMG Services Pte. Ltd. (Registration No: 200003956G), a Singapore incorporated company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. Printed in Singapore.

31

NBNI G-SIFIs: the latest vibes

• The FSB plenary has recently approved a second consultation draft. Another consultation document will be published around end-2014 with a 90-day consultation

period. Specifically, the industry will be asked for types of activities that would be considered systemically important if conducted by IMs. Leverage will be of

particular importance.

• The FSB and IOSCO aim to finalise the assessment methodology in 2015 (Phase 1). In phase 2, they will elaborate on the implications of being identified as SIFI

(i.e. policy measures). Potential policy measures will be subject to public consultation and will be different from those applied to banks or insurance companies. In

phase 3, the individual countries will finally conduct the analysis and identify NBNI G-SIFIs.

• The possibility of ending with a null set was confirmed.

Comments at EFAMA’s Annual Forum, November 2014

Comments at IIF Annual membership Meeting, November 2014

The discussion has moved focus from

individual institutions to IM activities. This

is correct because IMs are not balance

sheet businesses. Size has different a

connotation in IM than in banking. Instead,

leverage, stock lending, repos etc. are the

important considerations

(ESMA)

IMs are intermediaries; banks are

principals. If IMs are SI, in what

way? Policy-makers are only just

beginning to get their heads around

this question

(Central Bank of Ireland)

This is increasing

understanding within the

FSB that IM is different

(Commission)

The discussion started from “too big to fail”

questions but now is about entities whose

failure could cause a systemic impact in

the market. Therefore, we have to look at

entities (the “FIs” in “SIFIs”) whose size or

nature make them SI

(IOSCO)

© 2015 KPMG Services Pte. Ltd. (Registration No: 200003956G), a Singapore incorporated company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. Printed in Singapore.

32

FSB/IOSCO 2nd Consultation Paper on NBNI G-SIFIs

• Extract from FS Regulatory CoE Blog, 5 March

• This second consultation paper is marginally better than the January 2014 paper in discussing what might make these types of firm systemically

important. However, it does not really pick up on, or develop, the arguments around the potential systemic importance of … investment funds, as put

forward most recently by Mark Carney and the IMF. It reads like it is stuck in a time warp from three years ago.

• Even where potential sources of systemic importance are identified (not always convincingly), the proposed metrics are not always closely related to

them. For example, … for investment funds, only the size metric – out of a long list of metrics - really picks up on the “fire sale of assets” source of systemic

importance, and even then only imperfectly (because the key issue here is size relative to the depth of the market(s) in which the fund is investing).

1. Balance sheet of $100bn or more; or

2. AuM of $1trn or more

Investment

Managers

1. $30bn NAV and leverage of 3x NAV, plus any over $100bn NAV; or

2. Over $200bn gross assets, unless can demonstrate that not dominant

player in its market

Investment

Funds

Appendix

Detailed MiFID II Information

© 2015 KPMG Services Pte. Ltd. (Registration No: 200003956G), a Singapore incorporated company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. Printed in Singapore.

34

MiFID II: Definitions

Retail and elective professional clients (Annex II, Section II of MiFID II)

Retail clients may be treated as professionals on request. This will result in

waiving some of the protections afforded by the conduct of business rules.

An investment firm may opt a client up only if it has assessed the client’s

expertise and knowledge and is satisfied that the client is capable of making its

own investment decisions and understanding the risks involved regarding the

types of transactions and services envisaged.

During this assessment, the firm must be satisfied that at least two of the

following criteria are satisfied:

• the client must have carried out transactions, in significant size, on the

relevant market at an average frequency of 10 per quarter over the

previous four quarters;

• the size of the client’s securities portfolio (including cash deposits and

financial instruments) exceeds €500,000;

• the client works or has worked in the financial sector for at least one year in

a professional position, which requires knowledge of the transactions or

services envisaged.

Professional client

A client who possesses the experience, knowledge and expertise to make its

own investment decisions and properly assess the risks that it incurs.

Examples

• Entities which are required to be authorised or regulated to operate in the

financial markets:

(a) Credit institutions;

(b) Investment firms;

(c) Other authorised or regulated financial institutions;

(d) Insurance companies;

(e) Collective investment schemes and management companies of such

schemes;

(f) Pension funds and management companies of such funds;

(g) Commodity and commodity derivatives dealers;

(h) Locals; and

(i) Other institutional investors.

• Large undertakings (subject to size requirements)

• International organisation (e.g. ECB and IMF)

MiFID II brings changes to client categorisation and now local public authorities

and municipalities can no longer be treated as professional clients or eligible

counterparties by default.

Professional clients (Annex II, Section I of MiFID II)

© 2015 KPMG Services Pte. Ltd. (Registration No: 200003956G), a Singapore incorporated company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. Printed in Singapore.

35

MiFID II: third country provisions

The term “third country” refers to jurisdictions outside the EU and “third country

firms” refers to entities incorporated outside the EU.

Access to regulated markets (Article 36 MiFID II)

Third country firms may seek to do business by way of:

(i) a branch established in the EU, or

(ii) on a cross-border basis, that is providing services to persons in one

jurisdiction from a place of business in another jurisdiction without any

establishment in the client's jurisdiction.

Access through establishment of an EU branch (Art. 39 MiFID II)

Member States may require that firms intending to provide investment services

to retail clients and elective professional clients on their territories establish

branches in those Member States. Various conditions will need to be met for the

establishment of a branch, including the existence of appropriate co-operation

arrangements between the two countries.

Where a Member State implements MiFID II to require the establishment of

branches, a third country firm that has not established a branch in that Member

State will not be able to provide investment services to retail clients or elective

professional clients.

Where a Member State does not implement that requirement, the provision of

services to retail clients and elective professional clients will be subject to its

national laws, rather than the provisions of MiFID II.

Passporting

Once a third country firm has established an authorised branch in an EU

Member State (if required to do so to access retail clients) and that firm is

established in a country whose legal and supervisory framework is recognised

as broadly equivalent by the EU Commission, the firm will be permitted to

provide its investment services and to perform activities throughout the EU to

eligible counterparties and professional clients without the need to establish

further branches. This is called ‘Passporting’.

The branch would need to comply with the information requirements for the

cross-border provision of services and activities under Art. 34 of MiFID II. In

these circumstances, there is no requirement for the branch to register with

ESMA as a permitted third country firm. Also, none of the restrictions would

prevent a third country firm from providing its services at the ‘own exclusive

initiative’ of the prospective client (Art. 42 MiFID II).

Retail and elective professional clients

Professional clients and eligible counterparties

Access from outside the EU (Art. 46 MiFIR)

A third country firm is permitted to provide investment services or perform

activities directly to eligible counterparties and to those categories of clients

considered to be professionals in the EU without the requirement to establish an

EU branch provided the EU Commission has first determined that the third

country‘s legal and supervisory regime is broadly equivalent to the EU’s in

certain respects.

A firm based in a third country deemed equivalent will need to apply to the

European Securities and Markets Authority (ESMA) to be included in a register

of permitted third country firms, and ESMA will duly register it provided that (i)

the firm is authorised to provide the relevant investment services or activities in

the jurisdiction of its head office and (ii) appropriate co-operation arrangements

are in place with the relevant third country.

Access through an EU branch (Passporting)

As an alternative to ESMA registration, third country firms can – subject to

certain conditions – provide investment advice to eligible counterparties or

professional clients in all Member States through an EU branch authorised by

the competent Member State authority (Art. 39 MiFID II).

© 2015 KPMG Services Pte. Ltd. (Registration No: 200003956G), a Singapore incorporated company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative ("KPMG International"), a Swiss entity. All rights reserved. Printed in Singapore.

36

Market Impact / Trading venues / Trading

• Can you identify all markets & platforms you trade on, including SIs, and

activity that may be defined as market making, or require you to face new

counterparty?

• Will your existing counterparties continue to provide same service i.e. desk

execution, direct market access?

• Governance & controls requirements for Trading Venues:

circuit breakers, OTR, increased fees, non-discriminate

access, direct market access

• Impact on trade placement strategy and achieving and

evidencing best execution.

• Third country firms dealing with retail clients in EU face

uncertainty over access.

• Third country equivalence assessment to be undertaken; may

duplicate EMIR equivalence assessment.

• Overlap with AIFMD timeline on EU access for third country firms.

• More onerous conditions for establishing branches and subsidiaries in EU

• Impacts on delegation and outsourcing?

Data Collection and Reporting

• Can you identify all products within your clients’ portfolios that will meet the

new MiFID definitions?

• Do you have the capacity and budget to store and retain relevant telephone

conversations and electronic communications for

five years?

• Transaction reporting – reliance on broker goes, number of fields

per transaction significantly increased. How will you build the system? Can

you source the data for all the (new) fields?

Do you have more than one data warehouse?

• More static data and referential data needed from

clients, including end-client legal identifier.

• Repaper clients for new MiFID products and services, new

suitability requirements.

• Can you meet best execution requirements on new products

under MiFID and prove the same to customers?

• Do inducements demonstrably enhance the quality of the service?

• Review product offering and assess viability of offering complex products to

retail clients given additional product governance and distribution processes.

• Review distribution arrangements and new product manufacturing to assess

areas of enhancement – MI, oversight and reporting.

Investor Protection Third Country Access & Passporting Challenges

MiFID II: Some key questions for asset managers

The information contained herein is of a general nature and is not intended to address

the circumstances of any particular individual or entity. Although we endeavour to

provide accurate and timely information, there can be no guarantee that such

information is accurate as of the date it is received or that it will continue to be accurate

in the future. No one should act upon such information without appropriate professional

advice after a thorough examination of the particular situation.

© 2015 KPMG Services Pte. Ltd. (Registration No: 200003956G), a Singapore

incorporated company and a member firm of the KPMG network of independent

member firms affiliated with KPMG International Cooperative (“KPMG International”), a

Swiss entity. All rights reserved.

Presentation by:

Diana Quinn

Director, Head of Investment Management, Financial Risk Management

Email: [email protected]

Tel: +65 6411 8443

Mob: +65 9388 3401

Other contacts

David Waller

Partner, Financial Services

Larry Sim

Partner, Financial Services Tax

Shahid Zaheer

Director, Financial Services Regulatory Compliance