european data centre landscape prepared for fact … · european data centre landscape prepared for...

TRANSCRIPT

PREPARED FOR PREPARED FOR European Data Centre Landscape

Fact or Fiction? Andrew Jay– Head of CBRE Data Centre Solutions

9th October 2014

2 CBRE DATA CENTRE SOLUTIONS

Source: CBRE Data Centre Research

AGENDA

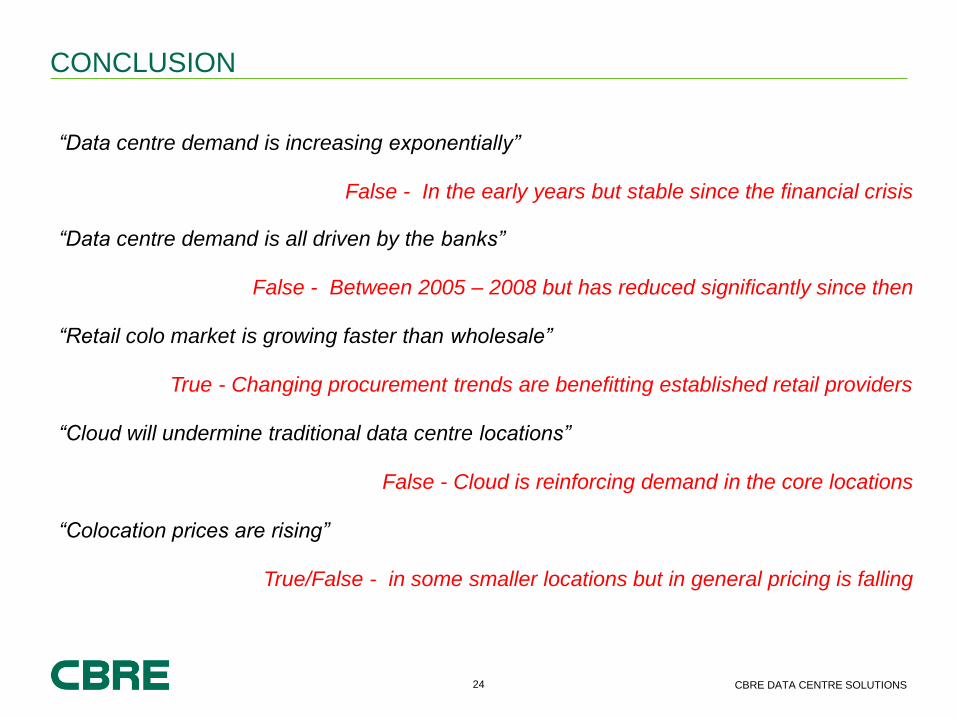

“Data centre demand is increasing exponentially”

“Data centre demand is all driven by the banks”

“Retail colo market is growing faster than wholesale”

“Cloud will undermine traditional data centre locations”

“Colocation prices are rising”

3 CBRE DATA CENTRE SOLUTIONS

Source: CBRE Data Centre Research

FACT OR FICTION?

“Data centre demand is increasing exponentially”

4 CBRE DATA CENTRE SOLUTIONS

Source: CBRE Data Centre Research

Forecast

0

10

20

30

40

50

60

70

80

90

MW

DATA CENTRE DEMAND European Colocation Take Up – Major Markets

5 CBRE DATA CENTRE SOLUTIONS

Source: CBRE Data Centre Research

EUROPEAN MARKET DEMAND

Source: Arial 9pt, Dark Grey

London Colocation Take Up Amsterdam Colocation Take Up

Paris Colocation Take Up Frankfurt Colocation Take Up

0

5

10

15

20

25

30

MW

Take Up MW Forecast

0

5

10

15

20

25

30

MW

Take Up MW Forecast

0

5

10

15

20

25

30

MW

Take Up MW Forecast

0

5

10

15

20

25

30

MW

Take Up MW Forecast

6 CBRE DATA CENTRE SOLUTIONS

Source: CBRE Data Centre Research

FACT OR FICTION?

“Data centre demand is all driven by the banks”

7 CBRE DATA CENTRE SOLUTIONS

Source: CBRE Data Centre Research

DATA CENTRE DEMAND By Sector

Cloud2% Corporate

14%

Financial19%

Technology37%

Managed Services

3%

Telecom/ISP12%

Systems Integrator

13%

2008-2010

Cloud38%

Corporate9%

Financial10%

Technology14%

Managed Services

11%

Telecom/ISP7%

Systems Integrator

11%

2011-2013

Cloud demand in 2014 currently accounts for 77% of total colocation take up!

2005-2007

Cloud1%

Corporate15%

Financial36%

Technology23%

Managed Services

3%

Telecom/ISP5%

Systems Integrator

17%

8 CBRE DATA CENTRE SOLUTIONS

Source: CBRE Data Centre Research

DATA CENTRE DEMAND Why has corporate spending slowed?

Capital Constraints

Capacity Over Procurement

Changing IT

Hybrid Outsourcing

Virtualisation Increased Processing

Power

9 CBRE DATA CENTRE SOLUTIONS

Source: CBRE Data Centre Research

FACT OR FICTION?

“Retail colo market is growing faster than wholesale”

10 CBRE DATA CENTRE SOLUTIONS

Source: CBRE Data Centre Research

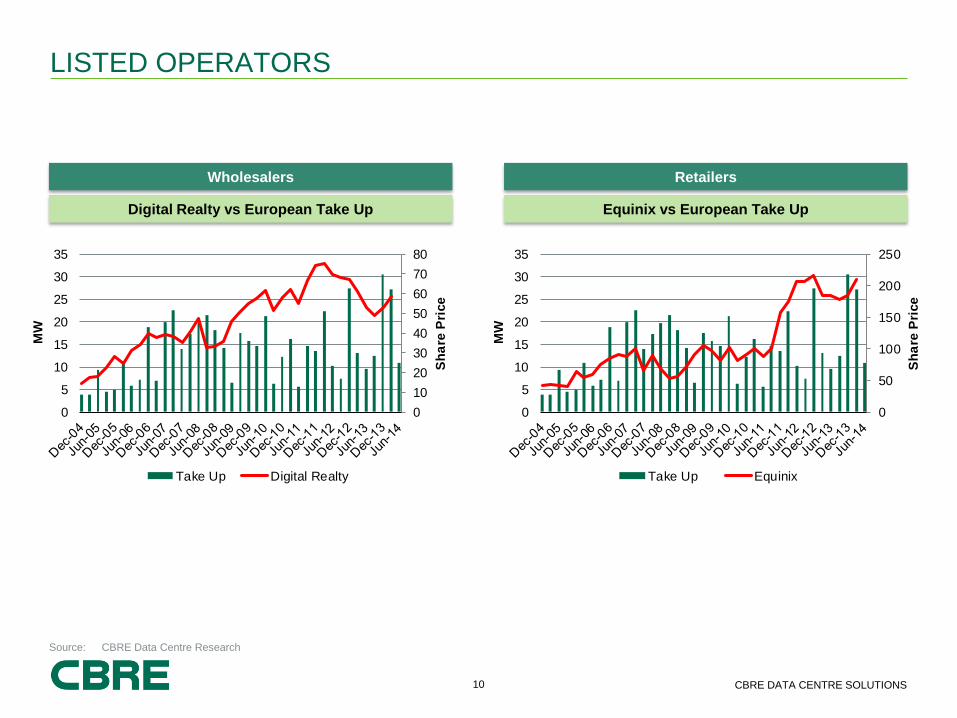

LISTED OPERATORS

Source: Arial 9pt, Dark Grey

Digital Realty vs European Take Up Equinix vs European Take Up

Wholesalers Retailers

0

10

20

30

40

50

60

70

80

0

5

10

15

20

25

30

35

Sh

are

Pri

ce

MW

Take Up Digital Realty

0

50

100

150

200

250

0

5

10

15

20

25

30

35

Sh

are

Pri

ce

MW

Take Up Equinix

11 CBRE DATA CENTRE SOLUTIONS

Source: CBRE Data Centre Research

Forecast

0

5

10

15

20

25

30

35

40

45

50M

W

Retail Wholesale

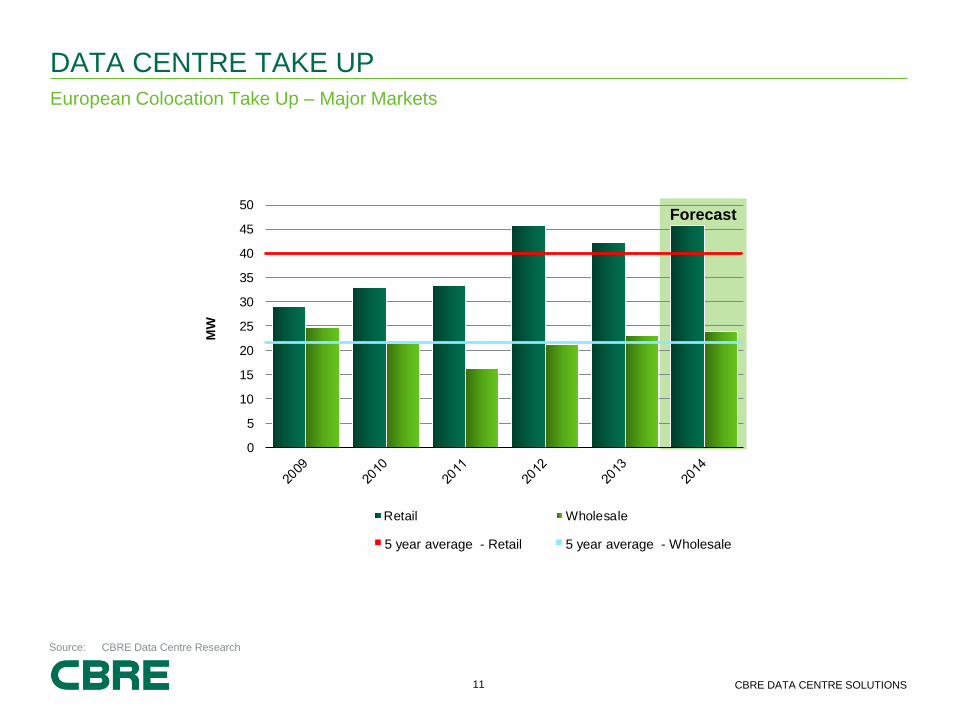

DATA CENTRE TAKE UP

Source: Arial 9pt, Dark Grey

European Colocation Take Up – Major Markets

5 year average - Retail 5 year average - Wholesale

12 CBRE DATA CENTRE SOLUTIONS

Source: CBRE Data Centre Research

-

1.0

2.0

3.0

4.0

5.0

6.0

2008 2009 2010 2012 2013 2014

Tra

nsa

cti

on

Siz

e M

W

TRANSACTION SIZE

Source: Arial 9pt, Dark Grey

Deal sizes are shrinking!

13 CBRE DATA CENTRE SOLUTIONS

Source: CBRE Data Centre Research

Forecast

0

5

10

15

20

25

30

35

40

45

50M

W

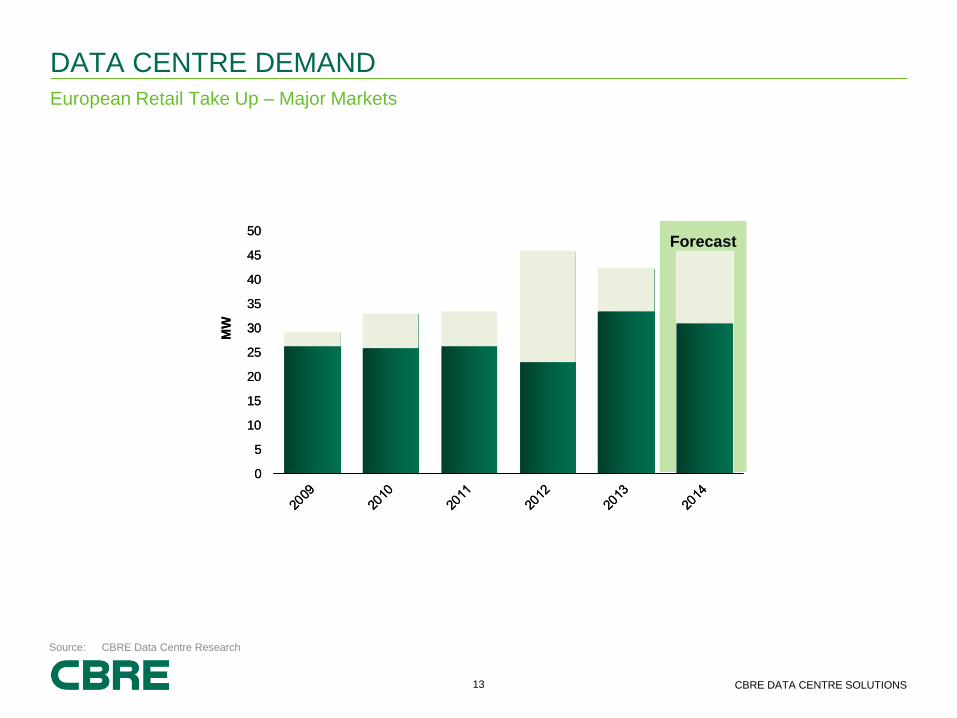

DATA CENTRE DEMAND

Source: Arial 9pt, Dark Grey

European Retail Take Up – Major Markets

0

5

10

15

20

25

30

35

40

45

50M

W

14 CBRE DATA CENTRE SOLUTIONS

Source: CBRE Data Centre Research

FACT OR FICTION?

“Cloud will undermine traditional data centre locations”

15 CBRE DATA CENTRE SOLUTIONS

Source: CBRE Data Centre Research

GLOBAL IT INFRASTRUCTURE COMPANIES

16 CBRE DATA CENTRE SOLUTIONS

Source: CBRE Data Centre Research

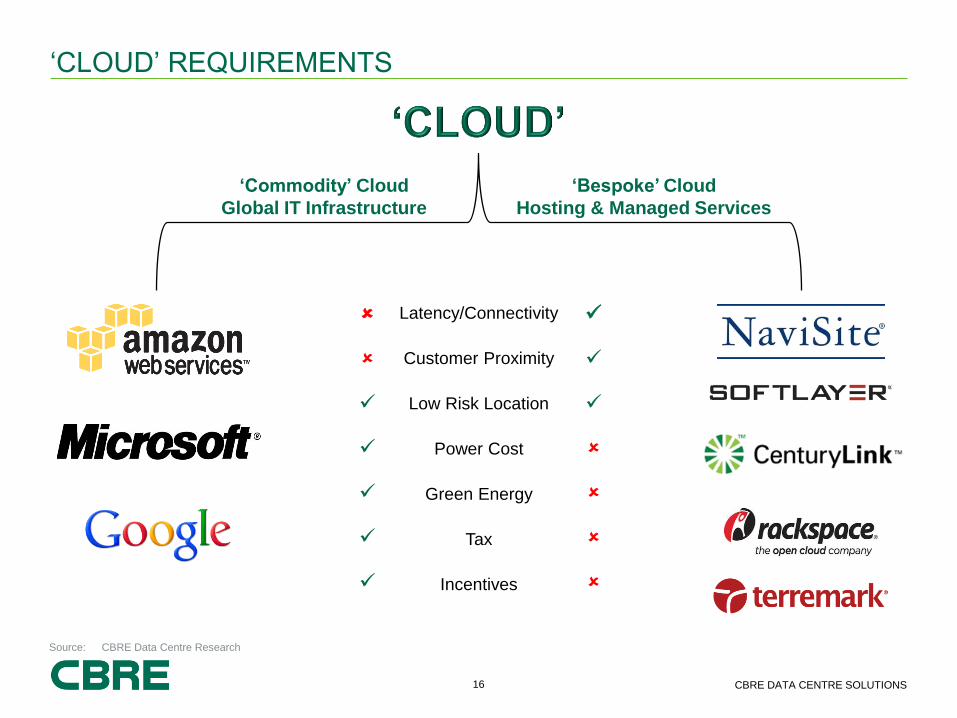

‘CLOUD’ REQUIREMENTS

Latency/Connectivity

Customer Proximity

Low Risk Location

Power Cost

Green Energy

Tax

Incentives

‘Commodity’ Cloud

Global IT Infrastructure

‘Bespoke’ Cloud

Hosting & Managed Services

17 CBRE DATA CENTRE SOLUTIONS

Source: CBRE Data Centre Research

DATA CENTRE DEMAND Total MW transacted – Major Markets

2005-2007

Cloud1

Corporate20

Financial51

Technology33

Managed Services

5

Telecom/ISP6

Systems Integrator

24

2008-2010

Cloud4 Corporate

28

Financial37

Technology70

Managed Services

5

Telecom/ISP23

Systems Integrator

24

2011-2013

Cloud74

Corporate19

Financial19

Technology27

Managed Services

22

Telecom/ISP13

Systems Integrator

21

In H1 2014 Cloud accounted for 29MW of total colocation take up!

18 CBRE DATA CENTRE SOLUTIONS

Source: CBRE Data Centre Research

EUROPE’S DATA CENTRE SUPPLY

0

Colocation Supply

(MW)

Commodity Cloud

(MW)

Colocation vs Commodity Cloud Self Build

19 CBRE DATA CENTRE SOLUTIONS

Source: CBRE Data Centre Research

FACT OR FICTION

“Colocation prices are rising”

20 CBRE DATA CENTRE SOLUTIONS

Source: CBRE Data Centre Research

EUROPEAN MARKET OVERVIEW

Source: Arial 9pt, Dark Grey

Colocation Available Supply

0

50

100

150

200

250

300

MW

Available

European Colocation – Major Markets

0

20

40

60

80

100

120

MW

Total Take Up

Colocation Demand

Forecast

21 CBRE DATA CENTRE SOLUTIONS

Source: CBRE Data Centre Research

0.0

1.0

2.0

3.0

4.0

5.0

6.0

Ab

sorp

tio

n ra

te (yrs

)

0.0

1.0

2.0

3.0

4.0

5.0

6.0

Ab

sorp

tio

n ra

te (yrs

)

London Market Absorption Amsterdam Market Absorption

Paris Market Absorption Frankfurt Market Absorption

0.0

1.0

2.0

3.0

4.0

5.0

6.0

Ab

sorp

tio

n ra

te (yrs

)

0.0

1.0

2.0

3.0

4.0

5.0

6.0

Ab

sorp

tio

n ra

te (yrs

)

0

50

100

150

200

250

300

Pri

ce– 5

00kW

(€/k

W)

0

50

100

150

200

250

300

Pri

ce– 5

00kW

(€/k

W)

0

50

100

150

200

250

300

Pri

ce– 5

00kW

(€/k

W)

0

50

100

150

200

250

300

Pri

ce– 5

00kW

(€/k

W)

EUROPEAN MARKET ABSORPTION

Source: Arial 9pt, Dark Grey

0.0

1.0

2.0

3.0

4.0

5.0

6.0

Ab

so

rpti

on

rate

(yrs

)

0

50

100

150

200

250

300

Pri

ce– 5

00kW

(€/k

W)

London

22 CBRE DATA CENTRE SOLUTIONS

Source: CBRE Data Centre Research

EUROPEAN MARKET DEMAND

Source: Arial 9pt, Dark Grey

0

50

100

150

200

250

Zurich Frankfurt

€p

er

kW

0

20

40

60

80

100

120

140

Dublin Frankfurt

€p

er

kW

Retail - Typical Pricing for 50 Kw Wholesale- Typical Pricing for 1MW

CONCLUSIONS

24 CBRE DATA CENTRE SOLUTIONS

Source: CBRE Data Centre Research

CONCLUSION

Source: Arial 9pt, Dark Grey

“Data centre demand is increasing exponentially”

“Data centre demand is all driven by the banks”

“Retail colo market is growing faster than wholesale”

“Cloud will undermine traditional data centre locations”

“Colocation prices are rising”

False - In the early years but stable since the financial crisis

False - Between 2005 – 2008 but has reduced significantly since then

True - Changing procurement trends are benefitting established retail providers

False - Cloud is reinforcing demand in the core locations

True/False - in some smaller locations but in general pricing is falling

Any Questions?