european industrial bioenergy initiative (eibi) eii 2013-2017 ip.pdf · (2) to strengthen eu...

TRANSCRIPT

1

European Industrial Bioenergy Initiative (EIBI)

Boosting the Contribution of Bioenergy to the EU Climate and Energy ambitions

Implementation Plan 2013 - 2017

Version of 24 January 2014

PREAMBLE

Since the official launch of EIBI in November 2010 a number of activities have taken place or are in the

process of implementation. So far in the scope of the EIBI a call for Expression of Interest (EoI) was

carried out which resulted in 53 submissions of potential EIBI projects of which 30 projects have

complied or nearly complied with the EIBI specifications. The results from the EIBI EoI show the huge

interest of the European Biofuels Industry in the EIBI and biofuels deployment.

Under FP7, the ERA-NET+ instrument pooling EU and MS funding has been used to support bioenergy

demonstration plants contributing to the implementation of the EIBI. Beyond these, some measures such

as FP7 demonstration projects, NER300 projects as well as relevant Members States projects (see annex

A) have made or are going to make contributions to the ambitious energy targets for 2020 set by the EU.

For biofuels alone, to reach a production capacity of 6Mtoe, approximately 30 large bioenergy plants are

needed in the next seven years, which is a very ambitious goal with regard to the investment needs and the

time needed for the construction of these capacities. The proposed EIBI schedule is set very tight which

strengthens the need to secure financing and long term political frameworks in the very near future.

This document proposes an Implementation Plan for the EIBI, for the period 2013-2017. For this purpose,

a number of actions are described (i.e. programme of demonstration1 and flagship

2 projects plus two

complementary activities), which are considered necessary to achieve the Initiative's objectives. Further

to this, some aspects of the implementation are also suggested for the different actions.

However, these implementation aspects still need to be streamlined and further defined, as some of the

issues associated to them are currently under discussion within the wider context of the overall SET-Plan

implementation (e.g. funding instruments, governance) and the preparation of the Horizon 2020

Framework Programme. Depending on the outcome of the on-going work, some adaptation may be

necessary. The EIBI Team is thus expected to keep working on the implementation modalities, under the

guidance of the SET-Plan Steering Group.

1. BACKGROUND, SCOPE & OBJECTIVES OF THE EIBI

1 Demonstration plants are considered the last non-economic step to demonstrate the performance and technical reliability of a

complete conversion concept in a value chain so that the the first-of-a-kind, commercial-scale industrial unit can be designed

with sufficient confidence for the investment (TRL 6-7). 2 Flagship plants are the first-of-a-kind, commercial-scale industrial demonstration units aiming at validating operational

sustainability and financial viability of a complete conversion concept defined by one of the value chains (TRL 8).

2

Bioenergy will play a key role in the EU long term energy strategy for all applications and especially the

transport sector, contributing up to 14 % of the EU energy mix and up to 10 % of energy demand in

transport in 20203. It is foreseeable that this EU demand will be dominated by renewable fuels substituting

gasoline, and middle distillates for the need of the road, aviation and marine transport sectors.

The feedstocks and bioenergy production technologies which are currently deployed already provide a

significant contribution, but will not be sufficient to reach these targets. The purpose of the EIBI is to

boost the contribution of sustainable4 bioenergy

5 to EU 2020 climate and energy objectives, with a

focused approach leveraging on public-private partnership to manage the risks and share the

financing.

Significant R&D and pilot activities have been going on for the past decade in EU Member States to

enlarge the feedstock basis and to develop processing technologies able to deal with a wider feedstock

basis, enhance feedstock conversion in valuable energy and co-products, minimize overall energy

consumption and meet EU sustainability criteria. These new processing technologies cannot be developed

at industrial scale on a stand-alone basis but as part of commercial “value chains”, i.e. integrated process

schemes, from feedstock to end products.

The scope of the EIBI is focused on innovative bioenergy value chains6 which are not yet

commercially available, and which could bring significant contribution to the bioenergy markets by

large scale deployment (large single units or larger number of smaller units), whilst complying with

the current sustainability requirements set in relevant EU legislation7.

The specific objectives of the EIBI are

(1) to enable commercial availability of advanced bioenergy at large scale by 2020, aiming

at production costs8 allowing competitiveness with fossil fuels at the prevailing economic

and regulatory market conditions, and advanced biofuels9, covering 6 to 9 Mtoe, i.e.

10at

least a minimum of 2 % of EU transportation energy needs by 2020. The rationale behind

3 Renewable Energy Roadmap — Renewable energies in the 21st century: building a more sustainable future, Communication

from the Commission to the European Parliament and the European Council Com (2006) 848, 10 Jan 2007 4 Throughout this document, the words “sustainability” and “sustainable” are covering three dimensions: social, environmental,

economic. 5 Bioenergy: heat and/or electricity and/or fuels produced at industrial scale from bio-resources (dedicated crops, agricultural

and forestry residues, municipal and industrial wastes and algae) 6 Value chain: specific combination of feedstock, processing technologies and marketable end-products. 7 Sustainability requirements as settled in the latest versions of the relevant RES Directive (2009/28/EC) and Fuel Quality

Directive (2009/30/EC) of the European Union 8 Production cost of biofuels depends heavily on investment intensity, on the degree of utilization of primary energy and on

feedstock price, with significant differences across geographic areas and specific feedstock types. 9 Advanced biofuels are biofuels typically produced from non-food/feed feedstocks such as woody biomass, wastes and

residues (i.e. wood, wheat straw, municipal waste), non-food crops (i.e. grasses, miscanthus) or algae:

Targeting similar or better end product properties than the biofuels currently on the market,

Having low carbon dioxide emission or high GHG reduction1,

Demonstrating high sustainability1 1 In accordance with the RED (2009/28/EC) and FQD (2009/30/EC) provisions.

10 Target amount of advanced biofuels as presented in the proposal COM(2012)595 for a Directive of the European Parliament

and of the Council amending Directive 98/70/EC relating to the quality of petrol and diesel fuels and amending Directive

2009/28/EC on the promotion of the use of energy from renewable sources from 17 Oct 2012.

3

the proposal of the target of at least a minimum of 2 % of EU transportation needs is based

on the compliance with the proposed revision COM(2012)595 of the RED and FQD.

(2) to strengthen EU technology leadership for renewable transport fuels, serving the fastest

growing area of transport fuels in the world

(3) to contribute to the targets of the Renewable Energy Directive of increasing the

percentage of renewable energy to 20 % through the increase of high efficiency CHP.

Because of the scale of investment needed and the risks involved (technology, feedstock & end product

prices, regulatory framework evolution), financing the latest stages of development of innovative

bioenergy technologies is a major obstacle for large scale industrial deployment of these

technologies. In order to meet the objective of producing 6 to 9 MToe of advanced biofuels by 2020,

substantial financial input is needed. Assuming a typical advanced biofuels unit has a capacity of 200

kToe/y, already for the 6 MToe objective 30 such units would need to be up and running by 2020.

Assuming a 3 year time line between decision to build and start up, and no decision to build before a

flagship unit (“first of its kind”) has been operating for at least 6 months, 30 units would need to be

decided by 2017. At 500 M€/unit, this would represent cumulative investments of 15 bn€. The main

challenge of the EIBI is to tackle this issue by leveraging on public-private partnerships based on efficient

governance and relevant funding sources and mechanisms.

The core activities of the EIBI aim at building and operating demonstration projects and/or flagship

plants for innovative bioenergy value chains with large market potential11

.

Seven such innovative bioenergy value chains have been identified (see chapter 2.1), which could bring

significant contributions to EU ambitious objectives, in addition to existing bioenergy value chains.

Within each of these “generic” value chains, different paths based on different biomass feedstocks

(including fossil co-processing), conversion technologies and/or energy products are possible, leading to a

wide range of options. Selecting the most relevant options cannot be achieved at a generic level, outside a

specific context of locally available feedstocks and targeted end products serving clearly identified

markets requesting them.

The EIBI is proposing a pragmatic approach to select the most promising options, based on

transparent criteria reflecting a set of key economic, environmental and social performances

expected. Its flexibility will allow adjusting the programme to the priorities of the EU and of the

Member States willing to join forces to boost the development of innovative bioenergy in Europe,

encouraging industry and technology champions to team up with the relevant European partners

and reach the capability and scale to bring a significant contribution to EU climate and energy

ambitions and compete on the world markets.

In line with the EU ambitions on climate and energy, sustainability aspects are central to the EIBI.

Economic, social and environmental sustainability is at the heart of the criteria proposed to evaluate

and select projects within this initiative (cf. section 3.2), and this along the whole value chain.

Further to this, a specific complementary activity is proposed to tackle the critical issue of

sustainable biomass supply (cf. section 4.1).

This paper describes the core activities needed for the phase between 2013 and 2017, in order to select,

fund, build and operate demonstration projects and flagship plants for the most promising options ready

for pre-industrial and/or industrial deployment. The complementary measures to be initiated during the

same period are also described. This document also suggests implementation modalities for the activities.

11 See pages 6 and 7 for the difference between funding mechanisms for demonstration and flagship plants.

4

If needed and decided by the EIBI Team, a revision of the Implementation Plan during the timeframe can

be anticipated.

For these actions to be possible and to give the programme credibility, it is crucial that adequate public-

private governance structures and funding mechanisms are defined as well as relevant funding secured. In

that context, the European Industrial Bioenergy Initiative closely cooperates with the Private Public

Partnership on Biobased Industries (Bio-based Industries Initiative)12

.

12 More information on the Bio-Based Industries Initiative: http://biconsortium.eu/

5

2. IMPLEMENTATION ACTIONS FOR 2013-2017

2.1 Overview of core activities

The core activity or “Implementation Actions for 2013-2017” aims at building and operating the early

demonstration and/or flagship projects which are ready to be deployed. The suggested implementation

approach is to use selection procedures already established for demonstration and flagship plants. This

document is presenting the complete scope of value chains of potential relevance to the EIBI. In principle,

within each of these seven “generic” value chains, “specific” value chains have the potential to be

developed to industrial scale based on existing technology and know-how developed up to pilot and

demonstration scale. In practise, authorities providing the public funding might decide to narrow the focus

to certain value chains and/or to “demonstration only” or “flagship only” projects, depending on the

sources, type and amount of funding. The EIBI is built as a coherent and flexible programme, adjusting to

level and sources of funding available, as they might evolve over time.

A main challenge to select the winning options is the diversity of bioenergy value chains of potential

relevance across the EU because of the diversity of feedstock situations and the different national

bioenergy markets, offering different level of support for the biofuels, bioheat and bioelectricity end

products. The seven value chains listed below reflect the variety of feedstocks and processing

technologies that will serve the advanced bioenergy markets of 2020. Each of the seven value chains is

viewed as an energy-driven biorefinery. Some of them may also produce high value by-products, e.g.

chemicals. These by-products might be produced aside the main energy products (fuels, power and heat) if

they contribute to the viability of a project. As indicated in the eligibility criteria, at least 70% of the

bioproducts produced by the plant shall be bioenergy, calculated on the basis of energy content of the

products sold.

Although significant efforts to develop processing technologies based on thermochemical and biological

pathways have been on going in the EU for more than a decade, there is a significant variation in the level

of maturity of technology options within each value chains. The few already existing demonstration

projects for specific variations of certain value chains do not allow concluding that these provide the best

approach and that no alternative route would deserve funding. Each value chain has the potential to

present relevant candidates between 2013 and 2017. These potential demonstration and flagship plants are

legitimate candidates to apply for funding under the EIBI. There is no fair, transparent and rational basis

to exclude “à priori” neither any of the 7 value chains nor specific variations of any of them. However,

value chain 7 “Energy carriers produced by photosynthetic microorganisms (algae or cyanobacteria)” is

less mature than other value chains at this moment. Thus, this value chain might not be eligible for

flagship plants at present technology status. But, the potential to shift this dynamics through technical

improvements exists and the learning rate is higher than that of other value chains so demo plants are

expected before the end of this decade. Hence the corner stone of the EIBI approach would be to

evaluate and select projects on the basis of transparent selection criteria.

The selection procedures for demonstration plants (described in section 2.2) and for flagship plants

(section 2.3) require the existence of adequate funding programmes. Possible timelines for the

implementation are displayed in Annex b. Figures 3 and 4 depict two different scenarios for the selection

procedures of demonstration and flagship plants and other EIBI activities based on assumptions that either

interim support to the financing of the plants will happen before the revision of the RED and FQD (figure

3) or the assumption that the investment decisions are delayed (figure 4). Based on the EoI results which

demonstrate that the different value chains have reached different levels of maturity, not separated, but

rather combined calls for demonstration- and flagship plants will be issued.

6

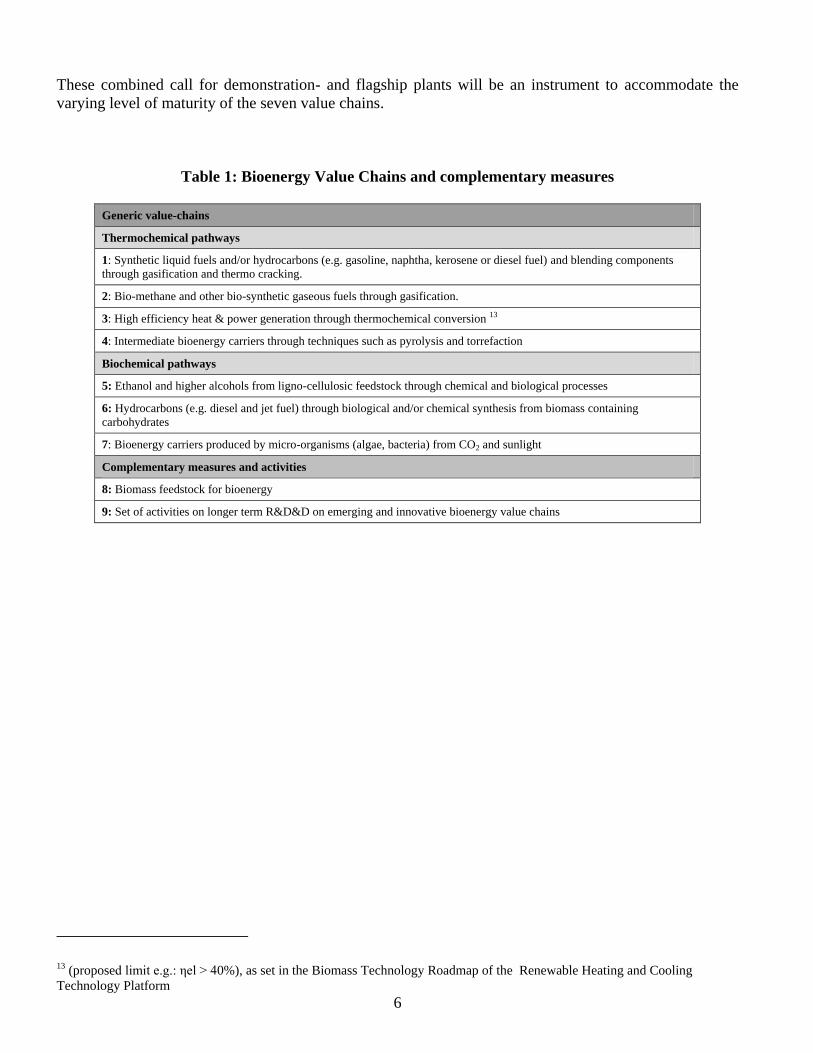

These combined call for demonstration- and flagship plants will be an instrument to accommodate the

varying level of maturity of the seven value chains.

Table 1: Bioenergy Value Chains and complementary measures

Generic value-chains

Thermochemical pathways

1: Synthetic liquid fuels and/or hydrocarbons (e.g. gasoline, naphtha, kerosene or diesel fuel) and blending components

through gasification and thermo cracking.

2: Bio-methane and other bio-synthetic gaseous fuels through gasification.

3: High efficiency heat & power generation through thermochemical conversion 13

4: Intermediate bioenergy carriers through techniques such as pyrolysis and torrefaction

Biochemical pathways

5: Ethanol and higher alcohols from ligno-cellulosic feedstock through chemical and biological processes

6: Hydrocarbons (e.g. diesel and jet fuel) through biological and/or chemical synthesis from biomass containing

carbohydrates

7: Bioenergy carriers produced by micro-organisms (algae, bacteria) from CO2 and sunlight

Complementary measures and activities

8: Biomass feedstock for bioenergy

9: Set of activities on longer term R&D&D on emerging and innovative bioenergy value chains

13 (proposed limit e.g.: ηel > 40%), as set in the Biomass Technology Roadmap of the Renewable Heating and Cooling

Technology Platform

7

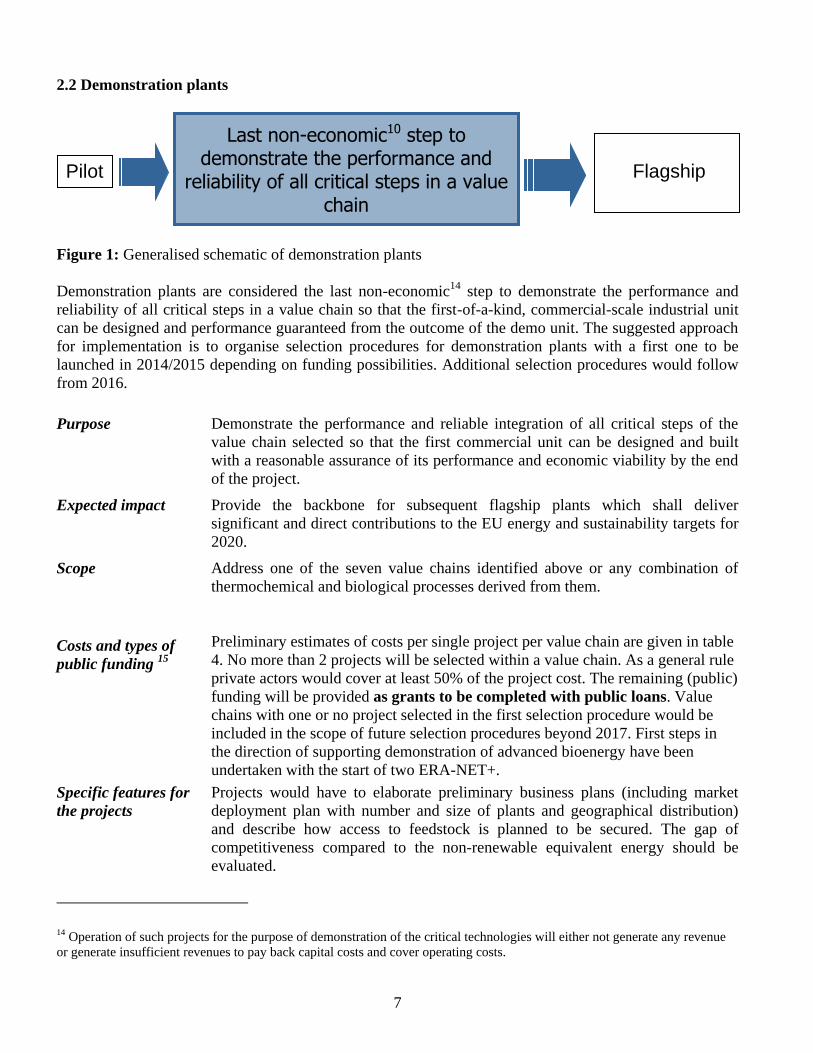

2.2 Demonstration plants

Figure 1: Generalised schematic of demonstration plants

Demonstration plants are considered the last non-economic14

step to demonstrate the performance and

reliability of all critical steps in a value chain so that the first-of-a-kind, commercial-scale industrial unit

can be designed and performance guaranteed from the outcome of the demo unit. The suggested approach

for implementation is to organise selection procedures for demonstration plants with a first one to be

launched in 2014/2015 depending on funding possibilities. Additional selection procedures would follow

from 2016.

Purpose Demonstrate the performance and reliable integration of all critical steps of the

value chain selected so that the first commercial unit can be designed and built

with a reasonable assurance of its performance and economic viability by the end

of the project.

Expected impact Provide the backbone for subsequent flagship plants which shall deliver

significant and direct contributions to the EU energy and sustainability targets for

2020.

Scope Address one of the seven value chains identified above or any combination of

thermochemical and biological processes derived from them.

Costs and types of

public funding 15

Preliminary estimates of costs per single project per value chain are given in table

4. No more than 2 projects will be selected within a value chain. As a general rule

private actors would cover at least 50% of the project cost. The remaining (public)

funding will be provided as grants to be completed with public loans. Value

chains with one or no project selected in the first selection procedure would be

included in the scope of future selection procedures beyond 2017. First steps in

the direction of supporting demonstration of advanced bioenergy have been

undertaken with the start of two ERA-NET+.

Specific features for

the projects

Projects would have to elaborate preliminary business plans (including market

deployment plan with number and size of plants and geographical distribution)

and describe how access to feedstock is planned to be secured. The gap of

competitiveness compared to the non-renewable equivalent energy should be

evaluated.

14 Operation of such projects for the purpose of demonstration of the critical technologies will either not generate any revenue

or generate insufficient revenues to pay back capital costs and cover operating costs.

Last non-economic10 step to demonstrate the performance and

reliability of all critical steps in a value chain

Pilot

Flagship

8

R&D components directly supporting the demonstration activity would be eligible

and get funding via existing R&D funding schemes at EU and national level.

Projects would have to include a clear description of the rationale for public

funding as well as sustainability assessment on the basis of a robust life-cycle

analysis approach for the entire value chain from feedstock production to the end

product.

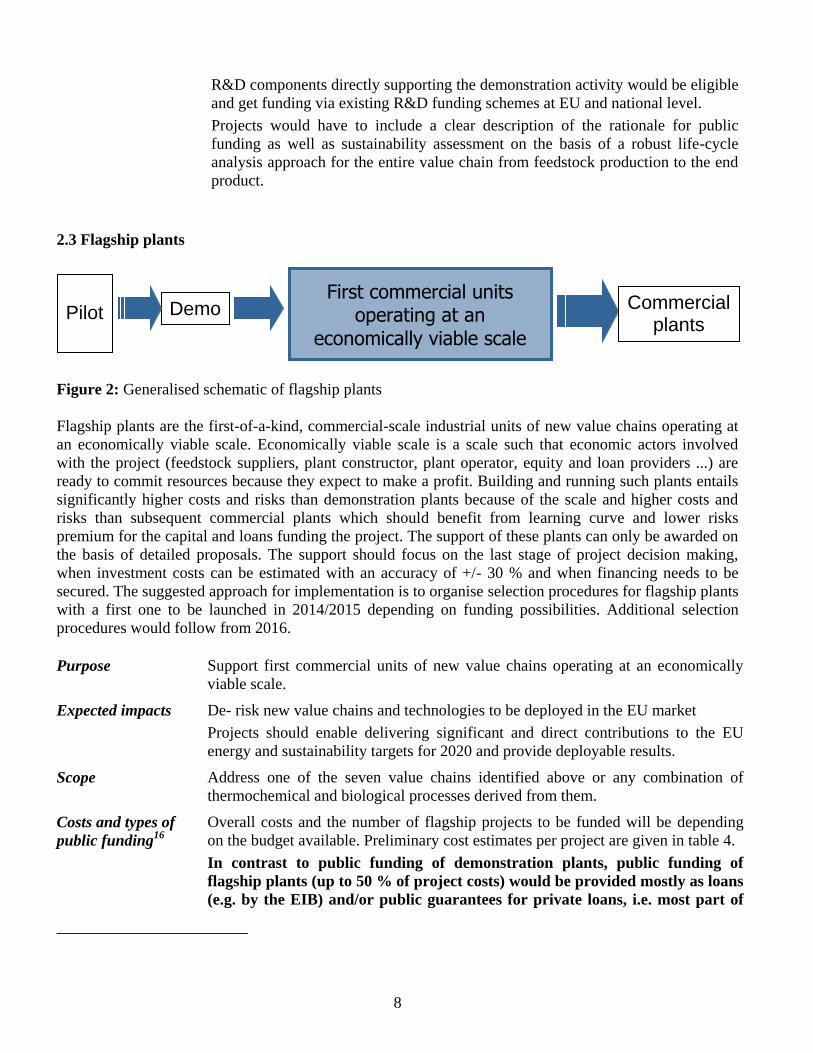

2.3 Flagship plants

Figure 2: Generalised schematic of flagship plants

Flagship plants are the first-of-a-kind, commercial-scale industrial units of new value chains operating at

an economically viable scale. Economically viable scale is a scale such that economic actors involved

with the project (feedstock suppliers, plant constructor, plant operator, equity and loan providers ...) are

ready to commit resources because they expect to make a profit. Building and running such plants entails

significantly higher costs and risks than demonstration plants because of the scale and higher costs and

risks than subsequent commercial plants which should benefit from learning curve and lower risks

premium for the capital and loans funding the project. The support of these plants can only be awarded on

the basis of detailed proposals. The support should focus on the last stage of project decision making,

when investment costs can be estimated with an accuracy of +/- 30 % and when financing needs to be

secured. The suggested approach for implementation is to organise selection procedures for flagship plants

with a first one to be launched in 2014/2015 depending on funding possibilities. Additional selection

procedures would follow from 2016.

Purpose Support first commercial units of new value chains operating at an economically

viable scale.

Expected impacts De- risk new value chains and technologies to be deployed in the EU market

Projects should enable delivering significant and direct contributions to the EU

energy and sustainability targets for 2020 and provide deployable results.

Scope Address one of the seven value chains identified above or any combination of

thermochemical and biological processes derived from them.

Costs and types of

public funding16

Overall costs and the number of flagship projects to be funded will be depending

on the budget available. Preliminary cost estimates per project are given in table 4.

In contrast to public funding of demonstration plants, public funding of

flagship plants (up to 50 % of project costs) would be provided mostly as loans

(e.g. by the EIB) and/or public guarantees for private loans, i.e. most part of

First commercial units operating at an

economically viable scale

Demo Commercial plants

Pilot

9

the funding will be provided by private actors.

Specific features for

projects

Projects would have to present complete business plans (including subsequent

market deployment plans with the number, size of plants and foreseen geographical

distribution) as well as present commercial strategies and pre contractual

commitments from credible partners for both feedstock sourcing and end product

marketing.

Demonstration stage must have been passed successfully, otherwise it must be

explained why the demonstration step is not necessary.

It would be mandatory for projects to include a sustainability assessment on the

basis of a robust life-cycle analysis approach for the entire value chain from

feedstock production to the end product.

2.4 Overall estimated costs for 2013-2017

Assuming that for each of the 7 generic value chains one demonstration and one flagship project would be

selected, this would represent (public17

and private) funding requirements of up to app. 2800 M€ (sum of

the higher range of demo and flagship projects cost estimate amount to app. 2800 M€, i.e. about 35% of

the total cost of EIBI over the 10 years).

17 The term “public funding” used throughout this document encompasses very different tools such as grants, loans and loan

guarantees. Adding them up is both meaningless and misleading.

10

3. IMPLEMENTATION MODALITIES AND MONITORING

3.1 General principles for the project selection procedures

EIBI stakeholders (industry, academia, NGOs), MS, EC and financing community (e.g. EIB) have

worked together and defined a robust set of eligibility and selection criteria, as written down in the

“Project eligibility and selection criteria” from October 2010 (see Annex D).

In order to align with the evolution of the situation at EU level and industry readiness, a call of

expression of interest was organised in 2011 (cf. below). It allowed developing a clear picture of

the number and types of projects ready to apply.

Projects would be funded on a flexible basis involving MS resources, EIB loans, loan guarantee

and other possible sources of funding. The selection procedures would follow specifically

designed organisational modalities to be fine-tuned with the authorities providing public funding.

The EC will facilitate interactions between the different European funding schemes such as

Horizon 2020, EIB and NER300, and with national programmes to avoid duplication, and optimize

the use of resources and the impact of all schemes.

Objective of the Calls for Expression of Interest and results of the first call

Calls for expression of interest would be issued in order to update the EIBI partners (Industry, MS, EC

and associated members) on the actual stage of development of Bioenergy projects in the EU

corresponding to the specificities of the EIBI demonstration and flagship projects. Number and intervals

of Calls for expression of interest will be decided by the EIBI team.

It would follow a simplified and light procedure, involving:

The submission of a short project description (specific templates for demo and flagship projects),

presenting technology options, bioenergy end products targets, main partners, location of the plant,

feedstock base, budget requirements and funding approach.

A review process undertaken by a small dedicated working group of experts nominated by the

EIBI team, with the objective to determine which of the projects meet the minimum requirements

of the EIBI so that EIBI team can inform the proponents accordingly.

SETIS as a tool for managing the submission and review process, as well as the information

flows18

.

There would be no scoring and no "Go" / "No Go" statement, the essential objective being to "inform the

process" of promoting new European public/private partnership in the area of Bioenergy. It is a

complement and contribution to the work of SETIS, with a particular focus on the requirements of the

EIBI.

18 SETIS: Strategic Energy Technologiy Information System, setis.ec.europa.eu

11

A first call for expression of interest (EoI) was carried out with deadline for submission in autumn 2011.

The scope of the EoI was to establish a clear picture of the industrial interest and readiness around the

seven generic value chains. The results from the Expression of Interest showed that from 53 submissions

15 flagship and 15 demonstration plants would be eligible (completely or possibly eligible) for EIBI

funding. It needs to be taken into account that the EoI was not a pre-selection procedure for the EIBI, thus

might not have received the full industrial attention.

3.2 Summary approach for project eligibility and selection criteria

A set of criteria, reflecting the key features of the EIBI, has been prepared to evaluate and select the

demonstration and flagship projects within the initiative. The EIBI Project Eligibility and Selection

Criteria consist of four criteria. The first concern the administrative aspects of each application, which

relate to whether the project can be admitted for evaluation, thus it addresses formal eligibility aspects.

The second criteria concern the overall aims and objectives of each project and whether these are within

the overall aims and objectives of the EIBI, thus it addresses the compatibility of the project with the

EIBI. Finally the last two criteria address respectively the overall project and overall technology

objectives and how reliable, accurate, traceable and realistic the planning, the technical, environmental,

economic and market assumptions made in the project are. The scoring of the project and technology

criteria is weighted in order to prioritise the most important criteria.

The following key principles shape the architecture of the eligibility and evaluation criteria:

EU dimension and Industrial leadership: Consortium actors from different Member States or

Associated Countries, with at least 2 industrial actors and a science & technology actor19

.

Scale/Maturity (for demonstration plants): the scale should be high enough to be able to prove

technical and economic performance and provide enough data so that the technology can be

realistically scaled-up to industrial size after successful operation of the demonstration.

Minimum bioenergy content: At least 70% of the bioproducts produced by the plant shall be

bioenergy (biofuels, heat, power) calculated on basis of energy content of the products sold.

Innovation: At least one “technology brick” or the integration of “technology bricks” within the

considered value chain should not have been deployed at demonstration/commercial scale.

Timeline: The operation of demonstration and flagship plants receiving support under the 1st Call

and 2nd

Call of Projects must be planned no later than four years after the approval for construction

Feedstock: Realistic scenario for feedstock sourcing for future industrial units should be described

and volume potential of corresponding bioenergy market should be outlined.

Sustainability: in accordance with the RED (2009/28/EC) and FQD (2009/30/EC) provisions.

The Project Eligibility and Selection Criteria document is presented as annex D to this Implementation

Plan.

20 The Key performance Indicators can be found at SETIS: http://setis.ec.europa.eu/implementation/eii/eii-key-performance-

indicators/KPIs_EIBI/view

12

3.3 Monitoring of demonstration and flagship projects (Key Performance Indicators)20

Monitoring is necessary on two levels: first on the level of the EIBI programme, second on the level of the

individual projects. The outcome of the demonstration and flagship plants built as results of the above

mentioned selection procedures will be monitored by the EIBI Team. Key performance indicators (KPIs)

will be used as a measure of performance of the project which applies for funding under the EIBI. KPIs to

monitor the progress of projects from a technological point of view have been developed jointly by

representatives of the European Commission, including the Joint Research Centre, and the EBTP. They

have been presented to and agreed by the EIBI Team.

The agreed list of KPIs is presented as annex C to this Implementation Plan.

20 The Key performance Indicators can be found at SETIS: http://setis.ec.europa.eu/implementation/eii/eii-key-performance-

indicators/KPIs_EIBI/view

13

4. COMPLEMENTARY MEASURES and ACTIVITIES

4.1 Sustainable biomass feedstock for bioenergy

The core of the EIBI Roadmap consists in the implementation of demonstration and flagship plants on the

currently most promising advanced bioenergy value chains. Sustainable and reliable supply of feedstock is

a critical success factor for the long-term perspective of biomass-based technologies on a large scale. This

relates to efforts in assessing the biomass availability for bioenergy purposes in EU27 and also in

improving productivity in these sectors, in developing reliable and sustainable supply chains that open up

the feedstock potentials, certification issues, and prevention of excessive disturbances in agricultural and

forest commodity markets. These challenges which are not specific to bioenergy use of biomass should be

addressed in a coherent effort shared with the relevant stakeholders and initiatives. To this aim, several

activities will be implemented in the framework of the EIBI.

Appropriate project eligibility and selection criteria have been developed to ensure that the above

mentioned plants will be designed with a full consideration of the sustainable availability of corresponding

feedstock.

In addition, a structured dialogue and continued interaction between the stakeholders of the EIBI and other

stakeholder groups involved in other initiatives covering the up-stream part of the described value chains

will be facilitated by the EC, in order to foster synergies between the respective strategies and

programmes especially the BioBased Industries PPP. This interaction will lead to joint initiatives linking

several services of the Commission, but possibly also of national research and implementation

programmes.

Suggested resources and financing instruments

Resources for these activities would be mainly public from the different FP7 Themes related to biomass,

and/or national research programmes. The total cost in period 2013-2017 is estimated at around 60 M €

per year, with a share of 75% of public source. The estimated cost per project is 5-15 M €.

EU added value

This set of activities will allow implementing joint programming of different research instruments at EC

level, ensuring their coherence, maximising their synergies and results while avoiding duplication.

4.2 Set of activities on longer term R&D on emerging and innovative bioenergy value chains

The core of the EIBI Roadmap focuses on value chains that will be commercially viable in the next five to

ten years, contributing to the 2020 targets of the RES Directive. But to go beyond these targets, new

technologies and value chains are to be developed. A longer-term R&D programme needs to be put in

place that will provide the industry with technologies that will reach commercial deployment beyond 2020

and for which a new programme of demonstration and flagship plants could be launched in five to ten year

time.

This will imply both addressing R&D improvements of technologies already existing at lab scale, but not

yet developed enough to be part of the EIBI targeted value-chains, and more fundamental research with

the aim to develop totally new bioenergy production avenues.

In order to identify research priorities, 2 ad-hoc workshops were organised by EERA in collaboration with

EC services in May 2013:

14

Workshop 1 "Accelerating the development of most promising existing bioenergy technologies",

involving European bioenergy experts, aimed at identifying R&D needs and priorities to be addressed

to improve bioenergy technologies already existing at lab scale, such as the development of bioenergy

carriers, biofuels for aviation sector and technologies using algae feedstock.

Workshop 2 "Longer term research on future breakthroughs of bioenergy technologies” involving

European engineers and scientists in fundamental and applied disciplines (such as physics, chemistry,

biology, genetics, engineering, bioenergy, biotechnologies), aimed at identifying the most critical gaps

in the current knowledge base in view of possible future bioenergy technology breakthroughs.

The outcome of the workshops is available on SETIS and should be used as a valuable input by EC and

MS while defining research areas to be funded at EU and national levels.

Suggested resources and financing instruments

Based on current project size and for maximum impact, the research activities addressing needs and

priorities for technologies already existing at lab-scale would absorb around 45 M € per year, with costs in

the range of 5-15 M € per project and a share of 50% of public sources. Actions on longer term research

would be in the order of 30 M € per year, with costs in the range of 5-15 M € per project and a share of

75% of public sources. Financing could come from Horizon 2020, MS, EERA, and/or the private sector.

EU added value and risk

The research described above would benefit from being performed at EU level as this would permit to

better exploit economies of scale and synergies.

15

ANNEX A: VALUE CHAINS, SUMMARY DESCRIPTION AND EXAMPLES OF ONGOING

PROJECTS

Within each of the generic value chains presented in Table 1, specific variations based on different

feedstocks and/or processing technologies are being developed, and are currently at different stages of

maturity; some of them have attained the pilot scale where their technical viability has been confirmed

while few have reached the demonstration phase and have ascertained their technical reliability. Only one

of the advanced biofuel related value chains identified in Table 1 has come close to establish economic

viability in Europe so far, resulting in a running industrial demonstration unit plant (Chemtex plant in

Crescentino producing ethanol from lignocellulosic feedstock, value chain 521

). Therefore an

implementation strategy based on flexible approach will be applied to ensure compliance with the key

objectives of the initiative and make best use of the limited resources available.

Some of the technologies that could be deployed in the 7 generic value chains are already supported by

various actions at national, local, industrial and EC level. The EIBI is aiming to support the projects for

which the existing local, national and EU programmes could not bring enough funding because of the

magnitude of funding required.

In the following section, each value chain is briefly described and examples of on-going projects (and

projects at advanced planning stage in italics) are given. However, this list is not exhaustive and with a

variable degree of reliability22

. Preliminary estimates of costs per single project per value chain are

presented in table 4. It should be noted that because demonstration and flagship plants are by definition

"first ever built" the costs cannot be accurately estimated, until a basic design engineering study (+or – 30

% estimate) or a detailed engineering study (+ or – 10 % estimate) have been performed. It is suggested

that only a limited number of demonstration and flagship projects is selected in a specific selection

procedure, depending on the availability of public budget, the matching budget from the private

sector and the project eligibility and selection criteria.

21 Crescentino capacity around 60 kt/a bioethanol; validation of the technology may take place in bigger plants (80+ kt/a) 22 The EBTP-SABS project - European Biofuels Technology Platform-Support for Advanced Biofuels Stakeholders which has

started on 1 Sep 2013 will continuously work on improving the database of relevant projects: http://ebtp-sabs.eu/ .

16

Thermochemical pathways

1: Synthetic liquid fuels and/or hydrocarbons (e.g. gasoline, naphtha, kerosene or diesel fuel) and

blending components through gasification and thermo cracking.

Main Feedstocks: Forest and agricultural residues, waste wood, energy crops, black liquor

Main Products: FT diesel and naphtha, DME, Methanol

Level of Maturity: 1-2

(1= Demo exists / next step: flagship plant; 2= Pilot exists / next step: demo or flagship plant)

Examples of EU on-going23

projects:

(projects in italics are at planning stage)

Pilots: BioDME (Sweden), Bioliq-KIT (Germany), Güssing, FT (Austria), BioTfueL

(France)

Demo: Värmlandsmethanol (Sweden), BioDME/Biomethanol (Sweden),

Flagship: Forest BtL Project (Kemi/Ajos plant)(Finland), UPM BtL Project (France),

WoodSpirit Project (Netherlands),, Värmlandsmethanol (Sweden),

Main technology challenges: Feeders, gas cleaning, catalysts

Technical challenges for all value chains: Feedstock flexibility, energy and carbon efficiency,

reliability & maintenance, capex efficiency

23 Ongoing means investment decision made and project at engineering, procurement, construction (EPC) stage.

17

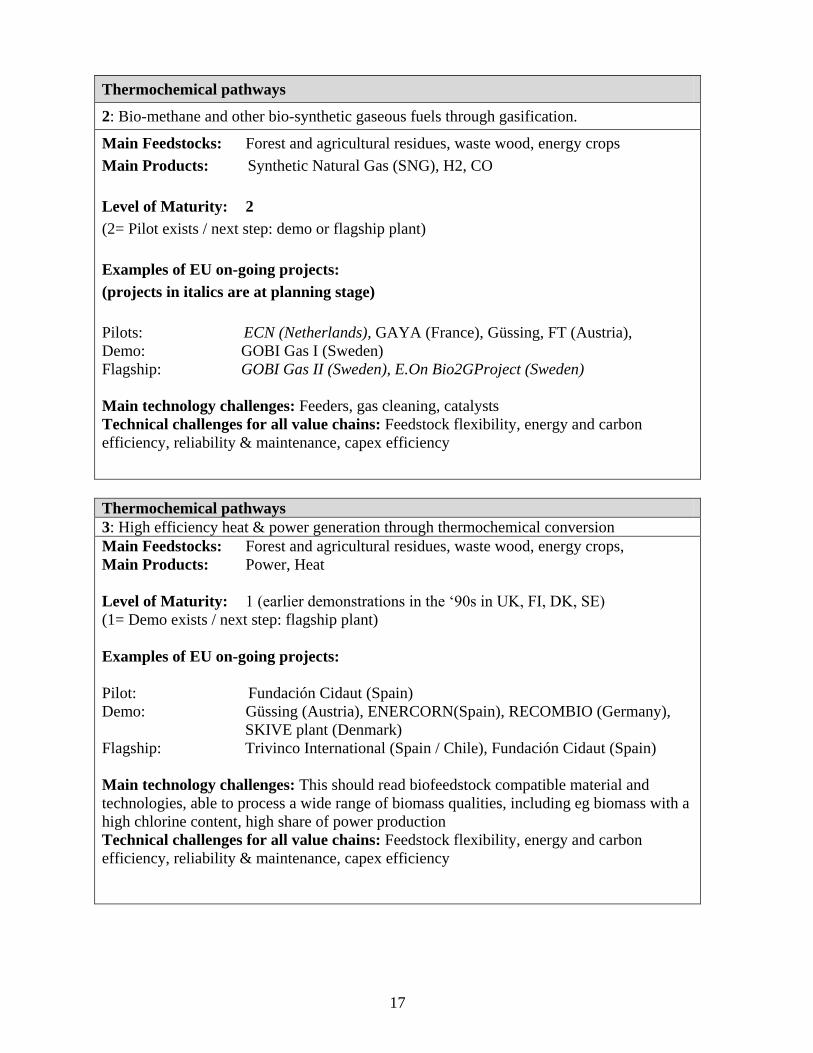

Thermochemical pathways

2: Bio-methane and other bio-synthetic gaseous fuels through gasification.

Main Feedstocks: Forest and agricultural residues, waste wood, energy crops Main Products: Synthetic Natural Gas (SNG), H2, CO

Level of Maturity: 2

(2= Pilot exists / next step: demo or flagship plant)

Examples of EU on-going projects:

(projects in italics are at planning stage)

Pilots: ECN (Netherlands), GAYA (France), Güssing, FT (Austria),

Demo: GOBI Gas I (Sweden)

Flagship: GOBI Gas II (Sweden), E.On Bio2GProject (Sweden)

Main technology challenges: Feeders, gas cleaning, catalysts

Technical challenges for all value chains: Feedstock flexibility, energy and carbon

efficiency, reliability & maintenance, capex efficiency

Thermochemical pathways

3: High efficiency heat & power generation through thermochemical conversion

Main Feedstocks: Forest and agricultural residues, waste wood, energy crops,

Main Products: Power, Heat

Level of Maturity: 1 (earlier demonstrations in the ‘90s in UK, FI, DK, SE)

(1= Demo exists / next step: flagship plant)

Examples of EU on-going projects:

Pilot: Fundación Cidaut (Spain)

Demo: Güssing (Austria), ENERCORN(Spain), RECOMBIO (Germany),

SKIVE plant (Denmark)

Flagship: Trivinco International (Spain / Chile), Fundación Cidaut (Spain)

Main technology challenges: This should read biofeedstock compatible material and

technologies, able to process a wide range of biomass qualities, including eg biomass with a

high chlorine content, high share of power production

Technical challenges for all value chains: Feedstock flexibility, energy and carbon

efficiency, reliability & maintenance, capex efficiency

18

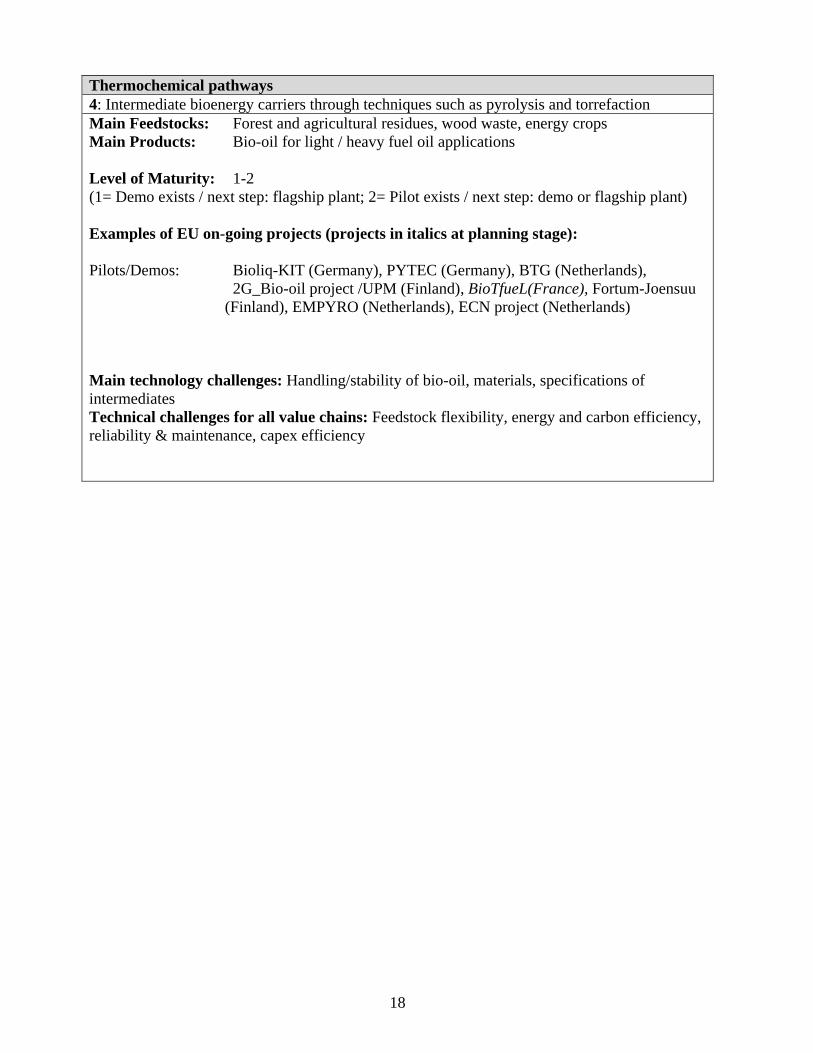

Thermochemical pathways

4: Intermediate bioenergy carriers through techniques such as pyrolysis and torrefaction

Main Feedstocks: Forest and agricultural residues, wood waste, energy crops

Main Products: Bio-oil for light / heavy fuel oil applications

Level of Maturity: 1-2

(1= Demo exists / next step: flagship plant; 2= Pilot exists / next step: demo or flagship plant)

Examples of EU on-going projects (projects in italics at planning stage):

Pilots/Demos: Bioliq-KIT (Germany), PYTEC (Germany), BTG (Netherlands),

2G_Bio-oil project /UPM (Finland), BioTfueL(France), Fortum-Joensuu

(Finland), EMPYRO (Netherlands), ECN project (Netherlands)

Main technology challenges: Handling/stability of bio-oil, materials, specifications of

intermediates

Technical challenges for all value chains: Feedstock flexibility, energy and carbon efficiency,

reliability & maintenance, capex efficiency

19

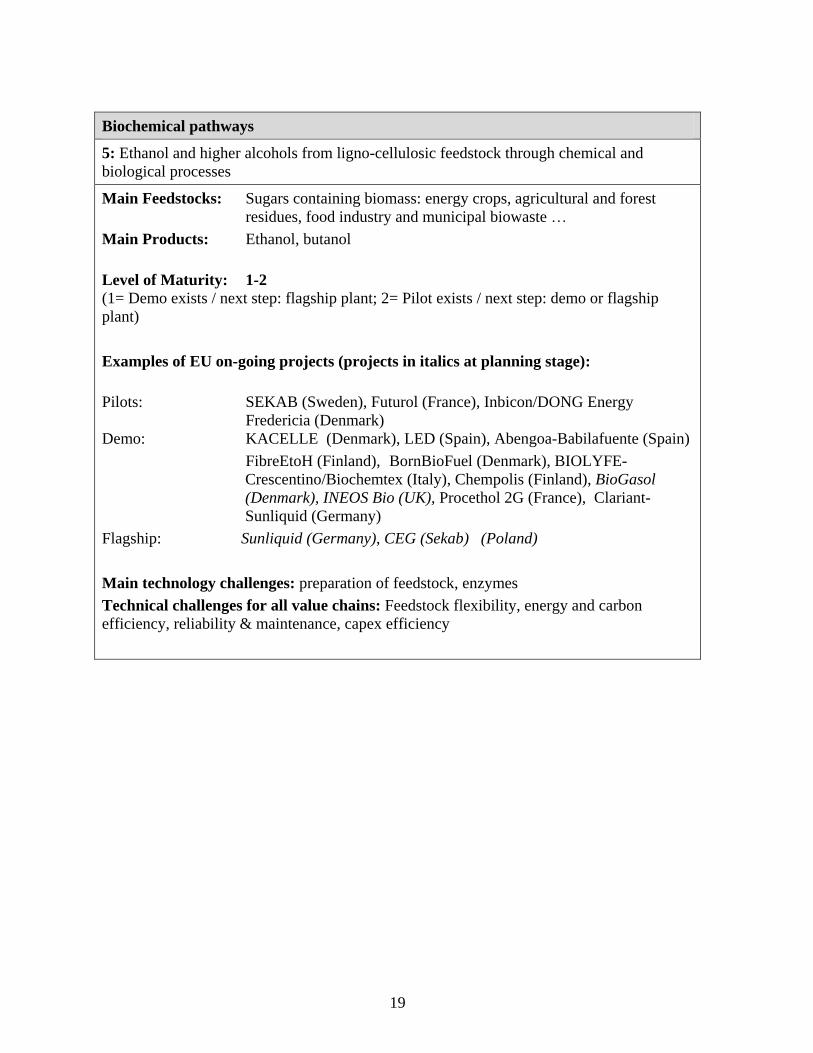

Biochemical pathways

5: Ethanol and higher alcohols from ligno-cellulosic feedstock through chemical and

biological processes

Main Feedstocks: Sugars containing biomass: energy crops, agricultural and forest

residues, food industry and municipal biowaste …

Main Products: Ethanol, butanol

Level of Maturity: 1-2

(1= Demo exists / next step: flagship plant; 2= Pilot exists / next step: demo or flagship

plant)

Examples of EU on-going projects (projects in italics at planning stage):

Pilots: SEKAB (Sweden), Futurol (France), Inbicon/DONG Energy

Fredericia (Denmark)

Demo: KACELLE (Denmark), LED (Spain), Abengoa-Babilafuente (Spain)

FibreEtoH (Finland), BornBioFuel (Denmark), BIOLYFE-

Crescentino/Biochemtex (Italy), Chempolis (Finland), BioGasol

(Denmark), INEOS Bio (UK), Procethol 2G (France), Clariant-

Sunliquid (Germany)

Flagship: Sunliquid (Germany), CEG (Sekab) (Poland)

Main technology challenges: preparation of feedstock, enzymes

Technical challenges for all value chains: Feedstock flexibility, energy and carbon

efficiency, reliability & maintenance, capex efficiency

20

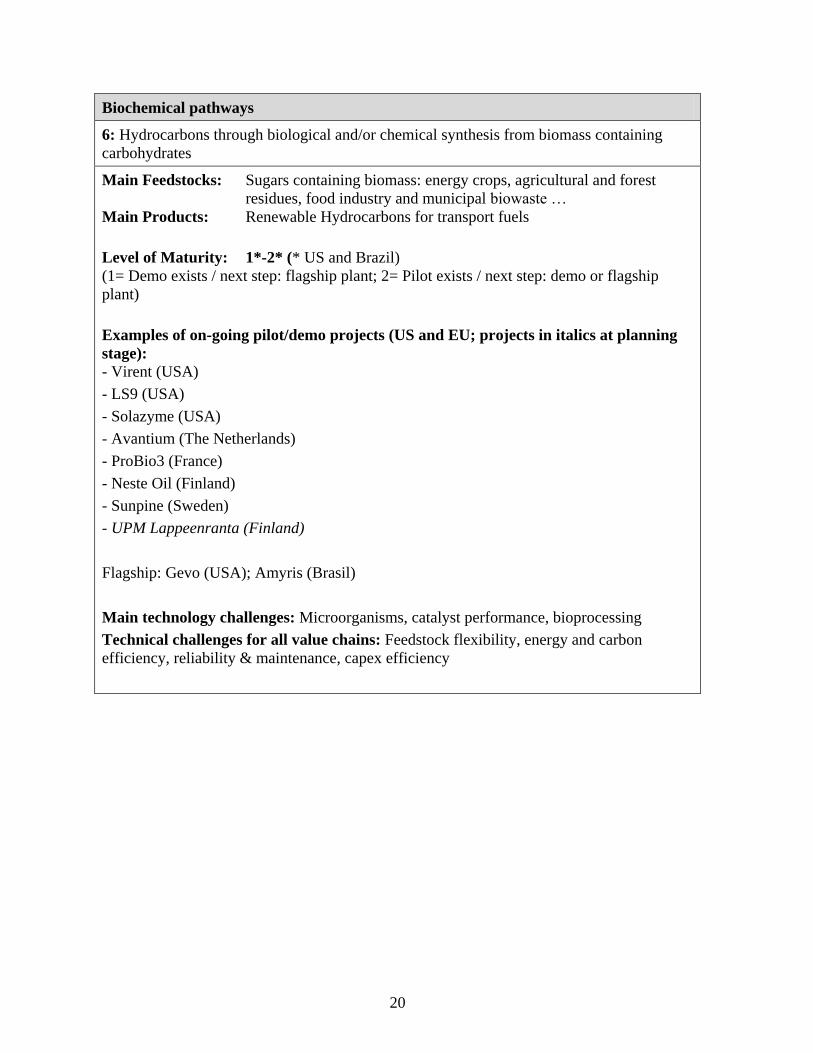

Biochemical pathways

6: Hydrocarbons through biological and/or chemical synthesis from biomass containing

carbohydrates

Main Feedstocks: Sugars containing biomass: energy crops, agricultural and forest

residues, food industry and municipal biowaste …

Main Products: Renewable Hydrocarbons for transport fuels

Level of Maturity: 1*-2* (* US and Brazil)

(1= Demo exists / next step: flagship plant; 2= Pilot exists / next step: demo or flagship

plant)

Examples of on-going pilot/demo projects (US and EU; projects in italics at planning

stage):

- Virent (USA)

- LS9 (USA)

- Solazyme (USA)

- Avantium (The Netherlands)

- ProBio3 (France)

- Neste Oil (Finland)

- Sunpine (Sweden)

- UPM Lappeenranta (Finland)

Flagship: Gevo (USA); Amyris (Brasil)

Main technology challenges: Microorganisms, catalyst performance, bioprocessing

Technical challenges for all value chains: Feedstock flexibility, energy and carbon

efficiency, reliability & maintenance, capex efficiency

21

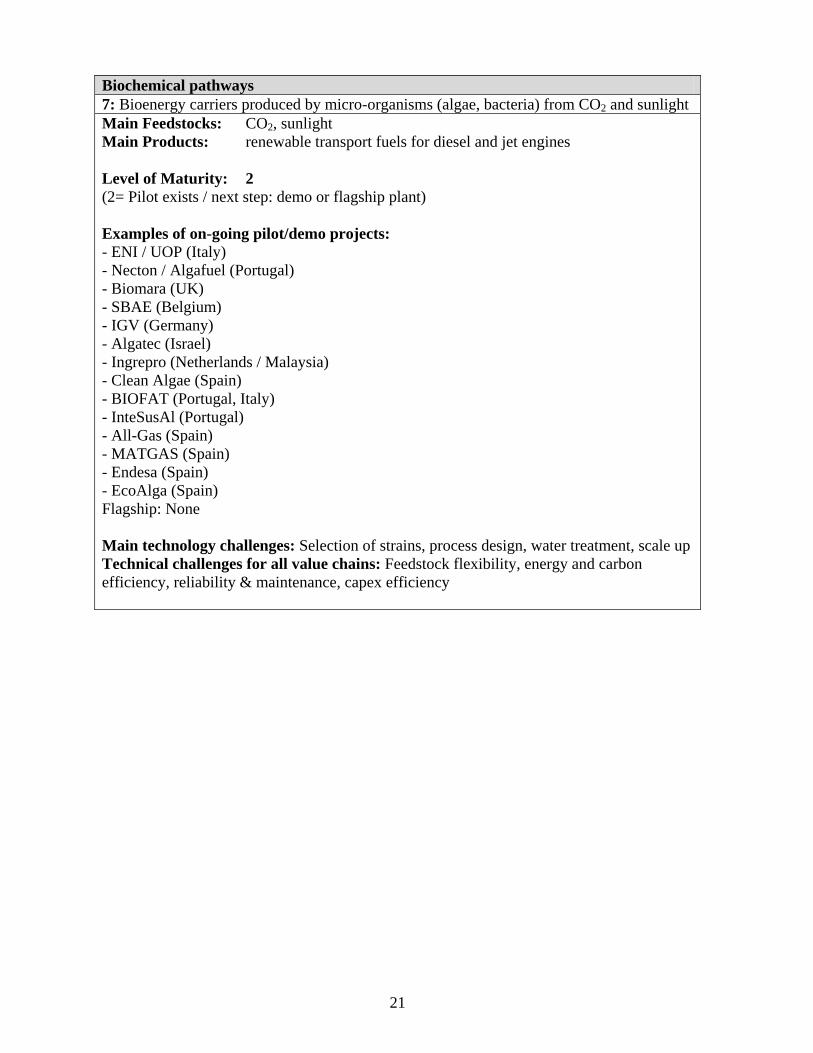

Biochemical pathways

7: Bioenergy carriers produced by micro-organisms (algae, bacteria) from CO2 and sunlight

Main Feedstocks: CO2, sunlight

Main Products: renewable transport fuels for diesel and jet engines

Level of Maturity: 2

(2= Pilot exists / next step: demo or flagship plant)

Examples of on-going pilot/demo projects:

- ENI / UOP (Italy)

- Necton / Algafuel (Portugal)

- Biomara (UK)

- SBAE (Belgium)

- IGV (Germany)

- Algatec (Israel)

- Ingrepro (Netherlands / Malaysia)

- Clean Algae (Spain)

- BIOFAT (Portugal, Italy)

- InteSusAl (Portugal)

- All-Gas (Spain)

- MATGAS (Spain)

- Endesa (Spain)

- EcoAlga (Spain)

Flagship: None

Main technology challenges: Selection of strains, process design, water treatment, scale up

Technical challenges for all value chains: Feedstock flexibility, energy and carbon

efficiency, reliability & maintenance, capex efficiency

22

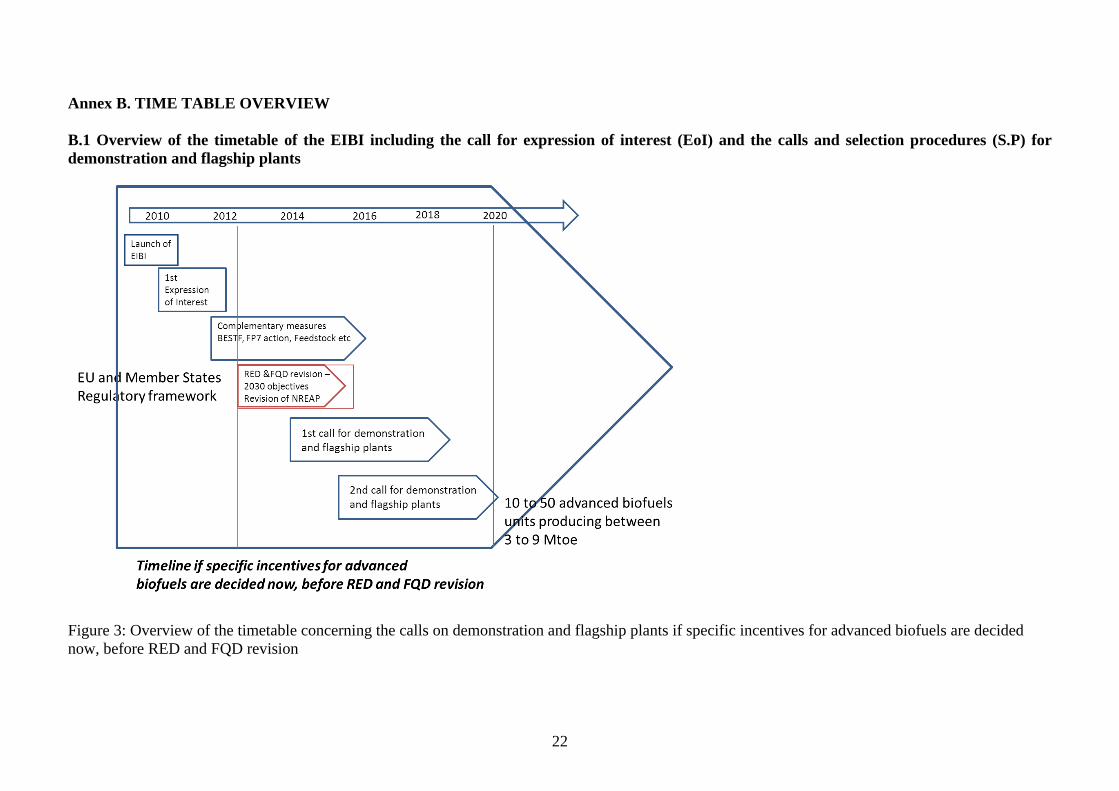

Annex B. TIME TABLE OVERVIEW

B.1 Overview of the timetable of the EIBI including the call for expression of interest (EoI) and the calls and selection procedures (S.P) for

demonstration and flagship plants

Figure 3: Overview of the timetable concerning the calls on demonstration and flagship plants if specific incentives for advanced biofuels are decided

now, before RED and FQD revision

23

Figure 4: Overview of the timetable concerning the calls on demonstration and flagship plants if investment decisions are delayed beyond the RED and

FQD revision

24

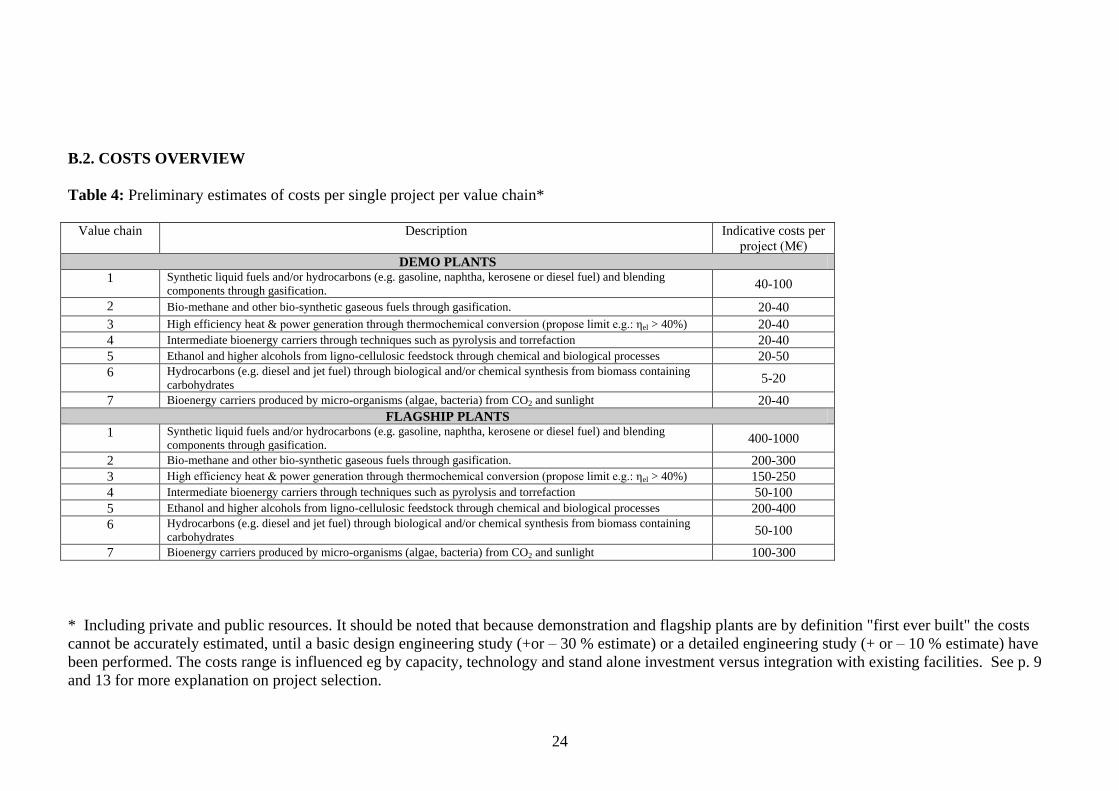

B.2. COSTS OVERVIEW

Table 4: Preliminary estimates of costs per single project per value chain*

Value chain Description Indicative costs per

project (M€)

DEMO PLANTS

1 Synthetic liquid fuels and/or hydrocarbons (e.g. gasoline, naphtha, kerosene or diesel fuel) and blending

components through gasification. 40-100

2 Bio-methane and other bio-synthetic gaseous fuels through gasification. 20-40

3 High efficiency heat & power generation through thermochemical conversion (propose limit e.g.: ηel > 40%) 20-40

4 Intermediate bioenergy carriers through techniques such as pyrolysis and torrefaction 20-40

5 Ethanol and higher alcohols from ligno-cellulosic feedstock through chemical and biological processes 20-50

6 Hydrocarbons (e.g. diesel and jet fuel) through biological and/or chemical synthesis from biomass containing

carbohydrates 5-20

7 Bioenergy carriers produced by micro-organisms (algae, bacteria) from CO2 and sunlight 20-40

FLAGSHIP PLANTS

1 Synthetic liquid fuels and/or hydrocarbons (e.g. gasoline, naphtha, kerosene or diesel fuel) and blending

components through gasification. 400-1000

2 Bio-methane and other bio-synthetic gaseous fuels through gasification. 200-300

3 High efficiency heat & power generation through thermochemical conversion (propose limit e.g.: ηel > 40%) 150-250

4 Intermediate bioenergy carriers through techniques such as pyrolysis and torrefaction 50-100

5 Ethanol and higher alcohols from ligno-cellulosic feedstock through chemical and biological processes 200-400

6 Hydrocarbons (e.g. diesel and jet fuel) through biological and/or chemical synthesis from biomass containing

carbohydrates 50-100

7 Bioenergy carriers produced by micro-organisms (algae, bacteria) from CO2 and sunlight 100-300

* Including private and public resources. It should be noted that because demonstration and flagship plants are by definition "first ever built" the costs

cannot be accurately estimated, until a basic design engineering study (+or – 30 % estimate) or a detailed engineering study (+ or – 10 % estimate) have

been performed. The costs range is influenced eg by capacity, technology and stand alone investment versus integration with existing facilities. See p. 9

and 13 for more explanation on project selection.

25

Annex C

EIBI Team Approved Version: 14-12-2011

EIBI

Key Performance Indicators

Draft working document – With proposed targets inserted

KPIs represent an essential toolkit for monitoring and reviewing the overall progress

of the EIBI, and of the individual research, development and demonstration (RDD)

activities performed in the frame of its implementation. KPIs will become

instrumental for planning RDD activities, funded under the current and up-coming

research and development programmes as well as other possible funding schemes that

will support the EIBI. More specifically, projects supporting implementation of the

EIBI will need to demonstrate the link between their objectives and the KPIs of the

EIBI to which they will contribute. As such, these projects will be integrated into the

Monitoring and Review Framework of the SET-Plan. The practicalities of this

exercise and the modus operandi, and particularly with reference to the later stages of

analysis of the data and their feeding into the technology-neutral planning toll of

SETIS, are still to be defined.

Drafting of the KPIs follows the principles established in the SET-Plan Information

System (SETIS), with both over-arching and specific key performance indicators

adapted to fit the needs of the bioenergy value chains identified by the EIBI. The KPIs

are compiled in parallel with the formulation of project eligibility criteria. It is clear

that implementation of the planning, monitoring and progress review in SETIS, based

on KPIs, first of all requires access to relevant and reliable data and the set-up of

monitoring and data feedback procedures. These procedures will be elaborated and

described in detail by the EIBI Team in the course of 2012.

Work on the development of KPIs is being carried out jointly by Commission staff

that represents SETIS, representatives of the European Biofuels Technology Platform

and representatives of the heat and power industrial sector. This document has been

compiled through input from a small Working Group comprising the following

members:

David Baxter (EC-JRC-IET), Mona-Maria Brinker (EBTP), Maria Georgiadou (EC-

RTD), Birger Kerckow (EBTP), Eva-Katrin Lindman (Euroheat & Power), Johan

Mogensen (Novozymes), Odile Pétillon (EADS), Philippe Schild (EC-RTD), Harri

Turpeinen (EBTP).

1. Over-arching KPIs

In many sectors bioenergy is used in direct competition with fossil energy and

transport fuels (energy carriers) and as such in most cases savings in greenhouse gas

26

(GHG) emissions are used as a comparator to assess “how good” bioenergy is in

terms of impact on the environment. Consequently, greenhouse gas (GHG) savings,

and the cost of achieving the savings, are an important indicator. The cost of

production of bioenergy or the energy-carrier product is also an important indicator,

although price to the customer on the market is ultimately the measure of economic

performance. (It is noted here that other EIIs, and the CCS EII in particular, use

Levelised Cost of Electricity and Cost of Avoided CO2 as KPIs, and if the EIBI Team

considers these measures appropriate, the same or similar methodologies could later

be incorporated into the EIBI KPIs.) In order to provide a measure of the performance

of the various bioenergy projects against the 2020 EU 20% target for renewable

energy, total bioenergy production from projects within the EIBI will also be

monitored. Hence, 3 over-arching KPIs are proposed:

Price before taxes24

of bioenergy products in 2020

(€/MWh) per value chain at point of sale to customer

(Annex I).

Targets for primary products:25 26

1. Synthetic liquid fuels by gasification: < 80 €/MWh

2. Biomethane (<= price as for natural gas) and other

synthetic gaseous fuels by gasification: (depends on

product, e.g. – DME <60 €/MWh), Hydrogen compressed

(<80 €/MWh ), CO (<30 €/MWh )

3, High efficiency heat and power by thermochemical

conversion: < 75€/MWh (el), <35 €/MWh (heat)

4. Intermediate bioenergy carriers: pyrolysis oil <50

€/MWh (to compete with Heavy Fuel Oil , but this depends

on actual product), torrefied product <30 €/MWh

5. Ethanol and higher alcohols from ligno-cellulosic

biomass by biological processes: <80 €/MWh (Note:

equates to <0,50 €/litre)

6. Hydrocarbons by biological processes and/or chemical

synthesis: < 80 €/MWh

7. Bioenergy carriers by micro-organisms (algae) from CO2

and sunlight: < 70 €/MWh for lipids (to be competitive

with vegetable oils and animal fats). Biomethane (<= price

as for natural gas)

GHG savings compared to fossil equivalents The GHG methodology and data behind the sustainability

scheme in the renewables directive (2009/28/EC) will be

24The purpose of this KPI is to give a rating for different technologies concerning their price

competitiveness, Hence this includes production, plus profit margin and relevant costs to point of sale

to a customer, and excludes product related taxes applied (e.g. VAT, excise duties and strategic

stockpile fee). 25 Energy content based on LHV 26 Reference is 2010 and based on an oil price of 86 USD/bbl: as appropriate, targets can be adjusted

with changes in the price of oil according to IEA

27

used as a reference for biofuels and bioliquids 27

.

Targets:

Biofuels – GHG savings from use of biofuels and

bioliquids shall be at least 60% (Reference: EU directive

2009/28/EC, production started on or after 1 January 2017

GHG savings). The methodology for calculation is given in

Annex V of directive 2009/28/EC.

For other energy products, reference data will be, as far as

available, obtained from recognised reference sources.

Targets:

For bioenergy products, other than biofuels and

bioliquids – while GHG savings are not yet defined in

directive 2009/28/EC, the Commission has indicated that in

the absence of specific targets, the targets set for biofuels

and bioliquids should be used (i.e. 60% according to RED)

and future agreed methodology will be adopted.

Total bioenergy produced by EIBI projects (TWh/year)

Targets:

2016: Intermediate step from 2012 to 2020 reflecting

maturity of first phase of demonstration projects (one

fourth of 2020 target)

2020: 35 TWh total energy from EIBI projects contribute to

the 20% renewables target; 17.5 TWh of the 10 %

renewable energy target for transportation will be reached

by advanced biofuels. The 17.5 TWh corresponds to 2 GW

installed capacity.

2. General KPIs for EIBI

Within each of the Value Chains, specific aspects of feedstock and/or processing

technologies are at different stages of development, some of them have attained the

pilot scale where their technical viability has been confirmed, while a few have

reached the demonstration phase and are being evaluated to ascertain their technical

reliability. None of the technologies in any of the Value Chains have reached the

flagship plant stage and consequently none have yet proven economic viability.

Some of the technologies that could be deployed in the 7 generic value chains are

already supported by actions at industrial, local, national and EC level and the

performance of those projects should be monitored. The general project KPIs are:

Number of Final Investment Decisions (FID) (i.e. approved projects of

Demonstration scale or Flagship scale) per value chain specified in the EIBI

27 One option would be to request information on the GHG savings and the methodology used in

obtaining the result

28

(See Bioenergy Roadmap)

Target: at least 1

Cumulative number of Final Investment Decisions (FID) (i.e. approved

projects of Flagship scale) based on technologies specified in the EIBI for all

value chains

Targets: at least 8

Gross installed output capacity of plants based on the EIBI value chains and

supported by the EIBI projects by 2020

Target: >2000 MW (total thermal capacity of all products)

Availability28

during agreed final period of project of demonstration/Flagship

plants in operation

Target: >95%

3. Project Specific KPIs:

To assess the progress of the portfolio of European projects and follow the success of

the value chains four types of KPIs are foreseen, Technology Specific, Resource

Specific, Health & Safety and Socio-Economic.

For the purpose of setting targets for the KPIs a cost base of 2010 has been assumed.

The price of oil will have a substantial impact on many costs in each of the value

chains and the cost base taken is $ 86 per barrel (IEA 2010).

It is noted that the “system boundary” for EIBI projects is defined as the plant gate as

the starting point, and the point at which the bioenergy product is sold to a customer

as a finished product (e.g. electricity or heat fed into a grid) or semi-finished product

(e.g. bio-oil for further refining) is the end point. Using this system boundary, costs

for conversion processes defined in the value chains are monitored. However, since

total costs of bioenergy products will also be (strongly) influenced by feedstock costs,

the latter will also be collected for policy monitoring purposes. It must be appreciated

that the cost of biomass feedstock paid by the conversion plant operator will depend

upon the state of the biomass delivered. The state of the biomass feedstock received,

whether wet (and needing to be dried), already dry, chipped, pelleted, torrefied, or in

the form of a bio-oil will have a significant effect on the cost of conversion and also

on the conversion efficiency of the process employed.

3.1 Technology-Specific

Plant at demonstration/flagship scale capable of achieving planned output

capacity during agreed final period of project (while meeting quality

28 Availability is defined as a percentage measure of the degree to which machinery and equipment is

in an operable and committable state at the point in time when it is needed; measured in hours per 8760

hours.

29

specifications of products29

, or meeting sales contract specifications)

Target: 100%

Plant at demonstration/flagship scale capable of product output at planned cost

Target: 100%

Greenhouse gas saving for each project compared with fossil fuel reference

Target: same as equivalent over-arching KPI

Net efficiency30

(based on LHV) of conversion of biomass feedstock from

plant gate to commercially marketable bioenergy product

Target: 75% (less than half of which is heat)

Capital intensity of the project (M€/MW)

Investment cost per unit of energy capacity (with allocation for fuel,

electricity, heat and co-products according to the proportion of the feedstock

used)

Value chain specific and for data collection purposes only, therefore no

targets

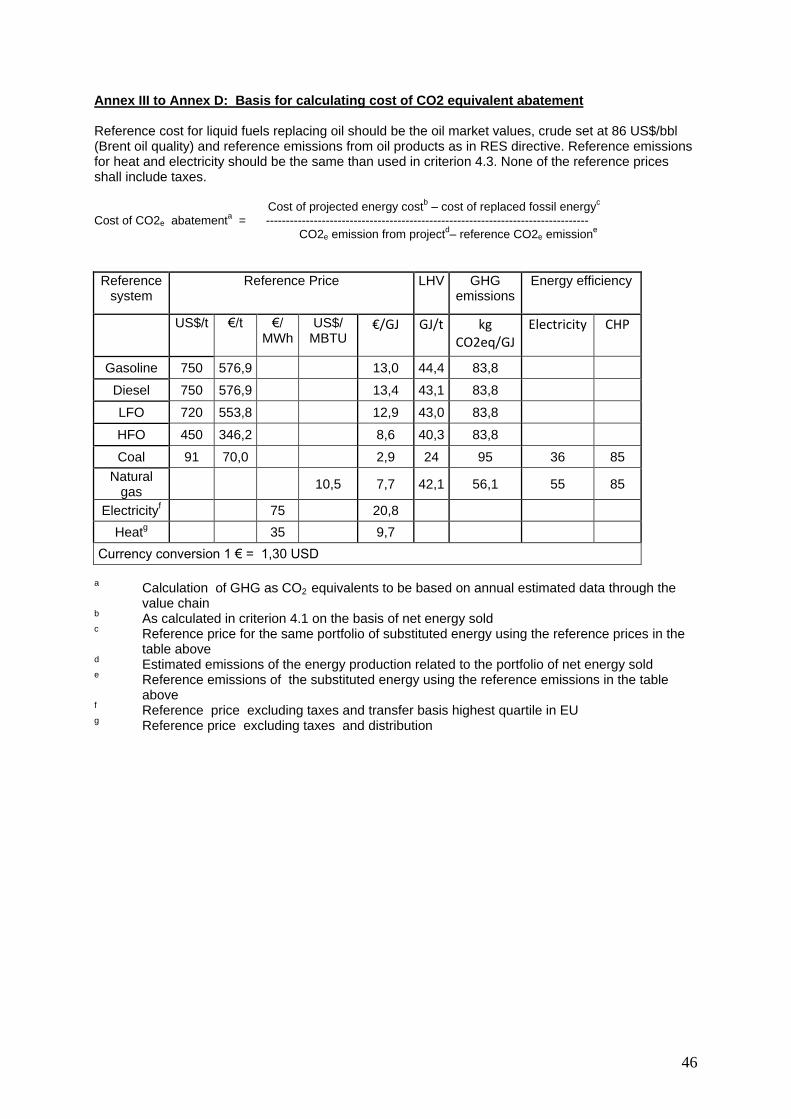

Cost per tonne of greenhouse gas saving (e.g. €/CO2 equivalent)

Target: dependent on technology (value chain). Refer to Eligibility Criteria

4.6 and Annex III

3.2 Resource-Specific

Cost of biomass resource delivered at the bioenergy plant gate

For data collection purposes only, therefore no targets

Price of biomass resource at farm, forest or market gate (while not in the

system boundary of the EIBI projects, this will indicate the intermediate costs

when taking into account the cost at the plant gate)

For data collection purposes only, therefore no targets

Annual quantity of biomass consumption by the project

Project specific and for data collection purposes only, therefore no targets

GHG emissions of value chain 7 (algae) “resource production to plant gate”

(e.g. CO2 equivalent per MWh biomass feedstock delivered)

Target: <108 kg/MWh.

29 Quality specifications may be CEN standards, CEN Workshop Agreements and in their absence

national or ISO standards 30 Net efficiency is the percentage of useful (commercially marketable bioenergy product) energy

output compared with the net sum of energy inputs (biomass and other energy inputs minus energy

content of commercially marketable non-energy bio-products)

30

3.3 Health, safety and environment

Number of deviations, license suspensions with respect to prevailing

emissions regulations along the whole value chain

Project specific and for data collection purposes only, therefore no targets

Number of accidents:

Targets: accidents <4; near-accidents31

<10

3.4 Socio-economic

Number of permanent jobs created by demonstration/flagship project,

including the plant itself and in the biomass supply and product chains (data

broken down indicating the location of the jobs, local, within a radius of 150

km, elsewhere in the EU).

Data collection purposes only, therefore no targets

4. Reporting

The practical implementation of the monitoring system requires a flow of information

from the projects to the EIBI Team and to SETIS. There are several steps in the

process with needs for input by various people:

o Data collection from EIBI projects and national projects - templates

will be used to satisfy the monitoring requirement of each of the KPIs

o Data checking, and when necessary verification, by the KPI

Monitoring Group (neutral experts) of the EIBI

o KPI Monitoring Group determines values for KPIs and reports to EIBI

Team

o Approved KPI data from EIBI reported to SETIS

o EIBI KPI Monitoring Group cooperation with SETIS on data

aggregation and reviewing of EIBI KPI data fed into the technology-

neutral planning tool of SETIS

o EIBI KPI Monitoring Group reports back to EIBI Team and the EIBI

Team reports back to projects

31 Computed as Lost Workday Injury Frequency (LWIF) of all workers (own staff and contractors),

where LWIF is calculated from the number of Lost Workday Injuries (LWI) divided by the number of

hours worked expressed in millions and as Total Recordable Case Frequency (TRCF). TRCF is

calculated from the sum of fatalities, LWIs, RWIs (Restricted Workday Injury) and MTC divided by

the number of hours worked in millions. These definitions are standard key performance indicators of

the oil industry sector, ref. CONCAWE Report 7/09 September 2009.

31

It is envisaged that data for KPIs would be collected periodically at maximum interval

of one year.

It is clearly the intention that all collected data are adequately protected and no

publication is allowed without the consent of the original project organisations.

The EIBI will follow guidance from SETIS on procedures for KPI reporting and any

other applicable data exchange.

The EIBI KPI Working Group will amend targets for demonstration/flagship projects

and on the data to be collected according to the needs defined by the EIBI Team. All

targets and methodologies need to be approved by the full EIBI Team.

32

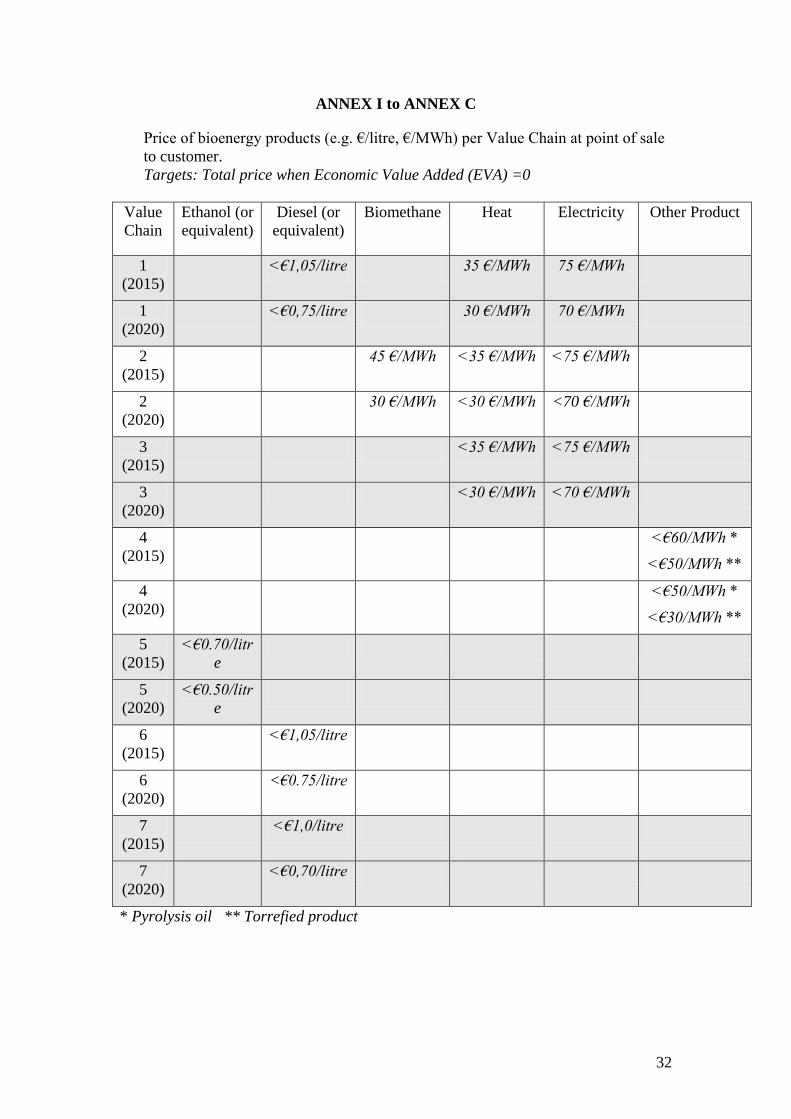

ANNEX I to ANNEX C

Price of bioenergy products (e.g. €/litre, €/MWh) per Value Chain at point of sale

to customer.

Targets: Total price when Economic Value Added (EVA) =0

Value

Chain

Ethanol (or

equivalent)

Diesel (or

equivalent)

Biomethane Heat Electricity Other Product

1

(2015)

<€1,05/litre 35 €/MWh 75 €/MWh

1

(2020)

<€0,75/litre 30 €/MWh 70 €/MWh

2

(2015)

45 €/MWh <35 €/MWh <75 €/MWh

2

(2020)

30 €/MWh <30 €/MWh <70 €/MWh

3

(2015)

<35 €/MWh <75 €/MWh

3

(2020)

<30 €/MWh <70 €/MWh

4

(2015)

<€60/MWh *

<€50/MWh **

4

(2020)

<€50/MWh *

<€30/MWh **

5

(2015)

<€0.70/litr

e

5

(2020)

<€0.50/litr

e

6

(2015)

<€1,05/litre

6

(2020)

<€0.75/litre

7

(2015)

<€1,0/litre

7

(2020)

<€0,70/litre

* Pyrolysis oil ** Torrefied product

33

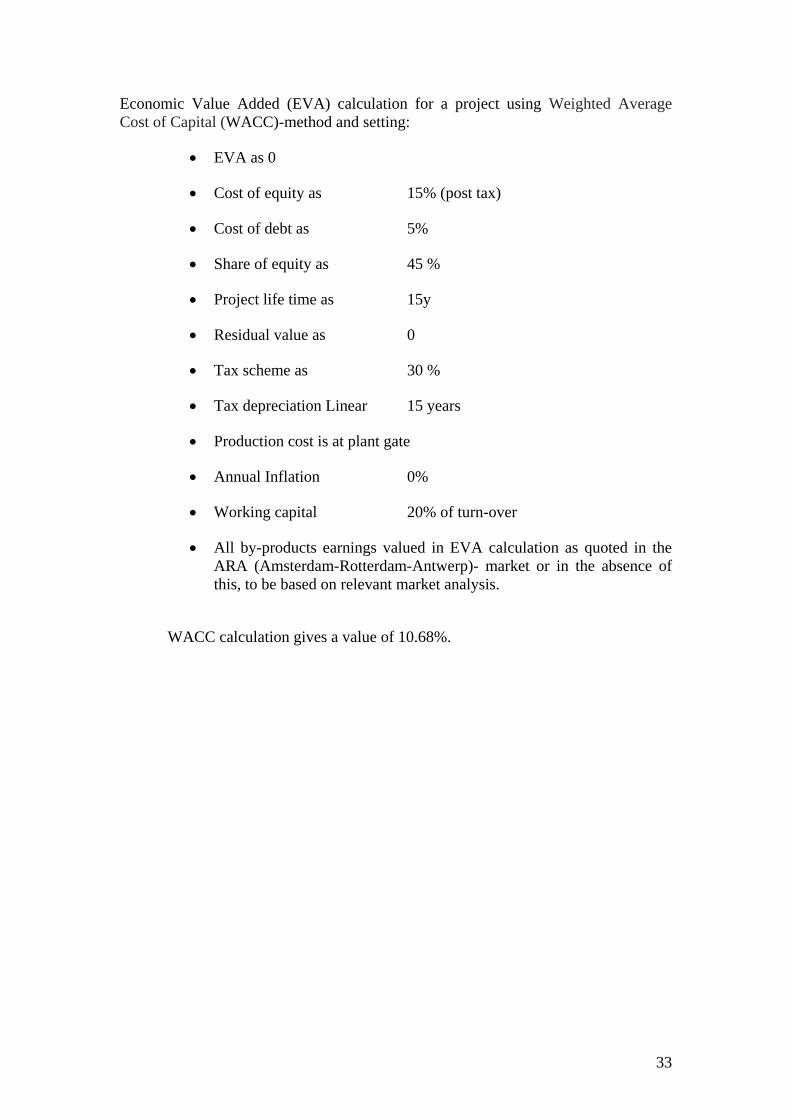

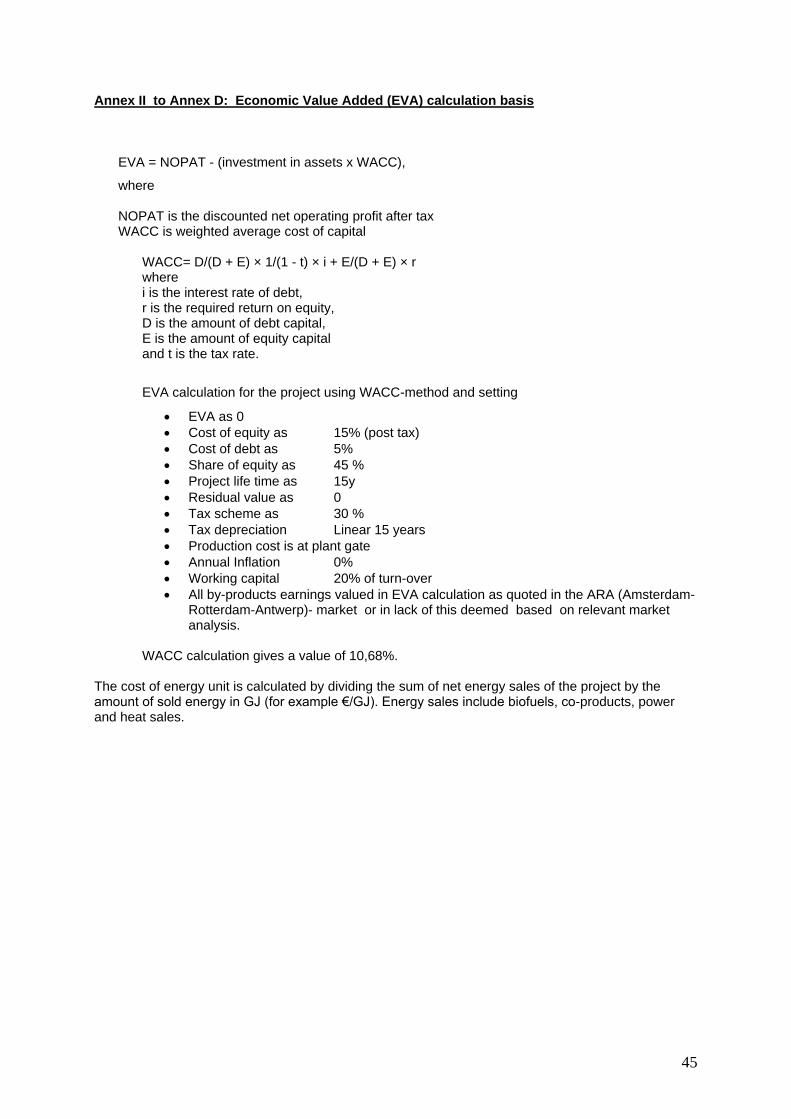

Economic Value Added (EVA) calculation for a project using Weighted Average

Cost of Capital (WACC)-method and setting:

EVA as 0

Cost of equity as 15% (post tax)

Cost of debt as 5%

Share of equity as 45 %

Project life time as 15y

Residual value as 0

Tax scheme as 30 %

Tax depreciation Linear 15 years

Production cost is at plant gate

Annual Inflation 0%

Working capital 20% of turn-over

All by-products earnings valued in EVA calculation as quoted in the

ARA (Amsterdam-Rotterdam-Antwerp)- market or in the absence of

this, to be based on relevant market analysis.

WACC calculation gives a value of 10.68%.

34

Annex D

Draft Project Eligibility and Selection Criteria for a European Industrial Bioenergy Initiative

Version 8, 11 October 2010

Draft working document Preamble The EIBI Project Eligibility and Selection Criteria have two basic objectives. First it aims to inform the future applicants on the main criteria that will be used by an independent team of experts to evaluate their projects, so that they can pay attention and put emphasis on the various issues that have to be addressed in detail in their applications. At the same time, it aims to provide the evaluation experts with an evaluation scoring template upon which the projects would be evaluated, by assigning a score per each individual evaluation criterion and adding up all the individual scores to determine the final project score. The evaluated projects will then be listed in terms of priority starting from the one of the highest score. The EIBI Project Eligibility Criteria consists of four Criteria. The first concern the administrative aspects of each application, which relate to whether the project can be admitted for evaluation, thus it addresses formal eligibility aspects. The second Criteria concern the overall aims and objectives of each project and whether these are within the overall aims and objectives of the EIBI, thus it addresses the compatibility of the project with EIBI. Finally the last two Criteria address respectively the overall project and overall technology objectives and how reliable, accurate, traceable and realistic the planning, the technical, environmental, economic and market assumptions made in the project are. The scoring of the project and technology Criteria is weighted in order to prioritise the most important criteria. Where necessary detailed formulas and tables with data for comparison have been provided in Annexes to create an equal level playing field for all applicants. 1. Administrative Requirements and Evaluation Procedure 1.1 Administrative Requirements A project will only be evaluated, if it meets all of the following conditions:

It is received by the "EIBI team" before the deadline given in the Terms of Reference (ToR) of the EIBI framework regarding Calls for Projects.

It involves at least the minimum number of participants given in the ToR of the EIBI framework regarding Calls for Projects.

It is complete (i.e. both the requested administrative forms and the project description are present). The projects will be submitted in PDF format.

The content of the project relates to the topic(s) and funding plan(s) (i.e. demonstration plants or flagship plants), including any special conditions given in the Terms of Reference (ToR) of the EIBI framework, described in the specific Calls for Projects.

1.2 Evaluation Procedure All projects are evaluated with the same set of criteria at two levels:

1.2.1. Eligibility step, with a go/no go to “selection” step outcome

35

1.2.2. Selection step, with a rating for ranking of projects

The Criteria 3 and 4 are to be used together for evaluating the projects. The weighting factors (0…10) in the right column of the tables are to be used as a multiplier when combining the individual criterion specific scores (scale 0…10) into an overall score for the project. Each of these Criteria provides a maximum of 500 weighted score points. Thresholds will be used as follows:

Individual criterion minimum score 5 (50%) Overall score minimum 350 weighted score points for each one of the

Criteria 3 and 4 (70%) and 700 weighted score points in total for both. Projects within a specific value chain are compared and selected. 2. Eligibility Evaluation Criteria 2.1. Relationship of a Project to EIBI At least 70% of the bioproducts produced by the plant shall be bioenergy (biofuels, heat, power) calculated on the basis of energy content of the products sold. 2.2. Technologies and Processes All projects must address innovative technologies and processes or novel integration of known technologies and processes to be established at the appropriate scale for first-of-its-kind

32 demonstration and flagship plants

33. At least one "section" of the value chain or the

integration of "sections" of the considered value chains should not have been deployed at demonstration / commercial scale before. 2.3. Feedstock, Renewable Energy Directive and Green House Gas emissions The projects have to be based on the conversion of biomass feedstocks for bioenergy (power, heat and biofuel), with full description of the feedstock supply chain, including feedstock production, logistics, and pre-treatment (if any). Projects addressing production of bio-products as a co-product to bioenergy as well as projects addressing co-processing of the biomass feedstocks with fossil fuels are also eligible. All projects, including power and heat generation, must comply with the sustainability criteria specified in the EU Renewable Energy Directive (RED 2009/28/EC, article 17) and meet the specified minimum Green House Gas (GHG) criteria for the year 2016; being 60 % deducted from Life Cycle Analysis (LCA)

34 and

based on RED calculation. 2.4. Site and Minimum Consortia Requirements The site of the demonstration plants or flagship plants must be in the EU or in the FP Associated Countries

35. To ensure an EU industrial dimension the projects will be based on

32

First-of-its-kind: projects concentrating on novel technologies and processes, and not replicating existing installations 33

Demonstration plants normally follow pilot-scale projects. They are considered the last non-economic step to demonstrate the technical, environmental and economical performance and reliability of all critical steps in a value chain so that the first commercial unit can be designed and the technical performance guaranteed from the outcome of the demonstration unit. Demonstration applies to processes that have been successfully tested at least at pilot scale. Flagship plants normally follow demonstration projects. They are the first commercial units of value chains operating at an economically viable scale 34

ILCD Handbook: General guide for Life Cycle Assessment – Provisions and action steps http://lct.jrc.ec.europa.eu/pdf-directory/ILCD-Handbook-General-guide-for-LCA-PROVISIONS-online-12March2010.pdf 35

Current, FP7, Associated Countries: Norway, Switzerland, Turkey, Israel, Albania, Bosnia and Herzegovina, Croatia, Faroe Islands, FYR Macedonia, Iceland, Liechtenstein, Montenegro, Serbia

36

consortia consisting from at least 3 organisations established in different EU Member States or in 2 different EU Member States and 1 Associated Country. At least 2 of the 3 minimum required organisations must be industrial actors and 1 must be a Science &Technology actor.

37

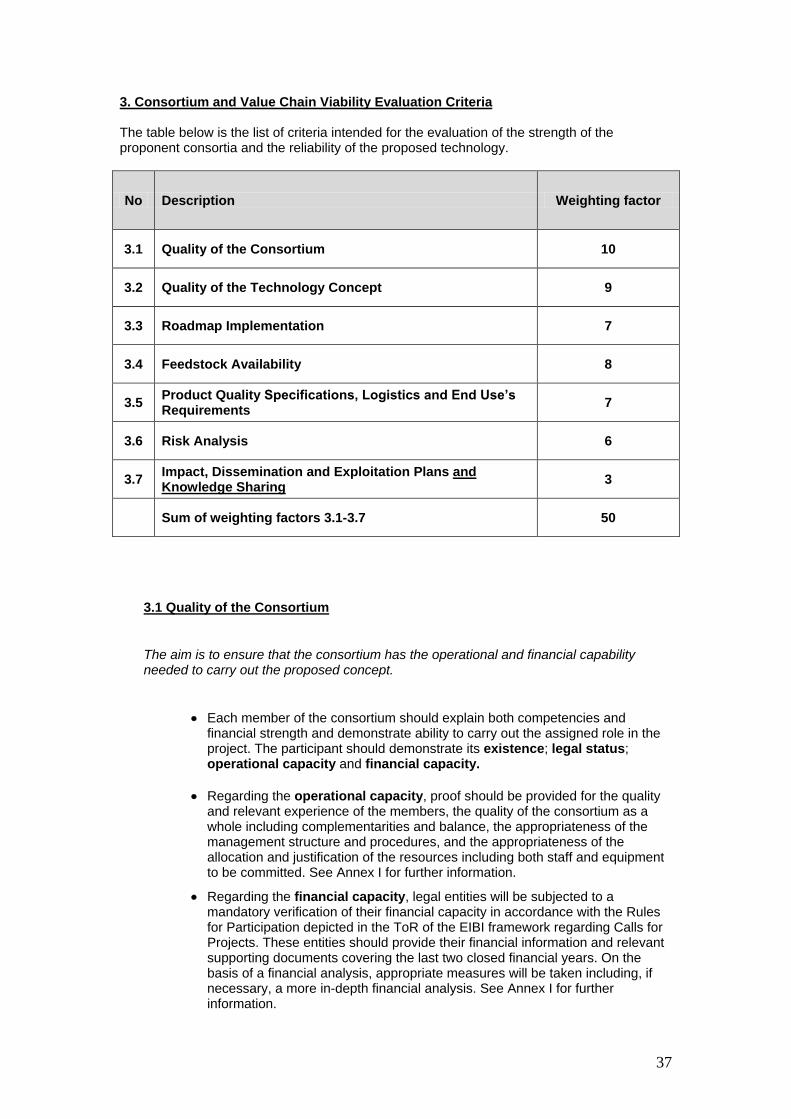

3. Consortium and Value Chain Viability Evaluation Criteria The table below is the list of criteria intended for the evaluation of the strength of the proponent consortia and the reliability of the proposed technology.

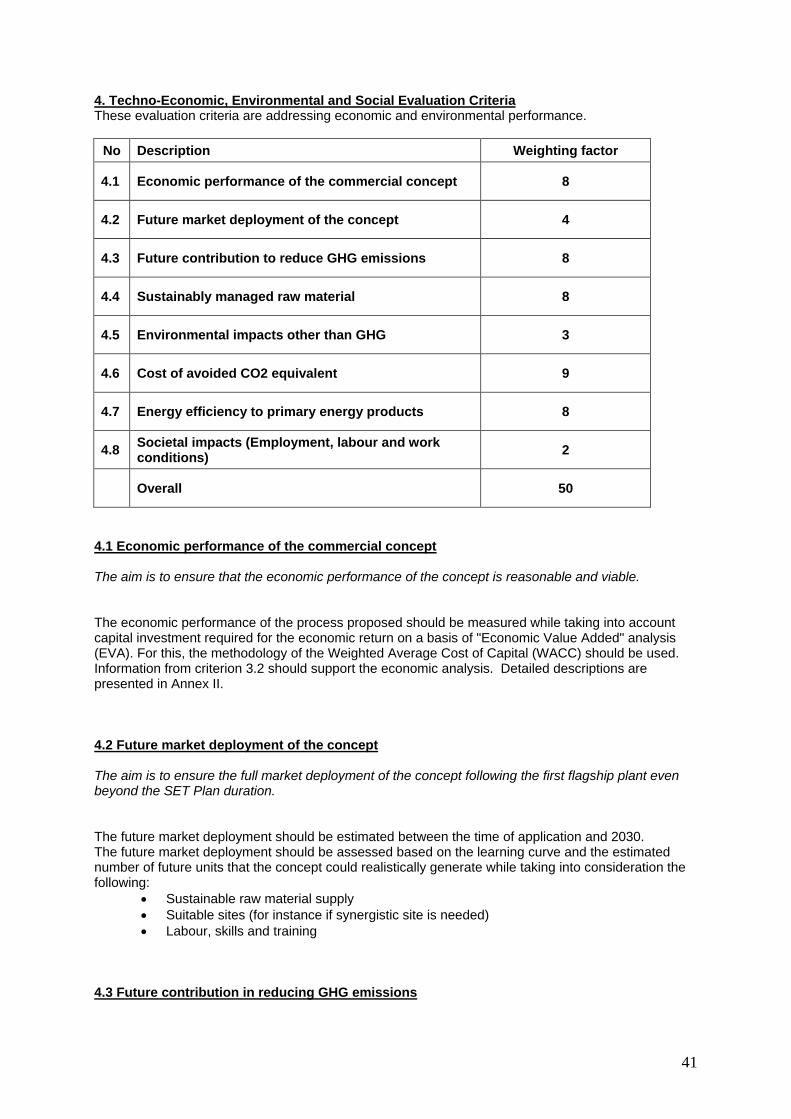

No Description Weighting factor

3.1 Quality of the Consortium 10

3.2 Quality of the Technology Concept 9

3.3 Roadmap Implementation 7

3.4 Feedstock Availability 8

3.5 Product Quality Specifications, Logistics and End Use’s Requirements

7

3.6 Risk Analysis 6

3.7 Impact, Dissemination and Exploitation Plans and Knowledge Sharing

3

Sum of weighting factors 3.1-3.7 50

3.1 Quality of the Consortium

The aim is to ensure that the consortium has the operational and financial capability needed to carry out the proposed concept.

Each member of the consortium should explain both competencies and financial strength and demonstrate ability to carry out the assigned role in the project. The participant should demonstrate its existence; legal status; operational capacity and financial capacity.

Regarding the operational capacity, proof should be provided for the quality and relevant experience of the members, the quality of the consortium as a whole including complementarities and balance, the appropriateness of the management structure and procedures, and the appropriateness of the allocation and justification of the resources including both staff and equipment to be committed. See Annex I for further information.

Regarding the financial capacity, legal entities will be subjected to a mandatory verification of their financial capacity in accordance with the Rules for Participation depicted in the ToR of the EIBI framework regarding Calls for Projects. These entities should provide their financial information and relevant supporting documents covering the last two closed financial years. On the basis of a financial analysis, appropriate measures will be taken including, if necessary, a more in-depth financial analysis. See Annex I for further information.

38

3.2 Quality of the Technology Concept

The aim is to ensure that a reliable technological concept is proposed in terms of techno-economic and environmental performance as well as in terms of working methodology and organisation.

An organised and hierarchical representation of all the work to be carried out in the project must be provided, broken down into sufficient detail to back up planning, assignment of proposed effort and costs, progress monitoring and control. (a detailed work plan, broken down into work clusters each encompassing identified deliverables and tasks. The work plan should follow the logical phases of the project implementation and portray specific milestones and a summary of efforts and costs

Illustration of the interdependencies between the components of the work clusters in terms of a graphic representation , e.g. Pert diagram or similar

Illustration of the planned timing of the work clusters and their components in terms of a graphic representation, e.g. GANTT chart or similar. The aim is to ensure that the technical objectives are followed but also that the project is completed within the approved budget and time.