european long-term growth and the euro crisis uri dadush new york university, stern school of...

TRANSCRIPT

European Long-Term Growth and the Euro Crisis

Uri Dadush

New York University, Stern School of Business

October 8, 2010

1

Main Points

• Aborted Long-Term Catch-Up

• Big Hit From the Great Recession

• Euro Crisis Far From Over

• Potential Growth Drivers Remain

2

Europe Compared

2009 Per Capita GDP

PPP, 2005 dollars

* EU12 (excludes Luxembourg): Belgium, Denmark, France, Germany, Greece, Ireland, Italy, Netherlands, Portugal, Spain, United Kingdom.Source: World Bank.

0

5000

10000

15000

20000

25000

30000

35000

40000

45000

UnitedStates

EU12*Average

Japan Russia Brazil China India

3

100

1000

10000

100000

1820 1840 1860 1880 1900 1920 1940 1960 1980 2000

Europe*

United States

Aborted Catch-UpPer Capita GDP

1990 GK dollars, logarithmic scale

* Austria, Belgium, Denmark, Finland, France, Germany, Italy, Netherlands, Norway, Sweden, Switzerland, United Kingdom.

Sources: Maddison (2006), World Bank.

4

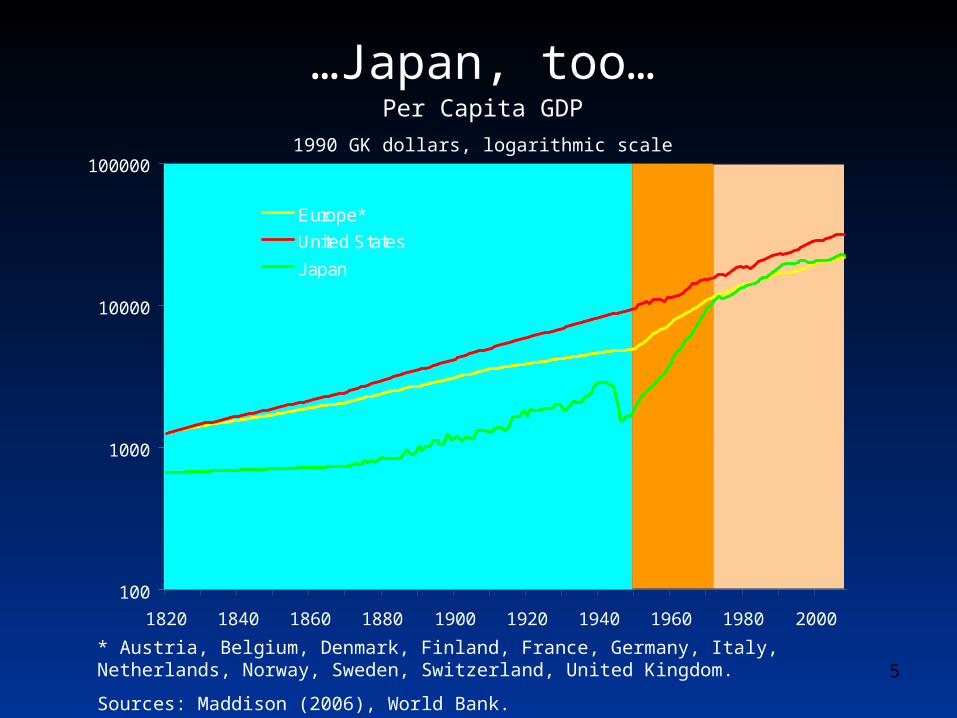

…Japan, too…Per Capita GDP

1990 GK dollars, logarithmic scale

* Austria, Belgium, Denmark, Finland, France, Germany, Italy, Netherlands, Norway, Sweden, Switzerland, United Kingdom.

Sources: Maddison (2006), World Bank.

100

1000

10000

100000

1820 1840 1860 1880 1900 1920 1940 1960 1980 2000

Europe*

United States

Japan

5

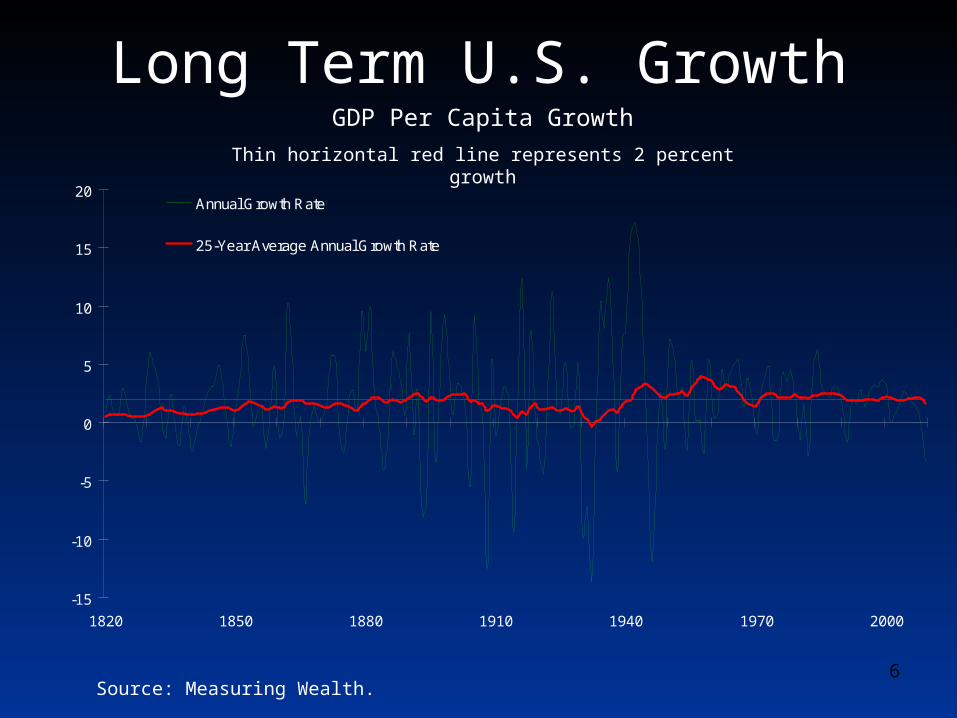

Long Term U.S. GrowthGDP Per Capita Growth

Thin horizontal red line represents 2 percent growth

Source: Measuring Wealth.

-15

-10

-5

0

5

10

15

20

1820 1850 1880 1910 1940 1970 2000

Annual Growth Rate

25-Year Average Annual Growth Rate

6

The Income Gap

Ratio of Europe* to the United States

0.4

0.6

0.8

1

1820 1840 1860 1880 1900 1920 1940 1960 1980 2000

Output per Capita

* Austria, Belgium, Denmark, Finland, France, Germany, Italy, Netherlands, Norway, Sweden, Switzerland, United Kingdom.

Sources: Maddison (2006), OECD, World Bank.7

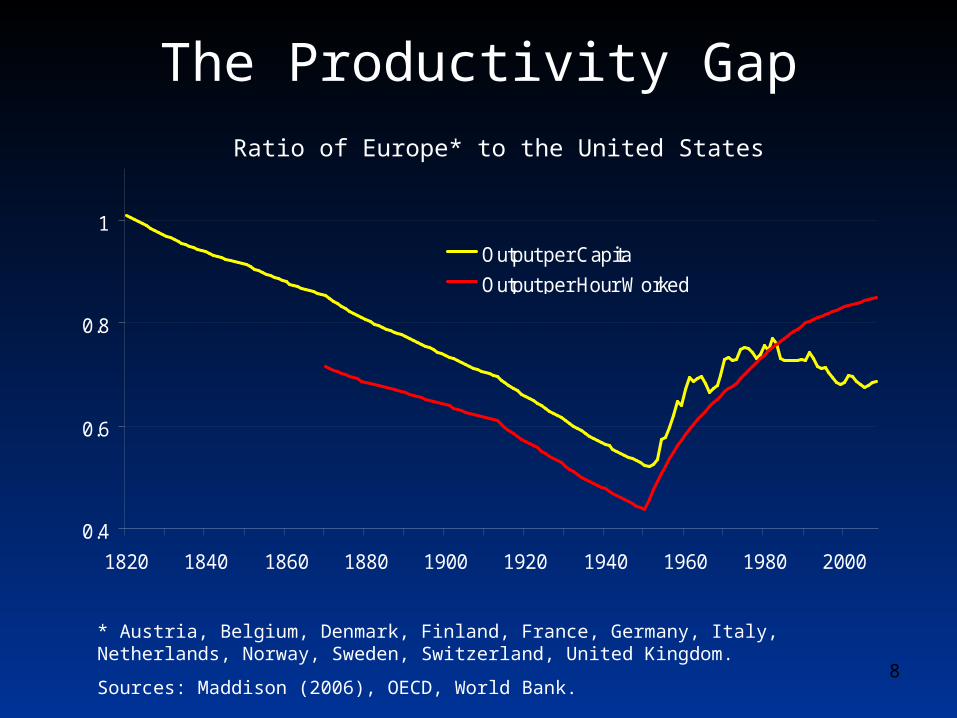

The Productivity Gap

Ratio of Europe* to the United States

0.4

0.6

0.8

1

1820 1840 1860 1880 1900 1920 1940 1960 1980 2000

Output per Capita

Output per Hour Worked

* Austria, Belgium, Denmark, Finland, France, Germany, Italy, Netherlands, Norway, Sweden, Switzerland, United Kingdom.

Sources: Maddison (2006), OECD, World Bank.8

The Lisbon AgendaEnacted in 2000 to transform Europe into “the most

dynamic and competitive knowledge-based economy in the world” by 2010.

• Objectives: • 70 percent of the working-age population employed• 3 percent of GDP spent on R&D• Environmental and social objectives

• Outcomes:• In 2009, 69.1 percent of the working-age population employed (71.3

percent in United States)• In 2008, 1.9 percent of GDP spend on R&D (2.8 percent in United

States)• Many environmental and social targets dropped in 2004

9

-6

-5

-4

-3

-2

-1

0

1

Q1 '08 Q2 '08 Q3 '08 Q4 '08 Q1 '09 Q2 '09 Q3 '09 Q4 '09 Q1 '10 Q2 '10

Euro area

United States

Big Hit From The Great Recession

Percent Change in GDP since 2008

Sources: Eurostat, BEA. 10

Interest Rate ConvergenceAnnual Inflation Rates and Long-Term Government Bond Yields

Average aggregate rate, percent

* Austria, Belgium, France, Germany, Netherlands.

Sources: IMF.

0

5

10

15

20

25

1980 1985 1990 1995 2000 2005

GIIPS Core*

GIIPS Core*

Bond Yield:Inflation:

11

-30

-20

-10

0

10

20

30

40

Ireland Italy Spain Greece Portugal Germany UK UnitedStates

CompetitivenessChange in Real Effective Exchange Rates, 2000-2008

Based on unit labor cost, relative to the EU and other major industrialized economies

Sources: European Commission. 12

..Not Just The Euro Area…Change in Unit Labor Cost

In euros, 2004-2008

* Austria, Belgium, France, Germany, Netherlands.

Sources: IMF.

-20%

0%

20%

40%

60%

80%

100%

Latvia Romania Estonia Lithuania Bulgaria Poland CzechRepublic

Hungary Germany

Peggers

Floaters

13

Governments GrewAverage Annual Growth of Government Expenditure

Percent, 1997-2007

Source: Eurostat.

0

2

4

6

8

10

12

14

Tough Deficit TargetsGovernment Deficit Projections

Percent of GDP

Note: Projections for Spain are for 2013; projections for Italy are for 2012. Sources: 2010 IMF Stand-by Arrangement Review (Greece), 2010 IMF Article IV Consultation (Spain, Italy, Ireland).

-15

-10

-5

0

Greece Spain Italy Ireland

2009 2010 2014 - Official forecast

15

Unrealistic?Government Deficit Projections

Percent of GDP

Note: IMF and official forecasts for 2010 are nearly identical. Greece, which accepted IMF support in May, does not provide official forecasts independent of the IMF. Projections for Spain are for 2013; projections for Italy are for 2012. Sources: 2010 IMF Stand-by Arrangement Review (Greece), 2010 IMF Article IV Consultation (Spain, Italy, Ireland).

-15

-10

-5

0

Greece Spain Italy Ireland

2009 2010

2014 - IMF forecast 2014 - Official forecast

16

Two-Speed Europe

Source: Eurostat.

Percent Change in GDP since 2003

0

2

4

6

8

10

12

2003

2004

2005

2006

2007

2008

2009

2010

Core

GIIPS

17

Adjustment Thus FarCore Prices

Percentage points above Germany since 2001

Source: Eurostat.

0

5

10

15

20

25

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Greece

Spain

Italy

Portugal

Ireland

18

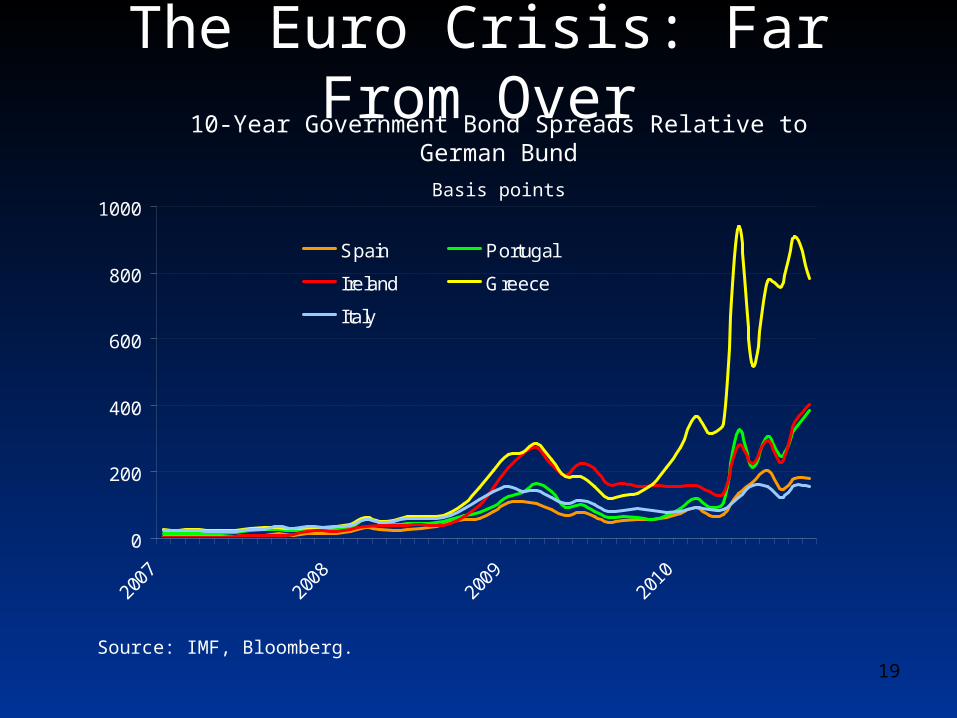

The Euro Crisis: Far From Over10-Year Government Bond Spreads Relative to German Bund

Basis points

Source: IMF, Bloomberg.

0

200

400

600

800

1000

2007

2008

2009

2010

Spain Portugal

Ireland Greece

Italy

19

Debt Levels: U.S. is Worse

Debt as a Percent of GDP

2007 2009 2015

United States 62.1 83.2 109.7

Japan 187.7 217.7 250

Germany 65 72.5 81.5

France 63.8 77.4 94.8

United Kingdom 44.1 68.2 90.6

Greece 95.6 114.7 158.6

Ireland 24.9 64.5 94

Italy 103.4 115.8 124.7

Portugal 63.6 77.1 68.4

Spain 36.1 55.2 94.4

Source: IMF 20

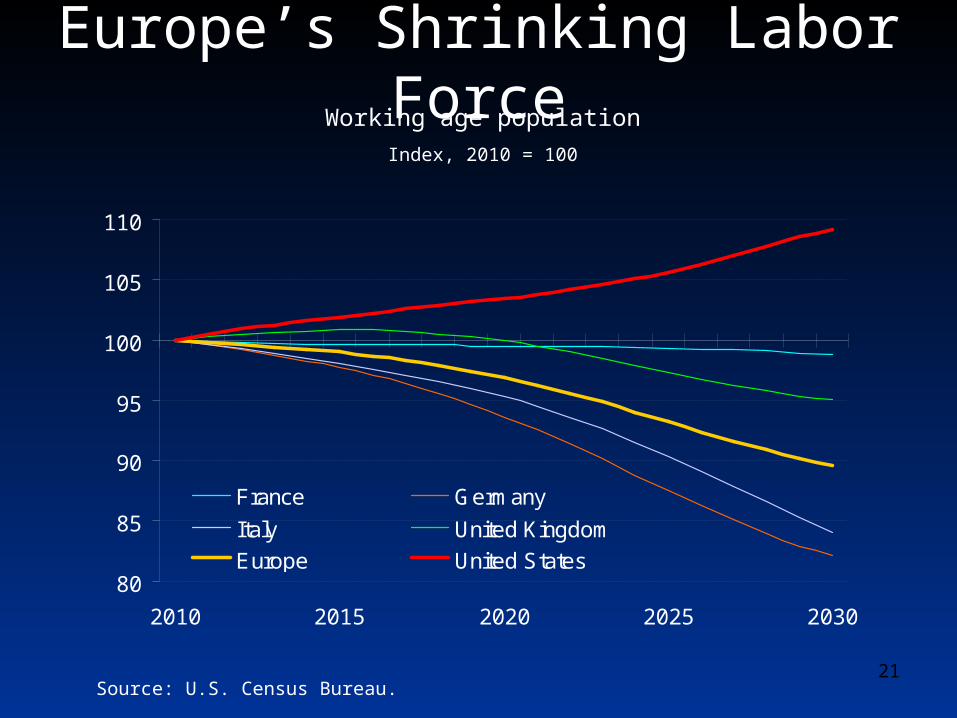

Europe’s Shrinking Labor ForceWorking age population

Index, 2010 = 100

Source: U.S. Census Bureau.

80

85

90

95

100

105

110

2010 2015 2020 2025 2030

France Germany

Italy United Kingdom

Europe United States

21

Convergence Conditions in PlaceIndex of Technological Catch-Up Conditions

0 denotes slowest convergence to the United States, 10 denotes fastest convergence

Note: The index above is an aggregate of indices that measure the following factors: educational attainment, communication and transportation infrastructure, governance, and business and investment environment. The United States has been omitted; the U.S. index score is 10.Source: World Bank World Development Indicators (2009), authors' calculation.

0

1

2

3

4

5

6

7

8

9

10

Uni

ted

Kin

gdom

Can

ada

Ger

man

y

Aus

tral

ia

Japa

n

Fra

nce

Kor

ea

Italy

Sau

di A

rabi

a

Sou

th A

fric

a

Mex

ico

Tur

key

Chi

na

Rus

sia

Arg

entin

a

Bra

zil

Gha

na

Indo

nesi

a

Indi

a

Ken

ya

Eth

iopi

a

Nig

eria

22

Incomes Rising GraduallyAnnual GDP Per Capita Growth, 2010 – 2030

PPP, percent change

Source: “The World Order in 2050”.

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

United Kingdom France United States Italy Germany

23

Potential Growth Drivers• ICT

• United States spent an average of 67 percent more per capita on ICT from 2003 to 2009.

• Emerging Markets• European merchandise exports to emerging markets average 5.3 percent of

GDP, compared to 2.5 percent in the United States.

• Further Integration • Average PPP per capita GDP in richest three EU economies is over three

times that of poorest three EU economies.

• Labor Market Reforms• On average, EU countries rank 40th out of 183 countries in ease of doing

business, but 104th in hiring employees.

24