european online travel agencies: phocuswright · phocuswright written by carroll rheem edited by...

TRANSCRIPT

MARKET RESEARCH • INDUSTRY INTELLIGENCE

PhoCusWrightWritten by Carroll Rheem

Edited by Lorraine Sileo

Sponsored by:

European Online Travel Agencies:Success Strategies for Today and Tomorrow

European Online Travel Agencies: Success Strategies for Today and Tomorrow June 2009

2©2009 PhoCusWright Inc. All Rights Reserved

Author: Carroll Rheem

Editor: Lorraine Sileo

Carroll Rheem Director, Research PhoCusWright, Inc.

Ms. Rheem contributes in-depth market reports, survey findings, and analysis for PhoCusWright’s Global and European Edition Research Subscription, Special Reports and custom client needs in her role as director, research. As the author of PhoCusWright’s Consumer Travel Report and Going Green: The Business Impact of Environmental Awareness on Travel, one of her core areas of focus is consumer research. Carroll also leverages her experience in hotel distribution for publications including PhoCusWright’s U.S. Online Travel Overview, and oversees content for the PhoCusWright Research Subscription: European Edition. Prior to joining the team, Carroll spent six years working for Starwood Hotels and Resorts Worldwide in various positions encompassing hotel operations, sales and global online distribution. She holds a Master of Management in Hospitality from Cornell University and a BA in Economics from New York University.

All PhoCusWright Inc. publications are protected by copyright. It is illegal under U.S. federal law (17USC101 et seq.) to copy, fax or electronically distribute copyrighted material beyond the parameters of the Licence or outside of your organisation without explicit permission.

Philip C. Wolf

President and CEO

Carol Hutzelman

Senior Vice President

Christine Lent

Vice President, Finance and Administration

Bruce Rosard

Vice President, Sales and Marketing

Lorraine Sileo

Vice President, Research

European Online Travel Agencies: Success Strategies for Today and Tomorrow June 2009

3©2009 PhoCusWright Inc. All Rights Reserved

Table of Contents

Figure 1 6Online Travel Agency and Supplier Web Site Share of Online Leisure/Unmanaged Business Travel Market Gross Bookings, 2008*

Figure 2 7Top Five Pan-European Online Travel Agencies,Market Shares, 2007

Figure 2a 8European Online Travel Agencies Estimated GrossBookings and Share (€M), 2006-2007

Figure 3 9Share of Total Leisure Travel Expenditure by Component

Figure 4 10Leisure Travel Destination Regional Distribution, by Country

Figure 5 13Usual Shopping and Purchase Methods

Figure 6 14Primary Reason for Choosing Usual Purchase Channel

Figure 7 15Incidence of Shopping for Travel from an Online Travel Agency but Purchasing Elsewhere, by Country

Figure 8 17Social Media

Figure 9 18Social Media

Section One: Key Findings, Overview and Methodology 4

Section Two: European Market Overview 6

Section Three: Travel Component Dynamics 9

Section Four: Shopping and Purchase Channel Trends 13

Section Five: Marketing Trends 17

Conclusion: Strategies Shaping the Future Success of Online Travel Agencies 19

Contents List of Figures

European Online Travel Agencies: Success Strategies for Today and Tomorrow June 2009

4©2009 PhoCusWright Inc. All Rights Reserved

Key Findings

• Online travel agencies (OTAs) areestimated to have reached €21 billion in 2008 gross bookings, reflecting 31% share of the online leisure and unmanaged business travel market.

• A major issue shaping European OTAair product strategy is access to content. Many OTAs use a multi-source strategy to mitigate some of the potential risks, such as working with multiple content providers and aggregators or building XML feeds to incorporate charter air product. Many OTAs are also adding additional products (i.e., destination activities, leisure packages, insurance) to enrich their content offerings.

• OTAs rank as the fourth most popularshopping channel at 15%, according to PhoCusWright’s European Consumer Travel Trends Survey2. Many European OTAs have adapted to the European traveller’s multi-channel mentality by offering their customers several ways of interacting with them, with some even incorporating physical locations.

• OTAs are focusing on price for goodreason. When consumers were asked why they chose their usual purchase channel, price was the most common response at 40%.

• Many European OTAs are in the midstof testing media products to build incremental revenue. While much uncertainty remains about the viability of various media programmes, the industry will witness a great deal of experimentation over the next several years as OTAs try to better monetise their traffic.

• European OTAs are adopting a widerange of strategies to improve their market positioning going forward. These include diversification of outlets, building mobile applications, market expansion and partnering with metasearch brands.

Overview

A decade has passed since the first European companies began to harness the power of the Internet for the sale of travel. Many things have changed over the past 10 years, but many familiar challenges remain. European online travel agencies are continually pressured to introduce new products and functionality to evolve the way consumers plan and purchase travel. Meanwhile, they must find new ways to compete against a powerful traditional distribution network that includes mega retail travel agencies and tour operators, as well as aggressive supplier disintermediation efforts and up-and-comers like metasearch.

European Online Travel Agencies: Success Strategies for Today and Tomorrow examines some of the most important trends shaping European online travel and how OTAs are driving success in a fiercely competitive environment. Not all OTAs follow the same rules, nor should they. Distinctive markets, diverse consumer audiences, and varied products all call for unique strategies. Based on a set of interviews with European executives, PhoCusWright reviews a range of successful strategies from OTAs large and small, global and local to summarise what they are doing to give themselves an edge today and tomorrow.

Section One: Key Findings, Overview and Methodology

2 Respondents may have used search engines to get the OTA url

European Online Travel Agencies: Success Strategies for Today and Tomorrow June 2009

5©2009 PhoCusWright Inc. All Rights Reserved

Methodology

PhoCusWright interviewed executives from a range of top European online travel agencies reflecting a mix of global, regional and local in May 2009. Executives were asked about their business goals, strategies, challenges and investments. PhoCusWright combines this research with findings from PhoCusWright’s European Online Travel Overview Fourth Edition and preliminary findings of the European Online Travel Overview Fifth Edition, which chronicles all segments of the European online travel industry by market.

To provide a consumer perspective, PhoCusWright also includes information from PhoCusWright’s European Consumer Travel Trends Survey. The survey was conducted by FieldWorks in 1Q08 in tandem with online panel company Research Now in four European countries - Great Britain, France Germany and Spain - with each country represented equally among 1,630 online travellers.

Respondents completed the survey via the Internet, and thus it is assumed they had Internet access. In addition, to qualify for participation, all respondents had to be 18 years or older, have taken a trip in the last 12 months by commercial airline, charter airline or rail for business or leisure (other than routine commuting), and have stayed at a hotel, motel or other paid accommodation (e.g., B&B) for leisure travel in the past 12 months. The survey averaged 18 minutes in length and was translated into the country’s native language for the three non-English speaking regions. The margin of error on the total sample was +/- 2.5% (by country: +/- 4.8%).

European Online Travel Agencies: Success Strategies for Today and Tomorrow June 2009

6©2009 PhoCusWright Inc. All Rights Reserved

Section Two: European Market Overview

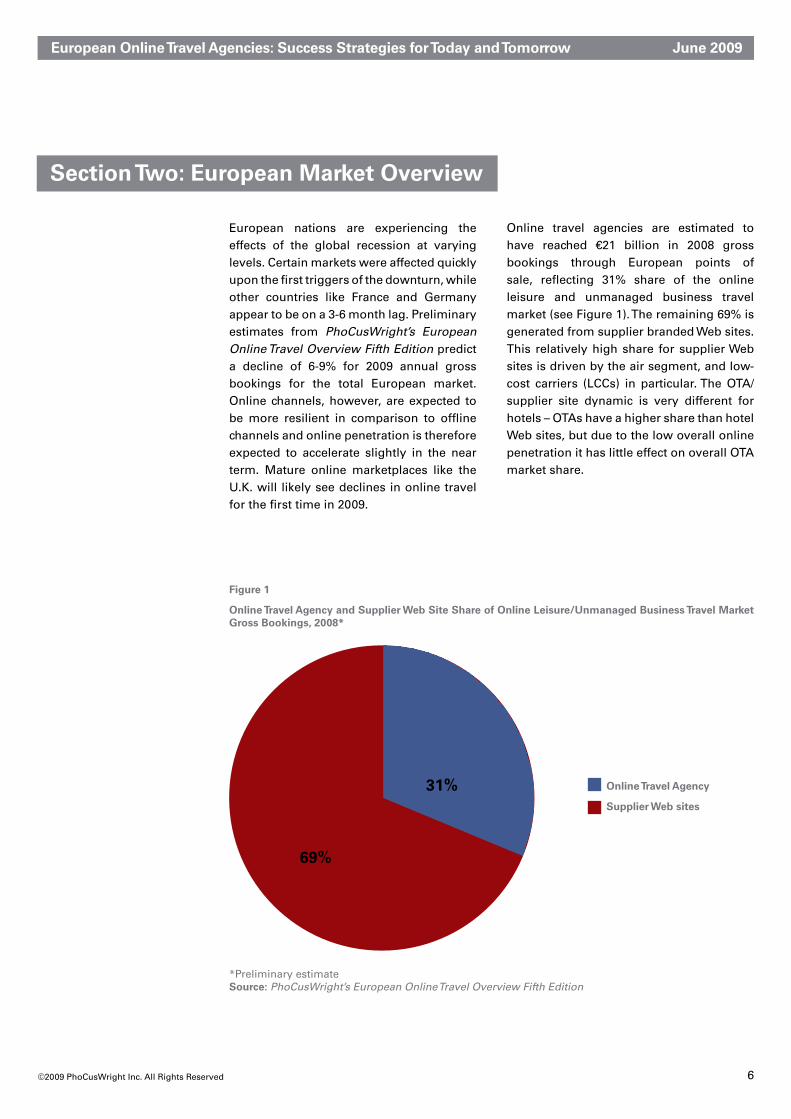

European nations are experiencing the effects of the global recession at varying levels. Certain markets were affected quickly upon the first triggers of the downturn, while other countries like France and Germany appear to be on a 3-6 month lag. Preliminary estimates from PhoCusWright’s European Online Travel Overview Fifth Edition predict a decline of 6-9% for 2009 annual gross bookings for the total European market. Online channels, however, are expected to be more resilient in comparison to offline channels and online penetration is therefore expected to accelerate slightly in the near term. Mature online marketplaces like the U.K. will likely see declines in online travel for the first time in 2009.

Online travel agencies are estimated to have reached €21 billion in 2008 gross bookings through European points of sale, reflecting 31% share of the online leisure and unmanaged business travel market (see Figure 1). The remaining 69% is generated from supplier branded Web sites. This relatively high share for supplier Web sites is driven by the air segment, and low-cost carriers (LCCs) in particular. The OTA/supplier site dynamic is very different for hotels – OTAs have a higher share than hotel Web sites, but due to the low overall online penetration it has little effect on overall OTA market share.

Figure 1

Online Travel Agency and Supplier Web Site Share of Online Leisure/Unmanaged Business Travel Market Gross Bookings, 2008*

*Preliminary estimateSource: PhoCusWright’s European Online Travel Overview Fifth Edition

Online Travel Agency

Supplier Web sites

31%

69%

European Online Travel Agencies: Success Strategies for Today and Tomorrow June 2009

7©2009 PhoCusWright Inc. All Rights Reserved

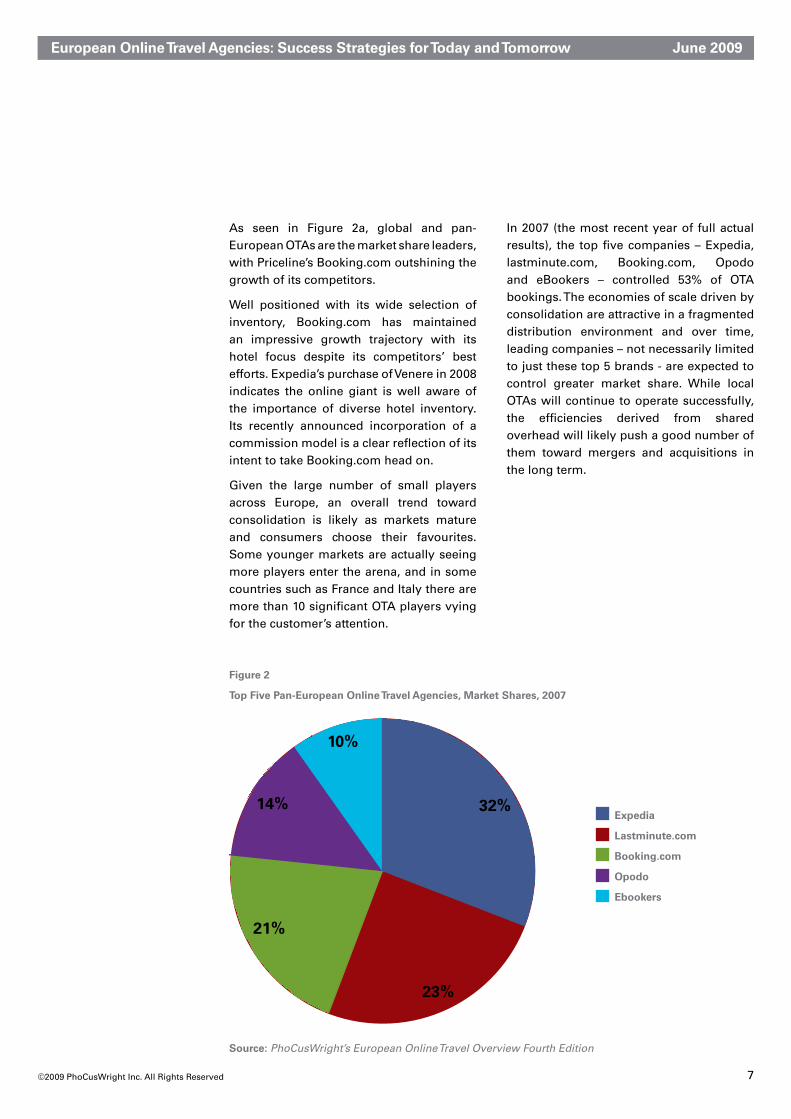

As seen in Figure 2a, global and pan- European OTAs are the market share leaders, with Priceline’s Booking.com outshining the growth of its competitors.

Well positioned with its wide selection of inventory, Booking.com has maintained an impressive growth trajectory with its hotel focus despite its competitors’ best efforts. Expedia’s purchase of Venere in 2008 indicates the online giant is well aware of the importance of diverse hotel inventory. Its recently announced incorporation of a commission model is a clear reflection of its intent to take Booking.com head on.

Given the large number of small players across Europe, an overall trend toward consolidation is likely as markets mature and consumers choose their favourites. Some younger markets are actually seeing more players enter the arena, and in some countries such as France and Italy there are more than 10 significant OTA players vying for the customer’s attention.

In 2007 (the most recent year of full actual results), the top five companies – Expedia, lastminute.com, Booking.com, Opodo and eBookers – controlled 53% of OTA bookings. The economies of scale driven by consolidation are attractive in a fragmented distribution environment and over time, leading companies – not necessarily limited to just these top 5 brands - are expected to control greater market share. While local OTAs will continue to operate successfully, the efficiencies derived from shared overhead will likely push a good number of them toward mergers and acquisitions in the long term.

Figure 2

Top Five Pan-European Online Travel Agencies, Market Shares, 2007

Source: PhoCusWright’s European Online Travel Overview Fourth Edition

Expedia

Lastminute.com

Booking.com

Opodo

Ebookers

10%

14%

21%

23%

32%

European Online Travel Agencies: Success Strategies for Today and Tomorrow June 2009

8©2009 PhoCusWright Inc. All Rights Reserved

Figure 2a

European Online Travel Agencies Estimated Gross Bookings and Share (€M), 2006-2007

Source: PhoCusWright’s European Online Travel Overview Fourth Edition

Brand CountryGross Bookings (€M) Market Share (%)

2006 2007 2006 2007

Expedia U.S. 2,391 3,085 17.4% 17.2%

Travelocity / lastminute.com U.S./U.K. 2,107 2,204 15.3% 12.3%

Priceline / Booking.com U.S./U.K. 1,068 1,973 7.7% 11.0%

Opodo Spain 1,195 1,300 8.7% 7.3%

Ebookers / Rates to go / HotelClub U.S./U.K. 773 912 5.6% 5.1%

Go Voyages France 400 460 2.9% 2.6%

Edreams Spain 315 407 2.3% 2.3%

Rumbo Spain 259 320 1.9% 1.8%

HRS Germany 208 296 1.5% 1.7%

Travel Republic U.K. 158 292 1.1% 1.6%

Seat24 / SRG (ETI) Scandinavia 218 280 1.6% 1.6%

Voyage-sncf.fr (excl. rail) France 220 260 1.6% 1.5%

Venere (Expedia purchased in 2008) Italy 204 229 1.5% 1.3%

Ab-in-den-Urlaub.de Germany 120 200 0.9% 1.1%

PartirPasCher (Karavel purchased in 2009) France 160 180 1.2% 1.0%

Terminal A Spain 125 176 0.9% 1.0%

Viajar.com Spain 120 140 0.9% 0.8%

Atrapalo Spain 100 136 0.7% 0.8%

L'tur Germany 111 127 0.8% 0.7%

Muchoviaje Spain 70 98 0.5% 0.5%

VIA Travel (gotogate/zolong/flybillet) Scandinavia 75 95 0.5% 0.5%

hotel.de Germany 63 92 0.5% 0.5%

weg.de Germany 30 91 0.2% 0.5%

Travelchannel Germany 71 80 0.5% 0.4%

Viajes ECI Spain 70 80 0.5% 0.4%

Marsans.com Spain 30 70 0.2% 0.4%

Travelstart Scandinavia 44 66 0.3% 0.4%

Travelpartner Scandinavia 38 42 0.3% 0.2%

Pan-European Brands 7,533 9,474 54.7% 52.9%

Total (Brands) 10,744 13,690 78.1% 76.4%

Others 3,018 4,229 21.9% 23.6%

Total 13,761 17,920 100.0% 100.0%

European Online Travel Agencies: Success Strategies for Today and Tomorrow June 2009

9©2009 PhoCusWright Inc. All Rights Reserved

% of Total

Tour package 34

All other vacation expenses 21

Accommodations / lodging 18

Airfare 13

Other activities, excursions and attractions 9

Car rental / private car hire 3

Cruise 3

Total 101

( N ) 1,578

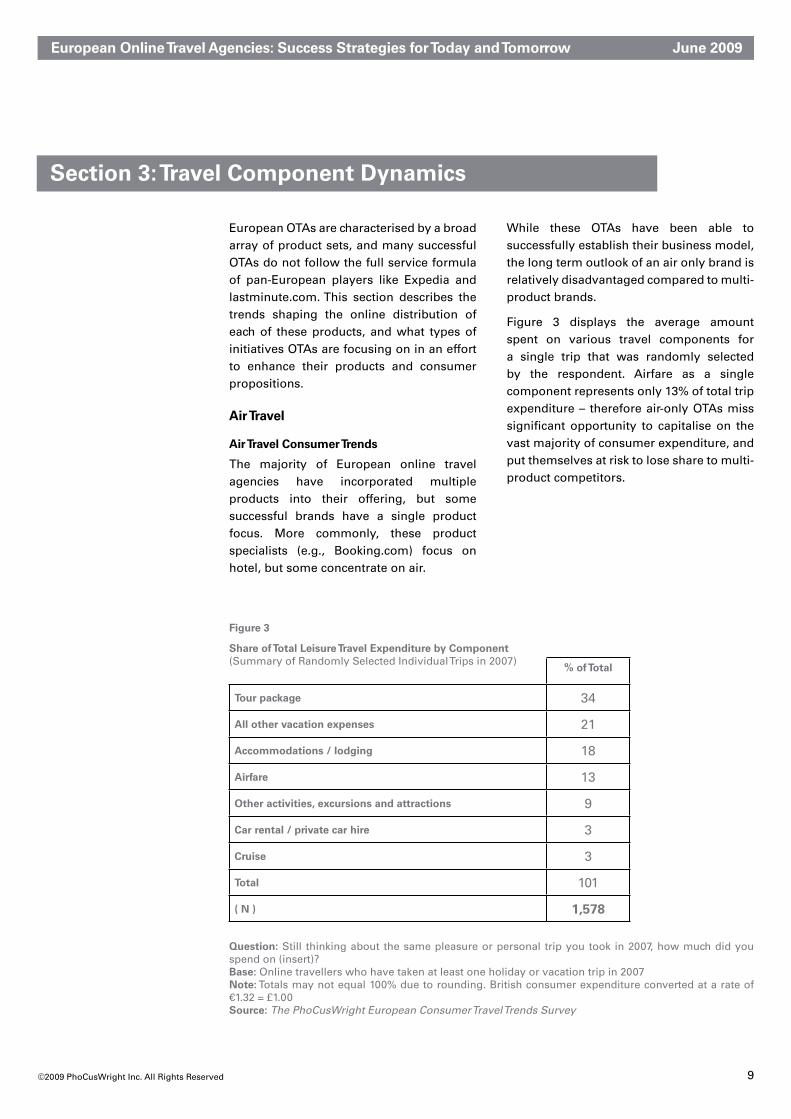

Section 3: Travel Component Dynamics

European OTAs are characterised by a broad array of product sets, and many successful OTAs do not follow the full service formula of pan-European players like Expedia and lastminute.com. This section describes the trends shaping the online distribution of each of these products, and what types of initiatives OTAs are focusing on in an effort to enhance their products and consumer propositions.

Air Travel

Air Travel Consumer Trends

The majority of European online travel agencies have incorporated multiple products into their offering, but some successful brands have a single product focus. More commonly, these product specialists (e.g., Booking.com) focus on hotel, but some concentrate on air.

While these OTAs have been able to successfully establish their business model, the long term outlook of an air only brand is relatively disadvantaged compared to multi-product brands.

Figure 3 displays the average amount spent on various travel components for a single trip that was randomly selected by the respondent. Airfare as a single component represents only 13% of total trip expenditure – therefore air-only OTAs miss significant opportunity to capitalise on the vast majority of consumer expenditure, and put themselves at risk to lose share to multi-product competitors.

Figure 3

Share of Total Leisure Travel Expenditure by Component (Summary of Randomly Selected Individual Trips in 2007)

Question: Still thinking about the same pleasure or personal trip you took in 2007, how much did you spend on (insert)?Base: Online travellers who have taken at least one holiday or vacation trip in 2007Note: Totals may not equal 100% due to rounding. British consumer expenditure converted at a rate of €1.32 = £1.00Source: The PhoCusWright European Consumer Travel Trends Survey

European Online Travel Agencies: Success Strategies for Today and Tomorrow June 2009

10©2009 PhoCusWright Inc. All Rights Reserved

TotalGreat Britain

France Germany Spain

Domestic 66% 56% 69% 56% 83%

Intra-European 62% 74% 49% 70% 54%

Extra-European 33% 42% 38% 31% 22%

( N ) 1,578 394 400 397 387

There are important differences in the destinations chosen by travellers in various European countries, which have significant impact on air travel. As would be expected, countries with warm weather resort areas like Spain and France have a higher incidence of domestic leisure travel (see Figure 4). English travellers have the highest incidence of intra-European and extra-European travel, suggesting that a wide breath of continental and long haul air product is very important for OTAs operating in the U.K. It also helps to explain why global brands have been able to better establish themselves in the U.K. in comparison to other European countries - beyond any cultural similarities to the U.S., global reach provides an advantage.

Spanish travellers represent the opposite end of the spectrum, having the lowest incidence of extra-European travel and the highest incidence of domestic travel. This suggests that short haul offerings are relatively more important for Spanish OTAs and an air only focus would be more risky due to drive/rail alternatives.

Figure 4

Leisure Travel Destination Regional Distribution, by Country

Question: In the last 12 months, how many of those total holiday or vacation trips did you take domestically? Within Europe, but not in the country where you live? Internationally or outside of Europe?Base: Online travellers who have taken at least one holiday or vacation trip in 2007Source: The PhoCusWright European Consumer Travel Trends Survey

European Online Travel Agencies: Success Strategies for Today and Tomorrow June 2009

11©2009 PhoCusWright Inc. All Rights Reserved

Air Travel Distribution Strategies

One of the most important industry issues shaping European OTA air product strategy is access to content. As major carriers like Lufthansa exercise their market muscle to push consumers toward their direct channels, certain carriers blatantly shun intermediaries altogether. Since unpublished air product maintains a sizable portion of air inventory, European content management continues to be challenging for OTAs. Every OTA executive interviewed expressed some level of concern regarding access to inventory in the future, and GDSs are considered vitally important to maintaining the widest access to content possible.

Unbundling of air services like checked baggage was largely not indicated as a concern. Many OTAs look to a multi-source strategy to mitigate the risk of content becoming unavailable at one source, such as working with multiple content providers or building XML feeds to incorporate charter air product. Some go a step further to purchase their own seats through charter airlines.

One of the challenges created by using a multi-source strategy is back-end integration. While most had automated a majority of their back-end processes, few had achieved a completely “touchless” process. From a booking engine perspective, most of the larger players invested in proprietary custom solutions, while some mid-size and smaller OTAs utilise third party solutions rather than building their own.

Ultimately the main priority found consistently across all types of OTAs was being able to provide the best priced option to their shoppers.

Hotel, Packaging and Other Products

Hotels and Lodging

As the most lucrative of travel products available for travellers to purchase (in terms of agent margin/commission) there has been a great deal of focus on hotel product in recent years. The large portion of small, independent properties in Europe presents both benefits and challenges for OTAs. On the one hand, it drives the demand for aggregators because it is simply difficult to investigate options otherwise – finding and getting a quote from individual hotels would be a time consuming (and undoubtedly frustrating) process. But it also creates complexities for OTAs that wish to offer a wide breadth of hotels because there are so many individual property relationships to manage. Accordingly, the use of “bed banks” is common among OTAs that wish to offer hotel product, or supplement directly obtained inventory.

Packages

Packaged products have evolved very differently in Europe in comparison to the U.S, where dynamic packaging is overwhelmingly dominant online. Pre-packaged holidays remain an extremely important product in Europe, and tour operators still generate more than double the bookings of OTAs. Dynamic packaging is continuing to grow its share however, both through the efforts of OTAs as well as tour operators, who recognise the importance of offering consumers control over package components. All OTAs that are not product specialists indicated they are looking to grow their mix of dynamic packages – not surprising given their relatively high transaction value and yield flexibility.

European Online Travel Agencies: Success Strategies for Today and Tomorrow June 2009

12©2009 PhoCusWright Inc. All Rights Reserved

Other products

Car hire, destination activities (i.e., show tickets, attractions), and insurance are additional products commonly offered by OTAs, and most non-specialist brands are continuing to develop and enhance these products. Destination activities represent a product where there is a notable difference in approach by various brands. Some OTAs viewed their destination products as strategically important due to their experiential nature and support of the brand positioning.

Additionally, it creates an opportunity to engage with consumers at another point in their travel process, post purchase. These companies indicated that consumers typically do not make destination activity purchases at the time of travel booking, and think about these activities much closer to the date of travel. This allows companies to enhance their consumer engagement and draw out their interaction with travellers. Other, generally small, OTAs view destination activities as a “nice to have,” and prefer to focus on other products. This is not necessarily a short-sighted view, given that consumers can often be overwhelmed by too many products and some prefer a pared down offering.

European Online Travel Agencies: Success Strategies for Today and Tomorrow June 2009

13©2009 PhoCusWright Inc. All Rights Reserved

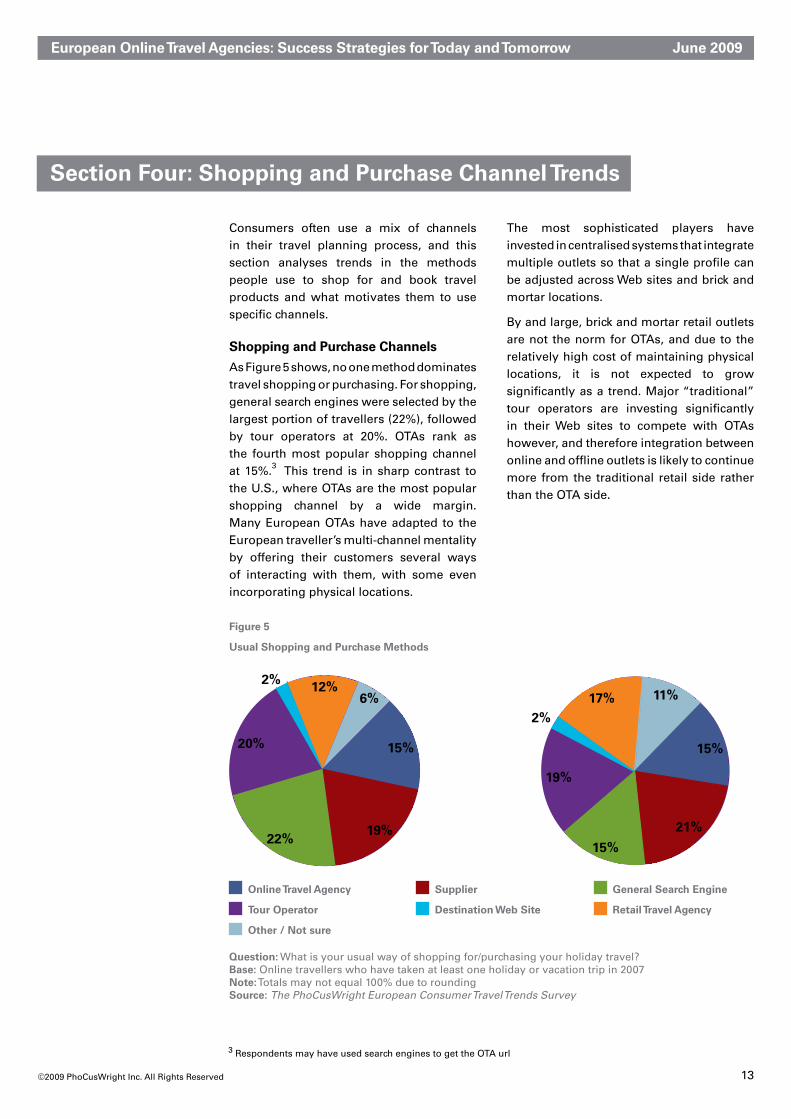

Section Four: Shopping and Purchase Channel Trends

Consumers often use a mix of channels in their travel planning process, and this section analyses trends in the methods people use to shop for and book travel products and what motivates them to use specific channels.

Shopping and Purchase Channels

As Figure 5 shows, no one method dominates travel shopping or purchasing. For shopping, general search engines were selected by the largest portion of travellers (22%), followed by tour operators at 20%. OTAs rank as the fourth most popular shopping channel at 15%.3 This trend is in sharp contrast to the U.S., where OTAs are the most popular shopping channel by a wide margin.Many European OTAs have adapted to the European traveller’s multi-channel mentality by offering their customers several ways of interacting with them, with some even incorporating physical locations.

The most sophisticated players have invested in centralised systems that integrate multiple outlets so that a single profile can be adjusted across Web sites and brick and mortar locations.

By and large, brick and mortar retail outlets are not the norm for OTAs, and due to the relatively high cost of maintaining physical locations, it is not expected to grow significantly as a trend. Major “traditional” tour operators are investing significantly in their Web sites to compete with OTAs however, and therefore integration between online and offline outlets is likely to continue more from the traditional retail side rather than the OTA side.

Figure 5

Usual Shopping and Purchase Methods

Question: What is your usual way of shopping for/purchasing your holiday travel?Base: Online travellers who have taken at least one holiday or vacation trip in 2007Note: Totals may not equal 100% due to roundingSource: The PhoCusWright European Consumer Travel Trends Survey

Online Travel Agency

Tour Operator

Other / Not sure

Supplier

Destination Web Site

General Search Engine

Retail Travel Agency

2% 12%6%

15%

19%22%

20%

2%17% 11%

15%

21%

15%

19%

3 Respondents may have used search engines to get the OTA url

European Online Travel Agencies: Success Strategies for Today and Tomorrow June 2009

14©2009 PhoCusWright Inc. All Rights Reserved

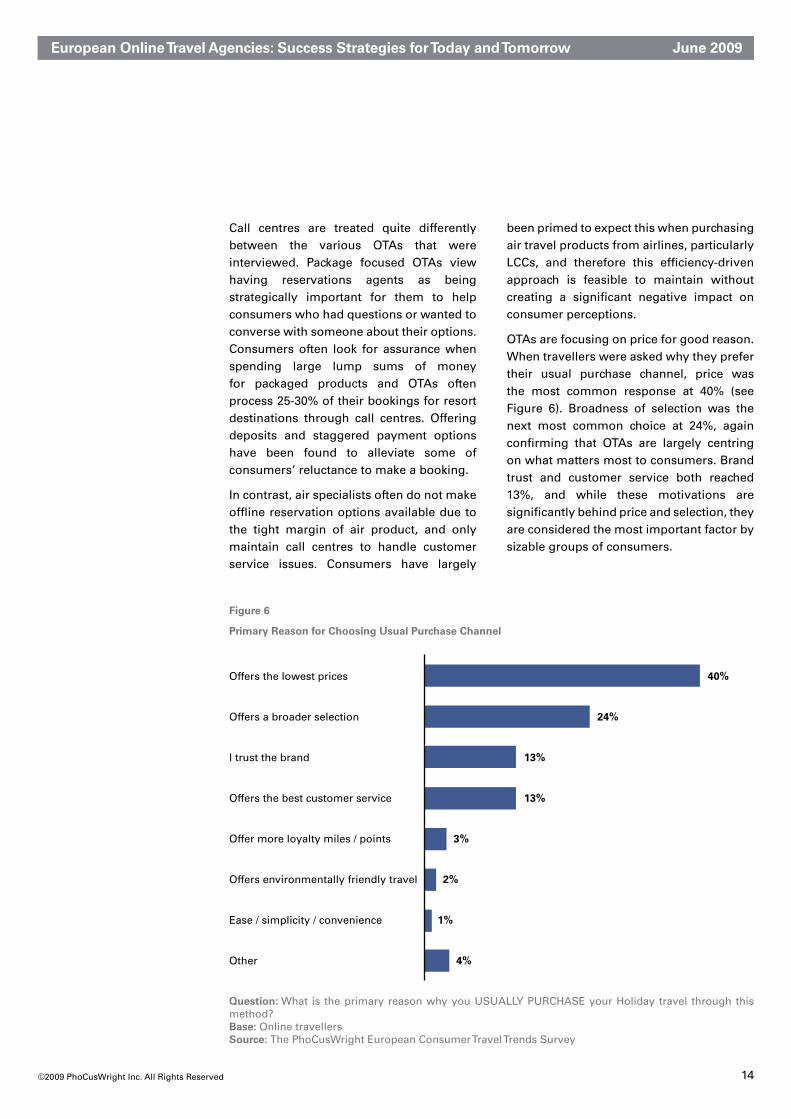

Call centres are treated quite differently between the various OTAs that were interviewed. Package focused OTAs view having reservations agents as being strategically important for them to help consumers who had questions or wanted to converse with someone about their options. Consumers often look for assurance when spending large lump sums of money for packaged products and OTAs often process 25-30% of their bookings for resort destinations through call centres. Offering deposits and staggered payment options have been found to alleviate some of consumers’ reluctance to make a booking.

In contrast, air specialists often do not make offline reservation options available due to the tight margin of air product, and only maintain call centres to handle customer service issues. Consumers have largely

been primed to expect this when purchasing air travel products from airlines, particularly LCCs, and therefore this efficiency-driven approach is feasible to maintain without creating a significant negative impact on consumer perceptions.

OTAs are focusing on price for good reason. When travellers were asked why they prefer their usual purchase channel, price was the most common response at 40% (see Figure 6). Broadness of selection was the next most common choice at 24%, again confirming that OTAs are largely centring on what matters most to consumers. Brand trust and customer service both reached 13%, and while these motivations are significantly behind price and selection, they are considered the most important factor by sizable groups of consumers.

Figure 6

Primary Reason for Choosing Usual Purchase Channel

Question: What is the primary reason why you USUALLY PURCHASE your Holiday travel through this method?Base: Online travellers Source: The PhoCusWright European Consumer Travel Trends Survey

Offers the lowest prices

Offers a broader selection

I trust the brand

Offers the best customer service

Offer more loyalty miles / points

Offers environmentally friendly travel

Ease / simplicity / convenience

Other

40%

24%

13%

13%

3%

2%

1%

4%

European Online Travel Agencies: Success Strategies for Today and Tomorrow June 2009

15©2009 PhoCusWright Inc. All Rights Reserved

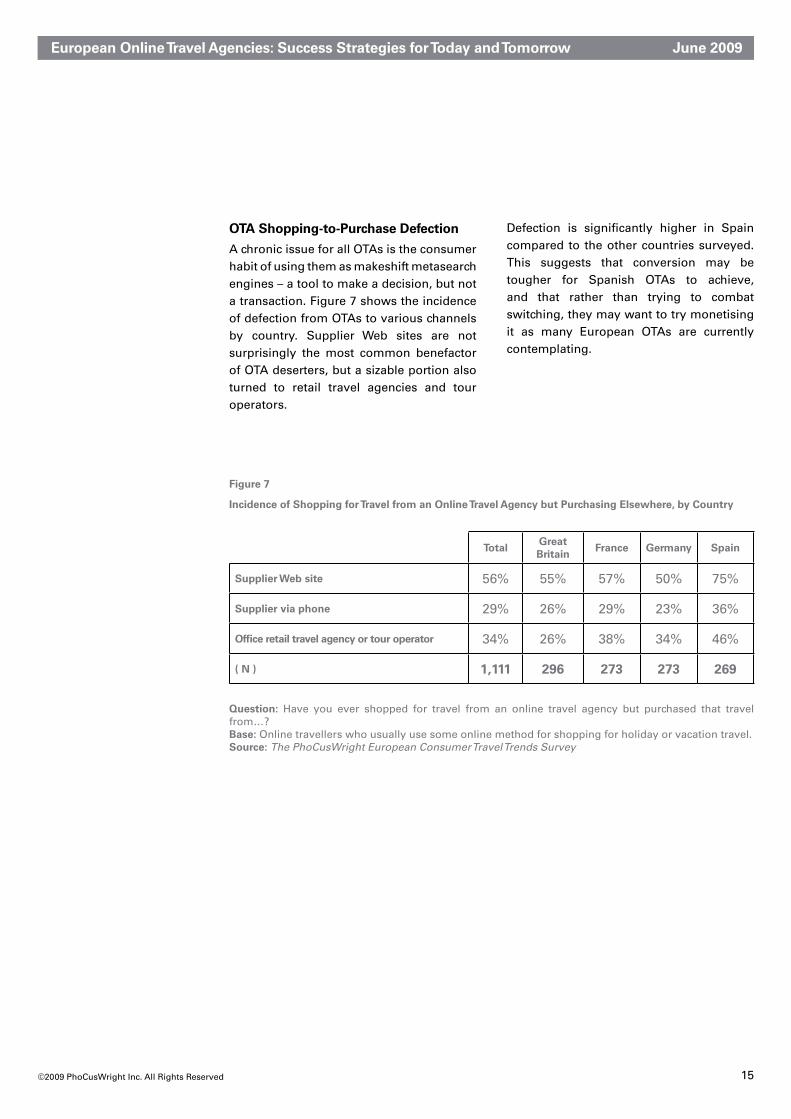

OTA Shopping-to-Purchase Defection

A chronic issue for all OTAs is the consumer habit of using them as makeshift metasearch engines – a tool to make a decision, but not a transaction. Figure 7 shows the incidence of defection from OTAs to various channels by country. Supplier Web sites are not surprisingly the most common benefactor of OTA deserters, but a sizable portion also turned to retail travel agencies and tour operators.

Defection is significantly higher in Spain compared to the other countries surveyed. This suggests that conversion may be tougher for Spanish OTAs to achieve, and that rather than trying to combat switching, they may want to try monetising it as many European OTAs are currently contemplating.

Figure 7

Incidence of Shopping for Travel from an Online Travel Agency but Purchasing Elsewhere, by Country

Question: Have you ever shopped for travel from an online travel agency but purchased that travel from…?Base: Online travellers who usually use some online method for shopping for holiday or vacation travel.Source: The PhoCusWright European Consumer Travel Trends Survey

TotalGreat Britain

France Germany Spain

Supplier Web site 56% 55% 57% 50% 75%

Supplier via phone 29% 26% 29% 23% 36%

Office retail travel agency or tour operator 34% 26% 38% 34% 46%

( N ) 1,111 296 273 273 269

European Online Travel Agencies: Success Strategies for Today and Tomorrow June 2009

16©2009 PhoCusWright Inc. All Rights Reserved

The incorporation of a media offering to drive new advertising revenue is a strategy that has met with mixed success in the U.S. In 2008, Orbitz experimented with displaying sponsored links in its booking path, only to pull them off the site after the testing period was over. The economics were simply not found to work in Orbitz’s favor. Travelocity has been displaying ads for its IgoUgo brand continually for quite some time, but IgoUgo is a referral site, versus a booking site, and is a sister brand. While the ads are directing consumers outside of Travelocity’s domain, they still remain under the larger company umbrella until the user clicks off the site. Expedia’s approach has become more focused on creating its own advertising network with its PassportAds product, which serves behaviourally targeted ads to consumers on other Web sites.

Many European OTAs are in the midst of testing media products to try their hand at adding additional revenue. The challenge is, of course, to sell downstream traffic without eroding conversion. Some may even consider a hybrid OTA/metasearch model that attempts to capture the best of both worlds. Not all OTAs agree that media models that enable consumers to click out of their Web sites will work, and some are resolved to maintain their “walled garden” approach – trying to keep visitors locked in the domain of their Web sites. While much uncertainty remains about the viability of various media programmes, the industry will witness a great deal of experimentation over the next several years as OTAs try to better monetise their traffic, and devise creative solutions that fit their market positioning.

European Online Travel Agencies: Success Strategies for Today and Tomorrow June 2009

17©2009 PhoCusWright Inc. All Rights Reserved

Section Five: Marketing Trends

While online advertising provides detailed metrics that OTAs have come to rely on, many are continuing and even increasing their offline marketing efforts. Particularly in less developed online markets, offline channels provide the opportunity to reach travellers who don’t spend much time online, and may help to convince offline purchasers to switch. While search and display advertising remain the critical bulk of overall marketing budgets, many OTAs are using a multimedia advertising approach incorporating print, radio, television as well as affiliate marketing to broaden their reach, enrich branding and diversify tactics to get noticed.

Social media and the overwhelming buzz that accompanies it are being received with mixed enthusiasm by OTAs. Many are actively managing their brand presence on social networking sites like Facebook and microblogs like Twitter, dedicating staff to monitor and engage with consumers on behalf of their brands. Unlike email messages that required deletion and therefore some degree of effort, Twitter messages (“tweets”) are not as intrusive – the feed format does not necessitate interaction with every message even for those who are “following” a company.

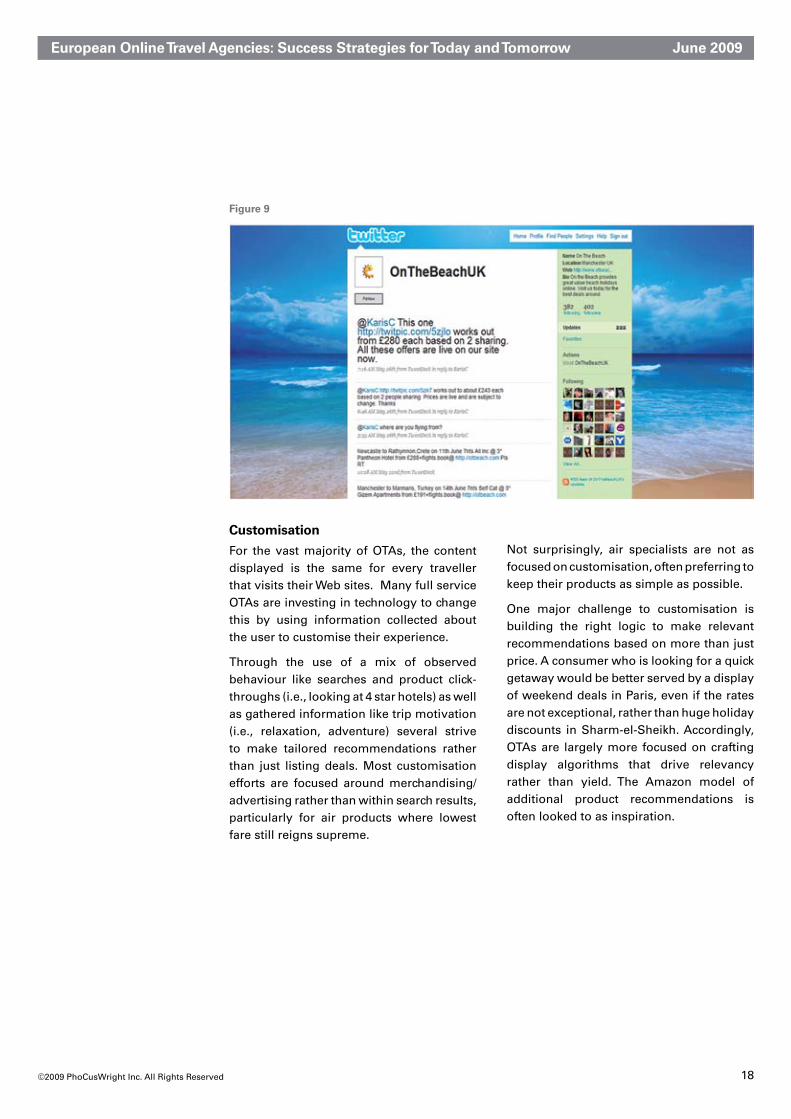

Many companies are using Twitter as a customer service tool as well as a promotional vehicle to run contests and extend their brand interaction with travellers even when they are not actively planning a trip (see Figures 8 and 9).

The most advanced OTAs are building applications on existing social network platforms to enable consumers to share their travel plans and facilitate group planning and input. Some OTAs, however, remain somewhat skeptical about social media’s importance and ultimate impact on business, viewing it as something to watch rather than something important to actively engage in with. Some of even Europe’s largest brands have yet to build their presence on social networks and microblogs.

In contrast, user generated reviews have become ubiquitous among brands that offer hotel products. Smaller OTAs that do not have the user base to effectively build their own cache of reviews often work with third parties like TripAdvisor to ensure they have enough coverage. In the U.S., OTA user reviews have become the most widely influential Web site feature, beating out professional reviews and even photography. User reviews are continuing to gain influence among European travellers.

Figure 8

European Online Travel Agencies: Success Strategies for Today and Tomorrow June 2009

18©2009 PhoCusWright Inc. All Rights Reserved

Figure 9

Customisation

For the vast majority of OTAs, the content displayed is the same for every traveller that visits their Web sites. Many full service OTAs are investing in technology to change this by using information collected about the user to customise their experience.

Through the use of a mix of observed behaviour like searches and product click-throughs (i.e., looking at 4 star hotels) as well as gathered information like trip motivation (i.e., relaxation, adventure) several strive to make tailored recommendations rather than just listing deals. Most customisation efforts are focused around merchandising/advertising rather than within search results, particularly for air products where lowest fare still reigns supreme.

Not surprisingly, air specialists are not as focused on customisation, often preferring to keep their products as simple as possible.

One major challenge to customisation is building the right logic to make relevant recommendations based on more than just price. A consumer who is looking for a quick getaway would be better served by a display of weekend deals in Paris, even if the rates are not exceptional, rather than huge holiday discounts in Sharm-el-Sheikh. Accordingly, OTAs are largely more focused on crafting display algorithms that drive relevancy rather than yield. The Amazon model of additional product recommendations is often looked to as inspiration.

European Online Travel Agencies: Success Strategies for Today and Tomorrow June 2009

19©2009 PhoCusWright Inc. All Rights Reserved

Conclusion:Strategies Shaping the Future Success of Online Travel Agencies

As European online travel matures, competition will only intensify. Growth will no longer be a given, and companies seeking to expand will have to wrest market share away from their competitors. To prepare themselves for the next decade of online travel, OTAs are investing in a range of strategies that align their brands to weather the challenges ahead and gain a competitive edge.

Diversification of Content Sources

With so much potential volatility in sourcing inventory, OTAs that are focused on their long term outlook are diversifying their sources of content. Many of the OTAs that were interviewed are maintaining multiple GDS connections as well as direct links to charter air consolidators. Some larger OTAs and brands that are part of tour operator entities invest in their own air inventory through charter airlines – enabling control over price and easing reliance on commercial airlines. GDSs offer the widest product range of all providers and can help OTAs secure broad access to content and competitive offerings.

Driving Relevancy

All OTAs are striving for consumer relevancy, but are utilising different methods to achieve it. Air specialists are focused on clean, simplified interfaces with little merchandising and a strong price-driven proposition. Full service OTAs aim to provide a rich experience that engages the consumer across multiple phases in the travel planning process - from the earliest phases of destination selection through the post-booking period when consumers are deciding what to do at the destination

By tailoring user experiences to what is most important for the individual consumer, OTAs can build immunity against the threat of commoditisation. Customisation will play a critical role in enhancing relevancy for OTAs that are striving to become more of a trusted source for ideas rather than just a listing of prices. Rich customer profiles will play a pivotal role in enabling customised content by storing valuable information in a central record.

Managing Metasearch

The theoretical proposition of metasearch is extremely well suited for European markets. The ability to consolidate products as well as booking channels solves a problem for travellers who may not even be aware of all the options available in the fragmented marketplace. Most OTAs view metasearch brands as both competitors and partners, and with good reason. Metasearch truly reduces the OTA proposition down to price and puts pressure on fees, but can also be an important source of referrals. While it was once presumed that supplier branded Web sites would receive the vast majority of referrals, metasearch brands in the U.S. found that this is not the case.

While metasearch is still in the early phases of European consumer adoption, a number of them are gaining traction, particularly in mature online markets. European metasearch brands are likely to evolve somewhat differently from U.S. brands by being simpler, and having fewer options for search result manipulation. The micromanagement preferred by many U.S. travellers is often not as appealing to European travellers.

European Online Travel Agencies: Success Strategies for Today and Tomorrow June 2009

20©2009 PhoCusWright Inc. All Rights Reserved

Driving Engagement through Social Media

While some OTAs may remain skeptical about the ability to use social media to drive transaction revenues, maintaining and monitoring a brand presence wherever consumers choose to discuss travel has important value. Word of mouth has tremendous power in consumer travel decisions and social media applications like Twitter allow companies to essentially “eavesdrop” on conversations and interact with consumers directly. The value of social networks for public relations and customer service are, at the very least, reason enough to build a branded presence in popular networks.

Interaction with consumers outside of a Web site adds a new facet to brand identity so that companies become more than just a URL- driving new touch points and higher levels of engagement. Many start-up companies are focused on developing applications that help consumers plan and share their travel experiences both inside and outside of existing social networks. OTAs are not all standing idly by, and some are widening their focus beyond the transaction to build their own branded applications.

Developing a Value Proposition Beyond Price

While price is undoubtedly a vitally important element of an OTA’s consumer proposition, as better and wider distribution networks develop, prices will become more consistent across channels. A consumer proposition that touts just price and selection has a limited lifespan, particularly if all the players are claiming to have the best prices. As online markets mature, OTAs must look to enhance their brands with something more – a means of differentiation.

For some OTAs it might be simplicity, for others it might be high service levels, another might choose environmental friendliness. Breadth of content and comprehensive offerings are also important to consumers – even niche providers can be successful if they provide deep content and choice. Whatever the positioning, it will become increasingly important for OTAs to strike a chord with consumers at some other level beyond price.

Mobile Applications

The advancements in mobile technology are opening new worlds of possibilities for travel companies. While early efforts by travel companies are often miniaturised versions of Web sites, consumers look for a different experience on their mobile “screens” than they do on their computer screens. And while consumers are not likely to book holidays on their mobile devices, they will book, re-book and change travel reservations as plans change. Being able to service consumers through the twists and turns of travel is a powerful proposition. Beyond travel product transactions, a significant bulk of travel expenditure occurs at the destination.

OTAs have not been able to tap into this very effectively because consumers do not usually think about destination activities at time of purchase. Mobile applications provide an ideal vehicle for travel companies to reach consumers when they are in the destination, when they are actively thinking about which sightseeing tour they want to take tomorrow and which restaurant they’d like to try.

European Online Travel Agencies: Success Strategies for Today and Tomorrow June 2009

21©2009 PhoCusWright Inc. All Rights Reserved

Monetising Media Assets

While many OTAs plan to maintain a “walled garden” approach, there are many opportunities to monetise traffic that do not involve sending consumers to competitors. Travellers represent an attractive demographic for advertisers, and selling advertising space to complimentary non-travel products (i.e., cameras, luggage) can offer new revenue streams without decimating conversion. Working with advertising networks presents an efficient alternative for smaller OTAs that may not have the resources to manage ad space directly. Testing and experimentation with various media models will be common in the next few years as companies craft the right advertising programmes their products.

Product Diversification

While some air specialists plan to continue their narrow focus, most online travel agencies look to widen the breadth of their product offering through products such as hotels, car hire, dynamic packaging, prepackaged holidays, vacation rental, insurance and destination activities. Dynamic packaging in particular represents an important area of development for OTAs who seek to provide an alternative to the traditional prepackaged holiday with new levels of flexibility and choice.

A full service approach encourages travellers to turn to OTAs for all their travel needs and maximises the opportunity to capture transactions from visitors. Even the largest players build partnerships with third party providers to enable new product offerings without significant investment. But companies that strive to create such a wide product selection must take care to design their user experience so that the process flows intuitively. Interfaces must balance product breadth with simplicity, so that visitors do not get overwhelmed.

Market Expansion

While growth is a major a priority for local and regional OTAs, many are being cautious about expanding too quickly into other markets. For many local players, the first priority is to become well established in their home markets before looking at any sort of expansion. The local perspective is often viewed as an important asset when competing with larger European and global brands that are positioned for mass appeal. In contrast, global OTAs are continually focused on developing new markets like Eastern Europe and Asia as they relentlessly append them to their inbound/outbound networks. Regional OTAs are largely concentrating on expanding within the Europe before targeting new areas such Asia.

Process Efficiency and Automation

One of the greatest challenges for travel agencies is building the end-to-end processes into a seamless flow – from availability and pricing, booking and ticketing, and post-booking and service delivery. Building an efficient, cost-minimising operation necessitates the automation of manual processes, such as centralised accounting, fulfilment and customer service on the back-end, and a single view of inventory and other relevant content through the Graphical User Interface (GUI) on the front end. Outsourced automation solutions often offer a favourable alternative to building custom systems that consume technical resources, time and capital internally.