european travel & tourism - home | wttc · 2017-10-18 · working with governments and...

TRANSCRIPT

April 2015

1April 2015

European Travel & Tourism:Where are the greatest current and future investment needs?

A report prepared by Oxford Economics for the World Travel & Tourism Council

European Travel & Tourism:Where are the greatest current and future investment needs?

ForewordThe World Travel & Tourism Council (WTTC) is the global authority on the economic and social contribution of Travel & Tourism. It promotes sustainable growth for the sector, working with governments and international institutions to create jobs, to drive exports and to generate prosperity.

Members are the Chairs, Presidents and Chief Executives of the world’s leading, private sector Travel & Tourism businesses. These Members bring specialist knowledge to guide government policy and decision-making, raising awareness of the importance of the sector as an economic generator of wealth.

Understanding and addressing the challenges inhibiting the sustainable growth of our sector is paramount for all industry stakeholders. Together with our research partner, Oxford Economics, and to coincide with the 15th annual WTTC Global Summit in Madrid, Spain in April 2015, WTTC is pleased to have produced this report on Travel & Tourism investment in Europe. The report draws on data from WTTC’s annual Travel & Tourism Economic Impact Research 2015 and the World Economic Forum’s Travel & Tourism Competitiveness Report 20131 , and seeks to understand whether and where the region’s infrastructure and investment will constrain or support future industry growth.

WTTC has forecast that there will be €2.1 trillion worth of Travel & Tourism investment made in Europe over the next decade. However, with the sector forecast to grow as fast, or faster, than the economies overall in every major European region, and the lagging state of much infrastructure today, baseline growth forecasts for both investment and Travel & Tourism’s overall contribution to GDP may only be met with sufficient and effective investment to support this demand.

Given the diversity of Europe, there are disparities in the relative contributions of Travel & Tourism to economies as well as to the state of Travel & Tourism infrastructure in the region. As a result, some countries are much better placed than others to capitalise on forecasted demand. While a positive relationship exists between Travel & Tourism infrastructure and the contribution the sector makes to GDP, this report gives heed to the fact that government deficits, fiscal austerity and high competition for foreign direct investment requires future investments to be smart and well-targeted.

This need for smarter investments gives even more importance not only to opportunities for greater collaboration between public and private actors, but also to seeking cross-border cooperation and creative funding options. Breaking down barriers to infrastructure development through the right business, political and regulatory frameworks will help to ensure that Travel & Tourism in Europe maintains a strong and competitive position.

David ScowsillPresident & CEO

World Travel & Tourism Council

1 www.weforum.org/reports/travel-tourism-competitiveness-report-2013

Restoration of the Parthenon on Acropolis – Athens, Greece

European Travel & Tourism: Where are the greatest current and future investment needs? April 2015

6 7

Executive summary

1 How investment and infrastructure support Europe’s Travel & Tourism sector

1.1 The economic contribution of the Travel & Tourism sector to Europe’s economy

1.2 DefiningtheroleofinvestmentandinfrastructureinsupportingtheTravel&Tourismsector

1.3 The importance of investment to success in the Travel & Tourism sector

1.4 Infrastructurequalityandcapacitytodayarestronglyrelatedtohistoricalinvestmentspending

2 WhichEuropeancountrieshavethegreatestneedforcurrentandfutureinvestment?

2.1 AssessingthequalityandcapacityofEurope’sTravel&Tourisminfrastructure

2.2 AssessingobjectivesubcomponentsofthethreemajorWEFinfrastructurepillars

2.3 Whichcountrieshavethegreatestinfrastructureneedsbetween2015and2025?

3 TheoutlookforEuropeanTravel&Tourisminvestmentspending

3.1 Aregionalcomparisonofforecastedinvestmentspending

3.2 Sectoral composition of investment spend

4 Conclusion–puttingTravel&TourisminvestmentonEuropeangovernments’agendas

Eastern Europe

BelarusBulgariaCzech RepublicEstoniaHungaryLatviaLithuaniaMoldovaPolandRomaniaRussiaSlovakiaUkraine

Southern Europe

AlbaniaBosniaandHerzegovinaCroatiaCyprusGreeceItalyMacedoniaMaltaMontenegroPortugalSerbiaSloveniaSpainTurkey

Western & Northern Europe

AustriaBelgiumDenmarkFinlandFranceGermanyIcelandIrelandLuxembourgNetherlandsNorwaySwedenSwitzerlandUnitedKingdom

European Regional Groupings

Forthepurposesofthisreport,EuropeisdefinedaccordingtotheUNregionalclassifications*listedbelow.Countriesandsub-classificationsofcountriesinEurope.

* Cyprus and Turkey reclassified as Southern Europe for purposes of this report. In addition, Western European and Northern European countries have been grouped together, as they frequently represent a common narrative.

Contents

08

11

11

13

14

16

17

17

22

27

29

29

32

36

European Travel & Tourism: Where are the greatest current and future investment needs? April 2015

8 9

Executive summary TheTravel&TourismsectormakesasubstantialcontributiontoEuropeaneconomies.In2014,includingitsdirect,indirect,andinducedimpacts,Travel&Tourismsupported33.5millionjobsandmadenearly€1.6trillionincontributiontogrossdomesticproduct(GDP),or9.3%oftotalEuropeanGDP.By2025,theTravel&Tourismsector’stotaleconomiccontributionisexpectedtogrowto38millionjobsand€2.1trillionincontributionstoGDP(9.9%oftotalEuropeanGDP).Inaddition,Travel&TourismwillbeakeytorecoveryforcountrieshithardestbyrecessionandtheEurozonecrisis,includingGreece,Spain,andPortugal.

Thesector’sgrowingGDPandjobscontributiondependsonsupportiveinfrastructureandinvestment.Whileinvestmentmustbesmart,thereisastronghistoricallinkbetweenthemagnitudeofTravel&TourisminvestmentspendingandthequalityandcapacityofEuropeancountries’ Travel & Tourism infrastructure. The success and size of the economic contribution from Travel & Tourism is directly linked to the amount of investment in the sector.

Travel&Tourismisforecasttogrowasfast,ifnotfaster,thantheeconomyoverallineverymajorEuropeanregion,puttingpressureoninfrastructurecapabilitiesandincreasingtheneedforadditionalinfrastructureinvestment.Forexample,WesternandNorthernEuropeancountriesareexpectedtoexperienceaverageannualgrowthintheirTravel&Tourismsectorsof2.7%,comparedtowholeeconomygrowthof1.9%peryear.InEasternEurope,Travel&Tourismgrowthof3.3%isexpectedtomarginallyoutpaceeconomy-widegrowthof3.2%,whileSouthernEurope’sTravel&Tourismsectorgrowthof2.8%peryearwilloutpaceeconomy-widegrowthof2.6%.

Comparedtobaselineforecasts,however,poorexistinginfrastructurequalityandcapacityorinadequatefutureinvestmentcouldslowgrowthinTravel&TourismGDPandjobscontributionsbetween2015and2025.ThisreportshowsthatseveralcountriescouldfailtoachievebaselineforecastsforTravel&TourismGDPandjobs,andfallbehindinglobalcompetitivenessterms,duetolimitedinfrastructureandunderinvestmentrelativetoTravel&Tourism demand.

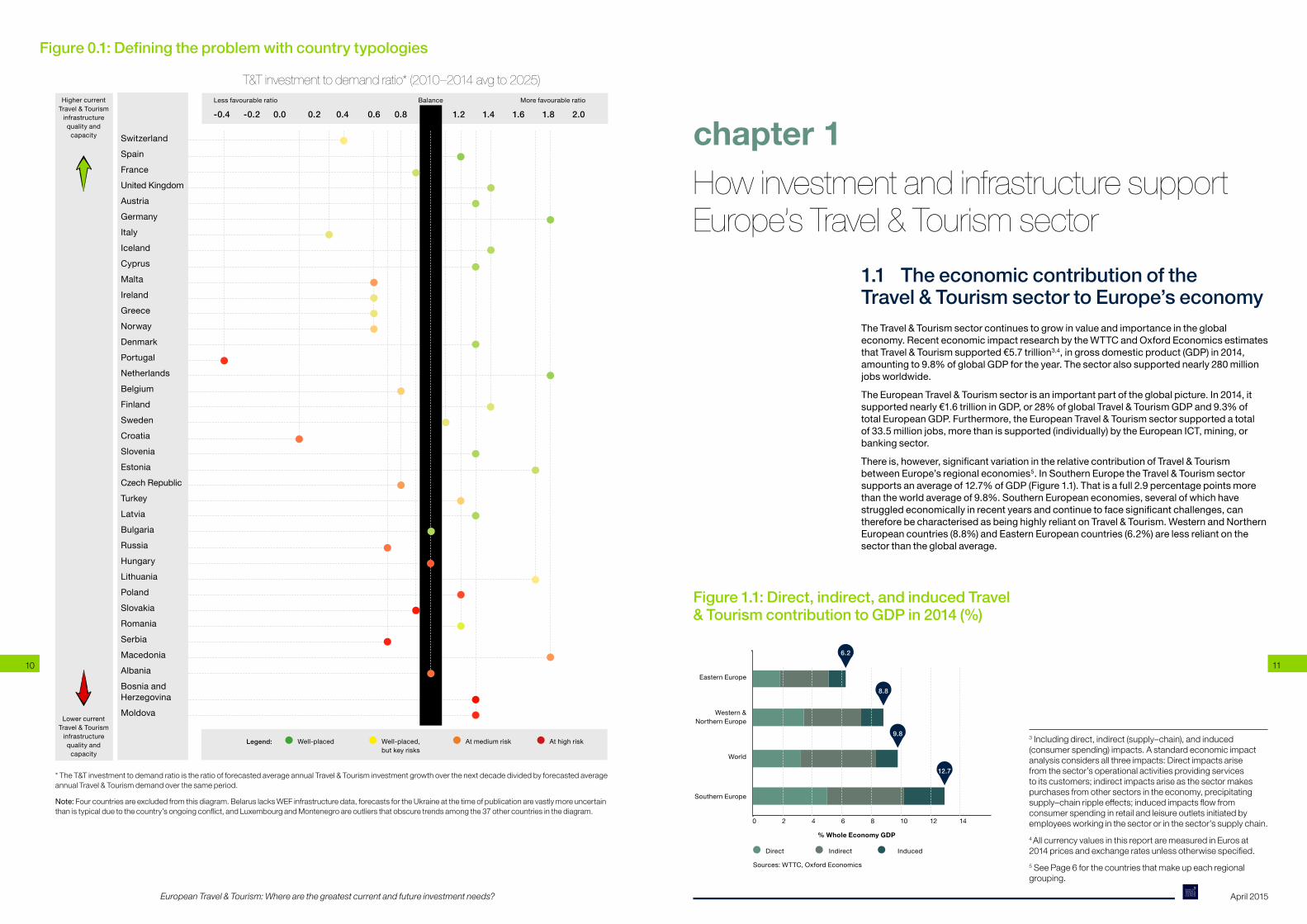

Thisreportusesthreecategoriestoidentifycountrytypologies,rangingfromthosethatareatriskoflosingTravel&Tourisminfrastructurecompetitivenessoverthenextdecade,tothosethatarewell-placedtobenefitfromforecastedinvestmentspendbetween2015and2025(Figure0.1):

• Well-placed:Thisgroupofcountries,exemplifiedbyAustria,GermanyandtheUnitedKingdom,hashighexistingqualityandcapacityofTravel&Tourisminfrastructurewhichtheyareexpectedtomaintainandimprovebetween2015and2025.Withinvestmentgrowthexpectedtooutpacedemandoverthatperiod,thesecountriesarewell-placedtocapturethefullbenefitsofforecastedTravel&Tourismdemand.

• Well-placed, but with key risks:France,Italy,Switzerland,Ireland,andGreeceareonesetofcountriesincludedinthiscategory.EachofthemhasexistingTravel&TourismqualityandcapacitythatisgreaterthantheEuropeanaverage.Yettheirstrongpositionsarelikelytodeterioratesomewhatoverthenextdecade,sinceTravel&TourismdemandgrowthisforecasttooutstripTravel&Tourisminvestmentgrowthovertheperiod.Similarly,DenmarkandFinlandhavebetterthanaverageTravel&Tourisminfrastructurequalityandcapacity;however,weakhistoricalinvestmentgrowthpresentsriskstotheforecastthatinvestmentgrowthwillexceeddemandgrowthinthenextdecade.SloveniaandLatviaarealso“wellplaced,withrisks”.Theirkeystrengthisthattheyareexpectedtoseeinvestmentgrowththatisstrongerthandemandgrowthoverthenextdecade;theirkeyriskistheirexistinginfrastructurequalityandcapacity,whichisbelowtheEuropeanaverage.

• At medium or high risk:ThiscategoryincludescountrieslikeAlbania,BosniaandHerzegovina,andMoldova,whichareconsideredtobeathighriskbecausetheyhavethepoorestexistinginfrastructurequalityandcapacityofthe41countriesanalysedinthisreport.Croatia,Serbia,andSlovakiaarealsoconsideredatrisk,becauseTravel&Tourisminvestmentgrowthisexpectedtolagbehinddemandgrowthoverthenextdecade,andtheirstartinginfrastructurequalityandcapacitytodayisaverage–inthecaseofCroatia–orlow–inthecaseofSerbiaandSlovakia.Portugal,havingrelativelystrongexistinginfrastructurecapabilities,isaspecialcase:becausedemandgrowthisexpectedtooutpaceinvestmentgrowthbysuchawidemargin,thecountryfacesariskthatitscurrentinfrastructurequalityandcapacitywilldegradeoverthenextdecade.UnlikeSpain,PortugaldidnothavethesamehighlevelofTravel&Tourisminvestmentintheperiodbeforetheglobalrecession.

FewcountriescanclaimahighrankingacrossallthreemajorTravel&Tourisminfrastructure‘pillars’analysedinthisreport,comprisingtourism,airtransportandgroundtransportinfrastructure. Southern and Eastern European countries tend to have weaker air transport capabilities,whileanumberofWesternandNorthernEuropeancountries–includingtheUK,GermanyandDenmark–needtoimprovetheirtourisminfrastructurebeforebeingranked‘bestinclass’forthatpillar.SeveralSouthernandEasternEuropeancountries,includingAlbania,Poland,Romania,andSerbia,fallshortonallthreeinfrastructurepillars.

The41Europeancountriesanalysedinthisreportareexpectedtoinvest€2.1trillioninTravel&Tourismbetween2015and2025.Thatis5%ofallforecastedEuropeaninvestmentovertheperiod.The14WesternandNorthernEuropeancountriesanalysedinthisreportwillcontributethelargestamount,at€1.3trillion,or62%oftheEuropeantotaland€210perforeignvisitoranddomesticresident.The14SouthernEuropeancountriesanalysedinthisreportwillcontribute€570billion,or27%oftheEuropeantotaland€100perforeignvisitoranddomesticresident.Andthe13EasternEuropeancountriesanalysedinthisreportwillcontributenearly€240billion,whichis11%oftheEuropeantotalandequivalenttoalittleover€50perforeignvisitoranddomesticresident.

FutureinvestmentintheEuropeanTravel&Tourismsectormustbesmart.Governmentdeficits,strainedcorporatebalancesheets,andstrongcompetitionamongmajorworldregionsforforeigndirectinvestmentmeanthatfutureinvestmentspendmustbewell-targeted.ArecentreportbytheEuropeanCourtofAuditors2highlightedthedangersofpoorlytargetedspending:of€460millioninCohesionpolicyfundsspenton20airportinfrastructureprojectsinEstonia,Italy,Greece,Poland,andSpain,28%wasdeemedtohavegonetoprojectsthatwere“notneededatall”.Sevenofthe20airportswhichreceivedfundingforexpansionprojectsareunprofitable,andwilllikelybeclosedintheabsenceofpermanentpublicfunding.Indicatively,onlyhalfoftheairportsanalysedhadmorepassengerspost-expansion,suggestingsignificantunderutilizationofthenewlybuiltinfrastructure.

GovernmentandfinancialsectorconstraintsonfundingsuggeststhatEuropeancountriesshouldseekopportunitiesforcross-bordercollaborationandcreativefundingoptions.Europe’srelativelysmallgeographicsizeandexistingintegrationmeanscrossborderTravel&Tourisminfrastructurecollaborationcanbeuniquelyeffective.ForEurope,smartinvestment,especiallyinperiodsoffiscalausterity,maycomeintheformofcreativefundingoptionslikepublicprivatepartnershipsorevencrowdfunding.

2 ‘EU-funded airport infrastructures: poor value for money’, (2014), European Court of Auditors, December.

Askøy Bridge – Bergen and Askøy, Norway

European Travel & Tourism: Where are the greatest current and future investment needs? April 2015

10 11

SwitzerlandSpainFranceUnitedKingdomAustriaGermanyItalyIcelandCyprusMaltaIrelandGreeceNorwayDenmarkPortugalNetherlandsBelgiumFinlandSwedenCroatiaSloveniaEstoniaCzech RepublicTurkeyLatviaBulgariaRussiaHungaryLithuaniaPolandSlovakiaRomaniaSerbiaMacedoniaAlbaniaBosnia and HerzegovinaMoldova

-0.4 -0.2 0.0 0.2 0.4 0.6 0.8 1.0 1.2 1.4 1.6 1.8 2.0BalanceLess favourable ratioHighercurrent

Travel & Tourism infrastructure

quality and capacity

More favourable ratio

Legend: Well-placed At medium riskWell-placed, but key risks

Athighrisk

* The T&T investment to demand ratio is the ratio of forecasted average annual Travel & Tourism investment growth over the next decade divided by forecasted average annual Travel & Tourism demand over the same period.

Note: Four countries are excluded from this diagram. Belarus lacks WEF infrastructure data, forecasts for the Ukraine at the time of publication are vastly more uncertain than is typical due to the country’s ongoing conflict, and Luxembourg and Montenegro are outliers that obscure trends among the 37 other countries in the diagram.

Lower current Travel & Tourism

infrastructure quality and

capacity

Figure 0.1: Defining the problem with country typologies

Direct

Eastern Europe

Western & Northern Europe

World

Southern Europe

0

Indirect Induced

% Whole Economy GDP

Sources:WTTC,OxfordEconomics

2 4 6 8 10 12 14

6.2

8.8

12.7

9.8

How investment and infrastructure support Europe’s Travel & Tourism sector

chapter 1

1.1 The economic contribution of the Travel & Tourism sector to Europe’s economyTheTravel&Tourismsectorcontinuestogrowinvalueandimportanceintheglobaleconomy.RecenteconomicimpactresearchbytheWTTCandOxfordEconomicsestimatesthatTravel&Tourismsupported€5.7trillion3,4,ingrossdomesticproduct(GDP)in2014,amountingto9.8%ofglobalGDPfortheyear.Thesectoralsosupportednearly280millionjobsworldwide.

TheEuropeanTravel&Tourismsectorisanimportantpartoftheglobalpicture.In2014,itsupportednearly€1.6trillioninGDP,or28%ofglobalTravel&TourismGDPand9.3%oftotalEuropeanGDP.Furthermore,theEuropeanTravel&Tourismsectorsupportedatotalof33.5millionjobs,morethanissupported(individually)bytheEuropeanICT,mining,orbankingsector.

Thereis,however,significantvariationintherelativecontributionofTravel&TourismbetweenEurope’sregionaleconomies5. In Southern Europe the Travel & Tourism sector supportsanaverageof12.7%ofGDP(Figure1.1).Thatisafull2.9percentagepointsmorethantheworldaverageof9.8%.SouthernEuropeaneconomies,severalofwhichhavestruggledeconomicallyinrecentyearsandcontinuetofacesignificantchallenges,canthereforebecharacterisedasbeinghighlyreliantonTravel&Tourism.WesternandNorthernEuropeancountries(8.8%)andEasternEuropeancountries(6.2%)arelessreliantonthesectorthantheglobalaverage.

Figure 1.1: Direct, indirect, and induced Travel & Tourism contribution to GDP in 2014 (%)

3 Including direct, indirect (supply–chain), and induced (consumer spending) impacts. A standard economic impact analysis considers all three impacts: Direct impacts arise from the sector’s operational activities providing services to its customers; indirect impacts arise as the sector makes purchases from other sectors in the economy, precipitating supply–chain ripple effects; induced impacts flow from consumer spending in retail and leisure outlets initiated by employees working in the sector or in the sector’s supply chain.4 All currency values in this report are measured in Euros at 2014 prices and exchange rates unless otherwise specified.5 See Page 6 for the countries that make up each regional grouping.

T&T investment to demand ratio* (2010–2014 avg to 2025)

European Travel & Tourism: Where are the greatest current and future investment needs? April 2015

12 13

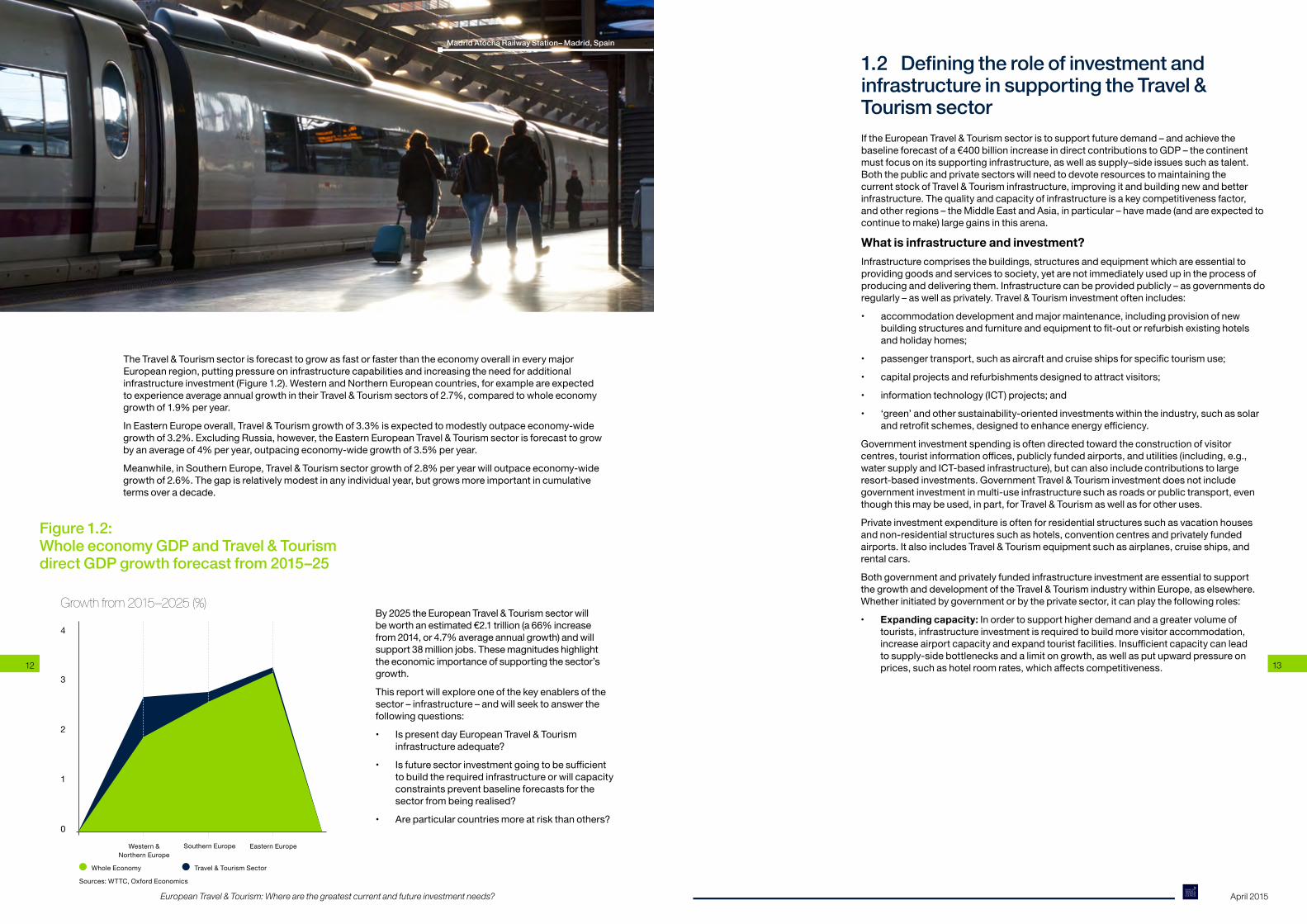

TheTravel&TourismsectorisforecasttogrowasfastorfasterthantheeconomyoverallineverymajorEuropeanregion,puttingpressureoninfrastructurecapabilitiesandincreasingtheneedforadditionalinfrastructureinvestment(Figure1.2).WesternandNorthernEuropeancountries,forexampleareexpectedtoexperienceaverageannualgrowthintheirTravel&Tourismsectorsof2.7%,comparedtowholeeconomygrowthof1.9%peryear.

InEasternEuropeoverall,Travel&Tourismgrowthof3.3%isexpectedtomodestlyoutpaceeconomy-widegrowthof3.2%.ExcludingRussia,however,theEasternEuropeanTravel&Tourismsectorisforecasttogrowbyanaverageof4%peryear,outpacingeconomy-widegrowthof3.5%peryear.

Meanwhile,inSouthernEurope,Travel&Tourismsectorgrowthof2.8%peryearwilloutpaceeconomy-widegrowthof2.6%.Thegapisrelativelymodestinanyindividualyear,butgrowsmoreimportantincumulativeterms over a decade.

Eastern EuropeWestern & Northern Europe

Southern Europe

0

1

2

3

4

Whole Economy Travel & Tourism Sector

Growth from 2015–2025 (%)

Sources:WTTC,OxfordEconomics

Figure 1.2: Whole economy GDP and Travel & Tourism direct GDP growth forecast from 2015–25

By2025theEuropeanTravel&Tourismsectorwillbeworthanestimated€2.1trillion(a66%increasefrom2014,or4.7%averageannualgrowth)andwillsupport38millionjobs.Thesemagnitudeshighlighttheeconomicimportanceofsupportingthesector’sgrowth.

This report will explore one of the key enablers of the sector – infrastructure – and will seek to answer the followingquestions:

• Is present day European Travel & Tourism infrastructureadequate?

• Isfuturesectorinvestmentgoingtobesufficientto build the required infrastructure or will capacity constraints prevent baseline forecasts for the sectorfrombeingrealised?

• Areparticularcountriesmoreatriskthanothers?

1.2 Defining the role of investment and infrastructure in supporting the Travel & Tourism sectorIf the European Travel & Tourism sector is to support future demand – and achieve the baselineforecastofa€400billionincreaseindirectcontributionstoGDP–thecontinentmustfocusonitssupportinginfrastructure,aswellassupply–sideissuessuchastalent.BoththepublicandprivatesectorswillneedtodevoteresourcestomaintainingthecurrentstockofTravel&Tourisminfrastructure,improvingitandbuildingnewandbetterinfrastructure.Thequalityandcapacityofinfrastructureisakeycompetitivenessfactor,andotherregions–theMiddleEastandAsia,inparticular–havemade(andareexpectedtocontinuetomake)largegainsinthisarena.

What is infrastructure and investment?Infrastructurecomprisesthebuildings,structuresandequipmentwhichareessentialtoprovidinggoodsandservicestosociety,yetarenotimmediatelyusedupintheprocessofproducinganddeliveringthem.Infrastructurecanbeprovidedpublicly–asgovernmentsdoregularly–aswellasprivately.Travel&Tourisminvestmentoftenincludes:

• accommodationdevelopmentandmajormaintenance,includingprovisionofnewbuildingstructuresandfurnitureandequipmenttofit-outorrefurbishexistinghotelsand holiday homes;

• passengertransport,suchasaircraftandcruiseshipsforspecifictourismuse;

• capitalprojectsandrefurbishmentsdesignedtoattractvisitors;

• informationtechnology(ICT)projects;and

• ‘green’andothersustainability-orientedinvestmentswithintheindustry,suchassolarandretrofitschemes,designedtoenhanceenergyefficiency.

Governmentinvestmentspendingisoftendirectedtowardtheconstructionofvisitorcentres,touristinformationoffices,publiclyfundedairports,andutilities(including,e.g.,watersupplyandICT-basedinfrastructure),butcanalsoincludecontributionstolargeresort-based investments. Government Travel & Tourism investment does not include governmentinvestmentinmulti-useinfrastructuresuchasroadsorpublictransport,eventhoughthismaybeused,inpart,forTravel&Tourismaswellasforotheruses.

Private investment expenditure is often for residential structures such as vacation houses andnon-residentialstructuressuchashotels,conventioncentresandprivatelyfundedairports.ItalsoincludesTravel&Tourismequipmentsuchasairplanes,cruiseships,andrental cars.

BothgovernmentandprivatelyfundedinfrastructureinvestmentareessentialtosupportthegrowthanddevelopmentoftheTravel&TourismindustrywithinEurope,aselsewhere.Whetherinitiatedbygovernmentorbytheprivatesector,itcanplaythefollowingroles:

• Expanding capacity:Inordertosupporthigherdemandandagreatervolumeoftourists,infrastructureinvestmentisrequiredtobuildmorevisitoraccommodation,increaseairportcapacityandexpandtouristfacilities.Insufficientcapacitycanleadtosupply-sidebottlenecksandalimitongrowth,aswellasputupwardpressureonprices,suchashotelroomrates,whichaffectscompetitiveness.

Madrid Atocha Railway Station– Madrid, Spain

European Travel & Tourism: Where are the greatest current and future investment needs? April 2015

14 15

• Maintaining and enhancing current infrastructure:Continuedinvestmentinexistinginfrastructureplaysacentralroleinmaintainingandimprovingitsfunctionalityandqualitythroughmajorrefurbishmentandupgrading.Capitalexpenditureonexistinginfrastructureisessentialforadaptinginfrastructuretoaccountfortheevolutioninconsumertastesovertime,suchasgrowingvisitordemandforWiFiservices,whilerefurbishmentsextendthelifeofexistinginfrastructureassets.

• Stimulating demand:Capitalexpenditureonnewvisitorattractionscangenerateadditionaldemandandhelpgainorretainmarketshareinthefaceofcompetition.Theseprojectsaimtoenhancetheappealofadestinationthroughimprovingitsoffering.Forexample,ahubairportcanputalocation–likeDubai–ontheTravel&Tourismmap,whichstimulatesdemandforTravel&Tourismserviceswellbeyondtheairport itself.

6 Four countries – Albania, Croatia, Malta, and Montenegro – have been removed from the figure. They are unique in that they are small economies with relatively undeveloped infrastructure, yet tourism impacts comprise exceptionally large shares of their GDP. They have been removed to avoid obscuring the relationship observed between infrastructure capability and Travel & Tourism impacts in the majority of European countries. These four countries comprise just 0.3% of the gross domestic product of the 41 countries comprising Europe in this report7 World Economic Forum, (2014), ‘Travel and Tourism Competitiveness Report 2013’. The WEF produces a Travel and Tourism competitiveness report every two years.8 The WEF composite infrastructure score is computed as the simple average of three key infrastructure pillars within the Travel and Tourism Competitiveness Report, including Tourism Infrastructure, Air Transport Infrastructure, and Ground Transport Infrastructure. Scores are ranked from 1-7 and are based on a WEF executive opinion survey.

1.3 The importance of investment to success in the Travel & Tourism sectorWhethertravellingforbusiness,visitingfriendsandfamily,orleisurepurposes,athomeorabroad,travellersdirectlyandindirectlyrelyonawiderangeofinfrastructure.Visitorstravelbyrail,road,airorsea;communicatebyphone,email,orinstantmessage;sleepinhotelsandotherformsofaccommodation;attendmeetingsandenjoyentertainmentoptionsthatwouldbeimpossiblewithoutsupportinginfrastructure,whetheritbearobustelectricalgridand water supply or a well-maintained road and airport network.

Historically,therehasbeenastronglinkbetweenthequalityandcapacityofacountry’sinfrastructureandthesuccessofitsTravel&Tourismsector,asmeasuredbythesector’seconomiccontribution.Thislinkcanbemeasuredstatisticallybycomparingthemeasuredquality of infrastructure related to Travel & Tourism and the estimated economic contribution ofthesectoracrosscountries.ThatrelationshipisshowninFigure1.3for37Europeancountriesin20146.ItusestheWorldEconomicForum’s(WEF)‘TravelandTourismCompetitiveness Report’7resultsasthe‘independentvariables’measuringinfrastructure8,while the WTTC’s estimates of direct Travel & Tourism GDP are the ‘dependent variables’ measuringtheassociationwitheconomicactivity.

Figure1.3providesalineofbestfitbetweenthesetwovariables.ItshowsthecorrelationbetweeninfrastructureandthemagnitudeofthedirectcontributionthatTravel&Tourismmakes to a country’s GDP.

AtthetoprightofthechartisSpain,whichreliesontheTravel&Tourismsectordirectlyfor5.6%ofitsGDP(comparedto3.4%forEuropeoverall)andhasverygoodinfrastructurecapabilities,representedbyaWEFcompositeinfrastructurescoreof6outof7.InthemiddleofthegraphliesacountryliketheCzechRepublic,whichhasacompositeinfrastructurescoreof4.6outof7anddirectlyreliesontheTravel&Tourismsectorfor2.6%ofitsGDP.AndatthebottomleftarecountrieslikeSerbiawhichhaspoorinfrastructurequalityandcapacity(itscompositeinfrastructurescoreis3.3outof7)anddoesnothaveasignificantlydevelopedTravel&Tourismsector(Serbiadirectlyreliesonthesectorfor2.1%ofitsGDP).SerbiawillrequireahostofinfrastructureimprovementstosupportalargerTravel&Tourismsector.Forexample,thecountrycouldimproveitsruralroads,overhaulanoutdatedrailnetworkthatisnotuptothestandardsofmostinternationaltourists,andincreaseairaccessibilitywithintheregions,whichitcoulddobyallowingcommercialflightsatmilitarybases.

It is too much to expect that Travel & Tourism infrastructure quality and capacity could explainallofthevariationshowninFigure1.3.Muchofthecross-countryvariabilityisduetodifferencesinclimate,geography,thenumberoftouristattractions,andthesizeofcompetingindustries.Forexample,allelseequal,Spain’snaturalclimateadvantagesrelative to Switzerland increase the likelihood that Spain will have a persistent comparative advantageinsatisfyingTravel&TourismdemandrelativetoSwitzerland.Unsurprisingly,Switzerland’seconomyismorereliantonsectorsthatdependlessontheweather,likefinance(11%ofGDPin2014)andmanufacturing(19%ofGDP).FinanceandmanufacturingaremorelikelytoholdlongstandingcomparativeadvantagesforSwitzerlandthanTravel&Tourism,andimprovingSwitzerland’salreadygoodTravel&Tourisminfrastructurequalityandcapacitywillnotchangethat.

Figure 1.3: WEF composite Travel & Tourism infrastructure score and Travel & Tourism direct GDP contribution in 2014

DenmarkRussia

Hungary

Czech RepublicSerbia

Macedonia

Switzerland

UnitedKingdomFrance

Spain

IcelandCyprus

Greece

Austria

Portugal

ItalyTurkey4

6

8

2

03 4 5 6 7

Direct Travel & Tourism GDP(%totalGDP)

WEFcompositeinfrastructurescore

Sources: World Economic Forum, WTTC, Oxford Economics

Note: Albania, Croatia, Malta and Montenegro are excluded from this analysis due to their distorting effect. These nations benefit from exceptionally high direct Travel and Tourism GDP contributions despite having relatively poor infrastructure.

Street Renewal Project – Brussels, Belgium

European Travel & Tourism: Where are the greatest current and future investment needs? April 2015

16 17

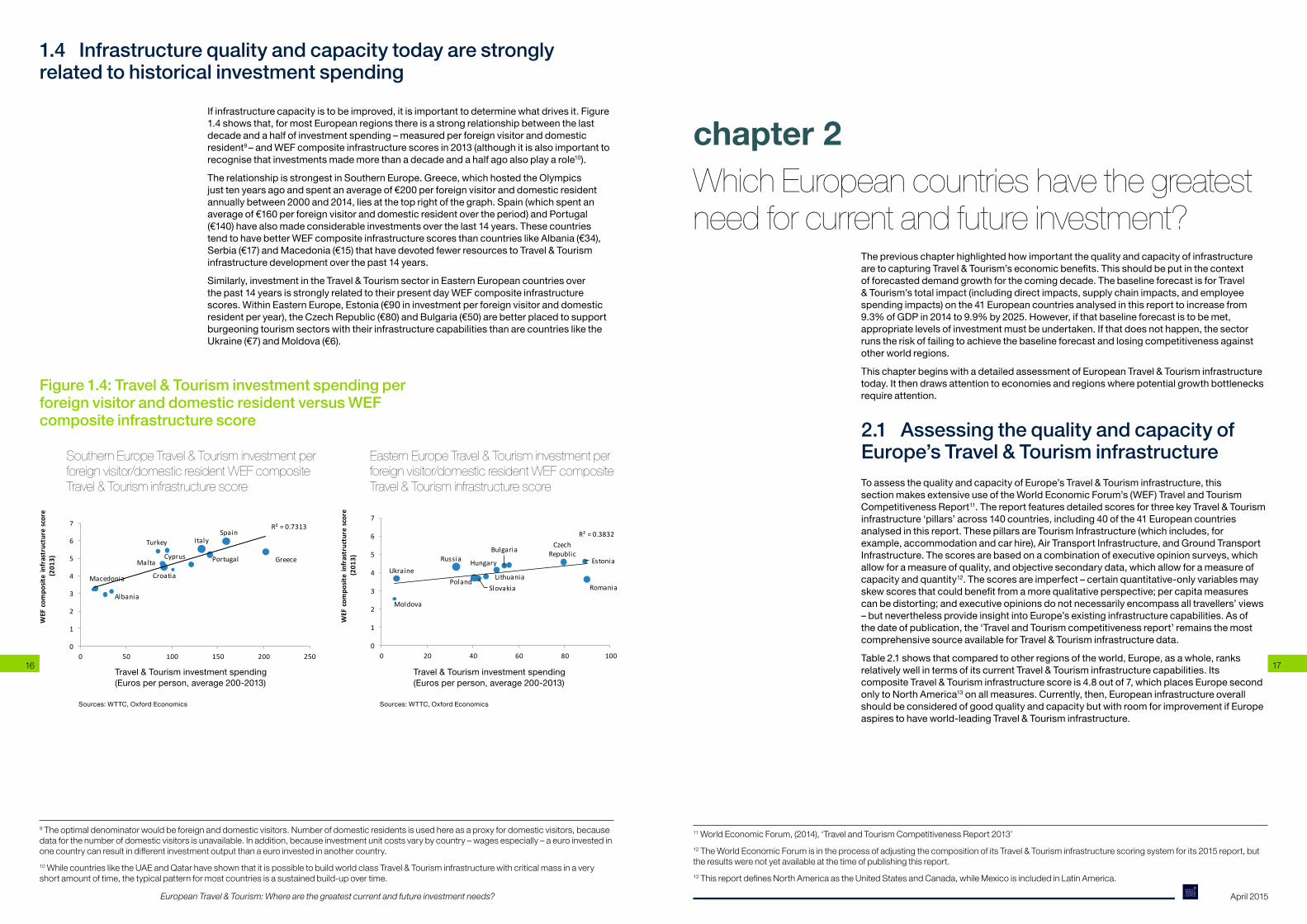

1.4 Infrastructure quality and capacity today are strongly related to historical investment spending

Ifinfrastructurecapacityistobeimproved,itisimportanttodeterminewhatdrivesit.Figure1.4showsthat,formostEuropeanregionsthereisastrongrelationshipbetweenthelastdecadeandahalfofinvestmentspending–measuredperforeignvisitoranddomesticresident9–andWEFcompositeinfrastructurescoresin2013(althoughitisalsoimportanttorecognisethatinvestmentsmademorethanadecadeandahalfagoalsoplayarole10).

TherelationshipisstrongestinSouthernEurope.Greece,whichhostedtheOlympicsjusttenyearsagoandspentanaverageof€200perforeignvisitoranddomesticresidentannuallybetween2000and2014,liesatthetoprightofthegraph.Spain(whichspentanaverageof€160perforeignvisitoranddomesticresidentovertheperiod)andPortugal(€140)havealsomadeconsiderableinvestmentsoverthelast14years.ThesecountriestendtohavebetterWEFcompositeinfrastructurescoresthancountrieslikeAlbania(€34),Serbia(€17)andMacedonia(€15)thathavedevotedfewerresourcestoTravel&Tourisminfrastructuredevelopmentoverthepast14years.

Similarly,investmentintheTravel&TourismsectorinEasternEuropeancountriesoverthepast14yearsisstronglyrelatedtotheirpresentdayWEFcompositeinfrastructurescores.WithinEasternEurope,Estonia(€90ininvestmentperforeignvisitoranddomesticresidentperyear),theCzechRepublic(€80)andBulgaria(€50)arebetterplacedtosupportburgeoningtourismsectorswiththeirinfrastructurecapabilitiesthanarecountriesliketheUkraine(€7)andMoldova(€6).

Figure 1.4: Travel & Tourism investment spending per foreign visitor and domestic resident versus WEF composite infrastructure score

BulgariaCzech

RepublicHungary

PolandRomaniaSlovakia

Moldova

Russia

UkraineEstonia

Lithuania

R² = 0.3832

0

1

2

3

4

5

6

7

0 20 40 60 80 100

WEF

com

posit

e in

fras

truc

ture

scor

e(2

013)

Travel & Tourism investment spending (Euros per person, average 2000-2013)

Eastern Europe Travel & Tourism investment per foreign visitor/domestic resident and WEF composite Travel & Tourism infrastructure score

Sources: WTTC, Oxford Economics

Greece

Italy

Portugal

Spain

Croatia

CyprusMalta

Albania

Macedonia

Turkey

R² = 0.7313

0

1

2

3

4

5

6

7

0 50 100 150 200 250

WEF

com

posit

e in

fras

truc

ture

scor

e(2

013)

Travel & Tourism investment spending (Euros per person, average 2000-2013)

Southern Europe Travel & Tourism investment per foreign visitor/domesticresident and WEF composite Travel & Tourism infrastructure score

Sources: WTTC, Oxford Economics

9 The optimal denominator would be foreign and domestic visitors. Number of domestic residents is used here as a proxy for domestic visitors, because data for the number of domestic visitors is unavailable. In addition, because investment unit costs vary by country – wages especially – a euro invested in one country can result in different investment output than a euro invested in another country. 10 While countries like the UAE and Qatar have shown that it is possible to build world class Travel & Tourism infrastructure with critical mass in a very short amount of time, the typical pattern for most countries is a sustained build-up over time.

11 World Economic Forum, (2014), ‘Travel and Tourism Competitiveness Report 2013’12 The World Economic Forum is in the process of adjusting the composition of its Travel & Tourism infrastructure scoring system for its 2015 report, but the results were not yet available at the time of publishing this report.13 This report defines North America as the United States and Canada, while Mexico is included in Latin America.

Which European countries have the greatest need for current and future investment?

ThepreviouschapterhighlightedhowimportantthequalityandcapacityofinfrastructurearetocapturingTravel&Tourism’seconomicbenefits.Thisshouldbeputinthecontextofforecasteddemandgrowthforthecomingdecade.ThebaselineforecastisforTravel&Tourism’stotalimpact(includingdirectimpacts,supplychainimpacts,andemployeespendingimpacts)onthe41Europeancountriesanalysedinthisreporttoincreasefrom9.3%ofGDPin2014to9.9%by2025.However,ifthatbaselineforecastistobemet,appropriatelevelsofinvestmentmustbeundertaken.Ifthatdoesnothappen,thesectorrunstheriskoffailingtoachievethebaselineforecastandlosingcompetitivenessagainstotherworldregions.

ThischapterbeginswithadetailedassessmentofEuropeanTravel&Tourisminfrastructuretoday.Itthendrawsattentiontoeconomiesandregionswherepotentialgrowthbottlenecksrequire attention.

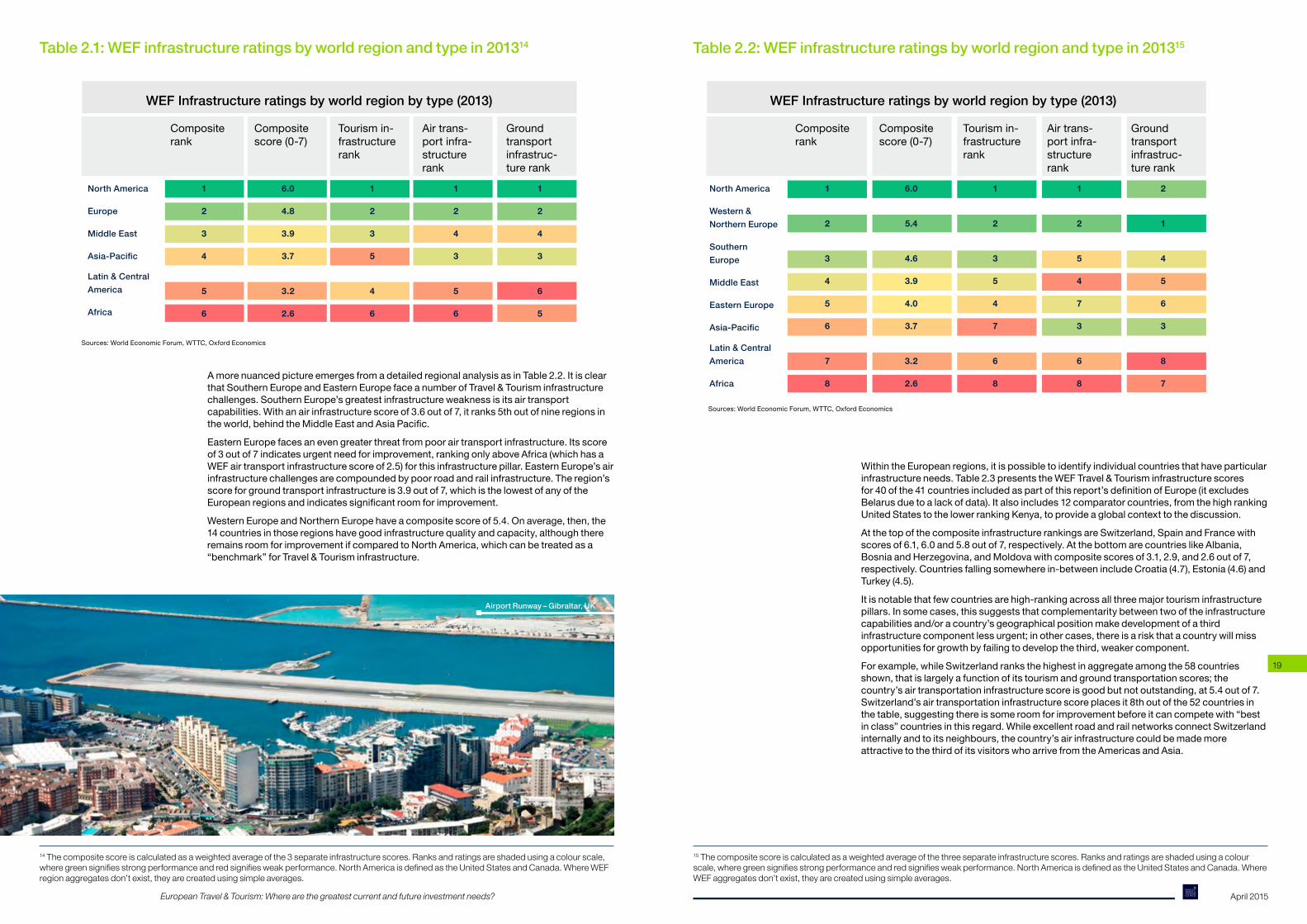

2.1 Assessing the quality and capacity of Europe’s Travel & Tourism infrastructureToassessthequalityandcapacityofEurope’sTravel&Tourisminfrastructure,thissectionmakesextensiveuseoftheWorldEconomicForum’s(WEF)TravelandTourismCompetitiveness Report11. The report features detailed scores for three key Travel & Tourism infrastructure‘pillars’across140countries,including40ofthe41Europeancountriesanalysedinthisreport.ThesepillarsareTourismInfrastructure(whichincludes,forexample,accommodationandcarhire),AirTransportInfrastructure,andGroundTransportInfrastructure.Thescoresarebasedonacombinationofexecutiveopinionsurveys,whichallowforameasureofquality,andobjectivesecondarydata,whichallowforameasureofcapacity and quantity12. The scores are imperfect – certain quantitative-only variables may skewscoresthatcouldbenefitfromamorequalitativeperspective;percapitameasurescanbedistorting;andexecutiveopinionsdonotnecessarilyencompassalltravellers’views–butneverthelessprovideinsightintoEurope’sexistinginfrastructurecapabilities.Asofthedateofpublication,the‘TravelandTourismcompetitivenessreport’remainsthemostcomprehensive source available for Travel & Tourism infrastructure data.

Table2.1showsthatcomparedtootherregionsoftheworld,Europe,asawhole,ranksrelatively well in terms of its current Travel & Tourism infrastructure capabilities. Its compositeTravel&Tourisminfrastructurescoreis4.8outof7,whichplacesEuropesecondonly to North America13onallmeasures.Currently,then,EuropeaninfrastructureoverallshouldbeconsideredofgoodqualityandcapacitybutwithroomforimprovementifEuropeaspirestohaveworld-leadingTravel&Tourisminfrastructure.

chapter 2

Travel&Tourisminvestmentspending(Eurosperperson,average200-2013)

Travel&Tourisminvestmentspending(Eurosperperson,average200-2013)

Sources:WTTC,OxfordEconomics Sources:WTTC,OxfordEconomics

Eastern Europe Travel & Tourism investment per foreign visitor/domestic resident WEF composite Travel & Tourism infrastructure score

Southern Europe Travel & Tourism investment per foreign visitor/domestic resident WEF composite Travel & Tourism infrastructure score

European Travel & Tourism: Where are the greatest current and future investment needs? April 2015

18 19

Table 2.1: WEF infrastructure ratings by world region and type in 201314

WEF Infrastructure ratings by world region by type (2013)

Composite rank

North America

Europe

Middle East

Asia-Pacific

Latin & Central America

Africa

1

2

3

4

5

6

6.0

4.8

3.9

3.7

3.2

2.6

1

2

3

5

4

6

1

2

4

3

5

6

1

2

4

3

6

5

Composite score(0-7)

Tourism in-frastructure rank

Air trans-port infra-structure rank

Ground transport infrastruc-ture rank

Sources:WorldEconomicForum,WTTC,OxfordEconomics

AmorenuancedpictureemergesfromadetailedregionalanalysisasinTable2.2.Itisclearthat Southern Europe and Eastern Europe face a number of Travel & Tourism infrastructure challenges.SouthernEurope’sgreatestinfrastructureweaknessisitsairtransportcapabilities.Withanairinfrastructurescoreof3.6outof7,itranks5thoutofnineregionsintheworld,behindtheMiddleEastandAsiaPacific.

EasternEuropefacesanevengreaterthreatfrompoorairtransportinfrastructure.Itsscoreof3outof7indicatesurgentneedforimprovement,rankingonlyaboveAfrica(whichhasaWEFairtransportinfrastructurescoreof2.5)forthisinfrastructurepillar.EasternEurope’sairinfrastructurechallengesarecompoundedbypoorroadandrailinfrastructure.Theregion’sscoreforgroundtransportinfrastructureis3.9outof7,whichisthelowestofanyoftheEuropeanregionsandindicatessignificantroomforimprovement.

WesternEuropeandNorthernEuropehaveacompositescoreof5.4.Onaverage,then,the14countriesinthoseregionshavegoodinfrastructurequalityandcapacity,althoughthereremainsroomforimprovementifcomparedtoNorthAmerica,whichcanbetreatedasa“benchmark”forTravel&Tourisminfrastructure.

14 The composite score is calculated as a weighted average of the 3 separate infrastructure scores. Ranks and ratings are shaded using a colour scale, where green signifies strong performance and red signifies weak performance. North America is defined as the United States and Canada. Where WEF region aggregates don’t exist, they are created using simple averages.

Table 2.2: WEF infrastructure ratings by world region and type in 201315

15 The composite score is calculated as a weighted average of the three separate infrastructure scores. Ranks and ratings are shaded using a colour scale, where green signifies strong performance and red signifies weak performance. North America is defined as the United States and Canada. Where WEF aggregates don’t exist, they are created using simple averages.

Sources:WorldEconomicForum,WTTC,OxfordEconomics

WEF Infrastructure ratings by world region by type (2013)

Composite rank

North America

Western & Northern Europe

Southern Europe

Middle East

Eastern Europe

Asia-Pacific

Latin & Central America

Africa

1

2

3

4

5

6

7

8

1

2

3

5

4

7

6

8

6.0

5.4

4.6

3.9

4.0

3.7

3.2

2.6

Composite score(0-7)

Tourism in-frastructure rank

Air trans-port infra-structure rank

Ground transport infrastruc-ture rank

1

2

5

4

7

3

6

8

2

1

4

5

6

3

8

7

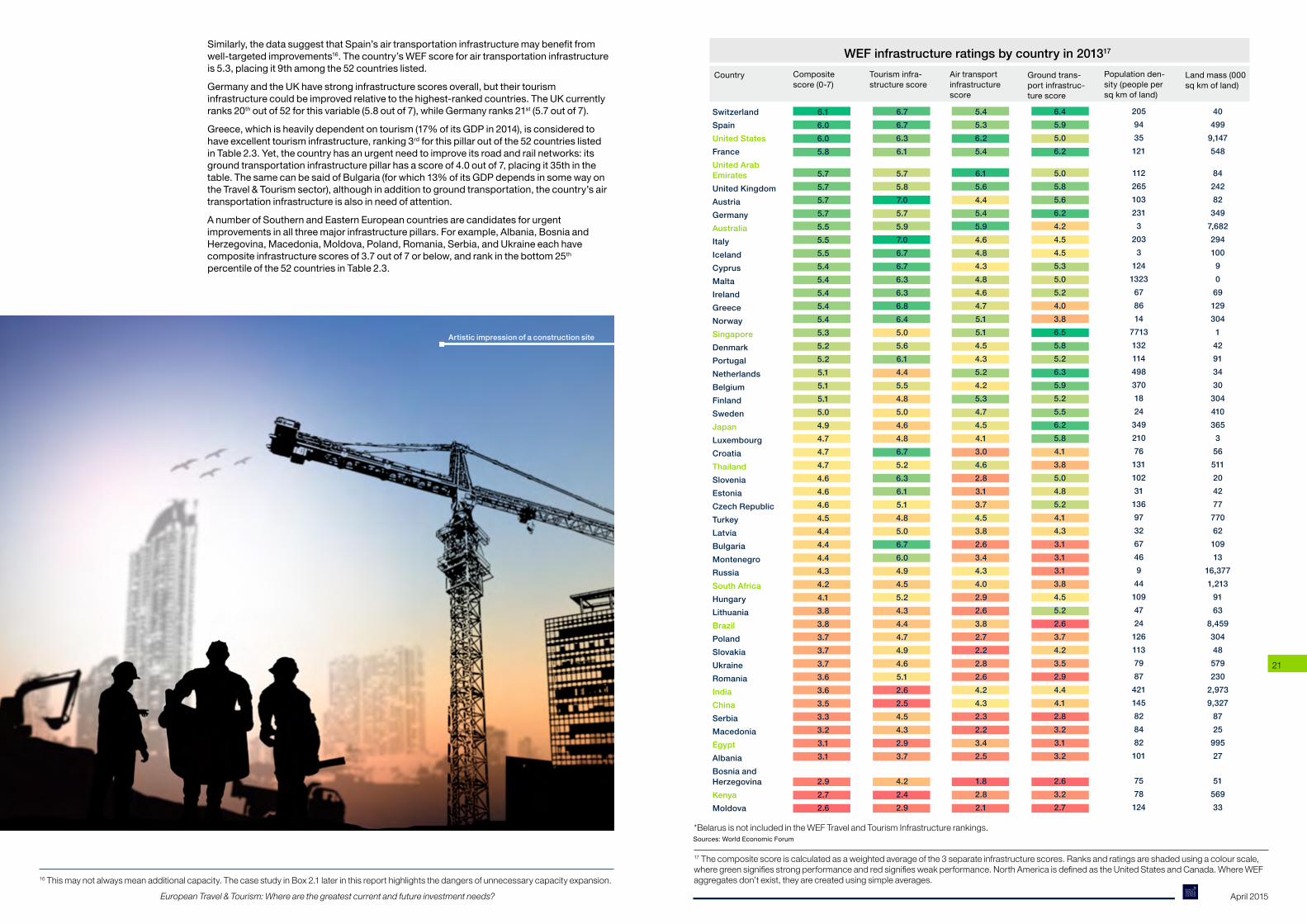

WithintheEuropeanregions,itispossibletoidentifyindividualcountriesthathaveparticularinfrastructureneeds.Table2.3presentstheWEFTravel&Tourisminfrastructurescoresfor40ofthe41countriesincludedaspartofthisreport’sdefinitionofEurope(itexcludesBelarusduetoalackofdata).Italsoincludes12comparatorcountries,fromthehighrankingUnitedStatestothelowerrankingKenya,toprovideaglobalcontexttothediscussion.

AtthetopofthecompositeinfrastructurerankingsareSwitzerland,SpainandFrancewithscoresof6.1,6.0and5.8outof7,respectively.AtthebottomarecountrieslikeAlbania,BosniaandHerzegovina,andMoldovawithcompositescoresof3.1,2.9,and2.6outof7,respectively.Countriesfallingsomewherein-betweenincludeCroatia(4.7),Estonia(4.6)andTurkey(4.5).

Itisnotablethatfewcountriesarehigh-rankingacrossallthreemajortourisminfrastructurepillars.Insomecases,thissuggeststhatcomplementaritybetweentwooftheinfrastructurecapabilitiesand/oracountry’sgeographicalpositionmakedevelopmentofathirdinfrastructurecomponentlessurgent;inothercases,thereisariskthatacountrywillmissopportunitiesforgrowthbyfailingtodevelopthethird,weakercomponent.

Forexample,whileSwitzerlandranksthehighestinaggregateamongthe58countriesshown,thatislargelyafunctionofitstourismandgroundtransportationscores;thecountry’sairtransportationinfrastructurescoreisgoodbutnotoutstanding,at5.4outof7.Switzerland’sairtransportationinfrastructurescoreplacesit8thoutofthe52countriesinthetable,suggestingthereissomeroomforimprovementbeforeitcancompetewith“bestinclass”countriesinthisregard.WhileexcellentroadandrailnetworksconnectSwitzerlandinternallyandtoitsneighbours,thecountry’sairinfrastructurecouldbemademoreattractive to the third of its visitors who arrive from the Americas and Asia.

Airport Runway – Gibraltar, UK

European Travel & Tourism: Where are the greatest current and future investment needs? April 2015

20 21

Similarly,thedatasuggestthatSpain’sairtransportationinfrastructuremaybenefitfromwell-targetedimprovements16.Thecountry’sWEFscoreforairtransportationinfrastructureis5.3,placingit9thamongthe52countrieslisted.

GermanyandtheUKhavestronginfrastructurescoresoverall,buttheirtourisminfrastructurecouldbeimprovedrelativetothehighest-rankedcountries.TheUKcurrentlyranks20thoutof52forthisvariable(5.8outof7),whileGermanyranks21st(5.7outof7).

Greece,whichisheavilydependentontourism(17%ofitsGDPin2014),isconsideredtohaveexcellenttourisminfrastructure,ranking3rdforthispillaroutofthe52countrieslistedinTable2.3.Yet,thecountryhasanurgentneedtoimproveitsroadandrailnetworks:itsgroundtransportationinfrastructurepillarhasascoreof4.0outof7,placingit35thinthetable.ThesamecanbesaidofBulgaria(forwhich13%ofitsGDPdependsinsomewayontheTravel&Tourismsector),althoughinadditiontogroundtransportation,thecountry’sairtransportation infrastructure is also in need of attention.

AnumberofSouthernandEasternEuropeancountriesarecandidatesforurgentimprovementsinallthreemajorinfrastructurepillars.Forexample,Albania,BosniaandHerzegovina,Macedonia,Moldova,Poland,Romania,Serbia,andUkraineeachhavecompositeinfrastructurescoresof3.7outof7orbelow,andrankinthebottom25th percentileofthe52countriesinTable2.3.

SwitzerlandSpainUnited StatesFranceUnited Arab EmiratesUnited KingdomAustriaGermanyAustraliaItalyIcelandCyprusMaltaIrelandGreeceNorwaySingaporeDenmarkPortugalNetherlandsBelgiumFinlandSwedenJapanLuxembourgCroatiaThailandSloveniaEstoniaCzech RepublicTurkeyLatviaBulgariaMontenegroRussiaSouth AfricaHungaryLithuaniaBrazilPolandSlovakiaUkraineRomaniaIndiaChinaSerbiaMacedoniaEgyptAlbaniaBosnia and HerzegovinaKenyaMoldova

6.16.06.05.8

5.75.75.75.75.55.55.55.45.45.45.45.45.35.25.25.15.15.15.04.94.74.74.74.64.64.64.54.44.44.44.34.24.13.83.83.73.73.73.63.63.53.33.23.13.1

2.92.72.6

6.76.76.36.1

5.75.87.05.75.97.06.76.76.36.36.86.45.05.66.14.45.54.85.04.64.86.75.26.36.15.14.85.06.76.04.94.55.24.34.44.74.94.65.12.62.54.54.32.93.7

4.22.42.9

5.45.36.25.4

6.15.64.45.45.94.64.84.34.84.64.75.15.14.54.35.24.25.34.74.54.13.04.62.83.13.74.53.82.63.44.34.02.92.63.82.72.22.82.64.24.32.32.23.42.5

1.82.82.1

6.45.95.06.2

5.05.85.66.24.24.54.55.35.05.24.03.86.55.85.26.35.95.25.56.25.84.13.85.04.85.24.14.33.13.13.13.84.55.22.63.74.23.52.94.44.12.83.23.13.2

2.63.22.7

40499

9,147548

8424282

3497,68229410090

69129304

142913430

304410365

3565112042777706210913

16,3771,213

9163

8,45930448579230

2,9739,327

8725

99527

5156933

2059435121

112265103231

3203

3124

1323678614

77131321144983701824

3492107613110231136973267469

4410947241261137987

421145828482101

7578124

WEF infrastructure ratings by country in 201317

Population den-sity(peoplepersqkmofland)

Landmass(000sqkmofland)

Composite score(0-7)

Country Tourism infra-structure score

Air transport infrastructure score

Ground trans-port infrastruc-ture score

Sources:WorldEconomicForum*Belarus is not included in the WEF Travel and Tourism Infrastructure rankings.

16 This may not always mean additional capacity. The case study in Box 2.1 later in this report highlights the dangers of unnecessary capacity expansion.

17 The composite score is calculated as a weighted average of the 3 separate infrastructure scores. Ranks and ratings are shaded using a colour scale, where green signifies strong performance and red signifies weak performance. North America is defined as the United States and Canada. Where WEF aggregates don’t exist, they are created using simple averages.

Artistic impression of a construction site

European Travel & Tourism: Where are the greatest current and future investment needs? April 2015

22 23

Box 2.1: Case study: The importance of smart investment

Not all investment expenditure results in improved infrastructure. Investment expenditure can be poorly targeted,subjecttopoliticalcorruption,orotherwisemisspent.Insuchcases,theresultinginfrastructureislikely to be poor value for money.

A recent analysis by the European Court of Auditors18suggeststhatpoorlytargetedinvestmentinairtransportinfrastructureisanimportantissueforanumberofEuropeancountries.Thereport,publishedinDecember2014,analysed€460millioninCohesionpolicyfunds(suchastheEuropeanRegionalDevelopmentFund)thatwerespenton20airportinfrastructureprojectsinEstonia,Italy,Greece,Poland,andSpain.Itfoundthatthefunding,whichwasspentbetween2000and2013,waspoorvalueformoneyoverall.

Overbuildingwasakeyreasonforthis.Justhalfoftheairportsanalysedincreasedpassengernumbersafterprojectcompletion,suggestingsignificantunderutilizationofthenewlybuiltinfrastructure.

Ahighrateoffailuretoachievefinancialsustainabilitywasanotherreasonforthereport’sconclusion.Sevenoutofthe20airportsanalysedareunprofitableandwilllikelybeclosediftheyarenotsupportedbyongoingpublicfunding.

TheEuropeanCourtofAuditorsreportconcludedthat28%oftheEUfundinganalysed,or€129million,wenttowardsprojectsthatwere“notneededatall”19.

Smartinvestments,then,mustbebasedonarealisticpossibilityofincreasingusernumbersandprofitability.ExamplesofmisplacedinvestmentintheEuropeanCourtofAuditors’reportoftenneglectedboth.Onesuchexample is Kastoria National Airport in Greece.

Anexampleofcost-ineffectivecapacityexpansion:KastoriaNationalAirportinGreece.

KastoriaNationalAirport,with5,300inpassengertrafficin2013,isoneofthesmallestairportsanalysedbytheEuropeanCourtofAuditorsreport.ThepotentialforairinfrastructurebottlenecksintheregionarelimitedbecausevirtuallyallresidentswithintheKastoriaAirport’scatchmentareahaveaccesstoanearbycompetingairportwithin50minutesbyroad,andtwoothercompetingairportscanbeaccessedwithintwohours’drive.

Withinthiscontext,thereportassesseswhetherarunwayexpansionproject,costing€16.5million(34%ofwhichwasEUfunded),wasgoodvalueformoney.Theassessmentnotesthattheexpandedrunwayhasneverbeenusedbythetypeofaircraftitwasbuiltforandtheairportoperatedatalossbetween2005and2012.Havinglost€275foreverypassengerusingtheairportoverthisperiod,thereportconcludesthattheexpandedrunway“cannotbeconsideredasaneffectiveuseofpublicfunds”20.

18 ‘EU-funded airport infrastructures: poor value for money’, (2014), European Court of Auditors, December. Quotes are from pages 14 and 66.19 Ibid. Page 14.20 Ibid. Page 27.

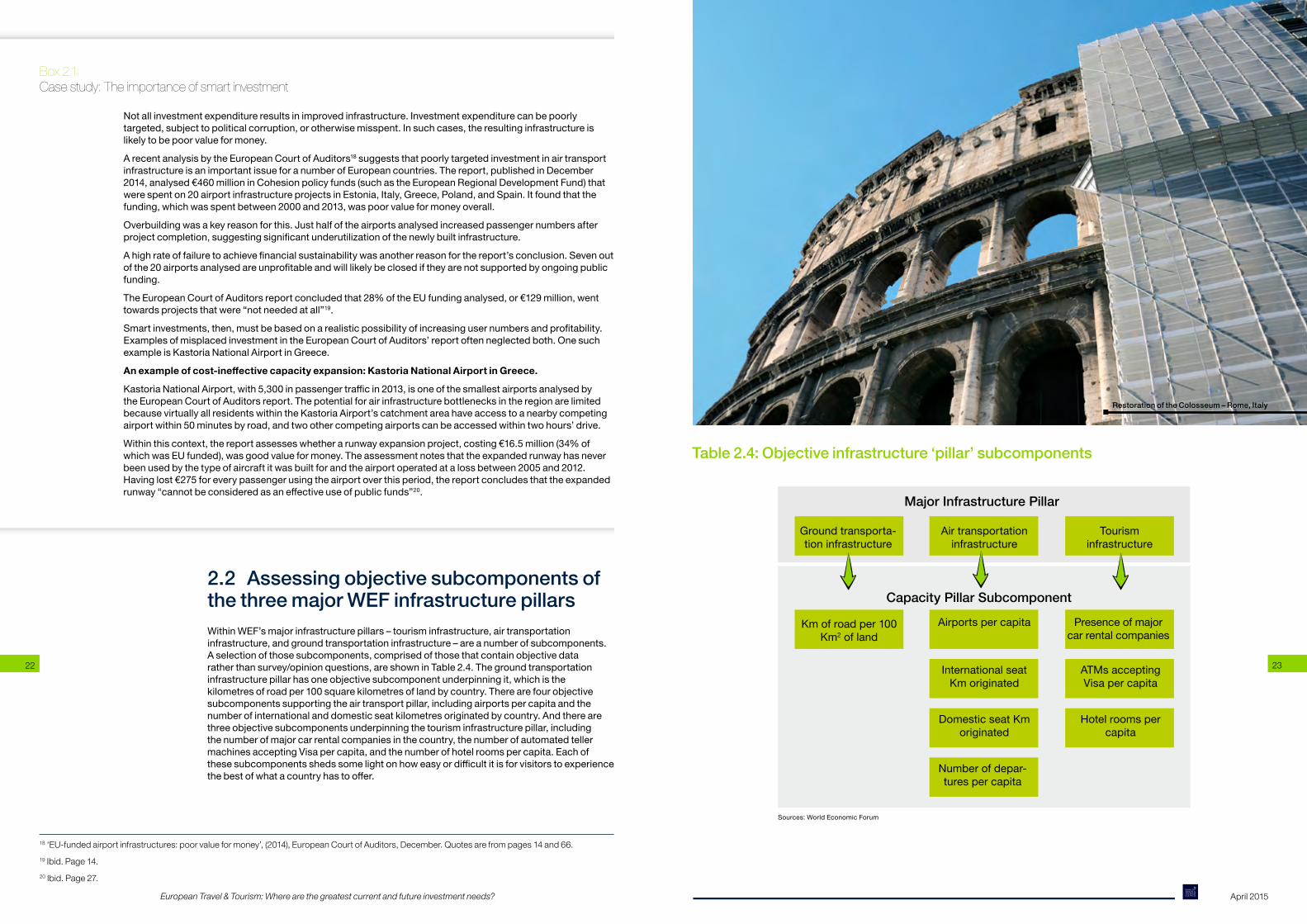

2.2 Assessing objective subcomponents of the three major WEF infrastructure pillarsWithinWEF’smajorinfrastructurepillars–tourisminfrastructure,airtransportationinfrastructure,andgroundtransportationinfrastructure–areanumberofsubcomponents.Aselectionofthosesubcomponents,comprisedofthosethatcontainobjectivedataratherthansurvey/opinionquestions,areshowninTable2.4.Thegroundtransportationinfrastructurepillarhasoneobjectivesubcomponentunderpinningit,whichisthekilometresofroadper100squarekilometresoflandbycountry.Therearefourobjectivesubcomponentssupportingtheairtransportpillar,includingairportspercapitaandthenumberofinternationalanddomesticseatkilometresoriginatedbycountry.Andtherearethreeobjectivesubcomponentsunderpinningthetourisminfrastructurepillar,includingthenumberofmajorcarrentalcompaniesinthecountry,thenumberofautomatedtellermachinesacceptingVisapercapita,andthenumberofhotelroomspercapita.Eachofthesesubcomponentsshedssomelightonhoweasyordifficultitisforvisitorstoexperiencethebestofwhatacountryhastooffer.

Table 2.4: Objective infrastructure ‘pillar’ subcomponents

Major Infrastructure Pillar

Capacity Pillar Subcomponent

Ground transporta-tion infrastructure

Kmofroadper100Km2 of land

Airports per capita

International seat Kmoriginated

Domestic seat Km originated

Number of depar-tures per capita

Air transportation infrastructure

Tourism infrastructure

Presenceofmajorcar rental companies

ATMsacceptingVisapercapita

Hotel rooms per capita

Sources:WorldEconomicForum

Restoration of the Colosseum – Rome, Italy

European Travel & Tourism: Where are the greatest current and future investment needs? April 2015

24 25

Table 2.5: Objective infrastructure subcomponent ranks

SwitzerlandSpainFranceUnited KingdomAustriaGermanyItalyIcelandCyprusMaltaIrelandGreeceNorwayDenmarkPortugalNetherlandsBelgiumFinlandSwedenLuxembourgCroatiaSloveniaEstoniaCzech RepublicTurkeyLatviaBulgariaMontenegroRussiaHungaryLithuaniaPolandSlovakiaUkraineRomaniaSerbiaMacedoniaAlbaniaBosnia and HerzegovinaMoldova

Western & Northern EuropeSouthern EuropeWestern & Northern EuropeWestern & Northern EuropeWestern & Northern EuropeWestern & Northern EuropeSouthern EuropeWestern & Northern EuropeSouthern EuropeSouthern EuropeWestern & Northern EuropeSouthern EuropeWestern & Northern EuropeWestern & Northern EuropeSouthern EuropeWestern & Northern EuropeWestern & Northern EuropeWestern & Northern EuropeWestern & Northern EuropeWestern & Northern EuropeSouthern EuropeSouthern EuropeEastern EuropeEastern EuropeSouthern EuropeEastern EuropeEastern EuropeSouthern EuropeEastern EuropeEastern EuropeEastern EuropeEastern EuropeEastern EuropeEastern EuropeEastern EuropeSouthern EuropeSouthern EuropeSouthern Europe Southern EuropeEastern Europe

6.16.05.85.75.75.75.55.55.45.45.45.45.45.25.25.15.15.15.04.74.74.64.64.64.54.44.44.44.34.13.83.73.73.73.63.33.23.1 2.92.6

9431132525222915121814106111716342838332182726367243119352023303932 4037

1234567891011121314151617181920212223242526272829303132333435363738 3940

1824717632127302011813926271210301930252353022301303015241416303030 2930

8168101971338151142435112332371752961712312234384042021243626302827 3233

7162111915264103117813121417525227192422286302329203136343733353932 4038

3221193724343851439930131531362025135291131812233401746282326102787 1622

66767777677777676666677677766777667766 74

2422181526312818310621314363154111216929302133725361939193427361735 2340

1139138235184282014191623713533407615312925122710223624261721323039 3438

1092751864321312183419252317112032142821242971530353337313816223936 2640

Country UN Classification* WEF composite infrastructure (scoreout of 7)

WEF composite infrastructure rank

KMs of road per 100sq. KMs land (rank)

KMs of road per vehicle (rank)

Airports per capita (rank)

Capacity: Inter-national seat KMs originated (rank)

Capacity: Domestic seat KMs originated (rank)

Number of departures per capita (rank)

Presence of major car rental companies (no out of 7)

ATMs accepting Visa per capita (rank)

Hotel Rooms per capita adjusted for visitors (rank)

26435447715273262222213333534101422222216 31

Direct Travel & Tourism contribution to GDP (%)

Sources:WorldEconomicForum

European Travel & Tourism: Where are the greatest current and future investment needs? April 2015

26 27

21 European Commission, (2012), ‘Measuring road congestion’.

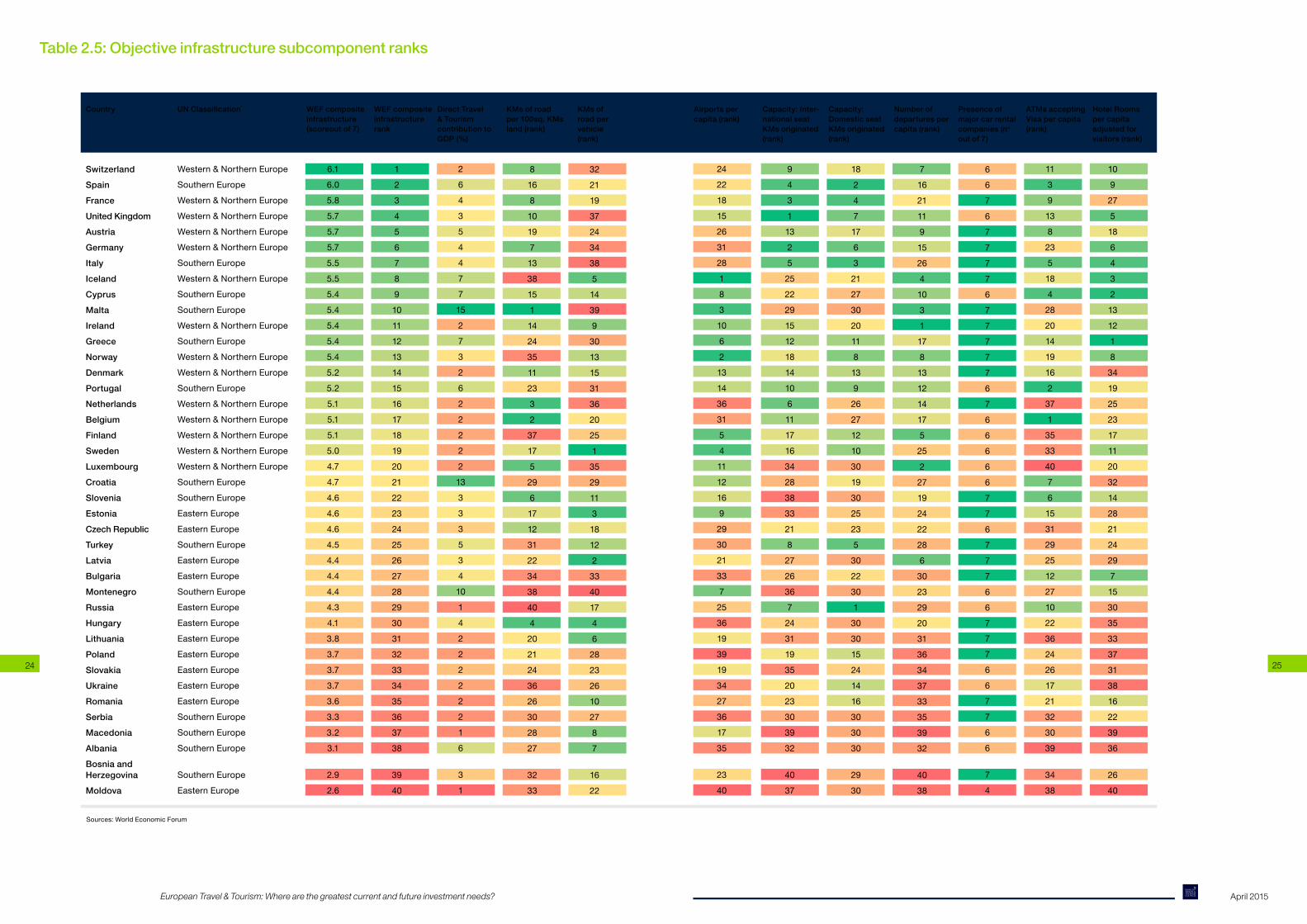

Table2.5showsobjectivesubcomponentranksforeachofthe40countriesforwhichWEFdataareavailable.Anumberofinterestingpatternsareapparentwithinthetable.

First,thereisroomforimprovementevenforcountrieswithhighaveragesamongthethreemajorinfrastructurepillars.Forexample,FranceandAustria,whichbothrankhighlyoverallforTravel&Tourisminfrastructurequalityandcapacity,couldstandtoincreasethenumberofavailablehotels.TheUnitedKingdom,theNetherlands,Luxembourg,andGermanyareamongthecountriesthatwouldbenefitfromincreasedroadcapacity.Eachhasatleast60%morecarsperkilometreofroadcapacitythantheEuropeanaverage.Thiscausescongestion,bothin urban areas and on inter-urban links. A recent European Commission report21 found that these countries have a disproportionate number of inter-urban links where delays of over ten seconds per kilometre are common.

Second,evenamongcountrieswithpoorinfrastructurescoresoverall,thereareraysofhope.Russia–perhapsnotsurprisingforsuchalargecountry–showsanimpressiveabilitytoshuttlepeoplearounddomestically,andhasgreaterATMsaturationthantheUnitedKingdom.TheCzechRepublic’sroadnetworkismoreextensivethanthatinItalyorIrelandifmeasuredrelativetolandmass.AndvisitorstoBulgariaandMontenegroareunlikelytocomplainofashortageofhotelrooms,whichareadequatetoservicetheirdomesticandvisitingpopulations.Suchcountriescanbuildonthesesuccessestoimprovetheiroverallinfrastructure capabilities. A sustained focus on the weaker points of infrastructure over the nextdecade(andbeyond)isimperativeiftheyaretomeetthebaselineforecastsfor Travel & Tourism’s economic impacts discussed earlier in this report.

2.3 Which countries have the greatest infrastructure needs between 2015 and 2025?Onanindividualcountrylevel,willpoorinfrastructurequalityandcapacityandalackofinvestmentconstraintheTravel&Tourismsector’sgrowth?Thissectionputsaspotlightonthecountriesthatfacethegreatestriskoffailingtomeetbaselineforecastsofeconomicbenefitsduetoinsufficientinfrastructureandinvestment.

Threeindicatorsareusedtoformthisassessment:

• HashistoricTravel&Tourisminvestmentgrowthbeenrelativelyhighorlow?Thisisassessedinthedecadeto2008,whichisrepresentativeofanormalisedmacroeconomicenvironment.

• WhatisthecurrentqualityandcapacityofTravel&Tourisminfrastructure,asassessedusingWEFcompositeinfrastructurescores?

• AccordingtoWTTCandOxfordEconomics’forecasts,isitexpectedthatTravel&Tourismdemandgrowthwilloutpaceinvestmentgrowthinthesectoroverthenextdecade?

Figure2.2presentstheresultsofthisassessment.Itgroupscountriesintothreecategories,rangingfromthosethatareatriskoflosingTravel&Tourisminfrastructurecompetitivenessoverthenextdecade,tothosethatarewell-placedtobenefitfromforecasteddemandbetween2015and2025.

Thegroupsincludethosethatare:

• Well-placed:Thisgroupofcountries,exemplifiedbyAustria,GermanyandtheUnitedKingdom,hashighexistingqualityandcapacityofTravel&Tourisminfrastructurewhichtheyareexpectedtomaintainandimprovebetween2015and2025.Withinvestmentgrowthexpectedtooutpacedemandoverthatperiod,thesecountriesarewell-placedtocapturethefullbenefitsofforecastedTravel&Tourismdemand.

• Well-placed, but with key risks:France,Italy,Switzerland,Ireland,andGreeceareonesetofcountriesincludedinthiscategory.EachofthemhasexistingTravel&TourismqualityandcapacitythatisgreaterthantheEuropeanaverage.Yettheirstrongpositionsarelikelytodeterioratesomewhatoverthenextdecade,sinceTravel&TourismdemandgrowthisforecasttooutstripTravel&Tourisminvestmentgrowthovertheperiod.Similarly,DenmarkandFinlandhavebetterthanaverageTravel&Tourisminfrastructurequalityandcapacity;however,weakhistoricalinvestmentgrowthpresentsriskstotheforecastthatinvestmentgrowthwillexceeddemandgrowthinthenextdecade.SloveniaandLatviaarealso“wellplaced,withrisks”.Theirkeystrengthisthattheyareexpectedtoseeinvestmentgrowththatisstrongerthandemandgrowthoverthenextdecade;theirkeyriskistheirexistinginfrastructurequalityandcapacity,whichisbelowtheEuropeanaverage.

• At medium or high risk:ThiscategoryincludescountrieslikeAlbania,Bosnia,andMoldova,whichareconsideredtobeathighriskbecausetheyhavethepoorestexistinginfrastructurequalityandcapacityoutofthe40countriesforwhichdataareavailable.Croatia,Serbia,andSlovakiaarealsoconsideredatrisk,becauseTravel&Tourisminvestmentgrowthisexpectedtolagbehinddemandgrowthoverthenextdecade.Portugal,havingrelativelystrongexistinginfrastructurecapabilities,isaspecialcase:becausedemandgrowthisexpectedtooutpaceinvestmentgrowthbysuchawidemargin,thecountryfacesariskthatitscurrentinfrastructurequalityandcapacitywilldegradeoverthenextdecade.

Construction of the Kalinin-Solntsevo Subway – Moscow, Russia

European Travel & Tourism: Where are the greatest current and future investment needs? April 2015

28 29

Figure 2.2: Country typologies: will current infrastructure quality and capacity and lack of investment constrain Travel & Tourism sector growth?

SwitzerlandSpainFranceUnitedKingdomAustriaGermanyItalyIcelandCyprusMaltaIrelandGreeceNorwayDenmarkPortugalNetherlandsBelgiumFinlandSwedenCroatiaSloveniaEstoniaCzech RepublicTurkeyLatviaBulgariaRussiaHungaryLithuaniaPolandSlovakiaRomaniaSerbiaMacedoniaAlbaniaBosnia and Herzegovina

-0.4 -0.2 0.0 0.2 0.4 0.6 0.8 1.0 1.2 1.4 1.6 1.8 2.0BalanceLess favourable ratioHighercurrent

Travel & Tourism infrastructure

quality and capacity

More favourable ratio

Legend: Well-placed At medium riskWell-placed, but key risks

Athighrisk

* The T&T investment to demand ratio is the ratio of forecasted average annual Travel & Tourism investment growth over the next decade divided by forecasted average annual Travel & Tourism demand over the same period.

Note: Four countries are excluded from this diagram. Belarus lacks WEF infrastructure data, forecasts for the Ukraine at the time of publication are vastly more uncertain than is typical due to the country’s ongoing conflict, and Luxembourg and Montenegro are outliers that obscure trends among the 37 other countries in the diagram.

Lower current Travel & Tourism

infrastructure quality and

capacity

The outlook for European Travel & Tourism investment spending

chapter 3

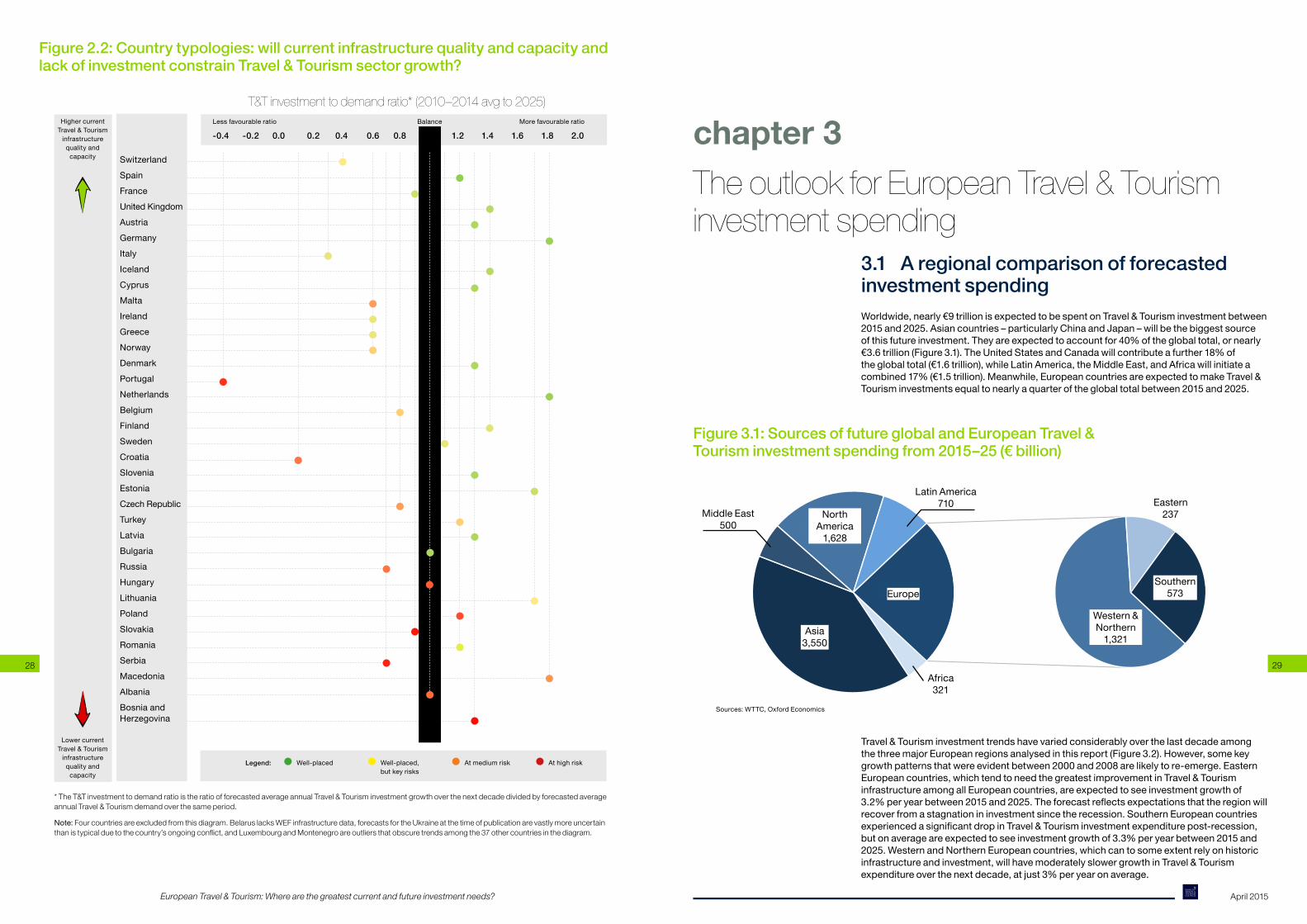

3.1 A regional comparison of forecasted investment spendingWorldwide,nearly€9trillionisexpectedtobespentonTravel&Tourisminvestmentbetween2015and2025.Asiancountries–particularlyChinaandJapan–willbethebiggestsourceofthisfutureinvestment.Theyareexpectedtoaccountfor40%oftheglobaltotal,ornearly€3.6trillion(Figure3.1).TheUnitedStatesandCanadawillcontributeafurther18%oftheglobaltotal(€1.6trillion),whileLatinAmerica,theMiddleEast,andAfricawillinitiateacombined17%(€1.5trillion).Meanwhile,EuropeancountriesareexpectedtomakeTravel&Tourisminvestmentsequaltonearlyaquarteroftheglobaltotalbetween2015and2025.

Figure 3.1: Sources of future global and European Travel & Tourism investment spending from 2015–25 (€ billion)

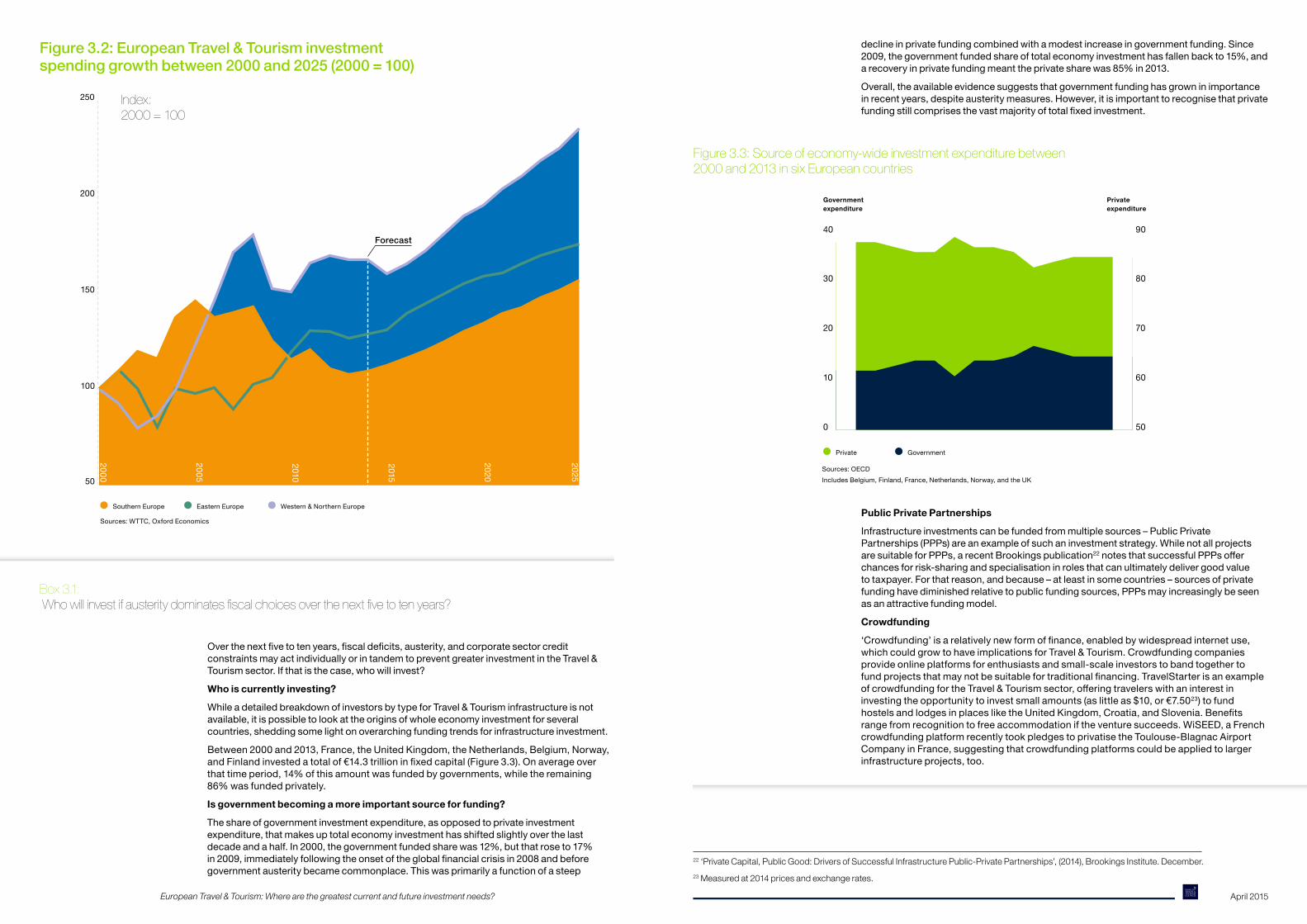

Travel&TourisminvestmenttrendshavevariedconsiderablyoverthelastdecadeamongthethreemajorEuropeanregionsanalysedinthisreport(Figure3.2).However,somekeygrowthpatternsthatwereevidentbetween2000and2008arelikelytore-emerge.EasternEuropeancountries,whichtendtoneedthegreatestimprovementinTravel&TourisminfrastructureamongallEuropeancountries,areexpectedtoseeinvestmentgrowthof3.2%peryearbetween2015and2025.Theforecastreflectsexpectationsthattheregionwillrecoverfromastagnationininvestmentsincetherecession.SouthernEuropeancountriesexperiencedasignificantdropinTravel&Tourisminvestmentexpenditurepost-recession,butonaverageareexpectedtoseeinvestmentgrowthof3.3%peryearbetween2015and2025.WesternandNorthernEuropeancountries,whichcantosomeextentrelyonhistoricinfrastructureandinvestment,willhavemoderatelyslowergrowthinTravel&Tourismexpenditureoverthenextdecade,atjust3%peryearonaverage.

T&T investment to demand ratio* (2010–2014 avg to 2025)

Africa, 321

Asia, 3,550

Middle East, 500

North America, 1,628

Latin America, 710

Western & Northern, 1,321

Eastern, 237

Southern, 573 Europe

Source: WTTC, Oxford Economics

Sources:WTTC,OxfordEconomics

Europe

Asia 3,550

Southern 573

Eastern 237

Africa 321

Western & Northern 1,321

North America 1,628

Middle East 500

Latin America 710

European Travel & Tourism: Where are the greatest current and future investment needs? April 2015

30 31

Figure 3.2: European Travel & Tourism investment spending growth between 2000 and 2025 (2000 = 100)

Box 3.1: Who will invest if austerity dominates fiscal choices over the next five to ten years?

Overthenextfivetotenyears,fiscaldeficits,austerity,andcorporatesectorcreditconstraintsmayactindividuallyorintandemtopreventgreaterinvestmentintheTravel&Tourismsector.Ifthatisthecase,whowillinvest?

Who is currently investing?

While a detailed breakdown of investors by type for Travel & Tourism infrastructure is not available,itispossibletolookattheoriginsofwholeeconomyinvestmentforseveralcountries,sheddingsomelightonoverarchingfundingtrendsforinfrastructureinvestment.

Between2000and2013,France,theUnitedKingdom,theNetherlands,Belgium,Norway,andFinlandinvestedatotalof€14.3trillioninfixedcapital(Figure3.3).Onaverageoverthattimeperiod,14%ofthisamountwasfundedbygovernments,whiletheremaining86%wasfundedprivately.

Is government becoming a more important source for funding?

Theshareofgovernmentinvestmentexpenditure,asopposedtoprivateinvestmentexpenditure,thatmakesuptotaleconomyinvestmenthasshiftedslightlyoverthelastdecadeandahalf.In2000,thegovernmentfundedsharewas12%,butthatroseto17%in2009,immediatelyfollowingtheonsetoftheglobalfinancialcrisisin2008andbeforegovernmentausteritybecamecommonplace.Thiswasprimarilyafunctionofasteep

declineinprivatefundingcombinedwithamodestincreaseingovernmentfunding.Since2009,thegovernmentfundedshareoftotaleconomyinvestmenthasfallenbackto15%,andarecoveryinprivatefundingmeanttheprivatesharewas85%in2013.

Overall,theavailableevidencesuggeststhatgovernmentfundinghasgrowninimportanceinrecentyears,despiteausteritymeasures.However,itisimportanttorecognisethatprivatefundingstillcomprisesthevastmajorityoftotalfixedinvestment.

Figure 3.3: Source of economy-wide investment expenditure between 2000 and 2013 in six European countries

0 50

10 60

20 70

30 80

40 90

Public Private Partnerships

Infrastructure investments can be funded from multiple sources – Public Private Partnerships(PPPs)areanexampleofsuchaninvestmentstrategy.WhilenotallprojectsaresuitableforPPPs,arecentBrookingspublication22notesthatsuccessfulPPPsofferchancesforrisk-sharingandspecialisationinrolesthatcanultimatelydelivergoodvaluetotaxpayer.Forthatreason,andbecause–atleastinsomecountries–sourcesofprivatefundinghavediminishedrelativetopublicfundingsources,PPPsmayincreasinglybeseenasanattractivefundingmodel.

Crowdfunding

‘Crowdfunding’isarelativelynewformoffinance,enabledbywidespreadinternetuse,whichcouldgrowtohaveimplicationsforTravel&Tourism.Crowdfundingcompaniesprovideonlineplatformsforenthusiastsandsmall-scaleinvestorstobandtogethertofundprojectsthatmaynotbesuitablefortraditionalfinancing.TravelStarterisanexampleofcrowdfundingfortheTravel&Tourismsector,offeringtravelerswithaninterestininvestingtheopportunitytoinvestsmallamounts(aslittleas$10,or€7.5023)tofundhostelsandlodgesinplacesliketheUnitedKingdom,Croatia,andSlovenia.Benefitsrangefromrecognitiontofreeaccommodationiftheventuresucceeds.WiSEED,aFrenchcrowdfundingplatformrecentlytookpledgestoprivatisetheToulouse-BlagnacAirportCompanyinFrance,suggestingthatcrowdfundingplatformscouldbeappliedtolargerinfrastructureprojects,too.

22 ‘Private Capital, Public Good: Drivers of Successful Infrastructure Public-Private Partnerships’, (2014), Brookings Institute. December.23 Measured at 2014 prices and exchange rates.

50

2000

2005

2010

2015

2020

2025

Forecast

Southern Europe Eastern Europe Western & Northern Europe

Sources:WTTC,OxfordEconomics

Index: 2000 = 100

100

150

200

250

Private Government

Government expenditure

Private expenditure

Sources:OECDIncludesBelgium,Finland,France,Netherlands,Norway,andtheUK

European Travel & Tourism: Where are the greatest current and future investment needs? April 2015

32 33

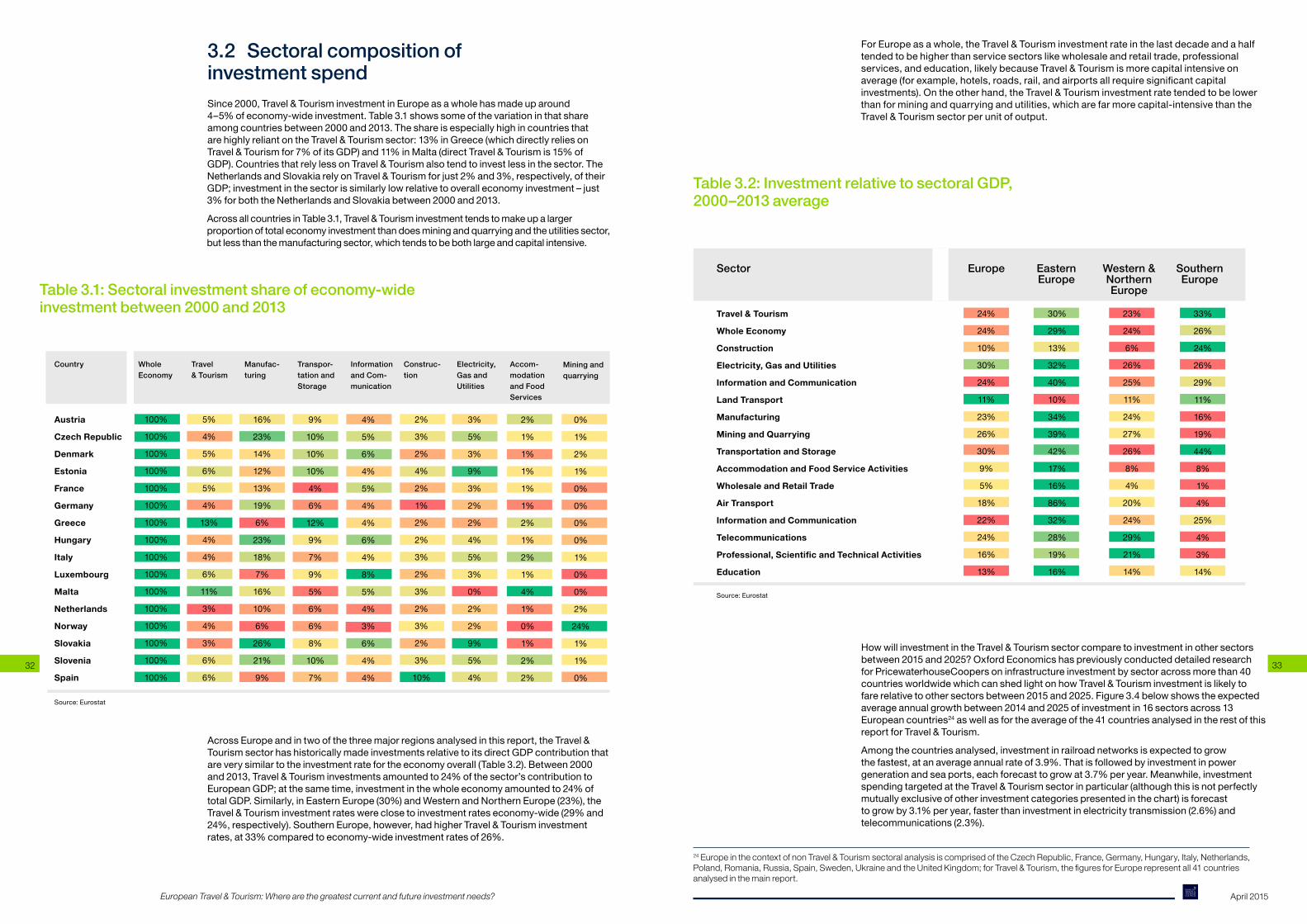

3.2 Sectoral composition of investment spendSince2000,Travel&TourisminvestmentinEuropeasawholehasmadeuparound4–5%ofeconomy-wideinvestment.Table3.1showssomeofthevariationinthatshareamongcountriesbetween2000and2013.TheshareisespeciallyhighincountriesthatarehighlyreliantontheTravel&Tourismsector:13%inGreece(whichdirectlyreliesonTravel&Tourismfor7%ofitsGDP)and11%inMalta(directTravel&Tourismis15%ofGDP).CountriesthatrelylessonTravel&Tourismalsotendtoinvestlessinthesector.TheNetherlandsandSlovakiarelyonTravel&Tourismforjust2%and3%,respectively,oftheirGDP;investmentinthesectorissimilarlylowrelativetooveralleconomyinvestment–just3%forboththeNetherlandsandSlovakiabetween2000and2013.

AcrossallcountriesinTable3.1,Travel&Tourisminvestmenttendstomakeupalargerproportionoftotaleconomyinvestmentthandoesminingandquarryingandtheutilitiessector,butlessthanthemanufacturingsector,whichtendstobebothlargeandcapitalintensive.

Table 3.1: Sectoral investment share of economy-wide investment between 2000 and 2013

ForEuropeasawhole,theTravel&Tourisminvestmentrateinthelastdecadeandahalftendedtobehigherthanservicesectorslikewholesaleandretailtrade,professionalservices,andeducation,likelybecauseTravel&Tourismismorecapitalintensiveonaverage(forexample,hotels,roads,rail,andairportsallrequiresignificantcapitalinvestments).Ontheotherhand,theTravel&Tourisminvestmentratetendedtobelowerthanforminingandquarryingandutilities,whicharefarmorecapital-intensivethantheTravel & Tourism sector per unit of output.

Table 3.2: Investment relative to sectoral GDP, 2000–2013 average

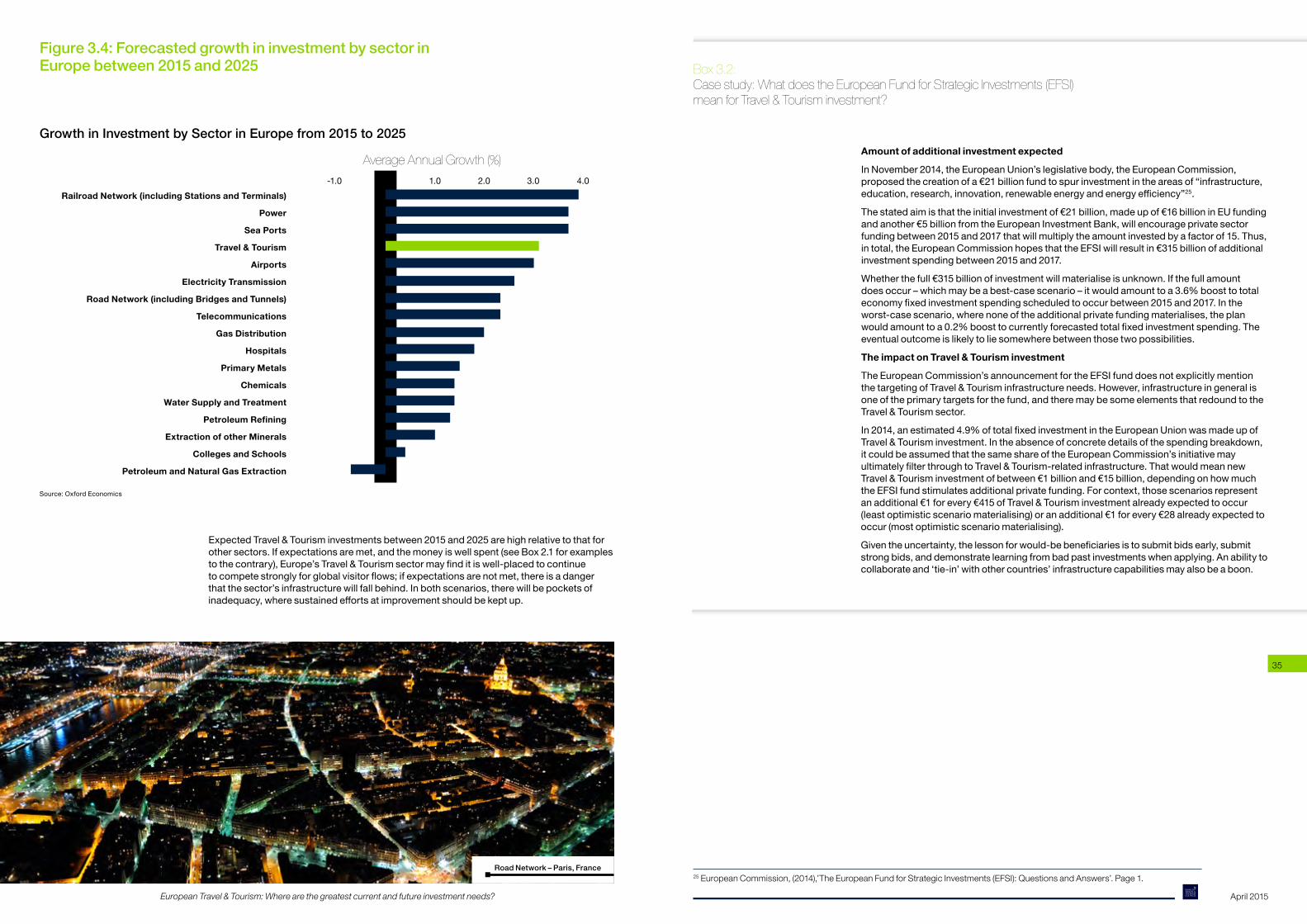

How will investment in the Travel & Tourism sector compare to investment in other sectors between2015and2025?OxfordEconomicshaspreviouslyconducteddetailedresearchforPricewaterhouseCoopersoninfrastructureinvestmentbysectoracrossmorethan40countriesworldwidewhichcanshedlightonhowTravel&Tourisminvestmentislikelytofarerelativetoothersectorsbetween2015and2025.Figure3.4belowshowstheexpectedaverageannualgrowthbetween2014and2025ofinvestmentin16sectorsacross13European countries24aswellasfortheaverageofthe41countriesanalysedintherestofthisreport for Travel & Tourism.

Amongthecountriesanalysed,investmentinrailroadnetworksisexpectedtogrowthefastest,atanaverageannualrateof3.9%.Thatisfollowedbyinvestmentinpowergenerationandseaports,eachforecasttogrowat3.7%peryear.Meanwhile,investmentspendingtargetedattheTravel&Tourismsectorinparticular(althoughthisisnotperfectlymutuallyexclusiveofotherinvestmentcategoriespresentedinthechart)isforecasttogrowby3.1%peryear,fasterthaninvestmentinelectricitytransmission(2.6%)andtelecommunications(2.3%).

24 Europe in the context of non Travel & Tourism sectoral analysis is comprised of the Czech Republic, France, Germany, Hungary, Italy, Netherlands, Poland, Romania, Russia, Spain, Sweden, Ukraine and the United Kingdom; for Travel & Tourism, the figures for Europe represent all 41 countries analysed in the main report.

AcrossEuropeandintwoofthethreemajorregionsanalysedinthisreport,theTravel&Tourism sector has historically made investments relative to its direct GDP contribution that areverysimilartotheinvestmentratefortheeconomyoverall(Table3.2).Between2000and2013,Travel&Tourisminvestmentsamountedto24%ofthesector’scontributiontoEuropeanGDP;atthesametime,investmentinthewholeeconomyamountedto24%oftotalGDP.Similarly,inEasternEurope(30%)andWesternandNorthernEurope(23%),theTravel&Tourisminvestmentrateswereclosetoinvestmentrateseconomy-wide(29%and24%,respectively).SouthernEurope,however,hadhigherTravel&Tourisminvestmentrates,at33%comparedtoeconomy-wideinvestmentratesof26%.

Travel & Tourism

Whole Economy

Construction

Electricity, Gas and Utilities

Information and Communication

Land Transport

Manufacturing

Mining and Quarrying

Transportation and Storage

Accommodation and Food Service Activities

Wholesale and Retail Trade

Air Transport

Information and Communication

Telecommunications

Professional,ScientificandTechnicalActivities

Education

24%

24%

10%

30%

24%

11%

23%

26%

30%

9%

5%

18%

22%

24%

16%

13%

23%

24%

6%

26%

25%

11%

24%

27%

26%

8%

4%

20%

24%

29%

21%

14%

30%

29%

13%

32%

40%

10%

34%

39%

42%

17%

16%

86%

32%

28%

19%

16%

33%

26%

24%

26%

29%

11%

16%

19%

44%

8%

1%

4%

25%

4%

3%

14%

Source:Eurostat

Sector Europe Eastern Europe

Southern Europe

Western & Northern Europe

Austria

Czech Republic

Denmark

Estonia

France

Germany

Greece

Hungary

Italy

Luxembourg

Malta

Netherlands

Norway

Slovakia

Slovenia

Spain

100%

100%

100%

100%

100%

100%

100%

100%

100%

100%

100%

100%

100%

100%

100%

100%

5%

4%

5%

6%

5%

4%

13%

4%

4%

6%

11%

3%

4%

3%

6%

6%

2%

3%

2%

4%

2%

1%

2%

2%

3%

2%

3%

2%

3%

2%

3%

10%

16%

23%

14%

12%

13%

19%

6%

23%

18%

7%

16%

10%

6%

26%

21%

9%

3%

5%

3%

9%

3%

2%

2%

4%

5%

3%

0%

2%

2%

9%

5%

4%

9%

10%

10%

10%

4%

6%

12%

9%

7%

9%

5%

6%

6%

8%

10%

7%

2%

1%

1%

1%

1%

1%

2%

1%

2%

1%

4%

1%

0%

1%

2%

2%

4%

5%

6%

4%

5%

4%

4%

6%

4%

8%

5%

4%

3%

6%

4%

4%

0%

1%

2%

1%

0%

0%

0%

0%

1%

0%

0%

2%

24%

1%

1%

0%

Country Whole Economy

Travel & Tourism

Manufac-turing

Transpor-tation and Storage

Information and Com-munication

Construc-tion

Electricity, Gas and Utilities

Accom-modation and Food Services

Mining and quarrying

Source:Eurostat

European Travel & Tourism: Where are the greatest current and future investment needs? April 2015

34 35

Figure 3.4: Forecasted growth in investment by sector in Europe between 2015 and 2025

ExpectedTravel&Tourisminvestmentsbetween2015and2025arehighrelativetothatforothersectors.Ifexpectationsaremet,andthemoneyiswellspent(seeBox2.1forexamplestothecontrary),Europe’sTravel&Tourismsectormayfinditiswell-placedtocontinuetocompetestronglyforglobalvisitorflows;ifexpectationsarenotmet,thereisadangerthatthesector’sinfrastructurewillfallbehind.Inbothscenarios,therewillbepocketsofinadequacy,wheresustainedeffortsatimprovementshouldbekeptup.

Box 3.2: Case study: What does the European Fund for Strategic Investments (EFSI) mean for Travel & Tourism investment?

Amount of additional investment expected

InNovember2014,theEuropeanUnion’slegislativebody,theEuropeanCommission,proposedthecreationofa€21billionfundtospurinvestmentintheareasof“infrastructure,education,research,innovation,renewableenergyandenergyefficiency”25.

Thestatedaimisthattheinitialinvestmentof€21billion,madeupof€16billioninEUfundingandanother€5billionfromtheEuropeanInvestmentBank,willencourageprivatesectorfundingbetween2015and2017thatwillmultiplytheamountinvestedbyafactorof15.Thus,intotal,theEuropeanCommissionhopesthattheEFSIwillresultin€315billionofadditionalinvestmentspendingbetween2015and2017.

Whetherthefull€315billionofinvestmentwillmaterialiseisunknown.Ifthefullamountdoesoccur–whichmaybeabest-casescenario–itwouldamounttoa3.6%boosttototaleconomyfixedinvestmentspendingscheduledtooccurbetween2015and2017.Intheworst-casescenario,wherenoneoftheadditionalprivatefundingmaterialises,theplanwouldamounttoa0.2%boosttocurrentlyforecastedtotalfixedinvestmentspending.Theeventual outcome is likely to lie somewhere between those two possibilities.

The impact on Travel & Tourism investment

TheEuropeanCommission’sannouncementfortheEFSIfunddoesnotexplicitlymentionthetargetingofTravel&Tourisminfrastructureneeds.However,infrastructureingeneralisoneoftheprimarytargetsforthefund,andtheremaybesomeelementsthatredoundtotheTravel & Tourism sector.

In2014,anestimated4.9%oftotalfixedinvestmentintheEuropeanUnionwasmadeupofTravel&Tourisminvestment.Intheabsenceofconcretedetailsofthespendingbreakdown,it could be assumed that the same share of the European Commission’s initiative may ultimatelyfilterthroughtoTravel&Tourism-relatedinfrastructure.ThatwouldmeannewTravel&Tourisminvestmentofbetween€1billionand€15billion,dependingonhowmuchtheEFSIfundstimulatesadditionalprivatefunding.Forcontext,thosescenariosrepresentanadditional€1forevery€415ofTravel&Tourisminvestmentalreadyexpectedtooccur(leastoptimisticscenariomaterialising)oranadditional€1forevery€28alreadyexpectedtooccur(mostoptimisticscenariomaterialising).

Giventheuncertainty,thelessonforwould-bebeneficiariesistosubmitbidsearly,submitstrongbids,anddemonstratelearningfrombadpastinvestmentswhenapplying.Anabilitytocollaborate and ‘tie-in’ with other countries’ infrastructure capabilities may also be a boon.

25 European Commission, (2014),’The European Fund for Strategic Investments (EFSI): Questions and Answers’. Page 1.

Railroad Network (including Stations and Terminals)

Power

Sea Ports

Travel & Tourism

Airports

Electricity Transmission

Road Network (including Bridges and Tunnels)

Telecommunications

Gas Distribution

Hospitals

Primary Metals

Chemicals

Water Supply and Treatment

PetroleumRefining

Extraction of other Minerals

Colleges and Schools

Petroleum and Natural Gas Extraction

-1.0 0.0 1.0 2.0 3.0 4.0

Average Annual Growth (%)

Source:OxfordEconomics

Growth in Investment by Sector in Europe from 2015 to 2025

Road Network – Paris, France

European Travel & Tourism: Where are the greatest current and future investment needs? April 2015

36 37

Putting Travel & Tourism investment on European governments’ agendas

The European Travel & Tourism sector is forecast to grow in importance over the next decade, according to the WTTC’s latest annual economic impact research

In2014,theTravel&Tourismsectorsupported33.5milliondirect,indirect,andinducedjobs(9.3%oftheEuropeantotal)andnearly€1.6trillioninGDP(9.3%ofEuropeanGDP).TheTravel&Tourismsector’stotaleconomiccontributionisexpectedtogrowto38millionjobs(10.4%ofEuropeanemployment)and€2.1trillioninGDPby2025(9.9%ofEuropeanGDP).Thisassumesthatsupply-sidecapacity,inareaslikeinfrastructureandtalent,doesnotactasaconstrainttotthesector’sgrowth.

Both industry and governments should therefore place Travel & Tourism investment high on their agendas, or risk failing to achieve the baseline forecast andresultingeconomicbenefits

ThestrongstatisticalrelationshipbetweenTravel&Tourisminfrastructurecapabilitiesand the sector’s economic impact means the issue warrants attention from both private andpublicinvestorsandpolicy-makers.Italsohighlightstheneedforbusiness-friendlypoliciesandlegislationintheTravel&Tourismsectortosupportandencourageinfrastructuredevelopment.Butanynewinfrastructuremustrepresenttherightsortofinvestmenttomeetspecificdemandrequirementsandaddressgaps,andnotbeinvestmentforthesakeofinvestment,giventhemoreconstrainedfinancialenvironmentand lessons from past ‘bad’ investments.

Travel & Tourism investment strategies must be evidence-based

ThisreportprovidesforecastsforTravel&Tourisminvestmentanddemandgrowth,providinganevidence-baseforindustryandgovernmentinvestmentstrategy,aswellasnational-leveltourismdevelopmentplansandoveralltourismstrategy.

This report highlights unique opportunities and challenges for three country typologies

• Well-placed:Austria,GermanyandtheUnitedKingdomshouldfocusonmaintainingandimprovingtheirexisting,high-qualityinfrastructure.AkeystrengthisthatTravel&TourisminvestmentgrowthisforecasttooutpaceTravel&Tourismdemandgrowthoverthenextdecade.

• Well-placed but with key risks:Denmark,Finland,France,Greece,Ireland,Italy,Latvia,Slovenia,andSwitzerlandshouldbewaryofcomplacencyandrelyingonexistinginfrastructurecapabilities.SeveralofthesecountriesriskTravel&TourisminvestmentgrowthinthenextdecadebeingoverwhelmedbygrowthinTravel&Tourismdemand.Othershavearecenthistory(inthedecadefrom1998to2008)ofdeclininginvestmentgrowth,presentingariskofreturningtopre-recessioninvestmentpatternsratherthanmeetingbaselineforecastsofinvestmentto2025.

• At medium or high risk:Albania,BosniaandHerzegovina,andMoldovaneedtoaddressurgentexistinginfrastructurequalityandcapacityissues.Croatia,Portugal,Serbia,andSlovakiaarelikelytoseeTravel&Tourismdemandgrowththatsignificantlyoutpaces investment in the sector over the next decade. Each of these countries is at riskoffailingtofullybenefitfromforecasteddemand.

conclusion

A focus on targeted, smart-investment will be critical to success

A recent report by the European Court of Auditors shows that additional capacity is not alwaysbebeneficial.Toavoidoverbuildingandensurehighreturnsandvalue-for-moneyinvestment,investmentstrategiesmustrealisticallyplantoincreasetherelevantuserbaseaftercompletionandthenachievefinancialsustainability.Well-targetedinvestmentsmayinvolveadditionalcapacity,buttheycanalsomaintainandexpandexistingcapacity,andencourageimprovementsinquality,competitiveness,productivityandsustainability.

Travel&Tourisminvestmentshouldbeongoingratherthanone-off

Travel&Tourismmarketsaredynamic,andtastesevolveovertimealongwithindividualdefinitionsofhomeversusluxurycomforts.ThiscallsforaconsistentandsustainedfocusonTravel&Tourisminvestmentacrosstimeinordertokeepupwithchangingmarketdemand characteristics.

Inperiodsofgovernmentandfinancialsectorfundingconstraints,investorsinthe Travel & Tourism sector should seek cross-border collaboration and creative funding options

Cross-borderTravel&TourisminfrastructurecollaborationcanbeuniquelyeffectiveonthecontinentbecauseofEurope’srelativelysmallgeographicsizeandexistingintegration.And,particularlyinperiodsoffiscalausterity,thoseengagedinTravel&Tourisminvestmentmaywishtoconsidercreativefundingoptionslikepublicprivatepartnershipsorcrowdfunding.

Cruise Ships in the Aegean Sea – Santorini, Greece

European Travel & Tourism: Where are the greatest current and future investment needs?

38

Sewage Treatment Plant – Wroclaw, Poland

European Travel & Tourism: Where are the greatest current and future investment needs?

40

The Harlequin Building65SouthwarkStreet

London,SE10HRUnitedKingdom

T.+44(0)2074818007F.+44(0)[email protected]

www.wttc.org