europe's best kept secret why portugal should ... best kept... · europe's best kept...

TRANSCRIPT

Europe's Best Kept SecretWhy Portugal should be your top tax choice

www.pwc.pt

Jaime Carvalho Esteves

Luís Flipe Sousa

29 October 2015

PwC

Agenda

1. IntroductionThe changing “tax world”

2. Portugal as a top choice for individualsThe Non Habitual Tax ResidentThe Golden VisaOther taxes or the lack of it

3. Things to remember

2

29 october 2015Why Portugal should be your top tax choice

PwC

1. IntroductionThe changing “tax world”

3

29 october 2015Why Portugal should be your top tax choice

PwC

1. IntroductionThe changing “tax world”

4

29 october 2015Why Portugal should be your top tax choice

PwC

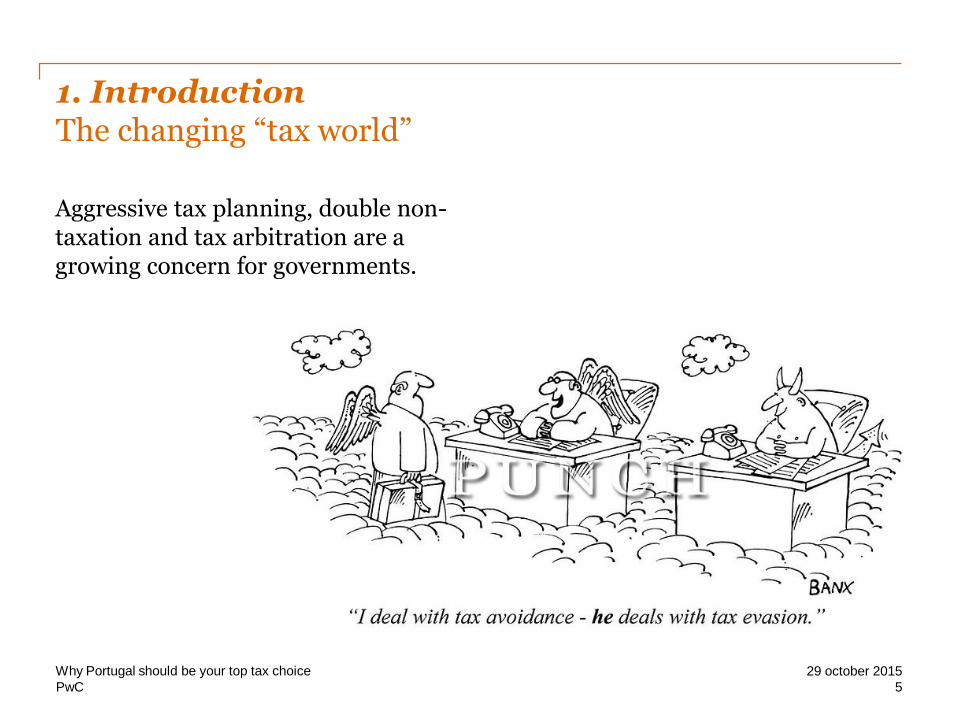

1. IntroductionThe changing “tax world”

Aggressive tax planning, double non-taxation and tax arbitration are a growing concern for governments.

5

29 october 2015Why Portugal should be your top tax choice

PwC

• Need for tax revenues.

• Tax competition.

• Transparency.

• Exchange of information (automatic).

• Changes in tax legislation – for example:

- Increasing the tax burden.

- Non Domiciled UK residents.

- Flexible UK pension withdrawals.

• Greater mobility/travel.

1. IntroductionThe changing “tax world”

6

29 october 2015Why Portugal should be your top tax choice

PwC

2. Portugal as a top choice for individuals

7

29 october 2015Why Portugal should be your top tax choice

Why is Portugal your top tax choice?

PwC

2. Portugal as a top choice for individuals

The Non Habitual Tax Resident

8

29 october 2015Why Portugal should be your top tax choice

PwC

The Non Habitual Tax Resident

Why was this regime created?

• Portugal intends to become a preferential residence option for ultra and high net worth individuals and their families.

• To attract excellence centres and R&D departments of multinational companies and, in general, activities regarded as “high value-added”.

• NHR regime is very favourable when compared with similar tax regimes in other countries.

9

29 october 2015Why Portugal should be your top tax choice

PwC

The Non Habitual Tax Resident

Who may benefit from the regime?

The regime is applicable to taxpayers who meet the following conditions:

• qualify as tax resident in Portugal in a certain tax year under Portuguese tax legislation; and

• did not qualify as tax resident in Portugal in any of the previous 5 years.

10

29 october 2015Why Portugal should be your top tax choice

PwC

The Non Habitual Tax Resident

For how long may an individual benefit from the regime?

A qualifying individual may benefit from the regime for a period of 10 consecutive years:

• during the 10-year period, the individual may break Portuguese tax residency and resume it at a later stage within the 10-year period;

• the taxation as NHR depends on the registration of the NHR status with the Portuguese Tax Authorities.

• application for the registration as Non-Habitual Resident should be made by 31 March of the year following the one in which the applicant becomes Portuguese tax resident.

11

29 october 2015Why Portugal should be your top tax choice

PwC

The Non Habitual Tax Resident

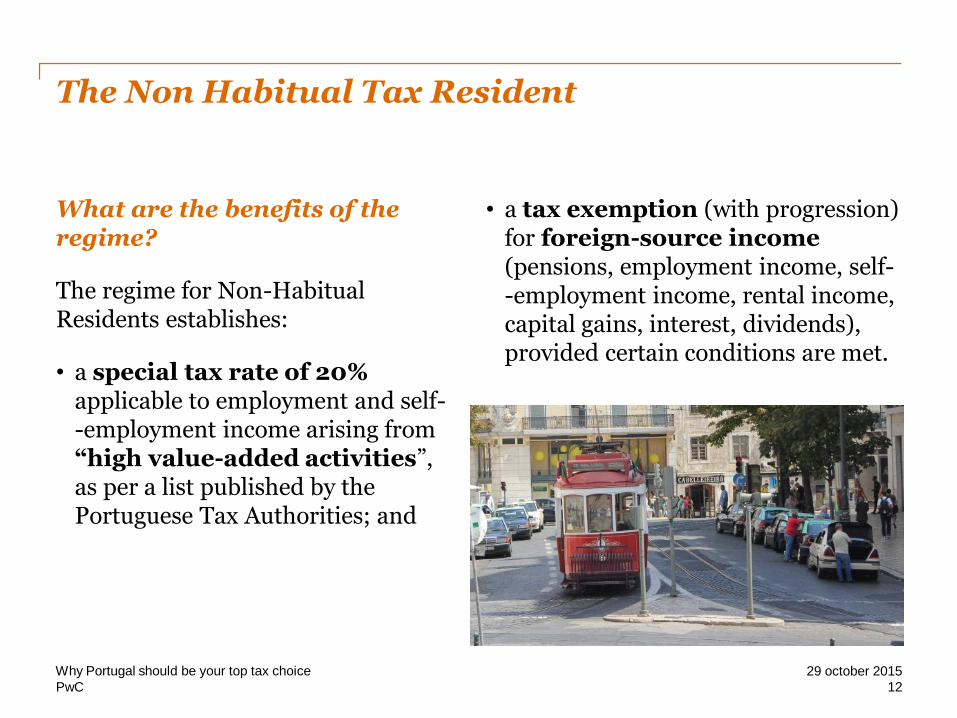

What are the benefits of the regime?

The regime for Non-Habitual Residents establishes:

• a special tax rate of 20% applicable to employment and self--employment income arising from “high value-added activities”, as per a list published by the Portuguese Tax Authorities; and

• a tax exemption (with progression) for foreign-source income (pensions, employment income, self--employment income, rental income, capital gains, interest, dividends), provided certain conditions are met.

12

29 october 2015Why Portugal should be your top tax choice

PwC

The Non Habitual Tax Resident

Taxation of foreign pensions

How is foreign-source pension income taxed?

Foreign-source pension income may benefit from an exemption (with progression), if:

• that income is taxed in the country of source in accordance with the DTT between Portugal and that country; or

Pensions may be excluded from taxation both in Portugal and in the country of source

• the income is not regarded as being obtained in Portugal, in accordance with domestic legislation. Pension income is regarded as Portuguese-source income only if it is paid by a tax resident entity or a permanent establishment in Portugal.

• the DTT country of source/ Portugal grants exclusive taxation rights to the country of residence (Portugal)

13

29 october 2015Why Portugal should be your top tax choice

PwC

The Non Habitual Tax Resident

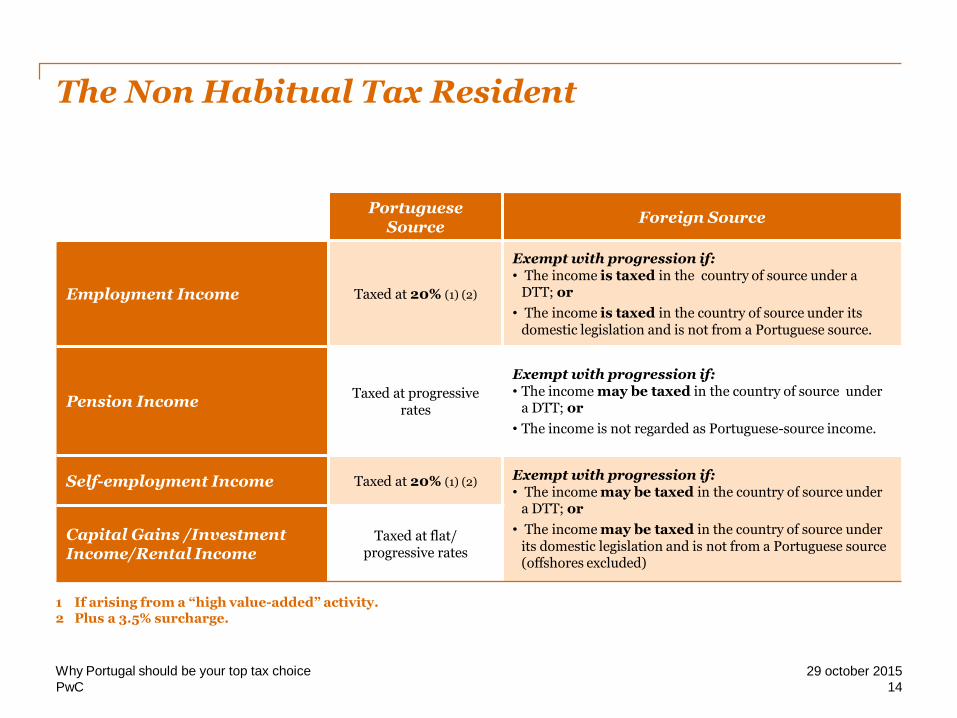

PortugueseSource

Foreign Source

Employment Income Taxed at 20% (1) (2)

Exempt with progression if:• The income is taxed in the country of source under a

DTT; or

• The income is taxed in the country of source under its domestic legislation and is not from a Portuguese source.

Pension IncomeTaxed at progressive

rates

Exempt with progression if:• The income may be taxed in the country of source under

a DTT; or

• The income is not regarded as Portuguese-source income.

Self-employment Income Taxed at 20% (1) (2)Exempt with progression if:• The income may be taxed in the country of source under

a DTT; or

• The income may be taxed in the country of source under its domestic legislation and is not from a Portuguese source (offshores excluded)

Capital Gains /Investment Income/Rental Income

Taxed at flat/progressive rates

1 If arising from a “high value-added” activity.2 Plus a 3.5% surcharge.

14

29 october 2015Why Portugal should be your top tax choice

PwC

The Non Habitual Tax Resident

Example

• Married couple.

• Interest from Switzerland: EUR 50,000.

• Rental income from Florida: EUR 80,000 (taxed in the US).

• UK pension: EUR 300,000.

• Dividends from The Netherlands: EUR 45,000 (taxed in The Netherlands).

• Employment income (“high value--added activities”): EUR 50,000.

15

29 october 2015Why Portugal should be your top tax choice

PwC

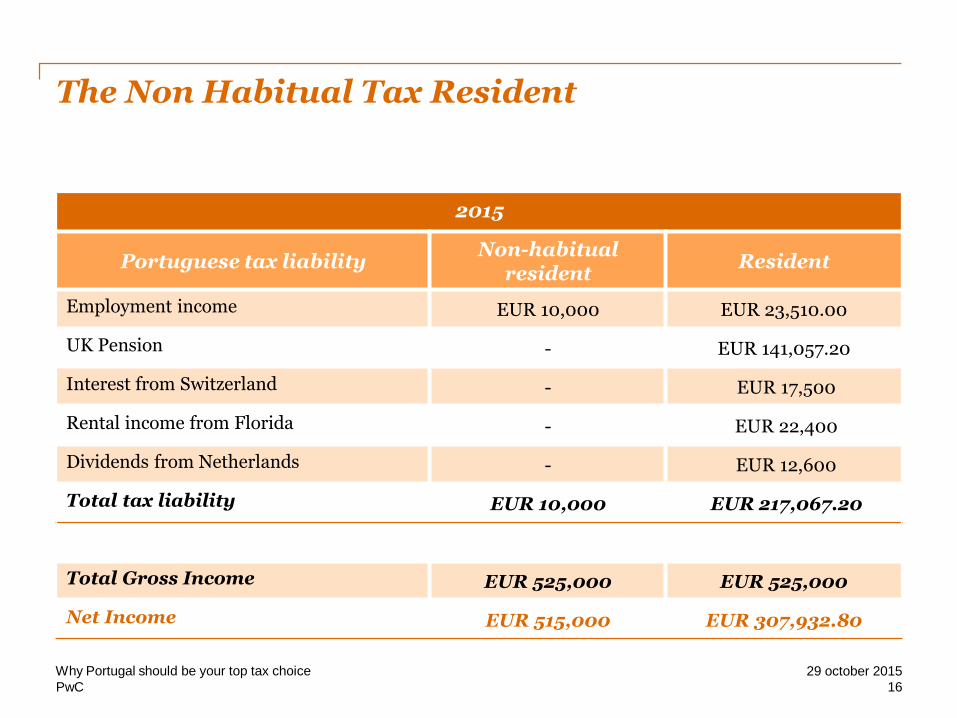

The Non Habitual Tax Resident

2015

Portuguese tax liabilityNon-habitual

residentResident

Employment income EUR 10,000 EUR 23,510.00

UK Pension - EUR 141,057.20

Interest from Switzerland - EUR 17,500

Rental income from Florida - EUR 22,400

Dividends from Netherlands - EUR 12,600

Total tax liability EUR 10,000 EUR 217,067.20

Total Gross Income EUR 525,000 EUR 525,000

Net Income EUR 515,000 EUR 307,932.80

16

29 october 2015Why Portugal should be your top tax choice

PwC

2. Portugal as a top choice for individuals

The Golden Visa

17

29 october 2015Why Portugal should be your top tax choice

PwC

The Golden Visa

Definition

• Non-EU investors must have legal residency and work permits to enter, work and invest in Portugal, and as such…

• With the aim of attracting foreign investment to Portugal, the Portuguese Government has created a special residence card for investors for non-EU nationals who wish to invest in Portugal.

• The Golden Visa will also allow the investor to travel within the Schengen area without the need for any other visa.

18

29 october 2015Why Portugal should be your top tax choice

PwC

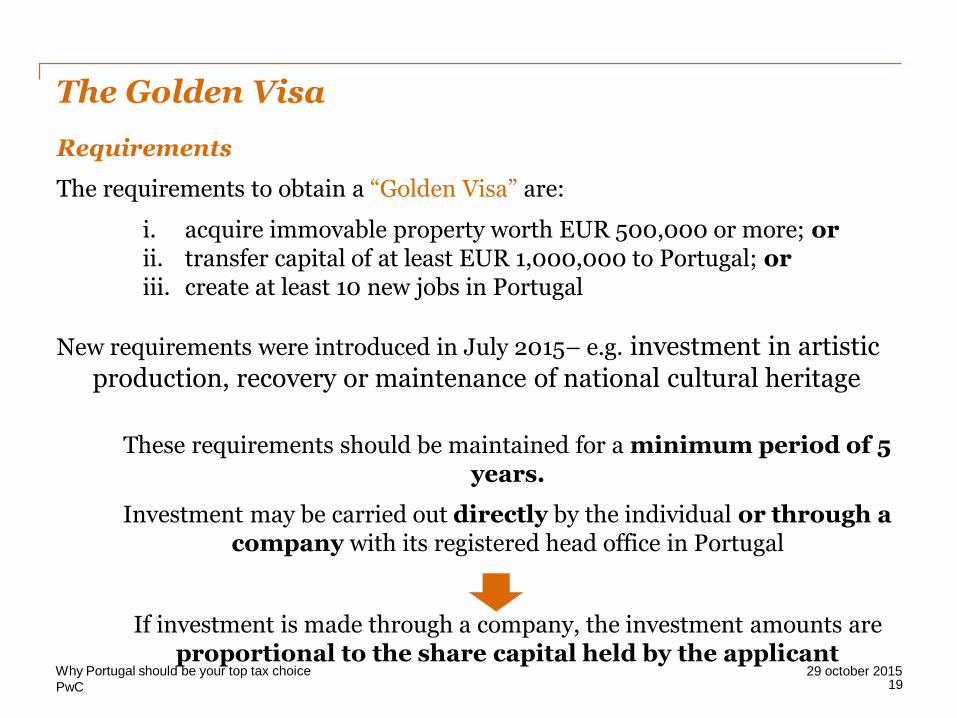

The Golden Visa

Requirements

The requirements to obtain a “Golden Visa” are:

i. acquire immovable property worth EUR 500,000 or more; orii. transfer capital of at least EUR 1,000,000 to Portugal; oriii. create at least 10 new jobs in Portugal

New requirements were introduced in July 2015– e.g. investment in artistic production, recovery or maintenance of national cultural heritage

These requirements should be maintained for a minimum period of 5 years.

Investment may be carried out directly by the individual or through a company with its registered head office in Portugal

If investment is made through a company, the investment amounts are proportional to the share capital held by the applicant

1929 october 2015Why Portugal should be your top tax choice

PwC

The Golden Visa

Evidence of requirements

• Evidence that the “Golden Visa’” requirements are met:

i. Transfer of capital to Portugal:o Statement issued by a financial institution registered in Portugal; oro Statement from the Commercial Registry / Portuguese Stock Market Regulator; or

o Statement from the Board of Directors and certified financial statements.

ii. Creation of 10 new jobs:o Statement issued by the Portuguese Social Security confirming the registration of

the employees.

iii. Acquisition of real estate:o Real estate registration certificate; oro Promissory contract before the initial application for the Golden Visa, provided

that a deposit of a minimum EUR 500,000 is paid.

20

29 october 2015Why Portugal should be your top tax choice

PwC

The Golden Visa

Validity

- The first “Golden Visa” is valid for one year and should be applied for at the Portuguese Foreign Services during the first 90 days of presence in Portugal.

- The Golden Visa may then be renewed for successive periods of two years, provided that the conditions are maintained.

- To be able to renew the “Golden Visa”, its holder should stay at least 7 days in Portugal during the first year of validity and at least 14 days during each of the two-year renewal period.

21

29 october 2015Why Portugal should be your top tax choice

PwC

The Golden Visa

Austria

Belgium

Czech Republic

Denmark

Estonia

Finland

France

Germany

Greece

Hungary

Iceland

Italy

Latvia

Lithuania

Luxembourg

Malta

Netherlands

Norway

Poland

Portugal

Slovakia

Slovenia

Spain

Sweden

Switzerland

22

29 october 2015

Benefits

• Simplified and privileged way to enter and stay in Portugal;

• Travel within the Schengen area, without any visa:

Why Portugal should be your top tax choice

PwC

The Golden Visa

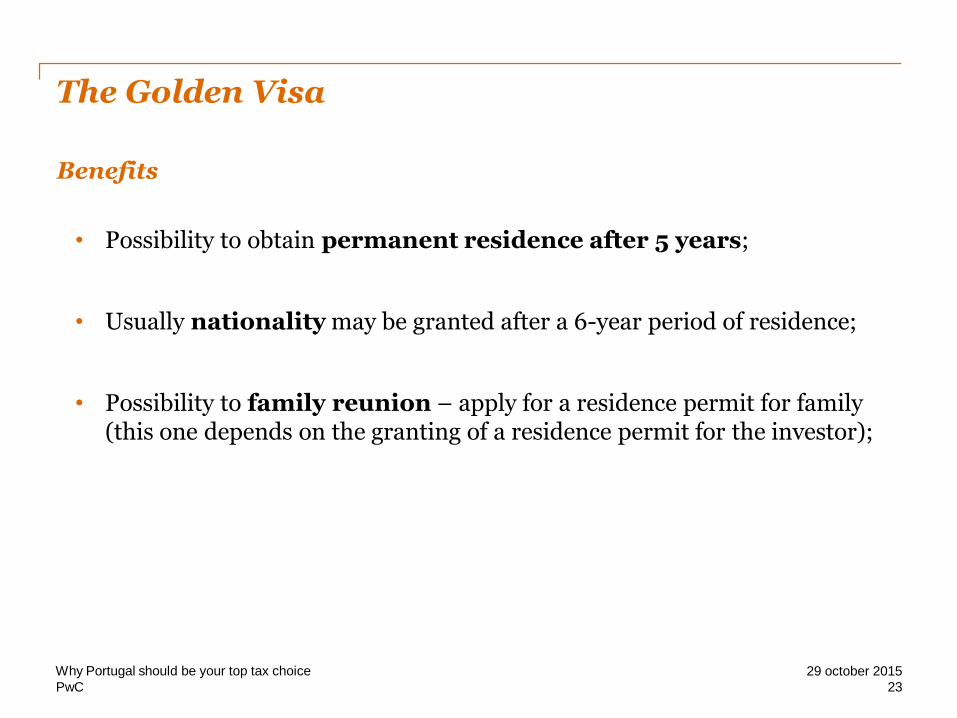

Benefits

• Possibility to obtain permanent residence after 5 years;

• Usually nationality may be granted after a 6-year period of residence;

• Possibility to family reunion – apply for a residence permit for family (this one depends on the granting of a residence permit for the investor);

23

29 october 2015Why Portugal should be your top tax choice

PwC

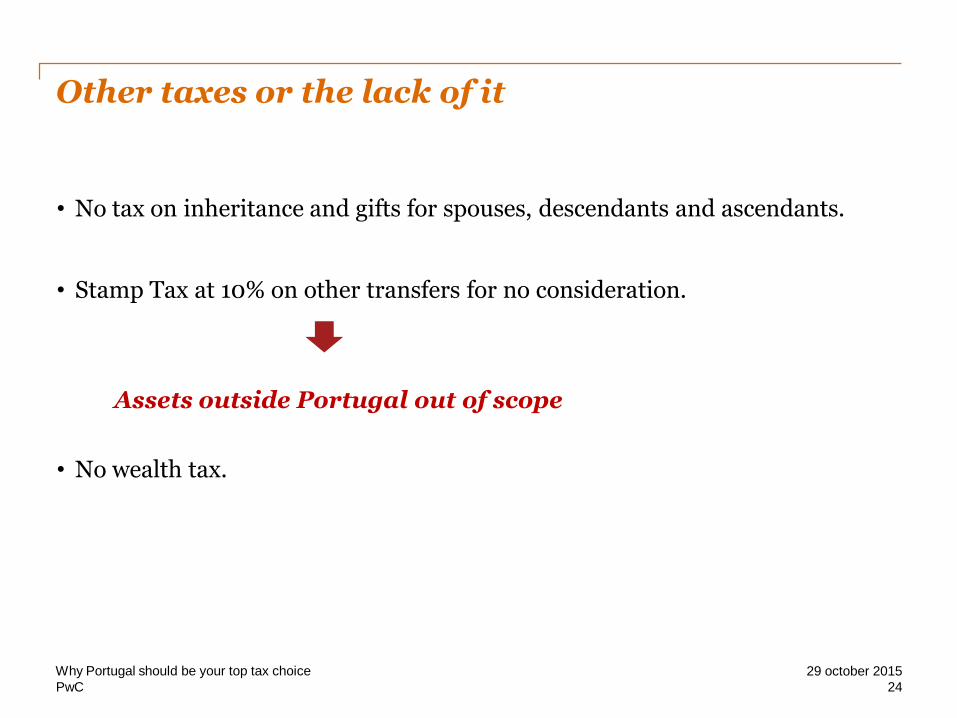

Other taxes or the lack of it

• No tax on inheritance and gifts for spouses, descendants and ascendants.

• Stamp Tax at 10% on other transfers for no consideration.

Assets outside Portugal out of scope

• No wealth tax.

24

29 october 2015Why Portugal should be your top tax choice

PwC

3. Things to remember

25

29 october 2015Why Portugal should be your top tax choice

PwC

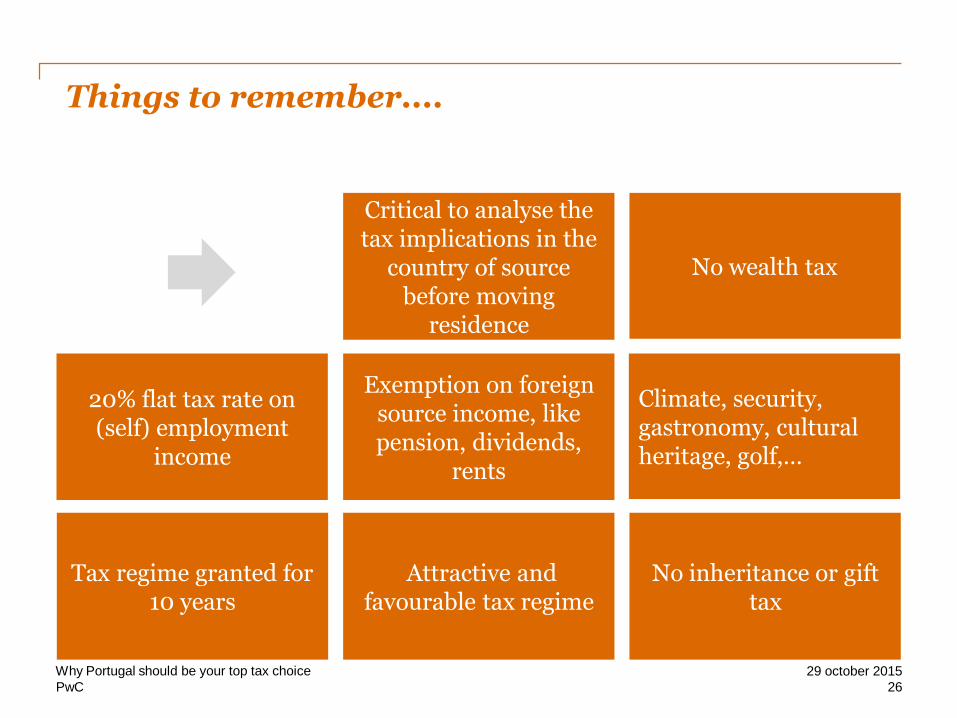

Tax regime granted for 10 years

20% flat tax rate on (self) employment

income

No inheritance or gift tax

Exemption on foreign source income, like pension, dividends,

rents

Attractive and favourable tax regime

Climate, security, gastronomy, cultural heritage, golf,…

Critical to analyse the tax implications in the

country of source before moving

residence

No wealth tax

Things to remember....

26

29 october 2015Why Portugal should be your top tax choice

PwC

Find out more...

www.pwc.pt/pt/fiscalidade/individuals-taxation.jhtml

www.pwc.pt/pt/fiscalidade/private-clients.jhtml

27

29 october 2015Why Portugal should be your top tax choice

Obrigado

Jaime Carvalho EstevesTax Lead Partner [email protected]

Luís Filipe SousaSenior [email protected]

www.pwc.pt

This publication has been prepared for general guidance on matters of interest only, and does not constitute professional advice. You should not act upon the

information contained in this publication without obtaining specific professional advice. No representation or warranty (express or implied) is given as to the

accuracy or completeness of the information contained in this publication, and, to the extent permitted by law. PricewaterhouseCoopers, its members,

employees and agents do not accept or assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to

act, in reliance on the information contained in this publication or for any decision based on it.

© 2015 PricewaterhouseCoopers. All rights reserved. In this document, “PwC” refers to PricewaterhouseCoopers & Associados - Sociedade de Revisores

Oficiais de Contas, Lda., which is a member firm of PricewaterhouseCoopers International Limited, each member firm of which is a separate legal entity.