evaluating out-of-court debt restructuring in romania paris, november 15, 2012 impact evaluation...

TRANSCRIPT

Evaluating out-of-court debt restructuringin Romania

Paris, November 15, 2012Impact Evaluation Workshop

Massimiliano Santini, Economist

Andres Martinez, PSD Specialist

THE WORLD BANKWorld Bank Group Multilateral Investment Guarantee Agency

2

Debt Restructuring Mechanisms and Reforms

Key Findings from the Literature on Insolvency Reforms

Impact Evaluation in Romania

o Design

o Implementation challenges

Next Steps

Agenda

THE WORLD BANKWorld Bank Group Multilateral Investment Guarantee Agency

Challenges Weak debt restructuring regulatory frameworks. Underdeveloped institutional capacity for commercial dispute resolution and

insolvency proceedings.

Consequences Low non-performing loan (NPL) recovery: billions of dollars of business value lost

as a result of weak loan recovery and business exit mechanisms.

Negative impact on business activity: entrepreneurship, access to credit, employment.

Debt Restructuring Mechanisms

3

*International Financial Statistics (IMF), Doing Business Database (World Bank Group).

Value Destruction* = Aggregate NPLs - Recovery Value

THE WORLD BANKWorld Bank Group Multilateral Investment Guarantee Agency

4

Objective Keeping viable businesses in operation. Liquidating unviable firms and allowing for a quick and inexpensive business

exit.

Reform interventions1. Improving insolvency regimes (credit environment improves by creating more

efficient regimes for banks to recover their credits and for businesses to leverage collateral).

2. Introducing new mechanisms for debt restructuring and reorganization.For example, out-of–court debt restructuring is perceived as more effective than the court process:

Debt Restructuring Reforms

Commercial disputes can be settled earlier. Debt can be recovered more often.

THE WORLD BANKWorld Bank Group Multilateral Investment Guarantee Agency

5

Bankruptcy reforms increase timely repayments and reduce the cost of debt. However, evidence is limited to few studies.

Debt Restructuring Reforms:Key Findings from the Literature

More evidence is needed, particularly from rigorous studies, to identify the effects of insolvency reforms on firm borrowing and investment behavior.

Reduce by 8.4% the failure rates of small and medium enterprises (Belgium).

Reduce duration of reorganizations from 34 to 12 months (Colombia).

New mechanisms for debt restructuring and reorganization

Increase the probability of timely repayments by 28% (India) through new debt recovery tribunals.

Reduce the cost of debt (Brazil) through a bankruptcy reform.

Improved insolvency regimes

THE WORLD BANKWorld Bank Group Multilateral Investment Guarantee Agency

6

Reform In November 2010, Romania introduced new out-of-court corporate debt

restructuring guidelines.Opportunity to launch a rigorous impact evaluation to study the reform’s impact.

Objectives of IETest the casual correlation of out-of-court debt restructuring on borrowers’ behavior:o Hypothesis 1: increased loan repayment rates.o Hypothesis 2: increased new loans granted to eligible debtors.

Project Teamo Leora Klapper (DEC), Shawn Cole (HBS), Raluca Desanu (HBS).o Mircea Dima and Claudia Staicu (CeC Bank)o Massi Santini, Najy Benhassine, Mahesh Uttachndani, Andres Martinez (CICBR)

Impact Evaluation in Romania - Intro

THE WORLD BANKWorld Bank Group Multilateral Investment Guarantee Agency

7

Encouragement design thorough an RCT: borrowers have limited knowledge about the existence of out-of-court debt restructuring guidelines.

Intervention: Trainings (workshops with an e-learning course, handouts reviewing the guidelines, presentations).

Sample: ~580 ‘struggling’ SMEs that have defaulted on their loans, but have not yet been delinquent on repayment (loans overdue by 30-90 days).

Sample divided into:

o The treatment group: ~290 borrowers (SMEs) will receive trainings on the guidelines.

o The control group: ~290 borrowers (SMEs) will not receive trainings.

Difference-in-difference approach to compare the two groups and determine effects of trainings on borrowers’ behavior following the intervention.

Impact Evaluation in Romania – Design 1/2

THE WORLD BANKWorld Bank Group Multilateral Investment Guarantee Agency

8

CeC Bank loan officers will distribute invitations to their client cohorts to ensure a higher intake rate of the intervention.

~590 borrowers (small and medium enterprises) are selected from the whole population of SMEs, and they will attend the trainings in four cities where CeC Bank has branches: Bucharest, Constanta, Sibiu, Timişoara.

These borrowers have not gone through an in court or out-of-court restructuring in the past, with a payment overdue by 30-90 days.

The training sessions will offer a 90-minute lecture consisting in:o A presentation by a local lawyer, handouts reviewing the guidelines and clarifying how

banks can use the principles in the case of delinquent loans, and the specific implications of the law for SME borrowers.

o An e-learning course consisting of an interactive CD developed jointly by WB and CeC Bank.

The data collected will include the following information: firm information, loan characteristics, new loan requests, repayment characteristics.

Impact Evaluation in Romania – Design 2/2

THE WORLD BANKWorld Bank Group Multilateral Investment Guarantee Agency

9

We have developed a Memorandum of Understanding (MoU), detailing the respective responsibilities of the WBG and the client (CeC Bank): the negotiations to agree on the final language have proven lengthy.

Obtaining the right amount of data from the counterpart could be difficult, and included issues of privacy.

Initial study design envisioned testing the impact through in-person training vis-à-vis other financial literacy delivery mechanisms (mail, video, or internet) for 3 different treatment groups. This design did not prove feasible due to the low sample size.

The design was subsecuently simplified to one treatment group receiving all training components.

Both the low sample size and a potential low turn out rate could undermine the magnitude of the impact.

Challenges

THE WORLD BANKWorld Bank Group Multilateral Investment Guarantee Agency

10

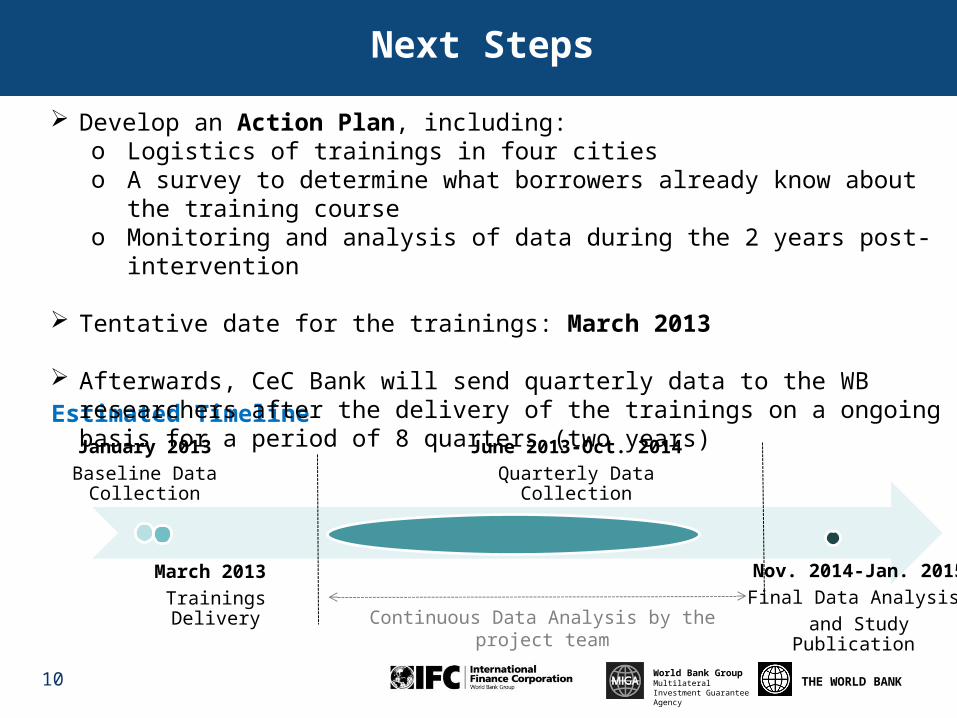

Estimated Timeline

Next Steps

January 2013

Baseline Data Collection

March 2013

Trainings Delivery

June 2013-Oct. 2014

Quarterly Data Collection

Nov. 2014-Jan. 2015

Final Data Analysis

and Study Publication

Continuous Data Analysis by the project team

Develop an Action Plan, including:o Logistics of trainings in four citieso A survey to determine what borrowers already know about the training courseo Monitoring and analysis of data during the 2 years post-intervention

Tentative date for the trainings: March 2013

Afterwards, CeC Bank will send quarterly data to the WB researchers after the delivery of the trainings on a ongoing basis for a period of 8 quarters (two years)

THE WORLD BANKWorld Bank Group Multilateral Investment Guarantee Agency

Thank you!