evaluating the performance efficiency of foreign banks ... · oriented efficiency is important. so...

TRANSCRIPT

Qualitative and Quantitative Research Review, Vol 3, Issue 3, 2018 ISSN No: 2462-1978 eISSN No: 2462-2117

97

EVALUATING THE PERFORMANCE EFFICIENCY OF FOREIGN

BANKS OPERATING IN INDIA: A DEA APPROACH

IBHA RANI

SSR College of Science & Management Studies, Bengaluru, India.

MUKUND SHARMA. N.

Department of Management Studies, BNM Institute of Technology, Bengaluru,

India.

Date of receipt: 06/02/2018

First Review: 03/04/2018

Second Review: 14/06/2018

Acceptance: 12/08/2018

ABSTRACT

The efficient financial system leads to better economic development of a

country because an efficient financial system guarantees the smooth

functioning of country’s payment system and effective implementation of

monetary policy. The literature analyzing efficiency of banking system has

increased rapidly over the last years. Data Envelopment Analysis (DEA) is

a non-parametric approach which is widely used to measure the efficiency

of financial institutions. Most studies only focus on Input side of /Technical

efficiency. Only few studies have measure the output side evaluating pure

technical and scale efficiency. We know that both input and output

oriented efficiency is important. So the Primary aim of this paper is to

evaluate the efficiency of foreign banks operating in India for the period of

2010-2017. The preset study is confined to both constant return to scale

(CRS) and variable return to scale (VRS).For DEA analysis the inputs

selected as interest expense and other expense while output selected as

interest income and other income.

Keywords: Efficiency measurement, banking industry, Data Envelopment

Analysis, Constant Return to Scale, Variable return to Scale

BACKGROUND INFORMATION

Banks are plays vital role in the Indian economy as they are sources of

financial intermediaries and country’s money supply. So the efficiency of

Qualitative and Quantitative Research Review, Vol 3, Issue 3, 2018 ISSN No: 2462-1978 eISSN No: 2462-2117

98

banks periodically needs to be evaluated for better working and effective

utilization of resources. Indian banking industry is a combination of

Public, Private and Foreign banks. Globalization and technological up

gradation have added extra pressure to banks to maintain market shares

and remain competitive. Entry of foreign banks in Indian industry with

technologically well-equipped add extra pressure to other public and

private sector banks.

Indian banking industry witnessed new way of innovative models like

payment and tiny finance banks. RBI’s new measure may go an added

method in helping to the restructuring of Indian banking system. The

digital payments system in India has evolved the most among twenty five

countries with India’s Immediate Payment Service (IMPS) being the only

system at level five in the Faster Payments Innovation Index (FPII). The

Indian banking industry consists of 27 public sector banks, 21 private

sector banks, 49 foreign banks, 56 regional rural banks, 1,562 urban

cooperative banks and 94,384 rural cooperative banks, in addition to

cooperative credit institutions in the year2017-18, total lending increased at

a CAGR of 10.94 % and total deposits increased at a CAGR of 11.66 % .

India’s retail credit market is the fourth largest in the emerging countries.

It increased to US$ 281 billion on December 2017 from US$ 181 billion on

December 2014. On the basis of economical term efficiency can be defined

as the ratio of output to input. Input refers to the scare resources and

output refers to the goods and services offered to the consumers. Efficiency

of banking system is one of the most important issues as an efficient

banking system will become the back bone of nation’s economy. In modern

era, there are numbers of methods available to measure the efficiency. It

can be a traditional approach or using the software to evaluate the

efficiency. , further it can be separated into three main categories.

1. Ratio Indicators- the traditional method of financial indices based

on the various financial ratio analyses.

2. Parametric Approach- it is based on the knowledge of production

function.

3. Non- parametric approach- this approach doesn’t require the much

knowledge of production function as compare to parametric

approach.

Qualitative and Quantitative Research Review, Vol 3, Issue 3, 2018 ISSN No: 2462-1978 eISSN No: 2462-2117

99

For the purpose of the present study the Non-parametric DEA method has

been chosen to assess the efficiency of foreign banks operating in India for

the time period 2010-2017. This study is based on the study of Farrell

(1957), who proposed that the efficiency of a firm consists of two

components: technical efficiency and allocated efficiency This study tries to

fill a gap by providing the most recent evidence on the performance of the

foreign bank operating in India. Unlike the previous studies on banks’

efficiency, the present study attempts to examine the efficiency of the

foreign banks by using non- parametric approach and it also divides the

foreign bank into two categories as efficient and inefficient bank. The

remedial measures are discussed in order to improve the efficiency of

banks.

History of Foreign Banks

Foreign banks are those banks which are incorporated outside of India and

operated through branch or subsidiary in India. The recent guidelines and

initiations of the Reserve Bank of India (RBI) for foreign banks have

encouraged in opening their operations. The existence of foreign bank can

be viewed through four different phases-

Ist phase – Foreign Banks in India (1786-1935)-

In this time period there were about 18 Foreign Banks that had been

facilitating the foreign trade of india. The bank operated in this period is

known as “Exchange bank “for the fact that they focused mainly on foreign

exchange and foreign trade businesses.

2nd Phase – Foreign Banks in India (1935-1969)

This period was marked by the establishment of Reserve Bank of India in

1935.to protect the banking system from negative effect of foreign bank

operation. RBI imposed strict regulation against foreign banking business.

3Rd Phase- Foreign Banks in India (1969-1991)

In this phase to ensure their survival foreign banks designed a strategic

diversification of services such as- Foreign Currency Loan, Investment

banking and portfolio management.

Qualitative and Quantitative Research Review, Vol 3, Issue 3, 2018 ISSN No: 2462-1978 eISSN No: 2462-2117

100

4Th Phase - Foreign Banks in India (1991 Onwards)

Economic liberalization, deregulation of finance sector and other economic

reforms contributed for the surge of FDI in India. The increased FDI in the

banking sector brought significant changes in the structure of banking

sector.

The major objective of establishment of foreign banks in India could be-

Developing a better economic relation with the home country of

foreign banks.

To provide them an opportunity for foreign trade considering the

size of its home country and economy.

Table 1 Number of Foreign banks and their branch size

Table-1

Number Of Foreign banks and their branch size

Year Total No. of

Foreign bank

No. of Foreign Bank

Offices

2010 33 295

2011 36 317

2012 41 324

2013 43 339

2014 43 322

2015 44 329

2016 45 332

2017 44 301

The no. of foreign bank offices increased from 145 in 1990 to 286 in January

2018.

Over the last many years, foreign banks have become much more

important in domestic financial intermediation, heightening the need to

understand their models. Foreign banks have helped in advancing the

technology used in the financing sector. The first Automated Teller

Qualitative and Quantitative Research Review, Vol 3, Issue 3, 2018 ISSN No: 2462-1978 eISSN No: 2462-2117

101

Machine ATM) in India was brought up by Hong Kong and Shanghai

Banking Corporation Ltd (HSBC). Foreign banks have become more &

more efficient now a days.

LITERATURE REVIEW

Several studies shown that the in developed countries notable attempts has

been made to evaluate the efficiency of banks but in developing country

such as India the attempts has been made far fewer. In Indian scenario,

Keshari and Paul in 1994 was first to evaluate the efficiency of banks using

the non-parametric approach (DEA).after that many attempts has been

made by researcher to analyze the efficiency of banks operating in India.

Das (2000) calculated the overall efficiency of twenty seven public sector

banks for one year (1998) using the DEA model. The overall efficiency

incorporates technical efficiency and allocative efficiency. The results show

that State Bank Group banks have performed better than nationalized

banks and they display lower dispersion as compared to nationalized

banks.

Sathye (2004) employed a non-parametric approach to measure the

efficiency of Public sector, private sector and foreign banks. He has used

two set of model to show how efficiency score vary with the variation of

different set of input and output. The result provided that efficiency score

are highly sensitive to the alternative set of input and output variables.

Rammohan and Ray (2004) evaluated the revenue maximizing efficiency of

three different ownership groups-Public, private and Foreign bank during

the year 1992-2000. He found that the public sector banks were

significantly better than the private sector on this, but the efficiency score

was not significant between the foreign and public sector bank.

Rajput and Gupta (2011) have measured the efficiency of foreign banks

operating in India for the period of 2005-2011.he found that the efficiency

of foreign banks has exhibits continuous improvement for the study period

with little drifts. Kumar and Batra (2012) have examined the efficiency

changes of Indian banking system for the period of 2006-2011.he found

that the during the study period Indian banking industry experienced

stagnation in the technological progress.

Qualitative and Quantitative Research Review, Vol 3, Issue 3, 2018 ISSN No: 2462-1978 eISSN No: 2462-2117

102

Roy (2014) have examined the 62 commercial bank divided between four

ownership –Nationalized Bank (20), Private sector (21), foreign bank (Fb)

and other SBI and its associates.

As per the result, the efficiency score of foreign bank were found to

increase over the tree era. Sigh (2016) has evaluated the efficiency of thirty

seven commercial bank for the period of 1997-2013 by using the input

oriented DEA model.

Thus as per the literature review efficiency score can be different of due to

difference in choice of technique, different set of input and output variable,

types of data and no.s of other factor pertaining to the application of

technique. Thus it is evident from the literature review that the most of the

research has been done on public and private sector banks but very few

attempts has been made to evaluate the efficiency of foreign banks which is

operating in India.

RESEARCH METHODOLOGY

Research Objective

Foreign banks play an important role in the Indian banking sector.

Through this paper we will observe the performance of foreign banks

through the Non-parametric approach DEA. The main aim of this paper is

following-

1. To analyse the overall performance of foreign banks operating in

India as a group.

2. To find out the changes in efficiency of Foreign banks operating

in India for the period of 2010-2017.

3. To measure the Technical, Pure Technical and scale efficiency of

foreign banks for the study period 2010-2017.

Database

In the present study 29 foreign banks considered for the efficiency

measurement for the time period of 2010-2017.the banks which is not

Qualitative and Quantitative Research Review, Vol 3, Issue 3, 2018 ISSN No: 2462-1978 eISSN No: 2462-2117

103

operating continuously for the study period is not considered for the

study.

Present study is based upon secondary data and following sources have

been used for the procurement of data such as RBI publication and other

banking sites.

Methodology

In this study we shall try to measure the efficiency of foreign banks with

DEA. We prefer non parametric over the parametric approach because of

DEA easily accommodates the multiple input and multiple output of

banks.

DEA

Data Envelopment analysis (DEA) is mathematical linear programming

based first introduced by Charnes et al, Cooper and Rhodes in 1978.it is

improvement of Farel’s work of 1957 which consider only single output

and single input to evaluate the efficiency, in DEA we can accommodate

multiple input and output. It is a non-parametric approach for evaluating

the relative efficiency of similar units known as Decision making unit

(DMU).earlier it was mainly used by Not-for-profit organization such as

schools & hospital later it’s extended to profit organization as well as

banking.

The basic models of DEA are CCR and BCC DEA model.

The CCR model-

It is developed by Charnes et al,Cooper and Rhodes in 1978 and known as

CCR DEA model it is based on the assumption of constant Return to Scale

(CRS). The application this model provides the technical efficiency score of

individual bank as well it gives information on input and output slacks

and reference set for peer banks. The efficiency measured from CCR model

is known as overall technical efficiency (OTE) scores. This scores helps to

determine the inefficiency due to input and output configuration and size

of operation.

Qualitative and Quantitative Research Review, Vol 3, Issue 3, 2018 ISSN No: 2462-1978 eISSN No: 2462-2117

104

The BCC model

It is developed by Banker, Cooper and Rhodes in 1984.it is an extension of

basic CCR DEA model which allows the return to scale to be variable. The

application of this model provides Pure technical efficiency (PTE) and it is

based on the assumption of Variable return to scale (VRS). It is a more

flexible than the CCR model as it allows for constant, increasing, and

decreasing returns-to-scale.

This models allow a bifurcation of technical efficiency (TE) into pure

technical efficiency (PTE) and scale efficiency (SE) components .Scale

efficiency (SE) for each DMU can be calculated by a ratio of OTE score to

PTE score .Scale efficiency can be calculated by

SE=OTE/PTE

Or

SE= TE (CRS)/ (TE VRS)

The DEA model helps to measure the efficiency score of individual bank.

The efficiency score lies between 0 to 1, where 0 ≤ SE ≤ 1 since CRS ≤VRS. If

the value of SE equals 1, the firm is scale efficient and all values less than 1

reflect scale inefficiency. A bank having Efficiency score of 1 considered as

100% efficient. The banks having less than 1 efficiency scores indicates its

inefficiency.

5 Inputs and Output Specifications

For evaluating the efficiency input and output variables plays an

important role. There is no accord in the literature survey which

constitutes input and output of a bank unlike the other firm. In case of

banking there are mainly two approaches for the measurement of input

and output of a bank namely Production and Intermediation approach.

Production Approach- this approach is introduced by Benston in 1965,

bank is defined as a producer of services for account holders. As per this

both loans and deposits are treated as outputs of a bank.

Qualitative and Quantitative Research Review, Vol 3, Issue 3, 2018 ISSN No: 2462-1978 eISSN No: 2462-2117

105

Intermediation approach- As per this banks act as an intermediary

between savers and borrowers and conceives total loans and securities as

outputs, whereas deposits along with labor and physical capital are

considered as inputs.

As per the literature review the intermediation approach is widely used in

different empirical studies, neither approach is totally satisfactory due to

the controversy over treatment of deposits as input or output. In this study

two inputs and two outputs have been used.

Table 2. Input output

S.N Input Output

1 Interest Expense Interest Income

2

Non-Interest

Expense

Non-Interest

income

RESULTS

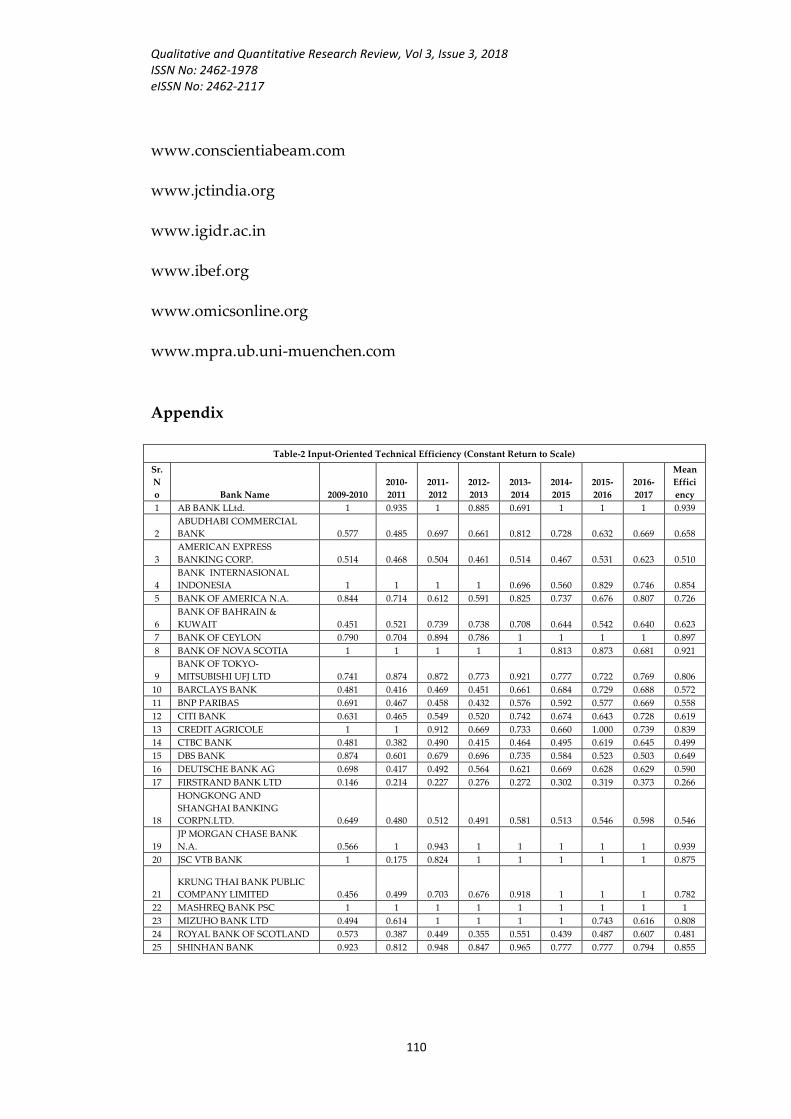

Input-Oriented Technical Efficiency (TE) -Constant Return to Scale

Table -2 exhibits the DEA efficiency score based on input oriented technical

efficiency (TE) under the constant return to scale of CCR Model.

The efficiency score of a DMU states the efficiency of the DMU in utilizing

the inputs to generate the outputs in comparison with other DMUs. Since

we are using an input oriented model, the major aim is to decrease inputs

as much as possible, keeping the output either constant or increasing it, if

possible. It gives the answer of question such as “By how much can input

quantities be proportionally reduced without changing the output

quantities produced?’

The banks with an efficiency score of 1 shows 100% efficiency and it

indicate that the inputs cannot be further decreased in their case and if it is

decreased, it will always have a negative impact on the output. They have

been able to make the optimal utilization of the input consistently

throughout the period. They have set examples for others to replicate.

Qualitative and Quantitative Research Review, Vol 3, Issue 3, 2018 ISSN No: 2462-1978 eISSN No: 2462-2117

106

They have been able to convert most of their interest expense into its

income. The banks with an efficiency score of less than 1 shows the

inefficiency and it indicate that there is still scope for improvement and

keeping the output constant the inputs can be further reduced thus the

efficiency of the firm can be increased. The analysis shows that 8 banks

attained maximum efficiency score for the year 2014-15.The average

efficiency score of all the banks for the entire period is less than one except

Mashreq Bank which is having the efficiency score of 1 during the entire

study period showing 100% efficiency.

Output-Oriented Pure Technical Efficiency (PTE)- Variable Return to

Scale

Table -3 exhibits the DEA efficiency score based on output oriented pure

technical efficiency under the VRS. In this there is an increment in number

of banks which exhibits the consistency in their performance. The

evaluation shows that twelve banks attained maximum efficiency score

one for the year 2011-2012. It’s been observed that there is a varying trend

in their pure technical efficiency score of foreign banks from 2010 to 2017,

the score lies in the interval [0.20, 1.00]. The average efficiency of all the

banks for the entire period is less than 1except 4 banks they are American

Express,Citi bank, Mashreq Bank and Standard Chartered Bank . These

four banks are 100 % efficient throughout the study period of 2010-2017.

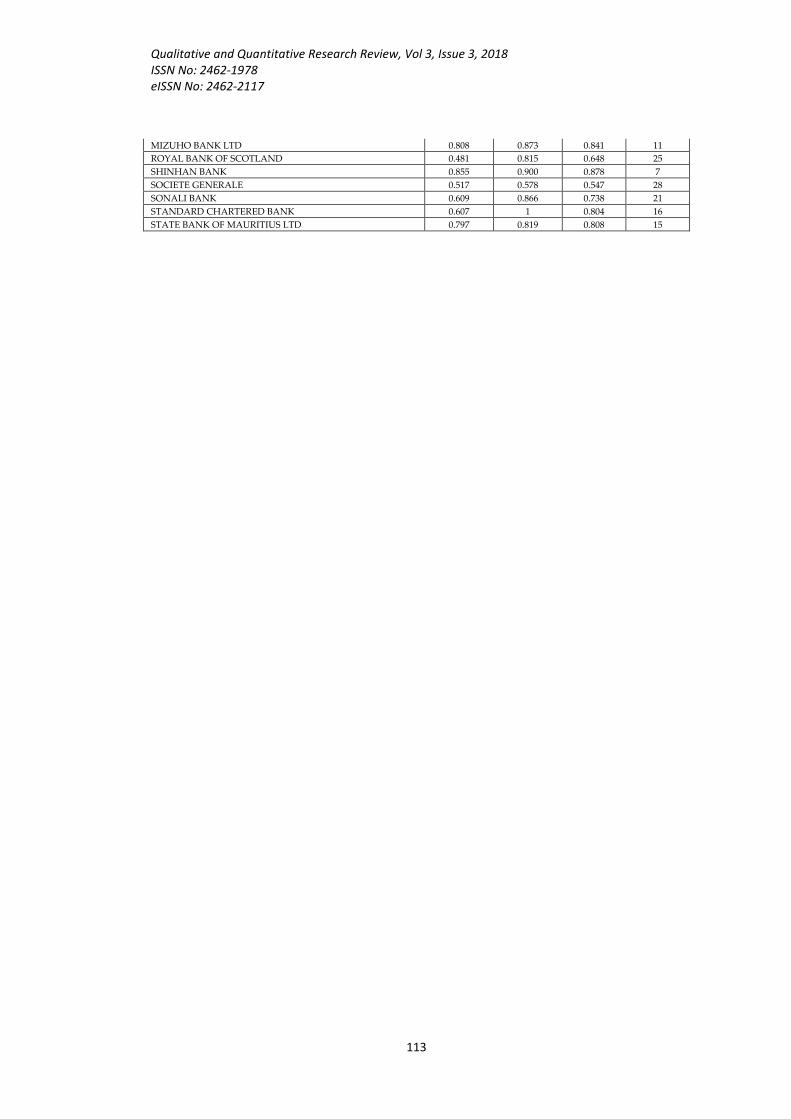

Scale Efficiency

Table 4 exhibits the scale efficiency score for the study period for each

bank. As discussed earlier, SE score of individual bank can be calculated

by ratio of OTE to PTE score. The value of SE equal to 1 implies that the

bank is operating at most productive scale size (MPSS) which corresponds

to constant returns-to-scale.

The result shows that Eight banks attained maximum efficiency score 1 for

the year 2014-2015.The average index of technical efficiency during the

study period varies from 26.6% - 100%, PTE varying at 57.8% - 100%, and

of SE varying from 87.66% -100%.

Qualitative and Quantitative Research Review, Vol 3, Issue 3, 2018 ISSN No: 2462-1978 eISSN No: 2462-2117

107

Overall mean efficiency

As per the result of overall mean efficiency only one bank is highly

consistent with the efficiency score of 1 and stands first among all the 29

banks considered for the study. The rank of all the 29 banks is given below

in the Table 5.

SUMMARY AND CONCLUSION

This paper has evaluated the technical, pure technical, and scale

efficiencies of 29 foreign banks operating in India for the time period of

2010-2017. The results show that the overall technical efficiency of foreign

banks is 70.1 percent. Thus, the magnitude of technical inefficiency is

around 29.9 percent. Mashreq bank is only fully efficient foreign bank

having efficiency score 1 for the entire study period, however the

remaining less efficient banks can be improved by the effective utilization

of their inputs. As a conclusion, this study suggests that there is an

abundant scope for improvement in the performance of inefficient foreign

bank by choosing a correct input output mix and selecting appropriate

scale size. The future work could extend our research in various directions

such as different input and output mix as well as for different time period.

There is chance to evaluate the technical, pure technical, and scale

efficiencies of different ownership of banking groups such as Public and

private sector Banks.

REFERENCES

Avkiran, N.K. (1999a). An application reference for data envelopment

analysis in branch banking: helping the novice

researcher, International Journal of Bank Marketing, 17(5), 206-

220, https://doi.org/10.1108/026523299 10292675

Dwivedi, A.K., & Charyulu, D.K. (2011) Efficiency of Indian Banking

Industry in the Post-Reform Era”, IIM Ahmedabad, Research and

Publication

Qualitative and Quantitative Research Review, Vol 3, Issue 3, 2018 ISSN No: 2462-1978 eISSN No: 2462-2117

108

Bhide, M.G., Prasad, A., & Ghosh, S. (2002), ‘Banking sector reforms: a

critical overview’, Economic and Political Weekly, Vol. 37, No. 5,

pp. 399–407.

Chatterjee, B., & Sinha, R.P., (2006). Cost efficiency and commercial bank

lending: some empirical results, The Indian Economic Journal, 54(10),

145-165.

Oke, D.M., & Poloamina, I.D. (2012). Further Analysis of Bank Efficiency

Correlates: The Nigerian Experience, Journal of Applied Finance &

Banking, 2(4), 1-11

Roy, D. (2014). Analysis of Technical Efficiency of Indian Banking Sector:

An Application of Data Envelopment Analysis. International Journal

of Finance & Banking Studies, 3(1), 150-160

Wozniewska, G. (2008). Methods of measuring the efficiency of commercial

banks: An example of polish banks, Ekonomika, 84.

Gupta, O.K., Doshit, Y. & Chinnubhai, A. (2008) Dynamics of Productive

efficiency of Indian Banks. International Journal of Operations Research

5(2), 78-90.

Nandi, J.K., (2013). Efficiency analysis of public and private sector banks in

India through data envelopment analysis. Vidyasagar University

Journal of Commerce, 18,

Gulati, RF. (2011) Evaluation of technical, pure technical and scale

efficiencies of Indian banks: An analysis from cross-sectional

perspective”13th Annual conference on money and Finance in the

Indian economy.

Mariyappan, P. (2012). A Study on Performance Efficiency of Nationalized

Banks of India: A DEA Approach Proceedings Book of ICEFMO,

2013, Malaysia Handbook on the Economic, Finance and

Management Outlooks, PP 120-133.

Qualitative and Quantitative Research Review, Vol 3, Issue 3, 2018 ISSN No: 2462-1978 eISSN No: 2462-2117

109

Ray, S.C., & Das, A. (2009). Distribution of Cost and Profit Efficiency:

Evidence from the Indian Banking, European Journal of Operational

Research.

Sathye, M. (2003). Efficiency of Banks in a Developing Economy: the Case

of India. European Journal of Operation Research, 148(3), 662-671.

Kumar, S., & Gulati, R. (2008). An Examination of Technical, Pure

Technical, and Scale Efficiencies in Indian Public Sector Banks using

Data Envelopment Analysis” Eurasian Journal of Business and

Economics 2008, 1 (2), 33-69.

Sensarma (2006). “Are Foreign Banks always the best? Comparison of

State-Owned, Private and Foreign Banks in India”, Economic

Modelling, April 7, pp. 717-735.

Edurkar, A., & Shaikh, A.A. (2005). Foreign Banks operating in India with

specific business practices models and their Scenario. Post RBI Road

Map 2005.

The RBI (2009). The Report of the Committee on Financial Sector

Assessment. RBI report. www.rbi.org.in.

The RBI. ‘The Report on Trend and Progress of Banking in India’, RBI

Publication, Various years. RBI report. www.rbi.org.in.

The RBI. “Statistical Tables Relating to Banks in India”, Various years. RBI

report. www.rbi.org.in.

The RBI (2010). A Profile of Banks, RBI Publication, RBI report.

www.rbi.org.in.

The RBI (2010; 2017). Financial Stability Reports, RBI Publication, monthly

report, March 2010, 2011. RBI report. www.rbi.org.in.

The RBI (2011). Headcount of foreign bank drops in 2010: RBI, Press Trust

of India (PTI), March 2011 (Mumbai) RBI report. www.rbi.org.in.

Online data:

Qualitative and Quantitative Research Review, Vol 3, Issue 3, 2018 ISSN No: 2462-1978 eISSN No: 2462-2117

110

www.conscientiabeam.com

www.jctindia.org

www.igidr.ac.in

www.ibef.org

www.omicsonline.org

www.mpra.ub.uni-muenchen.com

Appendix

Table-2 Input-Oriented Technical Efficiency (Constant Return to Scale)

Sr.

N

o Bank Name 2009-2010

2010-

2011

2011-

2012

2012-

2013

2013-

2014

2014-

2015

2015-

2016

2016-

2017

Mean

Effici

ency

1 AB BANK LLtd. 1 0.935 1 0.885 0.691 1 1 1 0.939

2

ABUDHABI COMMERCIAL

BANK 0.577 0.485 0.697 0.661 0.812 0.728 0.632 0.669 0.658

3

AMERICAN EXPRESS

BANKING CORP. 0.514 0.468 0.504 0.461 0.514 0.467 0.531 0.623 0.510

4

BANK INTERNASIONAL

INDONESIA 1 1 1 1 0.696 0.560 0.829 0.746 0.854

5 BANK OF AMERICA N.A. 0.844 0.714 0.612 0.591 0.825 0.737 0.676 0.807 0.726

6

BANK OF BAHRAIN &

KUWAIT 0.451 0.521 0.739 0.738 0.708 0.644 0.542 0.640 0.623

7 BANK OF CEYLON 0.790 0.704 0.894 0.786 1 1 1 1 0.897

8 BANK OF NOVA SCOTIA 1 1 1 1 1 0.813 0.873 0.681 0.921

9

BANK OF TOKYO-

MITSUBISHI UFJ LTD 0.741 0.874 0.872 0.773 0.921 0.777 0.722 0.769 0.806

10 BARCLAYS BANK 0.481 0.416 0.469 0.451 0.661 0.684 0.729 0.688 0.572

11 BNP PARIBAS 0.691 0.467 0.458 0.432 0.576 0.592 0.577 0.669 0.558

12 CITI BANK 0.631 0.465 0.549 0.520 0.742 0.674 0.643 0.728 0.619

13 CREDIT AGRICOLE 1 1 0.912 0.669 0.733 0.660 1.000 0.739 0.839

14 CTBC BANK 0.481 0.382 0.490 0.415 0.464 0.495 0.619 0.645 0.499

15 DBS BANK 0.874 0.601 0.679 0.696 0.735 0.584 0.523 0.503 0.649

16 DEUTSCHE BANK AG 0.698 0.417 0.492 0.564 0.621 0.669 0.628 0.629 0.590

17 FIRSTRAND BANK LTD 0.146 0.214 0.227 0.276 0.272 0.302 0.319 0.373 0.266

18

HONGKONG AND

SHANGHAI BANKING

CORPN.LTD. 0.649 0.480 0.512 0.491 0.581 0.513 0.546 0.598 0.546

19

JP MORGAN CHASE BANK

N.A. 0.566 1 0.943 1 1 1 1 1 0.939

20 JSC VTB BANK 1 0.175 0.824 1 1 1 1 1 0.875

21

KRUNG THAI BANK PUBLIC

COMPANY LIMITED 0.456 0.499 0.703 0.676 0.918 1 1 1 0.782

22 MASHREQ BANK PSC 1 1 1 1 1 1 1 1 1

23 MIZUHO BANK LTD 0.494 0.614 1 1 1 1 0.743 0.616 0.808

24 ROYAL BANK OF SCOTLAND 0.573 0.387 0.449 0.355 0.551 0.439 0.487 0.607 0.481

25 SHINHAN BANK 0.923 0.812 0.948 0.847 0.965 0.777 0.777 0.794 0.855

Qualitative and Quantitative Research Review, Vol 3, Issue 3, 2018 ISSN No: 2462-1978 eISSN No: 2462-2117

111

26 SOCIETE GENERALE 0.426 0.509 0.681 0.523 0.505 0.543 0.503 0.444 0.517

27 SONALI BANK 0.633 0.491 0.576 0.636 0.615 0.564 0.600 0.759 0.609

28

STANDARD CHARTERED

BANK 0.674 0.497 0.553 0.562 0.677 0.676 0.603 0.616 0.607

29

STATE BANK OF MAURITIUS

LTD 0.653 0.739 0.870 0.992 1 1 0.508 0.614 0.797

Mean Efficiency of overall Banks 0.689 0.616 0.712 0.690 0.751 0.721 0.711 0.723 0.701

Table-3 Output-Oriented Pure Technical Efficiency (Variable Return to Scale)

Sr.

No Bank Name

2009-

2010 2010-2011

2011-

2012

2012-

2013

2013-

2014

2014-

2015

2015-

2016

2016-

2017

Mean

Efficie

ncy

1 AB BANK LLtd. 1 0.936 1 0.910 0.711 1 1 1 0.945

2

ABUDHABI COMMERCIAL

BANK 0.644 0.516 0.708 0.666 0.813 0.743 0.643 0.763 0.687

3

AMERICAN EXPRESS

BANKING CORP. 1 1 1 1 1 1 1 1 1

4

BANK INTERNASIONAL

INDONESIA 1 1 1 1 0.748 0.627 0.855 0.802 0.879

5 BANK OF AMERICA 1 1 1 0.847 1 1 0.960 1 0.976

6

BANK OF BAHRAIN &

KUWAIT 0.487 0.561 0.751 0.759 0.715 0.693 0.546 0.706 0.652

7 BANK OF CEYLON 0.849 0.712 1 1 1 1 1 1 0.945

8 BANK OF NOVA SCOTIA 1 1 1 1 1 0.833 0.879 0.746 0.932

9

BANK OF TOKYO-

MITSUBISHI UFJ LTD 0.780 0.923 0.965 0.949 0.946 0.841 0.798 0.810 0.877

10 BARCLAYS BANK 0.770 0.799 0.707 0.669 0.785 0.926 0.974 0.868 0.812

11 BNP PARIBAS 1 0.741 0.653 0.655 0.716 0.757 0.758 0.964 0.781

12 CITI BANK 1 1 1 1 1 1 1 1 1

13 CREDIT AGRICOLE 1 1 1 0.684 0.734 0.762 1 0.997 0.897

14 CTBC BANK 0.935 0.406 0.503 0.426 0.465 0.512 0.681 0.830 0.595

15 DBS BANK 1 1 1 1 1 0.815 0.728 0.765 0.913

16 DEUTSCHE BANK AG 1 1 1 1 1 0.973 0.988 1 0.995

17 FIRSTRAND BANK LTD 0.655 0.216 0.780 0.887 0.861 0.870 0.859 0.850 0.891

18

HONGKONG AND

SHANGHAI BANKING

CORPN.LTD. 1 0.997 1 0.956 0.870 0.821 0.916 0.996 0.945

19 JP MORGAN CHASE BANK 0.751 1 1 1 1 1 1 1 0.969

20 JSC VTB BANK 1 0.200 1 1 1 1 1 1 0.900

21

KRUNG THAI BANK

PUBLIC COMPANY

LIMITED 0.579 0.536 0.983 1 1 1 1 1 0.887

22 MASHREQ BANK PSC 1 1 1 1 1 1 1 1 1

23 MIZUHO BANK LTD 0.575 0.616 1 1 1 1 0.901 0.897 0.873

24

ROYAL BANK OF

SCOTLAND 0.892 0.787 0.866 0.657 0.842 0.753 0.786 0.933 0.815

25 SHINHAN BANK 1 0.866 0.957 0.851 0.971 0.836 0.791 0.930 0.900

26 SOCIETE GENERALE 0.636 0.537 0.683 0.523 0.505 0.589 0.514 0.635 0.578

27 SONALI BANK 0.659 0.515 0.758 1 1 1 1 1 0.866

28

STANDARD CHARTERED

BANK 1 1 1 1 1 1 1 1 1

29

STATE BANK OF

MAURITIUS LTD 0.669 0.748 0.956 1 1 1 0.511 0.667 0.819

Mean Efficiency of overall Banks 0.858 0.802 0.906 0.877 0.886 0.874 0.865 0.902 0.873

Table-4 Scale Efficiency

Sr.

No Bank Name

200

9-

201

0

201

0-

201

1

201

1-

201

2

201

2-

201

3

201

3-

201

4

201

4-

201

5

201

5-

201

6

201

6-

201

7

Mean

Efficien

cy

1 AB BANK Ltd. 1 6 1 0.97 0.97 1 1 1 0.993

Qualitative and Quantitative Research Review, Vol 3, Issue 3, 2018 ISSN No: 2462-1978 eISSN No: 2462-2117

112

2 ABUDHABI COMMERCIAL BANK 0.89 0.94 0.98 0.99 0.99 0.98 0.98 0.87 0.956

3 AMERICAN EXPRESS BANKING CORP. 0.51 0.46 0.50 0.46 0.51 0.46 0.53 0.62 0.510

4 BANK INTERNASIONAL INDONESIA 1 1 1 1 0.93 0.89 0.96 0.93 0.965

5 BANK OF AMERICA N.A. 0.84 0.71 0.61 0.69 0.82 0.73 0.70 0.80 0.743

6 BANK OF BAHRAIN & KUWAIT 0.92 0.93 0.98 0.97 0.99 0.92 0.99 0.90 0.954

7 BANK OF CEYLON 0.93 0.98 0.89 0.78 1 1 1 1 0.950

8 BANK OF NOVA SCOTIA 1 1 1 1 1 0.97 0.99 0.91 0.985

9 BANK OF TOKYO-MITSUBISHI UFJ LTD 0.95 0.94 0.90 0.81 0.97 0.92 0.90 0.94 0.921

10 BARCLAYS BANK 0.62 0.52 0.66 0.67 0.84 0.73 0.74 0.79 0.701

11 BNP PARIBAS 0.69 0.63 0.70 0.66 0.80 0.78 0.76 0.69 0.715

12 CITI BANK 0.63 0.46 0.54 0.52 0.74 0.67 0.64 0.72 0.619

13 CREDIT AGRICOLE 1 1 0.91 0.97 0.99 0.86

0.74 0.937

14 CTBC BANK 0.51 0.94 0.97 0.97 0.99 0.96 0.90 0.77 0.882

15 DBS BANK 0.87 0.60 0.67 0.69 0.73 0.71 0.71 0.65 0.710

16 DEUTSCHE BANK AG 0.69 0.41 0.49 0.56 0.62 0.68 0.63 0.62 0.593

17 FIRSTRAND BANK LTD 0.22 0.99 0.99 0.65 0.67 0.70 0.73 0.68 0.710

18

HONGKONG AND SHANGHAI BANKING

CORPN.LTD. 0.64 0.48 0.51 0.51 0.66 0.62 0.59 0.60 0.581

19 JP MORGAN CHASE BANK N.A. 0.75 1 0.94 1 1 1 1 1 0.962

20 JSC VTB BANK 1 0.87 0.82 1 1 1 1 1 0.963

21

KRUNG THAI BANK PUBLIC COMPANY

LIMITED 0.78 0.93 0.71 0.67 0.91 1 1 1 0.878

22 MASHREQ BANK PSC 1 1 1 1 1 1 1 1 1

23 MIZUHO BANK LTD 0.86 0.99 1 1 1 1 0.82 0.68 0.921

24 ROYAL BANK OF SCOTLAND 0.64 0.49 0.51 0.54 0.65 0.58 0.61 0.65 0.587

25 SHINHAN BANK 0.92 0.93 0.99 0.99 0.99 0.93 0.98 0.85 0.951

26 SOCIETE GENERALE 0.67 0.94 0.99

0.99 0.92 0.97 0.69 0.902

27 SONALI BANK 0.96 0.95 0.76 0.63 0.61 0.56 0.60 0.75 0.731

28 STANDARD CHARTERED BANK 0.67 0.49 0.55 0.56 0.67 0.67 0.60 0.61 0.607

29 STATE BANK OF MAURITIUS LTD 0.97 0.98 0.91 0.99 1 1 0.99 0.92 0.973

Mean Efficiency of overall Banks 0.79 0.98 0.81 0.80 0.86 0.83 0.84 0.81 0.824

Table-5 Over all mean efficiency of all the measures put together

Bank name

Mean

efficiency of

the

individual

banks

[input-CRS]

Mean

efficiency of

the

individual

banks [input

VRS]

Mean of

mean

efficiency

Rank based

mean on

efficiency

AB BANK LLtd. 0.939 0.945 0.942 3

ABUDHABI COMMERCIAL BANK 0.658 0.687 0.672 23

AMERICAN EXPRESS BANKING CORP. 0.510 1 0.755 19

BANK INTERNASIONAL INDONESIA 0.854 0.879 0.867 9

BANK OF AMERICA N.A. 0.726 0.976 0.851 10

BANK OF BAHRAIN & KUWAIT 0.623 0.652 0.637 26

BANK OF CEYLON 0.897 0.945 0.921 5

BANK OF NOVA SCOTIA 0.921 0.932 0.927 4

BANK OF TOKYO-MITSUBISHI UFJ LTD 0.806 0.877 0.841 12

BARCLAYS BANK 0.572 0.812 0.692 22

BNP PARIBAS 0.558 0.781 0.669 24

CITI BANK 0.619 1 0.809 14

CREDIT AGRICOLE 0.839 0.897 0.868 8

CTBC BANK 0.499 0.595 0.547 28

DBS BANK 0.649 0.913 0.781 17

DEUTSCHE BANK AG 0.590 0.995 0.792 18

FIRSTRAND BANK LTD 0.266 0.891 0.579 27

HONGKONG AND SHANGHAI BANKING CORPN.LTD. 0.546 0.945 0.745 20

JP MORGAN CHASE BANK N.A. 0.939 0.969 0.954 2

JSC VTB BANK 0.875 0.900 0.887 6

KRUNG THAI BANK PUBLIC COMPANY LIMITED 0.782 0.887 0.834 13

MASHREQ BANK PSC 1 1 1.000 1

Qualitative and Quantitative Research Review, Vol 3, Issue 3, 2018 ISSN No: 2462-1978 eISSN No: 2462-2117

113

MIZUHO BANK LTD 0.808 0.873 0.841 11

ROYAL BANK OF SCOTLAND 0.481 0.815 0.648 25

SHINHAN BANK 0.855 0.900 0.878 7

SOCIETE GENERALE 0.517 0.578 0.547 28

SONALI BANK 0.609 0.866 0.738 21

STANDARD CHARTERED BANK 0.607 1 0.804 16

STATE BANK OF MAURITIUS LTD 0.797 0.819 0.808 15