evaluation of the implementation of internal …

TRANSCRIPT

EVALUATION OF THE IMPLEMENTATION OF

INTERNAL CONTROL OVER CASH MANAGEMENT

(A CASE STUDY OF PROVIDENT FUND BENEFIT)

IN PT JAMSOSTEK

SKRIPSI

BY

Eva Afrianti

008200900024

Presented to

The Faculty of Economics, President University

In partial fulfillment of the requirements

For

Bachelor Degree in Economics, Major in Accounting

President University

Cikarang Baru – Bekasi

Indonesia

2013

ii

PANEL OF EXAMINERS

APPROVAL SHEET

Herewith, the Panel of Examiners declares that the skripsi “EVALUATION OF THE

IMPLEMENTATION OF INTERNAL CONTROL OVER CASH

MANAGEMENT (A CASE STUDY OF PROVIDENT FUND” that was submitted

by Eva Afrianti majoring in Accounting, Faculty of Economics has been assessed and

proved to have passed the Oral Examination. on April 22th, 2013.

Chair, Panel of Examiner,

……………………………..

(H.Misbahul Munir, Ak, MBA, CPMA).

Examiner I

……………………………..

(Drs.H.Umar Subandijo, Ak, MBA)

Examiner II

……………………………..

(Ahalik, SE, Ak, M.SI, M.Ak, CMA, CPMA, CPSAK, QPW, CPA)

iii

SKRIPSI ADVISOR

RECOMMENDATION LETTER

This skripsi entitled “EVALUATION OF THE IMPLEMENTATION OF

INTERNAL CONTROL OVER CASH MANAGEMENT (A CASE STUDY OF

PROVIDENT FUND BENEFIT) IN PT JAMSOSTEK” prepared and submitted by

Eva Afrianti in partial fulfillment of the requirements for Bachelor Degree in

Economics - Major in Accounting, has been reviewed and found to have satisfied the

requirements for a thesis fit to be examined. We therefore recommend this thesis for

Oral Defense.

Cikarang, Indonesia, April 22th, 2013

Acknowledge

DR.Sumarno Zain,SE,MBA,AkHead, Accounting Study Program

Skripsi Advisor,

Drs.H.Umar Subandijo,Ak,MBA

iv

DECLARATION OF ORIGINALITY

I declare that this thesis entitled “EVALUATION OF THE IMPLEMENTATION

OF INTERNAL CONTROL OVER CASH MANAGEMENT (A CASE STUDY

OF PROVIDENT FUND BENEFIT) IN PT JAMSOSTEK” is to the best of my

knowledge and belief, an original piece of work that has not been submitted, either in

whole or in part, to another university to obtain a degree.

Cikarang, Indonesia, April 22th, 2013

Writer,

Eva Afrianti

008200900024

v

ABSTRACT

This research was conducted to evaluate the over cash management procedure inthis company, and to analyze the implementation of internal control over cashmanagement of the company. In this study, the writer took PT. JAMSOSTEK Cikarangbranch, Jababeka as the writer object. PT. Jamsostek is a public program that providesprotections for workers to overcome the socio-economic risks that use of socialinsurance mechanisms.

This research is using qualitative data analysis with instrument inquiry the client,observation, documentation, and confirmation. As such, the qualitative method used inthis research is to analyze and evaluate the internal control of over cash management. Itis for finding out whether the implementation of cash management flow alreadycomplies with the stated rules and regulation.

Based on the research that has been done, there are several employees in PT.Jamsostek who become brokers to help the participant to process their claim its makethe queuing disorganized and make the participant who come first waiting longer. thisproblem occurs because the process of claim assurance is too long so the participantdon’t want to waiting for a long time, and lack of counter cashier in provident fundbenefit payment its make the process of payment not efficient anymore based on theamount of the participant because of this problem PT. Jamsostek have to additionalworking hours the employee to cover all the participant

The writer recommends the PT. Jamsostek improve their internal control overcash management in provident fund benefit claim is starts from the brokers, head ofservice department should given the punishment to the employee who will be the brokerand for the counter cashier added based on the amount of participant to make theprocess of payment more effective and efficient

Key words: Internal control, cash management, provident fund benefit

vi

ACKNOWLEDGEMENT

First of all, I want to thank Allah SWT for the bless and will so this thesis that is one of

requirements to accomplish Bachelor Degree for Faculty of Economics in President

University could be finished eventually. Also, indeed I would not have enough spirit in

finishing this thesis without the encouragement from my beloved parents H. Kaprawi

Mahmud S.SOS and Hj. Jumiem SE, my lovely brothers Teguh Prayitno and all the

relatives. My thanks go first and foremost to them.

Second, I want to thank Drs.H.Umar Subandijo,Ak,MBA., as my adviser that advices

and monitors my progress during the completion of thesis. Also to H.Misbahul

Munir,Ak,MBA., and DR.Sumarno Zain,SE,MBA,Ak., who have helping me in starting

my thesis. And to all my lectures, especially for the lectures who have taught me from

the first semester. In addition, thanks to all lectures that will be my examiner in oral

defense that also have big contribution for me to accomplish my study.

Third, I want to thank to PT. JAMSOSTEK that has allowed me to do my Skripsi study

here. Thank you MR. Sony and Ms Putri who already help me a lot to complete this

Skripsi

Fourth, I want to thank all of my friends especially to “Palu Community”, dorm mates,

and “Accounting 2009”, who gave me precious unforgettable memories. Then, thanks to

my senior Yandri and M. Fikhri for their understanding. I sincerely thank for those who

supported me during the completion of this thesis, especially to, Tyas, Ramsi Ganteng,

Tika, Inggrit, Dinni, Mimi, Ima, Anggun, Rara, Eko, Irna, Putri, Igeb, the vongger’s

I hope this thesis can clearly illustrate the objectives of research that I gain during the

study in President University. However, I really open to any suggestion to improve my

understanding about this thesis.

Cikarang, April 22th, 2013

Eva Afrianti

vii

TABLE OF CONTENT

ContentsPANEL OF EXAMINERS............................................................................................ iiSKRIPSI ADVISOR.................................................................................................... iiiDECLARATION OF ORIGINALITY ......................................................................... ivABSTRACT ................................................................................................................. vACKNOWLEDGEMENT ........................................................................................... viTABLE OF CONTENT .............................................................................................. viiLIST OF FIGURES ..................................................................................................... ixCHAPTER I ................................................................................................................. 1

I.1. Research Background ......................................................................................... 1I.2. Problem Identification and Statement.................................................................. 21.3. Research Scope and Limitation .......................................................................... 31.4. Research Objectives ........................................................................................... 31.5. Research Benefits............................................................................................... 41.6. Research Method................................................................................................ 4

CHAPTER II ................................................................................................................ 5II.1. Internal Control ................................................................................................. 5

II.1.1. Definition of Internal Control...................................................................... 5II.1.2. Internal Control (COSO)............................................................................. 6II.2.3. Components of Internal Control .................................................................. 6II.1.4. Limitation of Internal Control ................................................................... 11II.1.5. The Objectives of Internal Control ............................................................ 12

II.2. Cash Management ........................................................................................... 13II.2.1. Cash Collection and Disbursement............................................................ 14II.2.2. Internal Control and the Management Process........................................... 16II.2.3. Provident Fund Benefit ............................................................................. 18

CHAPTER III ............................................................................................................. 22III.1. Data Collecting and Processing ...................................................................... 22III.2. Company’s Existing Condition....................................................................... 28

III.2.1. History of the Company........................................................................... 28III.2.2. Organization Structure............................................................................. 32III.2.3. The Company’s Operation on over Cash Management............................. 34III.2.3 Cash Receipt Process of provident Fund Benefit ....................................... 35

IV.1. Strength Findings ........................................................................................... 40IV.1.1. Control Environment ............................................................................... 40

viii

IV.1.2. Control Activity ...................................................................................... 42IV.2. Findings ......................................................................................................... 45

CHAPTER V.............................................................................................................. 48V.1. Conclusion ...................................................................................................... 48V.2. Recommendation............................................................................................. 51

REFERENCES ........................................................................................................... 52ATTACHMENTS....................................................................................................... 53

ix

LIST OF FIGURES

Figure 3.1 Organization Structures ..............................................................................................32

Figure 3.2 Cash Receipt Flow Chart ............................................................................................35

Figure 3.3 Cash Disbursement Flow Chart .................................................................................36

1

CHAPTER I

INTRODUCTION

I.1. Research Background

Every company has its own internal control to make sure the business runs in an

appropriate way, rely on the standard operation procedures to control all system

operations, any company needs internal control. Internal control is a procedure the

company to achieve company goals

In all companies, finance is the heart of the company, and the most important

element in finance is cash. Besides, cash is important it needs protection because of its

liquidity. Liquidity means that the company can use the money without any restriction

in daily operations. Without proper management and control of cash, operating a

successful business can be extremely difficult. Facing competition, working with

buyers, and countering outside forces are challenging in themselves. Many businesses

neglect to use their resources. Basically, the management has to ensure the cash

management and protection. Cash management means how you manage cash whether

cash receipt or cash disbursement and other liquid assets to meet company’s financial

goals.

The writer takes Jamsostek as material for this thesis because Jamsostek is a

service company, which systems of cash in and cash out are different with the other

companies. The existing problems in the company's cash management services is the

procedure of cash receipt and cash disbursement. In the service company cash

2

disbursement for assurance payment is conducted everyday and for cash receipt is

coming from assurance dues from members of Jamsostek

Based on description above, the writer is interested in doing research with the

title, “EVALUATION OF THE IMPLEMENTATION OF INTERNAL CONTROL

OVER CASH MANAGEMENT (A CASE STUDY OF PROVIDENT FUND BENEFIT)

IN PT. JAMSOSTEK“. Writer is using qualitative method in order to get primary data.

The writer gathers references or relevant theories from text books, internet sources, and

other scientific sources to be compared with data obtained from field research.

I.2. Problem Identification and Statement

Based on the preliminary survey in the company in some problems about cash

management might occur, in the process of cash disbursement payment of claim

insurance and cash receipt flow and procedure. Therefore, the writer looking for how is

the company solving the problems and has own procedure to managing the over cash

management.

The procedure is usually done by the company is cash receipts, reconciliation of

cash receipt, Bookkeeping, insurance claim procedures, The writer has found some

indicators of problems/weaknesses in over cash management provident fund benefit at

PT. Jamsostek

On this research, the writer on this research wants to ensure that the company

has implemented all of the internal control over cash management.

How is the flow of the cash receipt and the cash disbursement implemented?

How is the internal control of cash receipt and cash disbursement implemented in

the company?

3

1.3. Research Scope and Limitation

The writer focuses with the internal control over cash management in PT.

Jamsostek. The writers want to evaluate the over cash management activity and

implementation internal control on the process of cash receipt and cash

disbursement of provident fund benefit.

There are five components of internal control which are control

environment, risk assessment, control activities, communication and information,

and monitoring, but not in all criteria of those five components taken. The research

focuses on control environment and control activities only.

Firstly, In control environment the writer investigates only focus on

assignment of organization structure, policy and human resource, and authority and

responsibility

Secondly, in control activities the writer investigates only focus on approval,

authorization, and reconciliation

1.4. Research Objectives

The writer determines some objectives that must be accomplished in this study:

Understand the important thing of internal control of cash management at PT.

Jamsostek

To identified the weaknesses over cash management at PT. Jamsostek

To formulate the recommendation to overcome the weaknesses

4

1.5. Research Benefits

a. For company

The research can give benefit to the company with the result from the analyzes

especially in maintaining the internal control of cash management in the company.

Management can also take this research as one consideration for next internal control

development on cash management of provident fund benefit.

b. For Writer

This research can enrich knowledge and understanding in the implementation of

internal control over cash management for the writer. The writer can know more about

the company and know how to organize a company.

1.6. Research Method

This research uses qualitative method with case study approaches. In doing case

study approach, the writer collects data through literature review and field research.

Data that use is primary data and secondary data those data are taken directly from

field research.

In literature review, the writer finds out some theories from text books, journals,

internet, and others reliable scien3tific sources. Those theories will be used as criteria

to be compared with primary data collected through field research.

In field research, the writer uses instrument of audit in order to get the primary

data. This instrument is called audit evidence. It consists of Inquiries of The Client,

Observation, Documentation, and Confirmation, ect.

5

CHAPTER II

LITERATURE REVIEW

II.1. Internal Control

II.1.1. Definition of Internal Control

According to Horngren and Horrison (2007) a key responsibility of a business

owner is to control operations. Owners set goals; they hire managers to lead the way

and employee carry out the plan. Internal control is the organization plan and all the

related measures designed to:’

1. Safeguard Assets

A company must safeguard its assets; otherwise it’s throwing away resources. If you

fail to safeguard your cash, it will slip away.

2. Encourage Employee to Follow Company Policy

Everyone in an organization needs to work toward the same goal. With a friend

operating part of in motion, it’s important for both of you to pursue the same goal.

It’s also important for you to develop policies so that you treat all customers’

similarity.

3. Promote Operational Efficiency

You cannot to afford to waste resources. You work hard to make a sale, and you do

not want to waste any of the benefits. Eliminate waste, and increase your profit.

4. Ensure Accurate, Reliable Accounting Records

Good records are essential. Without reliable records you cannot tell which part of the

business is profitable and which part needs improvement. (p. 408).

6

II.1.2. Internal Control (COSO)

Internal control is a process, affected by an entity’s board of directors, management, and

other personnel, designed to provide reasonable assurance regarding the achievement of

objectives in the following categories:

Effectiveness and efficiency of operations

Reliability of reporting

Compliance with applicable laws and regulations.

II.2.3. Components of Internal Control

Robertson and louwers (2002) has defined the components of internal control

which divided into 5 categories, there are:

Control Environment

The control environment sets the tone of an organization, influencing the control

consciousness of its people. It is the foundation for all other components of internal

control, providing discipline and structure. Control environment factors include the

following:

o Management’s philosophy & operating style - The belief (or lack of it) in the

importance of internal control by management will affect the seriousness

with which is taken by the rest of the employees. This is especially the case

when decision-making in the company is dominated by a single individual.

o Management and employee Integrity & Ethical values – existence and

implementation of codes of conduct and other policies regarding acceptable

business practice, conflicts of interest or expected standard of ethical and

moral behavior. Dealing with employee, supplier, customer, investor,

creditor, insures, competitors and auditor. And pressure to meet unrealistic

performance targets.

7

o Company Organizational structure - A company that operates all over the

world has different internal control problems than one operating entirely

within a single building.

o Company Commitment to competence - Formal or informal job description

or other means of defining task that comprise particular jobs. And analysis of

knowledge and skill needs to perform jobs adequately.

o Functioning of the board of directors, particulary its audit committee - An

audit committee of the board of directors that actively monitors the internal

audit function produces a more attentive management on such matters.

o Methods of assigning authority and Responsibility assignment - The manner

in which authority, responsibility and accountability is assigned to different

employees determines the controls that will be needed. Again, the

domination of decision-making by a single individual holds significance,

since such power makes it extremely difficult for internal control to be

trusted.

o Human resource policies & practices – Extend to which policies and

procedure hiring, training, promoting, and compensanting employees are in

place.” (p. 146-147)

Control Activities

Control Activities are policies and procedures that help ensure that management

directives are carried out.

There are four elements which are:

Performance reviews – management has primary responsible for being met.

Performance reviews required management activities participation in the

8

supervising operation to ensuring the organization actual vs. budget, P/Y,

financial to non-financial.

Segregation of duties is includes assigning different people the

responsibilities authorizing transactions, recording transactions, maintaining

custody of assets, and performing comparisons. It is intended to reduce the

opportunities to allow any person to be in a position to both perpetrate and

conceal errors or irregularities in the normal course of their duties.

1. Authorization of transactions is this duty belongs to people who have

authority and responsibility for initiating the recordkeeping for

transaction. The authority may be general, referring to a class of

transaction or it may be specific.

2. Recording transaction of transactions is this duty refers to the accounting

and recordkeeping function whis, in most organization is delegated to a

computer system.

3. Custody of assets is this duty refers to the actual physical possession or

effective physical control of property.

4. Periodic reconcialition of existing assets or recorded amounts is this

duty refers to making comparison at regular intervals and taking

appropriate action with respect to any difference.

Physical controls is physical Access to assets and important record, document

and blank forms should be limited to authorized personnel. Such assets as

inventory and security should not be available to persons who have no need

to handle them.

9

Information processing controls are organized under three categories – input

controls, processing control and output controls.

1. Input control activities are designed to provide reasonable assurance that

data received for processing by the computer department have been

authorized properly and converted into the machine sensible form, and that

data have not been lost, suppressed, added, duplicated or improperly

changed.

There are 11 following control such as Input authorized and

Approved ,Check Digits, Record Batch financial totals,Batch hash ,Valid

character totals,Valid sign,Missing data test,Sequence test,Limit or

reasonableness test, and Error correction and resubmission

2. Processing control activities are designed to provide reasonable assurance

that data processing has been performed as intended without any omission

or double- counting of transaction. And this other important control such

as: run-to-run totals, control total reports, file and operator controls, limit

and reasonable tests.

3. Output control activities are the final check on the accuracy of the results

of computer processing. These controls should be designed to ensure that

only authorized person received reports or have to files produced by the

system. The typical outputs controls are: controls totals, mater file

changes, and output distribution.”(p.150-155)

Risk assessment

An entity's risk assessment for financial reporting purposes is its identification,

analysis, and management of risks relevant to the preparation of financial statements

that are fairly presented in conformity with GAAP. Risk assessment includes risks that

10

may affect an entity's ability to properly record, process, summarize, and report

financial data. Risk assessment, for example, may address how the entity considers the

possibility of unrecorded transactions or identifies and analyzes significant estimates

recorded in the financial statements.

Risks relevant to financial reporting include external and internal factors such as

the following: Changes in operating environment, new personnel, New or revamped

information systems, Rapid growth, new technology, New lines of business, products or

activities, Corporate restructurings, Foreign operations, and Accounting

pronouncements. “(p.147)

Information and communication

Information and communication is Refers to the I.D, retention, and transfer of

information in a timely manner allowing personnel to perform their responsibilities.

1. Info system consists of the methods and records used to record, process,

summarize and report Co.'s transactions and to maintain accountability for

the related accounts.

2. Communication involves establishing individual duties and responsibilities

relating to internal control and making them known to involved

personnel.”(p.148-149)

Monitoring

An important management responsibility is to establish and maintain internal

control. Management monitors controls to consider whether they are operating as

intended and that they are modified as appropriate for changes in conditions.

11

Monitoring is a process that assesses the quality of internal control performance over

time. (p.155-156).

The internal control system comprises policies, practices, and procedure

employee by the organization to achieve four broad objectives:

1. To safeguard assets of the firm.

2. To ensure the accuracy and reliability of accounting records and information

3. To promote efficiency in the firm’s operations.

4. To measure assumption with management prescribed policies and procedures.

II.1.4. Limitation of Internal Control

Robertson and louwers (2005) defined that “There are several limitation to

internal control systems that prevent management from obtaining complete assurance

that company controls are absolutely effective.

These limitation include:

1. Human error

2. Deliberate circumvention

3. Management override

4. Improper collusion.” (p.174)

According to Hall (1998) explained “every system of internal control has

limitation on its effectiveness, these are included:

1. Human error

2. Deliberate circumvention

3. Management override

4. Changing collusion.” (p.115)

12

Based on this limitation above, it can be conclude in the possible of errors not

system is perfect, in the circumvent is personnel may circumvent the system through

collusion or other means, management override is in a position to override control

procedure by personally distorting transactions or by directing a subordinate to do so,

and changing collusion may change over time so that existing control may become

ineffectual.

II.1.5. The Objectives of Internal Control

According to Arens there are seven objectives of internal control as follows:

- Validity: All transactions processed are valid.

- Completeness: All transactions are included.

- Timelines: All transactions are recorded on a timely basis.

- Authorization: All transactions are properly authorized.

- Valuation: All transactions are properly valued.

- Classification: All transactions are classified into the proper amount.

- Posting and summarization: All transactions are properly recorded in journals and

properly posted in special and general journals. (p.198)

According to Warren, James & Duchac said that, the objectives of internal

control are to provide reasonable assurance that:

1. Assets are safeguarded and used for business purposes.

2. Business information is accurate.

3. Employees and managers comply with laws and regulations.

Internal control can safeguard assets by preventing theft, fraud, misuse, or

misplacement. A serious concern of internal control is preventing employee fraud.

Employee fraud is the intentional act of deceiving an employer for personal gain.

Accurate information is necessary to successfully operate a business. Business must

also comply with laws and regulations, and financial reporting standard. (p.316)

13

II.2. Cash Management

According to Incorporate.com cash management is a broad term that refers to

the collection, concentration, and disbursement of cash. The goal is to manage the

cash balances of an enterprise in such a way as to maximize the availability of cash

not invested in fixed assets or inventories and to do so in such a way as to avoid the

risk of insolvency. Factors monitored as a part of cash management include a

company's level of liquidity, its management of cash balances, and its short-term

investment strategies.

In some ways, managing cash flow is the most important job of business

managers. If at any time a company fails to pay an obligation when it is due because

of the lack of cash, the company is insolvent. Insolvency is the primary reason firms

go bankrupt. Obviously, the prospect of such a dire consequence should compel

companies to manage their cash with care. Moreover, efficient cash management

means more than just preventing bankruptcy. It improves the profitability and reduces

the risk to which the firm is exposed.

Cash management is particularly important for new and growing businesses.

Cash flow can be a problem even when a small business has numerous clients, offers a

product superior to that offered by its competitors, and enjoys a sterling reputation in

its industry. Companies suffering from cash flow problems have no margin of safety

in case of unanticipated expenses. They also may experience trouble in finding the

funds for innovation or expansion. It is, somewhat ironically, easier to borrow money

when you have money. Finally, poor cash flow makes it difficult to hire and retain

good employees.

14

It is only natural that major business expenses are incurred in the production of

goods or the provision of services. In most cases, a business incurs such expenses

before the corresponding payment is received from customers. In addition, employee

salaries and other expenses drain considerable funds from most businesses. These

factors make effective cash management an essential part of any business's financial

planning. Cash is the lifeblood of a business. Managing it efficiently is essential for

success.

When cash is received in exchange for products or services rendered, many

small business owners, intent on growing their company and tamping down debt,

spend most or all of these funds. But while such priorities are laudable, they should

leave room for businesses to absorb lean financial times down the line. The key to

successful cash management, therefore, lies in tabulating realistic projections,

monitoring collections and disbursements, establishing effective billing and collection

II.2.1. Cash Collection and Disbursement

According to Inc.com cash collection systems aim to reduce the time it takes to

collect the cash that is owed to a firm. Some of the sources of time delays are mail

float, processing float, and bank float. Obviously, an envelope mailed by a customer

containing payment to a supplier firm does not arrive at its destination instantly.

Likewise, the payment is not processed and deposited into a bank account the moment

it is received by the supplier firm. And finally, when the payment is deposited in the

bank account oftentimes the bank does not give immediate availability of the funds.

These three "floats" are time delays that add up quickly, and they can force struggling

or new firms to find other sources of cash to pay their bills.

15

Cash management attempts, among other things, to decrease the length and

impact of these "float" periods. A collection receipt point closer to the customer—

perhaps with an outside third-party vendor to receive, process, and deposit the payment

(check)—is one way to speed up the collection. The effectiveness of this method

depends on the location of the customer; the size and schedule of its payments; the

firm's method of collecting payments; the costs of processing payments; the time

delays involved for mail, processing, and banking; and the prevailing interest rate that

can be earned on excess funds. The most important element in ensuring good cash flow

from customers, however, is establishing strong billing and collection practices.

Once the money has been collected, most firms then proceed to concentrate the

cash into one center. The rationale for such a move is to have complete control of the

cash and to provide greater investment opportunities with larger sums of money

available as surplus. There are numerous mechanisms that can be employed to

concentrate the cash, such as wire transfers, automated clearinghouse (ACH) transfers,

and checks. The tradeoff is between cost and time.

Another aspect of cash management knows a company's optimal cash balance.

There are a number of methods that try to determine this magical cash balance, which

is the precise amount needed to minimize costs yet provide adequate liquidity to ensure

bills are paid on time (hopefully with something left over for emergency purposes).

One of the first steps in managing the cash balance is measuring liquidity, or the

amount of money on hand to meet current obligations. There are numerous ways to

measure this, including: the Cash to Total Assets ratio, the Current ratio (current assets

divided by current liabilities), the Quick ratio (current assets less inventory, divided by

current liabilities), and the Net Liquid Balance (cash plus marketable securities less

short-term notes payable, divided by total assets). The higher the number generated by

16

the liquidity measure, the greater the liquidity—and vice versa. However, there is a

tradeoff between liquidity and profitability which discourages firms from having

excessive liquidity. http://www.inc.com/guides/finance/cashmanagement.html

II.2.2. Internal Control and the Management Process

According to Coyle (1999) explain the financial directors of a company has a

responsibility for ensuring that controls for cash are adequate and properly applied on a

day-to-day basis. “Control over cash management can be achieved by applying eight

long-established principles of internal control.” These are taught to accountancy

students and learned by mnemonics such as OAP SPASM or SPAM SOAP.

The eight principles of internal control are:

O Organization and procedural controls

A Authorization

P Physical controls

S Segregation of duties

P Personnel controls

A Accounting and arithmetic controls

S Supervision

M Management controls

Organization and Procedural Controls

The organization for cash management should have a clear structure of allocated

authority, responsibility, and lines of reporting. Routines and procedures should be

strictly enforced. Every individual must know he or she can and can’t do, and must or

17

must not do. For example, the person responsible for paying in checks has to be made

aware that checks must be banked on the day of receipt.

Authorization

There should be a limited number of individuals authorized to sign checks and to make

bank transfers. Two signatures might be required on checks over $2,000

Physical Controls

Physical controls should be applied to restrict the access of unauthorized staff to check

books and petty cash. Valuable items should be kept in a secure place until required.

“Physical restriction also should exist if possible to access limited to authorized

personnel only.” Thesed areas should be kept locked when empty.

Segregation of Duties

No single person should be responsible for authorizing, making, recording, and

monitoring cash payments. Where applicable, the cashier responsible for handling cash

payments/receipts should not be bookkeeper who records the transactions in the

cashbook, not the person responsible for authorizing payments.

Personnel Controls

Employees who will be handling cash receipt and payments should be screened as

potential security risks before their appointment. References from previous employers

should be checked.

Accounting and Arithmetic Controls

18

There should be rules and procedures for making detailed checks on the accuracy and

completeness of transactions; for examples checks that settlement discount have been

properly calculated and routine checks that all payments have been properly authorized.

Supervision

Ideally there should be regular supervision by responsible officials of day-to-day cash

transactions.

Management Controls

Managers should be responsible for the proper functioning of all cash management

controls through a system of regular reporting, analysis and review. This should include

budgeting and budgetary control reports, adhoc checks, ect.

Good management is a key requirement for effective security and controls because

management must be responsible for making sure that controls are adequate, that they

key exercised and that they work as well as can be expected.

II.2.3. Provident Fund Benefit

Social Security Program is a program that is basic protection for workers who aim to

ensure the security and assurance of social and economic risks, and is the guarantor of

the current means of receiving income for workers and their families resulting from the

occurrence of social risks in financing affordable by employers and labor.

Socio-economic risks addressed by this program is limited during the accident, illness,

pregnancy, maternity, disability, old age and death, which result in reduced or cut off of

19

labor income and / or require medical care of the Implementation of Social Security is

using insurance mechanisms Social.

Provident fund benefit program is intended as a substitute for labor income due to

disconnection of death, disability or old age and held the old-age savings

systems. Provident fund benefit Program provide assurance that revenue receipts are

paid at the time of labor reaches age 55 years old or has fulfilled certain requirements.

Provident Fund Benefit Program contributions:

* Company Contribution = 3.7%

* Charged Labor = 2%

Provident fund benefit amounts to the accumulated contributions plus investment

results.

Circular of the Director General of Inspection Guidance Ministry of labor and

Transmigration of Indonesia Number B.337/DJPPK/IX/05 explained provident fund

benefit will be refunded / paid registration fees collected plus investment results, if the

labor:

* Reached the age of 55 years or death, or total and permanent disability

* Experiencing layoffs after becoming a participant of at least five years with one-

month waiting period

* Went abroad never to return, or as civil servants / police / armed forces

20

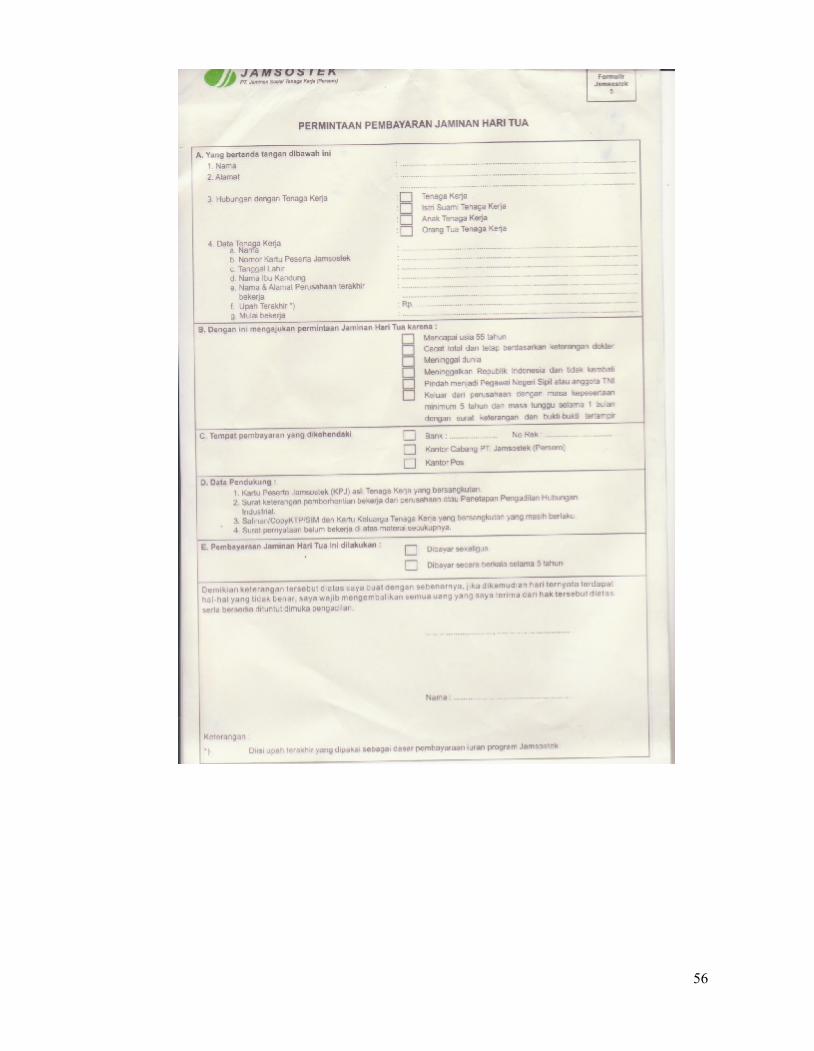

Procedures for Filing Assurance

1. Each request JHT, workers must fill out and submit forms to the office five

Jamsostek local

Social Security by attaching:

a. Jamsostek Card (KPJ) original

b. Self identity card identity card / driving license (photocopy)

c. A letter from the company stops working or the Industrial Relations Court

Decision

d. Waiver of stamp duty has not worked in moderation

e. Family Card (KK)

2. JHT payment request for workers who experience total disability accompanied by

Medical Certificate

3. Demand payment for labor JHT leave the territory of the Republic of Indonesia

accompanied by:

a. The statement does not work anymore in Indonesia

b. Passport Photocopy

c. Photocopy VISA

4. Old Ages Benefit payment request for workers who die before the age of 55 yrs is

attached:

a. A death certificate from the Hospital / Police / Villages

b. Photocopy Card family

5. Old Ages Benefit payment request for workers from the companies that stopped

working before the age of 55 yrs has met the membership has passed the five-year

21

waiting period 1 (one) months from the relevant workforce stop work, accompanied

by:

a. Photocopy letter from the company stopped working

b. Waiver is not working anymore

c. Old-ages Benefit payment request for workers who became Civil Service / Police /

Armed Forces

No later than 30 days after such submission PT Jamsostek (Persero) make payments

of old ages benefit.

22

CHAPTER III

METHOD OF DATA PROCESSING

AND COMPANY’S EXISTING CONDITION

III.1. Data Collecting and Processing

The writer did primary data collection start from November, 26st 2011 until

December, primary is data observe and collecting from field work. This data can

support the writer get information for this thesis and theories are following from text

book and other resource. From seven types of evidence, the writer using four types of

evidence approach such as inquiries of the clients, observation, documentation, and

confirmation. The data that collected are data related with internal control over cash

management

Inquiries of the clients

Researchers obtained data from the company through interviews and discussions

with some employees. The writer asked some questions to Operational Director,

Permanent Accounting Staff, and Provident Fund Benefit Department staff.

Although considerable evidences are obtained from client through inquiry, it usually

cannot be regarded as conclusive because it is not from independent source and may be

biased in the client’s favor.

In conducting the investigation to a client, the researchers got the data and

information such as problem in cash management, cash receipt procedure, cash

disbursement procedure, company profile, job description employees, and those have

the right to authorize in the company.

23

Interview took place on Monday November 26, 2012. The writer interviewed the

following staff of the company:

a. Finance department staff ( Sony Eka Santana)

b. Service department staff ( Putri)

Before conducting the interview, The writer already prepared the question.

Interviewed (writer) read the questions to the respondents and wrote the answer of the

interviewed was conducted directly and personally. Through this interview the writer

collected information as follows:

The result interview:

1. Jamsotek cash receipt transaction of provident fund benefit is by transfer in bank

Mandiri account

2. Jamsostek cash disbursement transaction of provident fund benefit is by check,

transfer to participant bank account, and cash

3. Jamsostek has a system about calculating and managing budgeting cash receipt

and cash disbursement, the name of this system is Key Performance Indicator.

4. Key performance indicator also review the performance every employee in PT.

Jamsostek monthly

5. Budgeting for cash disbursement is given from the central office every 6

months, and from that budgeting will be divided per month.

6. In Jamsostek income for cash receipt only from participant of Jamsostek and

sector informal

7. Every cash receipt in Cikarang branch the cash will be automatically transferred

to the central office of account.

8. Budget plan cash receipt according with the number of Jamsostek participants

24

9. Companies who commit fraud in the payment of dues, the company is liable to

imprisonment for ever 6 (six) months or a a maximum penalty of Rp.

50.000.000, -

10. Jamsostek do reconciliation every month between the bank statement of cash

receipt and participant of Jamsostek

11. To Provident Fund Benefit cash will only out if there are participants claim

12. Cash disbursements more than Rp 15,000,000 should be approve before from

the Head office, the head of Finance department and head of the of Service

department. If less than Rp 15,000,000.- only requires the approval of head of

Finance Department and head of the of Service department

13. There is no limit of cash disbursement for each day because Jamsostek conduct

in accordance claim Provident Fund Benefit per day

14. From claim assurance of provident fund benefit, participants should fill out the

form provided and attach the applicable requirements to avoid fraud

15. There is no limit to the amount of cash disbursement

Observation

In this procedure, the writer gathered data by seeing, smelling, hearing,

tasting and feeling to assess certain activities. Through observation, the writer

obtained information about the invoice process, cash receipt and cash

disbursement document, and how the finance and accounting department make

invoice based on the document.

By observing the activities of the company, researchers were able to know

how finance department to calculate the cash receipt and cash disbursements

The writer is conducting the observation on Monday March 4, 2013, at

08.00am- 03.00pm. The result as observation as follow

25

1. Work hours for provident fund benefit are 6 hours start from 08.00am –

03.00pm, there are 120 participants. In process take money of claim

assurance is need 5 minutes per person. PT. Jamsostek just provide just

one counter cashier and for all kinds of claim assurance and the

participant have to waiting for take money process is more or less 2 hors

per participant. As a result of the transaction writer today is

a. Transfer transactions is 12 persons.

b. Cash transaction is 108 persons.

2. In financial department there is separate section for verification of data.

so that incoming data can be ensured correctly

3. From claim assurance of provident fund benefit, participants should fill

out the form provided and attach the applicable requirements to avoid

fraud

4. For the public service department room the design is without any

restrictions, based on with the Jamsostek quality policy of transparency

between participants and employee of service department can

communicate well.

5. Job description at PT. Jamsostek run in accordance with the duties of

each individual

Documentation

Documentation is the process of tracking down evidences either internal or external

evidences of transactions or activities being researched. The documents examined by

the writer are the records used by the client to provide information for conducting its

business in an organized manner, and may be in paper form, electronic form, or other

media. During research period, the writer collected data such as evidence of cash

receipt and cash disbursement.

26

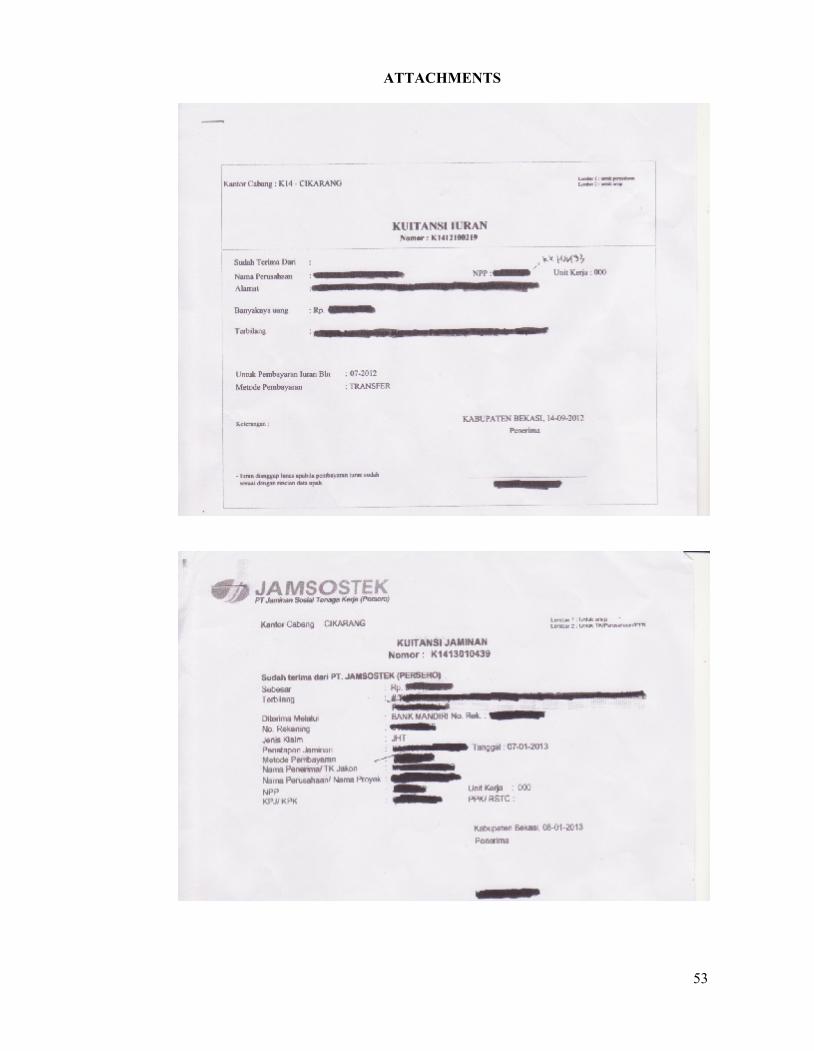

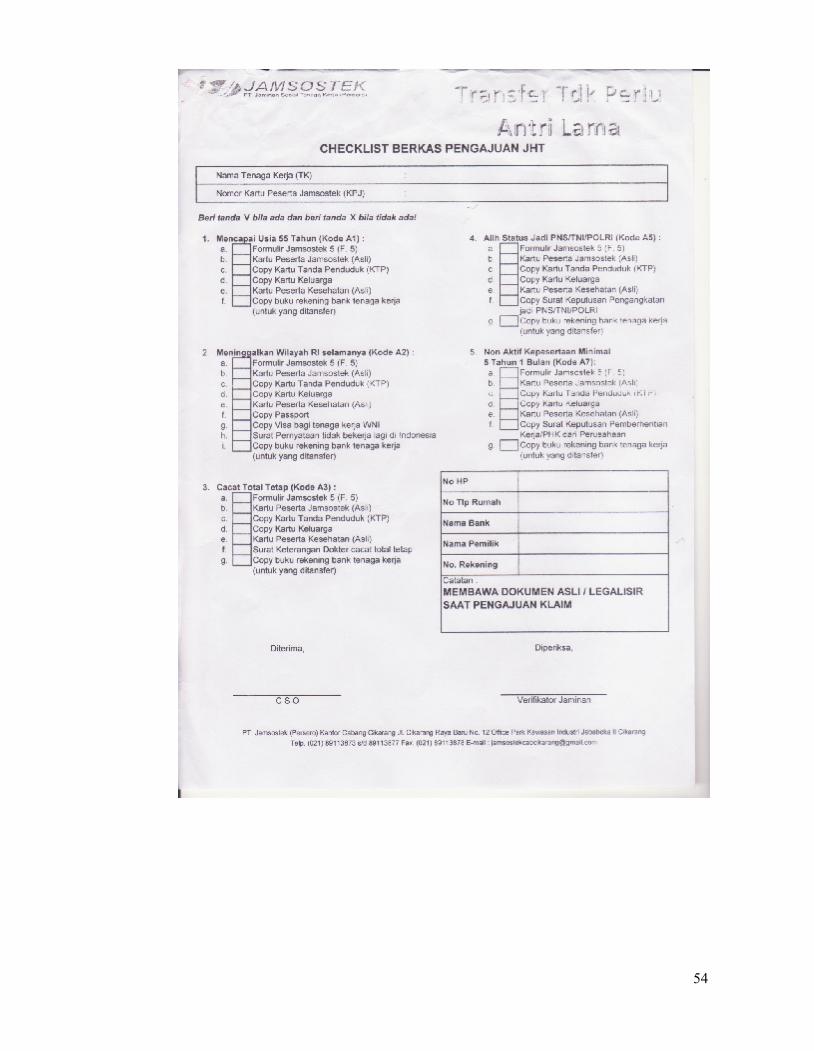

The writer collected some data as follows:

1. Flow chart cash receipt and cash disbursement

Flow charts provide information about the flow cash receipt and cash

disbursement flow in the form of images to make the reader easy to

understand the process.

2. Receipt of cash receipt and cash disbursement

Receipt, will give information about the company control of any cash

receipt and cash disbursement.

3. Job description

Job description, will give the information about any kind of job that need to

be done for each employee in the company

4. Organization structure

To know more clearly who authorize the documents in a company the

writer needs to understand the organization structure. With this

understanding, the writer will find out whether the process has an

appropriate authorization document process.

5. Company Profile

The purpose of company profile is to give a big picture about the

company’s history. This document provides information about what kind of

business that the company runs, when the founding of the company, what is

company’s mission and vision, ect.

6. Rules and Regulation

To understand more about the company, the writer need to understand too

overall procedure that related to over cash management.

27

Confirmation

Confirmation is process getting verification about certain information from third

party. The writer collects the information by conducting an interview with the third

party.

No Question Result information from provident

fund benefit participant

1 According to your opinion, what

the weaknesses in the process of

claim provident fund benefits?

1. The queue process take a long

time

2. Sometimes, there is the

cheater in queue.

2 What do you mean about the

cheaters?

There is brokers service (calo)

3 How do you know? I have experience with it

4 Who are offered you? Someone I meet in the office

5 so it means, the cause of the queue

number is not organized and take a

long time is because people who

use brokers?

Yes. something like that

6 Why you did not report this

problem?

Because I don’t want to get trouble if

I do it

7 Beside that, is there any complain? Yes, if possible the cashier to add and

make counter based on the payment

for cash, check, and transfer. so for

28

the transfer transaction can save the

time.

8 What the advantages of provident

fund benefit?

1. Good office facility such as

air conditioner, TV, and free

parking

2. If there is problem with

participantship, the customer

service officer manage it

faster and can be managed in

any branch office.

III.2. Company’s Existing Condition

III.2.1. History of the Company

Implementation of the social security program is one of the responsibilities and

obligations of the State to provide social protection to the public economy. In

accordance with the conditions of the financial capability of State, Indonesia as well as

many other developing countries, develop social security programs under funded social

29

security, social security is funded by the participants and the community is still limited

to formal sector workers.

History of the formation of PT Jamsostek (Persero) experienced a long process,

starting from the Law No.33/1947 jo Law No.2/1951 on workplace accidents,

Regulation of the Minister of Labor (PMP) PMP No.8/1956 on No.48/1952 jo relief

arrangements for the implementation of health workers, PMP No.15/1957 on the

establishment of Social Workers Foundation, PMP No.5/1964 on the establishment of

the Social Security Fund Foundation (YDJS), the enforcement of Law No.14/1969 on

the Principles of Labor, chronologically the birth process of social insurance labor

increasingly transparent.

After experiencing the progress and development, both related to the legal basis, a

form of protection and how the implementation, in 1977 obtained an important

milestone with the issuance of Government Regulation (PP) No.33 year 1977

concerning the implementation of social insurance programs of labor (ASTEK), which

obliges each employer and the SOEs to private entrepreneurs ASTEK program. Also

published PP No.34/1977 on the establishment of Perum Astek ASTEK organizers.

The next important milestone is the birth of Act No.3 of 1992 on Social Security

Workers (JAMSOSTEK). And through the enactment of Government Regulation

No.36/1995 PT Jamsostek as the body administering the Employee Social Security.

Social Security program provides basic protection to meet the minimum requirements

for workers and their families, by providing certainty of ongoing revenue stream of

family income as a substitute for partially or completely lost income, due to social

risk.

30

Furthermore, at the end of 2004, the Government also issued Law Number 40 Year

2004 on National Social Security System, which is associated with the 1945

Amendment to the changes in article 34 paragraph 2, where the People's Consultative

Assembly (MPR) has approved these amendments, which now reads: "The state has

developed a system of social security for all people and to empower the weak and

incapable in accordance with human dignity." Benefits of such protection can give

security to the workers so that they can concentrate more in increasing motivation and

productivity.

Company gait that prioritize the interests and rights in the Indonesian Labor normative

continues. Until now, PT Jamsostek (Persero) provides protection 4 (four) courses,

which include the Employment Accident Insurance Program (JKK), Death Benefit

(JK), Old Age Security (JHT) and Health Care (JPK) for the entire workforce and his

family.

With the implementation of more advanced, Social Security program is not only

beneficial to workers and employers but also plays an active role in improving

economic growth for the welfare of society and the nation's future development.

Vision and Mission

Vision

Being the Organizer of World Class Social Security Board (BPJS), reliable, friendly and

superior in operations and services.

31

Mission

As the agency administering the social security workforce that meets the basic

protection for workers as well as a trusted partner;

* Labor: Provide adequate protection to workers and families

* Entrepreneur: Being a trusted partner to provide protection for labor and increase

productivity

* Country: Participate in development

PT. Jamsostek Quality Policy and Quality Objectives

Quality Policy

Management and the entire branch staff have a strong commitment to always:

1. Increase the number of participant satisfaction and retention by providing

service excellence and optimal benefits.

2. Managing the organization's resources include: competency-based human

resources, finance, facilities, infrastructure, information, and transparent

working environment in accordance with the applicable provisions

3. Ensure that all activities within the organization to meet the requirements and

continually make improvements in all aspects of the organization's ongoing

immediately in order to increase corporate value and benefits to interested

parties.

Quality Objectives

32

a. The organization in implementing the quality management system has set a goal

of quality in every field in the form of Key Performance Indicator (KPI) that

refers to the strategic goals of the company’s current year

b. Quality objectives have been established, periodically monitored every month

and periodically evaluated every 3 months

III.2.2. Organization Structure

MARKETINGDEPARTMENT

Account OfficerStaff

Administration

Figure 3.1 Structure Organization

32

a. The organization in implementing the quality management system has set a goal

of quality in every field in the form of Key Performance Indicator (KPI) that

refers to the strategic goals of the company’s current year

b. Quality objectives have been established, periodically monitored every month

and periodically evaluated every 3 months

III.2.2. Organization Structure

DIRECTOR

SERVICEDEPARTMENT

insuranceVerification

CUSTOMERSERVICE OFFICER

INFORMATIONTECHNOLOGIDEPARTMENT

Operator

PUBLIC PERSONALDEPARTMENT

Human Resource

FINANCEDEPARTMENT

AccountingVerification

Tax Verification

Figure 3.1 Structure Organization

32

a. The organization in implementing the quality management system has set a goal

of quality in every field in the form of Key Performance Indicator (KPI) that

refers to the strategic goals of the company’s current year

b. Quality objectives have been established, periodically monitored every month

and periodically evaluated every 3 months

III.2.2. Organization Structure

Health CareService Division

Health CareService

Verification

insuranceVerification

Figure 3.1 Structure Organization

33

1. Marketing Department

Planning, implementing, controlling, and coordinates marketing activities. Do

marketing policy implementation to ensure the achievement of business targets

and participants dues

2. Service Department

Planning, conducting, co-coordinating, and controlling the activities of JKK,

AGE, and JPK to ensure a smooth service guarantee.

3. Information and Technology Department

Plan, implement, coordinate, and control the use of hardware and software to

optimize your network and guarantee a fixed operational, computer device, and

manage databases and applications to ensure service to participants.

4. Human Resources and General Department

Do the coaching to improve the performance of employees and co-ordinate the

activities of personnel administration, archiving, procurement, maintenance and

infrastructure work as well as households in order to provide the optimum

support of the smooth operational

5. Health Care Service Department

Plan, implement, organized, control the marketing activities, and the

construction of a special program of inclusion based on strategies and targets

that have been set

34

Financing System, participantship, benefits, and social security service system

The Social Security Program is a program that is the basis for protection of labor

which aims to guarantee the security and certainty of risk-the risk of social economy. It

is also a means of receiving current guarantor of income for the workforce and their

families as a result of the occurrence of social risks with affordable financing by the

employers and the workforce..

Socioeconomic risk addressed by the program limited to the time of the event of

an accident, sickness, maternity, maternity, disability, old age and death, which

resulted in reduced income or the disconnection of labor and/or in need of medical

care. Organization of the social security program uses a mechanism of social insurance.

As public programs, Jamsostek gives rights and burdening liability for certain

(compulsory) for employers and the workforce on the basis of law No. 3 of 1992

regulate the kind of work accident Assurance Program (JKK), old age (JHT), death

(JKM) and guarantees the maintenance of health (JPK), while the obligations of

participants is the orderly administration and pay your

III.2.3. The Company’s Operation on over Cash Management

PT Jamsostek is a service company, Jamsostek has several products that

provident fund benefit, life insurance, health insurance, and health care. For the case

study, the writer focuses on over cash management of provident fund benefit. In the

management of cash assurance there are two types of cash receipts and cash

disbursement

35

III.2.3 Cash Receipt Process of provident Fund Benefit

1. The company paid provident fund benefit dues to the PT. Jamsotek through

Mandiri bank accounts

2. Jamsotek get reports of Mandiri bank that is bank statement

3. Finance Department verification the data

4. The finance department doing reconciliation to checking the company records

and bank statement and then the finance department will print the voucher

receipt.

5. Finance department record the transaction the cash receipt accordance with the

company's depositor and make the receipt of cash receipt

6. receipt to be approve by head of finance department

Figure 3.2 Cash Receipt Flow Chart

36

7. Receipts and bank statements given the marketing department. after that the

marketing department will reconcile the amount of money being transferred and

the number of participant provident fund benefit

8. The receipt approved by head of marketing department

9. After the reconciliation, the receipt will be sent to the payer company.

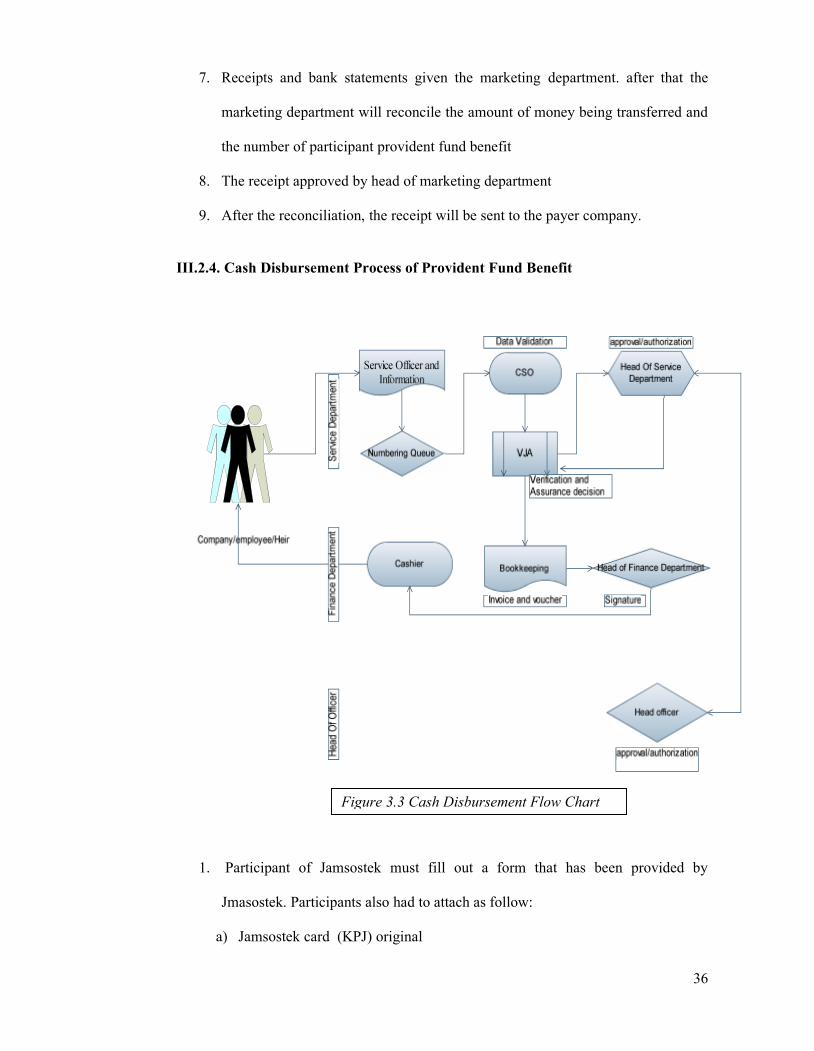

III.2.4. Cash Disbursement Process of Provident Fund Benefit

1. Participant of Jamsostek must fill out a form that has been provided by

Jmasostek. Participants also had to attach as follow:

a) Jamsostek card (KPJ) original

Figure 3.3 Cash Disbursement Flow Chart

Flowchart c

37

b) Self identity card identity card / driving license (photocopy)

c) Industrial A letter from the company stops working or the Industrial Relations

Court Decision

d) Waiver of stamp duty has not worked in moderation

e) Family Card (KK)

2. Jamsostek participant meet with service officer and information to ensure the

document claim is complete. Then the service officer will give a sign for data

completed.

3. Participant take a queue number for programs such as provident fund benefit,

assurance of death, accident insurance, and health insurance

4. Participants meet with customer service officer for validation data, ensuring that

the participants who make the claim is the right person, and participant filling

such security questions like give the mother's name, father's name, date of birth,

children's names, etc.

5. Next, document transfer to the verification guarantee. Jamsostek officers will

determine the guarantee determination, coordination with marketing to ensure

the data of participants, and organize files using the FIFO method

6. The document have to get approval from Head of Service Department

7. More than Rp 15,000,000 the document should be approve by Head of Officer

8. Files will be taken to the finance department to ensure approval has been done,

and make the receipt and vouchers for cash disbursement

9. Head of finance department will check again the document and give approval for

the cash disbursement

10. last participant data, receipts, and vouchers given to the cashier to be paid by

check, transfer to participant bank account, and cash

38

Cash Management provident fund benefit cash receipt start from collecting dues

from all participants every month. All the dues payment is done via bank account as an

internal control in the company and be sure to avoid fraud. After that the company will

receive the bank statement of data payments, next is verification the document for

ensure the document is valid, next bookkeeping according company name and data of

employees this is for the standard procedure from Jamsostek to keep the security of

process cash receipt, and all data will be reconciliation in marketing with a list of staff

salaries and the company reported this is for match all the participants and the amount

of money transferred and this is to avoid the errors.

For the cash disbursement the participant of provident fund benefit starts from

the participant fill the document for provident fund benefit, for the security data of

participant who want to claim is very important the data participants is must be clearly.

Next is the document must be verified in verification assurance, this is to ensure the

document is clear and the receiver of the assurance is the right person. Approval of head

of service department and head of office is needed for the authorization. After that

finance department will recheck all the documents, make the receipt and voucher as

evidence of payment assurance provident fund benefit, and head of finance department

will give approval for all document. The last is cashier will transfer, making check, or

give cash the money based on the amount and data of the receiver

In the planning process of cash receipt and cash disbursement Jamsostek have a plan

called the Work Plan and Budget (RKAP). Jamsostek Center will be providing the

budget for cash receipt and cash out of Jamsostek Cikarang branch. And from the

amount 6 months budget will be divided to be every month. Jamsostek is a service

39

company, so for cash disbursement each month will be different depending on the

participants. No limit for amount claim and the number of participants also made each

month could change. For this problem Jamsostek have the funds and plan to organize

over budget for cash disbursement

In the process of setting up the system of cash receipt and cash disbursement, Jamsostek

has a system has controls RKAP that is Key Performance Indicators (KPI) as have been

mentioned in Jamsostek quality objectives such as;

Quality Objectives

a. The organization in implementing the quality management system has set a goal

of quality in every field in the form of Key Performance Indicator (KPI) that

refers to the strategic goals of the company’s current year

b. Quality objectives have been established, periodically monitored every month

and periodically evaluated every 3 months

Key Performance Indicator serves to organize and maintain all cash management

processes in Jamsotek to achieve company goals.

40

CHAPTER IV

ANALYSIS AND EVALUATION

Based on the existing condition in the company, the writer found some best

practices and findings. The best practices are the conditions show that the company has

implemented internal control properly. Meanwhile the findings are the conditions show

that there are some weaknesses in internal control implementation that have possibility

to create problem. The best practices and findings will be explained as follows

IV.1. Strength Findings

IV.1.1. Control Environment

1. Organizational structures that separate functional responsibilities clearly

No Question Yes No N/A Note

1 Is the organization of the company clearly

defined in terms of lines of authority and

responsibility?

8 2

.

PT. Jamsostek has a written organizational structure, PT. Jamsostek has an

functionally classified organization structure. In over cash management division is

divided by same function and activities to do something in the company and finance

department the main of the cash management process. For the process of cash

management the related divisions are service department, finance department, and

marketing department. Service department is for receive the document of assurance

claim, finance department is for manage, bookkeeping, make voucher and receipt,

reconciliation, etc. and marketing division is for reconciliation to match the amount in

41

bank statement and the data of Jamsostek participant. PT. Jamsostek clearly arranges

the department based on the functioning of the department for the company

operational.

2. PT. Jamsostek clearly defined the authority and responsibility for each

employee

PT. Jamsostek has a written job description. They also described the job

description to each employee. Authority procedure explains clearly for each employee

according to their position. In cash management, the authority of cash out process need

approval from the head office, head of finance department and head of service

department, if the finance department or other not give approval so the process of cash

disbursement will be canceled. Each division also can not interfere in the other division

job, such as customer service officer cannot do the finance department job such as

bookkeeping, consolidation, etc. So each person has only one job just so they can be

responsible with their job.

3. PT. Jamsostek has their own control system the name is “Key Performance

Indicator”

No Question Yes No N/A Note

1 Are employee job responsibilities, including

specific duties, reporting relationships, and

constraints clearly established and communicated

to employees?

9 1

42

PT. Jamsostek has a system to control the employee performance every day

through the system is “key performance indicators”. The key performance indicator

system to evaluation the daily works for every employee. Every 3 month Jamsostek

Cikarang branch make reporting from the Key Performance system evaluation and then

every 6 months the Jamsostek head office will evaluate the report every employees in

branch office. For the best employee in branch office will get reward from Jamsotek

head office. This is a good system to motivate the employee and it will make

employees give their best performance and not careless in carrying out their duties

because of those who do not work well will get warning.

IV.1.2. Control Activity

1. PT. Jamsostek has a standard procedure for claims provident fund benefit

The standard procedure of PT. Jamsostek, all participants who want to claim

assurance of provident fund benefit have to the document standard assurance claim

such as:

f) Jamsostek card (KPJ) original

g) Self identity card identity card / driving license (photocopy)

h) Industrial A letter from the company stops working or the Industrial Relations Court

Decision

i) Waiver of stamp duty has not worked in moderation

j) Family Card (KK)

43

This requirement to maintain security of cash disbursement, so there is no fault

in the payment assurance process. Documentation is required as evidence of payment

to the Jamsostek participant assurance.

The functions of the procedure are to reduce errors and fraud. Every cash provident

fund benefit that should be given to the right person. Because the saving money of

prudent fund benefit is the right of the employee who work. If PT. Jamsostek make

mistaken in the insurance payment it will be make a big problem for Jamsostek

participant satisfaction and a value for the quality company. So to reduce any the risk

and added the value Jamsostek made standard procedure for data completeness for the

retirement decision.

2. PT. Jamsostek has a data verification system

No Question Yes No N/A Note

1 Is Jamsostek has a system of verification data? 10

2 Is there a special person assigned to do the data

verification?

10

According to the results from the questionnaire and each process of cash receipt and

cash disbursement PT. Jamsostek use data verification system. In the process of

verification of cash receipt is to make sure the documents is valid. Data verification

system function is to double check files of participants to avoid mistakes. In the over

cash management verification system use to cash out and cash in. Cash disbursement

verification is needed to ensure the document is completed data is valid and for the cash

receipt is needed for checking the bank statement.

44

3. PT. Jamsostek has a reconciliation procedure in cash receipt process

No Question Yes No N/A Note

1 Is PT. Jamsostek has reconciliation system

for cash receipt?

10

2 Is bank reconciliation prepared by someone

independent of the cash receiving, processing,

and recording activities?

10

Reconciliation is the process for match the company calculation and bank

statement. In Jamsostek reconciliation system consists for two processes first is bank

statements reconciliation and reconciliation of the amount has been transferred from the

company and the employee salary data.

Reconciliation is one of control to control the performance of the company.

Reconciliation function is to find out the causes of the difference between companies

calculation with bank statements. After that, if the is differences the company must

prepare reconciliation report so that the differences can be resolved as soon as possible.

4. The company has a good authorization in over cash management

process

No Question Yes No N/A Note

1 Is there a written rule for approval for

receipt and cash disbursement?

10

45

In the process of assurance claim, PT. Jamsostek has rules of assurance payment as

follow:

a. For the amount of claim insurance less than Rp 15,000,0000 the document will

be approved by head of service department and finance department.

b. For the assurance claim more than Rp 15,000,000 the documents will be

approved by the head of service department, the head of finance division and

head of office

For the authorized the cash disbursement has a security program and the people who

give the authorization is the trusted people. With using authorization system for cash

disbursement is to control for the security cash management.

5. PT. Jamsostek use the International organization standardization (ISO)

PT. Jamsostek use ISO 2001-2008 system as a control to running the company. ISO

is an international standard for quality management systems of the company. Because

of the ISO systems all the activity in Jamsostek more organized than before. All

activity must be documented and registered in the system to avoid fraud. With use the

ISO system it means the standardization of the management system in PT. Jamsostek

has been using the international standards.

IV.2. Findings

1. There are several employees of the company who become brokers to

help participant to process their claim

Based on confirmation from participants and observation in the field work, there are

employee in PT. Jamsostek who become broker. In the process of claim assurance the

process takes time. Firstly the participant takes the number of queue and wait to process

46

the data with account officer, this process claim assurance takes 4-5 hours therefore

some participant are not patient enough to wait, then employees the this opportunity to

become brokers to help the participant to process their claim faster without queue.

All participant should be treated equally and professionally. Should provide the best

service to its participants. Therefore there should be no brokers practice in the process

of claim.

This problem occurs because the process of claim assurance is too long and the

participant have to waiting minimal 4 hours because the amount of customer is too

much and the service officers only 4 person, so the participant try to ask for help of

employees to make the process as return the employee will receive certain amount of

money

The effect from the brokers is will make queuing not organized and make the

participant who come first waiting longer because the participant who use brokers do

not follow the queue number. Broker is also creating bad culture and will bring bad

effects to the quality and value of PT. Jamsotek.

The writer suggests that is the head of service department should make role for all

employees who to be a broker service will given a punishment so the employees not do

it again and the counter of customer service officer be added to make the process faster

to make the participant do not wait too long.

47

2. Lack of counter cashier in provident fund benefit payment

From the results of the observation the writer have done in payment of assurance it

was found that there is lack number of cashier counters.the number of participant is

more or less than 120 per day, the average time of payment process is around 5 minutes

per participant.

The company should serve its participants conventionally. The process of claim

should be fast

The cause of this problem is the lack of space and lack of employee of Jamsostek.

At the beginning PT. Jamsostek Cikarang branch is class 3 office so that the building

provided by the head office is not large, In 2010 the office turned into a class 1 office