evine investor presentation sept 2016

TRANSCRIPT

Investor PresentationSeptember 2016

2

This document may contain certain “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Such statements

may be identified by words such as anticipate, believe, estimate, expect, intend, predict, hope, should, plan, will or similar expressions. Any statements

contained herein that are not statements of historical fact may be deemed forward-looking statements. These statements are based on management's current

expectations and accordingly are subject to uncertainty and changes in circumstances. Actual results may vary materially from the expectations contained

herein due to various important factors, including (but not limited to): consumer preferences, spending and debt levels; the general economic and credit

environment; interest rates; seasonal variations in consumer purchasing activities; the ability to achieve the most effective product category mixes to

maximize sales and margin objectives; competitive pressures on sales; pricing and gross sales margins; the level of cable and satellite distribution for our

programming and the associated fees; our ability to establish and maintain acceptable commercial terms with third-party vendors and other third parties with

whom we have contractual relationships, and to successfully manage key vendor relationships and develop key partnerships and proprietary brands; our

ability to manage our operating expenses successfully and our working capital levels; our ability to remain compliant with our credit facilities covenants; our

ability to successfully transition our brand name and corporate name; customer acceptance of our new branding strategy and our repositioning as a digital

commerce company; the market demand for television station sales; changes to our management and information systems infrastructure; challenges to our

data and information security; changes in governmental or regulatory requirements; litigation or governmental proceedings affecting our operations;

significant public events that are difficult to predict, or other significant television-covering events causing an interruption of television coverage or that directly

compete with the viewership of our programming; our ability to obtain and retain key executives and employees; our ability to attract new customers and

retain existing customers; changes in shipping costs; our ability to offer new or innovative products and customer acceptance of the same; changes in

customers viewing habits of television programming; and the risks identified under “Risk Factors” in our recently filed Form 10-K and any additional risk

factors identified in our periodic reports since the date of such Form 10-K. More detailed information about those factors is set forth in our filings with the

Securities and Exchange Commission, including our annual report on Form 10-K, quarterly reports on Form 10-Q, and current reports on Form 8-K. You are

cautioned not to place undue reliance on forward-looking statements, which speak only as of the date of this announcement. We are under no obligation (and

expressly disclaim any such obligation) to update or alter our forward-looking statements whether as a result of new information, future events or otherwise.

Adjusted EBITDA

EBITDA represents net income (loss) for the respective periods excluding depreciation and amortization expense, interest income (expense) and income

taxes. We define Adjusted EBITDA as EBITDA excluding non-operating gains (losses); activist shareholder response costs; executive and management

transition costs; distribution center consolidation and technology upgrade costs; Shareholder Rights Plan costs and non-cash share-based compensation

expense. We have included the term “Adjusted EBITDA” in our EBITDA reconciliation in order to adequately assess the operating performance of our

television and online businesses and in order to maintain comparability to our analyst's coverage and financial guidance, when given. Management believes

that the term Adjusted EBITDA allows investors to make a more meaningful comparison between our business operating results over different periods of time

with those of other similar companies. In addition, management uses Adjusted EBITDA as a metric to evaluate operating performance under our

management and executive incentive compensation programs. Adjusted EBITDA should not be construed as an alternative to operating income (loss), net

income (loss) or to cash flows from operating activities as determined in accordance with generally accepted accounting principles and should not be

construed as a measure of liquidity. Adjusted EBITDA may not be comparable to similarly entitled measures reported by other companies. We have included

a reconciliation of Adjusted EBITDA to net income (loss), the most directly comparable GAAP financial measure, on Slide 12 of this presentation.

Data in this presentation may be unaudited.

Percentage changes represent Q2 2016 as compared to Q2 2015.

Safe Harbor Statement

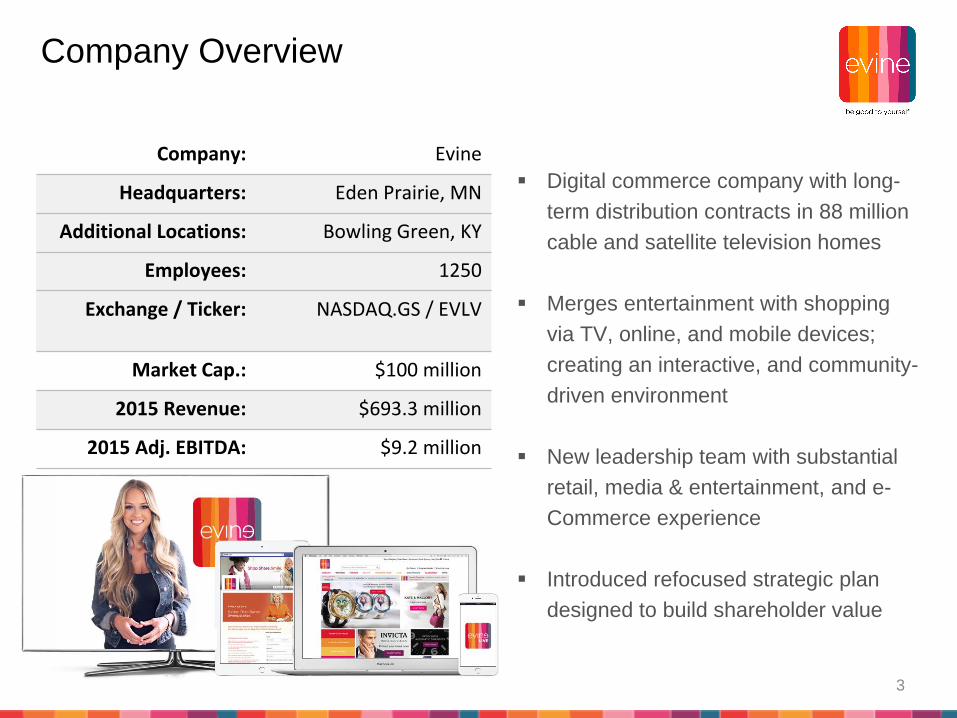

Company: Evine

Headquarters: Eden Prairie, MN

Additional Locations: Bowling Green, KY

Employees: 1250

Exchange / Ticker: NASDAQ.GS / EVLV

Market Cap.: $100 million

2015 Revenue: $693.3 million

2015 Adj. EBITDA: $9.2 million

Digital commerce company with long-

term distribution contracts in 88 million

cable and satellite television homes

Merges entertainment with shopping

via TV, online, and mobile devices;

creating an interactive, and community-

driven environment

New leadership team with substantial

retail, media & entertainment, and e-

Commerce experience

Introduced refocused strategic plan

designed to build shareholder value

3

Company Overview

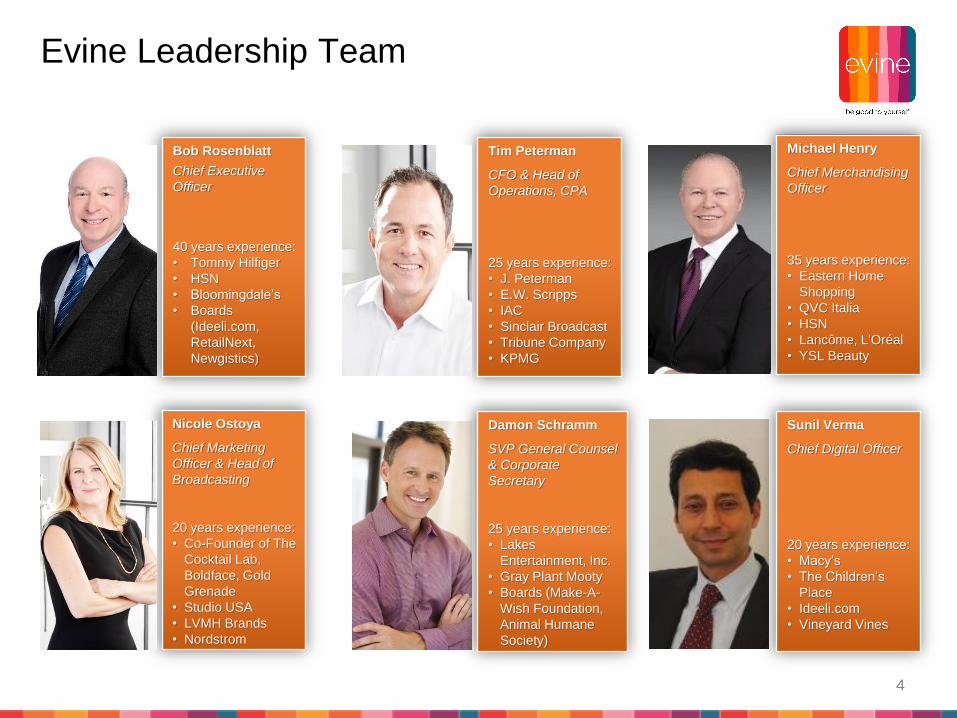

Bob Rosenblatt

Chief Executive

Officer

40 years experience:

• Tommy Hilfiger

• HSN

• Bloomingdale’s

• Boards

(Ideeli.com,

RetailNext,

Newgistics)

Tim Peterman

CFO & Head of

Operations, CPA

25 years experience:

• J. Peterman

• E.W. Scripps

• IAC

• Sinclair Broadcast

• Tribune Company

• KPMG

Nicole Ostoya

Chief Marketing

Officer & Head of

Broadcasting

20 years experience:

• Co-Founder of The

Cocktail Lab,

Boldface, Gold

Grenade

• Studio USA

• LVMH Brands

• Nordstrom

Damon Schramm

SVP General Counsel

& Corporate

Secretary

25 years experience:

• Lakes

Entertainment, Inc.

• Gray Plant Mooty

• Boards (Make-A-

Wish Foundation,

Animal Humane

Society)

Michael Henry

Chief Merchandising

Officer

35 years experience:

• Eastern Home

Shopping

• QVC Italia

• HSN

• Lancôme, L'Oréal

• YSL Beauty

Sunil Verma

Chief Digital Officer

20 years experience:

• Macy’s

• The Children’s

Place

• Ideeli.com

• Vineyard Vines

4

Evine Leadership Team

Evine is part of a 3 member oligopoly generating $9.5B in annual U.S. revenues*

Strategic focus on contribution margin and profitability beginning to yield results

Emerging Brands gaining traction and acceptance from market place

Established Brands continuing to provide stable cash flows and financial impact

Improved Distribution through Bowling Green Facility with new WMS system

Utilizing new technologies in mobile and logistics to drive better connectivity between

internet, TV, and mobile platforms

Future Expansion of TV Properties to improve customer penetration

New Management Team Additions – Chief Executive, Chief Marketing, Chief

Merchandising, and Chief Digital Officers

*$9.5 billion in US revenue for QVCUS, HSN (excluding Cornerstone), and Evine.5

Investment Highlights

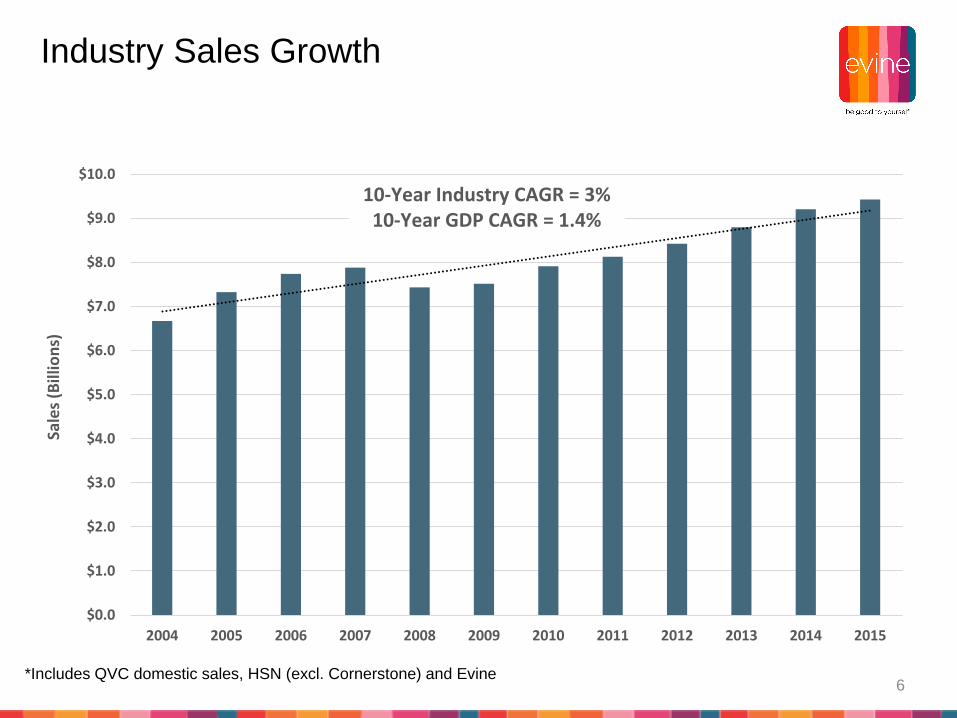

*Includes QVC domestic sales, HSN (excl. Cornerstone) and Evine

$0.0

$1.0

$2.0

$3.0

$4.0

$5.0

$6.0

$7.0

$8.0

$9.0

$10.0

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Sale

s (B

illio

ns)

10-Year Industry CAGR = 3%10-Year GDP CAGR = 1.4%

6

Industry Sales Growth

Driving Long Term Sustainable Growth

and Profitability

Strengthen Internal Culture

Drive Innovation & Efficiency

Grow Customer Base

Improve Quality of Merchandise

Drive Profitability

7

2016 Strategic Plan –

Focused on Profitable Growth

+52%Bob

Rosenblatt

named

Permanent

CEO

Improvement in

Adjusted

EBITDAImprovement

in Earnings

per Share

+40%

*Percentage changes represent Q2 2016 as compared to Q2 2015.

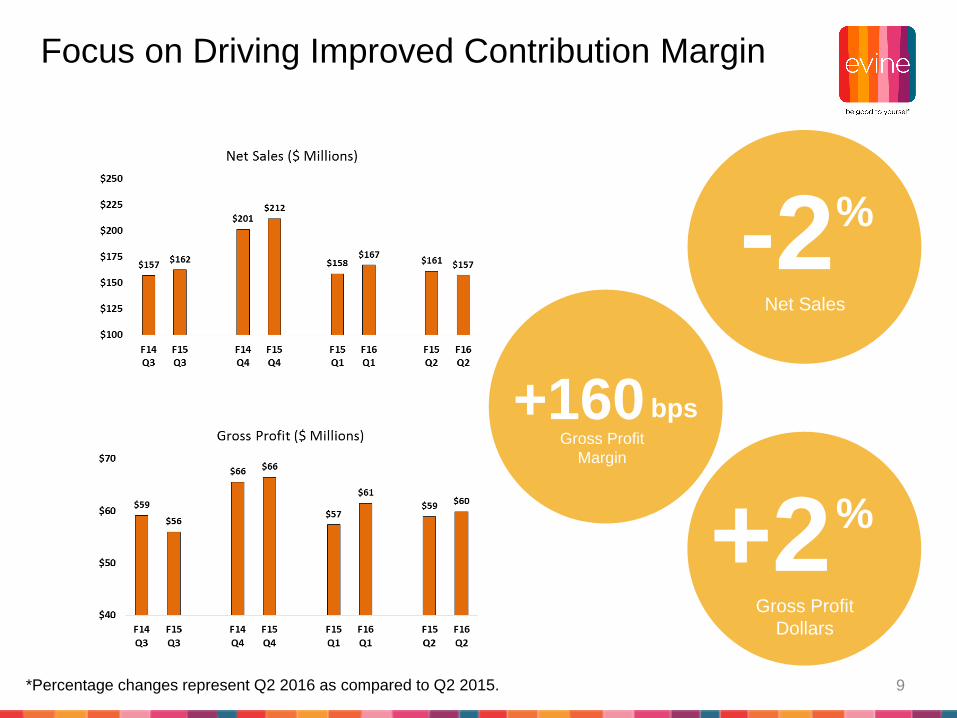

-2%Net Sales

GrowthGross Profit

Margin

+160 bps

Increase in

Total Cash

+150%

8

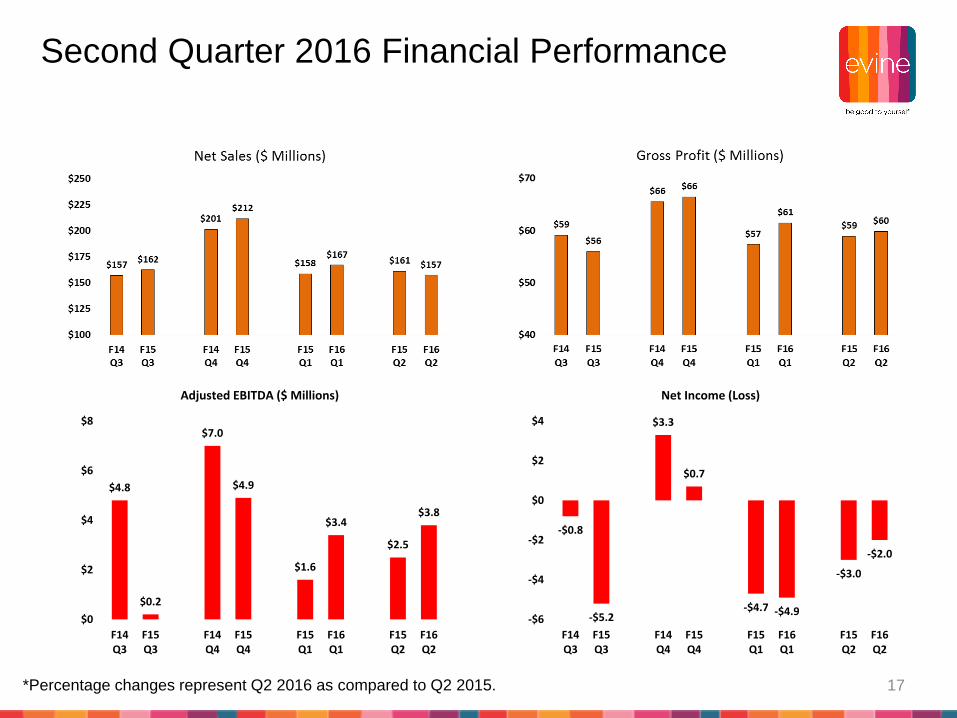

Second Quarter 2016 Highlights

Net Sales

%-2

Gross Profit

Dollars

%+2

-2%Net Sales

GrowthGross Profit

Margin

+160 bps

*Percentage changes represent Q2 2016 as compared to Q2 2015. 9

Focus on Driving Improved Contribution Margin

10

Brands with a Plan

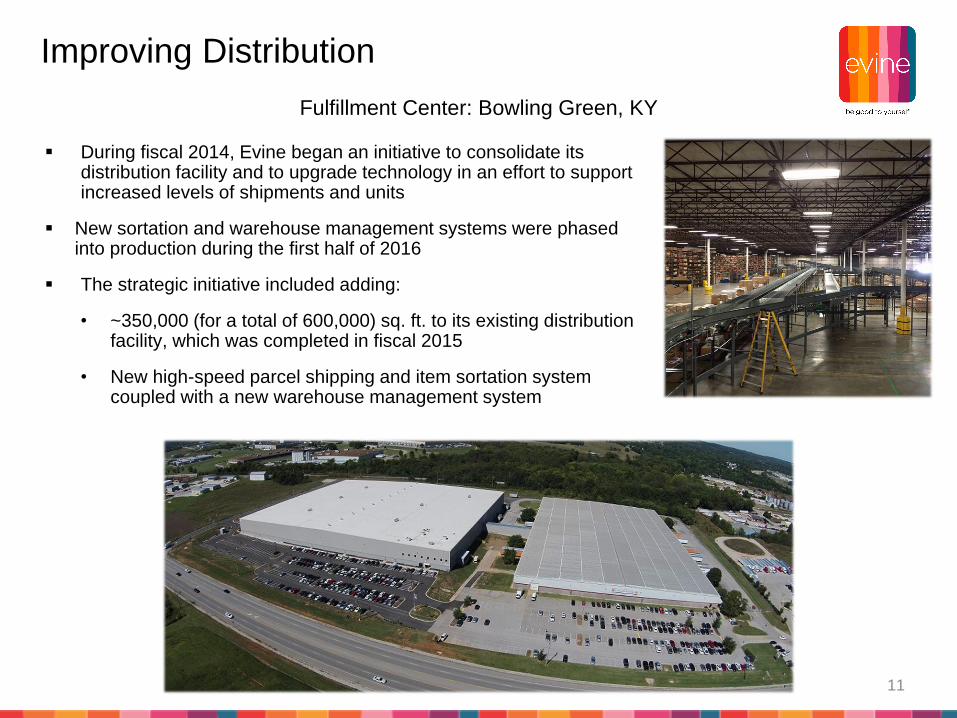

During fiscal 2014, Evine began an initiative to consolidate its distribution facility and to upgrade technology in an effort to support increased levels of shipments and units

New sortation and warehouse management systems were phased into production during the first half of 2016

The strategic initiative included adding:

• ~350,000 (for a total of 600,000) sq. ft. to its existing distribution facility, which was completed in fiscal 2015

• New high-speed parcel shipping and item sortation system coupled with a new warehouse management system

Fulfillment Center: Bowling Green, KY

11

Improving Distribution

-160bps

Return RatePurchase

Frequency

4.51%Increase Net

Shipped Units

*Percentage changes represent Q2 2016 as compared to Q2 2015. 12

Improving Customer Experience

13

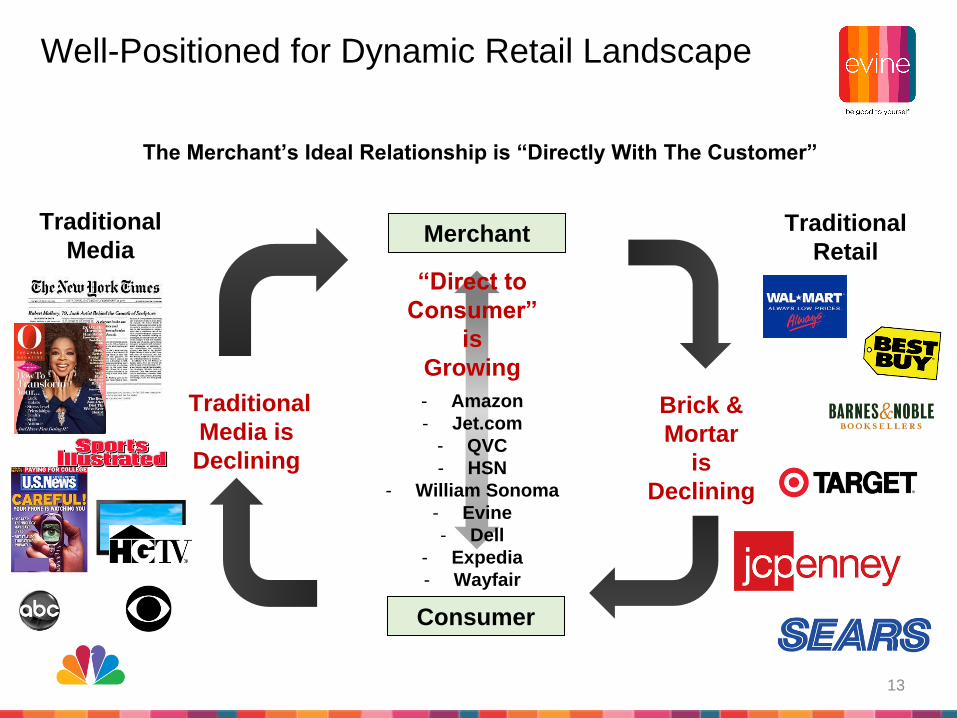

Well-Positioned for Dynamic Retail Landscape

The Merchant’s Ideal Relationship is “Directly With The Customer”

Merchant

Traditional

Media is

Declining

Brick &

Mortar

is

Declining

Consumer

“Direct to

Consumer”

is

Growing

- Amazon

- Jet.com

- QVC

- HSN

- William Sonoma

- Evine

- Dell

- Expedia

- Wayfair

Traditional

MediaTraditional

Retail

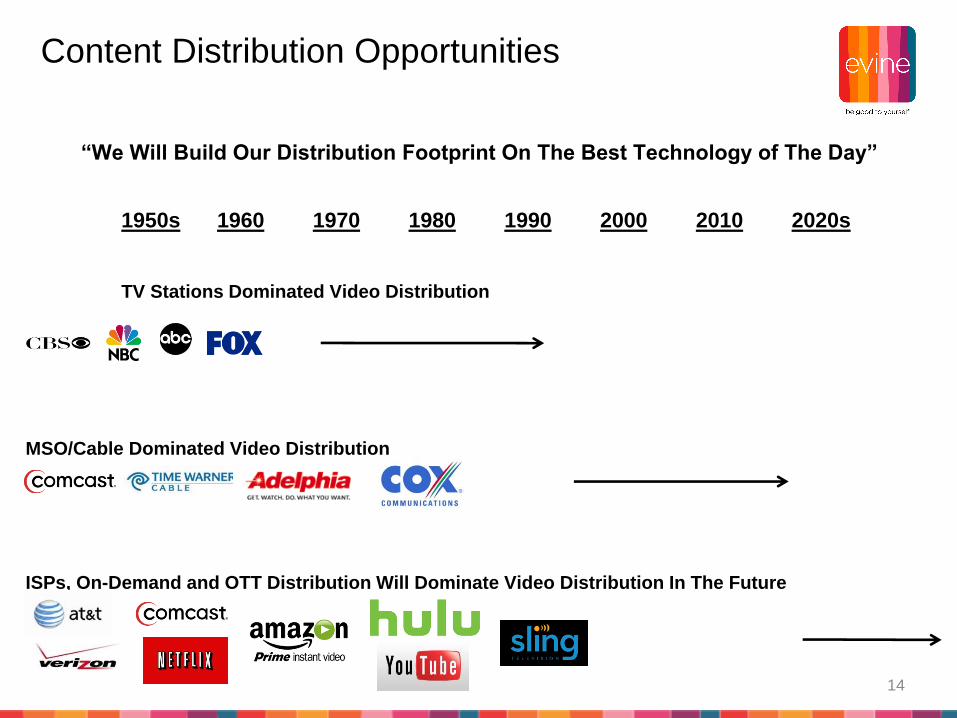

1950s 1960 1970 1980 1990 2000 2010 2020s

TV Stations Dominated Video Distribution

MSO/Cable Dominated Video Distribution

ISPs, On-Demand and OTT Distribution Will Dominate Video Distribution In The Future

“We Will Build Our Distribution Footprint On The Best Technology of The Day”

14

Content Distribution Opportunities

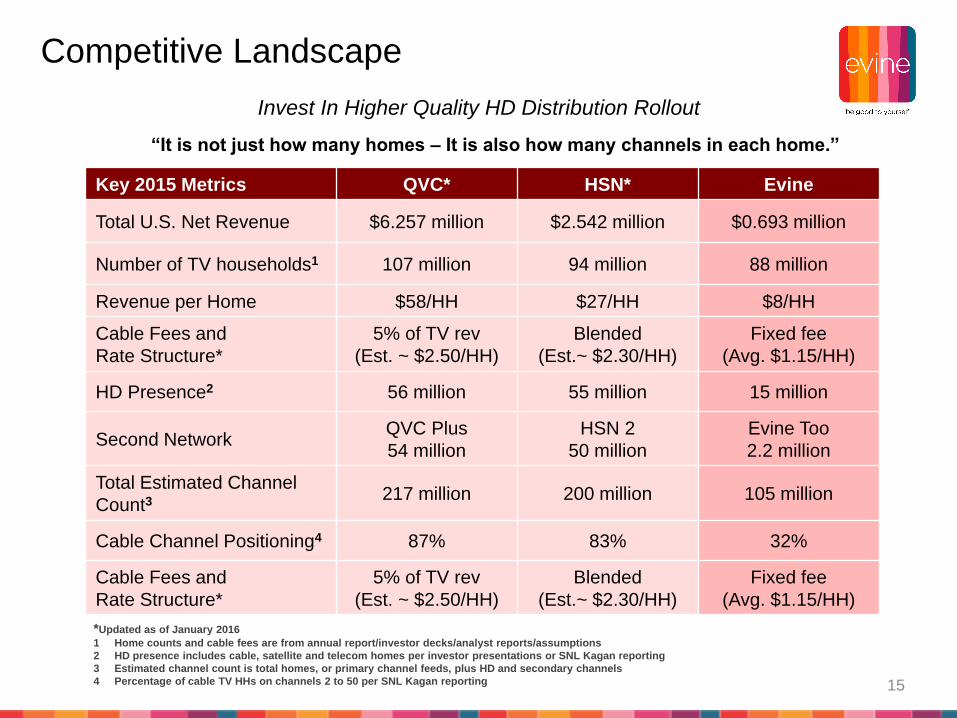

“It is not just how many homes – It is also how many channels in each home.”

Invest In Higher Quality HD Distribution Rollout

Key 2015 Metrics QVC* HSN* Evine

Total U.S. Net Revenue $6.257 million $2.542 million $0.693 million

Number of TV households1 107 million 94 million 88 million

Revenue per Home $58/HH $27/HH $8/HH

Cable Fees and

Rate Structure*

5% of TV rev

(Est. ~ $2.50/HH)

Blended

(Est.~ $2.30/HH)

Fixed fee

(Avg. $1.15/HH)

HD Presence2 56 million 55 million 15 million

Second NetworkQVC Plus

54 million

HSN 2

50 million

Evine Too

2.2 million

Total Estimated Channel

Count3217 million 200 million 105 million

Cable Channel Positioning4 87% 83% 32%

Cable Fees and

Rate Structure*

5% of TV rev

(Est. ~ $2.50/HH)

Blended

(Est.~ $2.30/HH)

Fixed fee

(Avg. $1.15/HH)

*Updated as of January 2016

1 Home counts and cable fees are from annual report/investor decks/analyst reports/assumptions

2 HD presence includes cable, satellite and telecom homes per investor presentations or SNL Kagan reporting

3 Estimated channel count is total homes, or primary channel feeds, plus HD and secondary channels

4 Percentage of cable TV HHs on channels 2 to 50 per SNL Kagan reporting 15

Competitive Landscape

16

Financials

$4.8

$0.2

$7.0

$4.9

$1.6

$3.4

$2.5

$3.8

$0

$2

$4

$6

$8

F14Q3

F15Q3

F14Q4

F15Q4

F15Q1

F16Q1

F15Q2

F16Q2

Adjusted EBITDA ($ Millions)

-$0.8

-$5.2

$3.3

$0.7

-$4.7 -$4.9

-$3.0

-$2.0

-$6

-$4

-$2

$0

$2

$4

F14Q3

F15Q3

F14Q4

F15Q4

F15Q1

F16Q1

F15Q2

F16Q2

Net Income (Loss)

*Percentage changes represent Q2 2016 as compared to Q2 2015. 17

Second Quarter 2016 Financial Performance

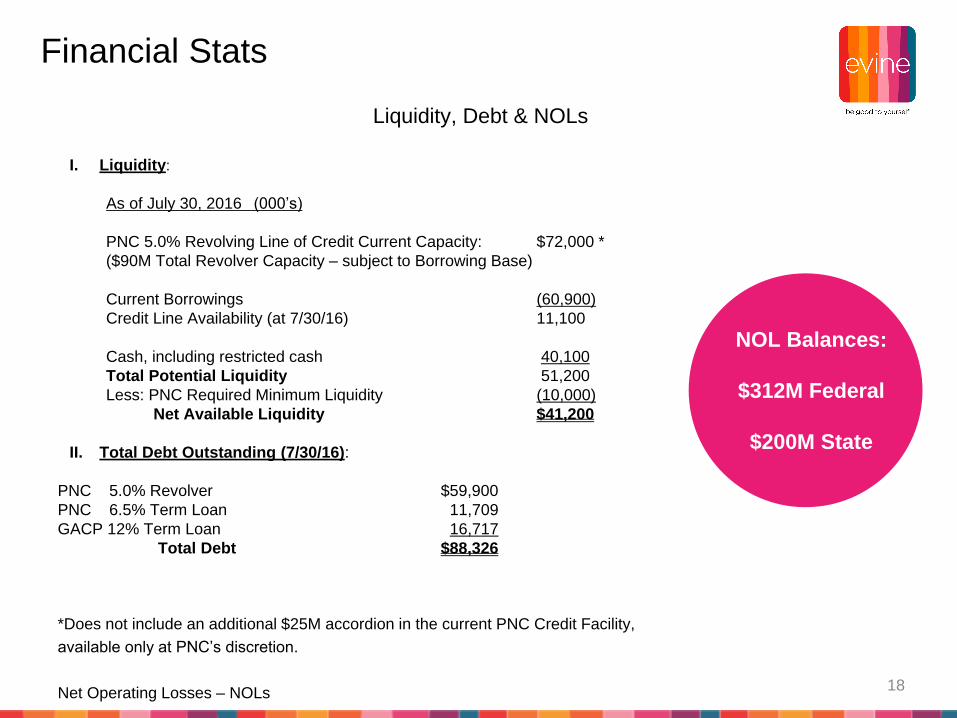

Liquidity, Debt & NOLs

I. Liquidity:

As of July 30, 2016 (000’s)

PNC 5.0% Revolving Line of Credit Current Capacity: $72,000 *

($90M Total Revolver Capacity – subject to Borrowing Base)

Current Borrowings (60,900)

Credit Line Availability (at 7/30/16) 11,100

Cash, including restricted cash 40,100

Total Potential Liquidity 51,200

Less: PNC Required Minimum Liquidity (10,000)

Net Available Liquidity $41,200

II. Total Debt Outstanding (7/30/16):

PNC 5.0% Revolver $59,900

PNC 6.5% Term Loan 11,709

GACP 12% Term Loan 16,717

Total Debt $88,326

*Does not include an additional $25M accordion in the current PNC Credit Facility,

available only at PNC’s discretion.

Net Operating Losses – NOLs

NOL Balances:

$312M Federal

$200M State

18

Financial Stats

19

Appendices

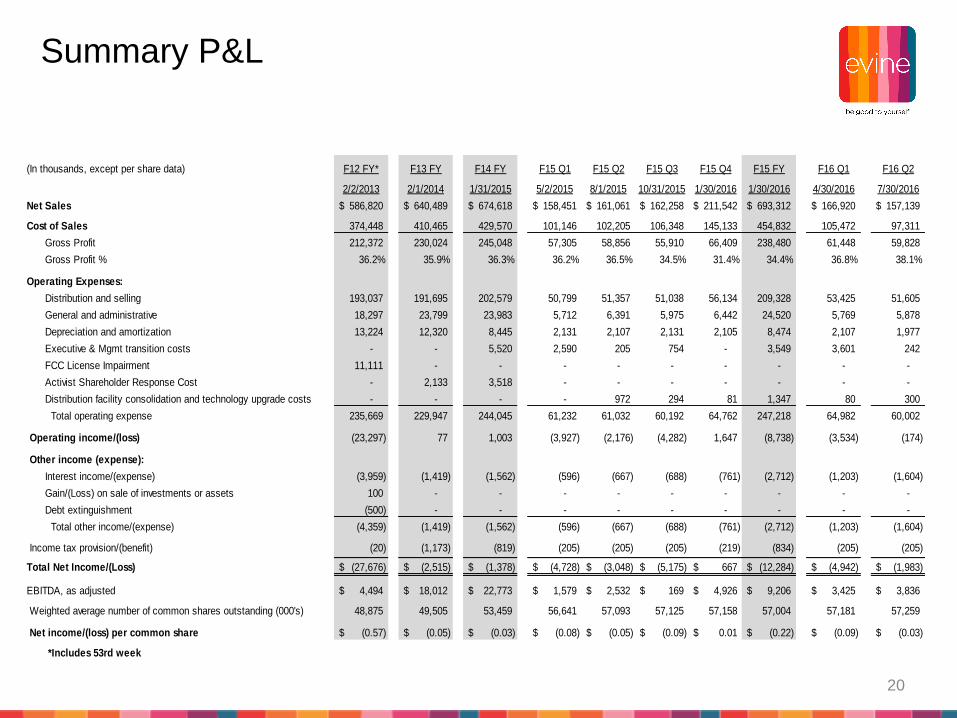

(In thousands, except per share data) F12 FY* F13 FY F14 FY F15 Q1 F15 Q2 F15 Q3 F15 Q4 F15 FY F16 Q1 F16 Q2

2/2/2013 2/1/2014 1/31/2015 5/2/2015 8/1/2015 10/31/2015 1/30/2016 1/30/2016 4/30/2016 7/30/2016

Net Sales 586,820$ 640,489$ 674,618$ 158,451$ 161,061$ 162,258$ 211,542$ 693,312$ 166,920$ 157,139$

Cost of Sales 374,448 410,465 429,570 101,146 102,205 106,348 145,133 454,832 105,472 97,311

Gross Profit 212,372 230,024 245,048 57,305 58,856 55,910 66,409 238,480 61,448 59,828

Gross Profit % 36.2% 35.9% 36.3% 36.2% 36.5% 34.5% 31.4% 34.4% 36.8% 38.1%

Operating Expenses:

Distribution and selling 193,037 191,695 202,579 50,799 51,357 51,038 56,134 209,328 53,425 51,605

General and administrative 18,297 23,799 23,983 5,712 6,391 5,975 6,442 24,520 5,769 5,878

Depreciation and amortization 13,224 12,320 8,445 2,131 2,107 2,131 2,105 8,474 2,107 1,977

Executive & Mgmt transition costs - - 5,520 2,590 205 754 - 3,549 3,601 242

FCC License Impairment 11,111 - - - - - - - - -

Activist Shareholder Response Cost - 2,133 3,518 - - - - - - -

Distribution facility consolidation and technology upgrade costs - - - - 972 294 81 1,347 80 300

Total operating expense 235,669 229,947 244,045 61,232 61,032 60,192 64,762 247,218 64,982 60,002

Operating income/(loss) (23,297) 77 1,003 (3,927) (2,176) (4,282) 1,647 (8,738) (3,534) (174)

Other income (expense):

Interest income/(expense) (3,959) (1,419) (1,562) (596) (667) (688) (761) (2,712) (1,203) (1,604)

Gain/(Loss) on sale of investments or assets 100 - - - - - - - - -

Debt extinguishment (500) - - - - - - - - -

Total other income/(expense) (4,359) (1,419) (1,562) (596) (667) (688) (761) (2,712) (1,203) (1,604)

Income tax provision/(benefit) (20) (1,173) (819) (205) (205) (205) (219) (834) (205) (205)

Total Net Income/(Loss) (27,676)$ (2,515)$ (1,378)$ (4,728)$ (3,048)$ (5,175)$ 667$ (12,284)$ (4,942)$ (1,983)$

EBITDA, as adjusted 4,494$ 18,012$ 22,773$ 1,579$ 2,532$ 169$ 4,926$ 9,206$ 3,425$ 3,836$

Weighted average number of common shares outstanding (000's) 48,875 49,505 53,459 56,641 57,093 57,125 57,158 57,004 57,181 57,259

Net income/(loss) per common share (0.57)$ (0.05)$ (0.03)$ (0.08)$ (0.05)$ (0.09)$ 0.01$ (0.22)$ (0.09)$ (0.03)$

*Includes 53rd week

20

Summary P&L

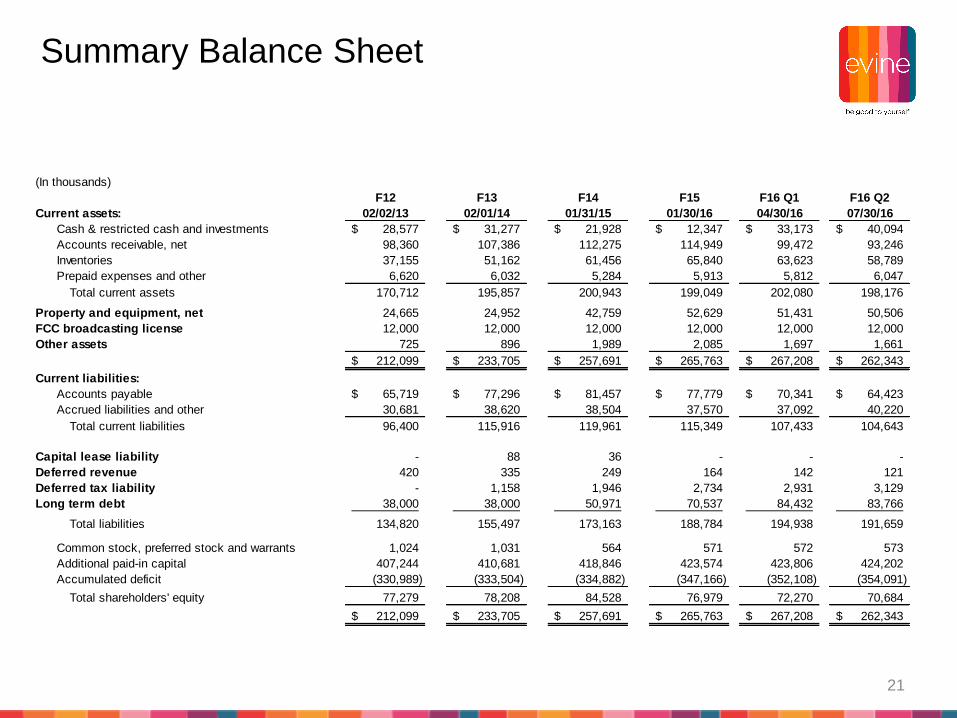

(In thousands)

F12 F13 F14 F15 F16 Q1 F16 Q2

Current assets: 02/02/13 02/01/14 01/31/15 01/30/16 04/30/16 07/30/16

Cash & restricted cash and investments 28,577$ 31,277$ 21,928$ 12,347$ 33,173$ 40,094$

Accounts receivable, net 98,360 107,386 112,275 114,949 99,472 93,246

Inventories 37,155 51,162 61,456 65,840 63,623 58,789

Prepaid expenses and other 6,620 6,032 5,284 5,913 5,812 6,047

Total current assets 170,712 195,857 200,943 199,049 202,080 198,176

Property and equipment, net 24,665 24,952 42,759 52,629 51,431 50,506

FCC broadcasting license 12,000 12,000 12,000 12,000 12,000 12,000

Other assets 725 896 1,989 2,085 1,697 1,661

212,099$ 233,705$ 257,691$ 265,763$ 267,208$ 262,343$

Current liabilities:

Accounts payable 65,719$ 77,296$ 81,457$ 77,779$ 70,341$ 64,423$

Accrued liabilities and other 30,681 38,620 38,504 37,570 37,092 40,220

Total current liabilities 96,400 115,916 119,961 115,349 107,433 104,643

Capital lease liability - 88 36 - - -

Deferred revenue 420 335 249 164 142 121

Deferred tax liability - 1,158 1,946 2,734 2,931 3,129

Long term debt 38,000 38,000 50,971 70,537 84,432 83,766

Total liabilities 134,820 155,497 173,163 188,784 194,938 191,659

Common stock, preferred stock and warrants 1,024 1,031 564 571 572 573

Additional paid-in capital 407,244 410,681 418,846 423,574 423,806 424,202

Accumulated deficit (330,989) (333,504) (334,882) (347,166) (352,108) (354,091)

Total shareholders' equity 77,279 78,208 84,528 76,979 72,270 70,684

212,099$ 233,705$ 257,691$ 265,763$ 267,208$ 262,343$

21

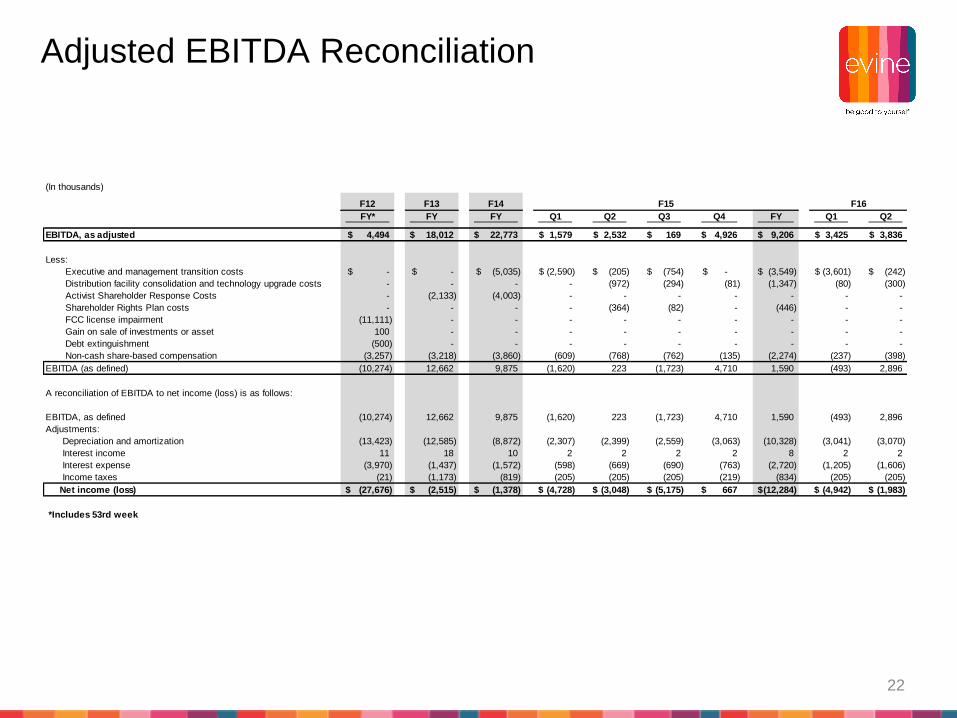

Summary Balance Sheet

(In thousands)

F13 F14

FY* FY FY Q1 Q2 Q3 Q4 FY Q1 Q2

EBITDA, as adjusted 4,494$ 18,012$ 22,773$ 1,579$ 2,532$ 169$ 4,926$ 9,206$ 3,425$ 3,836$

Less:

Executive and management transition costs -$ -$ (5,035)$ (2,590)$ (205)$ (754)$ -$ (3,549)$ (3,601)$ (242)$

Distribution facility consolidation and technology upgrade costs - - - - (972) (294) (81) (1,347) (80) (300)

Activist Shareholder Response Costs - (2,133) (4,003) - - - - - - -

Shareholder Rights Plan costs - - - - (364) (82) - (446) - -

FCC license impairment (11,111) - - - - - - - - -

Gain on sale of investments or asset 100 - - - - - - - - -

Debt extinguishment (500) - - - - - - - - -

Non-cash share-based compensation (3,257) (3,218) (3,860) (609) (768) (762) (135) (2,274) (237) (398)

EBITDA (as defined) (10,274) 12,662 9,875 (1,620) 223 (1,723) 4,710 1,590 (493) 2,896

A reconciliation of EBITDA to net income (loss) is as follows:

EBITDA, as defined (10,274) 12,662 9,875 (1,620) 223 (1,723) 4,710 1,590 (493) 2,896

Adjustments:

Depreciation and amortization (13,423) (12,585) (8,872) (2,307) (2,399) (2,559) (3,063) (10,328) (3,041) (3,070)

Interest income 11 18 10 2 2 2 2 8 2 2

Interest expense (3,970) (1,437) (1,572) (598) (669) (690) (763) (2,720) (1,205) (1,606)

Income taxes (21) (1,173) (819) (205) (205) (205) (219) (834) (205) (205)

Net income (loss) (27,676)$ (2,515)$ (1,378)$ (4,728)$ (3,048)$ (5,175)$ 667$ (12,284)$ (4,942)$ (1,983)$

*Includes 53rd week

F12 F15 F16

22

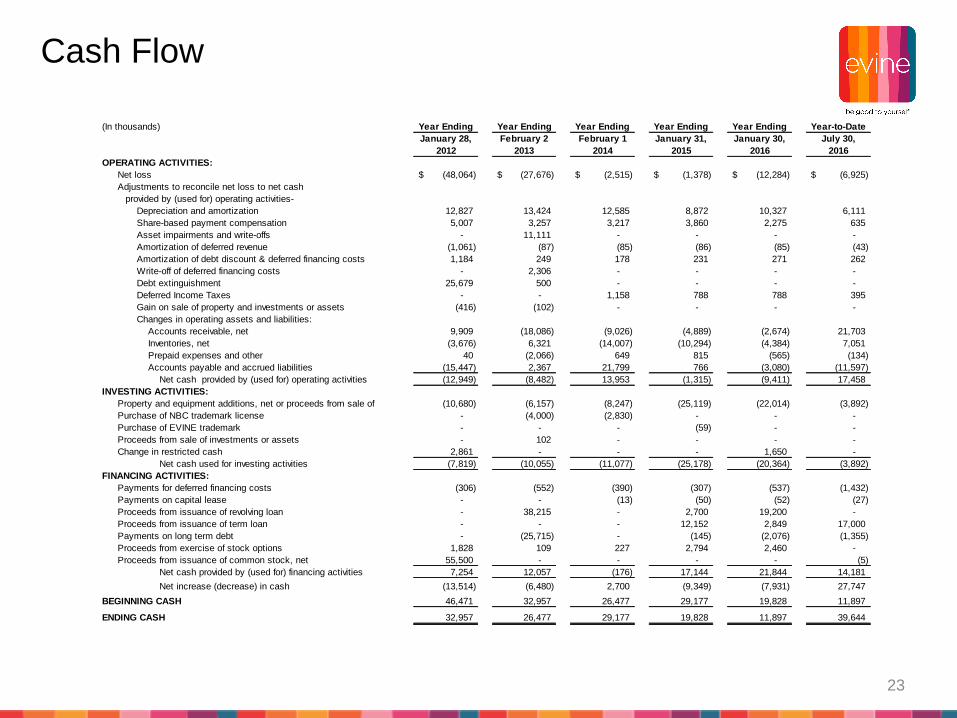

Adjusted EBITDA Reconciliation

(In thousands) Year Ending Year Ending Year Ending Year Ending Year Ending Year-to-Date

January 28, February 2 February 1 January 31, January 30, July 30,

2012 2013 2014 2015 2016 2016

OPERATING ACTIVITIES:

Net loss (48,064)$ (27,676)$ (2,515)$ (1,378)$ (12,284)$ (6,925)$

Adjustments to reconcile net loss to net cash

provided by (used for) operating activities-

Depreciation and amortization 12,827 13,424 12,585 8,872 10,327 6,111

Share-based payment compensation 5,007 3,257 3,217 3,860 2,275 635

Asset impairments and write-offs - 11,111 - - - -

Amortization of deferred revenue (1,061) (87) (85) (86) (85) (43)

Amortization of debt discount & deferred financing costs 1,184 249 178 231 271 262

Write-off of deferred financing costs - 2,306 - - - -

Debt extinguishment 25,679 500 - - - -

Deferred Income Taxes - - 1,158 788 788 395

Gain on sale of property and investments or assets (416) (102) - - - -

Changes in operating assets and liabilities:

Accounts receivable, net 9,909 (18,086) (9,026) (4,889) (2,674) 21,703

Inventories, net (3,676) 6,321 (14,007) (10,294) (4,384) 7,051

Prepaid expenses and other 40 (2,066) 649 815 (565) (134)

Accounts payable and accrued liabilities (15,447) 2,367 21,799 766 (3,080) (11,597)

Net cash provided by (used for) operating activities (12,949) (8,482) 13,953 (1,315) (9,411) 17,458

INVESTING ACTIVITIES:

Property and equipment additions, net or proceeds from sale of (10,680) (6,157) (8,247) (25,119) (22,014) (3,892)

Purchase of NBC trademark license - (4,000) (2,830) - - -

Purchase of EVINE trademark - - - (59) - -

Proceeds from sale of investments or assets - 102 - - - -

Change in restricted cash 2,861 - - - 1,650 -

Net cash used for investing activities (7,819) (10,055) (11,077) (25,178) (20,364) (3,892)

FINANCING ACTIVITIES:

1 Payments for deferred financing costs (306) (552) (390) (307) (537) (1,432)

2 Payments on capital lease - - (13) (50) (52) (27)

3 Proceeds from issuance of revolving loan - 38,215 - 2,700 19,200 -

4 Proceeds from issuance of term loan - - - 12,152 2,849 17,000

5 Payments on long term debt - (25,715) - (145) (2,076) (1,355)

6 Proceeds from exercise of stock options 1,828 109 227 2,794 2,460 -

7 Proceeds from issuance of common stock, net 55,500 - - - - (5)

Net cash provided by (used for) financing activities 7,254 12,057 (176) 17,144 21,844 14,181

Net increase (decrease) in cash (13,514) (6,480) 2,700 (9,349) (7,931) 27,747

BEGINNING CASH 46,471 32,957 26,477 29,177 19,828 11,897

ENDING CASH 32,957 26,477 29,177 19,828 11,897 39,644

23

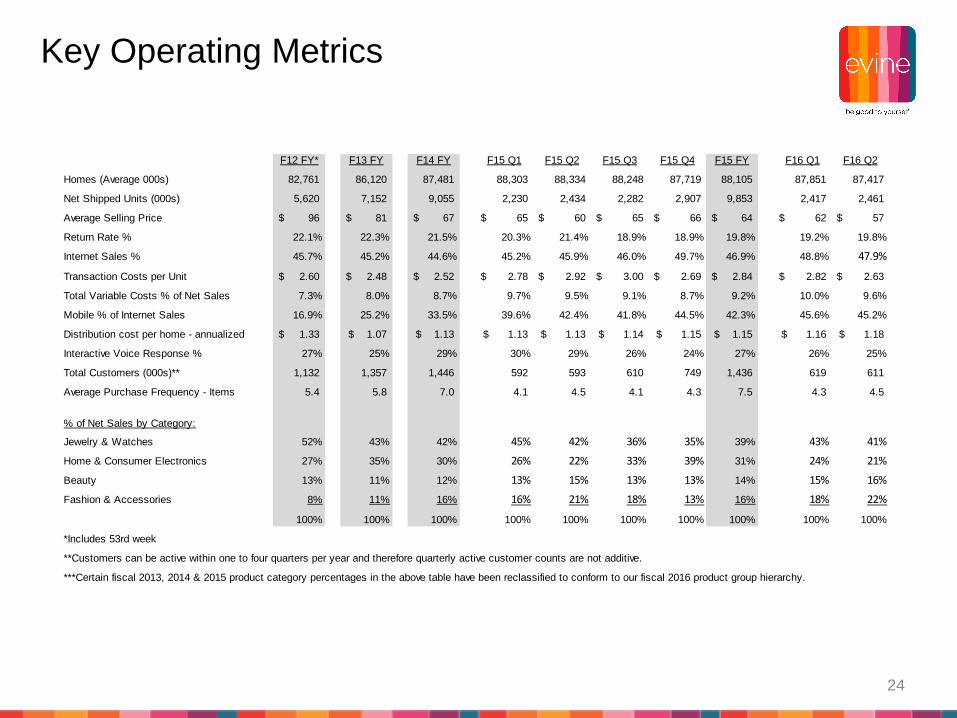

Cash Flow

F12 FY* F13 FY F14 FY F15 Q1 F15 Q2 F15 Q3 F15 Q4 F15 FY F16 Q1 F16 Q2

Homes (Average 000s) 82,761 86,120 87,481 88,303 88,334 88,248 87,719 88,105 87,851 87,417

Net Shipped Units (000s) 5,620 7,152 9,055 2,230 2,434 2,282 2,907 9,853 2,417 2,461

Average Selling Price 96$ 81$ 67$ 65$ 60$ 65$ 66$ 64$ 62$ 57$

Return Rate % 22.1% 22.3% 21.5% 20.3% 21.4% 18.9% 18.9% 19.8% 19.2% 19.8%

Internet Sales % 45.7% 45.2% 44.6% 45.2% 45.9% 46.0% 49.7% 46.9% 48.8% 47.9%

Transaction Costs per Unit 2.60$ 2.48$ 2.52$ 2.78$ 2.92$ 3.00$ 2.69$ 2.84$ 2.82$ 2.63$

Total Variable Costs % of Net Sales 7.3% 8.0% 8.7% 9.7% 9.5% 9.1% 8.7% 9.2% 10.0% 9.6%

Mobile % of Internet Sales 16.9% 25.2% 33.5% 39.6% 42.4% 41.8% 44.5% 42.3% 45.6% 45.2%

Distribution cost per home - annualized 1.33$ 1.07$ 1.13$ 1.13$ 1.13$ 1.14$ 1.15$ 1.15$ 1.16$ 1.18$

Interactive Voice Response % 27% 25% 29% 30% 29% 26% 24% 27% 26% 25%

Total Customers (000s)** 1,132 1,357 1,446 592 593 610 749 1,436 619 611

Average Purchase Frequency - Items 5.4 5.8 7.0 4.1 4.5 4.1 4.3 7.5 4.3 4.5

% of Net Sales by Category:

Jewelry & Watches 52% 43% 42% 45% 42% 36% 35% 39% 43% 41%

Home & Consumer Electronics 27% 35% 30% 26% 22% 33% 39% 31% 24% 21%

Beauty 13% 11% 12% 13% 15% 13% 13% 14% 15% 16%

Fashion & Accessories 8% 11% 16% 16% 21% 18% 13% 16% 18% 22%

100% 100% 100% 100% 100% 100% 100% 100% 100% 100%

*Includes 53rd week

**Customers can be active within one to four quarters per year and therefore quarterly active customer counts are not additive.

***Certain fiscal 2013, 2014 & 2015 product category percentages in the above table have been reclassified to conform to our fiscal 2016 product group hierarchy.

24

Key Operating Metrics

25

26

27

28