evolving opportunities and constraints in...

TRANSCRIPT

Evolving Opportunities and Constraints in Remittances: A View from SADC

London November 2006

Background / Context

• Genesis Analytics: Johannesburg based economics consultancy, with a wide range of experience in access to finance, including the remittance market

• Completed several studies on remittances in the SADC region

• Clients

• Donors

• Private banks

• Airtime distributors

Focus / Outline

• Research / presentation focused on:

• Who (sends and receives)?

• How (why)?

• How much?

• Innovation

• Constraints?

The intra-SADC remittance market

Patterns of migration in SADC

• South Africa is the principal destination country

• Principal emigration countries: Mozambique, Lesotho and Zimbabwe (the bulk of other SADC)

• Official data on migration is limited – captures flows, not stocks, and no estimates of undocumented

2.1 million total cross-border SADC migrants / 6 million domestic remitters

Other SADC23 000

Other SADC672 000

Malawians25 000

SouthAfricans13 000 Batswana

58 000

Mozambicans635 000

Basotho490 000

Swazis190 000

Other SADC23 000

Other SADC672 000

Malawians25 000Batswana

58 000

Mozambicans635 000

Basotho490 000

Swazis190 000

?

How is money sent?

Sources of information :

• Focus groups with cross-border remitters & long distance taxi drivers

• Supplementary data:

• Finscope Africa reports

• SA Migrancy project

• Banks and service providers

• Central banks

Findings

• Majority of remittances are sent informally

• Even for longer routes, half of all money sent is with either taxi drivers or friends and family

• Bank transfers are viewed as aspirational / desirable, but are seldom used cross-border

• Little evidence of Hawala

Source: Genesis calculations

% total flows

Taxi drivers 21%

Friends / relatives 32%

Post Office 32%

Bank 5%

Other 10%

Total 100%

International remittances

% total flows

Taxi drivers 20%

Friends / relatives 30%

Post Office 30%

Bank 15%

Other 5%

Total 100%

Domestic remittances

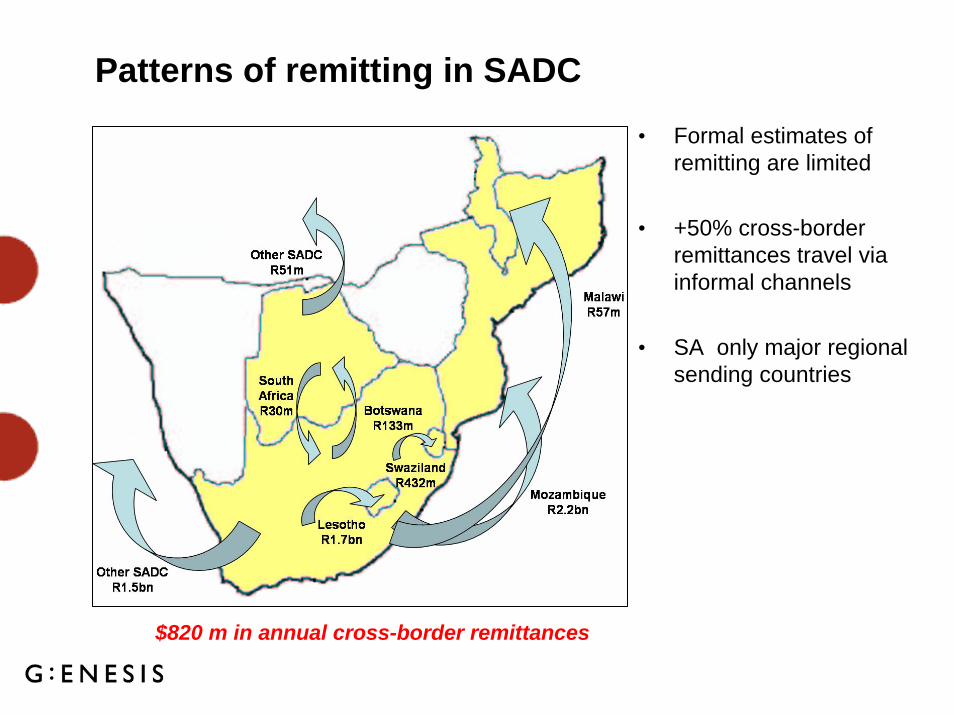

Patterns of remitting in SADC

• Formal estimates of remitting are limited

• +50% cross-border remittances travel via informal channels

• SA only major regional sending countries

$820 m in annual cross-border remittances

Pricing of Remittance Channel

Source: Focus group discussions, bank websites and telephonic enquiriesE-rate USD:ZAR – $1:R7.5

Heavy regulation has meant that Western Union has not been able to operate in South Africa!

Domestic transfersPrice for $40

transferTaxi driver $2.00

Friends/relatives $2.00

Post Office - money order $4.80

Bank deposits $1.10

Inter-account payments $1.10

International transfersTaxi driver $4.00

Friends/relatives $4.00

Post Office - money order $4.07

Post Office - telegraphic money order $6.90

Inter-account payments $22.28

Innovation

A card revolution is happing across Africa

• In the last 5 years the number of ATM’s and cards in circulation in Africa has increased dramatically in most countries

• Growing numbers of cards / ATM create the infrastructure that can support dozens of new products

17.7

28.4

40.3

58.5

83.00

2001 2002 2003 2004 2005

Visa cards in CEMEA regionMillion900

400

200

10050

Series

20052004200320022001

Card in UgandaThousand

Source: Genesis/USAID Source: Visa

Source: Genesis estimates

ATM’s in Kenya 350

200

75

30

2006

Series

200520042003

Allowing senders to link to recipients using the card infrastructure

• More and more senders have access to either debit or credit cards in sending countries

• Increasingly email and text are the means of communication between senders and recipients

• Creates potential for migration of remittances to card channels across the banked population

Two cards, one account

Card to card

Card to airtime

Card to bank account

Recipient Un-banked

Recipient Banked

Allowing a large number of products to compete with traditional money transfer services

14%

14%

9%

13%

12%

7%

$11

$22

$33

$55

$110

Active labour forcePercentage

Financial services coverage

Traditional bank coverage

IncomeMonthly$ 2004

32%

Western union penetration

Uncontested market

Source: UBOS, 2004; interviews with various banks & mobile phone providers

Allowing a large number of products to compete with traditional money transfer services

Active labour forcePercentage

Financial services coverage

Traditional bank coverage

IncomeMonthly$ 2004

Source: UBOS, 2004; interviews with various banks & mobile phone providers

Current low cost card models

Western union penetration

Mobile coverage

14%

14%

9%

13%

12%

7%

$11

$22

$33

$55

$110

32%

And the emergence of card to airtime as a new channel

Mobile penetration in African countries is reaching impressive levels – often deeper than the banked population

- Airtime can be transferred from card holders offshore to onshore

- But subject to important constraints…

26

36

49

74

2001 2002 2003 2004

Mobile phones Sub-Saharan AfricaIndividuals per thousand

F2004

103

Airtime is not as useful as money

• Airtime has built in % distribution fees for airtime distributors, makes it uncompetitive as amount to be transferred increases

• Recipients find it difficult to offload airtime in any volume

Bank Transfer

Money transfer

Airtime60

40

19

10

2217

1211

29272522

30020050 100

Cost of money transfers using alternative channelsUS$

Amount to be transferred

Card to card: allow card holders to use the payments system to bypass traditional products and channels

Visa Money Transfer

Lets cardholders transfer money from one Visa card to another. It’s secure, easy and convenient.

The Visa Money Transfer service is made available to cardholders by the bank or organisation that issues their Visa card.

To use Visa Money Transfer, cardholders need to sign on to their bank’s online banking service. They can then start using Visa Money Transfer at any time of the day or night.

Source: www.visaeurope.com

SA Banks block the BIN’s on SA cards for fear that the Central Bank will force them to repudiate transactions.

Conclusion: Channels and Technology

• SA has a technology infrastructure in line with a developed market

• The proliferation of channels and technology has the potential to rapidly transforming the remittance environment:

• Globally:

• Greater competition is reducing charges

• Lower charges support an increase in the value of transfers received

• Greater access in sending countries should increase the speed/ease with which spenders can get money home

• Emerging solutions are auditable and increase transparency and the potential for monitoring.

......providing regulation does not get in the way!

Regulation

Regulatory obstacles

• Three key regulatory barriers identified in SADC:

• Exchange controls (South Africa)

• Anti-money laundering legislation (South Africa, but increasingly widespread)

• Immigration laws (South Africa)

Sometimes the interaction between regulations is the source of much of the barrier..

Exchange control (Excon) remains in place

Excon regulations are unique to South Africa in SADC • Do not prohibit remittances – “gift allowance”• Three main sources of problems:

• Identity of remitter• Authorised dealer license• Reporting requirements

1: Identity of remitter• Excon distinguishes between residents, non and temporary residents• Non-residents (includes undocumented migrants) are not legally allowed

to earn money, and thus also not allowed to remit• Temporary residents need a work permit to access the financial system

– even with the right documentation, access is difficult

Exchange controls increase transactions costs

2: Authorised dealer licenses

• Only an authorised dealer is allowed to trade in foreign exchange

• Central Bank only awards licenses to banks (4 banks control 90% of the market)

3: Reporting requirements

• Dealer must report all transactions on the central bank reporting system

• Installing the system is expensive

• Data which needs to be reported per transaction is extensive:

• Residence permit number, address, phone number, proof of identity, utility bill

• The purpose of the transfer, description of the source of funds

• A bank based transfer takes on average 20-30 minutes to complete

• All documentation has to be executed in person at the branch (not on internet)

Exchange controls dramatically increase the cost to the bank of providing money transfer services

• Total impact is to raise fixed costs and per transaction costs

• Competition is restricted – only banks can enter market

• Net impact cost of formal transfers reflected in total cross-border fees being significantly more expensive than informal and/or Post Office transfers, which are not subject to Exchange control

AML legislation adds to the burden

• Principal AML legislation is the Financial Intelligence Centre Act (“FICA”)

• Before performing a transaction, must obtain identity number (ornationality and passport number) and residential address of the person + proof of residence (utility bill) and proof of source of income

• Verifying client identity in the low income market is extremely difficult:

• Many potential remitters do not have formal addresses

• Low income consumers increasingly prepay for their utilities, so no bill which can be used to verify address is generated

• Telephone numbers and e-mail addresses are not available

Remittances are unrequited flows

Don’t generate invoicing or other proof of purpose

Thus difficult to distinguish AML

processes from illegal flows

Banks are required to play their part in implementing Immigration legislation

• SA immigration law is unskilled migrant unfriendly

• Immigrants tend to enter the South Africa illegally – hence the large proportion of undocumented versus documented immigration in SADC

• Migration law then interacts with other regulatory barriers:

• FICA requires passport/ID as part of customer due diligence procedures,

• Exchange control requires residence status or a work permit to remit through the banks

• Exchange controls require proof of income (most immigrants work informally)

Policy recommendations

Conclusion

• The SADC remittance market is a vital feature of the regional economy, with an important role to play in poverty alleviation

• Technology and access to cards/ATM’s/Internet creates the conditions in which there could be a rapid flowering of low cost and secure alternatives to banks or traditional money transfer companies, leading to a rapid increase in the formalisation of transfers to the benefit of consumers, banks and regulators

• The regulatory burden imposed by South Africa is draconian, and prevents formalisation of the remittance market across the region

• To realise the benefits of formalisation, regulatory change is urgently needed in South Africa, most importantly the liberalisation of the foreign exchange market and the relaxation of KYC requirements on low value transfers